Abstract

In recent years, the essential roles of digital payment have gradually emerged. However, current research on digital payment adoption models rarely incorporates the outcomes of digital payment, and it also gives less consideration to rural residents. Considering these two issues as a research gap, this article establishes a unified digital payment use and credit availability model by extending the UTAUT2 framework in two aspects and applying it to China’s rural residents. The first extension is to add credit availability as an outcome variable of digital payment use. The second is to add two factors important to farmers, perceived riskiness and innovativeness, as constructs. Structural equation modeling is employed to analyze data collected from nearly 500 Chinese rural residents. The results show that almost 90% of rural residents have used digital payment. However, only a low proportion use it for many purposes or frequently. Rural residents’ digital payment use can increase credit availability. Performance expectancy, effort expectancy, social influence, price value, and innovativeness significantly and positively affect digital payment intention and behavior, thereby indirectly improving credit availability. However, the perceived risk does not influence digital payment adoption, possibly due to effective protective behaviors. In addition to the indirect effect, the results show that innovativeness also has a direct impact on credit availability.

Introduction

In China’s rural financial market, credit availability has been one of the long-standing difficulties. At the end of 2013, “to develop inclusive finance” was established as a national strategy in China in the Third Plenary Session of the 18th Central Committee of the Communist Party of China. Rural residents are an important target group of inclusive financial services. After years of efforts, the accessibility of financial services has continuously improved. However, there are still many problems in the area of the rural credit market, such as asymmetric information problems, high cost, unsustainability, mission drift, and high non-performing loan rate (Bi, 2024; G. He et al., 2018; J. He & Li, 2019; T. Sun et al., 2017; Yan et al., 2022). Since the introduction of the G20 High-Level Principles for Digital Financial Inclusion at the 2016 G20 meeting, the promotion of financial inclusion through digital technology has become a new theme. Digital inclusive finance, which uses digital technology for inclusive finance, has prominent advantages in reproducibility, availability, affordability, comprehensiveness, wide-coverage, deep service, and risk control (Gabor & Brooks, 2017; Xu et al., 2024), and therefore, it brings great hope and offers an efficient way to solve the financing difficulties in rural finance market (Huang & Tao, 2019; J. Li & Han, 2019). Digital payment is the entry to various financial services and is the most distinctive feature of digital inclusive finance (Gabor & Brooks, 2017; Ndung’u, 2018). As the foundation of digital inclusive finance, digital payment plays a crucial role in improving rural residents’ credit availability (Abdulai et al., 2024; Patra & Sethi, 2024). Theoretically, digital payment can alleviate the information asymmetry between rural residents and financial institutions (Annan et al., 2024; Sheng, 2021), enhance rural residents’ understanding of credit product information, decrease financial institutions’ requirements for collateral and guarantees, and reduce the cost to financial institutions of obtaining information (Barroso & Laborda, 2022; Mas, 2015; Ndung’u, 2018; Schmidt & Cohen, 2013). Therefore, the use of digital payment is crucial to improve rural residents’ credit availability and is of great importance for rural residents in financial distress; that is, improving credit availability may be an important outcome of digital payment use for rural residents.

In recent years, digital payment has grown significantly especially during and after the COVID-19 pandemic and hence the literature about its adoption and usage is gradually becoming richer (Annan et al., 2024; Behera et al., 2022; Hossain et al., 2020; Manrai et al., 2024; Susanto et al., 2022; Tang & Tsai, 2024; Wong et al., 2022). Since digital payment can be regarded as a kind of technology, the digital payment adoption model belongs to the technology adoption model. Technology adoption models are frameworks that systematically expound upon the influencing factors of technology adoption, including both use intention and use behavior. The most commonly used technology adoption models include Technology Acceptance Model (TAM), Unified Theory of Acceptance and Use of Technology (UTAUT) or Extended Unified Theory of Acceptance and Use of Technology (UTAUT2), Technology-Organization-Environment (TOE), Task Technology Fit (TTF), and Innovation Diffusion Theory (IDT) or Diffusion of Innovation (DOI; Hasan Emon, 2023).

TAM, proposed by Davis (1989), posits that perceived ease of use and perceived usefulness are the two primary factors influencing users’ adoption of technology. TAM demonstrates a certain level of universality in studying individual user technology adoption behavior; however, its application in specific research contexts tends to be overly simplistic (Lee et al., 2005). UTAUT proposed four constructs influencing user technology adoption, namely performance expectancy, effort expectancy, social influence, and facilitating conditions, in the base of TAM and simultaneously integrating the elements from the other seven models, and its explanatory power has significantly increased(Venkatesh et al., 2003). However, UTAUT primarily considers individual users within organizations. In the base of UTAUT, UTAUT2 added three more factors closely related to consumers—hedonic motivation, price, and habit—thereby extending UTAUT and can be used in consumer contexts (Venkatesh et al., 2012). Besides, UTAUT2 can achieve a high explanatory power of up to 74% due to its high comprehensiveness (de Blanes Sebastián et al., 2023).

In contrast to TAM, UTAUT, and UTAUT2, which primarily focus on the individual’s adoption behaviors, the Technology-Organization-Environment (TOE) Framework primarily focuses on the organization’s technology adoption behavior (Tornatzky et al., 1990

The Comparison of TAM, UTAUT, UTAUT2, TOE, TTF, and IDT(DOI).

Among the various technology adoption models, UTAUT2 has become a popular framework to examine technology use behavior in consumer contexts due to its strong comprehensiveness, high explanatory power, and particular suitability for consumer user groups (Tamilmani et al., 2021). Digital payment is mainly used in consumption situations, thus UTAUT2 is suitable for digital payment use (Bommer et al., 2023; Manrai et al., 2024; Moorthy et al., 2020) and will also be served as the basic framework of our study.

To adapt to different application scenarios, some studies have further enriched the influencing factors of UTAUT2: Migliore et al. (2022) incorporated the value barrier, risk barrier, tradition barrier, and image barrier. de Blanes Sebastián et al. (2023) added Perceived Security, Perceived Risk, and Trust. Z. Wu and Liu (2023) added perceived risk, personal innovativeness, uncertainty avoidance, and individualism. Liébana-Cabanillas et al. (2024) added perceived risk. The constructs added to the UTAUT2 model also give some spiration to our study.

With the vigorous development of digital payment, its various functions are gradually emerging. However, although the adoption of digital payment has attracted much attention, there is little literature incorporating the results of digital payment into the analytical framework. The outcomes of technologies are the important indexes determining whether these technologies are successful. Therefore, technology adoption models have been criticized for viewing usage as an end in itself rather than as a mean to realize its purpose (Dishaw & Strong, 1999; Y. Sun et al., 2009), hence many researchers recommend that the outcomes should be included in the models (Chittipaka et al., 2022; Tamilmani et al., 2021; Venkatesh et al., 2016). Table 2 shows some related studies. Y. Sun et al. (2009) added individual performance to the outcome of IT usage. Xiong et al. (2013) added the development of small business to the ICT adoption’s outcome. Jarvinen et al. (2016) added user indegree as the outcome of social networking service use. Buettner (2017) added job offer success as the outcome of social media use. Mishra et al. (2024) add the firm’s operational performance, innovational capability, and sustainability as the outcomes of blockchain technology adoption using the TOE framework. This literature provides some inspiration for our study. However, such models considering outcome variables are too few because information technology has so many kinds of outcomes. To the best of our knowledge, such literature on digital payment is even fewer, and only two pieces of literature are found: Oliveira et al. (2016) used intention to recommend as the outcome of the intention to adopt mobile payment and Gupta et al. (2022) treated the online shopping intention as the outcome of digital payment use. As the important roles of digital payment have gradually emerged, there is plenty of scope for this kind of outcome extension in digital payment adoption and use. Given that digital payment is likely to increase credit availability, this paper includes credit availability as an outcome variable in the analytical framework.

Literature That Incorporates Outcome Variables in the Information Technology Adoption Model.

In addition, current literature on digital payment adoption seldom uses rural residents as the research objective (Azman Ong et al., 2023; Shah & Bhatt, 2023). The small amount of such literature is shown in Table 3. Sharma and Sharma (2019) employ the UTAUT framework to analyze the digital payment adoption behavior in rural India, and its limitation is that UTAUT is only suitable for the organization context rather than the consumer context. Shah and Bhatt (2023) take ease of use, perceived security, perceived benefits, reliability, and user opinion as influence factors to analyze the digital payment usage in rural GUJARAT. However, it doesn’t have a systematic adoption model, which weakens the explanatory power. Both Manrai et al. (2021) and Azman Ong et al. (2023) use the relatively popular and highly explanatory UTAUT2 model and extend it with additional constructs, such as perceived credibility, perceived security, etc. Overall, the literature on adopting digital payment in rural areas is still quite limited. Some factors closely related to rural residents, such as innovativeness, have not been explored. Furthermore, the existing literature mainly focuses on India and Malaysia, with few studies on rural China. However, researching the digital payment adoption behavior of rural residents in China is also important: Firstly, rural residents’ digital payment usage rate is about 15% lower than that of urban residents in China (The Peoples Bank of China [PBC], 2022). Secondly, digital payment has special meaning for China’s rural residents in payment, credit and other financial areas due to the insufficient rural financial facilities (Kong & Loubere, 2021). Thirdly, the use rate of digital payment in China is among the highest in the world according to the World Bank’s Global Findex Database 2021, and the study of digital payment of China’s rural residents may bring some inspiration to other countries.

Literature on Rural Resident’s Digital Payment Adoption.

Since digital payment may have a special meaning for improving rural residents’ credit availability, we extend the digital payment use model by adding credit availability as an outcome variable. Considering the characteristics of rural residents, we further extend UTAUT2 model by adding innovativeness and perceived riskiness as influencing factors of the use of digital payment better to explain rural residents’ use behavior and credit availability. By constructing such an extended UTAUT2 model, we aim to answer the following two research questions:

RQ1: Under the framework of UTAUT2, which accommodates more complex relationships and leads to more robust conclusions, does digital payment adoption in rural areas positively impact credit availability?

RQ2: In rural areas, which factors directly or indirectly influence credit availability through digital payment adoption?

By answering the above two questions, we can provide policymakers with recommendations on how to develop digital payments and promote rural inclusive finance, particularly in rural credit.

The main contributions of the study are as follows: (1) We propose an integrated model in the context of digital payment use by adding credit availability as an outcome variable to the UTAUT2 model. Although there is existing literature on both the impact of digital payments on credit and the adoption of digital payments, no studies combine the two. Integrating these two areas can better capture the complex relationships between them and their influencing factors. (2) We further estimate the key factors that influence rural residents’ use of digital payment in China, which is helpful for China to improve rural residents’ digital payment and may inspire other countries.

This paper has six sections. Section 2 discusses the theoretical analysis and hypotheses and Section 3 focuses on variable explanations and data resources. Section 4 presents the data analysis and the results, and Section 5 is the discussion. Section 6 concludes.

Theoretical Model and Hypotheses

Mechanisms for UTAUT2 Factors to Influence Rural Residents’ Digital Payment Use

The well-known UTAUT2 model proposes seven constructs about technology behavioral intention in the consumer context: performance expectancy, effort expectancy, social influence, facilitating conditions, hedonic motivation, price value, and habit (Venkatesh et al., 2012). The original model is shown in Figure 1. In this section, we estimate the mechanism through which the factors influence rural residents’ use intention and the use behavior under the UTAUT2 model and take rural residents’ individual characteristics into account simultaneously.

Original UTAUT2 model (Venkatesh et al., 2012).

Performance expectancy is defined as the degree to which using technology will provide benefits to consumers in performing certain activities (Venkatesh et al., 2012). The benefit that rural residents can obtain from using digital payment is the convenience of payment (de Blanes Sebastián et al., 2023), and it may be more prominent than that for urban residents as the financial infrastructure in rural areas is usually poorer than that in urban areas (Kong & Loubere, 2021). Many studies under the UTAUT2 model verified that performance expectancy is one important construct to influence the intention to use the technology(Al-Adwan & Al-Debei, 2024; Shareef et al., 2024), including the field of digital payment (de Blanes Sebastián et al., 2023; Manrai et al., 2024; Z. Wu & Liu, 2023). Based on empirical findings from previous literature, hypothesize 1 is proposed.

Effort expectancy is the degree of ease associated with consumers’ use of technology (Venkatesh et al., 2012). It is empirically supported by Azman Ong et al. (2023), Shah and Bhatt (2023), and Das and Datta (2024) that the simpler the digital payment process, the more likely customers are to use digital payments. Most rural residents are not familiar with digital payment due to the lack of digital literacy in the context of the digital divide (de Clercq et al., 2023; Goncalves et al., 2018; Peng & Dan, 2023; Purbo, 2017; Shenglin et al., 2017). They need to learn to use digital payment and may pay more effort to some extent. When residents feel it is easy or they can acquire this knowledge with less effort, they may be more willing to use digital payment. Thus we propose Hypothesis 2.

Social influence is the extent to which consumers perceive those important others, such as friends, relatives, or administrative staff of the corresponding technology, believe that they should use a particular technology (Venkatesh et al., 2012). Previous literature confirms that the perception or opinion of important surrounding people does affect customer’s adoption of digital payments (Al-Okaily et al., 2024; de Blanes Sebastián et al., 2023). China’s rural areas are typically relation-based societies (Qiu et al., 2020; X. Wu & Yuan, 2023), and therefore the social influence may be more significant. When the social powers around rural residents believe they should use digital payment, they are more likely to be willing to use it. Thus we propose Hypothesis 3.

Facilitating conditions refer to consumers’ perceptions of the resources and support available to perform a behavior (Venkatesh et al., 2012). The use of digital payments requires various hardware resources, software and support facilities available to help users understand how to use or to seek assistance (de Blanes Sebastián et al., 2023). Gupta et al. (2022) and Al-Okaily et al. (2024) confirm that facilitation conditions have a positive effect on technology adoption. The better the facilities and related services for digital payments in rural areas, the more willing rural residents are to use them. At the same time, the perceived facilitating conditions will also influence the use behavior of digital payment directly (Venkatesh et al., 2012). Thus we propose Hypothesis 4 and Hypothesis 5.

The price value is the consumers’ cognitive tradeoff between the perceived benefits of the applications and the monetary cost of using them (Dodds et al., 1991; Venkatesh et al., 2012). It is empirically supported by Gupta et al. (2022) and Al-Okaily et al. (2024) that under a certain level of benefits, the lower the cost of using digital payments, the more willing customers are to adopt them. Compared with urban residents, rural residents’ income is lower (Y. Gao et al., 2014; Tao et al., 2024), and they are more concerned about the price or monetary costs of using digital payment. The greater the perceived benefits from using digital payment than the monetary costs paid, the higher the price value. That is, the higher the price value, the more willing rural residents are to use digital payment. Thus we propose Hypothesis 6.

The original constructs of UTAUT2 also include habit and hedonic motivation. However, a large amount of UTAUT2-based studies do not include habit, as habit is difficult to form in the early stages of technology adoption due to the limited duration of use (Das & Datta, 2024; Tamilmani et al., 2019). Since digital payment is still a new concept in China’s rural areas and is not established enough to form habits, this study also does not include the construct of habit. Hedonic motivation under UTAUT2 is suitable for many kinds of information technology, such as personal computers and mobile phones. However, the hedonic motivation of digital payment is not obvious. Therefore, this study does not include these two constructs.

According to Fishbein and Ajzen-(1977), behavior intention can predict voluntary behavior. Digital payment by rural residents is voluntary, not coercive behavior, and intention to use digital payment will therefore be a predictor of their use of digital payment, which is verified by Azman Ong et al. (2023) and Manrai et al. (2024). Thus we propose Hypothesis 7.

Mechanisms for Other Factors to Influence Rural Residents’ Digital Payment Use

UTAUT2 does not consider consumers’ innovativeness and perceived riskiness. According to Hirschman (1980), innovativeness is people’s desire to find something new and different. People’s daring to try new technologies is considered to be a manifestation of innovativeness (Slade et al., 2015). Education or knowledge level is treated as one factor influencing innovation (Eryigit, 2020; Sáenz et al., 2023). The higher people’s level of knowledge, the better they can understand the benefits new products bring, master the use of innovative products, and manage the risks that new products may bring. Another important influencing factor is income (Eryigit, 2020; Thakur & Jasrai, 2018). High-income groups are better equipped with the financial resources and opportunities to experiment with new products or behaviors. Besides, they tend to experience higher levels of life satisfaction, which fosters a sense of youthfulness and, consequently, increases their likelihood of engaging in novelty-seeking behaviors (Eryigit, 2020). Z. Wu and Liu (2023) have proved that innovativeness is a factor that positively influences digital payment adoption. Compared with urban residents, rural residents’ innovativeness may not be salient due to their lower education and lower income (Tao et al., 2024; Xiang & Stillwell, 2023). Therefore, rural residents’ innovativeness may be of special importance. If rural residents’ innovativeness is higher, then the residents are likely to be willing to try digital payment. Thus we propose Hypothesis 8.

Perceived riskiness refers to the uncertainty or anxiety about the possible adverse consequences of an action perceived by the consumer (Mandrik & Bao, 2005). New products are usually considered inherently risky. While digital payment is essentially a new concept for rural residents and risk should be considered (Manrai et al., 2024). When digital payment is used, the payer and the payee are separated in time and space, which will make the user feel insecure. In addition, the wireless network used to transmit digital payment signals may have some defects in the process of development and is vulnerable to some insecurity factors (such as hacker attacks). As the digital payment environment is complex and different service providers may use different technologies, users may feel confused and are likely to worry about the risks caused by operational errors. Privacy breaches are often regarded as an important risk for consumers when they use online transaction payment methods (Chauhan, 2024; Park et al., 2019; Sahi et al., 2022). The negative effects of perceived riskiness on digital payment have been validated in many studies (Azman Ong et al., 2023; Liébana-Cabanillas et al., 2024; Oliveira et al., 2016; Shin, 2010; Yang et al., 2012; Slade et al., 2015). Compared with urban residents, rural residents are more sensitive to risk for (1) their lack of ways to identify and mitigate risk due to lower education and (2) their insufficient risk resilience due to lower income (Tao et al., 2024; Tian, 2005; Xiang & Stillwell, 2023). If rural residents feel that the risk of digital payment is large, their willingness to use digital payment will be reduced. Thus we propose Hypothesis 9.

Mechanisms for Digital Payment Use to Influence Credit Availability

From the perspective of financial service suppliers, digital payment enables customers to get more opportunities to use financial services, which in turn promotes suppliers to obtain more deposits and thus increase their lending capacity (Abdulai et al., 2024; Ndung’u, 2018). Digital payment technology allows suppliers to acquire the digital traces of users, which helps them to understand customer information better, thereby reducing the transaction costs of supplying credit products and reducing interest rates (Patra & Sethi, 2024; Schmidt & Cohen, 2013), and meanwhile reducing financial institutions’ requirements for mortgage guarantees (Ndung’u, 2018; Sheng, 2021). From the perspective of the financial service users, digital payment promotes users to establish contact with financial institutions, which greatly helps users learn more about financial products and can also reduce the transaction costs for customers to obtain financial services, thereby increasing their willingness to use financial products, such as applying for a loan (Barroso & Laborda, 2022; Mas, 2015). While the greatest obstacles for rural residents to obtain credit are the high interest, unawareness of what credit is available, and the lack of collateral (Zheng, 2019), digital payment can play an active role in overcoming these three obstacles. A few recent empirical studies have also confirmed that digital payments can enhance access to credit (Abdulai et al., 2024; Patra & Sethi, 2024). Therefore digital payment can help alleviate financing difficulties or improve credit availability for rural residents. Thus we propose Hypothesis 10.

Mechanism for Innovativeness to Influence Credit Availability

One manifestation of innovativeness is that people dare to try new things (Slade et al., 2015). For a long time, rural residents have mainly resorted to informal finance when they lack capital (M. Gao & Hu, 2022; Turvey et al., 2010), and as a result, formal credit, especially from online platforms, can be regarded as a new concept for most rural residents. Salvi et al. (2024) have verified that an individual’s innovativeness has a positive influence on the intention to finance using equity crowdfunding. Therefore, rural residents with higher innovativeness may be more likely to try to use formal credit. Thus, we propose Hypothesis 11.

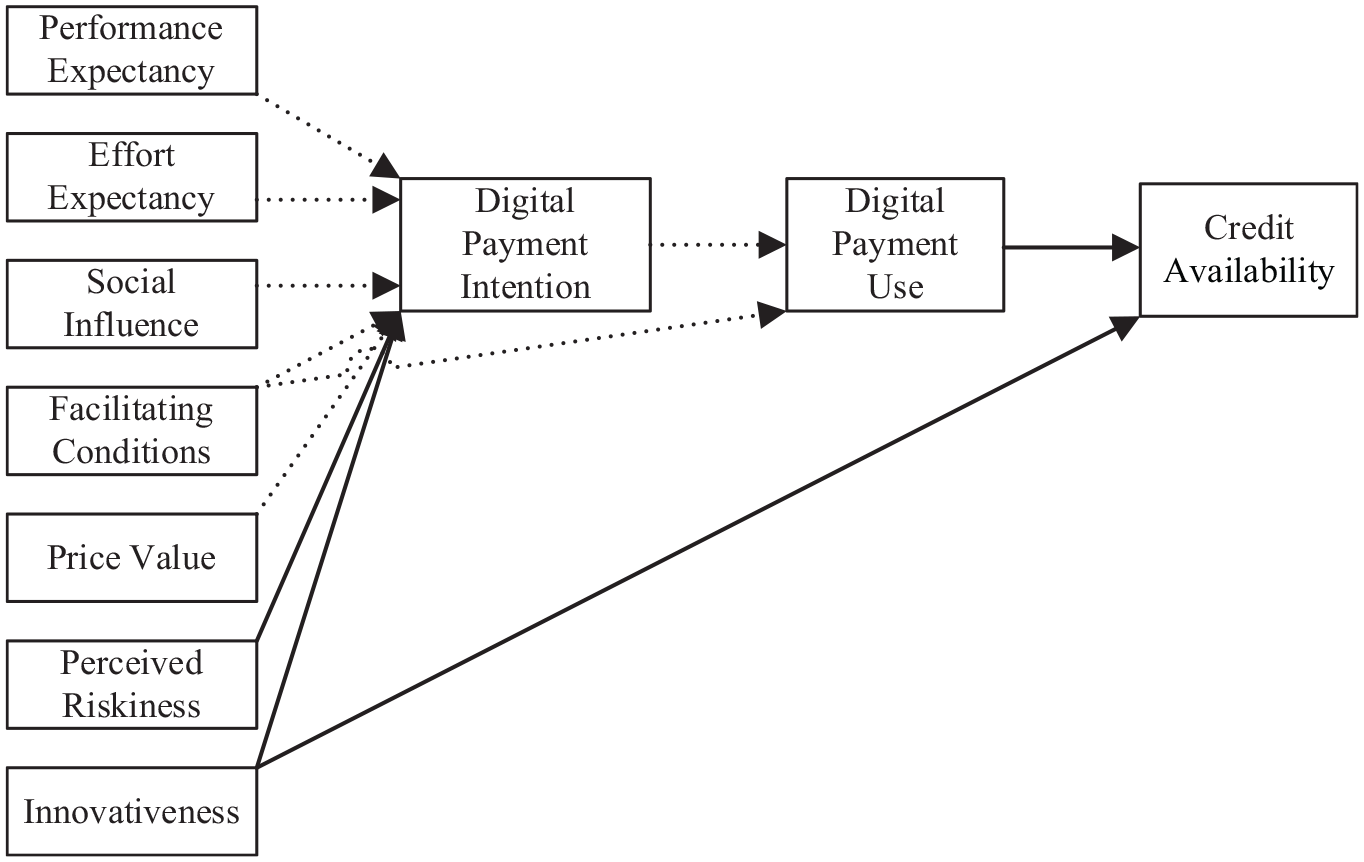

In summary, using the existing constructs from UTAUT2 (performance expectancy, effort expectancy, social influence, facilitating conditions, price value), two other constructs (innovativeness, perceived riskiness) and the credit availability as the outcome variable of digital payment use following digital payment intention, we form the unified model of digital payment use and credit availability, shown in Figure 2. The dotted lines show the parts from the UTAUT2 model, where performance expectancy, effort expectancy, social influence, facilitating conditions and price value influence digital payment use behavior through use intention, and facilitating conditions also influence digital payment use behavior directly. The solid lines are the extension based on UTAUT2, which shows that two constructs (innovativeness and perceived riskiness) and one outcome variable (credit availability) are added. Specifically, performance expectancy, effort expectancy, social influence, facilitating conditions, price value, innovativeness, and perceived riskiness influence credit availability indirectly through digital payment intention and use, and innovativeness influences credit availability directly. Using this extended UTAUT2, we aim to find ways to improve credit availability for rural residents from the perspective of digital payment usage.

Basic unified model of digital payment use and credit availability.

Method and Materials

Questionnaire

A survey was designed using constructs and scales from the literature to test the theoretical constructs and conducted in China’s rural areas. Our target population was rural residents over the age of 18. Specifically, the scales of performance expectancy, effort expectancy, social influence, facilitating conditions, and price value are adapted from Chen and Tang (2006), Venkatesh et al. (2012), and Oliveira et al. (2016). Facilitating conditions are deleted due to collinearity with performance expectancy. Therefore, we do not report the scale for facilitating conditions here. Perceived riskiness is adapted from Lu et al. (2011), Yang et al. (2012), and Slade et al. (2015). Innovativeness and digital payment intention are adapted from Oliveira et al. (2016). Digital payment use is adapted from Venkatesh et al. (2003), Chen and Tang (2006), and Venkatesh et al. (2012). Following Black and Strahan (2002) and Mi et al. (2018), credit availability is the number of times a rural resident obtained credit in the second half of 2018. All items except those for digital payment use are measured using a five-point Likert scale, with the anchors being 1 = “strongly disagree” and 5 = “strongly agree”. Digital payment use is measured using the quantity of the categories of digital payment and the frequency of digital payment per month.

The questionnaire was originally created in Chinese and used for the field investigation. Finally, it was translated into English by language professionals. The contents of the questionnaire are shown in Appendix 1. The questionnaire was pilot-tested in January 2019 with a sample of 30 subjects from two villages in Shandong Province: Zhangjia Village, Gaoguanzhai Township, Zhangqiu District in Jinan, and Chenzhuang Village, Xiaoli Township, Jiaxiang County in Jining. The results show that the scales are reliable and valid. The data from the pilot test was not included in the formal investigation.

Mobile payment is the main form of digital payment in China’s rural areas, according to the People’s Bank of China (PBC, 2019, 2022). Therefore, digital payment in this questionnaire mainly refers to mobile payment. Mobile payment is used in various domains (e.g., the purchase of commodities and services, investments, the payment of salary and dividends, and so on) through mobile communication equipment, such as mobile phones and laptops.

To avoid the possible reverse causality that credit availability may affect digital payment use, we measure these two variables using the different time periods in the questionnaire. For credit availability, we use the second half of 2018 as the time period, while for digital payment use behavior, we use the period from the first start of digital payment use behavior to the end of 2018. As the first start may be much earlier than mid-2018 and payment habits tend to exhibit a high level of persistence (Liu et al., 2019), the period of digital payment use behavior can be roughly treated as earlier than that of credit availability and the potential reverse causality can be solved to a large extend.

Samples and Data Collection

The sample area in this study is located in Shandong Province of China. According to the China National Bureau of Statistics, Shandong Province has 38.54 million rural residents in 2019, accounting for 38.13% of the total province population, which is similar to the proportion of the whole China’s rural population in 2019 of 37.29%. Although the rural population is decreasing with the development of urbanization, there are still 36.67 million rural population in 2021 in Shandong Province, accounting for 36.05% of the total province population, which is also similar to that proportion of the whole China’s rural population in 2021 of 35.28%. Shandong Province is a large agricultural province. Its gross agricultural output value has ranked first in China for many years, and its agricultural industry is also highly diversified. Thus, the study of the behavior of rural residents in Shandong Province has a certain degree of representativeness.

This study adopts multistage sampling, which is a probability sampling method. The main advantage of this method is its ability to effectively handle large-scale and widely distributed populations, ensuring the representativeness and operability of the sample while saving costs and time (Feng, 2021). In February 2019, we carried out the formal investigation after that trial one in January 2019, mentioned in the above “questionnaire” part. Among the 17 prefecture-level cities in Shandong Province, two counties (cities or districts) were randomly selected in each prefecture-level city, 1 to 2 natural villages were randomly selected in each county (city or district), and 15 rural residents (in different households) were selected from each sample village. During the conducting of the survey in each village, the enumerators were instructed to consult the village head to understand the age distribution of the adults in the village. Based on this age distribution, the approximate number of individuals to be surveyed in each age group (four age groups shown in Table 4, a total of 15 persons) was determined, and random sampling was then conducted within each age group. This approach ensures coverage of all demographic groups and helps mitigate the issue of overrepresentation to some extent. A total of 525 questionnaires were distributed, and 518 questionnaires were returned. Due to the missing sensitive information such as income and the misunderstanding of reverse questions in some questionnaires, a total of 470 valid questionnaires were finally obtained, with an effective response rate of 90.73%.

Sample Characteristics.

Note. Types of digital payment use include (1) purchase of commodities or services, (2) investment, (3) salary or dividend payment to others, and (4) other kinds of payment, such as alimony to children or parents. Income is the average annual income over the past 3 years.

Data

The sample characteristics are shown in Table 4. From the view of individual characteristics, 55.74% of the respondents were female. 25.96% were aged 26 to 35 years old and 32.77% were 36 to 45 years. 42.55% had an education level of middle school and 40.21% had an education level above high school. About 44.26% of the sample had an annual income of RMB 10,000 to 50,000 in the past 3 years, and 30.85% had an income of RMB 50,000 to 100,000 in the past 3 years. Only 12.13% of the respondents reported never using digital payment; therefore, 87.87% (100% minus 12.13%) had used digital payment. About half (51.70% = 14.47% + 37.23%) of the respondents used digital payment more than 10 times per month, and only 37.23% used it more than 16 times monthly. From the perspective of the aim of digital payment use behavior, 82.13% of the respondents report they use one type of digital payment, and only 5.74% (3.83% + 1.91%) use two or more types. From the perspective of credit availability characteristics, in the second half of 2018, 15.74% of the sample had loans, of which 4.26% had loans three times or more. The sample characteristics show that most rural residents have gradually accepted and used digital payment with the improvement of education and income in rural areas. The popularization of digital payment in rural areas may greatly reduce the cost of rural residents’ access to financial resources, help financial institutions obtain rural residents’ information, and improve credit availability to rural residents. It should be noted that, however, the proportion of rural residents who use digital payment for multiple purposes and with high frequency is still low.

Data Analysis Technique

Structural equation models (SEM) combines the methods of confirmation factor analysis and path analysis to overcome the limitations of traditional multivariate data analysis techniques (Hair et al., 2021). Confirmation factor analysis (measurement model) can be used to estimate the latent variables. And path analysis (structure model) can be used to analyze the multiple and complex causal relationships (Fan et al., 2016). The first advantage of SEM is that it can accommodate latent variables corresponding to hypothetical constructs to reflect a continuum not directly observable and cope with multiple and complex causal relationships. Another advantage is that it can estimate various relationships simultaneously and provide an overall fit and make, providing a summary evaluation of multiple equations, while models similar to SEM, such as multiple linear regression, can only test each equation individually (Kline, 2015; Tomarken & Waller, 2005). This paper discusses the attitude and behavior of digital payments adoption, credit availability, and various influencing factors, which inevitably involve some unobservable variables and complex causal relationships. Given the advantages of SEM, this paper chooses SEM to illustrate the model.

Data Analysis and Results

In this study, structural equation models and Mplus 7.4 software are used for data analysis. Kline (2015) recommends that data used for analysis using structural equation models should have at least 200 observations, so the sample size in this study is statistically adequate. The data analysis is carried out in two steps: the first step is to test the measurement model and examine the reliability and validity of the latent variables’ scale; the second step is to test the structural model, examining the causal relationship between latent variables.

Measurement Model

In this study, confirmatory factor analysis (CFA) was conducted using 8 latent variables and 28 measurement items. The number of loans in the second half of 2018 was used as the proxy of the variable of credit availability (CA), so CFA did not include credit availability (CA), and the results are shown in Table 5. According to Fornell and Larcker (1981), items that have a loading less than 0.7 should be removed from the model, and eventually a total of four items were deleted: PE4—Using mobile payment would enable me to conduct tasks more conveniently, EE4—It would be easy for me to become skillful at using mobile payment, INN3—In general, I am hesitant to try out new information technologies, and PR4—I feel secure sending sensitive information across using mobile payment systems. The modified model fits well (χ = 730.777, p < .001, χ2/df = 2.320; CFI = 0.963; TLI = 0.956; RMSEA = 0.053; SRMR = 0.045).

Constructs, Items, and Factor Loadings.

Note. Perceived Riskiness (PR) is a reversed item. Facilitating conditions are deleted due to collinearity with performance expectancy.

p < .01.

This study evaluates the construct reliability using composite reliability (CR). As shown in Table 6, the CR values for all the constructs range from 0.755 to 0.956 and are higher than the threshold value of 0.7 (Fornell & Larcker, 1981), which suggests that the constructs are reliable. The average variance extracted (AVE) and the factor loadings of the items are used to test the convergent validity. The AVE values of the latent variables in Table 6 range from 0.610 to 0.879, all higher than the threshold value of 0.5 (Fornell & Larcker, 1981). Moreover, except for PAYQ (the quantity of the categories of digital payment), the factor loadings of the items are higher than 0.7, and the p value shows that these results are significant at the level of .001. Thus we can conclude that the measurement model has a good convergent validity.

Composite Reliability, Convergent Validity, and Discriminant Validity of the Constructs.

Note. The bold numbers on the diagonal are the square root of AVE, and the lower triangle is the Pearson correlation coefficient matrix of the constructs.

Discriminant validity of the constructs is evaluated using Fornell-Larcker criteria, which states that the square root of AVE should be greater than all correlations between each pair of constructs. As shown in Table 6, there is no case where the correlation coefficient of the two constructs is greater than the square root of AVE, so the scales have good discriminant validity.

We examined the potential common method bias (CMB) by using three statistical analysis methods. First, Harman’s single factor test was used to examine the extent of CMB. The unrotated principal components factor analysis indicated that 39.34% of the total variance was explained by one single factor, which is less than the 50%, suggesting that CMB was not a critical issue (Podsakoff et al., 2003). Second, CFA single factor method test was conducted, and the results showed that the model fitness was not up to the standard (CFI = 0.507, TLI = 0.460, RMSEA = 0.196, SRMR = 0.124). Third, the Unmeasured Latent Method Construct (ULMC) method by including a common method factor was conducted, and the results showed that the model fitness became worse (ΔCFI =is −0.063, ΔTLI =is −0.071, ΔRMSEA =is 0.037, ΔSRMR =is 0.228), which means that the model fitness became worse. Thus common method bias can be regarded as nonexistent. In addition, the presence of multicollinearity is estimated through the variance inflation factor (VIF). All the VIF values are below 3.3 (Cenfetelli & Bassellier, 2009), indicating that the multicollinearity problem is nonexistent.

Hypothesis Testing

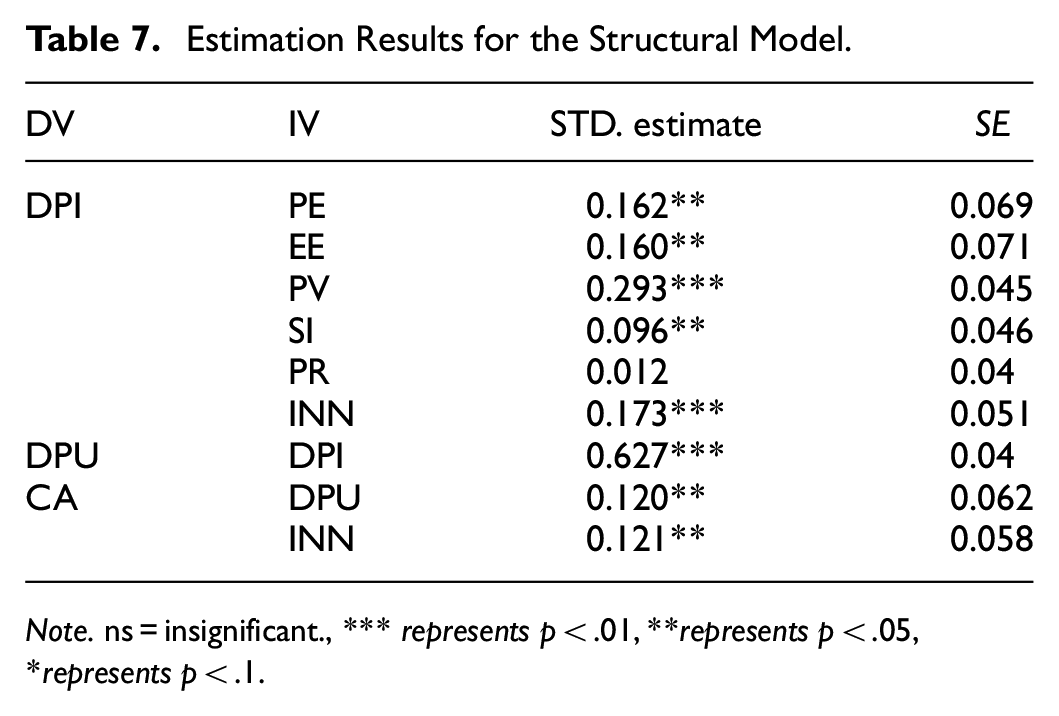

The results of the structural model are shown in Table 7 and Figure 3. The model fitness is robust (χ2 = 640.855, p < .001, χ2/df = 2.543; CFI = 0.958; TLI = 0.950; RMSEA = 0.057; SRMR = 0.059). The results state that PE (β = .162, SE = 0.069, p < .05), EE (β = .160, SE = 0.071, p < .05), PV (β = .293, SE = 0.045, p < .01), SI (β = 0.096, SE = 0.046, p < .05) and INN (β = .173, SE = 0.051, p < .01) have positive impacts on digital payment use intention (DPI). Hence, hypotheses 1, hypotheses2, hypotheses 3, hypotheses 6, and hypotheses 8 are supported. Among these constructs, PV has the most prominent positive influence, followed by INN. The impact of perceived riskiness (PR) on the digital payment intention (DPI) is not significant, so hypothesize 9 is rejected. Our model also tests the influence of digital payment intention (DPI) on digital payment use (DPU), which is significantly positive (β = .627, SE = 0.04, p < .01), and hypothesis 10 is supported. The influence of digital payment use (DPU) on credit availability (CA) is shown to be statistically positive (β = .120, SE = 0.062, p < .05), thereby supporting hypothesize 10. Lastly, innovativeness (INN) is found to have a positive impact on credit availability (CA; β = .121, SE = 0.058, p < .05), and then Hypothesis 11 is supported.

Estimation Results for the Structural Model.

Note. ns = insignificant., ***representsp < .01, **representsp < .05, *representsp < .1.

Estimation results for the structural model in graph.

Discussion

This study establishes an integrated model by incorporating digital payment use and credit availability. Based on the UTAUT2 model, we employ credit availability as an outcome variable of digital payment use, and add perceived riskiness and innovativeness as two influencing factors. The findings reveal that PE, EE, PV, and SI affect digital payment intention positively and significantly among China’s rural residents. Specifically, performance expectancy has a significant influence on digital payment intention, which is consistent with the previous study (Azman Ong et al., 2023; Shah & Bhatt, 2023). It implies that the greater the benefits rural residents gain from digital payment, such as convenience and speed, the more likely they are to be willing to use digital payment. China’s government attaches great importance to the construction of a digital countryside. “Digital Countryside Development Strategic Outline” in 2019, “Digital Countryside Development Action Plan” in 2022, and “2,024 Digital Countryside Development Work Points” were released successively, proposing key tasks for rural digital construction in areas such as digital infrastructure, rural digital economy, and rural digital technology. As a result, as of June 2024, China’s rural internet penetration rate has reached 66.5% (Zhang, 2024). The gradual improvement of digital infrastructure has enabled more rural residents, especially those in remote areas with limited financial infrastructure, to access convenient, and efficient financial payment services. Moreover, digital payment scenarios in rural areas are increasingly diverse, covering various fields such as food, housing, transportation, tourism, shopping, entertainment, and healthcare. Consequently, rural residents are increasingly benefiting from digital payments, which has driven the continuous increase in the usage rate of digital payments in China.

Similarly, effort expectancy has a significant positive impact on digital payment, which is consistent with the conclusions of the literature (Azman Ong et al., 2023; Shah & Bhatt, 2023). This shows that ease of use is vital for rural residents to accept digital payment. “The plan to facilitate the development of the digital economy in the 14th Five-Year Plan period (2021–2025)” rolled out by China’s State Council proposed to enhance national digital literacy and skills, and many effective measures have been implemented. Payment platforms have also continuously simplified and optimized operation processes to make the payment experience more seamless and efficient. Digital payment methods have gradually diversified, evolving from early QR code payments to “tap-to-pay,” followed by facial recognition, palm scanning, iris recognition, and voiceprint payments (B. Li, 2024). Therefore, the use of digital payments is becoming increasingly simple, continuously driving the growth of digital payment adoption in China.

Social influence also has a significantly positive impact on digital payment, which is consistent with Manrai et al. (2021, 2024), and Azman Ong et al. (2023). China’s natural village is usually established by relations, clans or geography and thus the relationship or connection among residents is close (X. Wu & Yuan, 2023). In this typical relationship-based society, the attitudes of people around them toward digital payment will have an important impact on rural residents’ adoption of digital payment.

Price value is also one of the crucial factors affecting rural residents, consistent with previous literature (Gupta et al., 2022; Oliveira et al., 2016), and among all constructs, price value has the greatest impact. It shows that rural residents are susceptible to the cost of using digital payment, which is in line with the relatively low income of rural residents. However, information costs in China have continuously decreased. During the “13th Five-Year Plan” period, from 2016 to 2020, the average fee for fixed broadband and mobile data decreased by over 95% (Pan, 2020). Besides, China has a wide range of smartphone brands, and the competition has become increasingly intense, leading to a continuous price drop. This has made it more likely for rural residents to choose a suitable phone. Overall, the cost of using digital payments for rural residents has been decreasing, which has led to an increase in their willingness to adopt digital payments.

This study extends the UTAUT2 model with two more constructs, INN (Innovativeness) and PR (Perceived Risk). Innovativeness has a significant impact on the intention to use digital payment for China’s rural residents, consistent with Jackson et al. (2013) and Oliveira et al. (2016). The results show that the coefficient of innovativeness is the second largest among all constructs, which indicates that innovativeness is of special importance to China’s rural residents.

The impact of perceived riskiness on digital payment intention is not significant, consistent with Al-Saedi et al. (2020) and Z. Wu and Liu (2023), indicating that rural residents who use digital payment do not feel that digital payment is safe. In fact, some rural residents feel that there are many security problems in using digital payment, but they still use it. In other words, among the rural residents who use digital payment, some feel safe, but some may not feel safe. Then why do the residents who don’t feel safe still use digital payment? According to Chauhan (2024), protective behaviors can weaken the negative impact of perceived risk on the use of digital payments. In China, one protective measure is the vigorous promotion of cybersecurity education and publicity through websites, TV programs, and even the village notice board, focusing on how to handle risks when they arise. To some extent, this has alleviated concerns about potential dangers for digital payment users. Another protective measure is the free account safety insurance related to digital payments (de Blanes Sebastián et al., 2023). Alipay and WeChat are the two main digital payment platforms that account for 96.5% of the Chinese mobile payment market and 96.4% of the internet payment market in 2023. Both these two platforms provide account safety insurance freely to all users. We take Alipay account safety insurance as an example. The scope of compensation is all direct losses in the Alipay account due to theft. The number of payouts is unlimited. The compensation amount is up to 1 million RMB, about 50 times the per capita income of rural residents in 2022, accumulatively within a natural year. WeChat is roughly the same. Due to free insurance, rural residents may feel that the consequences are not so serious even if there are risks, dramatically improving their tolerance to risks.

In addition, our study also extends the UTAUT2 model with an outcome variable, credit availability (CA). The results show that digital payment use has a significant positive impact on credit availability, which supports most previous theoretical and empirical findings that digital payment can effectively promote the availability of credit financial services in rural areas (Abdulai et al., 2024; Mas, 2015; Ndung’u, 2018; Schmidt & Cohen, 2013). Digital payment can reduce the transaction cost for financial institutions to obtain rural residents’ information, lower collateral requirements for rural residents, enable rural residents to get more opportunities to learn about credit, and thereby increase rural residents’ credit availability, which is of great significance in the context of rural financing being difficult and expensive for a long time.

Besides, the innovative characteristic of rural residents also has a significant positive impact on the use of credit. The results show that most rural residents’ purpose of using credit is consumption. Among the rural residents who obtain loans, 79.73% use loans for consumption. Consumer credit is mainly acquired through online platforms, such as Ant Huabei and Jingdong Baitiao, and obtaining credit through online platforms is obviously a novelty. In addition, under the situation of the low availability of rural finance for a long time, credit from formal finance is still new to most rural residents, so the innovative characteristics of rural residents have shown a significant positive impact on the amount of credit.

Although the survey was conducted in 2019, it is still valuable today. (1) The study in a normal situation before the pandemic is valuable. The isolation measures and the economic downturn during the pandemic led to anomalies in digital payment behavior, financial information such as income and consumption, and credit behavior. For instance, digital payments may have shifted from a voluntary behavior to a mandatory one, thus affecting the functioning of influencing factors. Or financial institutions may be compelled to lend for policy reasons. These anomalies are unlikely to disappear immediately after the pandemic ends and may persist for some time. Since our data was collected before the pandemic, when digital payment and credit behaviors were relatively normal, it remains valuable despite its earlier timeframe. (2) The study on digital payment adoption is still needed. Firstly, according to the latest data from the World Bank’s Global Findex Database last updated in 2021, still 65% of respondents in low-income countries have never used digital payments. Considering the relative stability of payment habits and the average annual growth rate of approximately 2.9% in digital payments from 2014 to 2021(Annan et al., 2024), it can be inferred that in the foreseeable future, there is still a significant proportion of the population that does not use digital payments. Secondly, new digital payment modes such as “tap,” facial recognition, palm scanning, iris scanning, and voiceprint payments have emerged but have not yet been widely accepted (B. Li, 2024). Thirdly, to obtain more digital traces, digital payment operators not only focus on whether customers use digital payments but also on the use frequency and scenarios that still have significant potential for improvement (L. Li, 2024). Lastly, the intensifying competition makes digital payment operators try to attract customers to use their own platforms (L. Li, 2024).

Theoretical Contributions

Previous research on the use of digital payment seldom considers the outcome. However, to consider the outcome will make the use of digital payment more meaningful. Besides, previous related literature pays little attention to rural areas. In rural areas with relatively weak financial infrastructure, digital payment that rely less on traditional financial branches will be of greater significance to rural residents. Considering these two shortcomings and combining them with the expectation that digital payment may improve rural residents’ credit availability, this paper introduces credit availability as an outcome variable in the digital payment adoption model UTAUT2, with rural residents as the objects of observation. Correspondingly, the first contribution of the study brings a relatively new direction in extending the digital payment adoption model by adding outcome variables. The second contribution is that it expands the applications of the UTAUT2 model in the context of rural residents. The third contribution is that the study’s results broaden the ways to improve rural financial services, including payment and credit. The last contribution is that this study may give other countries some inspiration on the aspects of rural residents’ digital payment adoption and credit availability.

Practical Implications

The results of this study show that rural residents’ digital payment use significantly promotes credit availability. Performance expectancy, effort expectancy, social influence, price value, and innovativeness all significantly and positively affect digital payment intention and behavior, thereby indirectly improving credit availability. In addition to indirectly affecting credit availability through digital payment intention and behavior, innovativeness has a positive and significant impact on credit availability directly. Since rural residents’ digital payment use can promote credit availability, it is necessary to encourage rural residents to use digital payment more, that is more often and in more situations. At the same time, financial institutions need to better use the information obtained from the digital traces left by digital payment.

Several approaches can be used to encourage rural residents to use digital payment more. First, continue to strengthen the construction of rural digital infrastructure. It is necessary to improve the breadth and depth of network coverage to ensure that rural areas have access to high-speed and smooth network services. Besides, it needs to accelerate the expansion of 5G networks into rural areas and enhance the level of mobile internet applications. Second, strengthen cross-industry integration and encourage deep collaboration between digital payment, finance, technology, business, and other sectors to expand more new application scenarios to improve the performance expectancy of digital payment. Third, continue to promote the simplification of digital payment, such as increasing the use of near-field transactions, to reduce the effort expectancy of rural residents, which is very important for rural residents, especially the older. At the same time, continue to enhance rural residents’ digital skills and literacy through education or training, especially refined and detailed guidance, to reduce the difficulty of using digital payments, thereby lowering their effort expectancy. Fourth, continue to reduce the cost of digital payment, both the price of hardware like mobile phones and the network use fee, to improve the price value. Meanwhile, continue to raise rural residents’ income to decrease their price sensitivity. Fifth, increase the publicity about digital payment in rural areas through various channels to enhance the overall understanding of digital payment among rural residents, thus expanding digital payment’s social influence. Sixth, promoting the concept of mass innovation to enter rural areas will be conducive to fostering rural residents’ individual innovativeness, which thus helps them try digital payment and various types of credit. Lastly, continue improving protective measures, such as insurance, rights protection, remedial actions, etc., in case of risks or losses.

As digital payment can increase credit availability, three ways are recommended to ensure financial service entities better use the traces left by digital payment. First, financial service entities are encouraged to enrich the digital payment scenarios, which is consistent with the suggestions about encouraging rural residents to use digital payment. Digital payment is the entry to various financial services, and in the context of the digital economy, digital payment has become a battleground for financial institutions. Having more use scenarios means financial service entities may know more about rural residents’ credit status, income status, and capital use status. Second, financial institutions must conduct efficient data mining after obtaining the traces left by various digital payments. Financial institutions need to increase investments in data mining, such as fintech and big data algorithms. Third, competition should be encouraged in the field of digital payment. Monopolization of this market would be detrimental to the diversification of application scenarios and, more importantly, would lead to higher interest rates on credit from these platforms, which would counter the “affordability” of financial inclusion.

These suggestions are also applicable to other countries to some extent. Countries with underdeveloped digital infrastructure or lacking mature digital service providers may seek international support and collaboration in cases where they don’t have the domestic capacity to foster these services.

Limitation and Scope of the Future Research

This study has some limitations and thus provides impetus for future improvements. Firstly, this study has not yet considered the moderating effects of demographic characteristics of individuals, such as gender, age, education level, and other factors, which might provide more detailed results that need to be further enriched and improved in future research. Secondly, for the factors that affect both digital payment adoption and credit availability, only one factor, innovativeness, is considered in this study. Still, there are many other factors, such as income and wealth. More such factors can be added to future research to increase the model’s explanatory power. Thirdly, for the outcome variable, this study only considers credit availability. However, digital payment can bring different outcomes, such as consumption and transaction convenience, which can be further estimated in future studies. Lastly, this study mainly focuses on rural residents in Shandong Province of China. Although the behavior of rural residents in Shandong Province can be somewhat representative of the whole country due to the similarity of the proportion of the rural population in Shandong Province to the whole country, the fact that its gross agricultural output value is the highest in the entire country, and the high diversity of its agricultural industry, the study cannot be fully representative of the whole country because of the fact that there are always differences among regions. Therefore, future studies can be based on rural residents across the whole of China to draw more general conclusions.

Conclusions

As digital payment booms, its various roles are gradually emerging. It is highly expected that rural residents’ credit availability will improve through the use of digital payment. This study expands the UTAUT2 model by incorporating credit availability as an outcome variable and adding two constructs of perceived riskiness and innovativeness, thus building a unified digital payment use and credit availability model. The research model was tested among rural residents from Shandong Province, China. The results show that digital payment can improve credit availability as expected. Thus, it is meaningful to improve digital payment use to alleviate the problem of financing being difficult and expensive in rural areas. Performance expectancy, effort expectancy, social influence, price value, and innovativeness positively impact digital payment adoption and thus have indirect impacts on credit availability, while perceived risk does not, which may be due to effective protective behaviors. In addition, innovativeness also has a direct and positive influence on credit availability. It is recommended: continue to strengthen the construction of rural digital infrastructure and the integration of digital payments with other industries, make the use of digital payment simpler and cheaper, increase the digital payment’s publicity in rural areas, encourage rural residents’ innovativeness, and give them better protections to encourage rural residents to use digital payment more. Promote financial institutions to broaden digital payment use scenarios, strengthen their financial technology, and encourage more competition to use the information from the digital traces better to improve rural residents’ credit availability. For researchers, this study brings a relatively new direction for incorporating important outcomes in the model of rural residents’ adoption of digital payment. For practitioners, this study will help them to take steps to construct a digital payment system that is more friendly to rural residents and better utilize the data assets that come with digital payment to improve credit availability.

Footnotes

Appendix

Questionnaire (Measurement items).

| Construct | Item | Source |

|---|---|---|

| Performance expectancy (PE) | PE1 Mobile payment is useful to carry out my tasks. | Chen and Tang (2006), Venkatesh et al. (2012), Oliveira et al. (2016) |

| PE2 Using mobile payment would enable me to pay more easily. | ||

| PE3 Using mobile payment would enable me to pay more quickly. | ||

| PE4 Using mobile payment would enable me to conduct tasks more conveniently. (dropped) | ||

| PE5 Mobile payment is an effective way to pay money. | ||

| Effort expectancy (EE) | EE1 I find mobile payment easy to use. | Venkatesh et al. (2012), Oliveira et al. (2016) |

| EE2 My interaction with mobile payment would be clear and understandable. | ||

| EE3 Using a mobile payment service is simple. | ||

| EE4 It would be easy for me to become skillful at using mobile payment. (dropped) | ||

| Facilitating conditions (FC; dropped) | I have the resources necessary to use mobile payment. | Venkatesh et al. (2012), Oliveira et al. (2016) |

| I have the knowledge necessary to use mobile payment. | ||

| Mobile payment is compatible with other systems I use. | ||

| I can get help from others when I have difficulties using mobile payment. | ||

| Price value (PV) | PV1 Mobile payment is reasonably priced. | Venkatesh et al. (2012), Oliveira et al. (2016) |

| PV2 Mobile payment is a good value for the money. | ||

| PV3 At the current price, mobile payment provides good value. | ||

| Social influence (SI) | SI1 People who influence my behavior think that I should use mobile payment. | Venkatesh et al. (2012), Oliveira et al. (2016) |

| SI2 People who are important to me think that I should use mobile payment. | ||

| SI3 People whose opinions I value prefer that I use mobile payment. | ||

| Perceived riskiness (PR) | PR1 I feel totally safe when I use mobile payment. | Lu et al. (2011), Yang et al. (2012), Slade et al. (2015) |

| PR2 I feel secure sending personal private information across the mobile payment. | ||

| PR3 I am not worried that other people may be able to access my account when using mobile payment. | ||

| PR4 I feel secure sending sensitive information across using mobile payment systems. (dropped) | ||

| Innovativeness (INN) | INN1 If I heard about a new information technology, I would look for ways to experiment with it. | Oliveira et al. (2016) |

| INN2 Among my peers, I am usually the first to try out new information technologies | ||

| INN3 In general, I am hesitant to try out new information technologies. (dropped) | ||

| INN4 I like to experiment with new information technologies. | ||

| Digital payment intention (DPI) | DPI1 I intend to use mobile payment in the future. | Oliveira et al. (2016) |

| DPI2 I predict to use mobile payment in the future. | ||

| DPI3 I will try to use mobile payment in my daily life. | ||

| Digital payment use (DPU) | PAYQ Quantity of the types of digital payments. | Chen and Tang (2006), Venkatesh et al. (2012) |

| PAYF Frequency of mobile payments use per month. | ||

| Credit availability (CA) | How many loans were obtained in the second half of 2018? | Black and Strahan (2002), Mi et al. (2018) |

Note. Perceived Riskiness (PR) is a reversed item.

Author Contributions

Shujuan Ding: Conceptualization, Methodology, Supervision, Funding acquisition, Data curation, formal analysis, Writing—Reviewing and Editing. Lei Dou: Methodology, Software, Funding acquisition, Data curation, formal analysis, Writing—Reviewing and Editing.

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: This work was supported by The National Social Science Fund of China [Grant No. 22BJY007], The Philosophy and Social Science Foundation of Shandong Province, China [Grant No. 21CGLJ34] and The Philosophy and Social Science Foundation of Shandong Province, China [Grant No. 22CJJJ05].

Data Availability

Data will be made available on request.