Abstract

In a quest for economies of scale, access to technologies, and, most importantly, expansion of market share, Chinese public companies have been engaged in several consecutive waves of mergers and acquisitions (M&As) involving mostly domestically domiciled non-listed targets from the same or adjacent industries. Relying on a comprehensive panel dataset of 7,998 transactions completed between 1993 and 2020 by 2,842 publicly listed acquirers domiciled in China, the paper attempts to establish whether M&A deals allow acquirers to improve their market share and, consequently, their relative market position. We use dynamic panel regression and ordered logit models to establish and quantify the link between deal characteristics and the post-deal market share of the combined entities. Our empirical findings demonstrate that corporate consolidations exercise no significant impact on the relative competitive positioning of firms. Only acquisitions by industry leaders produce a sizeable increase in the latter’s market share and lead to higher industry concentration. Most consolidations occur among outsiders exhibiting a high degree of similarity, relatively lower profitability, and stagnant market shares within the more competitive industries with higher rates of firm creation. These consolidations, often in the form of mergers, are not effective in advancing the combined entities’ competitive positioning. Despite the fact that the bulk of corporate consolidations appears unlikely to constitute a threat to competition in the medium term, careful regulatory oversight may be warranted within the currently fragmented and highly commoditized industries, which appear likely to consolidate at the fastest pace.

Introduction

Corporate consolidations, that is, takeovers of firms through mergers and acquisitions (M&As), impact industry development in two opposing ways. On one hand, they are known to stifle competition (Katz, 2021), preclude the appearance of powerful rivals capable of contesting the market and help incumbents derive economic surplus from the resulting dominant market position. In this context, the intensification of mergers and acquisitions waves stimulated by low interest rates and a relatively permissive regulatory framework during the last decade has led to widespread fears of the possible negative repercussions thereof for market competition. On the opposite side, M&As may perform the role of a useful market mechanism increasing the competitive pressure on would-be targets, allowing for recombination of resources of smaller entities (Sears & Hoetker, 2014), prompting cost optimization, and increasing the competitiveness of entire industries on an international scale (Baran & Saikevičius, 2015). Depending on the stage of the consolidation cycle within a particular industry (Deans et al., 2002), either of the two effects may prevail. At early stages of industry development, M&As predominantly serve to enhance efficiency and solidify the best-performing business models and industrial processes. Within mature industries dominated by a few large incumbents, consolidation may, however, pose a tangible threat to innovation, consumer choice, and transparent regulation (Alvarez-González & Otero-Neira, 2019).

Within the Chinese context, M&As are as yet regarded as a mechanism conducive to improved efficiency, productivity, and adoption of innovative practices (Sun et al., 2012). The predominance of this perception may be impacting the design of the regulatory framework and, as a result, the medium-term market structure development. Dynamic economic growth during the previous two decades gave rise to fragmented industries, whose growth was frequently fueled by the relatively low costs of labor with less attention paid to the efficiency and scalability considerations. Corporate consolidations are supposed to mitigate this problem by clearing the market of the less productive enterprises and by increasing competitiveness of the combined entities. So much so, that large enterprises started prioritizing inorganic growth (i.e., corporate takeovers) over organic internal operational restructuring and tangible investments. Perceived as a means to get quick access to strategic innovative technologies and cutting-edge business solutions, the wave of corporate consolidations has had an ambiguous performance record (Zhu & Zhu, 2016) and a yet unexplored impact on industry dynamics and competition (Saraswathy, 2016).

Chinese companies have a controversial record of M&A activities over the last two decades. Prior empirical studies demonstrate that Chinese companies tend to target firms with relatively higher indebtedness and lower profitability than their comparable peers in mature markets (Fuest et al., 2021). The driving force behind this pattern may reside in the fact that when choosing acquisition targets, Chinese companies are primarily concerned about taking over the resources (Luo et al., 2017) controlled by the acquiree in the form of raw materials, technologies, or workforce. In terms of post-deal performance, resource-oriented domestic deals are documented to have a better record than overseas M&As (Liu et al., 2021), even though in general takeovers are documented to have no material impact on the operational performance of the combined entities. On a global scale, Chinese companies have a higher proclivity to acquire resource-rich companies within countries with higher systemic risks (Buckley et al., 2016).

Overall, the overwhelming majority of existing empirical studies focus on the characteristics and short-term performance effects of M&As completed by Chinese companies. There are no up-to-date comprehensive studies investigating the impact of corporate consolidations on industry concentration.

The present study aims at verifying how M&A transactions impact the relative competitive positioning of firms and the degree of competition within consolidated industries. We divide the research task into two key research hypotheses.

H1. Mergers and acquisitions are associated with a subsequent statistically significant increase in the market share of the combined entities.

H2. M&A deals are associated with a statistically significant decline in the degree of competition within acquisitive industries.

Both hypotheses aim at establishing whether mergers and acquisitions may be considered an effective instrument for building and solidifying the acquiring firms’ market position. However, the two explore the problem from different angles. The first hypothesis may bring interesting insights from the managerial standpoint by showing whether executives may rely on M&A as a source of growth and strategic advantage. The second hypothesis is interesting from the standpoint of possible policy guidelines: the findings may give an indication of whether the ongoing M&A processes may constitute a threat to competition in the medium and long term.

Overall, we attempt to inquire into the interplay between M&As completed by Chinese public companies and the competitive dynamics within affected industries. To that end, we compile a dataset of mergers and acquisitions completed by 4,889 Chinese public companies between 1993 and 2020. Our econometric analysis suggests that M&As do not influence the relative competitive positioning of the combined entities.

To start with, we find that only consolidations completed by industry leaders—that is, firms having the highest market share as of the moment of transaction announcement—are conducive to a significant increase in the combined entities’ market share. For the bulk of acquirers, inorganic growth has a negligible impact on market share. These seemingly controversial findings are explained by the observation, that most M&A transactions occur within dynamically growing sectors with a high rate of new firm creation and a higher degree of firm similarity. Thus, the majority of transactions involve industry outsiders with low profitability, non-differentiated products/services, and a weak market position. Consolidations appear to be an ineffective remedy to those firms’ problems, as their relative market position following transaction completion is documented to remain unlikely to improve. In contrast, industry leaders are found to engage in acquisitions involving more dissimilar targets, more frequently domiciled abroad and operating within adjacent industries, thereby creating opportunities for resource recombination and operational diversification. The market position of industry leaders is in no way threatened by the ongoing consolidation processes, and outsiders are unlikely to enter the leaders’ group following transaction completion.

We find that the competitive landscape is not significantly affected by corporate consolidations. Only acquisitions by industry leaders are associated with higher concentration and the Herfindahl-Hirschman index. The bulk of transactions, which tend to occur within more competitive industries, do not influence the intensity of competition. At the same time, as market leaders are found to be statistically less likely to engage in inorganic growth than industry outsiders, M&As appear to be unlikely to threaten competition in the medium term, especially within industries in an early phase of consolidation cycle.

The study contributes to the ongoing debate on the role of inorganic growth in shaping emerging markets’ industrial organization and intra-industry competition. The majority of up-to-date empirical studies focus on the shareholder effects and operational outcomes of consolidation processes (Renneboog & Vansteenkiste, 2019). A broader analysis is necessary to establish the present stage of the consolidation curve in China and quantify its impact on the competitive landscape. The findings may serve as medium-term guidance for regulatory development and proactive anti-trust policy modifications. The study contributes to the extant literature in three respects. First, it is one of the few empirical studies delving into intertemporal patterns of the acquisitions-competition nexus on emerging markets. Second, we employ novel tools for the analysis of the degree of intra-industry competition relying on text mining techniques. Third, we show patterns that distinguish between transactions undertaken by industry leaders and outsiders, which may pre-determine further industry dynamics. The remainder of the paper is structured as follows. We start with a review of the extant literature on the role of inorganic growth in shaping competitive forces. We then discuss the research design and databases, on which the present study is built. A commentary on econometric findings and a discussion of the latter’s implications conclude.

Literature Review

The Interplay Between Corporate Consolidations and Competition

The conventional theory known as structure-conduct-performance paradigm (Weiss, 1979) postulates that unfettered industry consolidation is amenable to abuses of market power. The latter manifest themselves through increasing prices, abnormal profits earned by the incumbent market leaders, and stagnation in innovative activities due to lack of competitive threats (Regibeau & Rockett, 2019). The regulatory response to the intensification of corporate consolidations has, therefore, been a tightening oversight focused on the maximization of consumer surplus.

Threats from global competitors servicing large uniform markets and thus enjoying substantial economies of scale have rendered the approach toward antitrust legislation more nuanced with regulatory bodies paying increasing attention to priorities of industrial policy. As larger combined entities possess significant cost advantages and are better positioned to manage complex value chains requiring the participation of multiple entities, the overarching trend has been to relax oversight and adopt a more permissive stance with regard to M&As. This trend is observable across all developed economies (Thatcher, 2014) and, unsurprisingly, in China, where the priority of industrial policy has been to nurture national champions capable of contesting the markets of the world’s most powerful incumbents.

The question concerning the relative strength of the effects of M&A transactions on competition and consumer surplus remains open to debate. As a result, the goals of anti-trust policies are frequently conflicting and ambiguous. Imposition of strict regulatory limitations and requirements toward M&A deals may prove short-sighted and undermine the long-term competitiveness of the economy as smaller, yet more nimble, businesses may be incapable of competing internationally or servicing large overseas markets (Thun, 2004). At the same time, due care needs to be taken of the possible negative ramifications of strengthening the market power of combined entities on domestic markets, where regulatory capture and lobbying by large businesses may erode consumer welfare.

The analysis of the impact of M&As on competition is complicated by the intensification of consolidation processes engendered by softening monetary policies. The ensuing improved access to external financing and elevated liquidity increase the propensity of firms, especially market leaders, to engage in inorganic growth (Harford, 2005; Maksimovic et al., 2013) and initiate waves of takeovers, which threaten the competitive landscape or least made the analysis of industry dynamics more complex for regulators.

The Possible Negative Consequences of Uncontrolled Corporate Consolidations

The negative consequences of corporate takeovers for competition materialize through two transmission channels. First, by wielding a higher market share, the combined entities may act as price setters and cause a repartition of total surplus to the benefit of producers and to the detriment of consumers (Chirinko & Fazzari, 2000). This may be achieved either through a direct increase in prices or through the imposition of constraints on outputs. Second, a reduction of the number of entities within an industry following corporate takeovers facilitates cooperative optimization of market equilibrium parameters. The resulting coordinative effect plays to the benefit of firms participating in the collusive agreement. The incumbents may lobby for regulatory enactment of entry barriers or other hurdles (Baker et al., 2018), which may stifle competitive pressure and cause any pre-existing intra-industry inefficiencies to persist.

By creating and enforcing barriers to entry of new companies into the industry, corporate consolidations may result in stifled rates of new firm creation, a lower degree of innovation in terms of business models, as well as artificial constraints to production output. This tenet constitutes the principal argumentative basis of the structuralist theory of market regulation (Hovenkamp, 2010). The key policy guideline ensuing therefrom posits the need to limit the scale of corporate takeovers in order to preclude the transition of market structure toward concentrated oligopoly, which may threaten societal welfare. The potential collusive behavior of incumbent market leaders, which may be aggravated by the complementarity of products/services produced by oligopolists (Joskow, 1991), should be subject to regulatory scrutiny.

The opposing viewpoint advanced by the representatives of the neoliberal theory of anti-trust regulation (Glick, 2019) largely postulated that corporate consolidations are an imminent part of the process accompanying the maturation of industrial organization. M&A processes allow for selection of the best-performing business models, elimination of duplicate costs, and building large cooperative enterprises capable of competing on an international scale. The policies resulting from the implementation of this school have had a mixed performance record with lightly regulated industries subject to accelerating consolidations experiencing serious market failures (Neilson & Stubbs, 2015; Uhde & Heimeschoff, 2009).

One notable example of rapid industry consolidation with negative repercussions is commercial banking. Following takeovers, larger combined commercial banks have been shown to exhibit a lower proclivity to lend to small businesses (Udell, 1998). At the same time, due to larger market share and longer borrower–lender relationships, consolidated commercial banks may be more likely to exploit their advantageous access to material information regarding borrowers’ creditworthiness in order to extract higher interest margins. As larger institutions are better positioned to collect and process information, consolidations may be likely to result in both lower provision of credit recourses and higher interest charged on the borrowing by long-standing creditworthy clients (Xu et al., 2015).

It is worth noting that the consequences of consolidation processes for intra-industry competition and consumer welfare appear to be heterogeneous with some markets being more vulnerable than others. In some cases, the existence of a single company catering to the entire market may be the most rational strategy in view of the inherent features of the production processes, economies of scale, or network effects (Parker & Alstyne, 2005). Improvements in industrial processes and cost optimization push firms toward consolidation in order to reduce ordering costs, increase bargaining power vis-à-vis suppliers, and unite fragmented markets under recognizable brands. As such, consolidation processes may represent one of the natural stages of the development of some industries. Other markets, where the potential for abuse of market power is higher, may be in more significant danger following consolidations. In particular, M&As within the healthcare industry have been surrounded with controversy due to the perceived risks to the patients’ well-being and the costs of provision of irreplaceable services (Ho & Hamilton, 2000).

Methodological Challenges in the Study of M&A-Competition Nexus

The crucial feature of empirical studies of the impact of consolidation processes on competition has been the prevailing ambiguity with regard to the measures which should be utilized to judge the repercussions of corporate takeovers. The advocates of active regulatory policies draw attention to the high profitability of firms within consolidated industries arguing that profit may be the result of the calibration of prices and outputs sold by firms with the goal of maximizing producer surplus at the expense of consumers. The anti-trust policy may, therefore, focus on limiting the potential for tempering with market equilibrium. However, studies (e.g., Bork & Sidak, 2013) show that profitability may be an unsuitable measure of the degree of monopolization. Additionally, better bottom lines may result from improvements to operational efficiency—precisely in line with the tenets of schools advocating deregulation.

Consumer surplus is conventionally perceived as a useful gauge of the impact of industry concentration on societal welfare (Kirkwood, 2013). However, it may ignore the impact of market structure on the overall business efficiency and the productivity of entities participating in complex value chains, whose performance may be preconditioned upon the prevailing market structure and bargaining power of firms scattered throughout the production cycle. Despite the lack of unambiguous measures of the consequences of market concentration, the indicators of the degree of intra-industry competition have been standardized in the empirical literature. Concentration coefficients measuring the market share of the largest companies and the Herfindahl-Hirschman index are the conventional measures of the degree of market concentration used in the extant empirical literature. Disentangling the impact of M&A on firms’ market share from the effect of organic expansion is an analytically challenging task as takeovers generate synergies through cost optimization as well as cross-selling, product differentiation, and recombination of the participating entities’ unique resources.

Long-term studies focusing on the interconnection between corporate consolidations and market competition are constrained almost exclusively to mature markets (Berger et al., 2004; Cerasi et al., 2019; Siebert, 2019). The extant literature differentiates between takeovers motivated by the increase of market power and those aimed at increasing economic efficiency. While the former may exercise a distortionary impact on the market architecture causing redistribution of economic surplus through adjustment of equilibrium parameters, the latter may have a beneficial impact on societal welfare as production costs plummet. Surprisingly, Siebert (2019) reports that takeovers pursuing efficiency considerations may slow down the new firm creation while M&As aimed at maximizing the incumbents’ market power may be associated with a slower pace of industry concentration. Overall, mergers have been shown to entail an increase in market concentration and enhance the growth of combined entities. The nexus between takeovers and competition in emerging markets remains understudied. Due to the relatively laxer regulatory regimes, emerging markets may be more exposed to the negative consequences of corporate consolidations. The problem is alleviated by the higher rates of economic growth, which dilutes the market share of industry leaders by facilitating new market entries.

The Specific Features of M&A Activities of Chinese Companies

The present paper represents an attempt to elucidate and quantify the impact of corporate takeovers on the degree of industry concentration and competition in China. There are surprisingly few studies analyzing the impact of takeovers on the degree of industry concentration in China. The overwhelming majority of existing studies focus on cross-border M&As and their impact on the subsequent operational performance of the combined entities (Guo & Clougherty, 2022). The predominant consensus in the extant empirical literature posits that there are three fundamental features which shape and precondition the M&A activities of Chinese companies. To start with, Chinese companies exhibit a significantly higher proclivity to acquire companies with access to resources (Reddy et al., 2019), while the dominant motive in most acquisitions completed by companies in mature markets is the procurement of synergies and cost optimization. This explains why transactions completed by Chinese companies are likelier to involve targets with higher debt load and lower operational performance, than those selected by their peers from mature markets (Fuest et al., 2021).

Second, a substantial portion of transactions are completed by state-owned or state-controlled entities (Lin et al., 2020). In addition to economic considerations, such acquirers may pursue administrative, political, or social goals when contemplating an acquisition (Schweizer et al., 2019). The role of political connectedness in shaping transaction outcomes can be both positive and negative (Ren et al., 2019; Yang et al., 2022). Third, the industry composition of M&As is largely reflective of the structure of the underlying economy with the bulk of deals occurring in industrials and manufacturing. The latter may explain why the existing studies (e.g., Fisch et al., 2019) find no significant impact of corporate consolidation on the innovative activities of the combined entities or why there are no observable persistent shifts in operational performance after deal completion (Zhang et al., 2018).

Studies inquiring into the possible impact of M&As on the competitive dynamics of the Chinese market remain extremely scarce. Most papers (e.g., Ma et al., 2020) focus on the microeconomic repercussions of transactions, for example, pricing patterns or margins earned by the combined entities (Chu et al., 2021). Studies focusing on the comparative analysis of anti-monopoly regulations (e.g., Soomro et al., 2021) generally suggest that Chinese supervisory bodies are not excessively restrictive with regard to consolidations involving domestic companies, but may exhibit a substantial degree of protectionist oversight over transactions in which the acquirer is a foreign-owned entity. In fact, the industrial policies implemented by Chinese regulatory authorities may increase the likelihood of consolidations in some sectors, particularly those, in which the industrial policy is intended to grow local champions (Barbieri et al., 2021). It remains unclear how the ongoing consolidations impact the degree of competition within the affected industries.

The accelerating wave of consolidations, which is purportedly driving productivity and efficiency (Du et al., 2021), may threaten innovativeness and growth in the medium term provided that the possible negative repercussions are not addressed in a timely manner with properly targeted competition regulations. We approach the problem both at an individual-firm and industry level. At the micro-level, we try to establish whether M&As may be effectively relied on to consolidate or advance acquirers’ market position by facilitating the expansion of market share. At the industry level, we verify whether consolidations have consequences for firm entries and exits, net firm creation, and industry concentration. A multi-faceted approach should allow for a comprehensive assessment of the present positioning of the Chinese market on the consolidation cycle, and formulate a set of tailored policy guidelines.

Research Sample and Variables

For the purposes of the present study, we compiled a database comprising all M&A transactions completed by Chinese public companies (listed on Shanghai and Shenzhen stock exchanges) between 1993 and 2020. The transaction data were retrieved from the Thomson Reuters Database. The initial sample comprising the transactions had to be filtered along a number of criteria in order to better accommodate the purpose of the study. First, we removed any transactions completed by financial companies as the study focuses only on non-financial businesses. Second, we restricted the size of transactions qualified for the sample to one million US dollars. Third, we excluded any transactions for which incomplete records of the key experimental variables were available. The resulting sample comprises 7,998 mergers and acquisitions completed by 2,842 public companies (acquirers) during the studied period.

For each transaction, we collected data regarding the equity stake being acquired, the industry classification of the entities involved, the valuation of the target equity stake, the method of transaction settlement (cash or stock), the country of domiciliation of the target company, and the attitude of targets’ and acquirers’ boards toward the deal approval (positive or negative). We also compiled the descriptions of business profiles of the entities involved in the transaction. For each acquiring entity, we track the long-term record of deals over the studied period flagging firms, which completed multiple transactions in order to be able to subsequently cluster the deals by acquirers. The definitions of variables we encode for each deal are presented in Table 1.

Definitions of Variables.

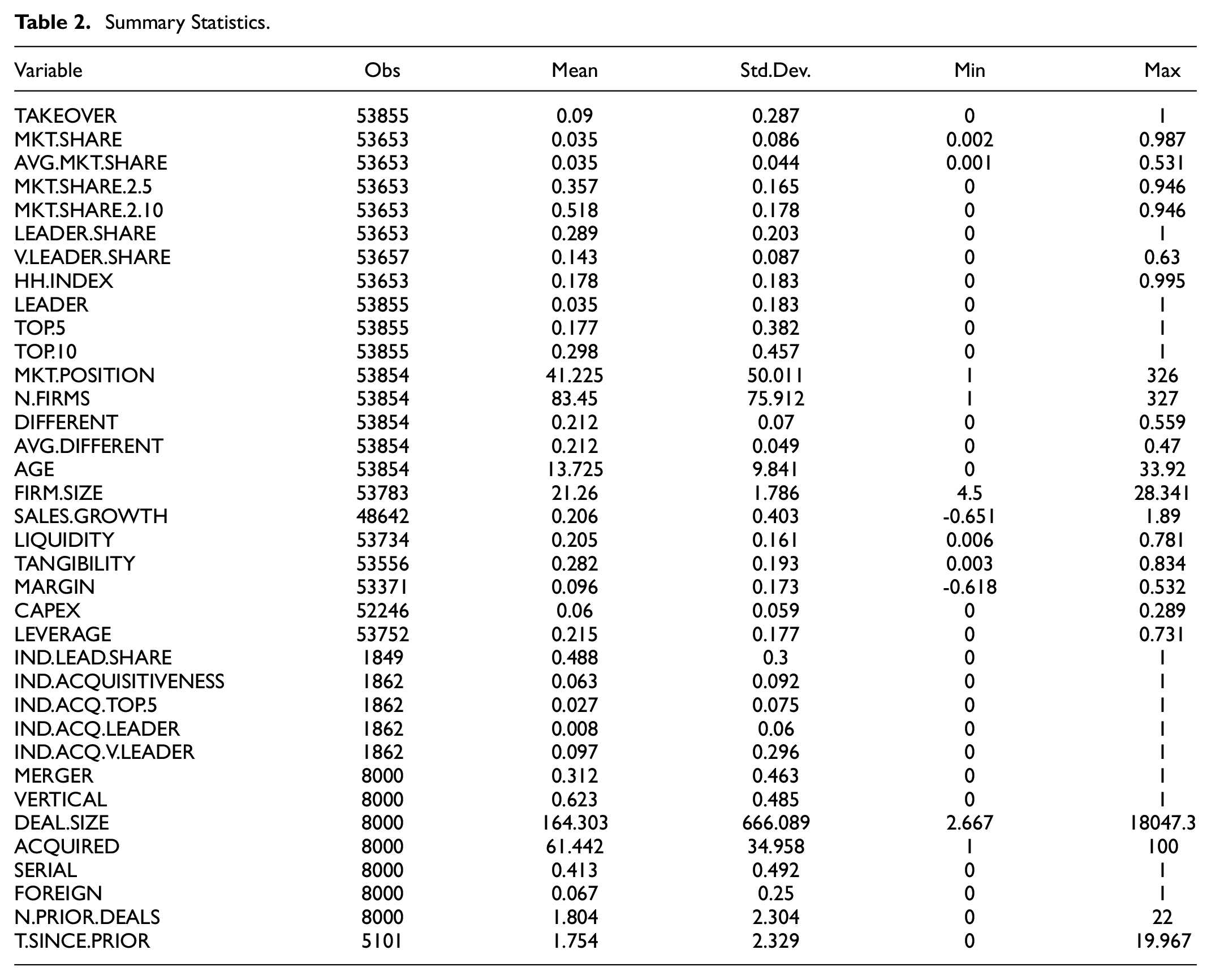

The descriptive statistics for the sample of deals are presented in Table 2. Of the analyzed transactions, 31.2% were concluded in the form of mergers, the remainder being acquisitions. An average deal involved a transfer of a 61.44% equity stake in the target company. The majority (ca. 62.3%) of analyzed transactions involved targets from adjacent industries, therefore, making it possible to classify them as vertical. Almost 41.3% of M&As were completed by serial bidders, that is, firms having completed more than two transactions prior to a given deal. An average acquirer completed 1.8 transactions prior to a given deal. The overwhelming majority of transactions involved domestically domiciled targets (93.3%). The average time elapsing between consecutive transactions for a given company is ca. 1.75 years. The process of corporate consolidation has substantially intensified over the last decade. One may clearly distinguish a wave of transactions peaking in 2015–2017. Despite a seemingly increasing proclivity of Chinese companies to engage in international expansion, the share of overseas deals remains modest. Therefore, the rapid process of industry consolidation primarily translates into changes to the domestic market structure, and should, therefore, draw the attention of domestic regulatory bodies.

Summary Statistics.

In order to approach the consolidation-competition nexus at the micro-level, we compiled a panel firm-level database for 4,889 Chinese public companies comprising all listed firms regardless of whether they completed any M&As during the analyzed period. Only non-financial companies are included in the final sample. We limited the sample to companies with a market capitalization exceeding one million US dollars. The result is an unbalanced panel database with 53,855 firm-year observations covering the span between 1993 and 2020. The unbalanced data does not constitute a methodological concern in the study for two reasons. For existing companies, we made sure that data is available throughout the entire observation span unless the company was founded after the start of observation or ceased to exist before the end of the observation span. Whenever data is missing in the middle of the time series, we presume it to be missing at random (MAR). The latter cases constitute no problem from the standpoint of the robustness of empirical results.

For each firm, we estimated dynamic yearly market share. This was done relying on standard industry classification dividing firms into 113 subindustries. Further fragmentation of the industry classification appeared unwarranted as many public companies operate a number of business segments making strict sample stratification a practical impossibility. A firm’s contemporaneous market share was estimated as a ratio of the firm’s sales to the total sales of all firms classified to a given subindustry during a given year. For each sampled company, we also collected all yearly financials (leverage, profitability, liquidity, tangible assets, etc.).

One of the goals of the present study is to establish how the degree of market fragmentation influences the interrelation between corporate takeovers and competition. Industry consolidation is prima facie proceeding faster and leading to greater degree of concentration on commoditized markets offering standardized products or services. Larger entities are more efficient at bundling and cross-selling complementary goods, while the economies of scale and low marketing costs allow them to overtake the market by offering lower prices. Therefore, one may reasonably expect to see a more pronounced impact of M&A transactions on market concentration within industries, where products/services are less differentiated and where firms offer close substitutes.

The methodological challenge complicating the verification of this conjecture resides in the measurement of the degree of market fragmentation. Relying on the extant literature (e.g., Hoberg & Phillips, 2010), we decided to use text mining techniques to calculate the average similarity of firms within each industry. We utilized standard text processing libraries to clean textual descriptions of business profiles of sampled companies of the common words and punctuation. Then we calculated cosine similarity coefficient for each pair of companies belonging to the same industry during a given year. The arithmetic average of the said pairwise similarity coefficients for each company represents the variable DIFFERENT. The indicator fluctuates between zero and one with higher values indicating greater average similarity of a given firm and its competitors operating in the same subindustry. Further using this variable in econometric analysis, we try to establish how it intermediates the relationship between corporate takeovers and intra-industry competition.

Shifting to the industry level, we aggregated firm-level data by subindustry in order to estimate how the average acquisitiveness of firms influences the degree of market concentration. We reshaped the firm-level database by assuming the industry-year as a unit of observation. We compiled records for 113 industries observed between 1993 and 2020 thereby creating a database of 1,862 industry-level observations. For each industry-year, we estimated a number of commonly utilized indicators of market concentration: (1) share of the market leader; (2) share of the top five companies in the industry; and (3) Herfindahl-Hirschman index. The indicator of industry acquisitiveness (IND.ACQUISITIVENESS) with an average value of 6.2% suggests that M&A occurred during an average of 6.2% firm-years in any given industry during a given year, thus pointing to the relatively rare occurrence of takeovers on the Chinese public market.

Econometric Methodology

The empirical analysis is structured in three consecutive stages. At the first stage, we study how M&As impact the market share of the combined entities. To that end, we run a set of dynamic GMM-SYS panel regressions (Arellano & Bond, 1991). The chosen analytical techniques allows for addressing the problem of endogeneity inherent in the studied relationships. We introduce lags of the explanatory variables in order to establish the causal links underpinning the postulated patterns. The Arellano-Bond models have been evidenced to outperform other econometric models when dealing with dynamic endogeneity (e.g., Li et al., 2021). The baseline model used at this stage of analysis has the following specification:

where

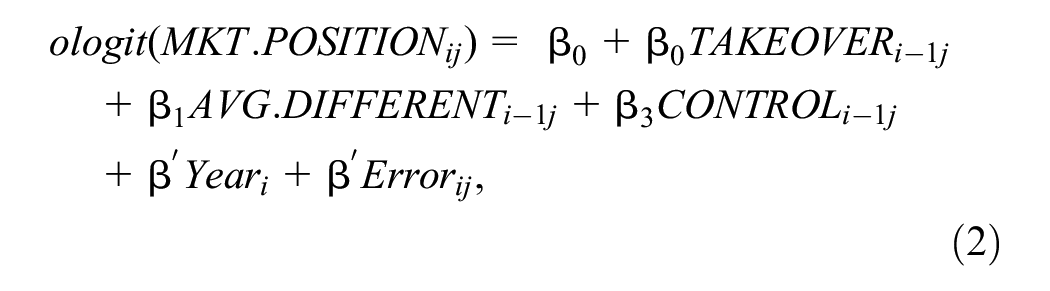

As a corroboratory test, we run additional regressions where the explained variable is firms’ market positioning, that is, their position in the ranking of firms in a given industry by market share. To create the experimental variable, we rank firms by market share during every year and in every industry separately. Firms with the highest market share are assigned rank “1,” others ranks are assigned in ascending order, that is, higher ordinal ranks correspond to lower market share during a given year in a given industry. Ordered logit—a model used to study the factors influencing ordinal variables—of the following specification is used to establish whether inorganic growth may help combined entities to advance in the rankings:

One of the key variables in model (2) is AVG.DIFFERENT, whose inclusion is aimed at establishing the interlink between M&As and market position contingent upon the degree of industry commoditization. A higher cross-firm similarity indicates a higher degree of commoditization, which is turn may facilitate market takeover through inorganic growth and corporate consolidations.

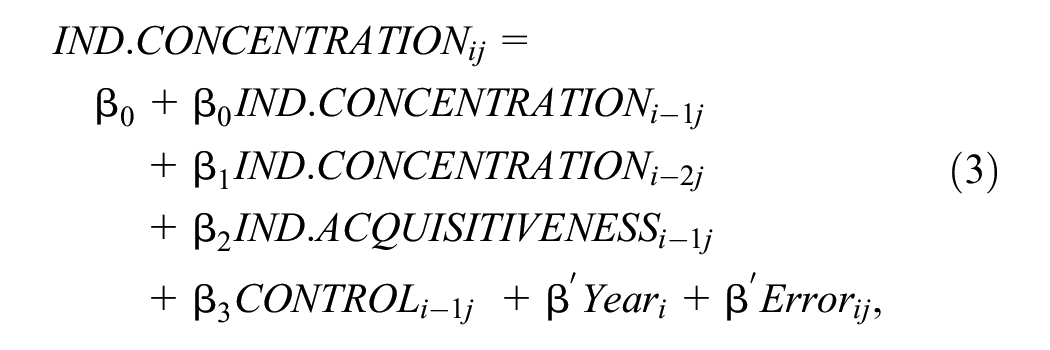

At stage two of the analysis, we explore the takeovers-competition nexus at industry level. The following dynamic panel models are tested:

where

In addition to exploring the link between consolidation and market architecture, we describe features, which allow to distinguish between acquisitive and non-acquisitive firms as well as fast and slowly consolidating industries.

At the final third stage of the study, we return to firm-level data and analyze the profile of an average acquirer in the Chinese market. In particular, we verify whether the majority of transactions are undertaken by the leading companies, which could endanger intra-industry competition, or by industry outsiders, which would signify that efficiency considerations outweigh market-dominance-related rent seeking in shaping firms’ likelihood to engage in M&A deals. The next section summarizes the key findings of our quantitative analysis.

Analysis of Empirical Results

The Impact of M&As on Firms’ Market Share and Market Position

Table 4 presents the results of tests of model (1) on firm-level panel data. In line with extant literature (e.g., Reimann et al., 2010), we find that industry commoditization is associated with higher per-firm market share. An increase of cross-sectional firm similarity coefficient by 10% is associated with an increase of an average firm’s market share by approximately 0.6 percentage points. Second, the faster growing industries—that is, those recording higher sales growth—are more fragmented with each firm occupying smaller market niche. Third, market share is documented to be positively associated with firms’ profitability, liquidity, and leverage thus pointing to the superior operational and financial performance of industry leaders. Most importantly, we evidence that corporate takeovers are associated with a subsequent significant increase of market share of involved entities. Finalization of a merger or an acquisition is found to be associated with a subsequent increase of market share by ca. 0.2% 1 year after deal completion (the respective regression coefficient reported in model (1) of Table 3 is statistically significant at 1% level) and by ca. 0.1% 2 years after (1% significance). Thus, we show that consolidations accelerate the expansion of the combined entities and, therefore, represent an important driver of firms’ growth. Crucially, we show that acquisitions undertaken by the top five firms in a given industry in terms of contemporaneous sales are associated with a subsequent increase of market share by ca. 1.2%, a coefficient significantly higher than the marginal effect reported for the entire sample. All models have been inspected for the validity of key econometric properties substantiating further statistical inference.

Link Between Corporate Takeovers and Combined Entities’ Market Share.

Note. The table presents the results of dynamic panel regression modeling (GMM-SYS). All models include the first and second lag of explained variables, year fixed effects, and firm-level controls. The coefficients for some of the control variables are not reported for reasons of brevity. Prefixes L. and L2. indicate the first and second lag of explanatory variables respectively.

Statistical significance of variables at 1%, 5%, and 10% level is denoted with ***, **, and * respectively.

Our findings provide empirical support for hypothesis H1 and demonstrate that M&A activities may be an important determinant of competitive dynamics within an industry. By enhancing the market share of the combined entity (Du et al., 2020), consolidations may endow it with greater pricing power, thus impacting the distribution of consumer surplus.

The tests reported in Table 4 are aimed at verifying whether consolidations may dilute the market position of industry leaders and vice-leaders. Models (1) and (3) clearly indicate that corporate takeovers pose no threat to the market positioning of incumbent leaders. The combined entities appear unable to contest the already occupied markets even though the additivity of the participating entities’ sales allows the combined firms to enjoy the presence in an overall larger market segment. In line with prior findings, we show that M&As undertaken by industry leaders and vice-leaders are associated with a substantial post hoc growth of their market shares by ca. 1.7% (the respective coefficient is significant at 1% level, model (2) in Table 4) and 0.7% (1% significance level, model (4) in Table 4) respectively.

The Impact of Corporate Takeovers on the Market Positioning of Industry Leaders and Vice-Leaders.

Note. The table presents the results of dynamic panel regression modeling (GMM-SYS). All models include the first and second lag of explained variables, year fixed effects, and firm-level controls. The coefficients for some of the control variables are not reported for reasons of brevity. Prefixes L. and L2. indicate the first and second lag of explanatory variables respectively.

Statistical significance of variables at 1%, 5%, and 10% level is denoted with ***, **, and * respectively.

Table 5 reports the findings on the interrelation between firms’ competitive positioning and completed M&A deals. Model (1) is an ordered logit regression with the explained variable being the firms’ ordinal position in the ranking of a given industry-year by sales. Corporate takeovers are documented to exercise no significant impact on the competitive positioning of firms. One, two, or three years following the transaction completion, the combined entities are unlikely to record any significant advance in the competitive ranking by market share. Models (2) and (3), which summarize the results of binary logit regressions, suggest that M&As are also unlikely to help firms enter the group of industry leaders. In neither of the two models is the regression coefficient at the TAKEOVER variable statistically significant. The results reported at this stage of analysis clearly suggest that despite modestly increasing firms’ market shares (particularly so in case of industry leaders), corporate takeovers do not impact the relative competitive position of firms within particular industries. Therefore, executives may not rely on inorganic growth as a primary pillar of firms’ competitive advantage. Importantly, M&As are effective at increasing the market share of incumbent industry leaders. Therefore, regulatory authorities should exercise appropriate supervision over leaders’ M&As in order to preclude excessive industry consolidation.

Takeovers and Market Position of the Combined Entities.

Note. Model (1) presents the results of ordinal logit model, in which the explained variable is the ordinal market position of acquirers. Models (2) and (3) summarize maximum likelihood estimates of binary logit models with the explained variables being the entities’ belonging to the industries’ top 5 or top 10 firms in terms of market share respectively. Z-coefficients are reported in parentheses under respective regression coefficients.

Significance of respective variables is denoted with asterisks: *p < .1. **p < .05. ***p < .01. The models include year fixed effects and firm-level controls.

Prior studies involving comparative analysis of the competition and anti-monopoly law (e.g., Soomro et al., 2021) demonstrate that Chinese regulators are not excessively restrictive with regard to consolidation transactions involving domestic entities, particularly when the acquirer is a state-controlled entity. M&As may be regarded as one of the factors of industrial policy aimed at nurturing local champions. While such an approach may indeed be conducive to the creation of powerful industry incumbents, it may also cause an excessive concentration of market power. The latter may be particularly detrimental within commoditized industries.

Differences Between Acquiring and Non-Acquiring Firms

The analysis of cross-sectional differences between acquiring and non-acquiring firms reported in Table 6 reveals a few interesting findings regarding the profile of a typical acquirer on the Chinese market. To start with, the majority of corporate consolidations are initiated by industry outsiders rather than leaders. An average industry rank of a typical acquirer in terms of sales is 22.26. Second, acquiring companies record below-average market shares at the level of ca. 5.6% as opposed to ca. 8.8% among non-acquiring companies. Third, the majority of transactions occur within the less consolidated industries with below-average shares of industry leaders, but higher-than-average market shares held by the top five. The most acquisitive industries are thus more likely to be oligopolies. The average number of companies operating within the acquisitive industries is also significantly higher (ca. 45.52 vs ca. 9.83 in non-acquisitive sectors; the difference of means is statistically significant at 1% level). Finally, M&As are more likely to occur within the more commoditized industries. Acquisitive firms exhibit a higher degree of similarity to their competitors than non-acquiring companies (22.5% vs 15.4%; the difference is significant at 1% level). Overall, the bulk of corporate takeovers takes place within sectors, where they are relatively less likely to constitute a medium-term threat to competition. This inference comes from the juxtaposition of two previously reported findings: (1) deals are mostly completed by outsiders rather than the leading firms; (2) M&As are unlikely to lead to the advancement of competitive positioning of the combined companies.

Cross-Industry Differences Between Acquiring and Non-Acquiring Firms.

Note. The table presents the results of Student t-tests of differences in mean values of a number of experimental variables aggregated at industry level. Industries are identified relying on GICS classification. Subsample (2) comprises acquiring firms at industry level, subsample (1) comprises non-acquiring firms aggregated at industry level.

denote statistical significance of the test at 1% level.

M&As and Industry Competition

Relying on aggregated industry-level data, we estimate the impact of takeovers on the dynamics of a number of consolidation indicators. Start with the Herfindahl-Hirschman index, the results for which are reported in Table 7. We document a lack of significant impact of the bulk of M&A transactions on the industry competition. Only deals completed by the largest firms in a given sector have a significant effect on the degree of competitive pressure (the respective regression coefficients are reported in models (2) and (6) of Table 7 and are statistically significant at 5% level). In line with expectations, the more commoditized industries are evidenced to experience faster consolidation.

Relationship Between Corporate Takeovers and Intra-Industry Competition Measured by Herfindahl-Hirschman Index.

Note. The table presents the results of dynamic panel regression modeling (GMM-SYS). All models include the first and second lag of explained variables, year fixed effects, and firm-level controls. The coefficients for some of the control variables are not reported for reasons of brevity. Prefixes L. and L2. indicate the first and second lag of explanatory variables respectively.

Statistical significance of variables at 1%, 5%, and 10% level is denoted with ***, **, and * respectively.

Likewise, corroborating our prior findings, we show in Table 8 that takeovers do not affect the market share of sector leaders as the combined entities are unlikely to rival them directly (the regression coefficient at the variable IND.ACQUISITIVENESS is statistically insignificant). In contrast, takeovers completed by industry leaders are confirmed to be conducive to higher levels of industry concentration (the respective coefficients reported in models (2) and (3) in Table 8 are significant at 5% level). These findings are further corroborated in Table 9, where we show that acquisitiveness is associated with a significant increase of the market share of firms ranked from two to ten in terms of contemporaneous sales. Thus, takeovers appear to play to the benefit of incumbent leaders while conveying no significant benefits for outsiders. This evidence speaks in favor of hypothesis H2, which states that M&As may be associated with a significant decline in the degree of competition within acquisitive industries.

Corporate Takeovers and the Market Share of Industry Leader.

Note. The table presents the results of dynamic panel regression modeling (GMM-SYS). All models include the first and second lag of explained variables, year fixed effects, and firm-level controls. The coefficients for some of the control variables are not reported for reasons of brevity. Prefixes L. and L2. indicate the first and second lag of explanatory variables respectively.

Statistical significance of variables at 1%, 5%, and 10% level is denoted with ***, **, and * respectively.

Post-Transaction Industry Concentration.

Note. The table presents the results of dynamic panel regression modeling (GMM-SYS). All models include the first and second lag of explained variables, year fixed effects, and firm-level controls. The coefficients for some of the control variables are not reported for reasons of brevity. Prefixes L. and L2. indicate the first and second lag of explanatory variables respectively.

Statistical significance of variables at 1%, 5%, and 10% level is denoted with ***, **, and * respectively.

A frequent concern voiced by the advocates of stringent anti-trust regulation and acquisition controls is that industry consolidation ensuing from M&As may stifle new firm creation (Hovenkamp, 2010), and cause the growth of barriers to entry for new contestants. We verify this conjecture by checking how industry-level acquisitiveness influences the average number of firms (after accounting for exits, entries, and takeovers). The respective findings are reported in Table 10. Surprisingly, we find that acquisitions are associated with a higher total number of firms in acquisitive sectors (the respective regression coefficient in the model (1) of Table 10 is significant at 10% level). This seemingly counterintuitive finding may be explained by the prevalent occurrence of acquisitions within industries with higher rates of net firm creation. As already noted previously, the bulk of acquisitions occur within fragmented sectors with high numbers of operating firms and relatively higher sales growth. The elimination of some firms through M&A deals is outweighed by the number of new entrants contesting the growing market segments. Deals completed by industry leaders do not alter the stated pattern either as they initiate a minority of sampled transactions. Thus, we unequivocally demonstrate that consolidations do not put a strain on the dynamics of new firm creation. These findings speak against hypothesis H2: we find that consolidation processes do not exercise any negative impact on market entries.

Nexus Between New Firm Creation and Takeovers.

Note. The table presents the results of dynamic panel regression modeling (GMM-SYS). All models include the first and second lag of explained variables, year fixed effects, and firm-level controls. The coefficients for some of the control variables are not reported for reasons of brevity. Prefixes L. and L2. indicate the first and second lag of explanatory variables respectively.

Statistical significance of variables at 1%, 5%, and 10% level is denoted with ***, **, and * respectively.

Our findings suggest that regulatory scrutiny aimed at limiting the potential detrimental consequences of excessive market power concentration should be primarily focused on precluding the formation of oligopolistic markets (Miklos-Thal & Shaffer, 2021) rather than on further facilitation of market entry as the latter appears to be unaffected by the ongoing consolidation processes.

Our findings obtained through analysis of industry-level data may be summarized in Figures 1 and 2. They show the interplay between the key factors influencing sector-wide acquisitiveness. Figure 1 demonstrates that the majority of transactions occur within highly fragmented, contestable industries with a relatively high degree of between-firm similarity. The presented three-dimensional chart shows the degree of acquisitiveness of firms depending on the similarity between firms in a given industry and the number of firms, which acts as a proxy for the degree of competition. The biggest cluster of transactions is seen in the area with a relatively high between-firm similarity and a high number of firms.

Interplay between intra-firm competition, degree of firm differentiation and industry acquisitiveness.

Kernel density estimate plots showing the differences between acquisitive and non-acquisitive industries in terms of industry concentration (a) and competition (b).

Kernel density estimates plots (Figure 2) compare acquisitive and non-acquisitive industries. We show that acquisitive industries have both a higher average number of firms (Figure 2a) and a higher degree of industry concentration (Figure 2b). These between-industry differences may suggest that smaller firms within acquisitive industries may be attractive acquisition targets. At the same time, these industries appear to exhibit a trend toward greater market power concentration in the future as industry leaders pursue further consolidation. In the long term, these sectors appear to be the most vulnerable to the potential detrimental consequences of growing concentration and consolidation. These are also the industries, where the returns to scale appear to be relatively higher and where gains from becoming the market leader in terms of size appear to be the most prominent. Due to dynamic growth, these industries are still in the relatively early phase of the consolidation cycle, however, the eventual winnowing of the most viable business models will precipitate a potent wave of takeovers led by a few industry champions. Therefore, regulatory scrutiny should pay particular attention to the dynamics of the degree of competition within these industries.

Overall, similarly to Ho and Hamilton (2000), our findings are inconclusive with regard to hypothesis H2. On one hand, we find a significant associative link between M&As and the market share of the combined entities. On the other hand, the relative competitive position of firms in the medium term appears unaffected by takeovers. New firm creation also appears unimpeded by corporate consolidations.

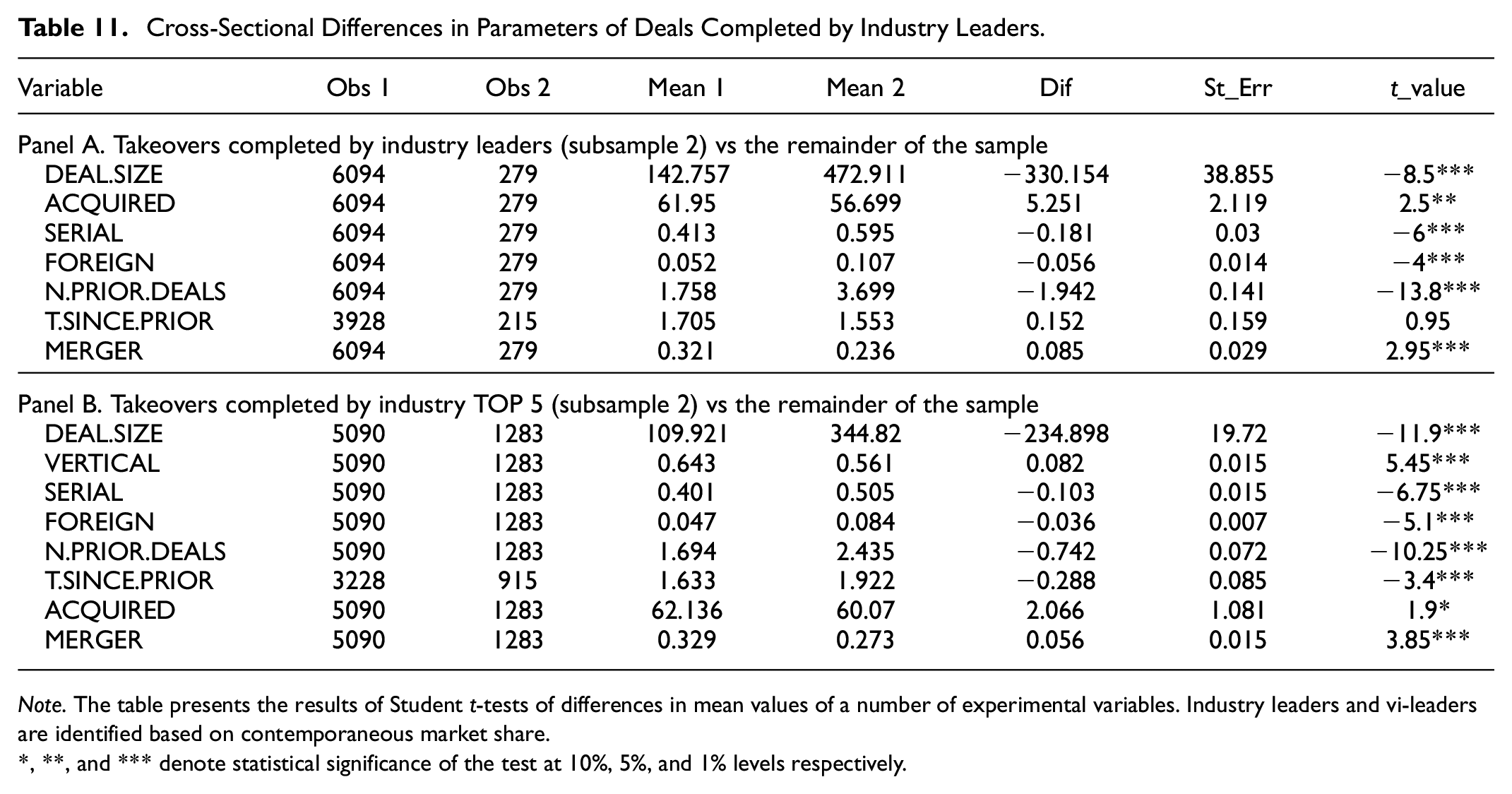

M&A Patterns of Industry Leaders and Outsiders

At the final stage of analysis, we elucidate factors differentiating between deals completed by sector leaders and outsiders. The results of univariate tests of differences in means are presented in Table 11. As opposed to the remainder of sampled companies, industry leaders and vice-leaders are found to engage in substantially larger transactions involving purchases of larger equity stakes. These deals are more likely to be structured as acquisitions, while in case of outsiders mergers appear to be much more prevalent. Thus, deals undertaken by outsiders seem to be motivated by efficiency considerations, while leaders seek to expand and differentiate themselves. This conjecture is proven by the fact that sector leaders and vice leaders are significantly more likely to engage in cross-border acquisitions. Because of their size, they are also more likely to be serial acquirers recording relatively shorter time lags between consecutive completed transactions. Overall, as evidenced in Table 12, industry leaders are statistically less likely to engage in inorganic growth than outsiders (OR: 0.78; sig.: 1%). Takeovers are more likely to occur within industries with a higher number of firms, more fragmented, and exhibiting higher rates of sales growth. The results remain robust under different modes of sample partitioning.

Cross-Sectional Differences in Parameters of Deals Completed by Industry Leaders.

Note. The table presents the results of Student t-tests of differences in mean values of a number of experimental variables. Industry leaders and vi-leaders are identified based on contemporaneous market share.

, **, and *** denote statistical significance of the test at 10%, 5%, and 1% levels respectively.

Likelihood of Takeovers Contingent Upon Acquirers’ Market Position.

Note. The table summarizes maximum likelihood estimates of binary logit models with the explained variables being the entities’ involvement in takeovers (panel A), mergers or acquisitions (panel B) during a given year. Z-coefficients are reported in parentheses under respective regression coefficients.

Significance of respective variables is denoted with asterisks: *p < .1. **p < .05. ***p < .01. The models include year fixed effects and firm-level controls.

Concluding Remarks

The present study attempts to look into the impact of corporate takeovers undertaken by Chinese public companies on the relative competitive positioning of firms and the degree of competition within industries subject to consolidation. Our quantitative analysis suggests that aside from those undertaken by industry leaders, M&As do not have a substantial effect on neither the combined entities’ market share nor on industry concentration. A number of implications emerge from the findings reported in the study.

To start with, we demonstrate that inorganic growth does not confer any significant competitive advantages to industry outsiders. Following deal completion, they appear unable to contest the market or overtake clients from the incumbent leaders. Their market share remains unaffected by M&As. In contrast, industry leaders can effectively use M&As for expansion, and thus preside over industry consolidation.

Second, since the bulk of transactions occurs within rapidly growing and fragmented industries, they are unlikely to threaten competition. Rather than concentrate market power, these deals appear to be directed at eliminating inefficient companies from the market. Deals completed by leading firms, which represent about 20% of all transactions, are, however, changing the market structure and leading to rapid concentration. This tendency appears to be more pronounced within commoditized industries, where leaders wield unsurmountable cost advantages. Therefore, regulators should exhibit caution with regards to the supervision of consolidation processes within such industries in order to preclude excessive concentration of market power.

Finally, unlike on other emerging markets, corporate consolidations in China do not lead to stifling of firm creation as rapid sales expansion creates space for new entrants. However, should the growth stagnate, the threat of corporate consolidations to competition may increase significantly.

The study has a number of limitations, which should be taken into consideration when analyzing the presented policy implications. To start with, the paper is based only on the analysis of M&As completed by publicly listed companies due to unavailability of comprehensive data for closely held companies. The composition of the resulting sample may have skewed the obtained empirical results. It also precludes the possibility of generalization to the population of privately owned companies.

Second, we do not analyze any cross-sectional patterns within specific industries. Instead, the study focuses on the patterns observable over the entire research sample with industry heterogeneity controlled through inclusion of industry-specific binary control variables into regression equations. Thirdly, the variable measuring target-acquirer complementarity using text-mined cosine similarity coefficient has some methodological shortcomings. In particular, the analysis is based on the descriptions of acquirers and targets in English rather than Chinese language. This may cause distortions in the measurement, which is however, mitigated by the fact that key text characteristics (length of description, common word frequency) follow a normal distribution for the entire research sample.

Finally, the policy recommendations are based on ex post statistical inference rather than on data obtained through natural experiment. The latter may cause the subsequent regulatory action based on presented policy guidelines to have unintended side effects or to fail in containing the possible negative repercussions of the observed waves of corporate consolidations in the future.

The follow-up studies should primarily focus on industry-specific patterns of corporate consolidations. Our findings hint at the possibility of rapid concentration of market power within the most susceptible commoditized industries including industrials, which are heavily represented among the public companies in China. Should concentration of market power become a concern, regulatory action could be targeted at specific industries rather than across the board in order to allow for productive consolidation of resources through takeovers of the less efficient companies, while preventing excessive concentration of market power and weakening of competition. Another strand of prospective empirical studies may revolve around the choices of acquisition targets by companies with different market positions. It may be interesting to know whether the outcomes of mergers and acquisitions are contingent upon the market power of acquiring entities. Finally, the findings presented in the paper could be linked to the theory of firm life cycle. Prospective studies could attempt to establish the stage of life cycle at which acquirers and targets are operating in order to predict or model the dynamics of future development within specific industries. Investigating the said features of mergers and acquisitions would necessitate an in-depth analysis of intertemporal patterns of transactions as well as a deep dive into the specificity of M&A waves observed over the last two decades.

Footnotes

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.

Ethics Statement

Not applicable.

Data Availability Statement

The data used in the study are available upon request from the corresponding author.