Abstract

The green fiscal policy instruments are one of the key tools employed by the Chinese government to address environmental pollution. This study applies content analysis to construct a three-dimensional analytical framework that includes policy instruments, policy development, and the Pressure-State-Response (PSR) framework. Using this framework, the study examines 169 central-level green fiscal policy documents from 2001 to 2023, demonstrating the internal structure and composition ratios of these instruments. Additionally, we explored the historical evolution, frequency of use, and driving factors behind the policies. The study shows that the severity of environmental pollution and the central government’s attention jointly drive a significant increase in the variety and number of green fiscal policy instruments. However, the government tends to rely heavily on regulatory policy instruments, while fiscal instruments aimed at encouraging green innovation, promoting green markets, and promoting coordination with financial policies remain underdeveloped. In light of this, future green fiscal policy formulation should focus on enhancing the diversity of policy instruments, strengthening the coordination between policy instruments, improving interdepartmental collaboration, and increasing social participation.

Introduction

In recent decades, the accelerated process of global industrialization has led to significant pollutant emissions, severely affecting the ecological environment in multiple regions and countries (Cai et al., 2018). As the largest developing country in the world, China also faces severe environmental pollution issues (Lin & Zhu, 2019; Yang et al., 2018). According to the 2022 China Ecological and Environmental Status Bulletin (CEEB), 25.4% of the 339 cities in China still exceeded the standards for fine particulate matter

As a crucial tool in government governance, public policy can effectively balance the delicate relationship between economic growth and environmental protection, continually promoting sustainable development in society (K. Li & Lin, 2016; Fang et al., 2018). In recent decades, the Chinese government has introduced a series of public policies aimed at promoting energy conservation and emissions reduction (Lin & Zhu, 2019; Wu et al., 2018). Among these, fiscal policy serves as a cornerstone of the public policy framework, providing a solid institutional foundation and economic support for stabilizing economic growth and protecting the ecological environment (Acemoglu et al., 2012; Aghion et al., 2016). The Chinese government has been continuously improving its green fiscal system, establishing a multi-level, diversified fiscal policy supply system. Green fiscal policies now cover various aspects of environmental governance, including forests, rivers, soil, air, deserts, and overall ecological systems. To facilitate the effective implementation of environmental protection efforts, the central government has allocated substantial fiscal funds for pollution control. From 2016 to 2020 alone, the central government allocated a total of 4.42 trillion RMB for ecological and environmental protection. Alongside this, the government has issued various regulations and detailed guidelines on the management and utilization of environmental funds. Over the past few decades, the number of green fiscal policies has grown rapidly.

Although researches on green fiscal policy is already comprehensive, there are still three notable gaps. First, most studies focus on examining the effectiveness of green fiscal policies at specific points in time, often using quantitative methods to illustrate the intensity of these policies. However, they fail to provide a detailed analysis of how green fiscal policies and their instruments have evolved over an extended period in response to environmental pressures and national strategies. Second, due to data availability constraints, previous studies tend to evaluate the effectiveness of individual green fiscal policy instruments. Yet, in governmental practice, multiple policy instruments are often employed simultaneously by fiscal authorities to achieve environmental governance objectives. As a result, there is a lack of comprehensive examinations of green fiscal policies, particularly in terms of analyzing the composition and proportional structure of the policy instruments used. Lastly, previous research has overlooked the relationship between green fiscal policy formulation, the level of environmental pollution, and the stage of economic development. These studies have not integrated these factors into a unified conceptual framework to analyze the inherent characteristics of green fiscal policies, such as instrument selection, instrument combinations, and interdepartmental coordination.

The research objectives of this study are mainly three fold. First, this study takes policy instruments as the core starting point, incorporating policy development and the Pressure-State-Response (PSR) framework to form a three-dimensional conceptual framework for analyzing green fiscal policies, thereby providing theoretical support for research on green fiscal policy. Second, this study employs content analysis to conduct a comprehensive examination of central-level green fiscal policy texts in China from 2001 to 2023. It analyzes the composition, distribution, evolution, and driving factors of green fiscal policy instruments, uncovering the shortcomings in the selection and combination of policy instruments by government departments. Lastly, based on the three-dimensional conceptual framework and content analysis of policy texts, the study summarizes the internal characteristics, composition, and patterns of change in China’s green fiscal policy instruments over the past two decades, and on this basis, try to propose recommendations for improving future green fiscal policies.

Literature Review

Green fiscal policy is defined as “fiscal policies aimed at correcting the market failures in the allocation of ecological resources” (Yan et al., 2009). These policies not only promote coordination between energy consumption and environmental protection but also address the prominent externalities in ecological governance through incentive, compensation, and coordination mechanisms (Chen & Qi, 2022). In practice, policy instruments refer to a set of technical means employed by governments to achieve their public policy objectives (Howlett, 1991). Green fiscal policy instruments are critical tools that governments use to tackle environmental challenges (Petrie, 2021), and they are typically divided into fiscal expenditure and fiscal revenue policy instruments. Numerous studies have shown a close relationship between the use of fiscal expenditure policy instruments and improvements in environmental quality (Halkos & Paizanos, 2016). Antweiler et al. (2001) argued that fiscal expenditure policies can effectively reduce pollutant concentrations, particularly emissions from heavily polluting industries. As the proportion of government spending on environmental protection increases, there has been a notable decrease in pollutant concentrations (López et al., 2011; López & Palacios, 2014). However, the effectiveness of fiscal expenditure tools varies depending on the type of pollutant being controlled. For example, the emission of sulfur dioxide

Data from 15 EU countries indicate that tax policy instruments can effectively reduce carbon emission levels (Gerlagh et al., 2018). In China, the environmental protection tax introduced in 2018 has significantly reduced industrial sulfur dioxide

Policy instruments, as the core components of policy design, not only illustrate the measures governments take to address specific public issues but also serve as concrete dimensions for evaluating policy systems. Currently, policy instruments are widely used in policy text analysis across various fields, such as environmental pollution (Zhao et al., 2020), tourism (Zhai & Shi, 2022), and wildlife management (Feng et al., 2021). In the classification of green policy instruments, most scholars divide them into regulatory-based and market-based instruments, aiming to define the boundaries between market mechanisms and government intervention (Aidt & Dutta, 2004; Ji et al., 2022). However, this classification method only examines the internal characteristics of policy instruments from a one-dimensional perspective and does not take-into account the external environment such as historical, social, and economic factors during policy formulation (Howlett, 2004). Therefore, many scholars have incorporated factors such as policy evolution and contextual environments into their analytical frameworks, presenting a comprehensive view of policies from a three-dimensional perspective (Cho et al., 2022; X. Li et al., 2022; Zhai & Shi, 2022; Zhao et al., 2020). Among them, some scholars have applied the Pressure-State-Response (PSR) framework to policy analysis, examining the driving mechanisms behind the evolution of China’s tourism support policies (Zhai & Shi, 2022), which also inspired this study.

Research Design and Theoretical Framework

Content analysis is a commonly used method for systematically exploring qualitative content, such as reports, newspapers, and expert interviews. It can also be combined with quantitative calculations to provide deeper insights (W. Chang et al., 2018; Gan et al., 2022; Zuo et al., 2017). This approach is well-suited for conceptually describing and quantifying empirical phenomena, offering an objective and systematic research tool (C. C. Chung et al., 2022; Elo & Kyngäs, 2008). Content analysis focuses on uncovering the essential meaning of the text, identifying the underlying implications, and converting qualitative markers into standardized quantitative data. This allows researchers to extract new insights and lessons from historical information, making it a widely applied method for policy document analysis (R. D. Chang et al., 2016; Peng & Liu, 2016; H. Zhang et al., 2012). Therefore, this study argues that content analysis is a suitable research method for exploring the evolution of China’s green fiscal policy instruments.

This study focuses on fiscal policy documents related to environmental protection from 2001 to 2023. Following the research steps outlined by Elo et al. (2014) and Liao (2016), relevant policies were systematically collected and categorized. The collected policy samples were sourced from the Central People’s Government website, the Ministry of Finance website, and the PUKLAW database. PUKLAW database is one of the oldest and most comprehensive policy and legal databases in China, established under the Peking University Center for Legal Information. It covers all laws, regulations, and administrative rules issued by institutions such as the National People’s Congress and the State Council since 1949 (Zhao et al., 2020).

First, we conducted a keyword search on the PUKLAW database using terms such as “environment,”“energy saving,”“low carbon,”“emission reduction,”“pollution,” and “green,” restricting the issuing authorities to the “Central Committee of the Communist Party of China,”“State Council,”“and “Ministry of Finance.” We used the document title as the reference and sorted the results by publication date to collect relevant policy documents initially. Second, we conducted additional searches on the official websites of the Central People’s Government and the Ministry of Finance using the same keywords to supplement any missing policy texts. Once all policy documents were collected, each text was carefully reviewed and filtered, eliminating invalid and irrelevant documents. Only currently valid policy texts were retained, specifically those issued by central-level institutions such as the Central Committee of the Communist Party of China, the State Council, and the Ministry of Finance, with a focus on green fiscal policy formulation and fund allocation. A total of 169 green fiscal policy documents were ultimately selected, as shown in Table 1.

Overview of Green Fiscal Policy Documents.

X Dimension: Basic Policy Instruments

Policy instruments stand for a set of policy combinations designed to achieve specific policy objectives (X. Li et al., 2022). These instruments can be classified in various ways. Lowie, Dahl, and Lindblom categorized policy instruments based on the degree of government regulation into regulatory and non-regulatory instruments. Howlett and Ramesh (2003) further divided them into voluntary, mandatory, and mixed instruments. McDonnell and Elmore (1987), considering the purposes of policy tool usage, classified them into four categories: coercive, incentive-based, capacity-building, and systemic change instruments. This study draws upon the framework developed by Rothwell and Zegveld (1985), dividing fundamental policy instruments into supply-side, demand-side, and environmental-side instruments. Supply-side and demand-side policy instruments serve to directly drive and pull environmental protection and green development, while environmental-side instruments exert an indirect influence (Huang et al., 2011; Zhao & Su, 2007).

Supply-side fiscal policy instruments refer to policies through which policymakers increase the quantity and quality of essential resources needed for production and business activities at the societal level, thereby directly supporting environmental protection and promoting green development. Demand-side fiscal policy instruments refer to a series of policy measures through which policymakers use fiscal resources to guide industrial development, expand the demand for green products, reduce pollutant emissions, and lead society toward energy conservation and environmental protection. These measures can further reduce market uncertainty, open up new market shares for green emerging industries, and enhance public participation in green activities. Environmental-side fiscal policy instruments, on the other hand, focus on creating a favorable institutional environment for the smooth implementation of environmental protection efforts. Through top-level design, regulatory frameworks, and incentive mechanisms, these instruments aim to cultivate a supportive atmosphere for policy execution, thereby enhancing policy effectiveness. Based on the above analysis, this paper categorizes green fiscal policies into three major types, comprising 14 specific instruments, as shown in Table 2.

Name and Meaning of Policy Instruments.

Y Dimension: Policy Development

To explore the development process and characteristics of green fiscal policies, this study adopts a longitudinal analysis of China’s use of green fiscal policy instruments, taking policy development as the Y-dimension for analysis. Since China’s accession to the World Trade Organization (WTO) in 2001, the country has experienced rapid GDP growth, achieving an economic miracle with an average annual GDP growth rate as high as 14.23% in 2007. However, alongside this economic boom, massive energy consumption and exploitative development inflicted severe damage on the ecological environment. The ongoing environmental degradation and excessive pollutant emissions have had a significant negative impact on China’s sustainable economic development (Song et al., 2013). In 2004 alone, the economic losses due to environmental pollution amounted to 3.05% of China’s GDP that year (Xiao & Lei, 2011). The central government began to recognize the importance of environmental protection for sustainable economic development and sought to guide society toward a green transition through public funding and fiscal policies. In March 2006, the Chinese government, as part of its long-term development plan to build a “resource-saving and environmentally friendly society,” included energy conservation and emissions reduction policies in the 11th Five-Year Plan. This plan introduced binding targets to reduce energy consumption and total pollutant emissions. Government departments promoted energy savings and emissions reductions by adjusting fuel prices and taxes, implementing consumption taxes on high-emission vehicles, and improving the resource tax system. Additionally, the government enhanced its green procurement policy to further expand the market for energy-saving and environmentally friendly products from the demand side. Since then, the number of green fiscal policies has steadily increased.

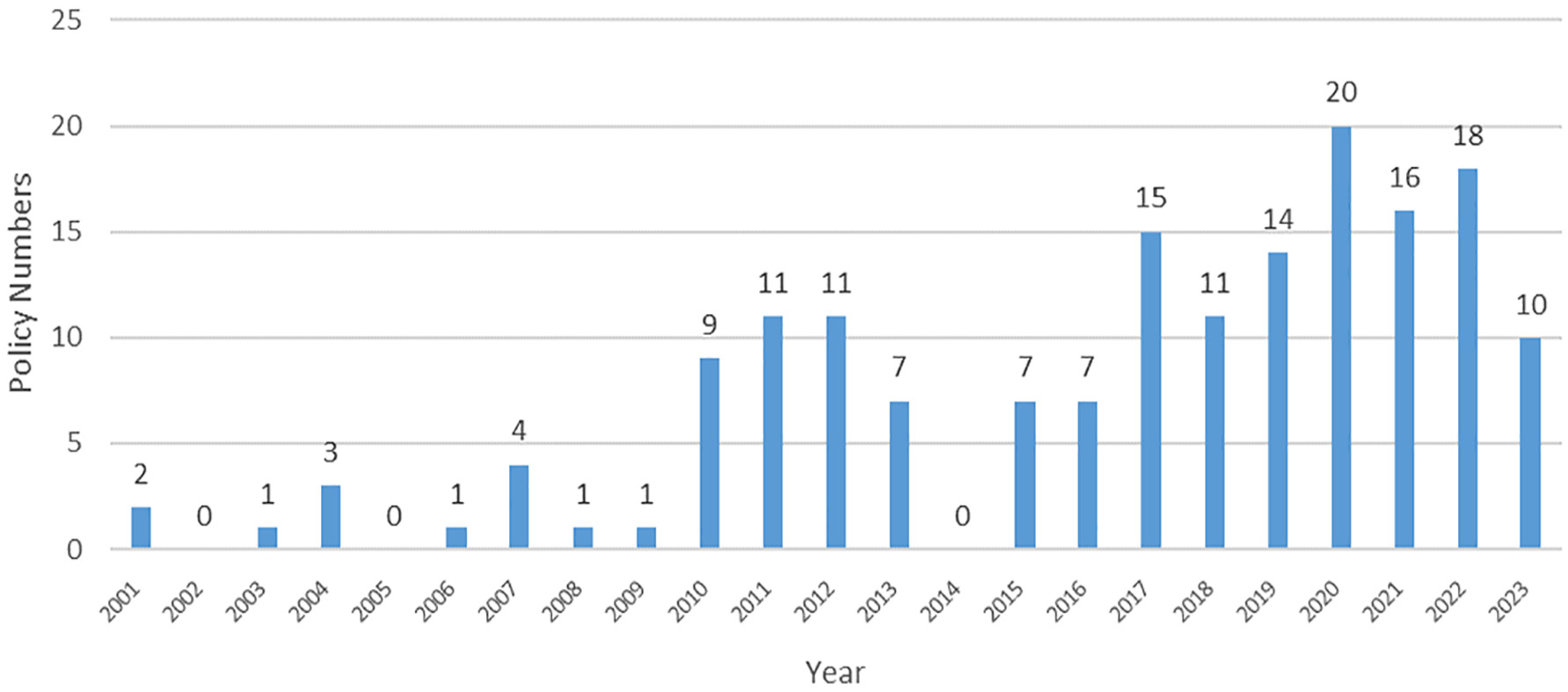

The year 2015 marked a remarkable moment in advancing China’s ecological civilization. The “Environmental Protection Law,” which came into effect on January 1, 2015, provided a solid legal foundation for environmental protection efforts, clearly outlining the responsibilities and specific activities related to environmental governance, enforcement, and supervision. In April of the same year, the Central Committee of the Communist Party of China and the State Council issued the “Opinions on Accelerating the Promotion of Ecological Civilization Construction,” the first comprehensive policy document from the central government that laid out the framework for ecological civilization and environmental protection. This document provided comprehensive and actionable guidance for subsequent environmental protection efforts. In September 2015, the central government further introduced the “Overall Plan for Ecological Civilization System Reform” and its supporting measures, which set clear regulations on natural resource asset ownership, the paid use of resources, and ecological compensation mechanisms. Simultaneously, the Ministry of Finance actively implemented the central strategy through a series of policy instruments such as subsidies, compensation, taxation, and fines. The number of fiscal policies related to environmental protection saw rapid growth during this period. In 2018, the “Opinions of the Central Committee and the State Council on Comprehensively Strengthening Ecological and Environmental Protection and Resolutely Fighting the Battle Against Pollution” laid out a detailed plan for enhancing environmental protection and launching a strong campaign against pollution. During this time, the central government significantly increased fiscal investments in environmental protection and introduced innovative green tax measures, replacing the pollutant discharge fee, which had been in place for 38 years, with an environmental protection tax. This period saw an unprecedented peak in the issuance of green fiscal policies, with a total of 125 policy documents, and in 2020 alone, 20 policies were issued. The specific statistics are illustrated in Figure 1.

Developmental map of green fiscal policies.

By tracing the development of green fiscal policies and considering key turning points and the number of policy issuances, this paper divides the evolution of green fiscal policies into three distinct stages: the emergent exploratory stage from 2001 to 2005, the gradual improvement stage from 2006 to 2014, and the comprehensive promotion stage from 2015 to 2023.

Z Dimension: The PSR Analytical Framework

In 1987, the World Commission on Environment and Development (WCED) recommended incorporating the concept of sustainable development into public policy formulation in its “Our Common Future” report, with the environment being a key dimension (Meyar-Naimi & Vaez-Zadeh, 2012a). The formulation and evolution of green fiscal policies are influenced by a combination of factors, including the extent of environmental degradation, the status of environmental restoration efforts, and the availability of government fiscal resources. Therefore, this section uses the PSR framework as the Z-dimension for analysis to explain how different environmental conditions impact the formulation of green fiscal policies.

The PSR framework was first introduced by the OECD in the 1970s (OECD Environment Directorate, 2004) and has since been widely applied to analyze environmental issues within the context of modern economies (Walz, 2000). It is used in a variety of fields, including ecosystem health assessment (Sun et al., 2019), biodiversity evaluation (Hughey et al., 2004; Tu et al., 2022), sustainable forest management strategies (Wolfslehner & Vacik, 2008), and the performance analysis of environmental governance (C. Li, 2016). The framework is favored for its scientific rigor, systematic approach, ease of use, clear causal relationships, and the inclusion of multiple influencing factors, making it highly applicable and widely adopted in various environmental evaluation frameworks (E.-S. Chung & Lee, 2009; Meyar-Naimi & Vaez-Zadeh, 2012b; Sun et al., 2019).

The PSR framework consists of three main components: “Pressure,”“State,” and “Response” (as shown in Figure 2). “Pressure” refers to the multiple stresses that human production activities impose on the natural environment, such as resource exploration, energy extraction and consumption, and pollutant emissions (OECD Environment Directorate, 2004). “State” represents the changes and current conditions of natural environmental elements, such as air, forests, soil, and water bodies, that result from human activities. “Response” describes the actions and policies adopted by government agencies or management institutions to improve environmental conditions. The interaction mechanism among these elements is that human production activities deplete natural resources, which leads to the continuous degradation of environmental states. Due to the externalities associated with natural resources and the environment, the private sector often lacks motivation to engage in environmental governance. Therefore, government authorities must assume the responsibility of implementing governance activities by formulating relevant regulatory policies aimed at reducing pollutant emissions and improving energy efficiency. The effective implementation of such governance policies can improve the condition of various environmental factors, alleviate the pressure that human activities place on the ecosystem, and ultimately enhance environmental quality and raise public awareness of environmental protection.

PSR analysis framework.

A Three-Dimensional Analysis Framework for Green Fiscal Policies

This study starting from the perspective of fundamental policy instruments, integrates the development history of green fiscal policies with the PSR analytical framework, and constructs a three-dimensional analytical framework for green fiscal policy texts, using the X-Y-Z axes as the spatial coordinate system (as shown in Figure 3). Following the approach suggested by Hsieh and Shannon (2005), this study adheres to a naturalistic paradigm, directly extracting information from the texts and subjectively interpreting and systematically categorizing the content. Drawing on existing research and theoretical frameworks, and with reference to the studies of Liao (2016) and C. C. Chung et al. (2022), we try to classify green fiscal policy instruments in a clear and structured manner. Each category is conceptually abstracted to uncover the specific characteristics of the subject being analyzed.

Three-dimensional analysis framework for fiscal policy texts.

Based on the above analysis, we identified the units of analysis and encoded the key constructs and variables that constitute the research subject, forming a coding summary table, followed by a reliability assessment. During the coding process, we located and coded the policy texts containing policy instruments according to the order of policy issuance and the content of the corresponding chapters. For instance, if the earliest issued green fiscal policy text in Chapter 2, Section 1, proposed “strengthening environmental policy advocacy,” we would code the relevant content as 1-2-1 according to the three-dimensional coding requirements. If the specific policy content only extends to the chapter level, the code will consist of two digits, without further extension. Subsequently, the coded content was abstracted and conceptualized, and matched with the types and names of policy instruments. If a section of the policy text reflects a single policy instrument, that section is treated as a unit of analysis. If a section contains multiple policy instruments, it is divided into several units of analysis. To ensure the accuracy of the interpretation of green fiscal policy texts, we conducted a word-by-word review of 169 collected relevant fiscal policy documents and cross-checked and coded each green fiscal policy instrument. After consistency checks and discussions, we ultimately identified 417 policy text units and 665 policy instrument codes. The qualified policy instruments were then imported into the analytical framework for quantitative analysis, and “Excel 2019” was used to statistically process the coding results. Table 3 presents a portion of the coding results.

Coding Table for Policy Text Content Analysis Units.

Analysis of Green Fiscal Policies Based on the Three-Dimensional Analytical Framework

Analysis of Basic Policy Instruments Dimension

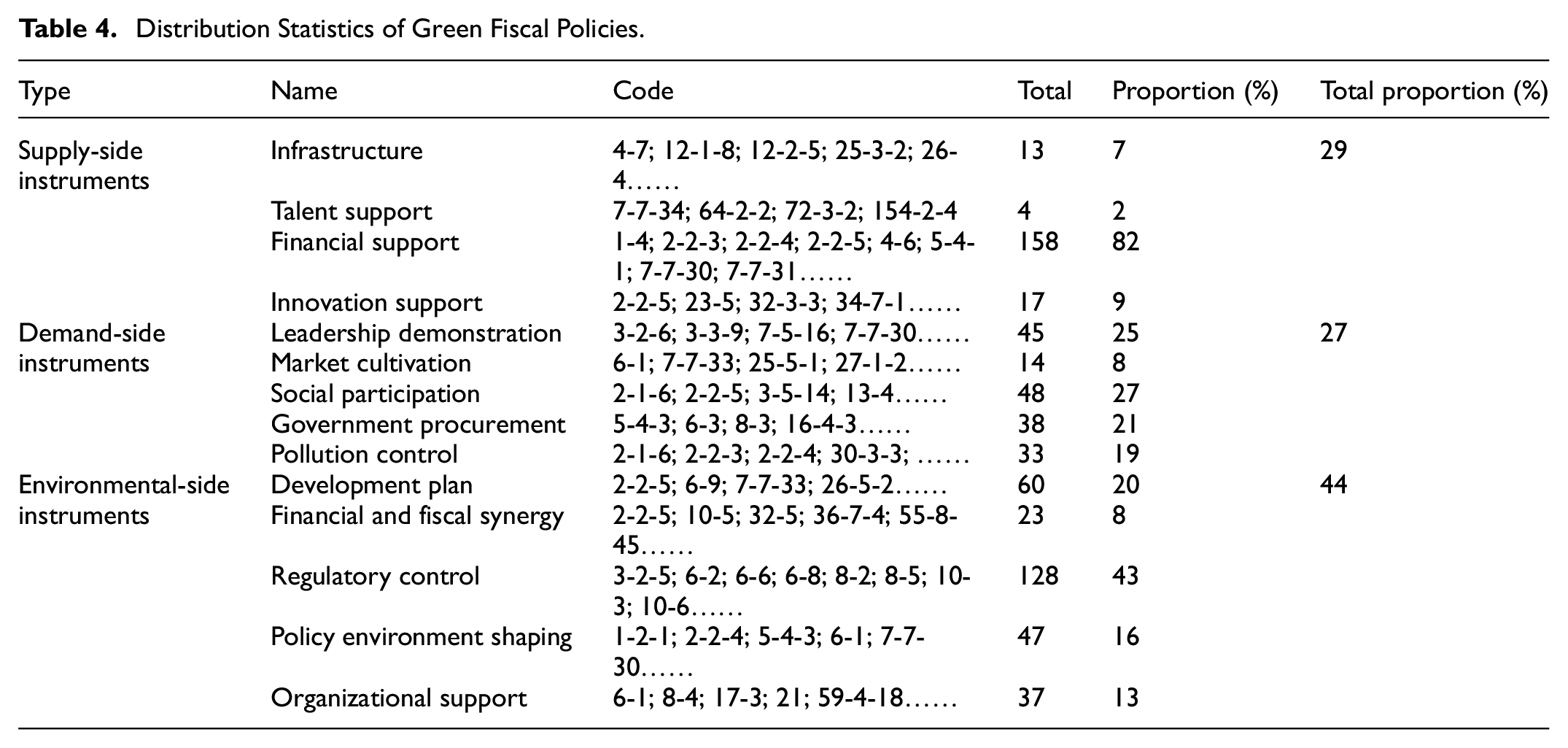

The distribution of green fiscal policy instruments is shown in Table 4. Overall, among the 665 policy instrument codes, supply-side policy instruments account for 29%, demand-side instruments represent 27%, and environmental policy instruments constitute a significant 44% (see Figure 4 for the detailed distribution of policy instrument types). It is evident that the central government places great emphasis on encouraging a favorable policy atmosphere and continually improving fiscal systems that promote green development and environmental enhancement. The ongoing provision of fiscal resources plays a critical role in supporting green development, helping to eliminate barriers to resource supply, reduce pollution emissions, and mitigate the negative externalities of over-exploitation. However, the relatively limited use of demand-side policy instruments indicates that the government has yet to fully guide and stimulate third-party participation in environmental governance.

Distribution Statistics of Green Fiscal Policies.

Proportional distribution chart of green fiscal policy instrument types.

Firstly, in the distribution chart of supply-side fiscal policy instruments, it is evident that Financial support instruments hold an overwhelmingly leading position (82%), indicating that the central government primarily relies on directly providing fiscal resources as the main method for environmental governance. From the global experience of environmental protection, substantial fiscal support is required in the early stages of environmental governance to guide heavily polluting enterprises through a green transition and to promptly reverse the environmental damage caused by early extensive development. Secondly, innovation support and infrastructure instruments hold relatively low shares, accounting for 9% and 7%, respectively. According to policy text analysis, a portion of the fiscal resources has been widely used in areas such as rural environmental pollution control, urban wastewater and solid waste management, the construction of environmental monitoring facilities, and innovation in energy-saving and environmentally-friendly technologies. Lastly, the number of talent support policy instruments is only four, indicating that issues such as the slow development of new technologies for green growth, the high cost of pollution control, and the shortage of relevant skilled professionals have not received adequate attention.

In the distribution chart of demand-side fiscal policy instruments, it is evident that social participation and leadership demonstration instruments account for 27% and 25%, respectively. Social participation primarily involves attracting private funds, encouraging private capital to participate in environmental governance, and standardizing relevant financial operation and guarantee systems, aiming to absorb social resources from multiple channels to alleviate the financial pressure on local governments. Leadership demonstration focuses on selecting regions with strong resource endowments nationwide and providing them with preferential fiscal policies. This is mainly achieved through pilot initiatives, such as implementing pollution control tax and fee policies, establishing ecological compensation mechanisms, and conducting pollution prevention and control policies. Additionally, enhancing public awareness of green consumption and promoting low-carbon lifestyles by reducing the consumption of highly polluting products is a critical component of this approach. Furthermore, government procurement instruments account for 21%, including the improvement of green procurement systems, the establishment of comprehensive green procurement standards, and the direct procurement of energy-efficient and environmentally friendly products by the government. By using fiscal resources to support green products that face insufficient market demand, the goal is to increase the market share of energy-saving and emission-reduction products. Next, pollution control instruments make up 19%, aiming to reduce various pollutant emissions through tax and fee-based policy instruments. Before 2010, pollution discharge fees were collected from polluting entities, but since 2018, this has been replaced entirely by the environmental protection tax. Lastly, market cultivation instruments only account for 8%, with a total of 14 relevant fiscal policy texts, indicating that the government’s focus and support for cultivating the green products market is relatively lacking. There is a limited number of fiscal policies supporting green economic entities, leaving some policy gaps in this area.

In the distribution chart of environmental fiscal policy instruments, regulatory control instruments dominate the structure, accounting for 43%. These tools primarily involve detailed regulations and controls on the sources and uses of fiscal funds, serving as a crucial prerequisite for ensuring the efficient and rational use of resources. In recent years, driven by the pursuit of improved government management and the efficiency of public fund usage, the central government has progressively transitioned the processes of budgeting, execution, and management of fiscal funds toward more refined performance management, aiming to enhance the effectiveness of fiscal resources and policy performance. Following this, development plan, policy environment shaping, and organizational support instruments account for 20%, 16%, and 13%, respectively. Development plan instruments mainly pertain to the allocation of funds across various departments in the environmental protection sector, reflecting national strategic priorities and key areas of environmental work. Policy environment shaping instruments primarily involve fiscal incentive systems, where financial rewards are given to responsible entities and government departments that make significant contributions or actively achieve policy goals in the field of environmental protection. This encourages departments to actively implement energy-saving and emission-reduction policies, supporting a positive social atmosphere that accept green development ideals. Organizational support instruments focus on the coordination of relevant departments and personnel, as well as guiding and coordinating lower-level governments and departments to ensure the smooth implementation of fiscal policies. Lastly, financial and fiscal synergy instruments have a relatively low share, accounting for only 8%. The policy texts indicate that only a few regions across the country have experimented with pilot programs to organize green fiscal and financial policies. Terms such as “encourage,”“advocate,” and “explore” frequently appear in the policy texts, encouraging regions to explore the integration of fiscal subsidies with financial policies like green insurance and environmental protection funds, aiming to enhance the effectiveness of fiscal policies and create policy synergies.

Analysis of the Policy Development Dimension

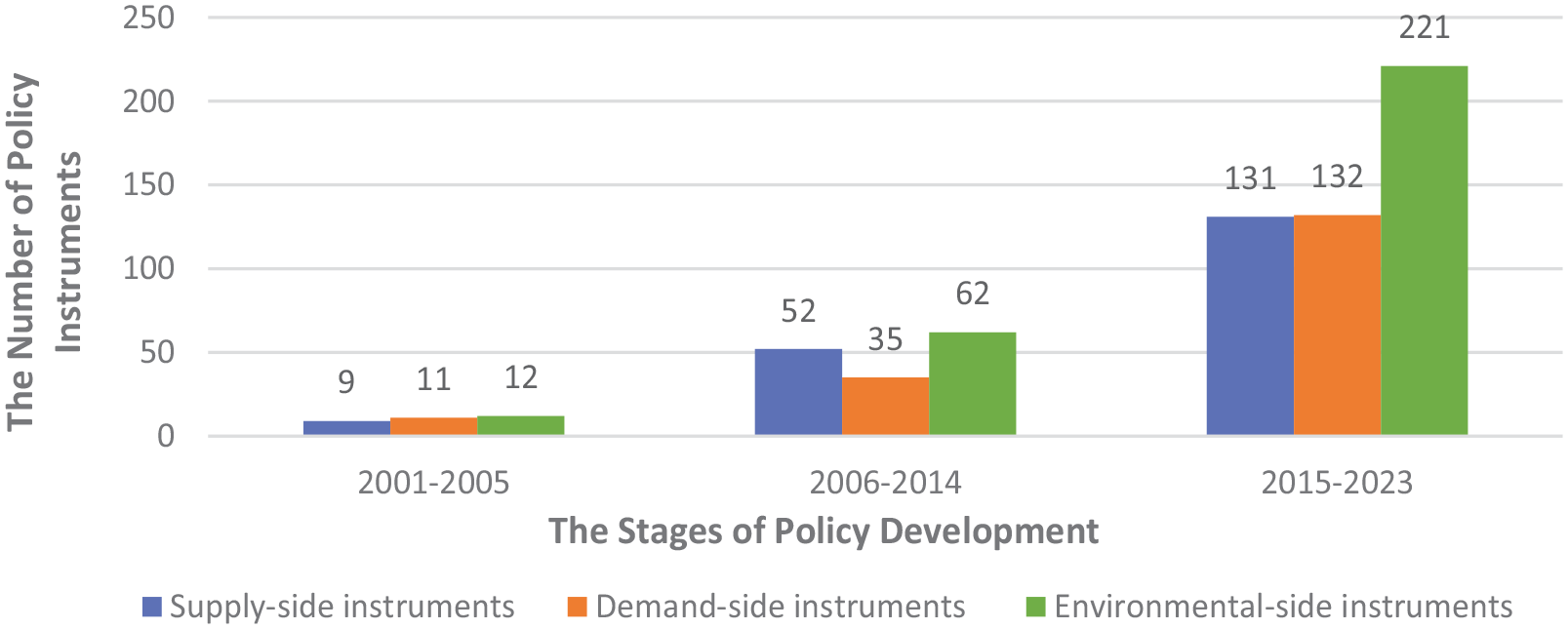

To further analyze the evolutionary characteristics of green fiscal policies across different historical development stages, incorporating the time factor into the policy analysis allows for a more detailed examination of the policy transformation process. In this study, green fiscal policies from 2001 to 2023 are divided into three phases: the emergent exploratory stage from 2001 to 2005, the gradual improvement stage from 2006 to 2014, and the comprehensive promotion stage from 2015 to 2023. As illustrated in Figure 5, the number of different types of green fiscal policy instruments shows distinct patterns of evolution throughout these three stages.

Statistical analysis of the quantity of green fiscal policy instruments in different development stages.

First, during the period from 2001 to 2015, green fiscal policies were still in the emergent exploratory stage, and the number of the three types of policy instruments remained at relatively low levels. In this phase, policy instruments primarily focused on regulatory measures to restrict the use and allocation of fiscal funds, with vague wording in policy statements. This suggests that the government lacked a systematic understanding of green development concepts, and fiscal policies for environmental protection were still in their infancy.

Second, between 2006 and 2014, the number of supply-side policy instruments increased nearly fivefold compared to the previous period. Public policy gradually began to shift toward the environmental protection sector, and the number of fiscal policies increased in tandem with the rise in fiscal investments. During this stage, supply-side and environmental-side policy instruments grew rapidly, as the central government simultaneously increased fiscal funding and strengthened controls over its use. The government sought to advance environmental protection efforts by significantly boosting fiscal investments. As China formally established sustainable development as a national strategy, the role of green fiscal policies in supporting this strategic transformation began to emerge.

Lastly, from 2015 to 2023, the central government’s emphasis on environmental protection reached unprecedented levels. Between 2016 and 2020 alone, the central government allocated a total of 4.4212 trillion RMB for ecological and environmental protection, with an average annual growth rate of 8.2%. Alongside the significant increase in environmental fiscal funds, the number and types of fiscal policy instruments employed by the government also grew rapidly. Among them, demand-side policy instruments saw the greatest growth, with demonstration leadership and government procurement instruments increasing the fastest. During this period, various regions in China carried out numerous policy pilots focusing on environmental protection, ecological restoration, and pollution prevention. The government also increased the procurement of energy-saving and environmentally-friendly products, further expanding the market for green products and reducing pollutant emissions. In addition, the number of environmental policy instruments grew significantly, reaching 3.5 times the number seen in the previous stage. The central government developed clearer objectives and a more refined understanding of the allocation and use of fiscal resources, making fund usage more precise and targeted. The implementation of performance assessment systems for fiscal funds further improved the efficiency of resource usage. Clearer reward systems and better coordination of responsibilities among departmental leaders created a conducive institutional environment for the smooth implementation of policies, continuously enhancing the quality and effectiveness of green fiscal policies.

Analysis Based on the PSR Framework

Although the central government has gradually recognized the negative impacts of environmental pollution on economic development, public health, social governance, and ecological balance, and has set clear pollution control targets, environmental governance remains a complex and lengthy process for any country. Since China joined the WTO in 2001, industrial output and foreign trade volumes have increased significantly, but trade liberalization has also led to higher carbon emissions, and the increase in trade openness has not improved the state of environmental governance (Jalil & Feridun, 2011). A recent study shows that 46% of China’s urban population accounts for 24.6% of the country’s carbon emissions, with pollutants primarily originating from industrial production, transportation, and power plants (Ali et al., 2022). By the end of 2005, national

In response to the severe environmental pollution situation, the Chinese government proposed in 2005 the establishment of a resource-conserving and environmentally friendly society, vigorously promoting energy-saving and emission-reduction technologies. The Ministry of Finance, together with other ministries, formulated a series of supportive policies and key action plans for pollution control, such as the “Air Pollution Prevention Action Plan,” the “Implementation Opinions on Government Procurement of Energy-Saving Products,” and the “Notice on Launching Comprehensive Demonstration of Energy-Saving and Emission-Reduction Fiscal Policies.” These policies not only expanded the boundaries of fiscal policy from a instrument perspective but also innovated fiscal expenditure mechanisms and further improved the green fiscal policy system. Between 2016 and 2018, the central government allocated 47.4 billion RMB for air pollution control, 39.6 billion RMB for water pollution control, 19.5 billion RMB for soil pollution control, 18 billion RMB for comprehensive rural environmental management, and 26 billion RMB for key ecological protection and restoration projects. These efforts effectively reduced various types of pollutant emissions, leading to significant improvements in air quality nationwide and a rapid enhancement of water quality. In 2023, the central government’s budget for ecological and environmental protection reached 247.582 billion RMB. Through fiscal policy instruments such as performance-based budgeting, financial coordination, ecological compensation, and forestry subsidies, strong support has been provided for China’s environmental protection efforts.

Discussion

This study based on the content of 169 green fiscal policy documents in China from 2001 to 2023, focuses on the evolution of green fiscal policy instruments. An analytical framework was constructed which comprising three dimensions: policy instruments, policy development, and the PSR framework. This framework was used to explore the main content and key characteristics of China’s green fiscal policy instruments. The research insights can be summarized into the following three aspects.

First, China should gradually shift from an over-reliance on regulatory instruments toward a more diversified set of policy instruments. As the analysis above indicates, environmental-side fiscal policy instruments account for nearly half (44%) of the total green fiscal policy instruments, with regulatory instruments making up 43% of the environmental-side instruments. Although the United States and Europe also relied heavily on regulatory instruments in the early stages of environmental governance, the centralized administrative authority in China has further strengthened the government’s dependence on regulatory policy instruments (van Rooij et al., 2016). This view has been confirmed in other similar studies (Huan et al., 2024; X. Li et al., 2022; Zhao et al., 2020). Notably, because fiscal policy involves the use and allocation of public funds, the government, driven by its responsibilities and obligations to taxpayers, tends to be particularly cautious in implementing fiscal policies and using public funds, often increasing regulation to minimize the waste of fiscal resources (Ong, 2012). Especially since 2018, China’s fiscal performance evaluation and management system has further increased the frequency of regulatory instruments. While moderate policy regulation can enhance accountability for fund users, regulatory instruments in China have not yet achieved the desired results, with factors such as rigid policy goals, flexible management targets, and the lack of independent oversight agencies leading to unsatisfactory regulatory outcomes (Kostka, 2016). Therefore, the government should aim to increase the use of supply-side and demand-side fiscal policy instruments by encouraging green innovation, attracting more private investment, and encouraging public participation to collectively build an environmentally friendly society.

Second, the selection of policy instruments should be more cautious, and the effectiveness of policy tool combinations still requires further evaluation. According to the PSR analytical framework, the policy objectives of China’s environmental protection and governance have shown a gradual evolution over recent decades, and policy instruments should be selected in line with the characteristics of these objectives (Howlett, 2018). Policy context analysis displays that in the early stages, China’s green fiscal policy instruments were primarily focused on simple instruments such as financial support and regulatory control. In recent years, however, the fiscal authorities have increasingly adopted more various policy instruments such as financial subsidies, ecological compensation, environmental taxes and fees, government procurement, and fiscal incentives to achieve various environmental governance goals. This aligns with the conclusions of most policy studies in China (Huan et al., 2024; Yu & Wang, 2023). Furthermore, a diversified set of policy instruments implies combinations and synergies between instruments. Faced with a complex policy context and multi-layered policy instruments, policymakers and researchers should pay more attention to the interactive effects of various instruments within policy bundles or combinations (Howlett et al., 2015). However, the current reality is that China’s “regional management” system can lead to fragmentation, isolation, and competition among local governments, which in turn results in a lack of coordination within policy tool combinations (Zhao et al., 2020). Therefore, the optimal balance and proportion of different policy instruments still need further exploration. Over-reliance on one type of instrument may crowd out the use of others, and achieving a balanced mix of policy instruments is critical to the overall success of policy implementation (Mao et al., 2019; Xu & Xu, 2020).

Third, interdepartmental cooperation still needs to be further strengthened, and collaboration between policy actors requires improvement. Environmental protection in China is a comprehensive task that involves cooperation across multiple departments. Responsibilities are distributed across various regions and government agencies, such as the environmental protection departments, the National Development and Reform Commission, the natural resources departments, and the energy departments. As a result, during policy implementation, overlapping policies can lead to inefficient use of fiscal resources and public assets, resulting in waste (Gong et al., 2020). Moreover, due to the low flexibility and high rigidity of regulatory policy instruments, the government’s over-reliance on these instruments does not solve the problems of departmental separation and policy overlap (Feng et al., 2021). Therefore, policymakers should intensify efforts to promote interdepartmental cooperation and enrich the core network structure of policy actors (Yin et al., 2023). Furthermore, policymakers should craft clearer policy content, strengthen policy interpretation, and improve the effectiveness of policy implementation through efficient collaboration among key stakeholders. This will help establish a healthy government-market relationship and attract more private capital into the environmental protection sector (Lambin et al., 2014; X. Li et al., 2022). In addition, as departments formulate future green fiscal policies, they should comprehensively assess multidimensional factors such as pressure, state, and response, while coordinating with other departments to create adaptive and stable green fiscal policies based on current environmental protection progress and specific policy goals. This will contribute to achieving long-term fiscal sustainability and continuous environmental improvement.

Conclusion

This study employs content analysis to construct a three-dimensional analytical framework based on policy instruments, policy development, and the PSR (Pressure-State-Response) framework. It analyzes the structural characteristics, development trajectory, and existing issues of 169 central-level green fiscal policies in China from 2001 to 2023. The results show that regulatory instruments in environmental policies account for a high proportion, while the number of supply-side and demand-side policy instruments is roughly similar but still insufficient. Although the formulation of green fiscal policies is influenced by various factors such as the severity of environmental pollution, government governance effectiveness, and fiscal funding allocation, the overall characteristic is strict regulation and control. The diversity of policy instruments remains limited, the pathways for selecting and combining policy instruments are unclear, and interdepartmental cooperation during the policymaking process needs further strengthening. Therefore, this study offers several optimization recommendations to improve the effectiveness of green fiscal policies and promote a more refined fiscal policy system.

First, the use and reliance on regulatory policy instruments should be gradually reduced, while increasing the number of supply-side and demand-side policy instruments. Since the rise of the New Public Management movement, establishing a service-oriented government has remained a governance goal for governments worldwide. This has transformed the relationship between government, market, and society, with a greater emphasis on bottom-up participatory processes, shifting the role of the government from control to guidance (Denhardt & Denhardt, 2000). At the same time, the fiscal pressure faced by governments at all levels in China poses challenges to the long-term commitment of substantial fiscal resources to environmental protection. Therefore, more policy instruments that attract private capital participation should be employed, such as fiscal loan subsidies, environmental protection funds, and insurance, to alleviate the fiscal burden on the government. Additionally, detailed standards for government funding support should be established.

Second, the selection of policy instruments and their internal combinations still require further optimization. The analysis shows that the Chinese government tends to favor relatively simple policy instruments such as regulatory instruments and financial supply. Although the number of each type of policy instrument has significantly increased compared to the early stages of environmental protection, there remains a large gap between the supply-side and demand-side instruments compared to environmental instruments, and the internal structure of policy instruments is uneven. There is a lack of instruments aimed at promoting green innovation, cultivating green markets, and encouraging the synergy of financial policies, resulting in an unbalanced structure of policy instruments. Therefore, policymakers should carefully select fiscal policy instruments and actively evaluate the alignment between existing policy tool combinations and current policy goals, making timely adjustments to the policy instrument mix.

Lastly, interdepartmental coordination should be strengthened, and the participation of non-governmental organizations (NGOs) and citizens in environmental protection should be enhanced. Environmental protection efforts require coordination across multiple departments, and good governance also calls for the participation and collaboration of multiple governance actors (Feng et al., 2021). Therefore, when formulating green fiscal policies, the central and local fiscal authorities should focus on interdepartmental coordination and encourage the public and non-governmental organizations to actively engage in environmental governance. Empowering democratic capabilities and improving the quality of fiscal policies, as well as enhancing fiscal transparency, can reduce information asymmetry and potential conflicts (Fiorino, 1990). The good news is that the Chinese government has already initiated pilot projects in some cities in the central and eastern regions, using instruments such as Public-Private Partnership (PPP) projects to guide and encourage social organizations to participate in environmental governance. In the future, the formulation of green fiscal policies should utilize more demand-side policy instruments to continuously enhance social and public participation.

Footnotes

Author Note

I have not submitted my manuscript to a preprint server before submitting it to SAGE OPEN.

All authors confirm that the work is original and has not been published previously nor is it currently under consideration for publication elsewhere at the time of submission.

Ethical Considerations

This research do NOT involve human participants and animal studies.

Consent for Publication

All authors approved the final manuscript and the submission to SAGE OPEN.

Author Contributions

All the authors have made important contributions to this research. Wensheng He is responsible for conceptualization, methodology, supervision, and review. Zetian Wang is responsible for writing, collecting data, summarizing, validating, visualizing, and editing. All authors have read and agreed to the published version of the manuscript.

Funding

The author(s) disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: This research was funded by the Major Program of National Fund of Philosophy and Social Science of China “Measurement Theory, Methods, and Chinese Practice for Enhancing the Efficiency of Fiscal Policies in the New Era” (Grant Numbers: 22&ZD089).

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Data Availability Statement

All policy documents that support the findings of this study are openly available in PKULAW at https://www.pkulaw.com/. The remaining supplementary policy documents are sourced from the official websites of the Ministry of Finance and the Chinese government website. These data were derived from the public domain: https://www.mof.gov.cn/. ![]() /. The policy text coding data has been organized and uploaded. The data analysis, policy categorization, and other research components were independently conducted by the authors.

/. The policy text coding data has been organized and uploaded. The data analysis, policy categorization, and other research components were independently conducted by the authors.