Abstract

The purpose of this study is to investigate the impact of asset status and external factors related to asset status on income distribution disparities among senior executives, employees, and shareholders. Incorporating micro-level data and theoretical analysis, the data of Chinese a-share listed companies from 2012 to 2021 are selected for panel regression analysis. Existing research has often focused on the main differences in income between employees and executives. This study reveals that the distribution of total corporate income among employees, executives, and shareholders can better reflect the fluctuating trend of income variance among different groups. It was found that asset efficiency, asset market value, and asset property rights, among other asset status factors, significantly influence the degree of inequality in income distribution. Empirical research results indicated that corporate executives can benefit similarly to shareholders from improvements in asset efficiency and other asset status factors. Following an increase in corporate cash holdings, executives tend to benefit more relative to employees. Additionally, digital inclusive finance and equity concentration both have moderating effects, mitigating the impact of asset status on inequality in income distribution.

Plain Language Summary

This new study bridges the identified gaps in the literature, and the current research intends to investigate the effect of asset status on income distribution. As far as we know, this paper is the first time to select total executive compensation, total employee compensation and shareholder returns are adopted as the basic variables to measure the polarization of wealth distribution, and to combine the regulating role of digital inclusive finance and equity concentration.

Highlights

Panel the data of China’s A-share listed companies from 2012 to 2021. The impact of asset status on the inequality of income distribution is explored.

Wealth distribution polarization is measured by the difference in the distribution ratio of total income. Asset status can significantly affect the degree of income distribution polarization.

Digital financial inclusion and ownership concentration attenuate wealth distribution polarization.

Introduction

Across the world, whether it is a community of shared interests, or economies or countries, the competition between them is focused on the competition of wealth accumulation, and severe inequality in income distribution is suppressing economic development and financial stability (Yi et al., 2021). Since the 1990s, China’s share of labor income has shown a volatile downward trend (Liu et al., 2022), the total proportion of labor remuneration in the primary distribution is about 50%, which is lower than the average level of developed economies (Li & Zhang, 2020). The wealth inequality of Chinese residents is still relatively high (Li et al., 2021), and income inequality has become an important factor affecting the macroeconomic fluctuations (Kaplan et al., 2018). How to achieve fair income distribution and narrow the wealth gap has become a major theoretical and practical problem that needs to be solved in China (Yang et al., 2021). Therefore, this study provides a new research perspective by empirically analyzing the impact of asset status on income inequality, exploring the influencing factors of income inequality, and promoting the fairness and efficiency of income distribution.

As the economy and society ushered in a new stage of development, the defects of low pricing efficiency in the past have been changed. The capital market will give more consideration to fairness and efficiency (Arjunwadkar, 2018), and the asset status is poised to become one of the critical factors influencing income distribution fairness. Specifically, changes in asset status can lead to variations in asset returns, but the extent to which these changes impact different interest groups varies. The thorough analysis of how asset status affects corporate wealth is of great significance in promoting income equality. With the maturity of China’s stock market, it has become a common method to integrate capital operation and develop productivity through capital market in stock market (Rhodes-Kropf & Viswanathan, 2004). At the same time, with the continuous concentration of industrial asset control, the scope of job opportunity of workers in the industry is passively reduced, and capital owners have stronger pricing power in employee compensation. The value of assets will be reassessed after listing, and the wealth of asset owners will be rapidly accumulated, which can reduce their financing constraints and lead to a gradual increase in the proportion of assets in production and operation (Spaliara, 2009). Autor et al. (2020) showed the correlation between the asset status and the income share of workers. As the wealth distribution problem caused by the gradual strength of assets becomes one of the important factors leading to income inequality, the income difference between management and labor will be more obvious, and the income growth of ordinary employees will be significantly lower than hat of executives and shareholders.

As for financial development and income distribution, some scholars have analyzed and found that financial development and maturity can narrow the gap between the rich and the poor by constructing the Greenwood-Jovanovic model (Greenwood & Jovanovic, 1990). Some scholars mentioned that in the early stage of financial development, the poor cannot obtain good financial services, which will lead to further widening the gap between the rich and the poor (Das &Chatterjee, 2023). Some scholars also believe that the impact of financial development on income distribution is not a single and negative one (Brei et al., 2023; Cihak & Sahay, 2020). Digital inclusive finance enables a fair and efficient allocation of financial resources, because its larger financial coverage and stronger financial depth and breadth provide more financial services for vulnerable groups (Corrado & Corrado, 2017). By balancing the allocation of financial resources (Claessens & Perotti, 2007) and alleviating the polarization of financial repression and credit allocation, digital inclusive finance is beneficial to promote the realization of income equality.

Existing research on compensation distribution primarily focuses on the average compensation for executives and employees or the average wage disparity between executives and employees. It points out that factors such as corporate operational efficiency, internal controls, and government subsidies can influence the compensation of executives and employees, as well as the disparities between their compensations (Lin & Xie, 2022), Few existing studies have considered the reasons for the difference in compensation distribution between senior employees and ordinary employees, and few studies have paid attention to the differences between employee compensation and shareholder dividends (Connelly et al., 2016). However, the average salary difference can not fully measure the realization of income equality.

This study holds that the differences in average salary only include the wealth distribution problem from the perspective of fairness, without considering the differences in efficiency wage generated by various personal ability of executives and the size of management companies. Therefore, the differences in average salary cannot measure whether the wealth distribution is concentrated to limited persons.

In this study, it is extremely necessary to find indicators other than average salary difference to measure the fairness and efficiency of income distribution. By measuring the income distribution among different groups, the current study discusses the impact of changes in enterprise asset status on the promotion of income distribution fairness. The econometric model is adopted to empirically test the impact of asset efficiency, asset value and asset property on senior executives and employees, senior executives and shareholders, employees and shareholders, and so forth. Combined with the concentration of ownership and the external environment of digital inclusive finance, the effect of regulation is empirically tested.

The main theoretical and managerial contributions of this study are as follows. 1. In order to analyze whether income distribution has a centralized tendency to a certain group, total executive compensation, total employee compensation, and shareholder returns are adopted as the basic variables to measure the polarization of wealth distribution. While taking into account fairness and efficiency, the scope of measuring the polarization of wealth distribution has been expanded to include senior executives and employees, executives and shareholders, employees and shareholders, and different kinds of executives. 2. Starting from the internal and external asset status such as asset efficiency, asset value, and the attributes of asset property, the influence of asset status on wealth distribution has been comprehensively tested in combination with the regulatory effects of digital inclusive finance and equity concentration on asset status. The innovation of this research is reflected in the adoption of enterprise asset value variables as explanatory variables, which not only studies the impact of asset value on employee compensation distribution, but also studies the wealth distribution between labor and capital. 3. The current study finds from empirical evidence that asset status has a different impact on wealth distribution among different objects. Since both senior executives and actual controllers of assets have varying degrees of control over assets, they can benefit from the improvement of asset status, and can obtain salary income or asset value accretion.

Theoretical Analysis and Research Hypothesis

Many countries, such as Argentina, Brazil, and the Philippines, have experienced a period of rapid economic growth but later found themselves trapped in the “middle-income trap.” One common characteristic among them is that during their rapid economic growth, income inequality remained persistently high. Therefore, promoting fair income distribution and achieving shared prosperity involve correcting and compensating for systemic factors that have led to inequality. This process aims to provide equal opportunities and capabilities for all citizens to participate in high-quality economic and social development (Yu & Ren, 2021). With the improvement of labor production efficiency caused by technological progress, the necessary labor time to produce the same amount of products is shortened, which leads to the continuous increase of relative surplus value. When more of the relative surplus value is captured by capital owners, it leads to wealth polarization in wealth distribution. In other words, changes in asset ownership affect the share of income for laborers. With technological innovation and increased asset efficiency, labor productivity rises, and changes in the composition of capital technology further enhance the significance of capital in production. The imbalance in the production relationship between labor and capital becomes one of the factors influencing the fairness and efficiency of income distribution. Additionally, credit constraints in financial development are an important factor affecting income inequality (von Ehrlich & Seidel, 2015) Meanwhile, relying on the cross-space characteristics of digital network technology, digital inclusive finance can effectively expand the coverage of financial services, improve the quality of financial services (Ge et al., 2022), and promote high-quality regional economic development, which provides a good financial environment for enterprises and strongly drives the coordinated development of common prosperity. Shleifer and Vishny (1986) showed that when the shareholding ratio of major shareholders increased, their functions would be continuously strengthened, thus affecting wealth distribution.

Asset Status and Labor Salary

Asset status can be primarily categorized into internal and external factors. Here’s a breakdown of these internal factors: 1. Asset Efficiency: Reflects how effectively a company utilizes its assets to create value. Efficient asset utilization is often associated with more balanced income distribution. 2. Asset Property Rights: Refers to the ownership and control structure of company assets, including state-owned, private, or mixed ownership. Different property rights can impact how a company operates and makes decisions, thus affecting income distribution fairness. 3. Asset Market Value: Indicates the market valuation of company assets, and an increase in market value can influence wealth distribution between executives and shareholders. 4. Cash Holdings: The amount of cash and cash equivalents held by the company is also part of internal asset status. The abundance or scarcity of cash can affect financial decisions and, consequently, impact compensation distribution.

The ability of senior executives to control capital is sometimes even stronger than the shareholders. According to the hypothesis of management power, senior executives has the ability and motivation to influence the wealth distribution (Bebchuk et al., 2002). Therefore, senior executives manipulate the wealth distribution among workers through their own power and become the main beneficiaries of the relative surplus value after the internal status of assets such as capital efficiency is improved. Some studies have also shown that under the market economy system, the improvement of asset efficiency will inevitably lead to the polarization of wealth distribution (Stiglitz, 2013). A similar situation may also occur when the market value of an enterprise is high or the cash of the enterprise is relatively abundant. Market economy can only produce economic efficiency, while lacks the ability to promote social equity and the power to eliminate the polarization of wealth distribution. To narrow the gap between the rich and the poor, government forces other than market economy is required to intervene in regulating wealth distribution (Alesina et al., 2018). Under the socialist market economy with Chinese characteristics, state-owned enterprises assume part of government functions and part of social responsibilities instead of the government, so state-owned enterprises may be better than other enterprises in terms of income gap elimination. Accordingly, the following hypothesis is proposed.

H1a: Asset status can affect the wealth distribution between senior executives and employees, and the executives benefit more from asset status than the employees.

H1b: Enterprises with different property rights have different effects on the wealth distribution between senior executives and employees.

Asset Status and Enterprise Capital

The continuous concentration of wealth to capital and a few people is not conducive to the internal stability and long-term development of the enterprise, and the internal wealth distribution in an enterprise will spontaneously adapt or strategically adjust with the change of asset status to ensure the stability and permanence of capital profits. Abowd et al. (1999) holds that enterprise owners sometimes transfer part of the relative surplus value to workers as efficiency wages, thereby motivating employees to obtain more relative surplus value. Shareholders can not only gain profits from operating results, but also gain capital gains from the growth of corporate value. When the value of an enterprise rises, the shareholders can obtain additional wealth appreciation from the capital market. Therefore, they are more willing to transfer part of the profits in the operation results as efficiency wages to motivate employees. By doing this, they can form a community of interests with shareholders, so as to maintain the good development trend of enterprises and promote the steady rise of enterprise value. As for the wealth distribution among employees, previous studies have shown that employee compensation is negatively correlated with enterprise value. As a means of employee motivation, the appropriate pay difference is the key variable to enhance the enterprise value (Chen & Huang, 2019). Therefore, the asset status can also become the realistic basis of affecting the wealth distribution. Based on this, the following research hypothesis is proposed:

H2: Asset status can affect the ability of stakeholders to capture relative surplus value, that is, the income distribution between labor and capital.

Asset Status and Digital Inclusive Finance

Digital inclusive financial services have the characteristics of wide coverage and low threshold (Fuster et al., 2019), which promote enterprises to obtain more economic opportunities. Digital inclusive finance can effectively alleviate the financing costs of the upstream and downstream of the whole industrial chain, reduce the financing costs of enterprises and broaden financing channels. It improves the overall efficiency of the industry through financial support to improve the internal asset state, and enables workers and enterprises to share the fruits of economic development (Hu et al., 2021). Meanwhile, digital inclusive finance also plays a positive role in the construction of regional financial markets, promoting the participation of regional households in financial asset allocation by reducing transaction costs and increasing the availability of financial resources (Zhang et al., 2022). Zhang et al. (2022) also proved that the development of digital inclusive finance can increase entrepreneurial activity, the demand for labor will also increase, and the improvement of regional financial environment will attract more high-quality capital. In the digital inclusive financial environment, the marginal contribution of capital status to wealth distribution decreases, i.e. the digital inclusive financial policy system should have a positive impact on income distribution. Based on this, the research hypothesis is proposed:

H3: Digital inclusive finance can reduce the ability of asset status to influence the polarization of income distribution.

Asset Status and Equity Concentration

Managers generally believe that the success of business operations is attributed to individuals, so there are cases where the management gets too much salary through the formulation of policies. When asset status can affect compensation distribution and surplus value, external forces which can control assets will also affect enterprise compensation distribution by intervening in management decisions and changing the influence ability of asset status (Baggs & De Bettignies, 2007). Gaur et al. (2015) and Qian & Liu, (2019) both pointed out that the concentration of ownership can reduce the cost of principal-agent, so that shareholders have more incentive to supervise the management; But with the dispersion of ownership, this regulatory impetus will gradually diminish; Meanwhile, when the ownership is concentrated, it is difficult to form checks and balances among shareholders because of the large voice of the major shareholders. Johnson et al. (2000) put forward the theory of Tunneling of major shareholders, which holds that the control rights of major shareholders will be enhanced after the concentration of equity, and affect the company’s management decisions, which has the possibility of encroaching on the interests of listed companies. Chen et al. (2020) found that the higher the concentration of ownership of major shareholders, the stronger their ability to control corporate dividend distribution. In such cases, major shareholders can not only influence dividend distribution (Shleifer and Vishny, 1997), but also have a stronger power in compensation distribution, which will weaken the influence of asset status on wealth distribution and may lead to polarization of wealth distribution. Based on this, the following research hypothesis is proposed:

H4: The subjective distribution ability of wealth distribution will be enhanced with the increase of ownership concentration, which will weaken the influence of asset status on wealth distribution.

Research Design

By selecting the data of China’s A-share listed companies, a panel regression model is established to test whether the hypothesis that the polarization of income distribution is affected by asset status is valid. On this basis, the moderating effect of digital inclusive finance and equity concentration on the influence of asset status on the polarization of wealth distribution is further studied.3.1 Sample selection and data source.

Sample Selection and Data Source

China’s A-share listed companies from 2012 to 2021 are selected as research objects, and samples with the following attributes were excluded: 1. Listed companies in the financial industry; 2. Abnormal trading listed companies in ST status; 3. Companies listed less than 1 year; 4. Listed companies with missing data or less than 5 years of sample size. In the sample year interval, a total of 2,878 enterprises were obtained. To eliminate the influence of individual outliers, Winsorized method was adopted to indent the data of major continuous variables by 1%. The variable of the development level of digital inclusive finance was selected from the Digital Inclusive Finance Index compiled by the Internet Finance Research Center of Peking University (Guo et al., 2020), and the other variable data came from CSMAR.

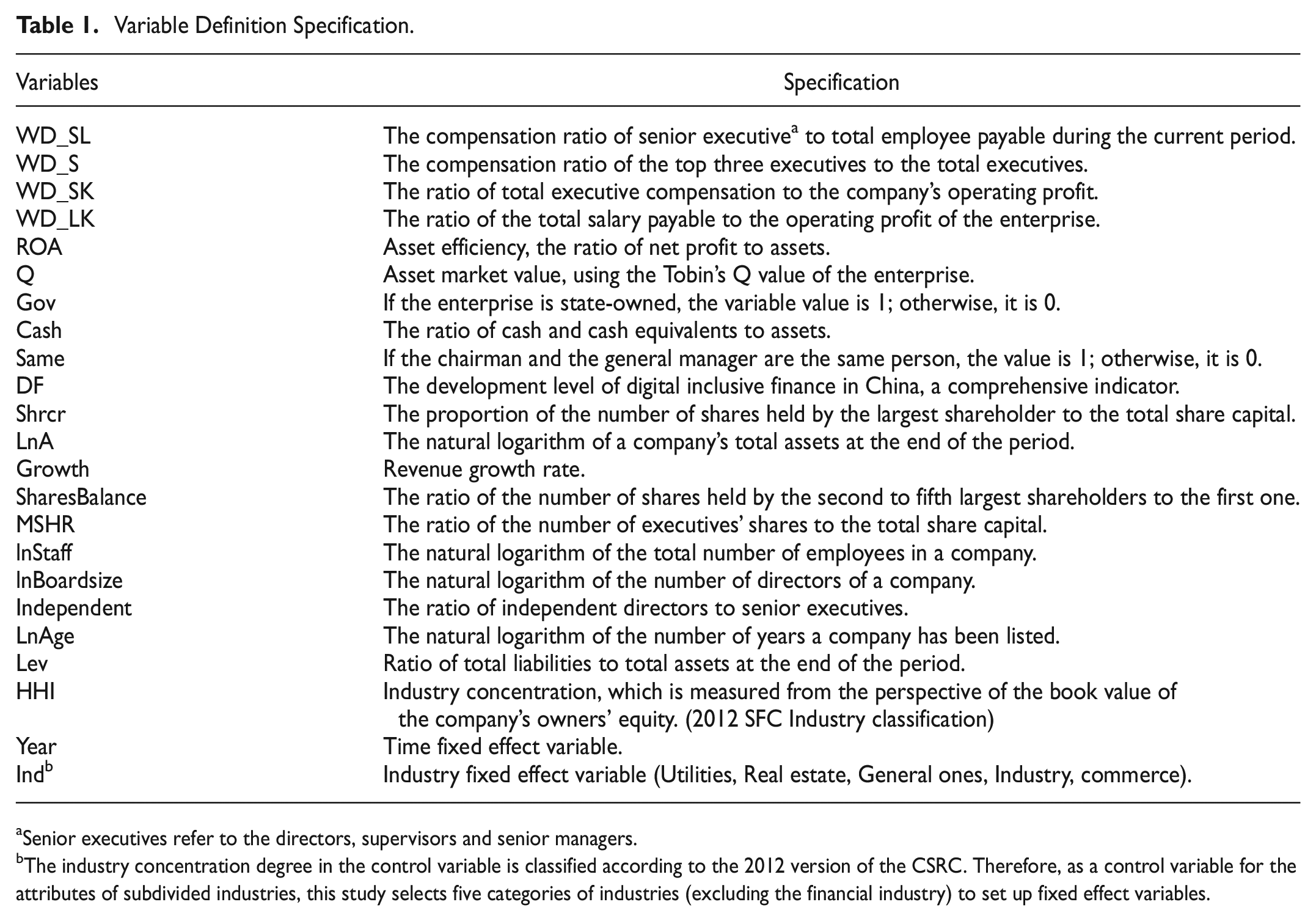

Variable Definition

Explained Variables

In this study, the variable of income distribution polarization is used as the explained variable. This variable measures the degree of polarization of wealth distribution among senior executives, employees and shareholders. Among them, senior executives include directors, supervisors and senior managers. Since income equality needs to balance fairness and efficiency, the total compensation of senior executives and the total amount of credit payable to employees in this year are selected as research data. In order to avoid the responsibility of senior executives due to the large size of the enterprise and the large number of employees, the average salary data is not adopted because the average salary data only consider fairness but not enough to consider efficiency.

Polarization of income distribution between executives and employees (WD_SL): The proportion of executive compensation to the credit amount of employee compensation payable in the current period is used to measure the degree of polarization of wealth distribution between senior executives and employees.

Polarization of income distribution within senior executives (WD_S): The proportion of the sum of the top three salaries in the total salary of senior executives is used to measure the polarization of wealth distribution among senior executives.

Polarization of income distribution between executives and shareholders (WD_SK): The ratio of total executive compensation to corporate operating profit is used to measure the polarization of wealth distribution between senior managers and capital.

Polarization of income distribution between employees and shareholders (WD_LK): The ratio of employee pay payable in the credit side to corporate operating profit is adopted to measure the degree of polarization of wealth distribution between employees and shareholders. This index not only represents the proportion of labor part, but also represents the ability of capital to acquire relative surplus value. When the ratio of employee pay payable to corporate net profit decreases, it is considered that the polarization of wealth distribution increases.

Core Explanatory Variables

In this study, relevant variables that can display asset status are selected as the core explanatory variables, including internal asset status and external asset status. The internal state includes the asset efficiency, the market value of assets and the proportion of cash in assets. The external state is the property of the asset controller, also known as the nature of property rights in assets.

Asset efficiency (ROA): The profit efficiency of an enterprise’s assets is measured by the return on total assets, which is calculated by dividing the after-tax net profit by the total assets.

Asset market value (Q): Tobin’s Q value is adopted to measure the market value of enterprise assets. The calculation method is: (enterprise A stock market value + (total equity − A-share equity) × (total owners’ equity at the end of the period ÷ paid-in capital at the end of the period) + enterprise liabilities) ÷ total assets.

Nature of asset property (Gov). The nature of the controlling shareholder is the state, state-owned legal person, domestic state-owned legal person of the enterprise is judged to be state-owned holding enterprises. The variable value of state-owned holding enterprise is 1, otherwise, it is 0.

Cash holding ratio (Cash). The ratio of cash and cash equivalents to total assets is calculated to measure corporate cash holdings.

Moderating Variable

Digital inclusive finance development level (DF): The combined index of provincial digital inclusive finance is selected to measure the development level of digital inclusive finance in the region where listed companies are located. Guo et al. (2020) conducted a quantitative study on the development level of digital inclusive finance in China by establishing a multi-level index system, and comprehensively measured the coverage breadth, utilize depth and digitization degree of regional digital inclusive finance through the combined index.

Ownership concentration (Shrcr): The proportion of the number of shares held by the largest shareholder to the total share capital is used to measure the ownership concentration of listed companies. The higher the ownership concentration, the stronger the control power of the major shareholders, and vice versa.

Control Variable

Based on existing studies, influence variables related to wealth distribution were selected as control variables, including: Asset size (LnA), operating revenue growth rate (Growth), equity balance degree (SharesBalance), management shareholding ratio (MSHR), natural log of the number of staffs (lnStaff), natural log of the number of directors (lnBoardsize), the proportion of independent directors to the number of senior executives (In dependent), two positions in one (Same), natural log of enterprise age (LnAge), financial leverage ratio (Lev), concentration ratio of industry (HHI); At the same time, industry fixed effect variables (Ind), and time fixed effect variables (Year) were established according to the industry attributes and time of the samples (Zhou & Zhu, 2010; Table 1).

Variable Definition Specification.

Senior executives refer to the directors, supervisors and senior managers.

The industry concentration degree in the control variable is classified according to the 2012 version of the CSRC. Therefore, as a control variable for the attributes of subdivided industries, this study selects five categories of industries (excluding the financial industry) to set up fixed effect variables.

Model Construction

Research Model of the Polarization of Income Distribution Among Labor Forces

To test H1a, model (1) is established to test the influence of asset status on the degree of polarization of wealth distribution between executives and employees. Model (2) is established to test the influence of asset status on the degree of polarization of wealth distribution among executives.

Research Model of the Polarization of Income Distribution Between Labor and Capital

To test hypothesis 2, model (3) is established to test the impact of asset status on the polarization degree of wealth distribution between executives and shareholders; Model (4) is established to test the impact of asset status on the polarization degree of wealth distribution of employees and shareholders.

Moderating Effect Model

To test hypothesis 3 and hypothesis 4, a moderating effect model is established by introducing interaction terms. The interaction term ShrcrROA between major shareholder shareholding ratio Shrcr and ROA of return on assets is established to test the moderating effect of Shrcr on the relationship between ROA and compensation (profit) distribution. The interaction term DFROA between the development level of DF and the ROA is established to test the moderating effect of the increase of DF on the relationship between ROA and wealth distribution.

Where,

Empirical Research

Descriptive Statistical Analysis of Variables

Table 2 shows the descriptive statistics of the variables. The results show that the mean value of WD_SL is 2.686% and the median value is 1.837%. Generally, senior executive salary accounts for a small proportion of the company’s total salary, but the maximum WD_SL has reached 16.40%, indicating that there is a strong polarization of wealth distribution between senior executives and employees who are workers in specific enterprises. The mean value of WD_S is 48.322%, indicating that the total compensation of the top three executives accounted for a higher proportion of the total salary of all executives. The mean values of WD_SK and WD_LKa are 5.261 and 274.901%, respectively, indicating that the share of wealth distribution between executives and the rest of labor and capital. The mean of the Gov is 0.362, indicating that the proportion of state-owned holding companies in the selected sample is 36.2%. The mean and median values of Shrcr are 33.6766 and 31.4005%, respectively, indicating that the largest shareholder of A-share listed companies generally has a high shareholding ratio and strong control ability over the management decisions of listed companies.

Descriptive Statistics of Variables.

The samples of WD_SK and WD_LK remove listed companies with negative operating profits.

The minimum value of WD_SK approaches 0, and the value is 0 after four decimal places.

Benchmark Regression Analysis of the Polarization of Income Distribution

Table 3 shows the regression results of the model of the influence of asset status on the polarization of wealth distribution. The coefficients of ROA and Q in column (1) are both positive; The increase of ROA and Q indicates that the internal efficiency and external value of assets increase, so that the enterprise management can obtain higher returns, which leads to the increase of WD_SL; The coefficient of Gov is significantly negative, indicating that companies with the property of state-owned holding enterprises can reduce WD_SL, that is, state-owned holding enterprises enable executives and employees to share the development achievements of enterprises, showing that they are more able to promote the realization of common prosperity. The coefficient of Cash held by enterprises is positive, indicating that senior executives can get higher income distribution than employees with the increase of enterprise Cash, which leads to the increase of WD_SL.

The Influence of Asset Status on the Polarization of Income Distribution.

Note. Authors’ own calculation.

, **, * represent significance at the significance level of 1, 5, and 10% respectively, and the Z-value of robust standard error is in parentheses, the same below.

The coefficient of ROA in column (2) is negative, indicating that the increase of ROA can reduce WD_S, that is, executives of the enterprise can share the operating results brought by the increase of enterprise efficiency. The coefficient of Q is positive, that is, the increase of Q can increase WD_S, which means that the increase in the market value of enterprise assets will further concentrate the wealth distribution within executives to a few people. The coefficient of Gov is negative, indicating that state-owned enterprises can narrow the gap in the internal wealth distribution of executives and make the wealth distribution fairer. The coefficient of Cash is positive, indicating that the internal wealth distribution of executives is concentrated to a few ones after the increase of cash holdings.

The coefficient of ROA in columns (3) and (4) is negative, indicating that the proportion of compensation obtained by labor in shareholders’ profits decreases, that is, the increase in asset efficiency leads to the concentration of wealth distribution to capital. The coefficients of Q are all positive, which means that the proportion of shareholder profits paid to labor goes up. This illustrates that when the value of the enterprise increases, the shareholders gain capital appreciation. In order to guarantee the virtuous circle of the company, the shareholders have the motivation to give part of the profits as the incentive for the senior executives and employees. In column (3), the coefficient of Gov is negative, while in column (4), it is positive, indicating that enterprises with state-owned holding property reduce WD_SK, but increase WD_LK. In the relationship among executives, employees and state-owned capital of state-owned holding enterprises, executives get lower salaries compared with state-owned capital profits, and employees get higher salaries compared with state-owned capital profits, that is, state-owned holding enterprises transfer more operating results to ordinary employees.

Subsample Regression

In the results of the benchmark regression model, Gov can significantly reduce the polarization of income distribution, that is, it can avoid the concentration of wealth to asset managers and shareholders, and promote the wealth distribution to the majority of workers, which is a strong guarantee factor for realizing common prosperity. On this basis, to get a clearer picture of its impact on different groups, the property rights of assets are adopted as subsample conditions to investigate the influence of asset status on wealth distribution under different property rights.

Heterogeneity Test: Trends in Income Distribution Among Workers

Columns (1) and (2) in Table 4 show that the coefficients of ROA are positive and that of Q are positive. This result indicates that the increase of ROA and Q can increase the polarization of wealth distribution between executives and employees, regardless of state-owned enterprises or non-state-owned enterprises. The Suest test value of Q regression coefficient in the two groups of samples is significant, indicating that the influence of Q in non-state-owned holding enterprises is greater than that in state-owned holding enterprises. The coefficients of Cash are not significant, indicating that Cash does not significantly affect the degree of polarization of wealth distribution between senior executives and employees after sample division.

The Influence of Asset Status of Listed Companies Under Different Property Rights on the Polarization of Executive-Employee Income Distribution.

Note. Authors’ own calculation.

, **, *represent significance at the significance level of 1, 5, and 10% respectively, and the Z-value of robust standard error is in parentheses.

Columns (3) and (4) show that ROA coefficients are not significant, indicating that ROA does not significantly affect the polarization degree of wealth distribution within executives after subsample. The coefficient of Q is positive, indicating that the increase of Q increases the polarization of internal wealth distribution of senior executives. However, the Suest test value of Q regression coefficient in the two groups of samples is not significant, and there is no significant difference in the impact of Q increase on the polarization of wealth distribution of senior executives between the two groups. The Cash coefficient is positive only in the model of non-state-owned holding samples, indicating that non-state-owned holding enterprises are more likely to aggravate the polarization of wealth distribution of internal executives when cash is abundant.

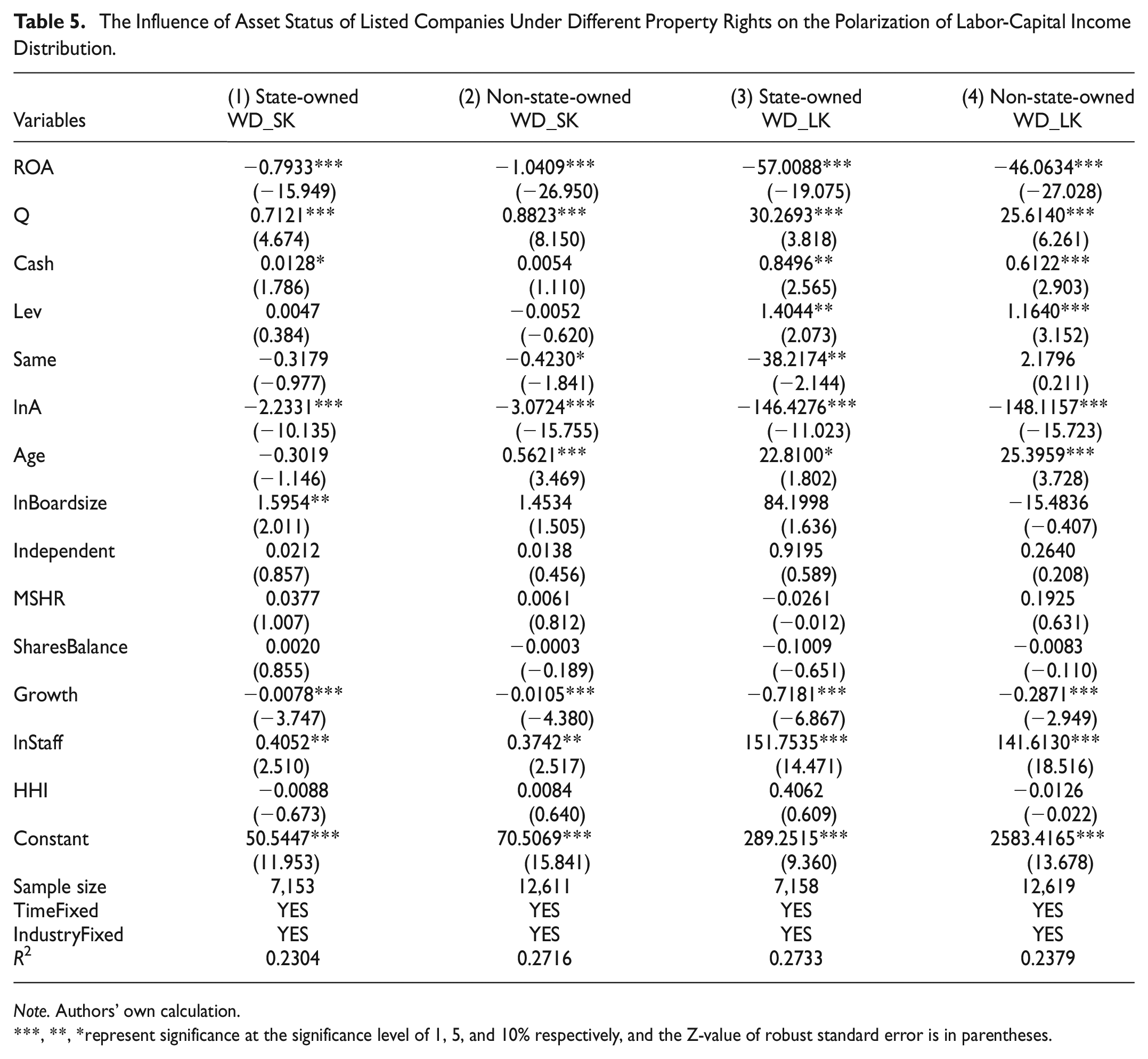

Heterogeneity Test: Trends in Income Distribution Between Labor and Capital

Columns (1) and (2) in Table 5 show that the coefficients of ROA are significantly negative, indicating that the increase of ROA has concentrated the distribution of wealth to capital and reduced the ratio of executive salaries to shareholder dividends. The Suest test value of ROA regression coefficient in the two subsamples is significant, indicating that this phenomenon is more obvious in non-state-owned enterprises. The coefficient of Q is significantly positive, indicating that after the market value of enterprise assets increases, the ratio of executive compensation to shareholder profits increases, that is, shareholders are willing to cede part of corporate profits as executive compensation after obtaining capital appreciation. However, the Suest test value of Q regression coefficient in the two subsamples is not significant, that is, there is no significant difference in the impact of Q increase on the polarization of wealth distribution between the two subsamples. The coefficient of Cash is positive only in the sample of state-owned holding enterprises, indicating that executives of state-owned holding enterprises can get higher proportion of salaries than corporate profits when the cash flow of enterprises is abundant.

The Influence of Asset Status of Listed Companies Under Different Property Rights on the Polarization of Labor-Capital Income Distribution.

Note. Authors’ own calculation.

, **, *represent significance at the significance level of 1, 5, and 10% respectively, and the Z-value of robust standard error is in parentheses.

The coefficients of ROA in columns (3) and (4) is significantly negative, indicating that the increase of ROA will concentrate the distribution of wealth to capital, which will reduce the ratio of employee compensation to shareholder profits. The Suest test value of the ROA regression coefficient in the two subsamples is significant, indicating that the proportion of the reduction of employee compensation relative to shareholder dividends in the samples of state-owned enterprises is larger. The coefficient of Q is significantly positive, indicating that after the market value of enterprise assets increases, the ratio of employee compensation to shareholder dividends increases, that is, shareholders are willing to surrender part of corporate profits as employee compensation after obtaining capital appreciation. However, the Suest test value of Q regression coefficient in the two subsamples is not significant, that is, there is no significant difference in the impact of Q increase on the polarization of wealth distribution between employees and shareholders in the two subsamples. The coefficient of Cash is positive, indicating that abundant cash flow can improve the ratio of employee compensation to capital profit, so that employees can get higher compensation than capital profit. Meanwhile, the Suest test value of Cash regression coefficient in the two subsamples is not significant, indicating that there is no significant difference in its influence degree.

Robustness Test

Variable Substitution

The robustness test is conducted by replacing core explanatory variables, including using ROE to replace ROA, using a new method to calculate enterprise market value Q_B or using BM to replace Q. The calculation method of Q_B assumes that all the share capital of the enterprise is listed in domestic A-shares, which is (total share capital × A-share price + corporate liabilities) ÷ total assets; Book-to-market ratio (BM) is calculated by dividing the company’s owner’s equity by the total market value. The higher the BM is, the lower the value of the enterprise’s assets in the market.

As can be seen from Table 6, after variable substitution, ROE, representing asset efficiency, and Q_C, representing asset market value, are still significant, and the direction is consistent with the previous benchmark regression model. The coefficient of BM is negative, which is in line with expectations, indicating good robustness of the model.

Variable Replacement Robustness Test Results.

Note. Authors’ own calculation.

, **, *represent significance at the significance level of 1, 5, and 10% respectively, and the Z-value of robust standard error is in parentheses.

Propensity Score Matching

In order to alleviate the endogeneity problems caused by errors in function setting, and in view of the difficulty in selecting alternative variables of asset property nature for robustness test, propensity score matching (PSM) method is used to obtain the net effect of Gov on the polarization of wealth distribution. The sample with Gov variable value 1 is the treatment group, and value 0 is the control group. Other core explanatory variables and control variables in the baseline regression model are selected as matching variables. Due to the large number of individuals in the control group, a one-to-four K-nearest neighbor matching in the caliper 0.05 range and Logit model are adopted. In order to ensure that the value range of propensity score of the treatment group and the control group has the same part (common support), only the samples conforming to the overlap assumption are matched.

According to the T-test results in Table 7, the average treatment effect of Gov is significantly negative before and after matching, indicating that the degree of polarization of wealth distribution can be significantly reduced when the property rights are state-owned, which is consistent with the results obtained by the benchmark regression model in the previous analysis. In the robustness test of variable replacement, no suitable variable was found to replace Cash held. Therefore, Cash was divided into two groups from high to low, with the first half being the treatment group and the second half being the control group. The same PSM method was used to obtain the net impact of Cash on the polarization of wealth distribution, and the robustness test was conducted. It can be seen from the test results in Table 7 that the Cash robustness test fails in the models of WD_SL and WD_SK. In the benchmark regression model and subsample regression model mentioned above, it can also be found that the significance of Cash is not stable. Therefore, the conclusion that Cash affects the wealth distribution between senior executives and employees as well as the wealth distribution between senior executives and shareholders needs to be treated with caution.

Test Results of Matching Sample Average Processing Effects.

Note. Authors’ own calculation.

, **, and * represent significance at the significance level of 1, 5, and 10% respectively.

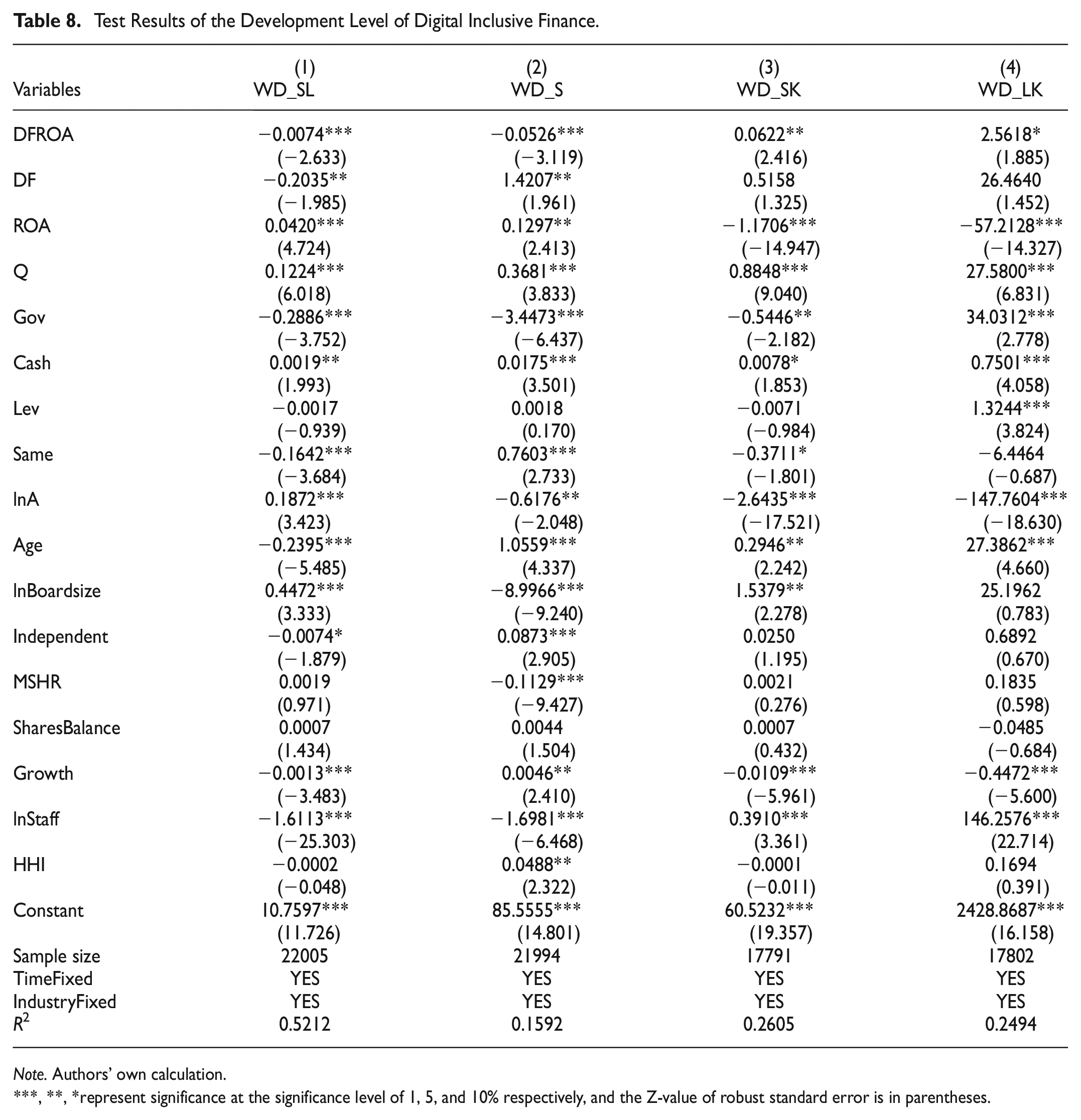

Further Study: Moderating Effect

The development level of digital inclusive finance, DF, and equity concentration, Skrcr, are selected as the moderating variables, and the interaction terms DFROA and SkrcrROA are constructed to test the moderating effects of DF and Skrcr on asset efficiency, ROA, and polarization of wealth distribution.

The regression results of columns (1) and (2) in Table 8 show that growth in DF can suppress the polarization of wealth distribution between senior executives and employees, and further strengthen the influence of ROA on reducing the polarization of wealth within executives. The results of columns (3) and (4) indicate that the increase in DF can inhibit the concentration of wealth distribution to capital.

Test Results of the Development Level of Digital Inclusive Finance.

Note. Authors’ own calculation.

, **, *represent significance at the significance level of 1, 5, and 10% respectively, and the Z-value of robust standard error is in parentheses.

The regression result of the model in column (1) in Table 9 shows that ShrcrROA is not significant, indicating that Shrcr does not significantly affect the intensity of ROA on the polarization of wealth distribution between senior executives and employees. Columns (2), (3), and (4) show that the ShrcrROA coefficient of interaction items are positive, indicating that the increase of Shrcr weakens the ability of asset efficiency to affect the polarization of internal wealth distribution of executives, and weaken the ability of asset efficiency to affect the polarization of wealth distribution between labor and capital. Therefore, ownership concentration reduces the objective influence of asset status on wealth distribution, and makes the subjective wealth distribution ability of enterprises occupy a certain influence.

Test Results of the Moderating Effect of Ownership Concentration.

Note. Authors’ own calculation.

, **, *represent significance at the significance level of 1, 5, and 10% respectively, and the Z-value of robust standard error is in parentheses.

Conclusion and Recommendation

Main Conclusions

According to the regression results, the improvement of asset efficiency and asset value has concentrated wealth distribution to asset managers and asset owners. The attributes of state-owned listed companies significantly weaken the polarization of wealth distribution, and therefore become an indispensable key force on the road to achieve income equality. When the cash holding is high, the workers can get a higher wealth distribution than the capital profit, and senior executives in the labor group can benefit more from wealth distribution than employees.

The findings of this study have shown that digital financial inclusion and equity concentration can regulate the intensity of the impact of asset status on the polarization of wealth distribution. Among them, digital inclusive finance can significantly reduce the impact of asset efficiency on the polarization of wealth distribution, which is of great significance for accelerating the rationalization of wealth distribution, building a human-centered enterprise modernization system, and accelerating the realization of common prosperity. Ownership concentration can also reduce the impact of asset efficiency on the polarization of wealth distribution. This is because the increase of ownership concentration means that major shareholders have a greater ability to intervene in the appointment of management, and they can subjectively influence the results of wealth distribution through the appointment and removal of the management.

There are still some shortcomings in the current study, which can be further discussed in the future. Exploring and trying to establish a wage incentive system compatible with the modern operation of different types of enterprises in the new era, and reducing the degree of labor mismatch within enterprises will also become important focuses of future research.

Policy Recommendations

The above research conclusions proved that asset status is one of the important factors affecting the realization of income distribution, and the following policy recommendations are put forward.

First of all, enterprises are encouraged to improve the income distribution system and implement equity incentive plans with wider coverage, so that workers can also benefit from asset appreciation and asset efficiency improvement. The implementation of equity incentive plan can significantly increase the labor income share of enterprises, and it is more obvious in non-state-owned enterprises and enterprises in the profit situation. Specifically, the implementation of equity incentive plans in non-state-owned enterprises is more conducive to increasing the share of labor income. A reasonable equity incentive ratio of senior executives can not only stimulate their behavior, but also play a certain constraint role. Moreover, the companies with higher cash holdings should pay more attention to rationality in income distribution to avoid irrational distribution due to abundant cash flow.

Second, it is necessary to develop digital inclusive finance, create a good financing environment, attract more capital into the region, and reduce the unequal distribution of wealth caused by capital scarcity. Furthermore, it is important to maintain the stable development of the capital market and implement the reform results such as the issuance system of the securities market, so as to prevent excessive fluctuations in asset prices from affecting asset value recognition and causing fluctuations in income distribution. Excessive volatility in asset prices can make markets unstable. An efficient and stable capital market can play a key role in motivating enterprises to innovate by ensuring innovation prospects, reducing financing costs and supervising managers.

Third, giving play to the complementary role of state-owned enterprises and the government in income distribution in the market economy and alleviating the imbalance of wealth structure is an effective means. Barkai’s(2020) research showed that in recent years, the share of labor’s salary in enterprises continues to decline with the continuous development of economy. The organic integration of a government with strong governance capabilities and state-owned enterprises that support social stability and the market is helpful for development.

Footnotes

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.

Data Availability

The brief data used to support the findings have been shown in the tables of the manuscript.