Abstract

A common limitation of the studies on the exchange rate-trade balance linkage is ignoring the USD’s role as a vehicle currency. Some recent papers have recognized this gap and proposed a hypothesis that the neglection of the USD’s role as a vehicle currency can restrict the significance of findings. This study aims to test that hypothesis in the trade between each of the 10 countries in ASEAN (Association of Southeast Asian Nations) with the whole EU-28. Specifically, this paper is the first to examine how the vehicle currency USD’s exchange rates, along with the real effect exchange rates, asymmetrically impact the trade balance of each ASEAN country with the EU-28 by employing the NARDL method to investigate whether the ignorance of the USD leads to fewer significant coefficients of exchange rates. The results indicate that the vehicle currency model (VCER) outperforms the real effective exchange rate (REER) model, which supports the hypothesis. In addition, the results are robust when controlling for the role of exchange rate volatility.

Keywords

Introduction

ASEAN consists of 10 member countries: Brunei, Cambodia, Indonesia, Laos, Malaysia, Myanmar, Philippines, Singapore, Thailand, and Vietnam. Most of them are emerging markets and developing countries with dynamic economies and high growth rates. Ranked at the eighth largest economy in the world, the entire ASEAN has approximately 640 million customers, which makes them an important partner in global trade (European Commission, 2021). In addition, ASEAN is respectively the largest trading partner of China (Harada, 2020), and the fourth largest trading partner of the US (Office of the United States Trade Representative, n.d.). Moreover, ASEAN is the EU’s third largest trading partner outside Europe, only behind China and the US (European Commission, 2021). Accordingly, realizing the prominence of ASEAN-EU trade, one priority of the EU is encouraging exportation to ASEAN countries (European Commission, 2021). Up to now, the EU-Singapore and EU-Vietnam free trade agreements already came into force, while the negotiation with Indonesia is ongoing and the negotiations with Malaysia, Philippines, and Thailand are delayed (European Commission, 2021). Besides, the EU has always been among the top trading partners of every ASEAN country. 1 Therefore, the ASEAN-EU trade has recently been received considerable attention.

In the trade between two partners, the currencies of the exporter or the importer, or the vehicle currency belonging to the third country can be used (Goldberg & Tille, 2008; Magee & Rao, 1980). The USD is the most dominant vehicle currency in global trade (Boz et al., 2020). It has been the world-leading vehicle currency for many decades and employed in around 88% of the global transactions, far exceeding the runner-up EUR (Bank for International Settlements, 2016, 2019; Krugman, 1980). Moreover, emerging market economies highly utilize the USD as a vehicle currency (Boz et al., 2020). Specifically, the share of USD in the exportation of emerging market economies in Asia is always more than 75%, and that of the Latin American counterparts is always nearly 87% (Boz et al., 2020). Furthermore, many high-income countries also substantially employ the USD as a vehicle currency. For instance, the EU-28 strongly utilizes the USD in trading with non-EU partners (Eurostat, 2021). Thus, the popularity of USD and its crucial role as a vehicle currency in global trade is undeniable as it is heavily used in the trade between any two countries, especially when they are not the US (Boz et al., 2020).

The exchange rate-trade balance relationship is a traditional topic in international finance and international economics. Based on the framework of the Marshall-Lerner condition and the J-curve effect, the literature is very abundant and available for a large number of countries (Bahmani-Oskooee & Hegerty, 2010; Bahmani-Oskooee & Ratha, 2004). Numerous studies were unable to find the significant impacts of exchange rates on trade balances due to the two main culprits: aggregation bias and the symmetric assumption of exchange rate-trade balance linkage (Usman et al., 2021). Recently, a new factor contributing to the lack of significant results was proposed: the neglection of the vehicle currency USD in the trade between any two non-US partners (Bao & Le, 2021b). Namely, in Vietnam’s bilateral trade with the countries in the EU and the UK, more significant results were detected when the USD’s role as a vehicle currency was incorporated (Bao & Le, 2021b). This finding raises a new question that whether the usefulness of including the USD’s role as a vehicle currency applies not only to the case of Vietnam but also the cases of other ASEAN countries. So far, this question has not been addressed by any research. In fact, very few studies have analyzed the exchange rate-trade balance linkage of an ASEAN member with respect to the EU-28 treated as a whole. To our knowledge, there are only two papers relating to this line of research: Bineau (2016) for Cambodia-EU trade, and Bahmani-Oskooee and Aftab (2017b) for Malaysia-EU trade, but they did not inspect the USD’s role as a vehicle currency. Hence, the trade of all ASEAN members with the EU-28 treated as a whole, along with the inclusion of the vehicle currency USD, has not been covered by any research.

Recognizing the importance of the USD as a vehicle currency, this paper tries to fill the gap unexamined by the existing studies about the ASEAN countries. Particularly, this paper explores the impacts of the vehicle currency USD’s exchange rates as well as real effective exchange rates on the trade balance of every ASEAN member with the whole EU-28. The main hypothesis to be tested in this paper is as follows:

Hm: The neglection of the USD’s role as a vehicle currency limits the significance of the findings. (In other words, the inclusion of the USD’s role as a vehicle currency can detect more significant impacts of exchange rates on ASEAN countries’ trade balances.)

To test this hypothesis, we compare the performance of the vehicle currency (VCER) model and the real effective exchange rate (REER) model. Moreover, for robustness check, we control for the role of exchange rate volatility and compare the performance of the extended VCER and REER models. The results support the hypothesis Hm.

This paper can contribute to the existing literature about the exchange rate-trade balance relationship in the cases of ASEAN countries. Namely, this paper is the first study to investigate the exchange rate-trade balance linkage for each of the 10 ASEAN countries in trading with the EU-28 treated as a whole. In addition, it is also the first to use the real effective exchange rate to fully capture the movement between an ASEAN country’s currency with all the currencies of the EU-28 rather than relying on the bilateral exchange rate between an ASEAN country’s currency with the EUR. Moreover, it is also the first paper to incorporate the role of USD as a vehicle currency in the trade of each ASEAN member with the entire EU-28, which allows more detailed findings and helpful policy recommendations when the impacts of real effective exchange rates and the vehicle currency USD’s exchange rates can be compared. Furthermore, this paper extends the results of Bao and Le (2021a) and reduce the aggregation bias which allows more significant findings. Last but not least, this paper enriches the literature of all ASEAN countries, especially for Brunei and Myanmar when hardly any research about these two countries has been published.

Literature Review

The exchange rate-trade balance nexus is a traditional topic that has been being inspected by numerous papers for a long time. Early studies tried to inspect if the devaluation of a country’s currency could stimulate its trade balance by validating the Marshall-Lerner condition. Accordingly, if they can prove that the absolute value of export demand elasticity plus the import analog is greater than one, the Marshall-Lerner condition is satisfied, and the devaluation policy is effective in boosting the trade balance (Wilson & Tat, 2001). The aforementioned approach is an indirect method to examine the influence of currency devaluation on the trade balance, and since the introduction of the term J-curve effect by Magee (1973), a large number of studies have evaluated the direct exchange rate-trade balance linkage (Soleymani & Chua, 2014). Bahmani-Oskooee (1985) first proposed the technique to detect the J-curve effect by observing the short-run pattern of the estimated exchange rate coefficients and proved that it existed in Greece, India, and Korea but not Thailand during the quarters from 1973 to 1980. Later, Rose and Yellen (1989) documented that the J-curve phenomenon is identified when the short-run exchange rate coefficients are negative and the long-run counterparts are positive. Grounded in the above-mentioned bases, manifold studies have scrutinized the relationship between exchange rates and trade balances of various countries and territories in the world, and their results are distinguishable (Bahmani-Oskooee & Hegerty, 2010; Bahmani-Oskooee & Ratha, 2004). Besides, the development of research has gone in line with the introduction of new econometric methods. Since the NARDL method was proposed by Shin et al. (2014), recent studies found strong evidences that exchange rates asymmetrically impact trade balances, and the use of NARDL method is superior to the ARDL one in analyzing the exchange rate-trade balance relationship (Iyke & Ho, 2018; Nusair, 2017).

Nearly all ASEAN countries have their own literature at different data levels. For example, at aggregate level, Arize (1994) contained five ASEAN members (Indonesia, Malaysia, the Philippines, Singapore, and Thailand) and reported that, among them, only Malaysia did not associate with the positive impact of currency depreciation on its trade balance during 1973Q1 to 1991Q1. However, when Yusoff (2010) used the VECM model and the 1977Q1 to 1998Q2 data, Malaysia’s trade balance with the rest of the world was encouraged when the ringgit depreciated. Nevertheless, when Bahmani-Oskooee and Kanitpong (2017) employed the ARDL and NARDL methods, they reported no reaction of Malaysia’s trade balance to the real effective exchange rate from 1975Q1 to 2016Q1. Thus, the findings of the same country vary with distinctive data, methods, and time frames. Accordingly, the results of Indonesia, the Philippines, Singapore, and Thailand reported by Bahmani-Oskooee and Kanitpong (2017) deviated from those of Arize (1994). For the case of Laos between 1993Q1 and 2010Q4, with the application of ARDL approach, Kyophilavong et al. (2013) identified no long-run impact of exchange rate on its trade balance. Lee (2018) examined the trade of Vietnam with the rest of the world proxied by her 15 largest trading partners in the period 1996Q1 to 2016Q4 by the ARDL technique and claimed that the depreciation of Vietnamese dong (VND) hurt Vietnam’s trade balance in the long run. In contrast, Phong et al. (2018) used 22 largest trading partners to represent the rest of the world, employed the ARDL method and the quarterly data spanning from 2000 to 2015, and demonstrated that the depreciation of VND facilitated Vietnam’s trade balance in a J-curve pattern.

Studies about the exchange rate-trade balance linkage at bilateral level are also available for most of the ASEAN countries, for instance, Cambodia (Bineau, 2016), Indonesia (Bahmani-Oskooee & Harvey, 2019), Laos (Kyophilavong et al., 2018), Malaysia (Bahmani-Oskooee & Harvey, 2010), the Philippines (Harvey, 2018), Singapore (Wilson & Tat, 2001), Thailand (Brahmasrene & Jiranyakul, 2002), and Vietnam (Lee, 2018). Remarkably, Bineau (2016) included the EU-28, along with other partners (Hong Kong, Indonesia, Japan, Korea, Malaysia, Singapore, Thailand, the UK, and the US) in his analysis of Cambodia’s bilateral trade in the quarters from 1998 to 2014. With the utilization of the Fully Modified OLS estimator, he concluded that the depreciation of riel improved Cambodia’s trade balance with all the partners. However, as the EU-28 consists of many countries, the bilateral exchange rate used by Bineau (2016) might not reflect the full movement of riel against all currencies of the EU-28. Thus, the real effective exchange rate between Cambodian riel and all currencies of the EU-28 can be a more suitable proxy. Some other notable papers relating to ASEAN members should also be listed. For example, Baharumshah (2001) assessed the relationship between the exchange rates and trade balances of Malaysia and Thailand with respect to the US and Japan during 1980Q1 to 1996Q4 by employing the VECM model. The results indicated that the depreciation of domestic currencies fostered Malaysia’s and Thailand’s trade balances with both the US and Japan, but the J-curve phenomenon was not supported. Wilson (2001) examined the impacts of exchange rates on the trade balance of Singapore, Malaysia, and Korea with respect to the US and Japan during 1970Q1 to 1996Q4. They reported that the depreciation of Malaysia’s currency encouraged its trade balance with the US, and no J-curve effect was detected.

Commodity-level studies are also available for some ASEAN countries, especially Malaysia. For example, Soleymani and Chua (2014) investigated the impacts of bilateral exchange rate on Malaysia’s trade balances with China in 52 industries during 1993Q1 to 2012Q4. The ARDL estimation results demonstrated that 18 industries were benefited from the depreciation of ringgit against yuan in the long run, but 13 industries were negatively affected. Again, Bahmani-Oskooee and Aftab (2018) focused on Malaysia-China trade in 59 commodities. Employing both ARDL and NARDL methods on the 2001M3 to 2015M12 data, they observed that the NARDL method was better than the ARDL counterpart in terms of providing more significant results. They also detected asymmetric short-run and long-run effects. Some other noticeable papers relating to Malaysia can be instanced as Bahmani-Oskooee and Aftab (2017a) for Malaysia-Thailand trade, and especially Bahmani-Oskooee and Aftab (2017b) for Malaysia-EU trade. Namely, applying both the ARDL and NARDL methods, Bahmani-Oskooee and Aftab (2017b) inspected the influences of EUR/MYR exchange rate on Malaysia’s trade balances with the whole EU-28 in 63 industries over the period 2000M5 to 2013M12. By choosing the EUR/MYR exchange rate, it could be suggested that the EUR was an important invoicing currency in Malaysia’s trade with all EU-28 countries even if nine of them (i.e., Bulgaria, Croatia, Czechia, Denmark, Hungary, Poland, Romania, Sweden, and the UK) did not employ the EUR as their official currencies. Nevertheless, the EUR cannot be considered vehicle currency 2 in the trade between Malaysia and the whole EU-28 because it belongs to the Eurozone which is a part of the EU-28. Hence, although the EUR/MYR is a good proxy, it may not fully capture the movement of MYR against all the currencies of the EU-28. Thus, the real effective exchange rate between MYR and all currencies of the EU-28 can be more appropriate. Apart from Malaysia, other countries such as the Philippines (Arize et al., 2017), Singapore (Arize et al., 2017), Thailand (Bahmani-Oskooee & Kanitpong, 2019), and Vietnam (Ho et al., 2021) have also been analyzed by the existing papers conducted at industry level.

While most of the existing literature about the exchange rate-trade balance nexus overlook the role of vehicle currency (Bao & Le, 2021b; Yang & Gu, 2016), a few papers have investigated this problem. Šimáková (2013) investigated the effects of EUR as a vehicle currency in Hungary-Czechia, Hungary-Poland, and Hungary-UK trade between 1997Q1 and 2012Q2, which revealed different responses of Hungary’s trade balance under the influences of the vehicle currency EUR’s exchange rates and the bilateral exchange rates. Yang and Gu (2016) acknowledged the crucial role of USD as a vehicle currency and discovered that China’s exportation and importation with Singapore were significantly affected by the depreciation of SGD or CNY against the USD during 1993M1 to 2013M12. Nhung et al. (2018) found that both the nominal bilateral exchange rate (JPY/VND) and the vehicle currency USD’s exchange rate (USD/VND) had significant impacts on Vietnam’s trade balance with Japan from 2001Q1 to 2017Q3. This result goes in line with the fact that roughly 90% of Vietnam’s trade value is invoiced in USD (Bao & Le, 2021b). Bao and Le (2021a) analyzed the trade between the entire ASEAN and the whole EU-28 in the period 2000Q1 to 2018Q1. They disclosed that the exchange rate between ASEAN’s currencies and the vehicle currency USD facilitated ASEAN’s overall trade balance with the EU-28, but the real effective exchange rate between them had no effect. Their findings reflect the importance of USD as a vehicle currency in the trade between ASEAN and the EU-28.

Methodology

A myriad of papers has relied on the standard two-country model to inspect the exchange rate-trade balance relationship (e.g., Iyke & Ho, 2017; Kyophilavong et al., 2013; Rose & Yellen, 1989). This study also employs the aforesaid model as follows:

In equation (1), the subscript i represents each of the 10 ASEAN members, and t denotes time. Although equation (1) looks like panel data specification, it represents the 10 time-series regressions of the 10 ASEAN countries. Regarding the variables,

In equation (2),

So as to investigate the role of USD as a vehicle currency, we use the model employed by Šimáková (2013) as well as Bao and Le (2021b):

where

In order to examine the asymmetric impacts of exchange rates on the trade balances, the variables

In equations (4) and (5),

Equation (1), combined with the partial sums of positive and negative changes of

In this paper, equation (8) is called the real effective exchange rate (REER) model because it allows evaluating both the short-run and long-run asymmetric impacts of real effective exchange rates on the trade balance of each ASEAN country with the whole EU-28. The NARDL method of Shin et al. (2014) is superior to the normal ARDL one in scrutinizing the impacts of exchange rates on trade balances and can provide more significant results (Nusair, 2017). In addition, the NARDL method possesses all the strengths of the ARDL method. Specifically, it permits the occurrence of I(1) and I(0) variables, and thus unit-root testing is not compulsory (Iyke & Ho, 2018). Shin et al. (2014) showed that equation (8) can be estimated by the conventional ARDL bound testing method of Pesaran et al. (2001). Particularly, the bound test will be conducted to identify the existence of cointegration among the variables. The null hypothesis of no cointegration H0:

Similarly, equation (2), together with the partial sums of positive and negative changes of

In this paper, equation (9) is regarded as the vehicle currency model (VCER) because it captures the short-run and long-run asymmetric effects of the vehicle currency USD’s exchange rates on the trade balances of the 10 ASEAN members with the whole EU-28. The estimation procedure of the VCER model is exactly the same as the REER model. Namely, in equation (9), the null hypothesis of the bound test for cointegration among the variables (i.e., H0:

The 2000Q1 to 2018Q1 data 3 used in this paper is collected from various sources including IMF’s Direction of Trade Statistics and International Financial Statistics, Eurostat, FRED (Federal Reserve Economic Data), OECD, ADB (Asian Development Bank), and General Statistics Office of Vietnam. All variables are in real terms and converted into indices in which the values of the base quarter 2000Q1 are set to 100. Due to the lack of quarterly GDP for Brunei, Cambodia, Laos, and Myanmar, annual data is retrieved and interpolated into quarterly data based on Kyophilavong et al. (2013, 2018).

Empirical Results and Discussion

Descriptive Statistics and Unit-Root Test

Before reporting the estimation results, it is useful to demonstrate some analyses of the descriptive statistics and unit-root tests of the variables. First, the descriptive statistics are presented in Table A1 in the Appendix section. For each ASEAN country, we have 73 observations of the variables lnTBi,t, lnYi,t, and lnYFi,t. Regarding the exchange-rate variables (i.e., REER+ i,t , REER–i,t, USD+ i,t , and USD–i,t), there are 72 observations as one observation is lost due to the first differences of exchange rates (see equations (4)–(7)). Thus, as the sample size is below 80, we can apply the critical values of bound tests for cointegration given by Narayan (2005) which are the small-sample adjustments of the large-sample ones developed by Pesaran et al. (2001). In addition, although the variables REER+ i,t , REER–i,t, USD+ i,t , and USD–i,t do not have the symbol “ln,” they are still in natural logarithm since they are calculated as the partial sums of positive or negative changes in lnREERi,t and lnUSDi,t (see equations (4)–(7)). Accordingly, their coefficients in the REER and VCER models where lnTBi,t is the dependent variable denote exchange rates’ elasticities.

The outcomes of unit-root tests are demonstrated in Table A2 in the Appendix section. The ADF and PP tests indicate no I(2) process. Moreover, the mixture of I(1) and I(0) variables is found in the majority of cases such as Brunei, Cambodia, Indonesia, Laos, Malaysia, Myanmar, and Vietnam. Therefore, the employment of NARDL method in this paper is appropriate. In addition, the NARDL method can also be applied for the cases with only I(1) variables (i.e., Philippines, Singapore, and Thailand), which is a notable advantage of ARDL-family methods (Odhiambo, 2009).

Estimation Results

The asymmetric impacts of exchange rates on the trade balances of the 10 ASEAN countries with the EU-28 between 2000Q1 and 2018Q1 are demonstrated in Table 1. For each of the 10 ASEAN countries, the real effective exchange rate (REER) and vehicle currency exchange rate (VCER) models are presented side by side. In addition, the symbol “POSi,t” represents the variables REER+ i,t in the REER model and USD+ i,t in the VCER model, respectively. Similarly, the symbol “NEGi,t” represents the variables REER–i,t in the REER model and USD–i,t in the VCER model, respectively. For each country’s models, the maximum lags are set to eight, and the optimal ones are selected by the Akaike information criterion (AIC). In case autocorrelation, heteroskedasticity, misspecification, etc. arise, we reduce the maximum lags and re-estimate the models. At first glance, the long-run relationship among the variables is found in nearly all cases, as evidenced by the significant bound-test F-statistics. Moreover, the outcomes are free from autocorrelation, heteroskedasticity and wrong functional form as none of the Breusch-Godfrey, Breusch-Pagan, and Ramsey RESET tests’ statistics are high enough to indicate such problems. Besides, the stability of the coefficients is affirmed when CUSUM tests are stable in all the cases and CUSUMSQ tests indicate the same results in the majority of them. Therefore, the NARDL estimation is trustworthy and can be used for further analyses.

NARDL Estimation Results of the Elementary REER and VCER Models.

Note. POSi,t represents REER+ i,t in the REER model and USD+ i,t in the VCER model, respectively. NEGi,t represents REER–i,t in the REER model and USD–i,t in the VCER model, respectively. The outcomes of Breusch-Godfrey, Breusch-Pagan, and Ramsey RESET tests are reported in terms of F-statistics. The results of CUSUM and CUSUMSQ tests are “S” (stable) or “U” (unstable). The significance levels 10%, 5%, and 1% are denoted by *, **, and ***.

Following the works of Bahmani-Oskooee & Fariditavana, 2016; Rose & Yellen, 1989), the J-curve effect is identified when the long-run coefficients of exchange rates are positive and their short-run counterparts are negative or insignificant. Thus, in the REER model, the J-curve effect is witnessed in the trade of Laos, Myanmar, the Philippines, and Vietnam with the EU-28. When the role of USD as a vehicle currency is captured in the VCER model, the Philippines and Thailand are associated with the J-curve phenomenon. Noticeably, the Philippines experience the J-curve effect in both the REER and VCER models. Additionally, 1% depreciation of Philippine peso (PHP) against the USD fosters the Philippines’ trade balance with the EU-28 by around 7.78% in the long run. However, the same amount of PHP depreciation against the currencies of the EU-28 only boosts the Philippines’ trade balance by around 3.83%. This implies that the Philippines’ trade balance is more sensitive to the fluctuation of the vehicle currency USD’s exchange rate (USD/PHP) than the real effective exchange rate.

The Marshall-Lerner condition can be supported if the depreciation of a country’s currency stimulates its trade balance in the long run (Rose, 1991). Thus, in this paper, if the long-run coefficients of REER+ i,t in the REER modelor USD+ i,t in the VCER model are positive, the Marshall-Lerner is supported for the ith country. The first row of Table 2 demonstrates that in six ASEAN countries including Cambodia, Laos, Malaysia, Myanmar, the Philippines, and Vietnam the depreciation of their currencies against the EU-28’s currencies improves their trade balances. Moreover, when the role of USD as a vehicle currency is considered, five ASEAN countries (i.e., Indonesia, Malaysia, Myanmar, the Philippines, and Thailand) satisfy the Marshall-Lerner condition. Especially, Cambodia, Myanmar, the Philippines, and Vietnam have the Marshall-Lerner condition supported in both REER and VCER models. Moreover, while devaluation policy seems ineffective for promoting the trade balances of Indonesia, Malaysia, and Thailand in case the real effective exchange rates are employed, it becomes effective when the vehicle currency USD is utilized. Thus, the choice of invoicing currencies could influence the effectiveness of the devaluation policy.

Summary of Long-Run Impacts of Exchange Rates on the Trade Balance of ASEAN Countries With the EU-28.

To test the main hypothesis Hm (which is mentioned in the Introduction section), we compare the performance of the REER and VCER models by counting the number of significant exchange rates’ coefficients in each model. From Table 3, it can be observed that the VCER model outperforms the REER model since all ASEAN countries have significant short-run and long-run exchange rates’ coefficients. Meanwhile, in the REER model, the number is only six. Thus, the main hypothesis of this paper is supported. Specifically, the neglection of the USD’s role as a vehicle currency is a factor contributing to the lack of significant results. This finding is analogous to Bao and Le (2021a) for ASEAN-EU overall trade. Thus, the USD’s role as a vehicle currency is too important to be overlooked in ASEAN-EU trade at various levels of analysis. Thus, the vital role of USD as a vehicle currency should not be neglected when inspecting the exchange rate-trade balance relationship between any two partners different from the US.

The Number of Significant Exchange Rates’ Coefficients in the Elementary REER and VCER Models.

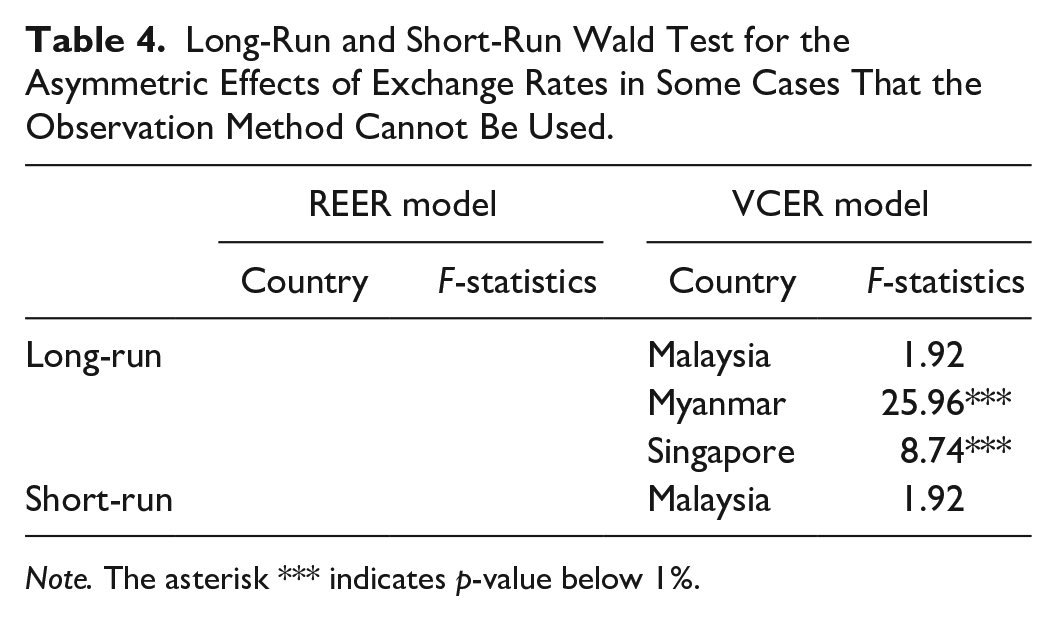

So as to detect the asymmetric influences of exchange rates on the trade balances, there are two main methods: observation or Wald test (Bahmani-Oskooee & Baek, 2019; Iyke & Ho, 2018). When the long-run coefficients denoting the depreciation and appreciation of a country’s currency are clearly distinguishable, the long-run asymmetry can be detected by observation. For example, in the VCER model of Indonesia, the long-run coefficient denoting the depreciation of rupiah against the USD (i.e., .64) is obviously different from the appreciation counterpart (i.e., −2.19), which indicates the presence of long-run asymmetry. Nevertheless, in the case of Malaysia, as the two long-run coefficients in the VCER model (i.e., 1.18 and 1.74) are positive and not so different in size, it is difficult to judge whether the long-run asymmetry exists. Hence, the Wald test is needed, and Table 4 shows the Wald test results for the cases that are unclear and thus cannot be concluded by the observation method. In the case of Malaysia, for instance, the Wald test’s F-statistic is low, and there is no long-run asymmetric effect accordingly. Additionally, the observation method can also be used to detect the short-run asymmetry when the lag lengths of ΔPOS and ΔNEG are different, or their coefficients are distinct at the same lag. In all the cases except Malaysia’s VCER model, short-run asymmetries are identified by observation. Regarding Malaysia’s VCER model, there is no evidence of short-run asymmetry because the Wald test’s F-statistic (i.e., 1.92) is not significant.

Long-Run and Short-Run Wald Test for the Asymmetric Effects of Exchange Rates in Some Cases That the Observation Method Cannot Be Used.

Note. The asterisk *** indicates p-value below 1%.

Besides, Table 5 lists all the long-run and short-run asymmetries, which reinforces the suitability of the NARDL method as the majority of ASEAN countries have short-run and long-run asymmetric effects of exchange rates on their trade balances with the EU-28. Specifically, all the 10 ASEAN members witness short-run asymmetries in the REER model while nine of them experience short-run and long-run ones in the VCER model.

Cases With Long-Run and Short-Run Asymmetries.

Robustness Check

In this section, we examine the robustness of the estimation results of the elementary models presented in Table 1 and the outcomes displayed in Table 3 by incorporating the volatility of exchange rates. It is well documented that the exchange rate volatility can impact a country’s export and import (Bailey et al., 1987; Hayakawa & Kimura, 2009; McKenzie, 1999). Thus, it can be used as a control variable for the trade balance (Singh, 2004). Moreover, the exchange rate volatility has been deemed a relevant factor affecting a country’s choices of invoicing currencies in its global trade (Bowe & Saltvedt, 2004; Liu & Lu, 2019; Witte, 2010). Therefore, we focus on the role of exchange rate volatility to conduct the robustness check of the elementary models to further scrutinize the impacts of real effective exchange rates and the vehicle currency USD’s exchange rates on the ASEAN countries’ trade balances with the EU-28.

Exchange rate volatility can be measured in different ways (McKenzie, 1999). Following Medhora (1990) and Bahmani-Oskooee et al. (2014), we use the within-period standard deviation to compute exchange rate volatility. Namely, in this paper, the standard deviation of the monthly real exchange rates in each quarter is employed to construct the quarterly exchange rate volatility, which is specified in equations (10) and (11):

In equation (10),

We incorporate the natural logarithm of

NARDL Estimation Results of the Extended REER and VCER Models.

Note. POSi,t represents REER+ i,t in the extended REER model and USD+ i,t in the extended VCER model. NEGi,t represents REER–i,t in the extended REER model and USD–i,t in the extended VCER model. lnVOLi,t denotes the natural logarithm of VOL_REERi,t in the extended REER model and the natural logarithm of VOL_USDi,t in the extended VCER model. The outcomes of Breusch-Godfrey, Breusch-Pagan, and Ramsey RESET tests are reported in terms of F-statistics. The results of CUSUM and CUSUMSQ tests are “S” (stable) or “U” (unstable). The significance levels 10%, 5%, and 1% are denoted by *, **, and ***.

From Table 6, we observe that the impacts of exchange rate volatility on ASEAN countries’ trade balances can be either positive, negative, or insignificant, which is analogous to the findings of the existing literature about its ambiguous effects on the trade flows of different countries (McKenzie, 1999; Sharma & Pal, 2018; Sugiharti et al., 2020). In addition, most of the ASEAN members witness the long-run significant impacts of exchange rate volatility on their trade balances, either in the extended REER model or the extended VCER model, except for Malaysia and the Philippines.

We notice high level of robustness when comparing the long-run exchange rates’ coefficients in Table 1 (which shows the estimation results of the elementary models) and Table 6 (which shows the estimation results of the extended models). Specifically, for the convenience of the readers, we report the summary of the long-run exchange rates’ coefficients in Table 7. Comparing the elementary and extended REER models, the coefficients of POSi,t and NEGi,t are similar in terms of sign when they are statistically significant in most of the cases except Laos. Meanwhile, regarding the elementary and extended VCER models, virtually all ASEAN countries have strongly robust coefficients in terms of sign and significance except Brunei. For example, Singapore’s trade balance is negatively affected by both the depreciation and appreciation of its currency against the vehicle currency USD in the elementary as well as extended VCER models. Additionally, the Philippines’ trade balance is fostered by the depreciation of its currency against the vehicle currency USD, as evidenced by the positive coefficients of POSi,t in both the elementary and extended VCER models (i.e., 7.78 and 8.83, respectively).

Summary of Long-Run Exchange Rates’ Coefficients of the Elementary and Extended REER and VCER Models.

Note. The significance levels 10%, 5%, and 1% are denoted by *, **, and ***.

To check the robustness of our main hypothesis Hm (i.e., the neglection of the USD’s role as a vehicle currency can lead to fewer significant results), we look into Table 6 and count the numbers of significant exchange rates’ coefficients in the extended REER and VCER models. The outcome is displayed in Table 8. When controlling for the role of exchange rate volatility, the extended VCER model still outperforms its counterpart in both the short run and long run. Thus, the main hypothesis Hm is supported by the elementary as well as extended models (see Tables 3 and 8). This finding reflects the fact that the ASEAN countries heavily rely on the vehicle currency USD in their international trade with many partners including the EU-28. Therefore, the ignorance of the USD’s role as a vehicle currency when analyzing the exchange rate-trade balance relationship is a factor contributing to the lack of significant results (Bao & Le, 2021a, 2021b).

The Number of Significant Exchange Rates’ Coefficients in the Extended REER and VCER Models.

Conclusion

This paper is the first to investigate the impacts of the vehicle currency USD’s exchange rates, together with the real effective exchange rates, on the trade balances of all ASEAN countries with the whole EU-28. The main hypothesis of this paper is supported with high level of robustness. Namely, the empirical results demonstrate the usefulness and prominence of the USD as a vehicle currency where all ASEAN members witness the significant effects of the USD’s exchange rates on their trade balances in both the short run and long run. Thus, studies on the exchange rate-trade balance nexus between any two partners different from the US should not ignore the importance of USD as a vehicle currency because it dominates the global trade.

The findings of this paper show that the trade balances of several ASEAN members react distinguishably to the real effective exchange rates and the vehicle currency USD’s exchange rates. Hence, the effectiveness of the devaluation policy to boost trade balances can depend on the usage of different invoicing currencies. For example, Indonesia’s and Thailand’s trade balances are unresponsive to the real effective exchange rates in the long run, but they are positively affected by the vehicle currency USD’s exchange rates. Thus, the weak-currency policy can help Indonesia and Thailand to foster their trade balances with the EU-28 if they utilize more proportion of the vehicle currency USD. Moreover, as ASEAN countries highly utilize USD as a vehicle currency, it can influence not only their trade balances with the US but also with other partners such as the EU-28. With strong reliance on the USD, ASEAN countries’ policy-makers should carefully monitor the fluctuation of their currencies against the USD as it can simultaneously impact their trade with various partners that may altogether occupy higher percentage than the share of the US in their total trade values. For example, the vehicle currency USD can affect ASEAN countries’ trade with the partners in the Regional Comprehensive Economic Partnership (RCEP) (i.e., Australia, China, Japan, New Zealand, and South Korea) which accounted for the higher share than that of the US in ASEAN’s total trade values. Therefore, the policy-makers should pay attention to the usage of the invoicing currencies, especially the USD, in the trade with the aforesaid RCEP partners. In addition, they should collect more data about the usage of the invoicing currencies used in the trade of each ASEAN country with various partners and investigate the factors affecting the choice of each currency.

This paper controls for the role of exchange rate volatility in the extended REER and VCER models, which indicates the robustness of the results. However, the limitation of this paper is that it has not included other variables that can affect the trade balances. Future studies can test the main hypothesis proposed by this paper for other countries by expanding the models with more control variables.

Footnotes

Appendix

Summary of Some Notable Empirical Papers.

| Papers | Focused countries | Partners | Methods and time | Models | Findings |

|---|---|---|---|---|---|

| Panel A: Studies focusing on ASEAN countries | |||||

| Arize (1994) | Indonesia, Malaysia, Philippines, Singapore, Thailand | The rest of the world | Method: Engle-Granger, Johansen cointegration | TB = f(E) | The depreciation of currencies fosters the trade balances of all countries except Malaysia |

| Time: 1973Q1 to 1991Q1 | |||||

| Baharumshah (2001) | Malaysia, Thailand | Japan, the US | Method: Johansen-Juselius cointegration | TB = f(E, Y, YF) | The depreciation of domestic currencies fosters Malaysia’s and Thailand’s trade balances with Japan and the US |

| Time: 1980Q1 to 1996Q4 | No evidence of the J-curve effect is found | ||||

| Wilson and Tat (2001) | Singapore | The US | Method: Engle-Granger, Johansen-Juselius cointegration | TB = f(E, Y, YF) | The exchange rate does not affect the trade balance of Singapore with the US |

| Time: 1970 to 1996 | The findings do not support the presence of J-curve effect | ||||

| Brahmasrene and Jiranyakul (2002) | Thailand | Germany, Japan, Singapore, the Netherlands, the UK, the US | Method: Engle-Granger cointegration | TB = f(E, Y, YF) | The depreciation of Thai baht fosters Thailand’s trade balances with all the partners except Singapore |

| Time: 1990Q1 to 2000Q4 | |||||

| Yusoff (2010) | Malaysia | The rest of the world | Method: VECM | TB = f(E, Y, YF) | The depreciation of ringgit fosters Malaysia’s trade balance |

| Time: 1977Q1 to 1998Q2 | The evidence of J-curve effect depends on the exchange rate regimes | ||||

| Kyophilavong et al. (2013) | Laos | The rest of the world | Method: ARDL | TB = f(E, Y, YF) | The depreciation of domestic currency does not improve the trade balance of Laos |

| Time: 1993Q1 to 2010Q4 | J-curve effect is identified | ||||

| Bineau (2016) | Cambodia | The EU-28, Hong Kong, Indonesia, Japan, Korea, Malaysia, Singapore, Thailand, the UK, the US | Method: FMOLS | TB = f(E, YF/Y) | The depreciation of domestic currency fosters Cambodia’s trade balance |

| Time: 1998Q1 to 2014Q3 | The overall panel data estimation results show no J-curve effect | ||||

| The J-curve effect is identified in Cambodia’s trade with Indonesia and Singapore | |||||

| Bahmani-Oskooee and Aftab (2017b) | Malaysia | EU-28 | Method: ARDL, NARDL | TB = f(E, Y, YF) | The NARDL method is superior to the ARDL method in detecting more significant results and more evidence of the J-curve effect |

| Time: 2000M5 to 2013M12 | The J-curve effect is identified in 12 out of the 63 industries | ||||

| Bahmani-Oskooee and Harvey (2019) | Indonesia | 12 Trading partners | Method: ARDL, NARDL | TB = f(E, Y, YF) | The NARDL method is superior to the ARDL method in detecting more significant results |

| Time: 1990Q1 to 2015Q4 | The J-curve effect is identified in Indonesia’s trade with the Philippines, Singapore, Thailand, the UK, and the US | ||||

| Phong et al. (2018) | Vietnam | The rest of the world | Method: ARDL | TB = f(E, Y, YF) | The depreciation of Vietnamese dong fosters Vietnam’s trade balance |

| Time: 2000Q1 to 2015Q4 | The J-curve effect is identified | ||||

| Bao and Le (2021a) | ASEAN | The EU-28 | Method: NARDL | TB = f(E, Y, YF) | The neglection of the USD’s role as a vehicle currency limits the significance of the results |

| Time: 2000Q1 to 2018Q1 | TB = f(V, Y, YF) | The real effective exchange rate demonstrates no impact on ASEAN’s trade balance with the EU-28 | |||

| The vehicle currency USD’s exchange rate positively affects ASEAN’s trade balance with the EU-28 | |||||

| The J-curve effect is detected in the vehicle currency model | |||||

| Bao and Le (2021b) | Vietnam | 27 Countries in the EU and the UK | Method: NARDL | TB = f(E, Y, YF) | The inclusion of the USD’s role as a vehicle currency helps detect more significant results and additional cases of J-curve effect |

| Time: 2000Q1 to 2018Q1 | TB = f(V, Y, YF) | ||||

| Panel B: Studies focusing on other countries | |||||

| Bahmani-Oskooee (1985) | Greece, India, South Korea, Thailand | The rest of the world | Method: Almon distributed lag | TB = f(E, Y) | This is the pioneering study to propose a method to detect the J-curve effect |

| Time: 1973Q1 to 1980Q4 | The results indicate that J-curve effect is found in Greece, India, and South Korea | ||||

| Rose and Yellen (1989) | The US | Canada, France, Germany, Italy, Japan, the UK | Method: Engle-Granger cointegration | TB = f(E, Y, YF) | This study provides the theoretical and empirical bases for the use of the standard two-country model in analyzing the impacts of exchange rates on trade balances. Namely, a country’s trade balance is modeled by the three independent variables: the exchange rate, the domestic income, and the partner’s income |

| Time: 1960Q1 to 1985Q1 (some partners have different time frames) | This study is also the first to propose a new method to detect the J-curve effect: the negative exchange rates’ coefficients in the short run combined with the positive ones in the long run | ||||

| The findings indicate no J-curve effect | |||||

| Singh (2004) | India | The rest of the world | Method: Johansen-Juselius cointegration, GARCH | TB = f(E, Y, YF, VOL) | Exchange rate volatility does not affect India’s trade balance |

| Time: 1975Q2 to 1996Q3 | The J-curve effect is not detected | ||||

| Bahmani-Oskooee et al. (2005) | Australia | 23 Partners | Method: ARDL | TB = f(E, Y, YF) | The positive effects of Australian dollar’s depreciation, alongside the J-curve effect, are found in the trade of Australia with Denmark, New Zealand, and South Korea |

| Time: 1973–2001 | |||||

| Gomes and Paz (2005) | Brazil | The rest of the world | Method: VECM | TB = f(E, Y, YF) | The depreciation of Brazil’s currency fosters its trade balance, thus supporting the Marshall-Lerner condition |

| Time: 1990M1 to 1998M12 | The evidence of J-curve effect is detected | ||||

| Narayan (2006) | China | The US | Method: ARDL | TB = f(E) | The depreciation of CNY against the USD fosters China’s trade balance with the US |

| Time: 1979M11 to 2002M9 | No J-curve effect is identified | ||||

| Šimáková (2013) | Hungary | Austria, Czechia, France, Germany, Italy, the Netherland, Poland, the UK | Method: Johansen-Juselius cointegration | TB = f(E, Y, YF) | This research captures the role of EUR as a vehicle currency in the trade of Hungary with Czechia, Poland, and the UK |

| Time: 1997Q1 to 2012Q2 | TB = f(V, Y, YF) | The Hungary-UK trade witnesses the existence of the J-curve effect | |||

| Šimáková and Stavárek (2014) | Czechia | Austria, France, Germany, Italy, Poland, and Slovakia | Method: Johansen-Juselius cointegration | TB = f(E, Y, YF) | This study is conducted at industry level |

| Time: 1993 to 2013 | The impacts of Czech koruna’s depreciation on Czechia’s trade balances vary with the partners and the industries | ||||

| No evidence of J-curve effect is found | |||||

| Bahmani-Oskooee and Fariditavana (2015) | Canada, China, Japan, the US | The rest of the world | Method: ARDL, NARDL | TB = f(E, Y, YF) | This is the pioneering study to propose the asymmetric assumption about the exchange rate-trade balance relationship |

| Time: 1971Q1 to 2013Q3 | The NARDL method is superior to the ARDL method in finding more cases of the J-curve effect. When the ARDL method is used, only Canada and the US experience the J-curve effect. When the NARDL method is used, the J-curve effect is identified in Canada, China, and the US. | ||||

| Future studies should pay attention to the asymmetric linkage between change rates and trade balances | |||||

| Bahmani-Oskooee et al. (2016) | Mexico | 13 Partners | Method: ARDL, NARDL | TB = f(E, Y, YF) | The NARDL method is better than the ARDL method in providing more support for the J-curve effects |

| Time: 1980Q1 to 2014Q4 (some partners have different time frames) | When the ARDL method is used, the J-curve effect is detected in Mexico’s trade with six partners: Brazil, Canada, France, Japan, South Korea, and the US | ||||

| When the NARDL method is used, the J-curve effect is detected in Mexico’s trade with ten partners: Brazil, Canada, France, India, Japan, Peru, South Korea, Spain, the UK, and the US | |||||

| Iyke and Ho (2017) | Ghana | The rest of the world | Method: ARDL, NARDL | TB = f(E, Y, YF) | When the ARDL method is used, the impact of Ghana’s exchange rate on its trade balance is insignificant. Thus, no J-curve effect is detected. |

| Time: 1986Q1 to 2016Q3 | When the NARDL method is used, the impact of Ghana’s exchange rate on its trade balance becomes significant. The presence of the J-curve effect is also supported. Therefore, the NARDL method is better than the ARDL method in studying the exchange rate-trade balance relationship. | ||||

| When the NARDL method is used, the J-curve effect is detected in Mexico’s trade with ten partners: Brazil, Canada, France, India, Japan, Peru, South Korea, Spain, the UK, and the US | |||||

| Nusair (2017) | 16 European transition economies | The rest of the world | Method: ARDL, NARDL | TB = f(E, Y, YF) | The NARDL method is better than the ARDL method in studying the exchange rate-trade balance relationship |

| Time: 1994Q1 to 2015Q2 (some partners have different time frames) | The J-curve effect is detected in 12 out of the 16 European transition economies | ||||

| Yazgan and Ozturk (2019) | 33 Countries | For each of the 33 countries, its partners are the remaining 32 countries in the sample | Method: panel data estimation by the CCE, CCEP, CCEMG estimators | TB = f(E, Y, YF) | The depreciation of domestic currencies can foster the trade balances |

| Time: 1981Q1 to 2010Q2 | The findings show the absence of J-curve effect | ||||

| Usman et al. (2021) | Pakistan | The UK | Method: ARDL, NARDL | TB = f(E, Y, YF) | The NARDL method is better than the ARDL method in studying the exchange rate-trade balance relationship, which helps identify more cases of J-curve effect |

| Time: 1980 to 2016 | The findings indicate the presence of J-curve effect in 14 out of 28 industries | ||||

Note. E = exchange rates; Y = the incomes of the focused countries; YF = the incomes of the partners; V = vehicle currencies’ exchange rates; VOL = exchange rate volatility; ARDL = autoregressive distributed lag; NARDL = nonlinear autoregressive distributed lag; CCE = common correlated effects; CCEP = common correlated effects pooled; CCEMG = common correlated effects mean group; GARCH = generalized autoregressive conditional heteroskedasticity; FMOLS = fully modified ordinary least squares; VECM = vector error correction model.

Source: Authors’ review of the literature.

Data Availability Statement

Data is available in public repository. The authors confirm that all data underlying the findings are fully available without restriction.

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: This work was supported by the European Union’s Horizon 2020 research and innovation programmed under Marie Skłodowska-Curie grant agreement No. 734712; Ho Chi Minh City University of Law. The authors owe extensive gratitude to the editor and the anonymous reviewers for their constructive comments.