Abstract

Expanding and stabilizing the middle class is critical for reducing income disparities, promoting social equality, and fostering sustainable economic growth. However, the middle class faces considerable vulnerability, which challenges achieving these goals. Digital inclusive finance, as a transformative financial innovation, offers potential solutions to mitigate this vulnerability, yet its role remains insufficiently explored in the existing literature. This study aims to examine the impact of digital inclusive finance on reducing middle-class vulnerability, with a specific focus on its mechanisms and inclusiveness. Using data from the China Family Panel Studies, the analysis employs the Vulnerability as Expected Poverty (VEP) model to quantify middle-class vulnerability and explore the protective effects of digital inclusive finance. The findings demonstrate that digital inclusive finance significantly reduces middle-class vulnerability, a result validated through robustness checks. Mechanism analysis reveals that digital inclusive finance enhances entrepreneurial activities, financial participation, and employment opportunities, collectively contributing to its protective effects. Additionally, the study highlights the inclusive nature of digital finance, as it helps bridge the ‘digital divide’ across regions, urban and rural areas, education levels, and age groups. The findings suggest that policymakers and financial institutions should prioritize expanding access to digital inclusive finance by improving digital infrastructure and financial literacy programs. Targeted initiatives, such as subsidizing digital tools or incentivizing financial innovation, could effectively reduce middle-class vulnerability.

Keywords

Introduction

The middle class is generally defined as the social group between society’s upper and lower tiers. It is often considered the backbone of the market economy and democratic systems in developed nations (Birdsall et al., 2000). The middle class promotes social stability, reduces poverty, and supports inclusive development (Shaban, 2021). As a cornerstone of the ‘olive-shaped’ social structure, it is crucial in advancing economic and social progress. Research shows that a strong middle class enhances income mobility (Boushey & Hersh, 2012) and drives growth through spending patterns (P. Li, 2017; Brueckner et al., 2018). By boosting consumer demand, providing essential skills to the labor market, and supporting the growth of small and medium-sized enterprises, the middle class significantly contributes to economic development (Boushey & Hersh, 2012; Hsieh et al., 2019).

Although numerous scholars have conducted extensive research on the middle class, their focus has primarily been defining and measuring the middle class in developed countries such as Europe and North America (Darity et al., 2021; Haller et al., 2022). In contrast, studies on the middle class in China remain relatively limited. In China and Western countries, the middle class generally refers to groups positioned in the middle of the socioeconomic hierarchy. Typically, the concept and connotation of the middle class can be categorized into two dimensions: sociological and economic. The concept of the middle class first emerged in Western sociological studies and is considered relatively broad. It encompasses income standards, occupational status, educational attainment, and class identity (Boushey & Hersh, 2012). However, in China, the middle class is often defined and categorized based solely on income, reflecting its role as an economic concept closely tied to income distribution (C. Chen & Qin, 2014). China has significantly contributed to global economic development as one of the fastest-growing economies. However, the proportion of the middle class in China remains behind that of Western countries (X. Chen & Li, 2023). Therefore, examining the formation of the middle class in the context of China offers valuable insights for understanding the rise of the middle class in other developing countries.

Additionally, existing research on pathways to expand the middle class is limited, with only a handful of studies addressing the influence of education, occupation, urbanization, industrialization, and economic globalization (Bonnefond et al., 2015; C. Chen & Qin, 2014; Kharas, 2010). Generally, the middle class grows through two primary avenues: upward mobility from the lower-income group and reducing the vulnerability of those already in the middle class. While there has been considerable focus on the dynamics of upward mobility, particularly about education and employment (Nissanov, 2017), research on mitigating the vulnerability of the middle class is sparse. The term ‘middle-class vulnerability’ refers to the susceptibility of middle-class households to economic hardship due to income fluctuations, job instability, and limited access to social security, which causes social class to fall. This vulnerability stems from their position between stable middle-class and low-income groups (Figure 1), making them particularly sensitive to economic shocks, unexpected expenses, or health crises. Ravallion (2010) notes that despite rapid growth, the middle class in developing countries remains highly vulnerable, which presents a significant obstacle to its expansion. Foster and Wolfson (2010), using data from the United States and Canada, observed a trend of income polarization leading to a shrinking middle class. Therefore, understanding the factors that affect the vulnerability of the middle class is crucial for ensuring its sustainable growth.

Social structure maps and middle-class vulnerability.

However, research on the relationship between the development of digital inclusive finance and the vulnerability of the middle class remains scarce. China is accelerating its digital transformation and the development of a low-carbon economy (Di et al., 2024; Sun et al., 2024), while traditional financial services fall short of meeting residents’ financial needs. The rapid development of digital inclusive finance has created new opportunities for increasing household income (F. Wu et al., 2023; J. Wu & Wu, 2023). The middle class primarily relies on wage income and has limited alternative income sources while facing an unstable employment environment, heightening its vulnerability (Bonnefond et al., 2015). Digital inclusive finance, driven by Internet technology, facilitates economic activities, financial innovation (Hussain & Papastathopoulos, 2022; K. Wu et al., 2022), and improve enterprise productivity (J. Wang et al., 2025). It enhances the inclusivity of financial services by improving access for populations underserved by traditional financial institutions, easing financing constraints, and improving the entrepreneurial environment (X. Tang et al., 2022; J. Wu & Wu, 2023). Moreover, digital inclusive finance leverages platforms such as the Internet and big data to reduce transaction costs and increase convenience for household financial participation (F. Wu et al., 2023; G. Xu et al., 2024). These developments suggest that digital inclusive finance could offer a new pathway for mitigating the vulnerability of the middle class.

Both theory and practice suggest that digital inclusive finance facilitates the expansion of financial services and promotes income growth. Investigating whether digital inclusive finance can mitigate middle-class vulnerability offers valuable insights into China’s ‘common prosperity’ strategy and poverty alleviation efforts in other developing countries. In recent years, China’s middle class has experienced rapid growth (Yang et al., 2024). However, high levels of vulnerability and regional development imbalances persist (X. Chen & Li, 2023). Few studies have attempted to measure middle-class vulnerability, and existing research has not determined whether digital inclusive finance can alleviate middle-class vulnerability. Clarifying this relationship could inform the development of targeted policies to strengthen and expand the middle class more effectively.

Therefore, building on previous research, we analyze the role of digital inclusive finance in mitigating the vulnerability of the middle class and make three key contributions. First, we apply the Vulnerability as Expected Poverty (VEP) method to identify the vulnerable middle class, thereby expanding existing studies on measuring middle-class vulnerability. Second, we incorporate digital inclusive finance and middle-class vulnerability into a unified research framework to examine how digital inclusive finance impacts middle-class vulnerability. This approach offers insights into strategies for strengthening and expanding the middle class. Third, our findings reveal that digital inclusive finance alleviates middle-class vulnerability by fostering entrepreneurship, enhancing financial participation, and improving employment. These insights contribute to a deeper understanding of how to increase middle-class income and reduce vulnerability risks.

The remainder of this paper is structured as follows: The second part is literature review and mechanism analysis; the third part explains the data, variable design, and methods; the fourth part analyses and discusses the results; and the final section is the discussion and conclusion.

Literature Review

Middle Class

The middle class plays a crucial role in driving economic growth and promoting social consumption across nations (P. Li, 2017). Its expansion is instrumental in alleviating poverty, reducing income inequality, and enhancing social stability (Shaban, 2021). In China’s ongoing economic transition and pursuing a low-carbon economy (Di et al., 2023; Sun et al. 2024), strengthening and expanding the middle class is essential for social development and stability.

Research on the middle class primarily focuses on its definition and measurement standards (Darity et al., 2021; Haller et al., 2022). A more petite body of literature explores the role of economic growth and globalization in driving middle-class expansion (Ravallion, 2010). In China, Crabb (2010) found that education significantly contributes to forming the middle class and emphasized the need for educational policy reforms to support its development. Similarly, Dartanto et al. (2020), using survey data from Indonesia, identified investments in human and physical capital as critical drivers of middle-class growth. C. Chen and Qin (2014) attributed the rapid expansion of China’s middle class to urbanization and industrialization, highlighting the roles of occupation and education. However, the challenges and threats faced by the middle class during its growth process remain largely underexplored. In particular, there is a significant gap in micro-level studies examining how to expand the middle class, a critical issue for developing countries aiming to overcome the ‘middle-income trap.’

One effective approach to expanding the middle class is to reduce its vulnerability and solidify its economic position in society. As resident incomes rise in developing countries, the issue of middle-class vulnerability has increasingly garnered global attention. Recent evidence from Latin America and North America indicates the presence of a significantly vulnerable middle-class population that is highly susceptible to economic fluctuations, deteriorating social conditions, and resource scarcity (Bilan et al., 2020; Rougier et al., 2021). Developing countries, in particular, are more exposed to economic, social, and environmental challenges (Di, et al., 2024), such as natural disasters, shrinking consumption, political instability, and widening income inequality. These risks pose serious threats to both individual households and the global economy. From this perspective, addressing middle-class vulnerability should be a core component of government public services, especially in developing countries. However, the vulnerable middle class is often overlooked due to its ambiguous status of being ‘better off than some groups but worse off than others.’

Effects of Digital Inclusive Finance

Ozili (2018) defines digital inclusive finance as ‘the digital access and usage of financial services by individuals who are excluded from or have limited access to traditional financial services’. This innovation enhances the accessibility of financial services, offering more convenient and cost-effective options, particularly in underdeveloped and rural areas (Kouladoum et al., 2022). Since its emergence, digital inclusive finance has been extensively studied, with research indicating its positive effects on socioeconomic growth (Emara & El Said, 2021), consumer spending (J. Li et al., 2020), and income distribution (Zhao et al., 2022).

Scholars widely agree that digital inclusive finance significantly contributes to social and economic development. For example, Ozili (2018) argues that its widespread adoption improves financial inclusivity and stability, addressing the limitations of traditional financial services. Other researchers highlight its positive impact on high-quality business development (Lee et al., 2023), social sustainability (G. N. Tang et al., 2022), and household wealth accumulation (F. Wu et al., 2023). Zhao et al. (2022) further suggest that internet technology has expanded financial services to those with limited access, helping to alleviate financial exclusion in underserved regions. This expansion promotes greater financial service equality between urban and rural areas, allowing residents in impoverished regions to benefit from the digital dividends of inclusive finance (Mignamissi & Djijo T, 2021). As a result, digital inclusive finance plays a crucial role in narrowing regional and urban-rural disparities and reducing poverty rates.

While existing literature has explored the definition of the middle class and the factors influencing its formation, studies on middle-class vulnerability remain scarce. Moreover, most research on digital inclusive finance focuses on its role in promoting economic growth, emphasizing its impacts at the national and corporate levels. However, there is limited research on how digital inclusive finance affects the middle class, especially its potential to reduce middle-class vulnerability. To address this gap, this study utilizes data from the 2020 China Family Panel Studies (CFPS). We employ the VEP metric to measure middle-class vulnerability and explore the role of digital inclusive finance in alleviating the vulnerability of the middle class. We further examine how digital inclusive finance alleviates middle-class vulnerability through entrepreneurship, financial participation, and employment. Additionally, we conduct heterogeneity analysis and robustness tests to ensure the validity of our results.

Analysis of Digital Inclusive Finance Reducing the Vulnerability of Middle Class

This study will explore the mechanisms through which digital inclusive finance reduces middle-class vulnerability from three critical perspectives (Figure 2).

Theoretical framework.

Entrepreneurship Channel

Entrepreneurial income is a significant contributor to household wealth. F. Wu et al. (2023) note that income from entrepreneurship makes up a growing portion of household wealth and income, significantly influencing income growth. However, entrepreneurial decisions are often shaped by factors such as capital availability and financing constraints, with the latter being a critical barrier to entrepreneurship (Banna et al., 2021; G. N. Tang et al., 2022). Motivated by a balance between returns and costs, traditional financial institutions typically establish service outlets in economically developed areas, favoring individuals with financial means. This leads to severe financial exclusion and limited access to financing (K. Wu et al., 2022). Low-income households are often marginalized by the traditional financial system, with high information costs and financing constraints hindering their entrepreneurial activities and income growth (J. Wu & Wu, 2023).

The rise of digital inclusive finance, powered by the Internet and big data, effectively reduces the cost of financial services for institutions (Reddick et al., 2020). Digital inclusive finance also transcends the limitations of time and space, lowers entry barriers, improves financial accessibility, and helps potential entrepreneurs overcome financing constraints, thereby increasing the likelihood of entrepreneurship (X. Xu, 2020). As a result, the development of digital inclusive finance can reduce information costs, alleviate financing constraints, encourage middle-class households to engage in entrepreneurship, boost operating income, and ultimately reduce the vulnerability of the middle class.

Financial Participation Channel

Household financial participation is significantly influenced by factors such as financial literacy, accessibility, and transaction costs (Kewangan, 2021). For middle-class households facing vulnerability risks, participation in financial markets is often low due to high transaction costs and a lack of financial knowledge and skills. This exclusion from traditional financial services limits their ability to accumulate wealth (Huang et al., 2021; X. Wang et al., 2022). The development of digital inclusive finance promotes the integration of the Internet with educational resources, expanding access to financial knowledge and improving financial literacy (Tan & Li, 2022). This increased dissemination of financial knowledge enhances awareness and encourages greater participation in financial markets, overcoming the barriers posed by insufficient financial education (Hermansson et al., 2022). Moreover, digital inclusive finance reduces the limitations of traditional financial services, addressing information asymmetry and potential risks, thereby enabling broader access to financial services (Kass-Hanna et al., 2022; Luo et al., 2021). Improved accessibility to financial services creates more economic opportunities for low-income groups, helping to narrow income disparities (Aghion & Bolton, 1997). As a result, the growth of digital inclusive finance increases the financial market participation rate among middle-class households, enhances household income from assets, and significantly reduces the vulnerability of the middle class.

Employment Channel

The traditional labor market often suffers from information asymmetry, leading to labor supply and demand imbalances and lower household employment rates (Bauder, 2001; Gordon et al., 1973). High information costs hinder effective job matching. However, the digital age has transformed this landscape, with technological advancements spurring the gig economy’s growth. Digital inclusive finance integrates the Internet with financial services and is crucial in this development. It broadens access to financial services, providing essential financial support and secure payment systems for gig workers (Guo et al., 2020). This expansion helps the gig economy flourish by offering diverse new business models and employment opportunities, addressing overcapacity issues, and stimulating economic growth (Tan & Li, 2022). The gig economy fosters enhanced information and resource sharing with digital technology and platform support. The spread of digital inclusive finance improves financial service efficiency and extends e-commerce capabilities to more regions and communities (Lee et al., 2023). Consequently, it bolsters the gig economy, creates jobs, increases household incomes, and reduces the vulnerability of middle-class households.

Based on the above literature and theoretical discussion, we propose the following hypotheses.

H1: Digital inclusive finance can effectively reduce the vulnerability of the middle class.

H2: Digital inclusive finance alleviates middle-class vulnerability by promoting entrepreneurship, financial participation, and employment.

Data, Variables and Methods

Data Source

This study explores how digital inclusive finance affects the vulnerability of the middle class. We use data from the China Family Panel Studies (CFPS), a comprehensive national survey that covers economic activities, education, family dynamics, migration, and health. Initiated in 2010, the survey is conducted biennially. Since this paper employs the theory of poverty vulnerability to calculate the vulnerability of the middle class, the limitations of the calculation method necessitate the use of cross-sectional data. Moreover, the COVID-19 pandemic has had a profound impact on residents’ economic and daily lives, potentially exacerbating the vulnerability of the middle class. Therefore, we focus on the most recent cross-sectional data from CFPS2020 to meet our methodological needs. This allows us to assess the timely impact of digital inclusive finance. Our empirical analysis also incorporates data from the Digital Inclusive Finance Index, provided by Peking University’s Digital Inclusive Finance Research Center.

Dependent Variables

The theory of poverty vulnerability emphasizes the likelihood of households falling into poverty due to exposure to risks and their limited capacity to cope with shocks. Unlike static poverty measures, this theory adopts a forward-looking perspective, focusing on the probability of future poverty rather than current income levels. It highlights the role of factors such as income volatility, insufficient social protection, and inadequate financial resources in shaping vulnerability. By identifying the dynamics of poverty risk, this approach provides a more comprehensive framework for analyzing economic stability and designing targeted interventions to reduce vulnerability.

According to the methodology employed by X. Chen and Li (2023) to estimate the vulnerability risk of China’s middle class. We use the VEP indicator from Chaudhuri et al. (2002) to assess the vulnerability of middle-class households. According to this measure, a household is considered at risk if the probability of facing future vulnerability exceeds a set threshold. In line with this approach, we estimate the likelihood of middle-class households encountering future risks. We assume that the natural logarithm of per capita annual income follows a normal distribution. We apply a three-stage feasible generalized least squares (FGLS) method for this estimation. The model’s specific form is detailed below.

First, construct the income equation for middle-class households and use the residuals squared to estimate income volatility for the next period.

Where

Second, the fitted values obtained from Equation 1 will be utilized to determine weights for the FGLS estimation, thereby estimating the expected income volatility for middle-class households in the next period.

Where

Last, assuming that the nature logarithm of income follows a normal distribution, establish the threshold for middle-class vulnerability and calculate the level of middle-class vulnerability.

Where

To estimate the vulnerability of the middle class, we first define this group and set a vulnerability threshold. We use Kharas’s (2010) definition of the global middle class, with an income range of $10 to $100 per day (2011 PPP). The vulnerability threshold is commonly set at a 50% probability (Chaudhuri et al., 2002). Thus, if a middle-class household has more than a 50% chance of facing future risks, it is considered vulnerable and assigned a value of 1; otherwise, it receives a value of 0.

Independent Variables

The independent variable in this study is digital inclusive finance. We utilize comprehensive data from the Peking University Digital Finance Research Center and Ant Group Research Institute (Guo et al., 2020). The digital inclusive finance index is based on three dimensions: coverage breadth, usage depth, and degree of digitization. This index reflects digital finance’s population, geographical scope, and usage depth, making it an authoritative dataset (Lee et al., 2023). For our analysis, we selected provincial-level indices from 2020 and applied a logarithmic transformation to reduce deviations from data differences.

Mediator Variables

This study examines three mediating variables: household entrepreneurship, household financial participation, and household employment.

Household entrepreneurship is measured based on the classification by Sarkar et al. (2018). Using data from the CFPS 2020 surveys, we determine whether a family engaged in entrepreneurial activities by asking, ‘Does your family engage in individual private activities?’ A value of 1 is assigned if the family was involved in entrepreneurship in 2020, and 0 if it was not.

Household financial participation is assessed by asking, ‘Does your family hold government bonds, stocks, funds, or other financial products?’ If the household held at least one financial product in 2020, it is assigned a value of 1; otherwise, it is assigned a value of 0.

Household employment is measured following the approach by Zhou et al. (2020), based on the number of individuals in the household employed in non-agricultural sectors in 2020.

Control Variables

This study incorporates control variables at both the householder and household levels. Considering the significant role of the householder in household decision-making, the householder variables include gender, age, health status, and marital status. The household variables also encompass the average educational attainment, average age, number of government employees, healthy number of family members, and family size.

Variable Descriptive Statistics Analysis

This study performed a descriptive statistical analysis of various variables, with the specific results presented in Table 1. According to these findings, 21.1% of middle-class households in 2020 were vulnerable. This proportion is relatively high for a binary measure, suggesting that China’s middle class is particularly susceptible to vulnerability. Given China’s population, this percentage, when considered in absolute terms, underscores the significant exposure of the middle class to vulnerability risks.

Definition Descriptive Statistics (N = 5,569).

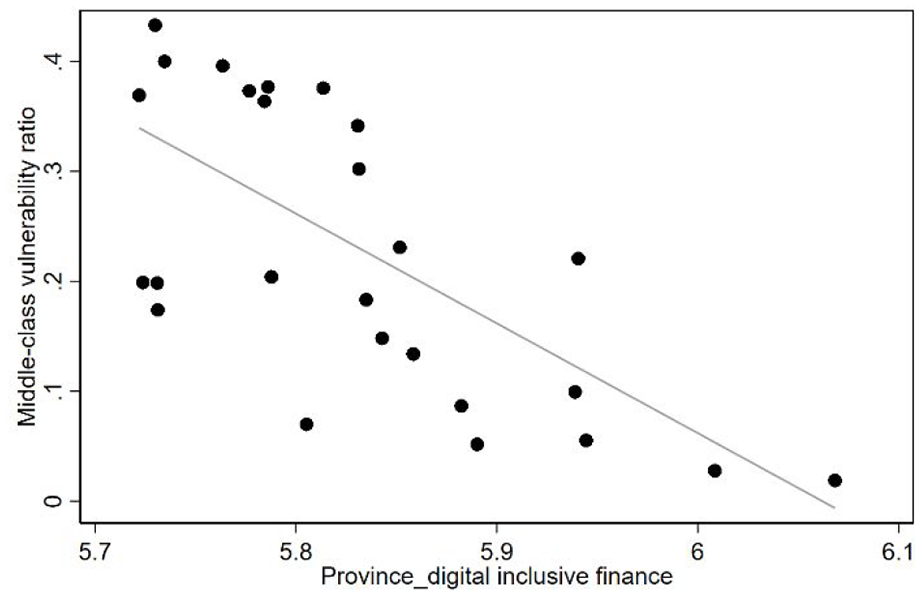

We also examine the relationship between the provincial digital inclusive finance index and middle-class vulnerability using a provincial-level index. Figure 3 presents this relationship for 2020, revealing a negative correlation between the digital inclusive finance index and middle-class vulnerability. This suggests that the development of digital inclusive finance may help reduce the vulnerability of middle-class households. However, this correlation alone does not fully establish whether digital inclusive finance directly reduces middle-class vulnerability. Therefore, further empirical analysis is necessary to validate the causal relationship.

Digital inclusive finance and middle-class vulnerability at province level.

Methods

Baseline Regression Model

Probit regression analysis is based on the concept of a normal distribution probability unit. In a Probit model, the dependent variable is binary, taking on only two possible values, typically represented as 0 and 1. The parameters of the Probit regression model generally are estimated using the maximum likelihood estimation (MLE) method. MLE identifies parameter values that maximize the observed data’s likelihood, ensuring the model’s best fit. As the dependent variable, examined in this study is a dichotomous variable coded as 0 and 1, a Probit regression model was used to analyze its influencing factors. Its analysis model is:

Where

Mechanism Test Model

To further explore how digital inclusive finance mitigates middle-class vulnerability, we adopt a mediating effect model following the approach of C. Wang et al. (2023). This model examines the roles of family entrepreneurship, household financial participation, and household employment in reducing middle-class vulnerability. The structure of the mediating effects model is outlined below:

Where

Results

Baseline Regression Results

Table 2 presents the regression results assessing the impact of digital inclusive finance on the vulnerability of the middle class. In column (1), where no control variables are applied, the regression coefficient for DIF is significantly negative, indicating a substantial reduction in middle-class vulnerability. Columns (2), (3), and (4) introduce controls for householder characteristics, household characteristics, and regional fixed effects, respectively, yet the regression coefficient for DIF remains consistently negative and significant at the 1% level. This suggests that digital inclusive finance plays a crucial role in reducing middle-class vulnerability and strengthening the stability of this socioeconomic group. Furthermore, as the development of digital inclusive finance advances, its mitigating effect on middle-class vulnerability intensifies. The H1 of this paper is verified.

Baseline Regression Results.

Note. Marginal effects rather than coefficients are reported; robust standard error is used and is listed in the brackets under the marginal effect coefficient.

p < .01. **p < .05. *p < .1.

In column (4) of Table 2, the education and government sector employment coefficients are significantly negative. Higher education levels in households help reduce middle-class vulnerability, highlighting education’s role in expanding this class (C. Chen & Qin, 2014). Additionally, more family members employed in the government sector decrease vulnerability due to higher salaries and job stability than non-government jobs. Moreover, having more healthy individuals in a household alleviates vulnerability by increasing employment opportunities and income (Nissanov, 2017). Conversely, the positive coefficient for household size suggests that larger families may face increased vulnerability due to more dependents, such as children and the elderly, which can strain resources.

Mechanism Test

Table 3 highlights how digital inclusive finance influences middle-class vulnerability. We omit Equation 5 results, aligning with column (4) of Table 2. In columns (1), (3), and (5), the regression coefficients of DIF are significantly positive, indicating that digital inclusive finance can facilitate the development of the middle class in terms of entrepreneurship, financial inclusion, and employment. In columns (2), (4), and (6), the regression coefficients of DIF, along with the mediator variables, are significantly negative. The absolute value of the regression coefficients of DIF is smaller than that in column (4) of Table 2. This suggests that digital inclusive finance reduces the vulnerability of middle-class households by promoting entrepreneurial activities, financial participation, and employment. Thus, it validates the H2 proposed in this paper.

Results of the Mechanism Test.

Note. Marginal effects rather than coefficients are reported; robust standard error is used and is listed in the brackets under the marginal effect coefficient.

p < .01. **p < .05.

Heterogeneity Analysis

Regional Differences

The research demonstrates that digital inclusive finance significantly reduces middle-class vulnerability. However, its impact varies due to differences in digital literacy, regional inequality, and urban-rural economic development. We analyzed regional heterogeneity by dividing the sample into Eastern and Central-West regions. Table 4 shows the regression results for these areas. In columns (1) and (2), the regression coefficient of DIF for the eastern region is −0.924, and for the central-western region is −1.072, passing the inter-group coefficient difference test (p value < .01), confirming a more substantial effect in the Central-West. The Central-West faces more severe financing constraints and has less access to traditional financial services (G. N. Tang et al., 2022). With lower urbanization rates and fewer financial outlets, the region benefits more from policies like ‘Digital China’ and ‘Smart Cities’, narrowing the digital divide. Thus, digital inclusive finance has a more pronounced impact in the Central-West.

Heterogeneity Analysis.

Note. Marginal effects rather than coefficients are reported; robust standard error is used and is listed in the brackets under the marginal effect coefficient; the p-value for the inter-group coefficient difference test was calculated using Fisher’s permutation test (Bootstrap 1,000 times). ***p < .01. **p < .05. *p < .1.

Urban-Rural Differences

Table 4 presents the regression results of digital inclusive finance on middle-class vulnerability in urban and rural areas. The coefficients in columns (3) and (4) show that digital inclusive finance reduces middle-class vulnerability in both regions. Specifically, the coefficient for urban areas is −0.886, while for rural areas, it is −1.620, passing the inter-group coefficient difference test (p value < .1), indicating a more substantial effect in rural regions. This more significant impact in rural areas may be due to the limited coverage and depth of traditional financial services compared to urban areas (Luo et al., 2021). Rural regions often lack credit records and face severe financing constraints. In contrast, urban households typically have adequate access to financial services and information for entrepreneurship and financial activities (J. Wu & Wu, 2023). Thus, digital inclusive finance more effectively alleviates financing constraints and reduces information costs, boosting entrepreneurship and financial participation among rural middle-class households.

Differences in Education Levels

Following Ma (2024), we categorized household education levels into low (up to 9 years) and high (more than 9 years). Excluding household education variables, Table 4 shows the impact of digital inclusive finance on middle-class vulnerability across these education levels. The coefficients in columns (5) and (6) reveal a mitigating effect for both groups. Specifically, the coefficient for high education is −0.393, while for low education, it is −1.713, passing the inter-group coefficient difference test (p value < .01), indicating a more substantial impact for the latter. Digital inclusive finance, leveraging internet technology, reduces education costs, alleviates financing constraints, and improves financial management for less-educated households (F. Wu et al., 2023). In contrast, highly educated households often benefit earlier from existing financial policies. Thus, digital inclusive finance more effectively reduces vulnerability for middle-class households with lower education levels.

Age Difference

Following Luan et al. (2023), we categorize households into two groups by age: middle and young (average age below 60) and old (average age 60 or above). After excluding the average age variable, Table 4 shows the impact of digital inclusive finance on middle-class vulnerability across these age groups. The coefficients in columns (7) and (8) indicate significant mitigation effects for both groups. Specifically, the coefficient for middle and young households is −1.029, and for old households, it is −1.654, both significant at the 1% level and passing the inter-group coefficient difference test (p value < .05). Digital inclusive finance has a more pronounced effect on older households. Previously limited by traditional financial services, older individuals faced challenges in financial participation due to learning and cognitive constraints. Digital inclusive finance allows them to gain financial knowledge online, access product information, make online payments, and reduce transaction costs, enhancing their financial involvement.

Robustness Test

This study tries to address potential endogeneity issues, particularly those arising from bidirectional causality and omitted variables. Following Yi et al. (2023), we use two-stage least squares regression (2SLS) and instrumental variable probit (IV Probit) estimation to address potential endogeneity concerns. We adopt the F. Wu et al. (2023) method, using the distance between a household’s city center and Hangzhou, Zhejiang Province, as an instrumental variable (IV) for digital inclusive finance. This variable is called ‘lndistance’, with distances converted to natural logarithms. Guo et al. (2020) found that the Digital Inclusive Finance Index shows convergence and strong spatial clustering. Hangzhou, home to Ant Group, leads in digital finance development and has the highest index value. This suggests a diffusion pattern centered around Hangzhou: the farther a location is from Hangzhou, the more challenging and delayed the development of digital inclusive finance. Thus, a negative correlation exists between distance from Hangzhou and digital finance development, meeting the relevance condition for instrumental variables. Additionally, geographical distance is independent of economic development and unrelated to household or individual characteristics, ensuring the exogeneity of this instrumental variable.

As shown in Panel A of Table 5, we apply the same control variables as in column (4) of Table 2. Columns (2) and (4) represent the first-stage estimation, and the coefficients for Lndistance are negative and significant at the 1% level. Additionally, the Minimum Eigenvalue is 2014.46, well above the threshold of 16.38 required to reject the null hypothesis of weak IV, thereby eliminating concerns about weak IV. The results from the linear 2SLS estimation in column (1) and the IV Probit in column (3) show that the coefficient for digital inclusive finance is negative and significant at the 1% level. This further confirms that digital inclusive finance significantly reduces middle-class vulnerability.

Robustness Check.

Note. Robust standard error is used and is listed in the brackets.

p < .01.

As shown in Panel B of Table 5, we employ an extended regression model (ERM) to reassess the impact of digital inclusive finance on middle-class vulnerability. According to Jiang and Wang (2020), ERM is versatile enough to address issues such as omitted variables, sample selection, and bidirectional causality simultaneously. Following the methodology of Yi et al. (2023), we apply linear ERM and Extended Probit estimation (Eprobit) in Panel B of Table 5, respectively. The results show that the coefficients for DIF remain significantly negative, reinforcing our previous findings that digital inclusive finance effectively reduces middle-class vulnerability.

In Table 6, we conduct robustness tests by varying the thresholds for the dependent variable using different treatment approaches. First, we adjust the vulnerability line, initially defined as 50% of a household’s expected income exceeding $10, to 30% and 40%, while also increasing the income standard from $10 to $20. The coefficients for DIF in columns (1), (2), and (3) remain significantly negative at the 1% level, providing further evidence that digital inclusive finance significantly reduces middle-class vulnerability.

Robustness Check: Replacement of the Measurement of the Dependent Variables.

Note. Marginal effects rather than coefficients are reported; robust standard error is used and is listed in the brackets under the marginal effect coefficient.

p < .01.

Discussion and Conclusion

Discussion

This study employs the VEP method to quantify the vulnerability of China’s middle class and examines the role of digital inclusive finance in mitigating this vulnerability. The findings indicate that digital inclusive finance significantly reduces the risk of vulnerability among the middle class. The rising vulnerability of the middle class is a key factor contributing to its shrinking size, a conclusion consistent with the findings of Rougier et al. (2021). Expanding the size of the middle class primarily involves two pathways: promoting upward mobility of low-income groups into the middle class and preventing the middle class from falling into lower-income groups by reducing their vulnerability. However, existing literature has predominantly focused on the former. For instance, Nissanov (2017) explored the role of household factors in the upward mobility of low-income groups from the perspective of income mobility.

In contrast, research on the vulnerability of the middle class remains relatively limited. Some scholars have investigated this issue; for example, Stampini et al. (2016) found that approximately 14% of the middle class in Latin America faces vulnerability risks. Similarly, X. Chen and Li (2023) quantified the vulnerability of China’s middle class using the VEP method and conducted an empirical analysis of household-level factors, identifying education levels and household assets as critical for alleviating vulnerability. Most existing studies focus on micro-level household influences while neglecting the occupational characteristics and income structures associated with middle-class vulnerability. In reality, middle-class households at risk of vulnerability are often engaged in low-service or informal self-employment, with wage income as their primary source of revenue (Sicular et al., 2022). Thus, increasing income levels emerges as the central strategy for mitigating vulnerability risks.

Existing research has paid insufficient attention to the role of digital inclusive finance in mitigating the vulnerability of the middle class. By integrating inclusivity and stability, digital inclusive finance effectively addresses the limitations of traditional financial services (Ozili, 2018). The empirical findings of this study demonstrate that digital inclusive finance significantly increases the income levels of the middle class through three pathways: fostering entrepreneurship, enhancing financial participation, and improving employment opportunities. Consequently, it reduces their vulnerability risk. This insight adds a new perspective to the existing literature, highlighting the macro-level impact of digital inclusive finance compared to studies focusing primarily on household-level factors. Moreover, the effect of digital inclusive finance in reducing vulnerability is particularly pronounced in central and western regions, rural areas, populations with lower education levels, and older demographic groups.

In summary, this study confirms the positive impact of digital inclusive finance in alleviating middle-class vulnerability and underscores its critical role in facilitating the sustained expansion of the middle class. These findings provide practical implications for promoting the growth of the middle class and expand the theoretical boundaries of research on middle-class vulnerability.

Based on the above research results, we put forward the following policy recommendations: First, building digital inclusive finance platforms and technologies is crucial to bridging the digital divide. Policymakers should address the lagging development of digital inclusive finance in central and western regions by providing financial transfers and dedicated support funds to enhance digital financial infrastructure. Specific measures include expanding internet coverage, improving network quality, and reducing internet usage costs. These actions aim to promote a balanced development of digital inclusive finance services across regions.

Second, in rural areas, policies should focus on developing digital finance services tailored to the needs of agricultural economies and rural residents, such as introducing small-loan platforms for agricultural production, providing accessible digital payment tools, and establishing financial technology support networks for rural areas. Training programs and awareness campaigns should also help improve rural residents’ understanding and usage of digital financial tools.

Finally, simplified and user-friendly digital financial platforms should be designed for middle-class individuals with lower education levels. At the same time, digital financial education and training should be enhanced to improve their digital literacy. These training initiatives can be implemented through community activities, online courses, and partnerships with vocational training companies. Such efforts ensure that policies are both targeted and practical. Additionally, to address the challenges older individual face in using digital inclusive finance, financial services, and technologies should be tailored to their needs. This includes optimizing user interfaces, introducing simple and easy-to-use financial products, and lowering the barriers for elderly individuals to participate in digital financial systems.

Limitations and Future Research Directions

This study offers valuable insights into the relationship between digital inclusive finance and middle-class vulnerability. Nonetheless, several limitations should be noted, pointing to promising future research directions: (1) the scope of our analysis is confined to China, which limits the generalizability of the findings to other countries. Considering the significant economic, institutional, and cultural differences across nations, future studies could adopt a comparative approach by extending the analysis to multiple countries or regions. This would provide a more comprehensive understanding of how digital inclusive finance impacts middle-class vulnerability in diverse economic contexts; (2) our methodology employs the VEP model based on cross-sectional data. Specifically, this study uses data from the most recent 2020 wave of the CFPS. While this approach allows us to capture a snapshot of middle-class vulnerability, it does not account for income mobility or dynamic changes over time. Future research could address this limitation by utilizing longitudinal data to track changes in middle-class vulnerability over multiple periods, thereby providing deeper insights into the long-term effects of digital inclusive finance; (3) this study focuses on three ways digital inclusive finance reduces middle-class vulnerability: promoting entrepreneurship, enhancing financial participation, and improving employment. However, these mechanisms are not exhaustive. Future research could explore additional pathways, such as the role of digital finance in increasing household insurance participation or mitigating unexpected financial risks. Examining these alternative channels would offer a more nuanced understanding of how digital inclusive finance influences middle-class vulnerability.

Conclusion

This study systematically analyzes the vulnerability of the middle class using CFPS2020 data and the theory of poverty vulnerability, focusing on the impact of digital inclusive finance. After controlling for various household variables and regional fixed effects, the findings indicate that digital inclusive finance significantly reduces middle-class vulnerability and helps stabilize the middle-class population. 2SLS and IV Probit estimations confirm a strong negative correlation between digital inclusive finance and middle-class vulnerability. The mechanism analysis reveals that entrepreneurship, financial participation, and employment are critical channels through which digital inclusive finance mitigates middle-class vulnerability. Further analysis shows that, compared to the eastern region, urban areas, and the highly educated middle class, those in the central and western regions, rural areas, and those with lower education levels are more vulnerable. The development of digital inclusive finance helps bridge the ‘digital divide’ across regions, urban and rural areas, educational disparities, and age groups. Notably, the effect of digital inclusive finance in reducing vulnerability is more pronounced in central and western regions, rural areas, those with lower education levels, and older groups.

Footnotes

Funding

The author(s) disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: This work was supported by the National Social Science Fund of China (Grant number. 18BJY047), and Zhejiang Office of Philosophy and Social Science (Grant number. 24NDQN202YBM).

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Data Availability Statement

This study utilizes data from the China Family Panel Studies (CFPS), a comprehensive longitudinal survey that captures changes in China’s society, economy, demographics, education, and health. The CFPS provides a robust data foundation for academic research and public policy analysis. Interested researchers can access the data through the official CFPS website: ![]() . Additionally, the specific dataset and related programs referenced in this paper can be made available upon request to the paper’s corresponding author.

. Additionally, the specific dataset and related programs referenced in this paper can be made available upon request to the paper’s corresponding author.