Abstract

Enterprises face cross-border legal, cultural, technical differences, market volatility, and cybersecurity threats during internationalization, needing resource investment for organizational agility and supply chain security to maintain global competitiveness. China, a major global outbound investor, had US $177.29 billion in outward FDI in 2023 (11.4% of global total), ranking top three for 12 years, and its outward FDI stock was US $2.96 trillion by end-2023, keeping a top-three global spot for 7 years. This study draws on a dataset comprising 40,251 annual observations of outward investment activities by A-share listed companies in China from 2010 to 2019. In this study, we leverage binary selection variables and employ the following Probit regression model as our benchmark specification. In this study, we adopt the following Probit regression model as our benchmark and conduct all subsequent regression analyses using Stata. This study highlights the pivotal role of digital transformation in advancing enterprise internationalization. Elevating digital proficiency and operational performance, while trimming transaction costs, allows businesses to more effectively broaden their international presence. The substantial influence of digital transformation on global capital flows and corporate expansion offers a theoretical basis for policymakers. This allows them to formulate strategies that foster digital innovation, upgrade infrastructure, and lower financing costs, thus promoting both digitalization and international growth. Financing constraints, equity concentration, access to regional bank loans, and the degree of marketization influence how digital transformation affects outward foreign direct investment (OFDI).

Keywords

Introduction

The global economy is undergoing a profound transformation driven by digital technologies. According to the World Bank (2023). China has emerged as a leader in artificial intelligence (AI) and blockchain adoption among emerging markets. However, this digital revolution presents a paradox: while multinational corporations (MNCs) increasingly recognize the strategic value of digitalization, many struggle to translate technological investments into tangible internationalization outcomes. Digital transformation provides new opportunities for enterprises pursuing internationalization. By leveraging digital technologies and fostering digital-driven strategies, firms can enhance innovation capabilities, optimize resource integration, reduce operational costs, and mitigate overseas investment risks, thereby increasing the likelihood of expanding abroad.

Despite its transformative potential, many firms struggle to effectively integrate digitalization into their internationalization strategies, facing challenges such as high adoption costs, lack of digital expertise, and regulatory uncertainties.

The digital transformation of enterprises has reshaped production processes, market transactions, and competitive landscapes, profoundly influencing firms’ internationalization.

Given the dual forces of economic globalization and digitalization, understanding how digital transformation influences enterprise internationalization is both theoretically significant and practically relevant for policymakers and businesses.

Digital transformation encapsulates the progressive incorporation of advanced technologies such as artificial intelligence, big data, and blockchain into production and management processes (Xicang et al., 2024). While existing studies have examined the role of digitalization in export performance and productivity enhancement (Fan et al., 2023). The digital technology with economic development, highlighting micro-level transformations. Moreover, it represents a shift in enterprise innovation, moving from traditional business models to those centered around the core of digital technology (Vial, 2021). The impact of digital technology on enterprise innovation performance is immediate and significant. Furthermore, the digital economy enhances product performance in production, bolstering an enterprise’s competitive advantage in sales. It fosters integrating the innovation, supply, and value chains within enterprise management. Consequently, digital transformation represents a disruptive technological shift for enterprises and a strategic imperative to align with development trends (Bertani et al., 2021; Goldfarb & Tucker, 2019). The impact of digital transformation on enterprises manifests in two key dimensions: Firstly, it significantly influences internal operations by enhancing the efficiency of operation management and internal controls. This advancement positively affects enterprise innovation, productivity, and financial performance (Du & Jiang, 2022; Gao et al., 2023; N. Zhao & Ren, 2023). Conversely, the impact of digital transformation extends to the external facets of the business, primarily through its informational effect. This transformation mitigates information asymmetry and agency problems, stabilizes share price volatility, and decreases the risk of market crashes. Additionally, it lowers financing costs and facilitates faster capital restructuring (Ai et al., 2023; Sun et al., 2022).

International transformation represents a critical strategy for enterprises, significantly contributing to expanding sales markets, enhancing management practices, and integrating diverse experiences, technologies, and management insights (Chen et al., 2021). In the context of intensifying economic globalization, China has adeptly capitalized on the opportunities it presents, significantly expanding its international cooperation. China’s outward foreign direct investment (OFDI) reached US $153.71 billion in 2020, marking a 12.3% increase from the previous year. Despite this growth, the OFDI pace has encountered substantial obstacles, including trade tensions with the United States and the global COVID-19 pandemic, which have notably decelerated the expansion of Chinese enterprises abroad. Addressing the challenges to promote a higher level of “going global” for Chinese enterprises has thus become an imperative issue (Song et al., 2021; W. L. Wu & Shao, 2023). Three principal factors influence the internationalization of enterprises. First among these is the home country factor, which includes political initiatives like China’s “Belt and Road” initiative. This strategy aims to enhance relationships with countries along the route, thereby facilitating an increase in outward foreign direct investment (OFDI; Yao et al., 2023). Regional factor prices represent a significant influence on firm internationalization. Additionally, the robustness or fragility of the regional institutional environment is a crucial environmental factor that directly impacts decision-making related to outward foreign direct investment (OFDI; Kong, Peng et al., 2021; Qiao et al., 2020). Furthermore, financial factors significantly constrain the internationalization of enterprises. For example, the appreciation of the Renminbi (RMB) facilitates the outward foreign direct investment (OFDI) of Chinese enterprises by reducing the financial barriers to internationalization (Feng et al., 2022). Secondly, the host country factor, particularly the price differential between the host and home countries, is the most direct influence on the internationalization strategies of enterprises (Riedel, 1975). Prior research has explored the effects of trade barriers on outward foreign direct investment (OFDI), including factors such as geographical, economic, and institutional distances, along with the business environment (Qian et al., 2022). Thirdly, internal factors also play a significant role; positive influences include executive cash compensation, total factor productivity, and corporate social responsibility (X. Liu et al., 2014; Qiao et al., 2020; Shao & Shang, 2016). Conversely, financing constraints negatively affect enterprise internationalization (Askenazy et al., 2015). Additionally, B. Yan et al. (2018) identified a negative marginal effect of financial constraints on OFDI related to productivity (B. Yan et al., 2018).

The motivations for enterprises to engage in outward foreign direct investment (OFDI) are diverse and complex, primarily encompassing market-seeking, resource-seeking, technology-seeking, and efficiency-seeking strategies (Tang & Deng, 2024; C. Zhang & Wang, 2024). Establishing production bases in regions with lower labor costs and higher production efficiency enables firms to gain cost advantages and enhance profitability. However, this process is not without challenges, as enterprises must navigate a myriad of risks, including political and economic uncertainties, cultural differences, and the complexity of the legal environment in the host country. Therefore, the effective evaluation and mitigation of these risks have become crucial tasks for firms undertaking OFDI.

A significant amount of academic literature explores the relationship between outward foreign direct investment (OFDI) and the digital transformation of Chinese enterprises. However, relevant studies have yielded inconsistent or even contradictory conclusions, indicating that there remains some research space in this field. For instance, the research found that digital transformation can enhance OFDI performance (Wen et al., 2024; Zhu, 2025), and its mechanism of action is primarily achieved through enhancing corporate reputation and innovation capabilities (Wang et al., 2024; S. Wu et al., 2025). However, some studies have also revealed a non-linear relationship between digital transformation and OFDI (He et al., 2024; C. Yan et al., 2024). Nevertheless, research on the specific mechanisms underlying the relationship between corporate digital transformation and OFDI remains insufficient. In particular, the mechanisms through which digital transformation achieves cost reduction and efficiency improvement, as well as the moderating effects of financing constraints and equity concentration, have not yet attracted widespread attention in the academic community.

Digital transformation holds significant potential in driving outward foreign direct investment (OFDI), yet its profound impact on OFDI strategies remains underexplored. Existing literature also pays limited attention to the varied responses of different corporate environments to digital transformation. Given that OFDI is a crucial tool for firms to achieve international expansion and resource acquisition, it is imperative to delve deeper into how digital transformation shapes OFDI strategies and outcomes. This study examines the impact and mechanisms of digital transformation on OFDI from both theoretical and empirical perspectives. We develop a conceptual framework that integrates digital transformation and OFDI, using data from Shanghai and Shenzhen A-share listed companies to validate its positive effects and analyze specific pathways. Additionally, we investigate the heterogeneous effects of digital transformation under varying corporate environments, such as financing constraints and levels of marketization. Through this research, we aim to provide new perspectives and empirical evidence on the relationship between digital transformation and OFDI, offering practical insights for firms to optimize their OFDI strategies. To empirically validate our hypotheses, we employ firm-level data from 2010 to 2019 in Shanghai and Shenzhen A-share listed companies and adopt a panel fixed-effects model. Robustness checks, including instrumental variable (IV) estimation and propensity score matching (PSM), ensure the reliability of our findings.

This study makes three key contributions. First, it expands the literature by systematically examining how digital transformation influences OFDI. Second, it proposes a dual-pathway framework, highlighting how productivity gains and transaction cost reductions drive firms’ international expansion. Third, it provides empirical evidence from Chinese listed firms, offering novel insights into the role of institutional and financial constraints in shaping the digitalization-internationalization nexus

The remainder of this paper is structured as follows. Section 2 develops the research hypotheses based on theoretical insights. Section 3 outlines the research design and methodology. Section 4 presents empirical results and robustness tests, followed by policy and managerial implications in Section 5. The final section concludes with key findings and future research directions.

Conceptual Framework

In the technology-driven era, embracing digital transformation (DT) and new technologies is crucial for staying competitive. DT isn’t just a trend; it fundamentally reshapes company operations, using modern technology to cut costs and boost production efficiency (Zheng & Bu, 2024). Regarding cost reduction, enterprises face communication and coordination challenges during the internationalization process due to institutional, cultural, and geographical differences, leading to information asymmetry and transaction costs (Cai et al., 2024). DT mitigates these costs by providing strategic information and technical support to reduce search costs and improve decision-making efficiency; by improving internal governance, coordinating external relations, integrating internal resources, reducing management costs and communication friction, enhancing internal governance, and providing a “risk reserve” for overseas risks.

In terms of improving production efficiency, DT enhances enterprise productivity through three main avenues: firstly, by strengthening innovation capabilities to achieve informatization, shifting from an enterprise-centered to a consumer demand-oriented innovation model, promoting industrial collaboration, and enhancing technological capabilities (Fang & Liu, 2024). Secondly, by utilizing the Internet of Things and big data to optimize the human capital structure (G. Yu, 2024), improve the level of intelligence, and attract high-quality talent. Thirdly, by promoting the integration of manufacturing and services, achieving specialized customer service through digital technology, and enhancing market competitiveness (P. Yu & Gao, 2024). These avenues reduce costs, meet market demands, improve productivity, and thereby promote the internationalization transformation of enterprises.

Digital transformation has a profound impact on corporate outward foreign direct investment (OFDI), but both internal and external factors of the enterprise will modulate this impact. Firstly, the degree of equity concentration is one of the important factors hindering the improvement of OFDI by digital transformation and has a significant moderating effect on the effect of digital transformation in promoting the internationalization transformation of enterprises. Generally, the higher the degree of equity concentration, the more centralized the decision-making power, which may weaken the driving force of digital transformation for the internationalization transformation of enterprises (Dong et al., 2024). In enterprises with highly concentrated equity, major shareholders may use their influence to hinder necessary digital transformations, thereby reducing the promoting effect of digital transformation on OFDI. Conversely, in enterprises with dispersed equity, digital transformation is more likely to gain widespread support and implementation due to the need to balance the interests of multiple parties, thereby more effectively promoting OFDI. Therefore, the higher the degree of equity concentration, the weaker the promoting effect of digital transformation on the internationalization transformation of enterprises.

External factors of enterprises, such as financing constraints, also affect the promoting effect of digital transformation on OFDI. Digital transformation enhances corporate OFDI capabilities by optimizing information processing and reducing transaction costs, but financing constraints may limit enterprises’ access to necessary funds, thereby weakening the positive impact of digital transformation on OFDI. In enterprises with ample funds, digital transformation is more likely to promote OFDI, while in enterprises with financing constraints, this promoting effect may be weakened (M. Li & Wei, 2024). Therefore, financing constraints play a key moderating role between digital transformation and OFDI.

The two important mechanisms by which corporate digital transformation affects corporate OFDI are cost reduction and production efficiency improvement, with the internal variable of equity concentration and the external variable of financing constraints playing a moderating role, jointly affecting this framework. Previous studies have not deeply explored the cost reduction and efficiency improvement mechanisms of digital transformation affecting OFDI, as well as the moderating effects of capital and shareholder structure. Therefore, this study aims to investigate the mechanisms by which digitalization affects foreign investment and the moderating effects of financing constraints and shareholder concentration. The conceptual framework is shown in Figure 1.

Conceptual framework.

Literature Review and Hypotheses Development

The Impact of Digital Transformation on Enterprises Internationalization

Digital transformation is a crucial phase in enterprise evolution, characterized by the integration of digital technologies into business operations and strategic decision-making. According to the knowledge-Based View (Grant, 1996), firms leverage digital technologies to enhance their ability to acquire, process, and utilize information, thereby reducing uncertainty in international markets. This technological transformation is closely linked to firms’ internationalization strategies. Digital transformation influences enterprise internationalization through two primary mechanisms: enhanced information processing and increased productivity. Digital transformation enhances the efficiency of information processing, improving the availability and accuracy of strategic data, which in turn facilitates enterprise internationalization. Through digital transformation, enterprises leverage digital technology to process large volumes of internal and external data into actionable insights, enhancing the efficiency of information utilization (Bloom, 2014). Firms apply these insights to optimize decision-making, enhance coordination between production and sales, and improve overall operational performance, thereby establishing a robust foundation for international expansion. Moreover, economies of scale in digital information processing reduce the marginal cost of data analysis while increasing its strategic value, thereby enhancing operational efficiency. The higher the enterprise’s information processing efficiency is, the clearer its internationalization strategy will be, and the stronger the promotion effect of OFDI will be. Based on these insights, the fundamental hypothesis of this paper is formulated as follows:

H1. Digital transformation has facilitated enterprises’ outward foreign direct investment (OFDI) activities.

The Mechanism of Digital Transformation Promoting Enterprises’ Outward Direct Investment

The impact of digital transformation on enterprise productivity is evident in three key dimensions, aligning with the Resource-Based View (Hooley et al., 1998), which posits that digital capabilities serve as a firm’s core strategic asset First, digital transformation fosters productivity growth by strengthening firms’ innovation capabilities. Digital firms increasingly shift from enterprise-centered innovation models to consumer-driven, collaborative innovation ecosystems, which enhances their technological edge in global markets (Neubert, 2018). Following digital transformation, enterprises gradually achieve informatization and shift from an enterprise-centered innovation model to a consumer demand-oriented innovation model, transitioning from individual enterprise innovation to collaborative industrial innovation, and enhancing technological innovation capability. Second, digital transformation optimizes the human capital structure by leveraging IoT and big data analytics for data integration, real-time analysis, and supplier collaboration, thereby enhancing enterprise intelligence and productivity (Cheng & Zhao, 2025). This technological advancement will replace ordinary labor with high-quality, highly educated talent, optimizing human capital structure. Third, digital transformation drives productivity by fostering the integration of manufacturing and service industries through advanced digital platforms and business models (Malewska et al., 2024). Traditional manufacturing and service industries are evolving into advanced and modern service industries under new platforms, business forms, and models that enable professional, customized customer interactions. Enterprises utilize relevant technologies to provide precise customer services, impacting manufacturing production and enhancing market competitiveness (Sharma et al., 2024). The application of high-end technology, along with investment in high-quality human capital, contributes to reducing production costs while meeting diverse market demands, thus improving overall productivity within enterprises.

H2. Digital transformation facilitates the international transformation of enterprises by increasing productivity.

In the process of enterprise internationalization, institutional, cultural, and geographical distances between the host and home countries create challenges in cross-border communication and coordination (Deng et al., 2019), These barriers can hinder firms’ ability to interact effectively with local suppliers and stakeholders, increasing the complexity and cost of international operations. Under these circumstances, firms incur costs associated with information search and processing, which contribute to transaction costs as defined by Transaction Cost Economics (Williamson, 2010). Information asymmetry exacerbates these costs by increasing uncertainty in foreign markets and making it more difficult for firms to identify and engage with reliable partners. Digital transformation mainly inhibits transaction costs in international transformation. By enhancing information transparency, streamlining contract enforcement, and improving cross-border coordination efficiency, digital transformation mitigates uncertainties associated with international market entry and operations. First, digital transformation enhances information transparency, reducing transaction costs associated with cross-border expansion. By leveraging big data analytics and AI-driven forecasting models, firms can identify international market risks more effectively and make data-driven investment decisions (Boubaker et al., 2023). Furthermore, digital technologies improve access to strategic information, enabling firms to optimize their internationalization strategies and mitigate uncertainties related to foreign investment. Second, digital transformation lowers market entry and operational costs by reducing information search expenses and improving decision-making efficiency. Digital platforms facilitate real-time communication with foreign stakeholders, enhance supplier coordination, and streamline logistics management (Abideen et al., 2023). These improvements lead to greater efficiency in international operations and lower overall transaction costs. Additionally, digital transformation enhances corporate governance, which in turn mitigates the adverse effects of transaction costs. By integrating digital monitoring systems and automating internal communication channels, firms can improve operational efficiency and strengthen stakeholder coordination (Plekhanov et al., 2023). These advancements reduce internal management costs, minimize communication friction, and optimize resource allocation across subsidiaries in different markets. Moreover, digital transformation establishes risk mitigation mechanisms, providing firms with a “risk buffer” against external shocks. Cloud computing, blockchain, and real-time data analytics enhance transparency in financial reporting and improve firms’ ability to respond proactively to potential financial losses or regulatory challenges in foreign markets (Qader & Cek, 2024). Therefore, enterprise digital transformation can reduce transaction costs and increase the “risk reserves” to offset the loss of transaction costs to facilitate international transformation. Accordingly, we propose the following research hypothesis:

H3: Enterprise digital transformation promotes outward direct investment through transaction cost mechanism.

The Moderating Effects of Financial Constraints and Ownership Concentration

While digital transformation strengthens enterprise internationalization by improving information management, boosting productivity, and reducing transaction costs, its influence on outward foreign direct investment (OFDI) is not uniform across all firms. Certain firm-specific characteristics may alter the extent to which digital transformation facilitates OFDI. Among these, financial constraints and ownership concentration are particularly influential, as they shape firms’ strategic investment decisions and risk-taking behaviors.

Financial constraints pose a significant barrier to firms’ ability to undertake large-scale investments, especially in international markets where expansion requires substantial capital. Pecking order theory (Leary & Roberts, 2010) suggests that financially constrained firms tend to rely on internal capital rather than external financing, often leading to suboptimal investment decisions. Even when digital transformation creates internationalization opportunities, capital shortages may hinder firms from fully capitalizing on them.

One of the key benefits of digital transformation is its potential to reduce information asymmetry and enhance operational efficiency, which can improve a firm’s creditworthiness and access to Y. Liu and He (2024). However, firms experiencing severe financial constraints may find it difficult to allocate sufficient resources toward digital infrastructure, market research, and overseas expansion efforts, ultimately weakening the positive impact of digitalization on OFDI.

H4: Financial constraints weaken the positive impact of digital transformation on outward foreign direct investment (OFDI).

Ownership concentration, which refers to the degree to which a firm’s equity is controlled by a small number of large shareholders, plays a crucial role in shaping corporate strategy, and investment preferences. Agency theory (Leary & Roberts, 2010) argues that concentrated ownership structures can lead to risk-averse decision-making, as controlling shareholders often prioritize wealth preservation and stability over aggressive expansion. This cautious stance may dampen firms’ willingness to engage in OFDI, even when digital transformation provides new avenues for international growth.

Moreover, high ownership concentration may contribute to managerial entrenchment, where dominant shareholders exert significant influence over strategic choices, favoring short-term financial stability over long-term international expansion (de Freitas Brandão & Crisóstomo, 2024). Such firms may be reluctant to make substantial digital investments that entail higher risk and delayed returns. Conversely, firms with dispersed ownership structures tend to be more inclined toward growth-oriented strategies (L. Yan et al., 2023), enabling them to more effectively leverage digital transformation for OFDI.

H5: Ownership concentration weakens the positive impact of digital transformation on outward foreign direct investment (OFDI).

The Moderating Effects of Banking Competition and Marketization

The extent to which digital transformation facilitates outward foreign direct investment (OFDI) depends on external financial and institutional conditions. Among these, banking competition and marketization significantly influence firms’ ability to translate digital advancements into global expansion.

A competitive banking sector improves firms’ access to external financing by enhancing credit availability, reducing borrowing costs, and broadening financial services. Digital transformation increases firms’operational transparency and financial credibility, making it easier to secure funding and supporting international expansion.

However, in less competitive banking environments, firms—especially private enterprises—face higher borrowing costs and stricter loan conditions. Despite digitalization’s efficiency gains, firms in these settings may struggle to obtain sufficient capital for overseas investment, dampening the positive effects of digital transformation on OFDI.

H6: Banking competition strengthens the impact of digital transformation on outward foreign direct investment.

Marketization, which reflects economic openness, institutional efficiency, and regulatory transparency, moderates the relationship between digital transformation and OFDI. In regions with higher marketization, firms experience fewer regulatory constraints, stronger legal protections, and greater economic freedom, which facilitate international expansion. Digital transformation further enhances firms’ ability to streamline operations, optimize cross-border coordination, and navigate regulatory environments, reinforcing its role in driving OFDI.

In contrast, low-marketization environments often involve policy unpredictability. Although digital transformation improves decision-making and efficiency, institutional rigidities and regulatory uncertainties can limit its effectiveness in promoting OFDI.

H7: Marketization strengthens the impact of digital transformation on outward foreign direct investment.

Data and Methodology

Sample Selection

The samples in this paper are Shanghai and Shenzhen A-share listed companies from 2010 to 2019. We processed the samples using the following steps: (1) Samples with ST, PT, and *ST in the sample period were deleted. (2) The sample of listed companies in the financial industry is deleted. (3) Companies listed in the sample period were deleted. (4) Samples with missing main variables were deleted. At the same time, considering the influence of extreme values, we winsorize the main variables by 1% and 99%. After processing, a total of 40,251 investment country-company annual observations were obtained. Financial data of listed companies, comprehensive governance data, and data of overseas affiliated companies are from CSMAR and Wind databases, regional economic data are from provincial statistical almanacs, and host country economic data are from the China Economic Net statistical database. The bank network data comes from the financial license information database of the China Banking and Insurance Regulatory Commission.

Variables

Dependent Variable

Referring to the practices of W. L. Wu and Shao (2023), we use the variable OFDI as the measurement index of enterprises’ internationalization transformation (W. L. Wu & Shao, 2023; Yi et al., 2022). Specific practices: According to the data of overseas affiliated companies in the CMSAR database, if the total shareholding ratio of the company’s direct control and indirect control exceeds 10% in the current year, the value of OFDIt+1 is 1; otherwise, the value is 0. Since the impact of digital transformation has a certain time lag, and to avoid the endogenous problem of mutual causality between digital transformation and OFDI, we choose t + 1 data as the variable explained in this paper.

Independent Variables

Digital Transformation Index

There is no unified metric to measure the extent of a company’s digital transformation. The primary methods include three approaches: First, assessing the level of digital transformation through surveys of IT personnel within companies (Ferreira et al., 2019; Mikalef & Pateli, 2017). The drawback of this method is that the application of IT is often merely basic network usage, which significantly differs from true digital transformation. Additionally, the sample size in questionnaire surveys is inherently limited. Second, identifying the proportion of a company’s intangible assets attributed to digitalization through the frequency of digital-related keywords (Jiang et al., 2022). Although this metric is straightforward, it is susceptible to companies overestimating their intangible assets and can confuse digital intangible assets with other intangible assets. Third, using text mining to measure the frequency of digital transformation-related keywords in company texts, thereby calculating the company’s digital transformation index (Gal, 2019; R. Li et al., 2022; X. Zhao et al., 2022).

We referenced S. Liu et al. (2023), Gao et al. (2023), and Zhuo and Chen (2023) to derive keywords for corporate digital transformation based on a generalized definition of digitalization. Using text mining methods, we measured the frequency of these digital transformation-related keywords in the “Management Discussion and Analysis” section of listed company announcements to assess the extent of their digital transformation (Boubaker et al., 2023; Gao et al., 2023; Zhuo & Chen, 2023). The specific steps for calculation are as follows: First, we extracted sources related to “digital transformation” from relevant policy documents and definitions of corporate digital transformation to establish a text retrieval database (see Table 1 in Appendix A for the lexicon). Next, we created search keywords based on the retrieval database and used Python crawling technology to capture the frequency of “digital” keywords in mid-year reports of listed companies. Finally, we cleaned and normalized the data to obtain a variable measuring the extent of corporate digital transformation (DTI). The specific calculation formula is as follows:

The formula variables are defined as follows: TWit represents the total frequency of “digital” keywords for a single company, minTWit represents the annual minimum total frequency within the industry, and maxTWit represents the annual maximum total frequency within the industry.

Mediating Variable

(1) Total Factor Productivity (TFP)

Drawing on the methods of Askenazy et al. (2015), Cheng et al. (2023), and Wang et al. (2023), we use the LP method, OLS method, and fixed effects to calculate Total Factor Productivity (TFP) as a proxy variable for production efficiency. The specific construction formula is as follows:

First, we assume that the production function of firm i at time t is a Cobb-Douglas production function (C-D production function):

Where Yit is the output of firm i at t, Lit is the labor input, Kit is capital input, and α and β are the output elasticities of capital and labor, respectively.

And Ait is the total factor productivity (TFP). Next, let y = lnY, l = lnL, k = lnK, and convert (2) into linear form:

In which ε represents the logarithmic form of total factor productivity. Again, this paper derives the following model to estimate total factor productivity:

Where Yit represents the industrial added value of firm i in year t, Lit and Kit represent the number of employees and fixed assets of firm i in year t, respectively; λ, η, and δ represent the fixed effects of time, industry, and region, respectively; uit is the random disturbance term.

Thus, from the above analysis and the TFP formula, we can obtain:

Then, the formula for Total Factor Productivity (TFP) can be derived from the above equation:

Finally, the Total Factor Productivity (TFP) calculated using different methods results in three variables:

First, this paper transforms fixed assets into intermediate inputs to overcome zero investment. Using the Generalized Method of Moments (GMM) and employing capital from period t and intermediate inputs from period t − 1 as instrumental variables, we estimate model (6) and obtain the TFP calculated by the Levinsohn-Petrin method (TFP_LP); Second, according to model (4) and formula (5), we estimate and calculate the TFP using the OLS method (TFP_OLS); Third, we estimate model (4) by adding individual fixed effects to model (4), and then calculate the TFP using the fixed effects method (TFP_FE) according to formula (5).

(2) Transaction Costs (TCost)

Drawing on the research of Peng, Yang, and Jiang (2022) and Fan et al. (2023), we use Mcost, Fcost, and Tcost to represent the internal transaction costs, external transaction costs, and operating transaction costs faced by firms, respectively. The specific calculation formulas are as follows:

where MFit represents the firm’s management expenses, FFit represents the financial expenses, OCit represents the operating costs, TLit represents the total liability, and TAit represents the total assets.

Control Variables

Referring to the studies of X. Liu et al. (2014), Peng, Jiang et al. (2022), and D. Zhang et al. (2023), this paper selects the following variables as control variables: debt-to-asset ratio (Leverage), cash assets, return on equity(ROE), capital intensity (Capital), foreign shareholding ratio (OFII), audit opinion (Opinion), host country GDP growth rate (GDP), and host country total population (population). The specific variable definitions and symbols are shown in Table 1.

Definitions of Variables.

Model Construction and Regress Approach

Benchmark Regression Model Setting

To verify the impact of digital transformation on enterprises’ outward direct investment (H1) and based on existing research (Kong, Tong et al., 2021), since the breadth of outward direct investment OFDIt+1 is a binary variable, we set the following Probit regression model as the benchmark model according to the characteristics of binary choice variables:

Among them, OFDIi,c,t+1 is the dummy variable for the outward direct investment of enterprise iii in country c in year t + 1 (breadth of outward direct investment). DTIi,t is the digital transformation index of enterprise i in year t, Xi,c,t is a series of control variables as shown in Table 1, λt represents the time-fixed effects, ηj represents the industry fixed effects, and εit represents the random disturbance term.

At the same time, in the robustness test, we use the outward direct investment frequency (OFDISt+1) and set the following Poisson regression model according to the characteristics of discrete variables to verify the impact of digital transformation on the depth of enterprises’ outward direct investment, thereby also verifying the robustness of the benchmark regression:

Among them, OFDISi,c,t+1 is the frequency of outward direct investment of enterprise i in country c in year t + 1 (depth of outward direct investment), and the other variables are the same as in (10).

Mediation Effect Model Setting

To verify H2 and H3, following the testing procedures of Baron and Kenny (1986) and Gao et al. (2023), we set the following mediation effect models:

Among them, the regression equation for total factor productivity (TFP) is a Poisson regression model, and the regression model for transaction cost (TCost) is a mixed least squares regression model.

Results and Discussion

Descriptive Statistics

The descriptive regression results of the main variables are shown in Table 2. We can see from Table 2 that the mean value of foreign direct investment (OFDIt+1) is 0.49, the maximum value is 1, and the minimum value is 0, indicating that nearly half of the companies carried out foreign direct investment activities during the sample period, and the standard deviation is 0.5. It shows that the sample companies’ foreign direct investment showed great differences during the sample period. The maximum value of the enterprise digital transformation index is 0.89, the minimum value is 0, the mean is 0.11, and the standard deviation is 0.17, indicating that the degree of digital transformation among sample companies varies greatly, and some companies have not yet carried out digital transformation activities.

Descriptive Statistics.

Result of Basic Regression

Table 3 presents the results of the baseline regression. From the regression results, the estimated coefficients of the Digital Transformation Index (DTI) are 0.235, 0.357, 0.167, and 0.214, all significant at levels above 5%. This indicates that the higher the degree of digital transformation, the higher the probability of a company investing abroad. Therefore, the above regression results do not reject H1; digital transformation promotes the internationalization of companies.

The Results of the Baseline Regression.

Note. The t-values within parentheses are calculated at the host country cluster level.

, **, denote significance levels at 1%, 5%, respectively.

Result of Regression of Mediating Effect

The Mechanism Effect of Productivity

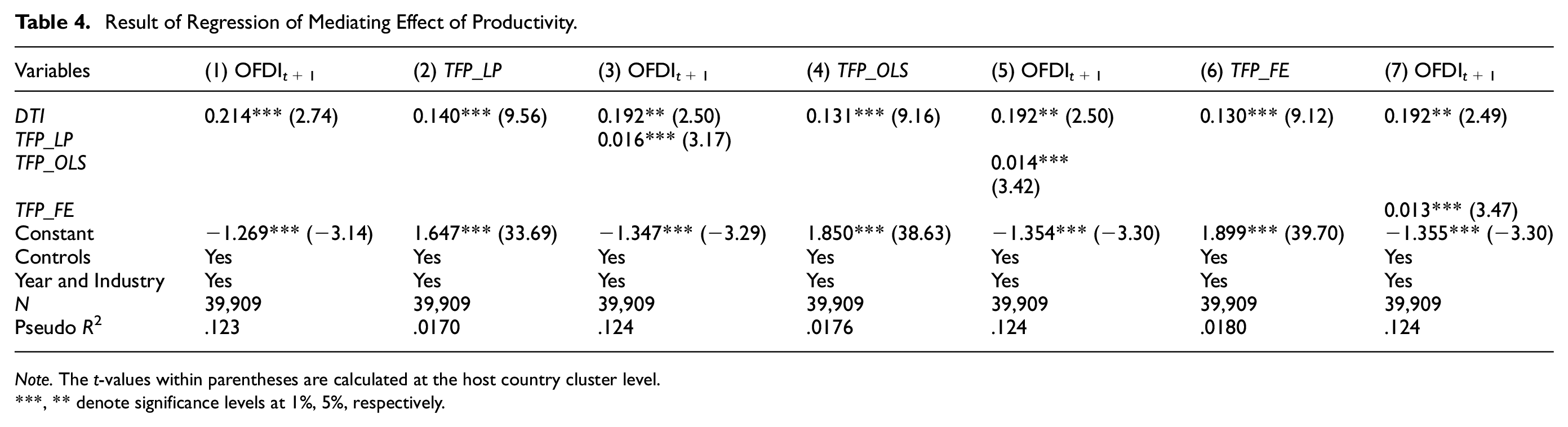

Table 4 shows the regression results of the mediating effect of productivity. According to the regression results, Column (1) is the baseline regression, where the coefficient estimate of the Digital Transformation Index (DTI) represents the total effect of the mediating mechanism. In Columns (2), (4), and (6), the coefficient estimates of the Digital Transformation Index (DTI) are 0.140, 0.131, and 0.130, respectively, all of which are significantly positive at the 1% level, indicating that digital transformation enhances total factor productivity. In Columns (3), (5), and (7), the coefficient estimates of total factor productivity (TFP_LP, TFP_OLS, TFP_FE) calculated by three methods are 0.016, 0.014, and 0.013, respectively, all of which are significantly positive at the 1% level, indicating that corporate productivity positively affects OFDI. Meanwhile, the Digital Transformation Index (DTI) coefficient estimates are all 0.192 and significantly positive at the 5% level, with significance and coefficient values lower than those of the baseline regression, indicating that the productivity mechanism exists, is positive, and constitutes a partial mediating effect. The above regression results show that corporate digital transformation promotes internationalization through enhanced productivity, suggesting that H2 cannot be rejected.

Result of Regression of Mediating Effect of Productivity.

Note. The t-values within parentheses are calculated at the host country cluster level.

, ** denote significance levels at 1%, 5%, respectively.

The Mechanism Effect of Transaction Cost

Table 5 displays the regression results of the mediating effect of transaction costs. From the regression results, Column (1) shows the baseline regression, where the Digital Transformation Index (DTI) coefficient estimate represents the mediating mechanism’s total effect. In Columns (2), (4), and (6), the coefficient estimates of the Digital Transformation Index (DTI) are −0.02, −0.004, and −0.391, respectively, all significantly negative at the 1% level, indicating that digital transformation can reduce corporate transaction costs. In Columns (3), (5), and (7), the coefficient estimates of internal transaction costs (Mcost), external transaction costs (Fcost), and operational transaction costs (Tcost) are −0.082, −2.249, and −0.041, respectively, all significantly negative at levels above 10%, indicating that transaction costs have a negative impact on ODFI. Meanwhile, the coefficient estimates of the Digital Transformation Index (DTI) in Columns (3), (5), and (7) are 0.212, 0.205, and 0.199, respectively, all significantly positive at the 5% level. The significance and coefficient values are smaller than those in the baseline regression, indicating the existence of a transaction cost mechanism that is positive and partially mediates the effect. These regression results suggest corporate digital transformation promotes international transformation by reducing transaction costs, supporting hypothesis H3.

Result of Regression of the Mediating Effect of the Transaction Cost.

Note. The t-values within parentheses are calculated at the host country cluster level.

, **, * denote significance levels at 1%, 5%, and 10%, respectively.

Test for Robustness

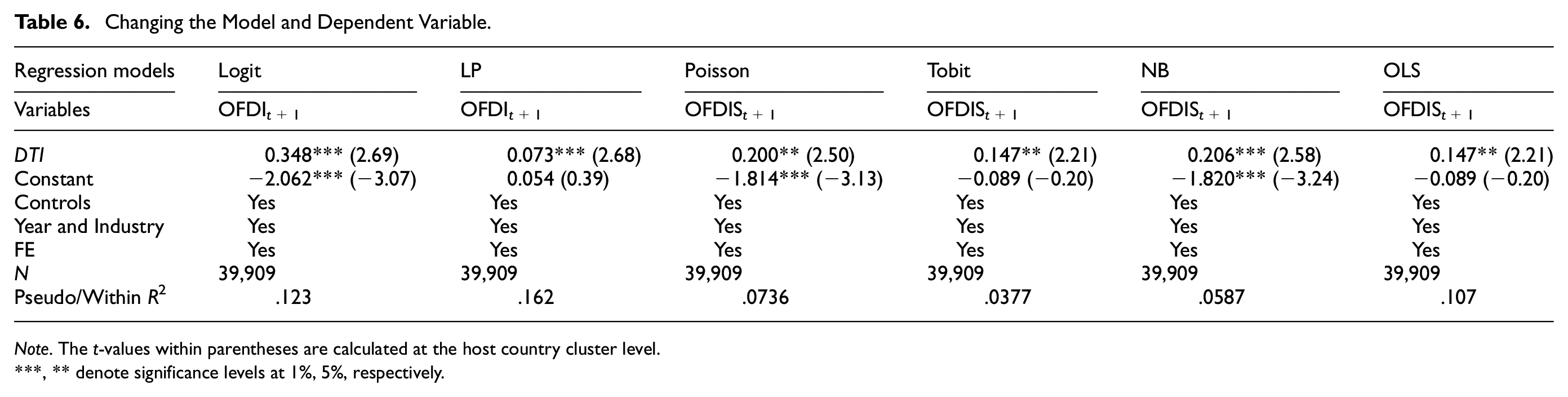

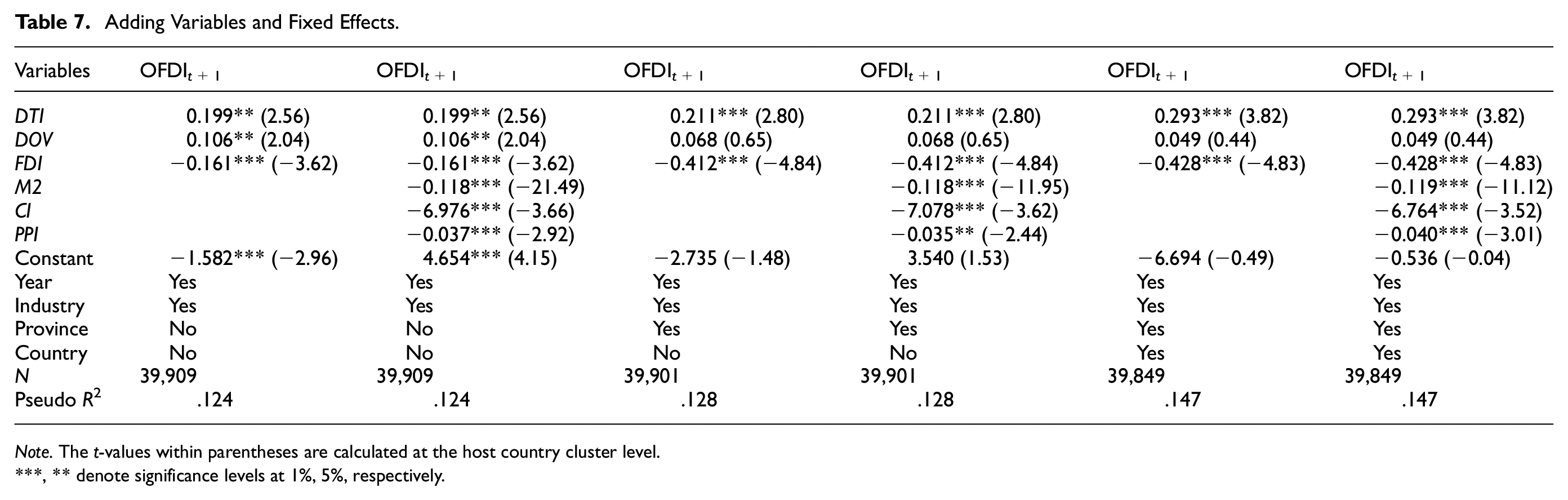

In the above empirical verification, this paper has dealt with a one-period lag to the explanatory variables and control variables to minimize the endogeneity problem of reverse causality. First, we use the non-parametric permutation method for placebo tests, with the results shown in Figure 2. Second, based on the characteristics of the data, we replace the dependent variable with the frequency of outward foreign direct investment (OFDISt+1) and employ Poisson regression, Tobit model, Negative Binomial regression model (NB), and Ordinary Least Squares regression model (OLS). Additionally, we replace the original Probit model with the Logit linear probability model (LP). The regression results are presented in Table 6. These regression results suggest corporate digital transformation promotes international transformation. Third, we introduce regional per capita GDP (PerGDP, logarithm of regional per capita GDP), regional openness level (DOV, the ratio of regional total imports and exports to regional GDP), foreign direct investment (FDI, the ratio of regional FDI to regional GDP), money growth rate (M2, growth rate of broad money), social fixed asset investment (CI, the ratio of total social fixed asset investment to GDP), and producer price index (PPI, growth rate of the producer price index). We also add province and country fixed effects. The corresponding empirical results are shown in Table 7, all models indicate that DT and OFDI are significantly positively correlated, with significance at least at the 5% level. Fourth, following the methods of Peng, Yang, and Jiang (2022) and N. Zhao and Ren (2023), we use the regional internet penetration rate (IP) as an instrumental variable for two-stage least squares regression. Table 8 shows the regression results of the instrumental variable method. From the first-stage estimation results in the table, the regression results of the instrumental variables and endogenous explanatory variables are significantly positive at the 1% level, and the unidentifiability test is passed. This indicates a strong correlation between the instrumental variables and the endogenous variables, and there is no issue of weak instrumental variables. In addition, in the second stage, the estimation results show that after considering the above endogeneity effects, the estimated coefficient of corporate digital transformation remains positive. This suggests that the positive effect of corporate digital transformation on outward foreign investment remains unchanged.

Placebo test results.

Changing the Model and Dependent Variable.

Note. The t-values within parentheses are calculated at the host country cluster level.

, ** denote significance levels at 1%, 5%, respectively.

Adding Variables and Fixed Effects.

Note. The t-values within parentheses are calculated at the host country cluster level.

, ** denote significance levels at 1%, 5%, respectively.

IV Instrument: Method.

Note. The t-values within parentheses are calculated at the host country cluster level.

denote significance levels at 1%.

We use the propensity score matching method (PSM) to test for sample selection bias. The regression results after PSM are displayed in Table 9 All models indicate that DT and OFDI are significantly positively correlated, with significance at least at the 5% level. The robustness test results all indicate that the empirical results supported by the baseline regression are robust.

PSM Method.

Note. The t-values within parentheses are calculated at the host country cluster level.

, ** denote significance levels at 1%, 5%, respectively.

Moderating Effect Analysis

Internal Moderating Effect

We introduce the KZ index and the shareholding ratio of the largest shareholder to examine the differences in the impact of corporate digital transformation on internationalization under the moderating effects of financing constraints and ownership concentration. Drawing on Kaplan and Zingales (1997) and B. Yan et al. (2018), we use the KZ index to measure corporate financing constraints. Referring to the studies of Sun et al. (2022) and Yi et al. (2022), we use the shareholding ratio of the largest shareholder (Top1) as a proxy variable for ownership concentration. The calculation formula for the KZ index is as follows:

Among them, CFit represents the company’s operating cash flow, Dividendsit represents the company’s paid cash dividends, Cashit represents the company’s cash level, and Qit represents Tobin’s Q ratio; TLit represents the company’s total liabilities, and TAit represents the company’s total assets.

Table 10 shows the regression results of the internal moderating effect of financing constraints and shareholder ownership on the company. In the regression results for the moderating effect of financing constraints, shown in columns (3) and (4), the coefficient estimate for the interaction term between the Digital Transformation Index (DTI) and the KZ Index (KZ) is 0.002, with an average treatment effect of 0.001, which is not statistically significant. The coefficient value and the average treatment effect are much smaller than the corresponding values for the baseline regression of the Digital Transformation Index (DTI), indicating that the stronger the financing constraints, the weaker the promoting effect of digital transformation on the company’s outward direct investment. In the regression results for the moderating effect of shareholder ownership, shown in columns (5) and (6), the coefficient estimate for the interaction term between the Digital Transformation Index and the shareholding ratio of the largest shareholder (Top1) is 0.006, with an average treatment effect of 0.002, which is significant at the 1% level. The coefficient value and the average treatment effect are much smaller than the corresponding values for the baseline regression of the Digital Transformation Index (DTI), indicating that the higher the ownership concentration, the weaker the promoting effect of digital transformation on the company’s international transformation.

Internal Moderating Effect.

Note. The t-values within parentheses are calculated at the host country cluster level. AE = average treatment effect; EC = estimated coefficient.

denote significance levels at 1%. The odd columns represent the ECs, while the even columns represent the corresponding AEs. The control variables are consistent with the baseline regression.

External Moderating Effect

We introduce the degree of bank competition and marketization to examine the differences in the impact of corporate digital transformation on internationalization under the moderating effects of bank loan accessibility and marketization. Following the approach of Chong et al. (2013), we use the regional bank competition level (AHHI) as a proxy variable for bank loan accessibility. Referring to the study by Wang et al. (2023), we use the Marketization Index (MI) as a proxy variable for the regional marketization level. The calculation formula for the regional bank competition level (AHHI) is as follows:

Where NB represents the number of new bank branches in the region, and TB represents the total number of bank branches in the region.

Table 11 presents the regression results of the moderating effects of regional bank loan accessibility and marketization level. In the regression results for the moderating effect of bank loan accessibility, that is, column (3) and column (4), the coefficient estimate of the interaction term between the Digital Transformation Index (DTI) and the regional bank competition level (AHHI) is 0.402, with a corresponding average treatment effect of 0.139, which is significant at the 1% level. The coefficient value and average treatment effect are much higher than the corresponding values of the baseline regression for the Digital Transformation Index (DTI), indicating that the stronger the bank loan accessibility, the stronger the promoting effect of corporate digital transformation on internationalization. w?>In the regression results for the moderating effect of the Marketization column (5) and column (6), the coefficient estimate of the interaction term between the Digital Transformation Index (DTI) and the regional Marketization Index (MI) is 1.915, with a corresponding average treatment effect of 0.662, which is significant at the 5% level. The coefficient value and average treatment effect are much lower than the corresponding values of the baseline regression for the Digital Transformation Index (DTI), indicating that the higher the regional marketization level, the more significant the promoting effect of corporate digital transformation on internationalization.

External Moderating Effect.

Note. The t-values within parentheses are calculated at the host country cluster level. AE = average treatment effect; EC = estimated coefficient.

, ** denote significance levels at 1%, 5% respectively. The odd columns represent the ECs, while the even columns represent the corresponding AEs. The control variables are consistent with the baseline regression.

Conclusion

In an era of rapid digital economic growth and heightened external uncertainties, enterprises increasingly rely on digital technologies to support their internationalization strategies. This study, based on data from Chinese listed companies from 2009 to 2019, employs a two-way fixed-effects regression model to examine the impact of digital transformation on outward investment. The findings indicate that digitalization significantly facilitates international expansion by improving productivity and reducing transaction costs. However, its effectiveness is influenced by financing constraints, equity concentration, regional banking conditions, and marketization levels. These results underscore the strategic significance of digital transformation in global business expansion. From a policy standpoint, enterprises should harness digital technologies to overcome traditional market barriers, streamline operations, and enhance their global competitiveness. Incorporating digital strategies can attract investment, ease financial constraints, and strengthen corporate governance, ultimately reinforcing firms’ international positioning. Beyond corporate initiatives, policymakers and financial institutions play a crucial role in fostering a supportive environment for digital-driven globalization. Governments should refine regulatory frameworks to advance digital infrastructure, facilitate cross-border data flows, and incentivize the adoption of cutting-edge technologies such as artificial intelligence, blockchain, and big data analytics. Furthermore, regulations should balance cybersecurity with the need for an open and interconnected international business landscape. Financial institutions, including commercial banks and investment firms, should design specialized financial instruments to support enterprises undergoing digital transformation, and internationalization. Expanding access to digital financing, improving credit risk assessment for technology-driven businesses, and offering targeted financial incentives—such as low-interest loans and subsidies—can help mitigate capital constraints that hinder global expansion. Additionally, local governments should introduce supportive measures, including tax benefits, trade facilitation programs, and institutional reforms, to create an innovation-friendly and competitive market environment. Future research should refine the measurement of digital transformation and internationalization by incorporating more detailed indicators that capture their depth, scope, and efficiency. Moreover, examining the long-term effects of digitalization on global business expansion across various industries and regulatory contexts would provide further valuable insights.

Limitations and Future Research Directions

Despite its contributions, this study has some limitations. First the measurement of digital transformation relies on existing indicators, which may not comprehensively reflect its dynamic and multifaceted nature. Future studies could explore more precise and real-time metrics, such as firm-level digital investments, AI-driven process automation, or technology adoption rates, to provide a more refined assessment of digitalization’s impact.

Secondly, while this study considers financial and institutional factors as moderators, other external influences—such as geopolitical risks, cultural differences, and environmental regulations—may also shape the relationship between digital transformation and internationalization. Future research could incorporate these dimensions to offer a more comprehensive understanding of global expansion dynamics.

Lastly, the empirical approach primarily relies on a fixed-effects regression model. Future studies could apply alternative econometric techniques, such as instrumental variable approaches or machine learning methods, to address potential endogeneity concerns, and enhance causal inferences.

By addressing these limitations, future research can further deepen the understanding of digital transformation’s role in corporate internationalization and provide more targeted policy recommendations to support firms navigating an increasingly digitalized global economy.

Footnotes

Appendix A

Digital Transformation Keywords.

| Project | Keywords |

|---|---|

| Artificial Intelligence Technology | Artificial Intelligence, Business Intelligence, Image Understanding, Investment Decision Support Systems, Intelligent Data Analytics, Intelligent Robots, Machine Learning, Deep Learning, Semantic Search, Biometric Recognition Technology, Facial Recognition, Speech Recognition, Identity Verification, Autonomous Driving, Natural Language Processing |

| Big Data Technology | Big Data, Data Mining, Text Mining, Data Visualization, Heterogeneous Data, Credit Scoring, Augmented Reality, Mixed Reality, Virtual Reality |

| Cloud Computing Technology | Cloud Computing, Stream Computing, Graph Computing, In-Memory Computing, Multi-Party Secure Computing, Brain-Like Computing, Green Computing, Cognitive Computing, Converged Architecture, Billion-Level Concurrency, Exabyte-Level Storage, Internet of Things, Cyber-Physical Systems |

| Blockchain Technology | Blockchain, Digital Currency, Distributed Computing, Differential Privacy Technology, Smart Financial Contracts |

| Digital Technology Application | Mobile Internet, Industrial Internet, Mobile Connectivity, Internet Healthcare, E-commerce, Mobile Payments, Third-party Payments, NFC Payments, Smart Energy, B2B, B2C, C2B, C2C, O2O, Online Linkage, Smart Wearables, Smart Agriculture, Smart Transportation, Smart Healthcare, Smart Customer Service, Smart Home, Smart Investment Advisory, Smart Tourism, Smart Environmental Protection, Smart Grid, Smart Marketing, Digital Marketing, Unmanned Retail, Internet Finance, Digital Finance, Fintech, Financial Technology, Quantitative Finance, Open Banking |

Ethical Considerations

This study did not involve any human or animal testing, and therefore no ethical approval was required.

Funding

The author(s) disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: The authors acknowledge the financial support from the project of the Provincial and Ministerial Level: “Green Finance Empowering the Implementation of ‘Four Waters and Four Regulations’ in the Poyang Lake Basin: Internal Mechanisms and Implementation Paths” (23YJ35). The funders had no role in study design, data collection and analysis, decision to publish, or preparation of the manuscript.

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Data Availability Statement

The data that support the findings of this study are openly available upon request.