Abstract

Recently, China has emerged as the largest trading partner and a significant source of investment in the African continent. Although there is consent on the increasing importance of China and Africa’s economic partnership, there are many controversies on how it affects African countries. Debates on China in Africa have, however, relied on grandiloquence rather than empirical studies. This study explores the causal link between China-Africa trade, China’s outward foreign direct (OFDI), and economic growth of 24 Sub-Saharan Africa countries from 1999 to 2018. The aggregated panel is classified into upper-middle-income, low-middle income, and low-income Sub-Saharan African countries. In the long run, key findings from the feasible generalized least squares (FGLS) estimator unveiled that; (i) China-Africa trade negatively contributes to economic growth among all panels. (ii) China’s OFDI improves economic growth in the low middle and low-income African countries whereas a significant negative liaison is evidenced in the upper-middle-income African countries. (iii) Labor force have a negative impact on economic growth whiles gross capital formation is evidenced to positively impact economic growth at all the panels. The Dumitrescu and Hurlin Granger causality unveiled a one-sided causal link from China-Africa trade to economic growth at all panels. The study proposes policy recommendations based on the results.

Introduction

China exerts the highest gravitational pull even on the so-called major market economies, and almost every developing or emerging market has been gathered into its economic orbit. After nearly 60 years of uninterrupted trade ties with its colonial masters, there is a paradigm shift in bilateral trade destinations as most countries in Africa continue to witness countries contemporaneous mass movements to pursue a favorable trade relationship with China (Luo & Gao, 2020). Currently, China is the largest trading partner and a significant investment source in Africa compared to the conventional trade partners of Africa due to the unprecedented increase in the volume of China-Africa trade and Overseas Foreign Direct Investment (Miao, Lang et al., 2020). The value of China’s trade with Africa reached its peak in 2015 with a trade value of approximately US$ 145 billion (UN Comtrade, 2015), with many Chinese industries exporting goods and undertaking projects in the various sectors of Africa; and Africans importing a variety of consumer goods and exporting primary commodities to China (Pigato & Tang, 2015). Consequently, China’s outward foreign direct investment (OFDI) stock to Africa increased to US$ 37 billion in 2015 (UN Comtrade, 2015), making China the largest emerging country to invest in Africa.

Since then, China’s share of trade volume in Africa has witnessed a persistent rise reaching an all-time high of US$208 billion in 2019. But not for the impact of the coronavirus pandemic, African economists had predicted a higher trade volume between Africa and China in 2020 due to the expected effects of the African Free Trade and Continental Agreement (Munday, 2021). Also, China and Africa outline social and economic activities aimed at fostering a “win-win” partnership which is a prominent feature in the Forum on China-Africa Cooperation (FOCAC) (Esterhuyse & Moctar, 2014).

China’s growing interest in Africa has, however, sparked heated debate among researchers and policy analysts. Although there is consent on the increasing importance of China and Africa’s economic partnership, there are many controversies on how it affects both sides, especially Africa’s economic performance (Chen & Dollar, 2018). There are also doubts about whether China’s OFDI to African countries promotes productivity growth, and technology absorption in the Africa continent (Negash et al., 2020). Further, a new strand of African economic literature questions the extent to which Africa’s trade deals with China and China’s OFDI to Africa seeks to satisfy a “win-win situation” as often trumpeted by China’s Master Facility (Habyarimana & Opoku, 2018; Luo & Gao, 2020; Megbowon et al., 2019). For developing economies in Africa, trade and FDI inflows from other countries are essential as they may help them develop infrastructure, absorb new technologies, transfer knowledge to domestic firms and increase the labor force to boost productivity and economic growth (Sakyi & Egyir, 2017). China has, therefore, launched several global infrastructures development initiatives, with a particular emphasis on expanding infrastructure across the African continent. For example, Chinese conglomerates are involved in the provision of utilities, construction of a dam, hydroelectric power plants, railways, and the provision of telecommunication infrastructure and agricultural technology in Africa. Chinese Development Banks are also among the largest creditors in Africa.

However, the effects of China–Africa trade and Chinese investment on Africa’s economic growth have strewn muddle and remain a key topic in the economic literature. Although a number of studies have examined potential problems and merits linked to China-Africa economic relationship, most of these studies (Ademola et al., 2016; Lisimba, 2020; Munday, 2021; Pigato & Tang, 2015) adopted descriptive and macroeconomic approaches; therefore, restricted to general policy prospects on China in Africa. While the other empirical studies that analyzed the economic effect of China-Africa trade and Chinese OFDI in a panel setting ignored the standard econometric procedure of testing for the presence or absence of residual cross-sectional reliance (Hou et al., 2021; Miao, Lang et al., 2020; Miao, Yushi et al., 2020; Zhang, 2021). The existence or non-existence of residual cross-sectional connectedness present in a panel data system is vital with regard to selecting the appropriate econometric approaches. Further, the majority of the studies on the China-Africa relationship to date do not take into account the income levels or country-specifics. It has been established that trade and FDI effects are not the same for all countries, and some African economies, particularly the low-income countries, are considered to face more enormous risks.

Relying on the limitations of previous studies on the China-Africa partnership, this current study empirically examines the causal link between China-Africa trade, China OFDI, and the economic growth of African countries. The study considers cross-sectional dependency and heterogeneity issues among the selected countries. To avoid the well-known problem associated with low-power conventional econometric techniques, modern panel data models are used. Additionally, the study considers both panel and country income classifications. This, therefore, allow for the analysis of a broad-based link within a framework categorized by factor unique to the panel and each income level. The findings of this study are believed to help other emerging economies to recognize the potential factors that may be significant to boost economic growth.

The rest of the study is structured as follows: Section 2 provides the recent literature on the topic. Section 3 provides the theoretical model, econometric approaches utilized, and data. Section 4 presents the empirical results and discussion; Section 5 comprises the conclusion and policy recommendations, while Section 6 provides the limitation of the study.

Literature Review

China-Africa Trade and Economic Growth

For several decades, the assertion that trade stimulates economic growth has been debated by economists and researchers across the world (Egyir et al., 2020; Ramzan et al., 2019). On the theoretical dimension, some studies exposed that trade accelerates economic growth by enabling the diffusion of knowledge and technology from the import of technological goods (Ciruelos & Wang, 2005; Perez-Trujillo & Lacalle-Calderon, 2020). The theory of Smith (1776) states that countries generate more revenues when they purchase through trade those goods that they could not produce competently and manufacture only those goods that they could produce.

A variety of empirical studies have been performed based on this conventional viewpoint, the impact of trade on the economic growth of African countries (Admassu, 2019; Dvouletý, 2019; Manwa et al., 2019). The China-Africa trade and economic growth nexus has attracted even greater attention in recent years, in the wake of increasing trade ties between developing countries. Studies on whether China-Africa trade stimulates economic growth of Africa countries, however, remain one of the complex issues in the economic literature with regards to Ademola et al. (2016), Eisenman (2012), and Habyarimana and Opoku (2018) asserting that China-Africa trade has both positive and negative influence on the economic growth of African countries. According to Drummond and Liu (2015), the increasing African trade relationship with China has paved the way for African economies to expand their export base across nations, away from developed economies, which can be regarded as positive growth. He (2013), upon exploring the exports of manufactured products from Sub-Saharan Africa to reflect the output of countries concluded that Africa-China trade has a significant positive effect on the economic growth of African countries. Miao, Yushi et al. (2020) argued that the economic partnership between China and African countries is subject to the domestic standard of African countries’ institutions. Their study results evidenced a significant influence of China-Africa trade on the total factor productivity (TFP) of 44 African economies. More particularly, Baliamoune-Lutz (2011) exposed that Africa economies export to China and imports from China positively accelerate growth in Africa. In specific, the authors finding contradict the notion of the resource curse and dislocation effects. Similarly, Kummer-Noormamode (2014) showed evidentiary proof that the China-Africa trade relationship is more beneficial to African economies than trade with the European Union (EU). A recent study by Hou et al. (2021) shows that trading with China provides greater opportunities for Ghanaian manufacturing firms to increase productivity than trading with OECD economies. Thus, increased import intensity from China excites productivity gains, whereas increased exports to China boost productivity in Ghana industries. This departs from earlier studies by Hanusch (2012) and Yin and Vaschetto (2011) that China-Africa trade poses a negative and insignificant effect on African productivity and economic growth.

In conclusion, the above-mentioned literature review shows that the effect of China-Africa trade on Africa’s economic performance is not uniformly positive. As a result, the empirical studies’ findings are inconclusive, and further research into its effect on economic growth is warranted.

China OFDI in Africa and Economic Growth

It is generally argued that FDI is an essential tool for rapidly evolving international economic integration and ties between countries (Acquah & Ibrahim, 2020). According to Fosfuri et al. (2001), FDI excites the output of domestic companies through labor mobility mechanisms. The endogenous growth theory proposed that FDI subsidizes economic growth in a scarce capital economy by increasing the income level and the efficiency of the physical investment (Grossman & Helpman, 1994; Lucas, 1988; Romer, 1986, 1990). Thus, FDI provides short-term capital through the transfer of technologies, managerial and marketing skills that lead to economic growth, the creation of jobs, and the enhancement of skills.

Several empirical studies on the effect of FDI on economic growth have been conducted following the endogenous growth theory (Acquah & Ibrahim, 2020; Bekere & Bersisa, 2018; Opoku et al., 2019). More precisely, studies on the effect of Chinese OFDI on Africa’s economic growth have strewn muddle and remain questionable. For instance, Donou-Adonsou and Lim (2018) analyzed the importance of China’s investment in Africa’s development. They realized that China’s OFDI contributes to income in the region. Similarly, Doku et al. (2017) observed that the growing Chinese OFDI to Africa has significantly increased the economic growth of African countries. Whalley and Weisbrod (2012) found that China’s OFDI to Africa countries contributes intensely to GDP growth in most African countries while examining the contribution of Chinese FDI to Africa’s pre-crisis growth for thirteen (13) Sub-Saharan African nations from 1990 to 2008. Lu and Liu (2018) argued that China’s manufacturing OFDI opens up new avenues for Africa to address structural manufacturing issues. Research by Khodeir (2016) similarly justifies that Chinese investment has a positive effect on the employment rate in African countries. Additionally, Negash et al. (2020) find that Chinese companies to be more productive than domestic companies in Ethiopia. The authors also stated that Chinese companies had created positive spillover effects of productivity for domestic companies that can support the sustainable development of the country. (Zhang, 2021) provided clear evidence that Chinese investments in Africa improve the host country’s capacity to absorb and use foreign capital.

A growing body of evidence (Elu & Price, 2010; Zhang et al., 2014), however, shows that Chinese OFDI to Africa may not always pose a positive effect on the GDP growth of Africa. Shen (2013), also realized that private Chinese FDI has a negative influence on technology transfer and varied effects on domestic industries in Africa countries. Busse et al. (2016) and Miao, Lang et al. (2020) argue that the Chinese OFDI to Africa countries, which continues to be fueled by China’s growing economy, does not correspond to the continent’s economic growth. Moreover, in a recent study, Megbowon et al. (2019) examined the effect of China’s OFDI on the industrialization of Sub-Saharan Africa. The authors noted that China’s OFDI is not enough to improve industrialization in Sub-Saharan Africa countries.

Based on the above-mentioned literature review, it is clear that further empirical research into the link between China’s OFDI and Africa’s economic growth is warranted. Furthermore, to the best of the authors’ knowledge, no study has yet examined the economic effect of China-Africa trade and China OFDI taking into account both the panel and country income classifications. Hence, this study fills that void.

Model Specification and Data

Theoretical Model

The main purpose of this current study is to examine the relationship between China-Africa trade, China OFDI, and the economic growth of African countries. Following existing literature (Hou et al., 2021; Zhang, 2021) on trade, OFDI, and economic growth, we employ the neoclassical Solow growth model, which is expressed in a function of labor and capital stock as;

where

In a Cobb-Douglas production function framework, the Solow model in equation (1) is formulated as;

Specifically, the concept of economic growth is mostly reliant on the neoclassical growth function (Solow, 1956). Theoretically, the neoclassical growth model constantly consists of the only labor force and capital stock as a closed system within which goods are provided without trade openness and outward foreign direct investment. It is important to note that the total factor productivity factor (

This, therefore, implies that equation (2) can be extended as;

Where

To standardize the data measurements and as well improve upon results accuracy (Shahbaz, 2012), a natural logarithm is applied to linearize equation (4). Thus, the log-linear transform extended Cobb-Douglas function in terms of trade openness and outward foreign direct investment is expressed as;

with

where

Econometric Approaches

The importance of econometric methods that account for cross-sectional dependence and heterogeneity among slope coefficients has been emphasized in recent years (Durusu-Ciftci et al., 2017). This is especially significant because most traditional econometric panel techniques do not account for cross-sectional dependence. The results of techniques that do not account for cross-sectional dependence may be inaccurate. Also, in this study, the sample African countries used may display cross-sectional dependencies in their respective panels, given the geographical and socio-economic similarities between them. Therefore, in the first phase of the analytical procedure, the existence of cross-sectional reliance is examined by utilizing the Pesaran (2004) CD test. To detect whether slope coefficients are homogeneous or not, this current study employed the approach of M. Pesaran et al. (2008) (henceforth; P-Y) test, which is developed on the Swamy (1970) technique to estimate the delta tilde (

This empirical process in the second phase analyzed the integration properties of variables using Im, Pesaran, and Shin (Im et al., 2003), cross-sectional Im, Pesaran, and Shin (CIPS), and cross-sectional augmented dickey fuller (CADF) unit root test developed by Pesaran (2007). The above-mentioned unit root tests are used due to the presence of cross-sectional dependence and heterogeneity (See Tables 4 and 5). The cointegration relationship of the observed variables is confirmed precisely by using the Westerlund (2007) bootstrap panel cointegration technique, which is also robust in accounting for residual cross-section reliance issues in a panel series. The Westerlund cointegration test is predominantly relevant when error corrections are cross-sectionally dependent.

The study empirically estimates the long-run coefficients on the study explanatory variables once a long-run affiliation is confirmed based on a cointegration test. Considering the possible incidence of heterogeneity between slope coefficients and cross-sectional dependency problems, we used the Feasible Generalized Least Squares (FGLS) estimator by Fomby et al. (1984). The FGLS estimator takes cross-sectional dependency and heterogeneity across countries into account and enables the parameters of non-stationary variables to be examined (Bai et al., 2021). To help validate the outcomes from the FGLS estimator, we used the generalized method of moments (GMM) estimation approach. The GMM, on the other hand, is resilient in accounting for the variety of endogeneity. It gives reliable outcomes even the presence of endogeneity from diverse sources, such as dynamic endogeneity and unobserved heterogeneity (Egyir et al., 2020).

As the estimators mentioned above irrefutably offer significant inferences but are unable to reveal the direction of causal association amid the variables, the study took a step further to examine the causal relationship and direction among the variables using the Dumitrescu and Hurlin (2012) Granger causality approach (henceforth; D-H). The D-H approach is used as an alternative to conventional causality tests (e.g., VECM and pairwise granger causality tests) as it accounts for potential issues of residual cross-sectional connectedness and heterogeneity. This test also takes into consideration the linear heterogeneous panel model.

Variable Selection

The most commonly used measure of a country’s growth is the gross domestic product (GDP). This standard measure has been used by economists, researchers and is commonly debated in the public arena (Bekere & Bersisa, 2018). It shows how much the output of a nation has increased. Hence, following the recent works of (Miao, Lang et al., 2020; Miao, Yushi et al., 2020; Zhang, 2021), this current study proposes to reflect economic growth using Sub-Saharan Africa GDP per capita, an accurate measure that appears to be in line with previous studies.

Also, several empirical studies have been done to prove the assertion of a connection between trade, OFDI, and economic growth in developing countries (Ramzan et al., 2019; Sakyi & Egyir, 2017; Tahir et al., 2019). From a plethora of findings highlighted by (Habyarimana & Opoku, 2018; Hou et al., 2021; Miao, Lang et al., 2020) China-Africa trade and Chinese investment in Africa advance the transfer of new technologies and positively influences the economic growth of African countries. Conversely, other studies have confirmed that China’s OFDI to Africa increases productivity, employment, and economic growth in African countries (Acquah & Ibrahim, 2020; Bekere & Bersisa, 2018; Kalai & Zghidi, 2019; Opoku et al., 2019). Based on previous reviews, the primary study assumption is that China-Africa trade and Chinese OFDI to Africa contributes to the economic growth of African countries. Hence, the study includes China-Africa trade and Chinese OFDI to Africa as the main independent variables.

Further, it is widely accepted that building capital equipment on a sufficient scale to improve productivity is the main objective of economic growth (Egyir et al., 2020). Kong et al. (2020), Zhang et al. (2014), and Keho (2017) offered substantial evidence to support the assertion that gross fixed capital formation positively affects economic growth in African countries. Several studies also posit that the labor force contributes to the rise in productivity and economic growth (Ahmad & Khan, 2019; Devadas, 2017; Iamsiraroj, 2016). The Solow-Swan model relating to the Harrod-Domer model assumes that labor additionally plays a major role in a country’s output to capital. Regarding the basic Cobb-Douglas production function, productivity is determined by three basic elements: capital input, labor input, and technology level. Consistent with previous studies (Donou-Adonsou & Lim, 2018; Meyer & Sanusi, 2019) and the Cobb-Douglas production function, the study assumes that labor force and capital investment contribute to economic growth in the African regions. Hence, the study integrates labor force and gross fixed capital formation as additional variables to reduce the omission of variable biases.

Data Source

The study utilized annual panel data over the period 1999 to 2018 for 24 Sub-Saharan African countries. The sample of Sub-Saharan African countries and the income-level classifications used in this study are presented in Table 1. To examine the link amid China-Africa trade, China OFDI, and Africa economic growth, five variables (Trade, OFDI, labor force, gross fixed capital formation, and GDP per capita) are used relying on the Cobb-Douglas production function approach. Trade (measure as Sub-Saharan Africa import from China and China export to Sub-Saharan Africa), OFDI (measured as the stock of China’s outward foreign direct investment to Sub-Saharan Africa) data were sourced from United Nations Com Trade (UNCTAD). The GDP per capita, gross fixed capital formation, and labor force of Sub-Saharan Africa countries were extracted from World Development Indicators (WDI). Table 2 depicts variables used in the study and their respective sources.

Sample of Sub-Saharan Africa Countries and Income-Level Classifications based on World Development Indicators (WDI).

Definition of Utilized Variables.

Descriptive Statistics

A summary of the descriptive statistics for the variables, GDP, OFDI, trade, labor force, and gross fixed capital formation used in this study concerning the chosen period is shown in Table 3. The descriptive statistics are established on three African country classifications (upper middle income, low-middle income, and low-income economies) and the entire selected African countries from 2000 to 2018. Considering the whole panel of selected African countries, it can be realized that trade is the variable of interest with the highest standard deviation of (3.316). Gross fixed capital formation recorded the highest mean (21.861), followed by trade (19.498), the labor force (15.423), and economic growth (7.110), whereas China’s OFDI has the lowest mean at 3.413. This shows that African nations commit a higher percentage of gross domestic product (GDP) to investment. The governments in Africa are encouraged to provide a significant amount of capital investment to improve the economy.

Descriptive Statistics.

The results from descriptive statistics (Table 3) also outlined that upper-middle-income countries are the highest economy with a mean of (8.982) for GDP, followed by low middle-income economies (7.208) and low-income economies (6.251). Regarding China-Africa trade, upper-middle-income countries again recorded the highest mean value of (19.944), whiles low middle-income economies have the lowest (18.950). In terms of Chinese OFDI, upper-middle-income countries have a preeminent investment (3.745), followed by low-middle income (3.735) and low-income economies (2.958). This shows that China-Africa trade and Chinese investment are essential in African countries. African governments are recommended to expand their economic cooperation with China and encourage more Chinese investment to boost the economy.

Empirical Results and Discussions

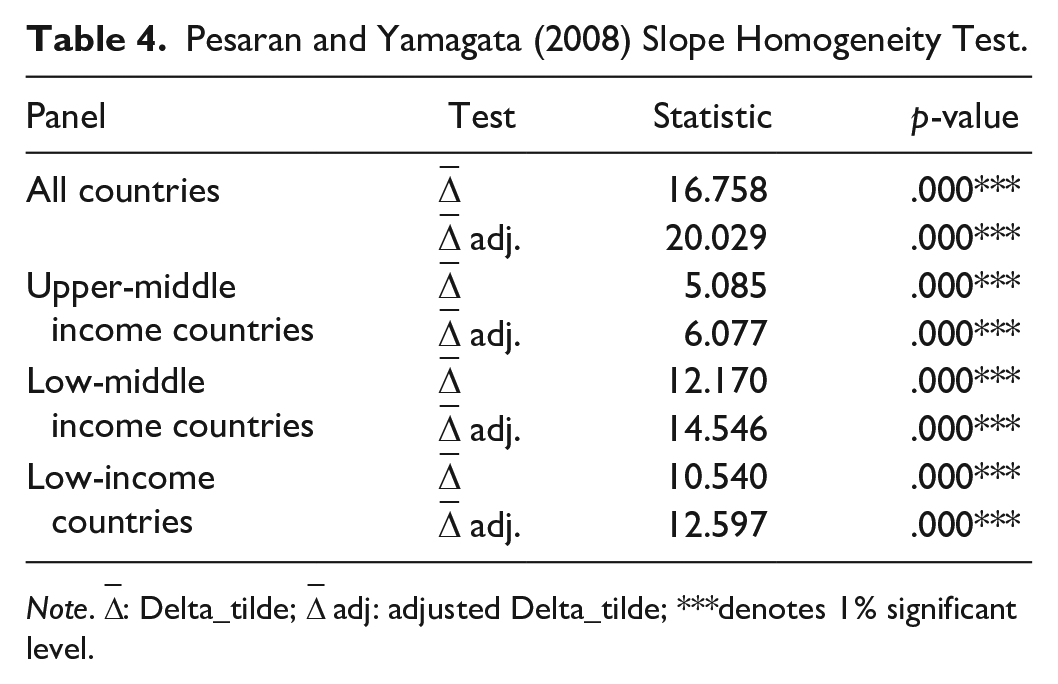

Homogeneity Test Results

Table 4 outlines the findings on the homogeneity test. Considering outcomes from the delta tilde (

Pesaran and Yamagata (2008) Slope Homogeneity Test.

Note.

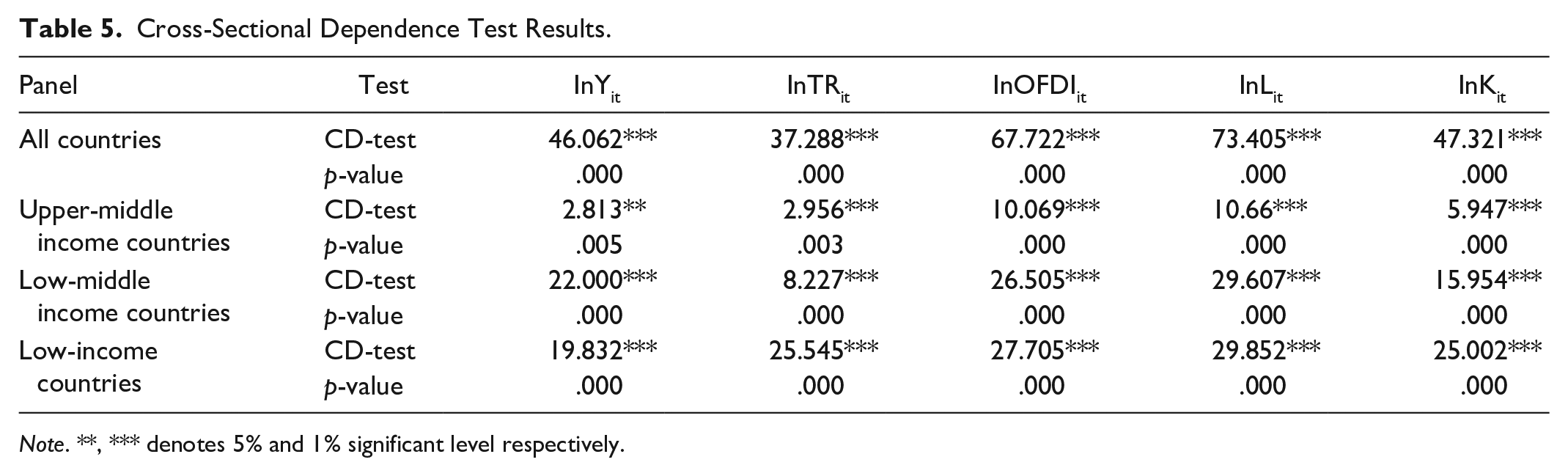

Cross-Sectional Dependence Test Results

The results of cross-sectional reliance tests are presented in Table 5. Relying on the cross-sectional reliance results which include CD-test statistics with their respective probability values, we intensely reject the null hypothesis of cross-sectional independence in all panels for the study variables respectively. This, therefore, indicates that there exist issues of residual cross-sectional connectedness within the employed panel data. From the economic perspective, the presence of cross-sectional dependence within the panel data shows that a shock in any of the series within the Africa panel can spread to the other member states within the same panel due to close economic relations between different cross-sections. Econometrically, the fact that issues of both heterogeneity and residual cross-sectional correlations are evidenced calls for the use of second-generation panel data approaches to obtain accurate and reliable results. Thus, using only conventional unit root tests and cointegration approaches will give bias outcomes.

Cross-Sectional Dependence Test Results.

Note. **, *** denotes 5% and 1% significant level respectively.

Panel Unit Root Test Results

Taking into account the presence of cross-sectional reliance and slope heterogeneity, the study further examined stationarity of the variables within each panel using Im et al. (2003) (IPS), cross-sectional Im, Pesaran, and Shin (CIPS) and cross-sectional augmented dickey fuller-(CADF) panel unit root tests. Econometrically, using stationary variables avoids generating spurious statistical results. Table 6 outlines the unit root results based on the aforesaid panel unit root tests correspondingly. Results from the panel unit root tests show that all the variables are non-stationary in their levels but become stationary at the first difference, indicating that all observed variables are integrated at the same order I (1).

Panel Unit Root Test Results.

Note. Im, Pesaran, and Shin-(IPS); cross-sectional Im, Pesaran, and Shin-(CIPS); cross-sectional augmented dickey fuller-(CADF); *, **, *** denotes 10%, 5%, and 1%, respectively.

Westerlund Panel Cointegration Test Results

After confirming the presence of cross-sectional dependency and stationarity, we utilized Westerlund (2007) bootstrap panel cointegration technique, which is efficient to heterogeneity and residual cross-sectional connectedness to assess the cointegration of the variables. Table 7 presents the results of the cointegration test. Relying on the robust probability values, it is strongly evidenced that the null proposition of non-cointegration is rejected for (Gt, Ga ) and (Pt, Pa) test values at a 1% 5%, and 10% significant level respectively. Generally, the bootstrapped p-values (robust p-values) show greater proof of co-integration among the utilized variables. Nevertheless, the existence of a long-run relationship between trade, OFDI, labor force, gross fixed capital, and economic growth is confirmed.

Westerlund (2007) Cointegration Test Results.

Note. *, **, *** denotes 10%, 5%, and 1%, respectively.

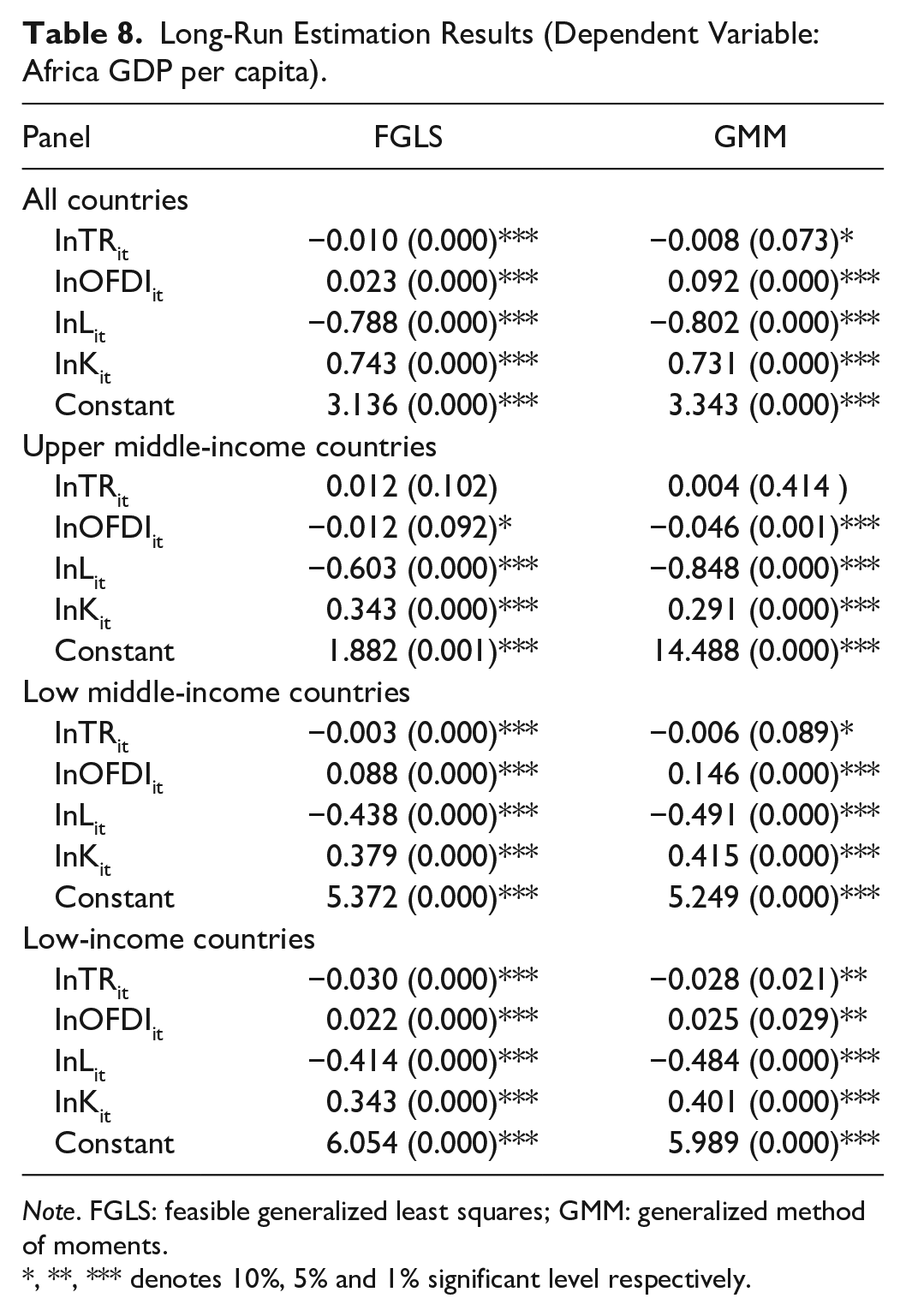

Long-Run Estimation Results

Our study examined the long-term effect of China-Africa trade and China OFDI (variable of interest) together with the labor force, gross fixed capital formation on economic growth, exploring the FGLS approach. Findings of the long-run estimation based on the aggregated panel together with the upper-middle-income, low-middle income, and low-income of Sub-Saharan African countries are presented in Table 8.

Long-Run Estimation Results (Dependent Variable: Africa GDP per capita).

Note. FGLS: feasible generalized least squares; GMM: generalized method of moments.

**, *** denotes 10%, 5% and 1% significant level respectively.

Specifically, the estimated coefficients of trade are negative and significant for the aggregated panel together with the low-middle income and low-income countries. These results mean that a 1% increase in China-Africa trade causes a decrease in the economic growth of Sub-Saharan Africa, particularly in the low-middle income and low-income economies by 0.010%, 0.003%, and 0.030%, respectively. Likewise, Hanusch (2012) and Yin and Vaschetto (2011), show that China-Africa trade poses a negative effect on African productivity and economic growth. This is plausible as most African nations face inadequate efficient production (Miao, Lang et al., 2020). In comparison to the import of products from China, African countries’ trade is dominated by the export of primary commodities, which command relatively low quantity and prices (Were, 2015), thus, having a negative spillover effect on the economic growth of Sub-Sharan African countries. Also, challenges, such as lack of human and physical capital, ineffective institutions, and poor infrastructure contributes to the low competitiveness of Africa exports in global markets, limiting their capacity to gain the benefit of trade ties with China. For many African countries, capacity and poor economic diversification will not improve dramatically, indicating that trade with China is not a long-run source of economic growth. It is, therefore, important for policymakers to consider this aspect when formulating policies on Sino-Africa trade and strive to ensure that accurate trade policy can be maximized. Thus, the government’s capacity to implement accurate Sino-Africa trade policies is essential for African economies to realized trade benefits and boost economic growth. These findings are inconsistent with the results of (Hou et al., 2021; Kummer-Noormamode, 2014; Miao, Lang et al., 2020) who disclosed that for many African economies, the positive effects of trading with China on economic growth outweigh the negative effect.

Further, the aggregated panel, together with low-middle-income and low-income Saharan African countries, are characterized by a positive and statistically significant long-run effect from OFDI to economic growth with coefficients of 0.023, 0.088, and 0.022 respectively, while a negative and significant effect coefficient of 0.012 is evident in upper-middle-income Saharan African countries. These findings, in line with the study of (Doku et al., 2017; Donou-Adonsou & Lim, 2018; Nabil Khodeir, 2016) portray that China’s OFDI is more beneficial in the low-middle income and low-income Sub-Saharan African countries than the upper-middle-income economies. Recently, many Chinese industries have been set up in low-income countries and are undertaking projects in the various sectors of Africa. These Chinese firms subsequently create jobs, contribute to skill development, and use technologies that are more suitable for domestic industries which improve the economic growth of Sub-Saharan African countries to some extent (Habyarimana & Opoku, 2018; Lisimba, 2020). Thus, the win-win situation of Chinese investments in African countries can be attained particularly in low-middle income and low-income African countries. Policymakers within Africa need to implement policies that are conducive to attracting more Chinese investors as suggested by (Zhang, 2021) to boost economic growth. The adverse effect of OFDI on economic growth in upper-middle-income Sub-Saharan African countries coherent with (Busse et al., 2016; Megbowon et al., 2019; Miao, Lang et al., 2020) could be related to high competition created by Chinese firms which make domestic firms to inexpertly shut down, thus, yielding a reduction in GDP per capita. Also as domestic currency is the exchange for foreign currency, a serious capital drain will be inflicted on the host country’s economy leading to a drastic economic situation.

The labor force coefficient is also significantly and negatively connected with economic growth for the aggregated panel together with upper-middle-income, low-middle income, and low-income countries. This result means that a 1% increase in the labor force substantially reduces GDP by 0.788%, 0.603%, 0.438%, and 0.414%, respectively. While these findings are inconsistent with the studies of (Novignon et al., 2015; Zhang et al., 2014) who evidenced a positive significant impact of the labor force on economic growth in African countries, it could be related to the fact that employment structures in Africa are marked by a lack of higher-wage jobs, a reliance on low income and low-skill labors with the relatively high unemployment rate. Thus, skilled laborers without adequate physical capital and the accumulation of physical capital without skilled operators lead to diminishing returns on output (Devadas, 2017). Further, productivity level reduces when a country increases the proportion of unskilled laborers thereby resulting in reduced GDP growth in Sub-Saharan Africa. These findings, thus, reflect that Sub-Saharan Africa’s economic growth is determined sustainably by technological factors, such as new equipment, process, and new technology, instead of the labor force. Hence, the notion of (Solow, 1956, 1957) model has been established that labor inputted in production would have diminishing returns on output with a certain stage of technology. The results also confirm the assumption of Belloumi (2014), that a surge in Africa’s low-skilled laborers can negatively affect economic growth. This is, therefore, a wake-up call for Sub-Saharan Africa countries to give special attention to the labor sectors and implement economic policies that encourage growth in sectors to realize the benefits of the labor force on GDP growth.

Moreover, the coefficient of gross fixed capital formation at the aggregated panel level together with the upper middle income, low-middle income, and low-income Sub-Saharan African countries are positively and significantly linked to GDP. Thus, a percentage increase in gross fixed capital formation tends to increase economic growth by 0.743%, 1.882%, 0.379%, and 0.343%, respectively. The result also implies that capital formation contributes to economic growth, thus, through technological advancement and large-scale production in Sub-Saharan African countries (Phale et al., 2021). These findings confirm the earlier studies which showed that a higher level of capital investment is related to better economic growth among African countries (Keho, 2017; Kong et al., 2020; Uneze, 2013). Most African countries recently have been investing heavily in more fixed assets such construction of schools, roads, hospitals, and railways, which allows for a spillover impact of increased GDP growth and development. Also, as capital formation leads to adequate extraction of natural resources and the growth of various industries, rates of income increase, allowing individuals’ multiple needs to be met (Bekere & Bersisa, 2018). Thus, it fosters Sub-Saharan African citizens’ economic well-being and serves as a measure of economic growth. Therefore, any improvement in gross capital formation in the future will have a significant influence on the economic performance of Sub-Saharan African countries. Our study, thus, advocates for more capital formation in African countries, which would lead to higher economic growth.

The results of FGLS are reaffirmed by using the generalized method of moments (GMM) approach. The results of GMM presented in Table 8 are similar to FGLS results in terms of the significance of the coefficient. This shows that our results are accurate.

Panel Causality Results

To confirm the direction of the causality amid each explanatory variable and economic growth, the study utilized the conventional D-H Granger Causality test. To make the output of the results based on the causality test more ostensible, a summary of the D-H Panel Granger causality results is shown in Figure 1, together with Table 9.

Summary of the D-H panel Granger causality results.

Results from Heterogeneous Panel Granger Causality Test.

Note. → Depicts long-run uni-directional Granger causality and ↔ denotes a long-run bidirectional Granger causality.

**, *** denotes 10%, 5% and 1% significant level respectively.

With regard to causal interactions amid GDP (Y) and each explanatory variable which is of greater importance in the study, the following results were found and deliberated as follows.

At the panel level, the presence of a unidirectional Granger causality is observed from trade to GDP, trade to gross fixed capital formation, and labor force to gross fixed capital formation. This, therefore, shows that booming China-Africa trade would lead to a considerable increase in the economic growth of African countries. More particularly, this indicates that African countries benefit from importing manufactured goods from China and reducing expenses by consuming low-cost Chinese products. Manufacturers in Africa could take advantage of China’s low-cost inputs in the production process, consequently increasing economic growth (Busse et al., 2016). Likewise, the D-H approach confirms a long-run bidirectional Granger causality between OFDI and GDP, labor force and GDP, gross fixed capital formation, and GDP. It can be inferred that Chinese investment in African countries plays a part in the creation of jobs, development of infrastructure, improvement in technology, skills, and, consequently, economic growth in African economies. The results also presupposed that the GDP of African countries promotes new capital formation, increases employment rate, and vice versa. These findings, thus, confirm the earlier studies of (Habyarimana & Opoku, 2018; Iamsiraroj, 2016; Negash et al., 2020; Zhang, 2021). However, these findings are inconsistent with the results of (Miao, Lang et al., 2020; Shen, 2013).

For the upper-middle-income African countries, the study witnessed that trade, OFDI, labor force, and gross fixed capital Granger cause GDP growth. These findings suggest the role China-Africa trade and Chinese investment plays in transforming upper-middle-income African economies. The upper-middle-income African countries show the largest divergence across a number of features, and any strategy to fix these variables dramatically alters GDP. Additionally, we observed a long-run Granger causality from GDP to OFDI, trade to the labor force, trade to gross fixed capital formation, and gross fixed capital formation to OFDI. Our findings further confirmed the empirical conclusions that economic growth plays an invaluable role in promoting Chinese investment in African countries (Shan et al., 2018). The study also shows that the labor force Granger causes the gross fixed capital formation and vice versa in the upper-middle-income economies. That is, increased labor force and gross fixed capital formation have a predictive influence over each other. Analogous findings are established from (Manwa et al., 2019; Meyer & Sanusi, 2019) studies in upper-middle-income African countries.

Similar to the upper-middle-income African countries, we found that trade Granger stimulates GDP, OFDI labor force, and gross fixed capital formation in the low middle-income African economies. This finding implies that trade exchanges between China and African countries, particularly the low-middle-income economies, improve GDP (Hou et al., 2021). These findings confirm the empirical assumption that Africa’s GDP will be gradually increased with the increasing China-Africa trade and that Chinese investment in African countries is more likely to stimulate economic growth (Doku et al., 2017; Drummond & Liu, 2015; Kummer-Noormamode, 2014). We also observed a two-way causal link between OFDI and GDP, labor force and GDP, gross fixed capital formation and GDP, gross fixed capital formation and OFDI, gross fixed capital formation, and labor force. This finding can be attributed to the fact that upper-middle-income countries in Africa have a significant market size and economy that serves as a driving factor for Chinese investment (Mourao, 2018). The findings also align with economic literature, which asserts that labor force and gross fixed capital formation can complement economic growth (Boamah et al., 2018; Keho, 2017; Zhang et al., 2014).

With the low-income African economies, we evidenced a one-way Granger causality from trade to GDP, labor force to OFDI, gross fixed capital formation to OFDI, and gross fixed capital formation to the labor force. This reaffirms that Sino-Africa trade ample GDP and Chinese investment increases employment rate with better economic fundamentals in many low-income African countries. Our study, thus, strongly supports the findings of (Habyarimana & Opoku, 2018; He, 2013). Moreover, a two-way causality is found between OFDI and GDP, OFDI and trade, labor force and trade, gross fixed capital formation and trade, gross fixed capital formation, and labor force. This endorses that Chinese investment in Africa promotes GDP, trade, and vice versa in many low-income African countries. The findings also reflected a growing China-Africa trade trend toward integration of employment rate and capital investment.

Conclusion and Policy Recommendations

China-Africa trade and Chinese investment in African countries have increased enormously in recent years. China’s growing involvement in the African regions, however, continues to excite questions about the impact of its involvement in the continent. Studies on China’s engagement with African countries have relied on grandiloquence rather than empirical analysis. This study empirically examines the relationship between China-Africa trade, China OFDI, and African countries’ economic growth based on income classifications (upper-middle-income, low-middle income, and low income) along with the whole panel of selected Sub-Saharan African countries from 1999 to 2018 using the FGLS, GMM estimator, and D-H heterogeneous panel causality approach. To avoid omitted variables bias, the study included additional explanatory variables such as labor force and gross fixed capital formation. The main conclusions resulting from the application of the recently developed econometric approaches are as follows;

(i) The findings of the cross-sectional dependency and slope heterogeneity test confirmed the presence of connection amid cross-sections and slope heterogeneity across the African countries.

(ii) The unit root tests with IPS, CIPS, and CADF revealed all the variables as non-stationary at levels but became stationary after first differencing. Thus, all the variables as being integrated into the first order I(1).

(iii) The Westerlund-Edgerton panel cointegration test disclosed that economic growth, trade, OFDI, labor force, and gross fixed formation are integrated, which ratifies the long-run connection between the utilized variables.

(iv) In confirming the long relationship among the variables, the FGLS estimator results show that China-Africa trade has a negative but a positive impact of China OFDI on SSA economic growth at the aggregated panel. When the study assessed the estimator for each income level, the trade and labor force negatively impacted GDP in the low middle, low-income economies, and insignificant positive effect in upper-middle-income economies. It is essential to infer that a higher Sino-Africa trade and labor force level reduces economic growth in SSA countries. Moreover, the long-run estimate shows that China’s OFDI and gross fixed capital formation positively and significantly influence economic growth in SSA countries, upper-middle. The robustness test portrayed consistent outcomes through the GMM estimation approach.

(v) In the context of the causal relationship among the utilized variables, unidirectional causalities were witnessed between China-Africa trade and economic growth at the whole panel and the income-level classifications. Based on the findings of our study, some policies have been proposed as follows:

(i) Primarily, the study findings show that trade and the labor force have a negative effect on economic growth. This shows a detrimental effect of China-Africa trade on GDP growth, particularly for low-middle and low-income Sub-Saharan African economies. Hence, to address the adverse impact and substantially benefit from trade ties with China, we recommend policymakers in African countries improve upon their trade policies and adjust potential trade agreements. Also, given the inexorable technological gap amid trading partner countries, policymakers are recommended to implement effective trade policies that take into account not only the potential learning opportunities and knowledge offered by their trade partners but also the industrial framework, as production capability.

(ii) African Continental Free Trade Area (AfCFTA) authorities should endeavor to consider the China-Africa trade in the formulation of their policies. In the face of the Belt and Road Initiative, both China and Africa policymakers must endeavor to introduce more favorable trade measures to promote economic growth and development in Africa.

(iii) Moreover, the study evidenced that Chinese investment in Africa positively contributes to the GDP growth of African countries with low-middle income and low income, whiles it adversely impacts the GDP growth of upper-middle-income countries. To improve economic growth, African governments particularly those in the low-middle income and low-income African countries must prioritize Chinese investment in their plans, strategies and encourage more Chinese investments in Africa. Additionally, African policymakers should formulate accurate and innovative investment policies in upper-middle-income African countries to improve the adverse effect and reap the benefits of growing Chinese investments.

(iv) To improve the unfavorable impact of the labor force on economic growth, this study advocate for policymakers in the Africa continent to enact economic policies that will boost growth in sectors that are labor-intensive and can contribute significantly to employment and economic growth, such as manufacturing companies, retail, technology, research, and development. Likewise, policymakers should develop policies that encourage labor force participation in economic activities and invest in education and human capital development. Also, a policy suggestion for enhanced growth in Africa will be to reform Africa’s labor sectors to ensure increased productivity.

Limitations and Future Research Directions

While as many observations as possible have been attempted and recent advanced econometric methods have also been applied, this current study still has some limitations as follows:

(i) This study was limited to 24 Sub-Saharan Africa countries and used trade as a proxy for China-Africa trade. Therefore, future research can expand our present study by using more developing countries and disaggregating trade into export and import to look at the effect of each on economic growth.

(ii) In reducing the omission of variable biases, our study ignored financial development as a role in promoting economic growth. Some research findings suggest financial development plays a crucial role in economic development. This means that the efficient financial system is beneficial for economic growth since the advent of advanced financial derivatives supposedly allowed for an accurate transfer of risk to those who could best bear it. Hence, future studies can incorporate financial development as additional variables in the economic model.

(iii) The study found a negative effect of the labor force on Sub-Saharan Africa’s economic growth. Future studies should focus on analyzing how institutional quality and technology can leverage the labor force on GDP growth while mitigating potentially adverse effects.

(iv) Additionally, this study centered on the case of the aggregate panel and income levels. However, if country specifics are taken into account along with the aggregated panel, such a study would be valuable in the future as it is possible to obtain varied results to make the research more remarkable.

Footnotes

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: The authors appreciate the financial support from the National statistical science research project (No. 2014566); Qing Lan Project of Jiangsu Province, and the Key Members of the Outstanding Young Teacher Training Project of Jiangsu University. We also acknowledge the extensive contributions of Dr. Henry Asante Antwi and Dr. Isaac Adjei Mensah.