Abstract

This study investigates liquidity trends in key Southeast Asian markets, specifically focusing on the ASEAN-6 countries (Indonesia, Thailand, Singapore, Malaysia, Vietnam, and the Philippines) during and after the COVID-19 pandemic. Utilizing regression models, we analyze how trading volume, volatility, price movements, and their interactions have collectively influenced liquidity dynamics across these markets within 121 days around the pandemic’s announcement. We use three primary liquidity indicators: bid-ask spreads, Amihud’s illiquidity ratio, and the return-turnover ratio. The findings indicate that in the short term, COVID-19 shock, trading volume, and volatility significantly affected liquidity across the ASEAN-6 indices, with notable variations among the markets. Specifically, the Singapore and Malaysia markets demonstrated a greater capacity to absorb and adapt to pandemic-induced disruptions, showing the least decline and a swift recovery within 121 days around the pandemic’s announcement. Furthermore, our descriptive analysis highlights that Indonesia, Singapore, and Malaysia (KLSE) have emerged as the top-performing markets in terms of liquidity throughout the pandemic and its aftermath.

Introduction

The COVID-19 pandemic triggered unprecedented disruptions across global financial markets, revealing significant volatility and liquidity challenges that tested the resilience of both developed and emerging economies. Beginning with reports of pneumonia-like symptoms in Wuhan, China, in December 2019, the virus quickly spread worldwide. Initially thought to be a resurgence of SARS, it was soon identified as a novel coronavirus (2019-nCoV) by the World Health Organization (WHO). By March 2020, it was declared a global pandemic (Gofran et al., 2022; Salo, 2020). In response, governments worldwide enacted strict containment measures—such as border closures, lockdowns, and mask mandates—profoundly impacting industries reliant on travel and social interaction. This led to a 4.7% economic contraction across OECD countries in 2020 (Salo, 2020). The economic turmoil rapidly affected stock markets, driving investors to exit riskier assets and triggering sharp declines in major indices such as the S&P 500, FTSE 100, and MSCI Emerging Markets Index.

As the pandemic unfolded, global financial markets became increasingly sensitive to developments related to infection rates, vaccine progress, and policy responses, leading to significant fluctuations. The crisis also revealed significant shifts in market liquidity indicators, influencing bid-ask spreads, price impacts, and trading volumes across the globe. In the U.S. and Europe, bid-ask spreads for major indices expanded dramatically as investors sought liquidity, while emerging markets faced increased price impacts due to less robust trading infrastructures.

The ASEAN-6 countries—Indonesia, Malaysia, the Philippines, Singapore, Thailand, and Vietnam—exhibit rapid economic growth and evolving financial infrastructures, presenting significant growth potential. Each nation in this group possesses distinct economic characteristics; for instance, Indonesia, Thailand, and Vietnam are rich in natural resources, while Singapore serves as a global financial hub. Together, the ASEAN-6 comprises a young and growing population of over 600 million, creating diverse market demands.

Despite their crucial roles in economic development through facilitating capital raising and investment opportunities, the ASEAN-6 markets often encounter substantial risks, particularly related to liquidity. These challenges are primarily driven by political instability and economic volatility, which are compounded by smaller market sizes and less developed financial infrastructures compared to their counterparts in developed markets. The limited size of these markets typically results in a reduced number of shares available for trading, leading to lower trading volumes and increased price volatility. Moreover, underdeveloped financial infrastructures contribute to inefficiencies in trading and settlement processes, characterized by slower transaction speeds and higher costs. External shocks, such as the COVID-19 pandemic, further exacerbate these liquidity challenges by undermining investor confidence and disrupting economic activities. This disruption can lead to severe liquidity crises marked by heightened volatility, widened bid-ask spreads, and impaired market functioning.

While extensive literature exists on liquidity challenges in developed markets, there is a significant gap in understanding the unique challenges faced by ASEAN-6 markets during crises. Although some studies have explored the impact of COVID-19 on individual Asian economies, including Malaysia and Vietnam (Chia et al., 2023; Nguyen et al., 2021), a comprehensive examination across the ASEAN-6 countries is notably lacking. This research gap highlights the need for a broader exploration of how stock liquidity has been affected across these diverse markets in the post-pandemic period.

This study aims to analyze liquidity trends in the ASEAN-6 countries during and after COVID-19. By examining indicators such as bid-ask spreads, Amihud’s illiquidity ratio, return-turnover ratios, and trading volumes, the research seeks to identify the factors influencing market resilience and recovery in these key Southeast Asian markets.

Our study makes some significant contributions to the understanding of liquidity dynamics in the ASEAN-6 markets—Indonesia, Thailand, Singapore, Malaysia, Vietnam, and the Philippines—during and after the COVID-19 pandemic.

First, it addresses a critical gap in the literature on emerging market liquidity by providing a detailed analysis of how the pandemic affected these economies. We find that liquidity in the ASEAN-6 markets was profoundly impacted, with the most pronounced effects observed in Malaysia, Singapore, the Philippines, and Vietnam. This highlights the unique vulnerabilities of these markets to external shocks.

Second, the study employs a comprehensive range of liquidity indicators—such as bid-ask spreads, Amihud’s illiquidity ratio, return-turnover ratios, and trading volumes—to explore the drivers of market resilience and recovery. This approach not only identifies factors influencing liquidity but also reveals the distinct variations in liquidity responses across the ASEAN-6 countries. The findings shed light on how COVID-19 affected the relationship between liquidity and trading volume, illustrating the pandemic’s unique influence on markets throughout the region.

Finally, our research provides a valuable resource for policymakers, investors, and market participants by delivering empirical insights to support strategic decisions aimed at strengthening liquidity conditions in emerging Asian economies. Beyond capturing immediate market reactions, this study offers an in-depth look into the evolving liquidity landscape in the post-pandemic context, which is critical for navigating future uncertainties and enhancing market resilience. Understanding how stock liquidity adapted to significant economic shocks is essential for designing effective regulatory frameworks and market interventions. For investors, our analysis of bid-ask spreads, trading volumes, and Amihud ratios highlights liquidity trends and volatility in the ASEAN-6 markets, aiding in the assessment of market stability. These insights allow investors to evaluate liquidity risks, gauge the effects of crises like COVID-19 on their portfolios, and identify optimal entry or exit points. For corporate management, these findings inform capital-raising strategies, particularly in high-liquidity periods when issuing equity or debt may be less costly. Insights into liquidity dynamics amid external shocks support firms in developing robust strategies for future disruptions and managing stock liquidity more effectively. For governments and regulators, our findings lay a foundation for policies that stabilize markets in times of crisis. By identifying factors behind quicker recoveries in specific ASEAN markets, policymakers can reinforce economic fundamentals and financial infrastructure, enhancing resilience and investor confidence for a more stable market environment.

Literature Review

According to Alaoui Mdaghri et al. (2020), while stock markets are naturally influenced by major and exceptional events—such as sporting events, political events, social media content, natural disasters, and religious events (Kaplanski & Levy, 2010; Kollias et al., 2011; Liu & Zhang, 2015), no study had previously highlighted the significant impact of pandemics on global stock markets. However, the COVID-19 pandemic tells a different story. Baker et al. (2020) investigated its impact on global equity markets and found that the response was unprecedented. The volatility in the US equity market reached levels that surpassed those seen in October 1987, 1 December 2008, 2 and, before that, in late 1929 3 and the early 1930s.

Since the outset of the COVID-19 pandemic, numerous investigations have explored its influence on market liquidity in both developed and emerging capital markets. Many of these studies have concentrated on individual economies or specific industries.

Studies on Global Markets

Baig et al. (2020) examined how the pandemic affected the structure of US equity markets, analyzing fluctuations in liquidity and volatility using metrics that capture various aspects of the pandemic. They found that increases in COVID-19 cases and fatalities correlated with significant spikes in market illiquidity and volatility. Similarly, declining market sentiment and the enforcement of restrictions and lockdowns contributed to market instability and reduced liquidity. Li et al. (2020) investigated the liquidity challenges encountered by US banks, noting a surge in demand for liquidity in March 2020. They observed that firms drew extensively from existing credit lines and loan commitments in anticipation of disruptions to cash flow caused by economic shutdowns aimed at curbing the COVID-19 crisis. This heightened demand primarily affected the largest banks serving major firms, straining liquidity reserves, although banks managed to meet demand without facing severe financial constraints. Farzami et al. (2021) focused on the pandemic’s impact on liquidity linkages among different US industry sectors. Using an approach that examines lead-lag liquidity networks, they discovered that sectors had varying degrees of interdependence in terms of liquidity before COVID-19, with some sectors more interconnected than others. Their research highlighted that the pandemic significantly altered these liquidity networks, increasing interconnections across all sectors compared to pre-pandemic levels. The utilities sector experienced the most pronounced effects, whereas telecommunications services showed a relatively lesser impact.

In Australia, Narayan et al. (2021) assessed the pandemic’s impact on different sectors using a quantile regression approach. They observed that while the health, information technology, and consumer staples sectors benefited from the pandemic, other sectors experienced either negative impacts or remained largely unaffected.

Tiwari et al. (2022) explored the broader global impacts of the virus on market liquidity. Their study investigated the causality and co-movements between COVID-19 and aggregate stock market liquidity in China, Australia, and the G7 countries (Canada, France, Italy, Japan, Germany, the UK, and the US) from December 2019 to July 2020. Using wavelet coherency analysis, they found that the co-movements of market liquidity and COVID-19 outbreaks exhibited multi-scale dynamics. Particularly, illiquidity and COVID-19 cases and deaths showed strong co-movements at low frequencies.

Also, Gofran et al. (2022) investigated the liquidity impact of the COVID-19 pandemic on equity markets in the USA, UK, Brazil, China, Germany, and Spain. They found that the pandemic caused a short-term liquidity loss, evidenced by significant increases in bid-ask spreads. Their analysis of long-term financial stability using price impact ratios showed that only China experienced a lasting impact from COVID-19. Additionally, their examination of spread decomposition indicated that the widening of spreads was primarily due to information asymmetry rather than changes in trading costs around pandemic-related news. This finding was consistent across all the observed capital markets, except for China.

He et al. (2020) examined the global effects of COVID-19 on stock markets and associated spillover effects. Through statistical tests on daily stock returns from various countries including China, Italy, South Korea, France, Spain, Germany, Japan, and the USA, they found that COVID-19 initially exerted a short-lived negative impact on affected stock markets. They also observed mutual spillover effects between Asian and Western countries. Importantly, their study did not find evidence that the impact of COVID-19 on these stock markets exceeded the global average.

Research on Emerging Markets

Researchers have shown significant interest in analyzing China’s stock markets during the COVID-19 pandemic (Apergis et al., 2023; Cai & Zhang, 2023; P. Zhang et al., 2021). Al-Awadhi et al. (2020) highlighted that daily increases in confirmed cases and deaths in China had a substantial impact on stock returns across various market segments. Apergis et al. (2023) further noted that the pandemic had a pronounced negative effect on stock market liquidity in China, suggesting that smaller-cap firms may have been less severely impacted in terms of liquidity compared to larger firms. They identified three critical factors influencing liquidity during the pandemic: earnings dispersion, equity risk premia, and trade credit restrictions. Gofran et al. (2022) found that both U.S. and Chinese equity markets experienced significant price impacts due to COVID-19, with the effects persisting for up to 60 days after the outbreak. However, China’s equity market rebounded more swiftly, likely due to the earlier onset of the pandemic and lower mortality rates. Sansa (2020) also reported a strong correlation between new COVID-19 cases and stock market performance in both China and the U.S. during March 2020.

Karim et al. (2021) focused on the liquidity and financial stability of listed banks in Bangladesh, observing a decline in liquidity and financial health following the pandemic’s onset. The already weak liquidity ratios and financial metrics of these banks deteriorated notably in the second quarter of 2020. Alaoui Mdaghri et al. (2020) conducted one of the pioneering studies in the MENA region, investigating both tightness and depth aspects of stock market liquidity. They found that COVID-19 significantly affected liquidity, with depth measures positively correlated with the number of confirmed cases, deaths, and the stringency of pandemic measures. Both small-cap and large-cap firms experienced notable liquidity impacts due to rising case numbers, and the stringency index had a significant effect on liquidity depth.

In the Middle East, Tissaoui et al. (2021) documented the substantial impact of market volatility on market illiquidity in the Saudi stock market, using the multiple Wavelet coherence (MWC) technique. They found that the COVID-19 outbreak had a negative impact on market liquidity, with a strong response to the total number of confirmed cases. Their analysis also revealed that extreme volatility was likely to occur in the short and medium terms.

Farooque et al. (2023) compared the pandemic’s effects on stock liquidity across six developed and emerging economies. Their findings showed that infection rates and death tolls significantly reduced stock liquidity across all sampled countries, with a stronger impact in developed economies and among firms facing high economic policy uncertainty (EPU). Conversely, the effect was less pronounced in emerging economies, firms with lower EPU, and larger firms.

ASEAN-Specific Works

While numerous past studies have highlighted the potential impact of pandemics on ASEAN stock markets (e.g., Adnan, 2023; Chopra & Mehta, 2022; Mishra & Mishra, 2021; Rabhi, 2020; Wang et al., 2023), the specific effects of the COVID-19 outbreak on market liquidity remain underexplored. Some researchers have focused on individual markets, such as Vietnam (Nguyen et al., 2021) and Malaysia (Chia et al., 2023).

Nguyen et al. (2021) investigated the influence of the COVID-19 outbreak and the Vietnamese government’s disease control measures on stock returns and liquidity among Vietnam-listed companies in the financial services sector. Analyzing data from 50 banking, insurance, and finance companies from January 30, 2020, to May 15, 2021, the study found that the daily growth in COVID-19 cases significantly impacted stock market returns and liquidity. The authors also noted that government-imposed lockdowns had a positive effect on stock performance, with significant variations in returns between large-cap and small-cap stocks during the pandemic.

Chia et al. (2023) examined the impact of COVID-19 and related government policies on stock liquidity among the top 30 companies on the FTSE Bursa Malaysia KLCI. Their findings revealed a negative correlation between the number of COVID-19 cases and stock liquidity, while vaccination programs had a positive impact. Sector-specific analysis indicated increased liquidity in the transportation, logistics, and energy sectors, but significant negative effects on the plantation sector. Vaccination programs were particularly beneficial for liquidity in the utilities sector.

Mishra and Mishra (2021) analyzed stock market behavior in 15 selected Asian markets during the COVID-19 pandemic. Their findings indicate a surge in market return volatility, driven primarily by impaired investor sentiment in response to announcement effects. The study observed that stock market performance in these Asian countries was influenced by various factors, including the number of confirmed COVID-19 cases and deaths, stock index returns, market volatility, oil prices, inflation rates, and interest rates. Despite these insights, comprehensive research on the impact of the COVID-19 pandemic on stock market liquidity across ASEAN countries remains relatively limited.

Research Hypotheses

The Efficient Market Hypothesis (EMH) states that stock prices reflect all available information (Fama, 1970), which influences market price adjustments, especially during crises like COVID-19. Access to information is crucial for analyzing market reactions to news and events, with the media playing a key role in information dissemination.

Market uncertainty—due to factors like interest rate fluctuations, inflation, and exceptional events—greatly impacts investors’ information needs (Hasan et al., 2018). During a pandemic, this uncertainty can heighten information asymmetries, complicating assessments of economic fundamentals and leading to reduced trading activity, wider bid-ask spreads, and decreased liquidity. Investor reactions to new information were evident during the COVID-19 outbreak, which significantly affected stock market performance.

Additionally, insights from Behavioral Finance show that investor sentiment is crucial in crises. Heightened anxiety can lead to increased selling pressure as investors rush to liquidate holdings, further deteriorating liquidity. Studies have explored investors’ reactions to COVID-19 across various countries, indicating that both private and public information influence stock prices (see, Neupane et al., 2024; Smales, 2020; Y. Zhang & Sun, 2023).

In light of the theoretical and empirical frameworks established, we propose several hypotheses to guide our investigation:

Methodology

Data Collection

We analyze the markets of the six largest countries in the Association of Southeast Asian Nations (ASEAN-6), including Indonesia, Thailand, Singapore, Malaysia, Vietnam, and the Philippines. These countries have witnessed some of the most rapid economic growth in recent years, driven by robust domestic consumption, expanding middle classes, and increasing foreign investment. Our study focuses on the performance of the benchmark indices: FTSE Bursa Malaysia KLCI (Malaysia), IDX Composite (Indonesia), PSEi Index (Philippines), SET (Thailand), STI (Singapore), and VN-Index (Vietnam). Table 1 provides detailed information about each index.

Overview of Six Indices in the Research.

To explore the effects of COVID-19 on market liquidity, we gathered daily closing prices for each index within a [−60, +60] day period centered around March 11, 2020. This date was chosen as it coincides with the World Health Organization’s declaration of COVID-19 as a pandemic, marking a significant turning point in global financial markets (Salo, 2020). All data used in our analysis was sourced from Bloomberg Terminal, ensuring consistency and reliability in our study.

Research Method

We will analyze the effects of trading volume, volatility, and the COVID-19 shock on liquidity measures across six key indices: FTSE Bursa Malaysia KLCI, IDX Composite, PSEi Index, SET, STI, and VN-Index. Initially, we will investigate the impact of the COVID-19 shock on liquidity over a 121-day period surrounding the announcement date of the pandemic. To do this, we will adopt a multivariate regression approach, following the methodologies outlined by Gregoriou (2015) and Gofran et al. (2022) (see Equation 1). Subsequently, we will further analyze the performance of liquidity measures from January 2020 to June 2024 for all six indices: FTSE Bursa Malaysia KLCI, IDX Composite, PSEi Index, SET, STI, and VN-Index.

Where i represents the index (FTSE Bursa Malaysia KLCI, IDX Composite, PSEi Index, SET, STI, and VN-Index) and t represents day (−60, +60). Liquidity is the liquidity for indices i at time t. Volume represents the logarithm of the trading volume (for index i at time t). Covid represents the dummy variable which is equal to 1 during the post-pandemic announcement period and 0 otherwise. Price represents the closing price of index i at time t. Volatility is return standard deviation for index i at time t for each trading day in the event window [− 60, +60].

Liquidity Measure

Study by Sarr and Lybek (2002) notes that liquid markets generally exhibit four primary characteristics: (1) Depth, which denotes the ability to trade a specific volume of assets without significantly affecting their quoted price; (2) Tightness, linked to low transaction costs, indicating the capability to buy and sell assets at comparable prices simultaneously; (3) Immediacy, reflecting trading efficiency by measuring the time required to execute orders promptly; and (4) Resiliency, referring to the quick absorption of new orders to correct market imbalances. However, it’s important to recognize that no single liquidity measure fully encompasses all these dimensions.

Due to the multifaceted nature of liquidity, we chose to employ various proxies to capture aspects of market depth and tightness. Owing to data limitations, we did not include measures for resiliency and immediacy. Market depth is assessed using Amihud’s (2002) illiquidity measure, and for market tightness, typically gauged by bid-ask spreads, we utilized the relative spread as the second dependent variable.

We construct the Amihud illiquidity measure following Amihud (2002), defined as the absolute value of stock return divided by the dollar trading volume on a given trading day.

Where n is the number of days,

The Amihud illiquidity measure presents both strengths and weaknesses. As highlighted by Le and Gregoriou (2020), this measure effectively serves as a benchmark for assessing liquidity. The Amihud measure, which links stock returns to dollar volume, provides a clear framework for understanding the impact of trading volume on price movements. This is particularly relevant for analyzing liquidity dynamics during and after the COVID-19 pandemic. By capturing price sensitivity to trading activity, the Amihud measure is essential for identifying liquidity fluctuations in volatile markets

However, it does suffer from a limitation identified by Azevedo et al. (2014) and Florackis et al. (2011) regarding its inability to compare stocks across different market capitalizations, thereby introducing a size bias. Florackis et al. (2011) proposed a remedy with their liquidity measure named return-to-turnover ratio (RtoTR), designed specifically to mitigate this size bias. This measure normalizes returns relative to trading volume, mitigating size bias and enabling equitable comparisons among firms. By integrating the turnover ratio, the RtoTR provides a comprehensive view of market tightness and trading efficiency, which is crucial for understanding liquidity dynamics.

Where n is the number of days,

We follow Gofran et al. (2022) compute the relative spread of around the 60 days pre- and post-pandemic announcement date, March 11, 2020, by the WHO using the following equation:

Where i represents the index (FTSE Bursa Malaysia KLCI, IDX Composite, PSEi Index, SET, STI, and VN-Index) and t represents day (−60, +60). High and Low are the high price and low price of index i at day t.

Results and Discussions

Statistical Description

Figure 1 displays the time-series plots of six major stock market indices: FTSE Bursa Malaysia KLCI, IDX Composite, PSEi Index, SET, STI, and VN-Index. The charts reveal significant declines across all indices in mid-March, coinciding with the announcement of the COVID-19 pandemic. This evidence underscores the profound impact of the pandemic on global financial markets. Among these indices, the PSEi Index suffered the most drastic decline, plummeting nearly 40% from its peak within the 121-day period surrounding the COVID announcement date. Conversely, the FTSE Bursa Malaysia KLCI showed the smallest decline, with a drop of 25% from its highest point during the same period.

Stock market indices around the COVID-19 pandemic announcement date, March 11, 2020.

The charts reveal significant declines across all indices in mid-March, coinciding with the announcement of the COVID-19 pandemic. This evidence underscores the profound impact of the pandemic on global financial markets. Among these indices, the PSEi Index suffered the most drastic decline, plummeting nearly 40% from its peak within the 121-day period surrounding the COVID announcement date. Conversely, the FTSE Bursa Malaysia KLCI showed the smallest decline, with a drop of 25% from its highest point during the same period. Additionally, the FTSE Bursa Malaysia KLCI demonstrated resilience by quickly recovering from the COVID-19 shock. Within the 60-day period following the COVID announcement date, the index nearly returned to its pre-COVID peak. Similarly, the VN-Index and SET also exhibited strong recovery trends over the same period.

Table 2 provides a statistical overview of key liquidity variables across six major indices: FTSE Bursa Malaysia KLCI, IDX Composite, PSEi Index, SET, STI, and VN-Index. The relative spread (Spread), which measures market tightness and transaction costs, varies across these indices, showcasing notable differences. FTSE Bursa and STI exhibit lower mean relative spreads (0.012 and 0.015, respectively), suggesting tighter markets compared to IDX (0.019), PSEi (0.019), SET (0.019), and VN-Index (0.020).

Variable Description.

Note. Standard deviations are in parentheses.

In terms of market depth, measured by the Amihud illiquidity measure, STI shows the lowest mean (0.002), indicating deeper liquidity, while PSEi displays the highest mean (6.664), indicating relatively shallower market depth. The turnover ratio to trading volume (RtoTR), designed to mitigate size bias in liquidity measures, also varies significantly across indices, with SET having the highest mean (39.423) and FTSE Bursa the lowest (6.167).

Overall, the STI index and FTSE Bursa Malaysia KLCI stand out as the most liquid markets among the indices analyzed. They exhibit the lowest Relative Spread at 0.015 and 0.012, respectively, indicating the tightest market conditions, and the lowest Amihud Illiquidity measure at 0.002 and 0.004, respectively, suggesting good market liquidity. Additionally, the STI and FTSE Bursa Malaysia KLCI have lower RtoTR values of 13.368 and 6.167, which is favorable as smaller RtoTR values indicate better liquidity and less size bias. In contrast, markets like the SET and IDX Composite show higher RtoTR values, indicating relatively lower liquidity. Therefore, the combination of tight spreads, low illiquidity, and favorable RtoTR position the STI and FTSE Bursa Malaysia KLCI as the markets with the best overall liquidity.

On the contrary, the PSEi Index emerges as the most illiquid market among the indices analyzed. It has a relatively high Relative Spread of 0.019, indicating less tight market conditions compared to other indices like the FTSE Bursa Malaysia KLCI and STI. Moreover, the PSEi Index’s exceptionally high Amihud Illiquidity Measure of 6.664 highlights its substantial illiquidity, as this measure indicates significant price changes in response to trading volumes. Although the PSEi Index has a high RtoTR of 31.718, which reflects active trading relative to market capitalization, this trading activity does not mitigate its overall illiquidity. The combination of a high relative spread, extraordinarily high Amihud Illiquidity Measure, and high RtoTR underscores the severe liquidity challenges faced by the PSEi Index, making it the market with the lowest liquidity in this analysis.

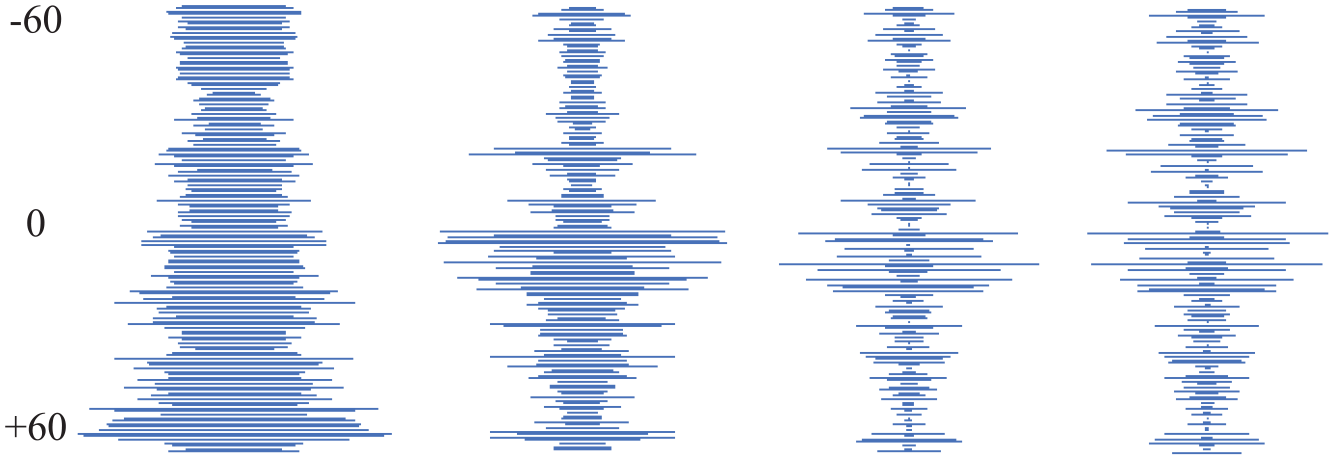

Figures 2 to 7 illustrate the funnel charts for the six indices: FTSE Bursa Malaysia KLCI, IDX Composite, PSEi Index, SET, STI, and VN-Index. These charts present data on the following variables: Volume, Spread, Amihud, and RtoTR in the 121 trading days around the COVID announcement date.

Funnel charts for FTSE Bursa Malaysia KLCI in 121 trading days around COVID announcement date. (Volume, Spread, Amihud, RtoTR).

Funnel charts for IDX composite in 121 trading days around COVID announcement date. (Volume, Spread, Amihud, RtoTR).

Funnel charts for PSEi Index in 121 trading days around COVID announcement date. (Volume, Spread, Amihud, RtoTR).

Funnel charts for SET in 121 trading days around COVID announcement date. (Volume, Spread, Amihud, RtoTR).

Funnel charts for STI in 121 trading days around COVID announcement date. (Volume, Spread, Amihud, RtoTR).

Funnel charts for VN-Index in 121 trading days around COVID announcement date. (Volume, Spread, Amihud, RtoTR).

Across the six markets analyzed, Spread, Amihud, and RtoTR all exhibited notable fluctuations following the COVID-19 announcement. These liquidity proxies experienced significant increases, reflecting a pronounced reduction in market liquidity across Southeast Asian stock markets. This underscores the substantial impact of COVID-19 shock on market liquidity specifically, and financial markets more broadly.

Notably, in the 60-day period following the COVID-19 announcement, the Vietnamese, Singaporean, and Philippine markets continued to exhibit elevated Spread compared to the period before COVID-19. Furthermore, the Philippine market sustained high levels of Amihud and RtoTR ratios, indicating a prolonged impact of COVID-19 on liquidity in this market compared to others.

Although volume experienced a significant shock on and immediately after the announcement date, it appears to have followed an increasing trend over time across all indices.

Table 3 presents the results of T-tests, which compare the means of two groups. We conducted T-tests for various time windows: 5 days before and after the COVID announcement date (−5,+5), 10 days before and after the COVID announcement date (−10,+10), 30 days before and after the COVID announcement date (−30, +30), and 60 days before and after the COVID announcement date (−60,+60).

Liquidity Proxies Around the COVID-19 Pandemic Announcement Date, March 11, 2020.

p < .01. **p < .05. *p < .10.

Regression Results

Table 4 presents regression results examining the impact of the COVID-19 shock on market liquidity over a 121-day period surrounding the COVID-19 announcement date. The analysis focuses on liquidity measures, including the Relative Spread, Amihud’s Illiquidity Measure, and the return-to-turnover ratio (RtoTR), across the ASEAN-6 indices: FTSE Bursa Malaysia KLCI (KLSE), IDX Composite (IDX), PSEi Index (PSEi), SET Index (SET), Straits Times Index (STI), and VN-Index (VN Index). The R-squared values, ranging from 0.4215 to 0.9222, indicate a strong fit for the model, while the F-test values confirm the overall significance of the regressions.

Regression Results.

p < .01. **p < .05. *p < .10.

COVID-19 Impact (Covid)

Overall, the COVID-19 shock harms liquidity in ASEAN-6 markets with most of the indices experiencing increasing spreads and Amihud ratios after the pandemic’s announcement date.

In the Spread model, the COVID-19 dummy variable reveals a significant and positive coefficient for several indices: FTSE Bursa Malaysia KLCI (0.004, p < .05), PSEi Index (0.007, p < .1), STI (0.006, p < .05), and VN-Index (0.004, p < .05). These findings suggest that spreads widened following the pandemic announcement, indicating a decline in liquidity within these markets. In contrast, the coefficient for the IDX Composite is negative (−0.008) but lacks statistical significance, reflecting a less definitive impact of COVID-19 on its liquidity. The increase in spreads translates to higher transaction costs for investors, which may discourage trading activity. Policymakers should recognize that elevated spreads can indicate market stress, underscoring the necessity for interventions to maintain liquidity during crises.

The PSEi Index of the Philippines exhibited a significant positive impact of COVID-19 on Amihud, indicating decreased liquidity during the pandemic period. Additionally, indices like the FTSE Bursa Malaysia KLCI and the STI Index showed smaller positive effects that were statistically significant at lower confidence levels, suggesting some reduction in liquidity, although less pronounced compared to the PSEi.

In the TtoTR model, the IDX Composite and PSEi Index exhibit positive coefficients of 20.338 and 13.681, respectively, indicating substantial declines in liquidity following the pandemic announcement. In contrast, the SET Index shows a negative coefficient of −8.824, suggesting an increase in liquidity, although this result is not statistically significant. These varied responses to external shocks highlight the necessity for regulators to tailor their strategies to effectively address the distinct needs of each market.

Trading Volume (Volume)

The trading volume shows a significant and positive impact on Spread for Malaysian market (2.52E-11, p < .01), Singapore market (1.23E-09, p < .05), and Vietnamese market (2.08E-10, p < .01), suggesting that higher trading volumes are associated with increased spreads and thus reduced liquidity. The impact on the other indices is positive but not significant.

However, in both the Amihud and RtoTR models, trading volume consistently showed negative coefficients across all indices, indicating that trading volume positively impacts liquidity. Specifically, reduced (or increased) trading volume is associated with decreased (or increased) liquidity during the analyzed period in these markets. This relationship underscores the fundamental principle that heightened trading activity typically reflects deeper and more liquid markets, which facilitate smoother transactions and better price discovery, especially during market disruptions.

While elevated trading volumes can signal a healthy market, they may also lead to liquidity challenges in times of crisis. For investors, being aware of trading volume trends can enhance decision-making, while regulators might consider strategies to encourage sustained trading activity to promote liquidity.

Interaction of Volume and COVID-19 (Volume x Covid)

The interaction term between trading volume and COVID-19 demonstrates a significant positive impact on the Spread for the PSEi Index in the Philippines (2.83E-08, p < .1). This finding indicates that the combination of increased trading volume during the post-pandemic period results in a wider spread, further exacerbating the decline in liquidity. In contrast, the other indices do not exhibit significant interaction effects on the Spread.

Additionally, the Amihud and RtoTR measures show a significant positive relationship with the interaction variable in the Indonesian, Singaporean, and Vietnamese markets. This suggests that heightened trading volumes in conjunction with the pandemic environment intensify illiquidity effects or restrict liquidity in these markets. The moderating effect of COVID-19 on the relationship between volume and liquidity is noteworthy. During the turbulent periods triggered by the pandemic, COVID-19 significantly undermines market liquidity in certain ASEAN-6 economies.

This finding implies that, during crises, simply having higher trading volumes may not be enough to ensure liquidity; the surrounding context is crucial. Regulators should be aware of the dynamics between market conditions and trading behaviors to formulate effective strategies for sustaining liquidity.

Volatility (Volatility)

Volatility consistently shows significant positive coefficients across all indices (p < .01), demonstrating a strong correlation between higher volatility and increased spreads. This relationship reflects the heightened risk and uncertainty associated with volatility, which tends to diminish liquidity. As anticipated, increased volatility generally results in wider spreads due to the associated risks, further constraining liquidity. For investors, understanding that volatility can lead to reduced liquidity underscores the importance of effective risk management strategies. Regulators should also consider implementing measures to mitigate the impact of volatility, such as establishing circuit breakers to temporarily suspend trading during extreme market conditions.

Price (Price)

The price variable exhibits significant negative coefficients for FTSE Bursa Malaysia KLCI (−0.000, p < .01), IDX Composite (−1.2E-05, p < .01), SET (−3.84E-05, p < .01), and VN-Index (−0.000, p < .01), suggesting that lower prices are associated with larger spreads, indicating reduced liquidity and vice versa. For the STI, the price coefficient is positive but not significant.

In the Amihud model, only SET shows a statistically significant coefficient for the closing price. This suggests that price movements may have influenced liquidity dynamics inversely during the pandemic period, possibly due to market-specific factors or investor behaviors.

Notably, the data for Singapore and Malaysia indices exhibit a positive coefficient in the RtoTR model, suggesting that despite the high volatility in prices due to the impact of COVID-19, the effects of COVID-19 on stock prices in Singapore and Malaysia are less prolonged compared to other ASEAN-6 countries. This finding aligns with the earlier analysis showing that the FTSE Bursa Malaysia KLCI experienced the least decline and rapid recovery following the COVID-19 shock during the (−60, +60) time window. The relative stability and quick recovery of the Singapore and Malaysia markets suggest that these markets were better able to absorb and adapt to the disruptions caused by the pandemic. Factors contributing to this resilience could include stronger economic fundamentals, effective government interventions, and well-developed financial infrastructures. This relative robustness might have helped maintain investor confidence, leading to more stable trading patterns and less pronounced price declines. The interconnectedness of price and liquidity highlights that substantial price drops can negatively impact trading conditions. For investors, remaining vigilant during periods of sharp price movements is essential, while regulators should ensure that sufficient measures are in place to stabilize prices and maintain liquidity.

Liquidity Performance From COVID-19 to the Present

This section provides the overview of the performance of liquidity measures over the period from January 2020 to June 2024 for all six indices: FTSE Bursa Malaysia KLCI, IDX Composite, PSEi Index, SET, STI, and VN-Index.

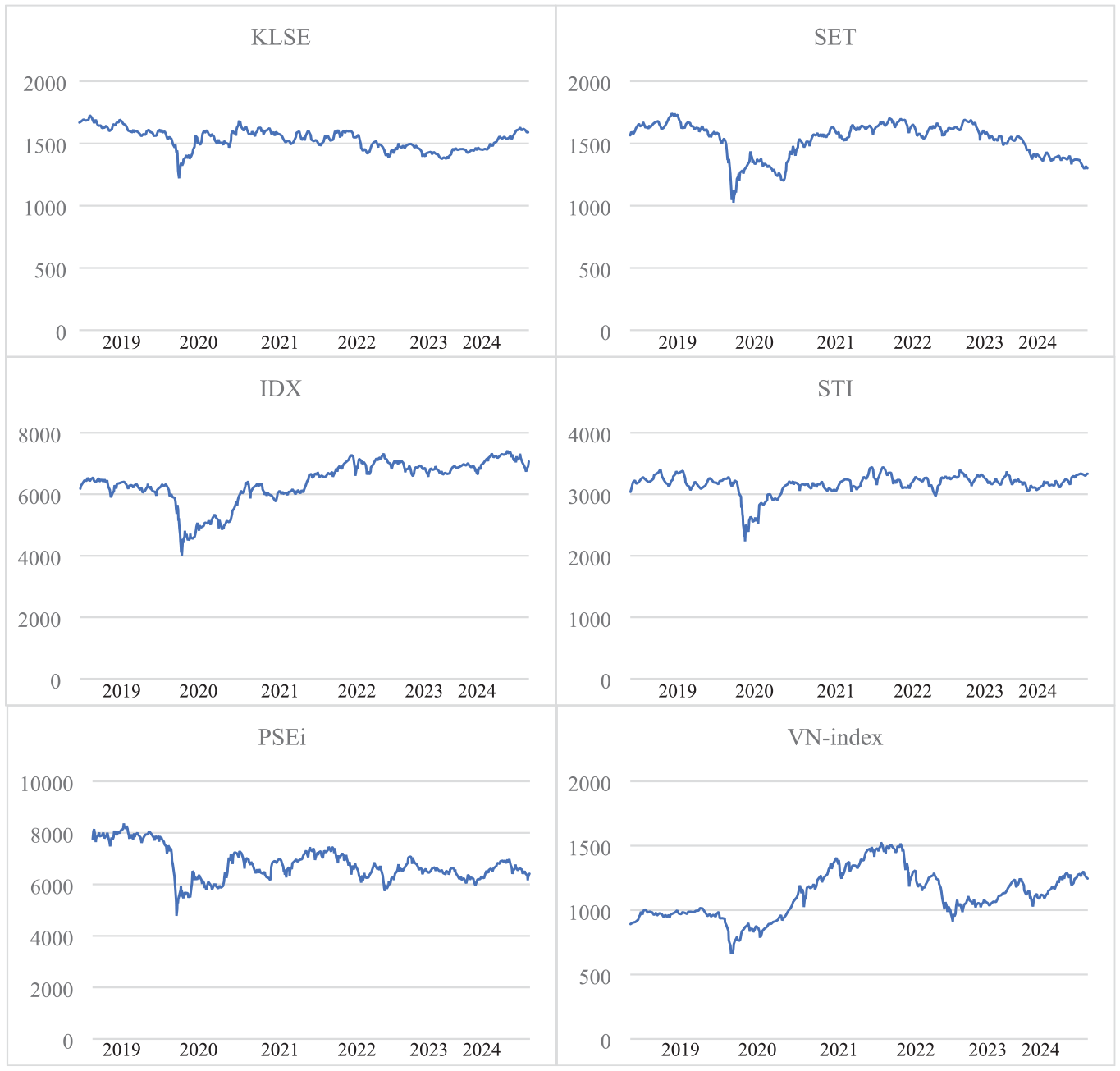

Figure 8 displays the time-series plots for the prices of the six indices mentioned above. Overall, after a sharp decline in price, characterized by high volatility, at the onset of the COVID-19 pandemic in 2020, there was a general trend of gradual recovery across these indices post-COVID-19. Despite differences in the pace of recovery, all indices showed signs of rebounding from their pandemic lows. This recovery might be a result of government stimulus measures, fiscal policies, and support for key sectors that played crucial roles in stabilizing markets and aiding recovery.

Stock market indices from January 2019 to June 2024.

In detail, the IDX Composite in Indonesia and the VN-Index in Vietnam showed some of the strongest recoveries in overall price levels among the ASEAN indices post-COVID-19. After an initial decline, both indices swiftly rebounded, propelled by robust economic growth and effective management of the pandemic. Not only did the overall price levels of these indices recover, but they also surpassed pre-pandemic highs, reflecting strong economic performance and heightened investor confidence.

However, despite the impressive rebounds in 2021 and 2022, the VN-Index displayed the highest price fluctuations during 2023 and 2024. This volatility highlights the necessity for continuous monitoring of market conditions. Regulators in these regions should prioritize the implementation of policies aimed at enhancing market resilience, especially in anticipation of potential future disruptions. Strategies that focus on increasing transparency and providing targeted support measures can be crucial in stabilizing liquidity and maintaining investor trust during challenging periods.

The PSEi Index in the Philippines experienced the slowest recovery in overall price levels compared to other ASEAN indices. Following a significant decline at the onset of the pandemic, the PSEi’s recovery was hindered by prolonged lockdowns and economic contractions. Although there was some improvement as restrictions were lifted, the overall price levels of the PSEi remained below pre-pandemic benchmarks, reflecting a more drawn-out recovery process. This sluggish recovery highlights the need for regulators to take proactive measures to address the unique challenges faced by struggling markets. Implementing targeted fiscal stimulus or support for critical sectors could play a vital role in revitalizing these economies and fostering a stronger recovery.

The Straits Times Index (STI) experienced a steady recovery in overall price levels following the COVID-19 pandemic. By late 2021, the STI had approached their pre-pandemic levels and continued to stabilize through 2022 and 2023. The FTSE Bursa Malaysia KLCI saw a quick recovery in overall price levels in 2020 and 2021. However, despite this recovery, the KLCI’s overall price level remained subdued compared to pre-pandemic highs, reflecting ongoing economic challenges and uncertainties. Thailand’s SET index saw a strong recovery in overall price levels post-COVID in 2021 and 2022. The SET index’s overall price levels managed to climb back to, and even surpass pre-pandemic levels, reflecting the resilience of Thailand’s economy and the effectiveness of government measures. However, the index has dropped almost 8% so far this year, following a 15% decline in 2023, accompanied by a significant drop in daily trading value. These fluctuations in liquidity measures across the various indices underscore the need for continuous vigilance from both market participants and regulators. A comprehensive understanding of the factors influencing liquidity can help stakeholders adapt their strategies and regulatory frameworks to promote enhanced market stability.

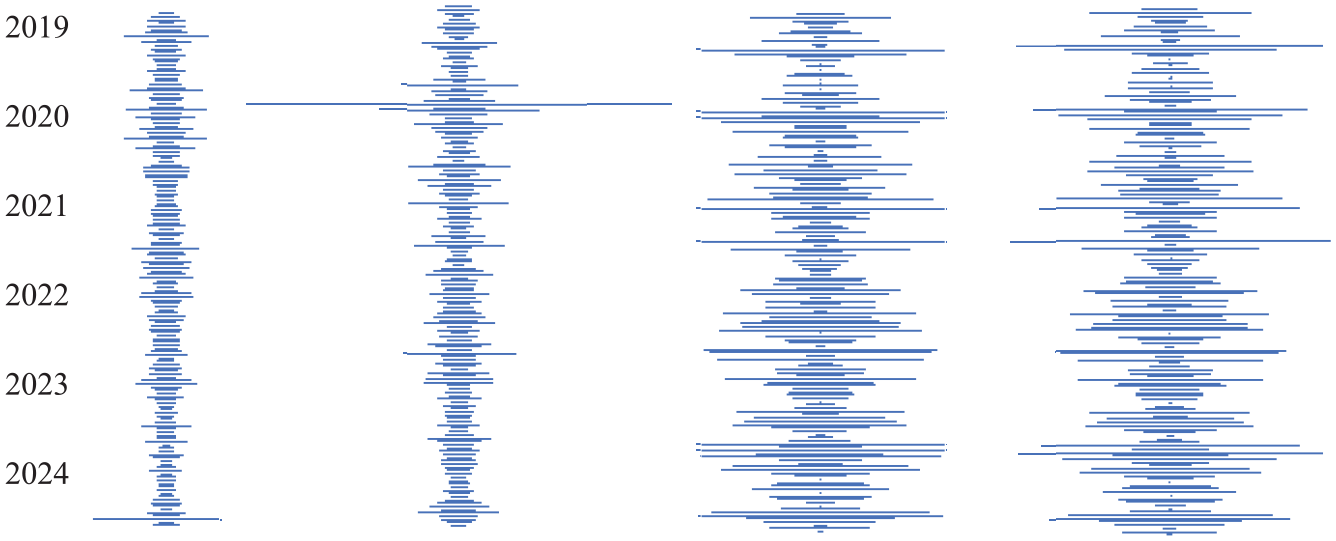

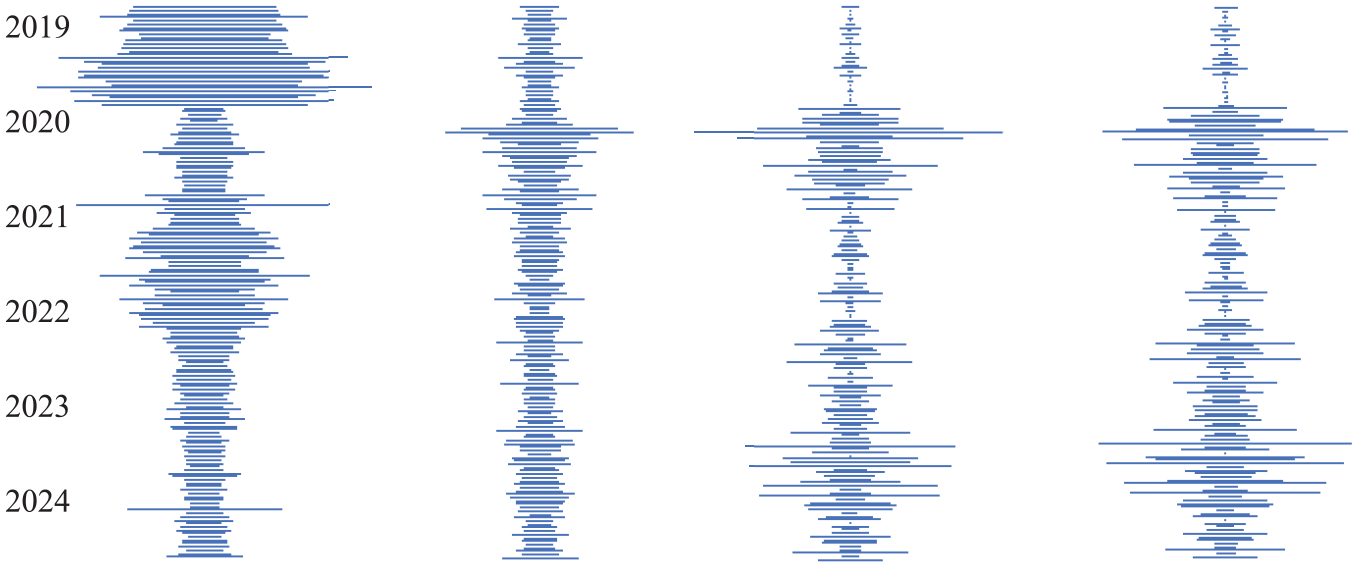

Figures 9 to 14 present funnel charts for the six indices, focusing on Volume, Spread, Amihud, and RtoTR from January 2019 to June 2024. The IDX Composite and VN-Index showed a significant increase in trading volume post-COVID-19, whereas the SET Index and PSEi Index saw a notable decline compared to pre-COVID-19 levels in 2019. This trend aligns with the previously analyzed price movements of these indices.

Funnel charts for FTSE Bursa Malaysia KLCI from 2019 to 2024. (Volume, Spread, Amihud, RtoTR).

Funnel charts for IDX composite from 2019 to 2024. (Volume, Spread, Amihud, RtoTR).

Funnel charts for PSEi Index from 2019 to 2024. (Volume, Spread, Amihud, RtoTR).

Funnel charts for SET from 2019 to 2024. (Volume, Spread, Amihud, RtoTR).

Funnel charts for STI from 2019 to 2024. (Volume, Spread, Amihud, RtoTR).

Funnel charts for VN-Index from 2019 to 2024. (Volume, Spread, Amihud, RtoTR).

The STI Index, despite stable trading volumes before and after COVID-19, experienced significant volatility in the latter half of 2023 and the first half of 2024. This volatility is likely due to global economic uncertainties, including fears of potential recessions and fluctuating inflation rates, contributing to market instability.

In terms of relative spread, the VN-Index displayed a different trend compared to other indices. While other markets saw spreads return to pre-2019 levels after initially increasing during COVID-19, the VN-Index continued to exhibit high spreads into 2024, indicating ongoing liquidity challenges or other trading issues beyond the pandemic period.

The Amihud and RtoTR patterns varied across the indices. Markets in Malaysia and Indonesia showed effective control over these liquidity measures, with decreasing trends post-COVID-19. Conversely, the Philippine stock market maintained high levels of these measures during and after COVID-19. The SET Index, despite performing well in terms of Amihud and RtoTR in 2021 and 2022, faced high ratios in 2023 and the first half of 2024, even surpassing pre-COVID-19 levels. Notably, the STI Index in Singapore experienced considerable volatility in 2023 and 2024, which may result from substantial fluctuations in trading volume during the same periods.

Conclusion

Our research offers valuable insights into liquidity performance during and after the COVID-19 period. First, we employed regression models to explore how trading volume, volatility, price movements, and their interactions collectively influenced liquidity dynamics across the ASEAN-6 markets. Following this, we provided a descriptive overview of how liquidity measures behaved in these markets post-COVID-19. This knowledge is crucial for policymakers, investors, and market participants to navigate and manage liquidity risks in dynamic economic environments, especially during times of heightened uncertainty and market volatility.

Our results indicate that COVID-19, trading volume, and volatility significantly impact liquidity measured by spread across the ASEAN-6 indices, with notable variations among different markets. The increase in spreads post-COVID-19 and with higher volatility highlights the challenges in maintaining liquidity under stress conditions.

Notably, the data for Malaysia and Singapore indices exhibit a positive coefficient in the return-to-turnover (RtoTR) model, suggesting that despite the high volatility in prices due to the impact of COVID-19, the effects of COVID-19 on stock prices in Singapore and Malaysia are less prolonged compared to other ASEAN-6 countries. This finding aligns with the earlier analysis showing that the FTSE Bursa Malaysia KLCI experienced the least decline and rapid recovery following the COVID-19 shock during the (−60, +60) time window. The relative stability and quick recovery of the Singapore and Malaysia markets suggest that these markets were better able to absorb and adapt to the disruptions caused by the pandemic. Factors contributing to this resilience could include stronger economic fundamentals, effective government interventions, and well-developed financial infrastructures. This relative robustness might have helped maintain investor confidence, leading to more stable trading patterns and less pronounced price declines.

During the COVID-19 pandemic, large trading volumes have a positive impact on the relative bid-ask spread but a negative impact on the Amihud ratio and return-to-turnover ratio (RtoTR), despite all being measures of illiquidity. This outcome can be explained due to their focus on different aspects of market liquidity and the distinct market dynamics at play. The relative bid-ask spread is the difference between the highest price a buyer is willing to pay (bid) and the lowest price a seller is willing to accept (ask), normalized by the midpoint price. During times of high volatility and uncertainty, such as the COVID-19 pandemic, large trading volumes can lead to wider bid-ask spreads. This widening occurs because market makers face higher risks and potential order imbalances, leading them to demand greater compensation for providing liquidity. Additionally, heightened trading activity can reflect significant buy or sell pressures and increased information asymmetry among traders, causing market makers to adjust prices to account for these factors, further widening the spread. In contrast, the Amihud ratio and return-to-turnover ratio (RtoTR) measure the price impact of trades by calculating the daily absolute return divided by the daily trading volume. A negative relationship between trading volume and the Amihud ratio suggests that larger trading volumes reduce the price impact per unit of volume, indicating better liquidity. This is because higher trading volumes can facilitate more efficient price discovery and enhance market depth, allowing large trades to be absorbed without significantly moving the price. Consequently, the price impact of individual trades decreases, reflecting improved liquidity conditions. In summary, during the COVID-19 pandemic, large trading volumes can increase the relative bid-ask spread due to the higher risks and uncertainties faced by market makers, leading to wider spreads. Simultaneously, these large volumes can decrease the Amihud ratio by indicating better market depth and more efficient price discovery, reducing the price impact of trades. This divergence arises because the above-mentioned measures capture different dimensions of liquidity and respond differently to the same market conditions.

Indonesia (IDX Composite), Singapore (Straits Times), and Malaysia (KLSE) have emerged as the top-performing markets in terms of liquidity during and after COVID-19. Their ability to maintain stable liquidity measures and narrower bid-ask spreads throughout the pandemic underscores their resilience and effective regulatory responses. Vietnam (VN-Index) also demonstrated a notable recovery, reflecting robust economic fundamentals and effective management of the pandemic. Well-developed financial infrastructures and proactive measures by regulatory authorities played a pivotal role in supporting market stability. In contrast, the Philippines (PSEi Index) faced the most significant liquidity challenges and exhibited the slowest recovery, indicating deeper impacts from the pandemic and suggesting that governments must prioritize robust frameworks to withstand future shocks.

Our research has some limitations. Firstly, the analysis focuses on only six key indices, which may not fully capture the broader market dynamics within each country. Important factors, such as the performance of smaller companies or alternative asset classes, could provide a more comprehensive understanding of market liquidity. Additionally, the findings may not be generalizable to other emerging markets due to variations in economic structures and regulatory environments. Finally, the research primarily employs quantitative measures to assess liquidity, potentially overlooking qualitative factors such as investor sentiment, market psychology, and external economic conditions that significantly influence market behavior. Addressing these gaps in future research will be crucial for formulating effective policies and strategies aimed at enhancing market resilience in the face of future challenges.

Looking ahead, our research opens several avenues for further investigation. Exploring longer-term liquidity trends post-COVID-19 could yield valuable insights into the enduring impacts of the pandemic on market behavior. Furthermore, conducting a comparative analysis between the ASEAN-6 markets and other emerging markets could highlight best practices and differing responses to liquidity crises. Such studies would deepen our understanding of market resilience and inform policymakers on effective strategies for enhancing liquidity during periods of uncertainty.

In conclusion, as global markets continue to navigate the repercussions of the pandemic, our findings underscore the critical role of liquidity in maintaining financial stability and the necessity for ongoing research into the factors that influence market dynamics. This knowledge is essential for developing strategies that can mitigate future risks and bolster the resilience of emerging markets.

Footnotes

Funding

The author(s) disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: This research is funded by the National Economics University, Hanoi, Vietnam.

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Data Availability Statement

Data sharing not applicable to this article as no datasets were generated or analyzed during the current study.