Abstract

This study examines the relationship between liquidity, FinTech development, and credit risk in the Indonesian banking industry. Specifically, it investigates the impact of FinTech, particularly in peer-to-peer lending and payment systems, on credit risk in conjunction with liquidity. The analysis is conducted using panel data from 142 commercial banks in Indonesia over a 15-year period from 2004 to 2018. The results reveal that higher liquidity leads to a reduction in credit risk, whereas FinTech development is found to increase credit risk, particularly in small banks (BUKU 3 and BUKU 4) and private national banks. Notably, this study identifies that the impact of liquidity on credit risk is conditional on the level of FinTech development. Furthermore, the findings suggest that the effects of FinTech on credit risk are contingent on the bank’s characteristics and the economic environment. These results have significant policy implications for designing an inclusive financial framework in the digital era, especially in managing the risks associated with FinTech development.

Introduction

Maintaining adequate liquidity is crucial for a bank to fulfill its obligations and prevent default. When a bank experiences a negative effect on its liquidity, it resorts to interbank loans, selling reserve assets, or increasing deposit interest rates to attract depositors. However, these measures can result in high-interest expenses and increased credit risk, which create an ambiguous relationship between liquidity and credit risk. Prior research indicated a unidirectional correlation between liquidity and credit risk (Bryant, 1980; Diamond & Dybvig, 1983; Diamond & Rajan, 2005; Imbierowicz & Rauch, 2014; Prisman et al., 1986). Additionally, other studies showed that excess liquidity could increase credit risk (Acharya & Naqvi, 2012; Cheng et al., 2015; Hassan et al., 2019; Khan et al., 2017; Wagner, 2007).

Several recent studies investigate the relationship between liquidity risk and credit risk in the banking sector. Wang (2022) analyzed data from Chinese commercial banks and determined that liquidity risk has a significant positive effect on credit risk, highlighting the need for these banks to manage their liquidity risk to mitigate adverse effects on credit risk. In a similar vein, Hsieh and Lee (2020) analyzed banks in 27 Asian countries from 1999 to 2013 and discovered that bank liquidity creation has a positive effect on credit risk, suggesting that banks with greater liquidity creation may engage in riskier lending practices. Arias et al. (2022) analyzed Ukraine banks and found that systemic liquidity risk can have a substantial impact on the credit risk of individual banks. Finally, Abdelaziz et al. (2020) analyzed banks from MENA countries from 2008 to 2017 and demonstrated that liquidity risk has a significant positive effect on credit risk, emphasizing the significance of managing liquidity risk to mitigate negative impacts on credit risk in this region.

At the same time, as FinTech continues to grow as a competitor to traditional banking systems, it is crucial for regulators to monitor the potential emergence of liquidity and credit risks. A FinTech company, short for Financial Technology (FinTech), refers to a business that integrates information technology to provide innovative solutions within the financial industry. FinTech encompasses various services, including digital payments, online lending, financial management, and investments, with the goal of accelerating, simplifying, and enhancing accessibility to financial services through digital platforms. FinTech companies often present efficient modern alternatives compared to traditional financial institutions. Zhang et al. (2019), who examined Chinese FinTech peer-to-peer lending, discovered that FinTech affected the balance of domestic bank loans, with a dynamic non-linear correlation between FinTech and domestic bank loan balances. Tang (2019) indicated that FinTech, particularly peer-to-peer lending, impacted substitution rather than complement, resulting in a decline in loan volume for small commercial banks in rural areas. Yudaruddin (2023a) demonstrated that FinTech startups negatively impacted bank lending. Meanwhile, a study by Arner et al. (2015) found that peer-to-peer lending platforms might have been subject to liquidity risk, which could have led to a higher probability of loan defaults.

In Indonesia, regulators are particularly concerned about tight bank liquidity and the threats of non-performing loans (NPL). The Deposit Insurance Corporation (LPS) posits that the resilience of banking liquidity in 2023 will persist, despite the presence of a recession and an upward adjustment in the benchmark interest rate. The discussion on bank liquidity is crucial as it directly impacts a financial institution’s ability to meet its short-term obligations and withstand economic downturns. Additionally, addressing the risks associated with non-performing loans is essential for maintaining the stability of the financial sector, as high NPLs can undermine the overall health of banks and hinder economic growth. Furthermore, the emergence of Financial Technology (FinTech) introduces a dynamic element to the financial landscape, offering innovative solutions that challenge traditional banking models.

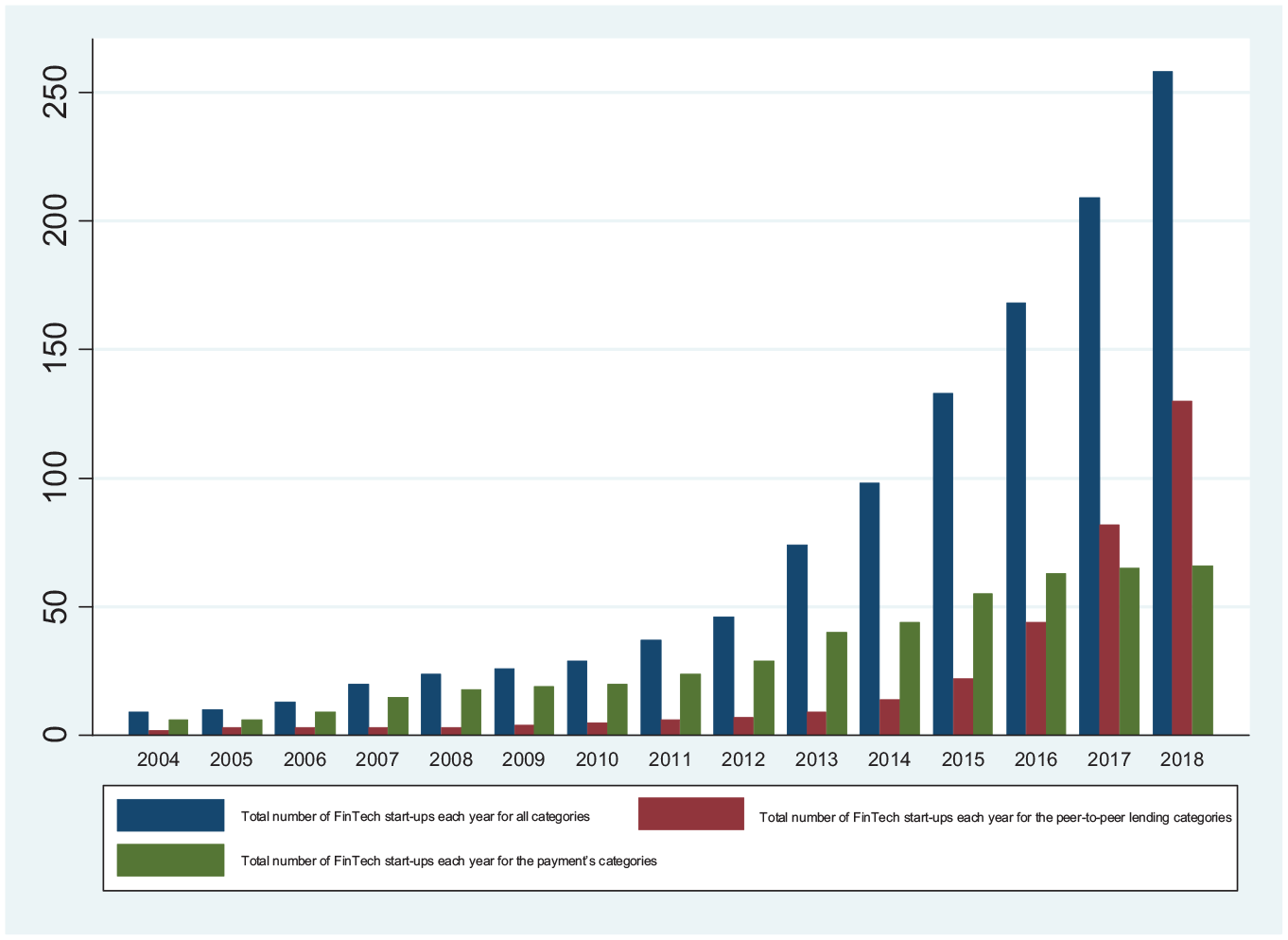

FinTech is expanding rapidly in Indonesia (Figure 1), which raises the question of how FinTech’s development affects the relationship between liquidity and credit risk. Indeed, the development of financial technology (FinTech) also has a positive impact on the banking industry, especially for small banks (Yudaruddin et al., 2023). However, Bank Indonesia (2017) warned that FinTech’s existence may disrupt the performance of the banking industry and increase financial system risks if regulatory measures are inadequate. This competition can affect third-party funds’ stability and in-credit interest rates. This is important because Indonesia was selected because it is among the Asia Pacific countries with good returns on average equity following the data collected by Dahl et al. (2019). Nevertheless, Yudaruddin (2023b) and Phan et al. (2020) showed that FinTech has a negative impact on banking performance in Indonesia Therefore, a study of the role of FinTech in influencing the relationship between liquidity and credit risk in Indonesia needs to be explored.

FinTech startups in Indonesia in 2004 to 2018.

This study analyzes the impact of FinTech development on the relationship between liquidity and credit risk in Indonesia. It focuses on the general effects of FinTech, particularly peer-to-peer lending and payment systems, which dominate Indonesian FinTech development. The study uses panel data from 142 commercial banks in Indonesia from 2004 to 2018. Prior research has suggested that banks with low liquidity tend to take higher risks (Acharya & Naqvi, 2012), and innovative financial systems are more vulnerable to crisis (Thakor, 2012). Therefore, FinTech’s theoretical impact on risk and financial instability is significant. This study provides empirical evidence in three significant aspects.

First, this study examines the effects of FinTech development on the relationship between liquidity and credit risk, which differs from previous studies that did not consider the aspect of financial innovation (Abdelaziz et al., 2020; Acharya & Naqvi, 2012; Arias et al., 2022; Bryant, 1980; Cheng et al., 2015; Diamond & Dybvig, 1983; Diamond & Rajan, 2005; Hassan et al., 2019; Hsieh & Lee, 2020; Imbierowicz & Rauch, 2014; Khan et al., 2017; Prisman et al., 1986; Wagner, 2007; Wang, 2022). Thus, this study aims to fill this research gap.

Second, this study provides empirical evidence on the impact of FinTech, particularly peer-to-peer lending, on the relationship between liquidity and credit risk in Indonesia. The effects of this financial innovation depended on bank ownership, size, and the crisis period. Moreover, this study presented the first empirical finding on how FinTech affected third-party funds toward non-performing loans in a given condition. Previous studies (Narayan & Sahminan 2018; Phan et al., 2020) analyzed the impact of FinTech on banks without classifying them into specific groups with a similar business model.

Lastly, this study sheds light on the adoption rate of FinTech by banks in Indonesia, a developing country. Our analysis revealed that FinTech adoption in Indonesia was relatively slow and immature, with limited traffic payment systems dominating the market. This finding contrasted with the experiences of developed countries such as the U.S., England, and China, where FinTech newcomers played in vast transnational markets to develop their economic scale (Ernst & Young, 2019; Mittal et al., 2016). While prior studies on FinTech and banks had mostly focused on developed economies like the U.S. (Buchak et al., 2018; Jagtiani & Lemieux, 2018; Tang, 2019; Wolfe & Yoo, 2018), China (Z. Chen et al., 2017), Germany (Bömer & Maxin, 2018), and India (Anand & Mantrala, 2019), this paper contributed to the literature by examining the specific case of Indonesia.

Literature Review

Liquidity and Credit Risk in Banking

Several studies have examined the relationship between liquidity and bank risk. Bryant (1980), Diamond and Dybvig (1983), Prisman et al. (1986), Diamond and Rajan (2005), Wagner (2007), and Acharya and Naqvi (2012) explored this correlation. Financial intermediation theory, as proposed by Bryant (1980) and Diamond and Dybvig (1983), and the industrial organization approach to banking, such as the Monti-Klein model (Prisman et al., 1986), provided a framework for understanding this relationship. According to Diamond and Rajan’s (2005) model, there was a positive correlation between liquidity risk and credit risk. When economic projects funded by loans were too numerous, banks may not have been able to satisfy the depositors’ demands, which increased both liquidity and credit risk. However, Imbierowicz and Rauch’s (2014) study of U.S. banks from 1998 to 2010 found only a weak positive correlation between liquidity and credit risk. Similarly, Ghenimi et al. (2017) found a positive but weak correlation between the two risks in their study of banks in the Middle East and North Africa. Despite the lack of correlation between the two risks, both contributed to the probability of bank default, either individually or simultaneously. In contrast, Hassan et al. (2019) found a negative correlation between liquidity and credit risk in Islamic banks in the Organization of Islamic Cooperation.

These studies also explored the relationship between liquidity and credit risk during periods of normalcy and crisis. Wagner (2007) proposed a correlation theory between asset liquidity and bank stability, suggesting that bank asset liquidity undermined its stability during financial crises, but not during normal periods. During crises, increased liquidity encouraged banks to take new risks beyond the positive stability impacts. Cornetta et al. (2011) found that the financial crisis reduced market liquidity and categorized banks into two groups: those with deposits and equity as primary funding sources, which were likely to lend more, and those with non-liquid assets, which were likely to cut lending to increase liquidity. However, reducing credit supply could also lead to credit risk. Acharya and Naqvi (2012) proposed that access to high liquidity could aggravate the risk-taking moral hazard in a bank, leading to excessive loans and asset price bubbles, thereby increasing the potential for future crises.

Furthermore, an increase in loan interest rates could prompt risk-taking in bank loans, leading to bank default. Cheng et al. (2015) proposed principal-agent theory, suggesting that a manager who avoided risk required higher compensation to work in a finance company with greater asset uncertainty. Therefore, banks with higher risk tolerance could pursue more aggressive lending strategies during periods of excess liquidity. Acharya and Naqvi (2012) suggested that abundant liquidity encouraged more aggressive lending, as banks could lend more at a lower interest rate. Lucchetta (2007) found that banks took higher risks when risk-free interest rates increased, as they invested more in risk-free obligations, which eventually increased liquidity supply and encouraged interbank loans. This, in turn, encouraged other banks to invest in risky assets. According to Wagner (2007), higher liquidity increased the instability of a banking system and externalization related to default.

FinTech: A Complementary or Substitutional Force in the Financial Industry?

The emergence of FinTech was regarded as a disruptive innovation for the financial industry, particularly banking, according to theoretical analyses by Aaker and Keller (1990), Christensen (1997), and Thakor (2012). Aaker and Keller’s (1990) consumer theory suggested that FinTech services could substitute traditional bank services by meeting consumers’ demands for more accessible and cost-effective financial services. Similarly, Christensen’s (1997) disruptive innovation theory explained how newcomers, such as FinTech, could create competition in the market by offering more affordable services. Thakor’s (2012) model further established that financial innovation thrived in a competitive system with lower charges.

However, empirical studies also showed that FinTech development disrupted the banking industry and its intermediation function. Philippon’s (2015) study on the US financial system found that FinTech had failed to reduce intermediation costs. Meanwhile, Zhang et al. (2019) study on Chinese FinTech peer-to-peer lending found that FinTech affected the balance of domestic bank loans, with a dynamic non-linear correlation between the loan balance of FinTech and domestic banks. Tang’s (2019) study suggested that FinTech, especially peer-to-peer lending, impacted substitution rather than complement, leading to a falling loan volume for small commercial banks in the countryside. Yudaruddin (2023a) showed that FinTech startups had a detrimental effect on bank lending.

Recent studies explore the impact of FinTech on bank profitability, performance, credit risk, and liquidity risk. Lv et al. (2022) found that the development of FinTech had a cooperative relationship with banks’ profitability. FinTechs had a “U”-shaped impact on the profitability of banks, with initial stages impacting business and reducing profitability, followed by advantages gradually increasing in the middle and later stages, leading to increased profitability. Meanwhile, Zhao et al. (2022) showed that financial technology innovation reduced banks’ profitability and asset quality in the aggregate. This finding was more pronounced for large state-owned commercial banks, but it improved banks’ capital adequacy and management efficiency, albeit to a smaller degree for policy banks and state-owned commercial banks. Nguyen et al. (2022) also found that FinTech credit tended to reduce bank profitability while improving bank risk-related performance. This suggests that as FinTech grows, it competes with banks and takes some share of profits, but it also benefits banks in terms of stability. Stricter regulations contributed positively to bank stability, and the impact of FinTech credit on bank performance may depend on the degree of banking regulation.

In addition to profitability and performance, FinTech also presents environmental concerns. Tao et al. (2021) addressed the question of whether FinTech development helped economies transition to lower levels of carbon and greenhouse gas emissions. They found that FinTech development could help reduce greenhouse gas emissions when appropriate control variables were incorporated, and these results were robust even after considering the potential endogeneity of FinTech development.

Despite the challenges FinTech poses to the traditional banking system, empirical studies also highlight its potential to create competitive advantages. Ozili (2018) found that most investors quickly deposited more money to other banks in minutes, driving them to enhance their service quality. Additionally, depositors were willing to deposit their assets to FinTech startups through credit cards, debit, or electronic wallets, posing a risk to the banking industry’s potential consumer base due to new competitors and pressure on profit margins (Romānova & Kudinska, 2016). Yudaruddin (2023a) demonstrated that interactions between banks and FinTech firms benefited banks.

However, banks can gain a competitive advantage by collaborating with FinTech startups. Juengerkes (2016) found that such collaborations can enhance customer trust and lead to complementary effects, which become a strategy to face disruptive innovation. Li et al. (2017) also indicated a positive correlation between funding growth and transactions in FinTech companies and return on the stock to incumbent retail banks in the US, suggesting that FinTech is more of a complement to traditional banks than a substitute and disruptive innovation.

In conclusion, while FinTech’s emergence has disrupted the traditional banking industry, empirical studies suggest that it can also create opportunities for competitive advantage through collaboration and complementary effects. Therefore, FinTech is more of a complementary force to traditional banks than a substitute one.

FinTech and Its Impact on Liquidity and Credit Risk in the Banking Industry

Liquidity is crucial for banks to fulfill their obligations and maintain financial stability. Problems with liquidity can signal bank default, which is indicated by a decrease in Third-Party Funds (TPF). This lack of liquid assets may lead banks to make interbank loans or sell reserve assets, which can increase credit risk. Basel III has introduced higher liquidity requirements for banks to make them more immune to financial pressure. However, this may also reflect the characteristics of banks that face more risks (Brandao-Marques et al., 2013).

The relationship between liquidity and credit risk is often uncertain. While several studies have shown positive correlations between liquidity and credit risk (Bryant, 1980; Diamond & Dybvig, 1983; Diamond & Rajan, 2005; Imbierowicz & Rauch, 2014; Prisman et al., 1986), other studies have found that excess liquidity can stimulate an increase in credit risk (Acharya & Naqvi, 2012; Cheng et al., 2015; Hassan et al., 2019; Khan et al., 2017; Wagner, 2007). Access to high liquidity can lead to moral hazard behavior in banks, triggering credit booms and asset price bubbles. This indirectly arouses future crises and banking system instability.

The development of FinTech plays an essential role in the digital era, particularly in the frame of financial inclusion. However, it can be seen as a competitor to the banking industry (Ferrari, 2016; Milian et al., 2019; Navaretti et al., 2017; Ozili, 2018; Zhang et al., 2019), and has resulted in tension on bank profit margin (Romānova & Kudinska, 2016). The competition between FinTech and banks has also increased bank risk (Buchak et al., 2018; Jagtiani & Lemieux, 2018; Phan et al., 2020; Tang, 2019; Wolfe & Yoo, 2018). Its presence has shifted the function of bank intermediation to shadow banking, encouraging moral hazard behavior and bank instability (Buchak et al., 2018).

However, several studies present FinTech as a complement rather than a substitute and a disruptive innovation (Juengerkes, 2016; Li et al., 2017; Zalan & Toufaily, 2017). Collaboration between FinTech and banks reduces tight liquidity and increases bank credit, hence decreasing bank risk. According to Pierri and Timmer (2020), the adoption of technology in loans potentially increases financial stability, particularly in reducing credit risk.

Investing in FinTech could allow banks to access exclusive rights in using specific applications or licenses. It also enables them to exclude their competitors from their policy and protect their primary business. Additionally, such investment enables the banks to control and directly influence their product development and FinTech service strategy. Therefore, liquidity risk and credit channels are limited when banks adopt new information technology management (Navaretti et al., 2017). However, FinTech companies need to comply with bank regulations in case they exercise intermediation functions.

Overall, the relationship between liquidity and credit risk in the banking industry is complex and uncertain. While FinTech can be a competitor to banks, the collaboration between the two can lead to reduced liquidity risk and credit channel, hence decreasing bank risk. Investing in FinTech can also allow banks to access exclusive rights, control product development, and service strategy, and limit liquidity risk and credit channels.

Variables, Data, and Methodology

This study aims to investigate the correlation between liquidity, the development of Financial Technology (FinTech), and credit risk within the Indonesian banking industry during the period spanning from 2004 to 2018. The primary variables under consideration encompass credit risk, liquidity, and FinTech startups. This section elucidates the variables encompassed in this study and their corresponding measurements. Subsequently, a comprehensive elucidation of the utilized data and its respective sources is provided. Additionally, the methodology employed for addressing the research question is elucidated, encompassing the various stages involved in the process of data analysis.

Variables

Table 1 presents the independent and dependent variables used in this study. The dependent variable, credit risk, is measured by non-performing loans (NPL), which reflects the quality of bank credit. A higher NPL value indicates either greater bank credit or a lower quality of credit management. Liquidity, an independent variable, is measured by the growth of Third-Party Funds (GTPF), consistent with previous research by Demirgüç-Kunt and Huizinga (2004), Acharya and Naqvi (2012), Soedarmono and Tarazi (2016), and Khan et al. (2017). Third-Party Funds comprises Current Accounts, Savings, and Deposits for conventional banks and Wadiah Current Accounts, Mudharabah Savings, and Deposits for Islamic banks. Bank liquidity is a crucial aspect of their ability to meet financial obligations promptly and efficiently, and higher liquidity signifies the ability to handle large customer withdrawals without incurring any operational difficulties. Thus, Growth of Third-Party Funds is a suitable indicator of liquidity as it is insensitive to interest rates and has low costs. Additionally, the study employs Indonesian FinTech (FINALL, P2P, and PAY) as another independent variable. These variables are categorized into payment, peer-to-peer lending, personal finance & wealth management, comparison, insurtech, crowdfunding, post system, crypto & blockchain, and accounting. The number of FinTech start-ups each year is used to measure the impact of FinTech on credit risk (Narayan & Sahminan, 2018; Phan et al., 2020; Yudaruddin 2023b).

Description of Variables.

The study employs a set of control variables to explore their influence on credit risk, including bank concentration (HHI), bank size (SIZE), inefficiency (CTI), income diversification (NON), profitability (ROA), unemployment rate (UNM), inflation (INF), economic activity (GDP), dummy variable of Islamic Banks (ISLAMIC), and Listed Banks (LISTED), as proposed by Berger and DeYoung (1997), Salas and Saurina (2002), Nkusu (2011), Louzis et al. (2012), Samet et al. (2018), Hassan et al. (2019), Susamto et al. (2020), and Dibooglu et al. (2022). Bank concentration is measured using the Herfindahl–Hirschman Index, and high ownership concentration leads to more considerate risk-taking through tighter controls toward bank management, resulting in a negative influence on credit risk. However, Louzis et al. (2012) suggested that high ownership concentration increases bank credit risk due to the aggressive loan’s strategy. Bank size is measured by total assets, and while there is an ambiguous correlation between bank size and credit risk, bigger banks have higher non-performing loans (NPL) according to Louzis et al. (2012). Inefficiency is measured from the ratio of banks’ operational expenditure, and there is a positive correlation between efficiency and NPL. Income diversification is measured from the ratio of non-interest income of total assets, and there is a negative correlation between income diversification and NPL as suggested by Salas and Saurina (2002). Profitability, measured from the ratio of profit before tax to total assets, has an ambiguous correlation with NPL. Unemployment, measured from the percentage of the open unemployment rate, has a positive effect on NPL based on Louzis et al. (2012) and Pop et al. (2018). Inflation has a positive effect on NPL, according to Nkusu (2011). Economic activity, measured by the growth of gross domestic product, has a negative correlation with NPL as indicated by empirical studies (Dimitrios et al., 2016; Ghosh, 2015; Louri & Karadima, 2021; Salas & Saurina, 2002). Islamic Bank is measured by a dummy variable, and there is a negative and significant relationship between liquidity and credit risk according to Hassan et al. (2019). However, during normal times there is no difference in credit risk between Islamic and conventional banks (Dibooglu et al., 2022; Susamto et al., 2020). Listed Banks are also measured by a dummy variable, and listed banks have more excellent financial stability and lower insolvency risk than non-listed banks according to Samet et al. (2018). The definitions of all the variables used in this study are presented in Table 1.

Data

This study employs banking data from a sample of 142 banks in Indonesia, including Islamic banks, from 2004 to 2018. To ensure comprehensive coverage, unbalanced panel data available during the predetermined period are also utilized. The annual count of FinTech startups is obtained from reputable sources, including FinTech Singapore (FinTech news.sg), Indonesian Joint Funding FinTech Association (AFPI), and Financial Services Authority (OJK). To capture banking concentration, we use bank-specific data obtained from the database of OJK and Bank Indonesian. We supplement our analysis with macroeconomic data on inflation and annual GDP growth, which are obtained from the official statistics agency in Indonesia, Statistics Indonesia (BPS).

Methodology

To investigate the link between liquidity and credit risk, we proceed with the analysis in several stages. In the first stage, we initially investigate the impact of liquidity on credit risk in general (Equation 1). In the second stage, this study includes Equation 1, which has been changed to include the interaction term between liquidity and FinTech, as shown in Equation 2. In general, the rise of FinTech can impact the dynamics of credit risk. As a competitor, FinTech may drive banks to compete more efficiently and innovatively, but simultaneously, this competition can elevate credit risk if not managed properly. On the other hand, collaboration between FinTech and banks can bring benefits, such as increased liquidity and better access to financial technology, potentially reducing credit risk. The increase in bank liquidity, fundamentally, can mitigate credit risk as banks have more resources to meet their obligations. However, improper liquidity management can also heighten risk if utilized to fund more precarious activities. In the third stage, repeat the estimation conducted in Equation 2 for samples broken down between government-owned and private banks, large and small banks, and crisis and normal periods.

The present study utilizes a formulated model based on the works of Demirgüç-Kunt and Huizinga (2004), Louzis et al. (2012), Ghosh (2015), and Hassan et al. (2019) to investigate the impact of bank liquidity on credit risk. Equation 1 outlines the econometric model developed to analyze this relationship, which aligns with the study’s first objective of investigating the impact of GTPF on NPL.

Moreover, the study presents Equation 2, which illustrates an econometric model developed to examine how the development of FinTech impacts the correlation between bank liquidity and credit risk, supporting the study’s second objective. The incorporation of FinTech in the model is an essential factor in capturing the recent technological developments and their impact on the banking sector.

We use a dynamic panel data model with the two-step system GMM (generalized methods of moments) estimator developed by Blundell and Bond (1998) and Arellano and Bover (1995) to estimate these third stages. Recent research in FinTech, Liquidity, and Credit Risk also employs a dynamic panel data analysis (Ghenimi et al., 2017; Hassan et al., 2019; Imbierowicz & Rauch, 2014; Narayan & Sahminan, 2018; Phan et al., 2020). In general, the use of dynamic panel data estimation in the study of the determinants of credit risk is appropriate, as credit risk as a dependent variable may be influenced by its past values. Using dynamic panel data estimation can also prevent problems involving reverse causality between independent and dependent variables. In addition, the study also accounts for the infinite population correction developed by Windmeijer (2005) and identifies orthogonal transformations instrument to explain unobservable banking factors. To test the consistency of the estimation results, the Autocorrelation Test in the GMM approach is used, which is determined by the Arellano-Bond m1 and m2 statistics (Arellano & Bond, 1991). The GMM system is deemed valid when the AR Test (2) and Hansen-J Test are not rejected, with the consistency of the model shown through significant m1 values (p-value < α) and insignificant m2 values (p-value > α).

Results and Discussion

Descriptive Statistics and Correlation

The descriptive statistics and correlation analysis are presented in Tables 2 and 3. Credit risk is measured by NPL value, which averaged 3.12% over the past 15 years, indicating that Indonesian banks are still below the maximum limit set by OJK, specifically 5%. Bank liquidity is measured by the Growth of Third-Party Funds, with an average of 0.24% during the research years. The FinTech variables and control variables in Table 1 encapsulate crucial aspects of the Indonesian banking landscape. The total number of FinTech startups for all categories (FINALL) exhibits an average of 74.474, with a minimum of 9 and a maximum of 258, showcasing the substantial presence of FinTech entities in the market. For peer-to-peer lending (P2P) FinTech startups, the average count is 21.535, ranging from 2 to 130, reflecting varied levels of activity in this specific sector. Payment-related FinTech startups (PAY) have an average count of 31.175, with values ranging from 6 to 66, underscoring the diversity within this subset.

Descriptive Statistics.

Correlation Matrix.

Moving to control variables, Bank Concentration (HHI) demonstrates an average of 636.98, indicating a competitive banking environment. Bank Size (SIZE), represented by the logarithm of total assets, has an average of 15.712, reflecting the scale of financial institutions in the dataset. Inefficiency (CTI) shows an average ratio of 0.8311, pointing to varying degrees of operational efficiency among the banks. Income Diversification (NON) has a mean ratio of 0.0195, suggesting limited reliance on non-interest income. Profitability (ROA) stands at an average of 1.9340, reflecting overall positive returns on assets. Other macroeconomic variables, such as the Unemployment Rate (UNM), Inflation Rate (INF), and Gross Domestic Product Growth (GDP), provide context for the economic backdrop. The dummy variable for Islamic Banks (ISLAMIC) has an average of 0.0657, indicating a relatively small proportion of Islamic banks in the dataset. The dummy variable for Listed Banks (LISTED) shows an average of 0.2720, suggesting that a substantial portion of banks in the sample are listed.

Table 3 presents the correlation matrix among the variables, offering insights into the presence of multicollinearity. Multicollinearity is a concern when independent variables in a regression model are highly correlated, potentially leading to unstable coefficient estimates. However, upon examining the correlation matrix, it is evident that there are no excessively high correlations among the independent variables, suggesting a lack of severe multicollinearity. Table 3 shows the correlation between independent variables, including FinTech startup for all categories (FINALL), and peer-to-peer lending (P2P) and payment (PAY) category. The correlation analysis reveals that including all FinTech startup variables in a single regression analysis may cause multicollinearity problems and could be misleading. To avoid this issue, the study employs separated regression analyses for the FinTech startup variables.

The Impact of Liquidity on Credit Risk

This study investigates the impact of liquidity on credit risk, measured by non-performing loans (NPL), using data from banks in Indonesia. Liquidity is measured by Growth of Third-Party Funds, and the estimation results for the baseline model are presented in Table 4. Using the two-step GMM approach, we find that liquidity has a negative and significant effect on credit risk at the 5% level of significance (Column 1–6). Furthermore, the analysis does not suffer from any problems of overidentification or inconsistency, ensuring the robustness of the results. All dynamic panel data models in Table 3 are valid, because the AR(2) test and the Hansen-J test are not rejected. Specifically, an increase in Growth of Third-Party Funds indicates a lower funding risk, but an increase in NPL raises credit risk and vice versa. These results are consistent with previous studies by Bryant (1980), Diamond and Dybvig (1983), Prisman et al. (1986), Diamond and Rajan (2005), Wang (2022), Hsieh and Lee (2020), Arias et al. (2022), and Abdelaziz et al. (2020).

Liquidity and Credit Risk (Baseline Regression).

Note. Standard errors of each coefficient are in parentheses.

, **, and * indicate significance at the 1%, 5%, and 10%, respectively.

The practical implications of the empirical analyses in this study suggest that maintaining adequate bank liquidity is crucial for reducing credit risk and lowering the NPL of banks in Indonesia. Therefore, bank managers and policymakers should focus on strategies to maintain sufficient liquidity levels to mitigate funding risk and avoid high levels of NPL. Additionally, the findings from this study could serve as a useful guide for developing effective policies and regulations related to bank liquidity and credit risk management. Ultimately, this study provides practical insights for banks in Indonesia to improve their overall financial health and stability by maintaining optimal levels of liquidity.

The emergence of financial technology (FinTech) has revolutionized the banking industry in recent years. This study aims to examine the impact of FinTech on non-performing loans (NPL) in Indonesia. The findings suggest that FinTech, specifically peer-to-peer lending (P2P) and FinTech for all categories, negatively (β = −.0055; −.0186 and −.0144, respectively) and significantly affect NPL at the 5% level of significance (Column 2, 4, and 5). These results indicate that the development of FinTech does not contribute to the increase in NPL, and therefore not a disruptive innovation (Juengerkes, 2016; Li et al., 2017; Yudaruddin et al., 2023; Zalan & Toufaily, 2017). However, this study finds a positive and significant coefficient (β = .2308, p < .05) of the payment (PAY) FinTech category (Column 6). This suggests that the development of payment FinTech supports the increase in NPL and may be considered a disruptive innovation (Aaker & Keller, 1990; Christensen, 1997; Thakor, 2012).

The practical implications of the empirical analyses show that the development of FinTech, particularly P2P lending and FinTech for all categories, can potentially reduce NPL in Indonesia. However, caution should be exercised in the development of payment FinTech, as it may increase NPL and lead to a disruptive innovation. The findings of this study can provide valuable insights for policymakers and financial institutions in Indonesia to better understand the impact of FinTech on NPL and make informed decisions regarding the regulation and development of FinTech in the country. By promoting the development of FinTech for all categories while monitoring and regulating the growth of payment FinTech, policymakers and financial institutions can help to ensure the stability and sustainability of the banking industry in Indonesia. Overall, these findings have significant implications for policymakers and banks in Indonesia, as they highlight the need to monitor the development of payment FinTech and its potential impact on NPL.

Table 4 presents the control variables, revealing that bank concentration (HHI), bank size (SIZE), unemployment (UNM), and inflation (INF) have a positive and significant impact on NPL. However, variables such as ROA and GDP demonstrate a negative and significant correlation. Specifically, our study finds that HHI has a negative and significant effect on NPL, consistent with the research of Louzis et al. (2012). This highlights that higher ownership concentration rates increase credit risk, as banks adopt an aggressive loan strategy. Moreover, SIZE has a positive and significant effect on NPL at the 5% level of significance, as larger banks have greater leverage, potentially leading them to lend to low-quality borrowers based on the moral hazard of too-big-to-fail, in line with the studies of Stern and Feldman (2004) and Louzis et al. (2012).

Regarding efficiency, CTI displays a positive and significant correlation with NPL in Indonesian banks. This implies that less efficient banks experience higher NPL, whereas more efficient ones have lower NPL, as shown by the research of Berger and DeYoung (1997), Podpiera and Weill (2008), and Louzis et al. (2012). These studies support the “bad management hypothesis,” which suggests that incompetent managers fail to supervise loan portfolio management due to poor loan evaluation skills or the inability to allocate resources for supervision, resulting in a significant amount of bad credit.

Furthermore, our study reveals that ROA has a negative and significant effect on NPL at the 1% level of significance, indicating that profitable banks dissociate from risky activities that could lead to future loan default, consistent with Berger and DeYoung (1997). In terms of macroeconomic variables, our findings demonstrate that UNM and inflation have a positive and significant impact on NPL. This result confirms the research by Louzis et al. (2012) and Pop et al. (2018), which show a positive correlation between the unemployment rate and NPL. The inflation variable also displays a positive and significant correlation with NPL, as an increase in inflation raises the cost of debtors, thus reducing the available funds for credit payments. This finding is consistent with the research by Nkusu (2011), Salas and Saurina (2002), Ghosh (2015), Dimitrios et al. (2016), and Louri and Karadima (2021), which suggest a negative correlation with NPL. Therefore, our study highlights that economic activities significantly impact NPL negatively, as revealed in Column 6.

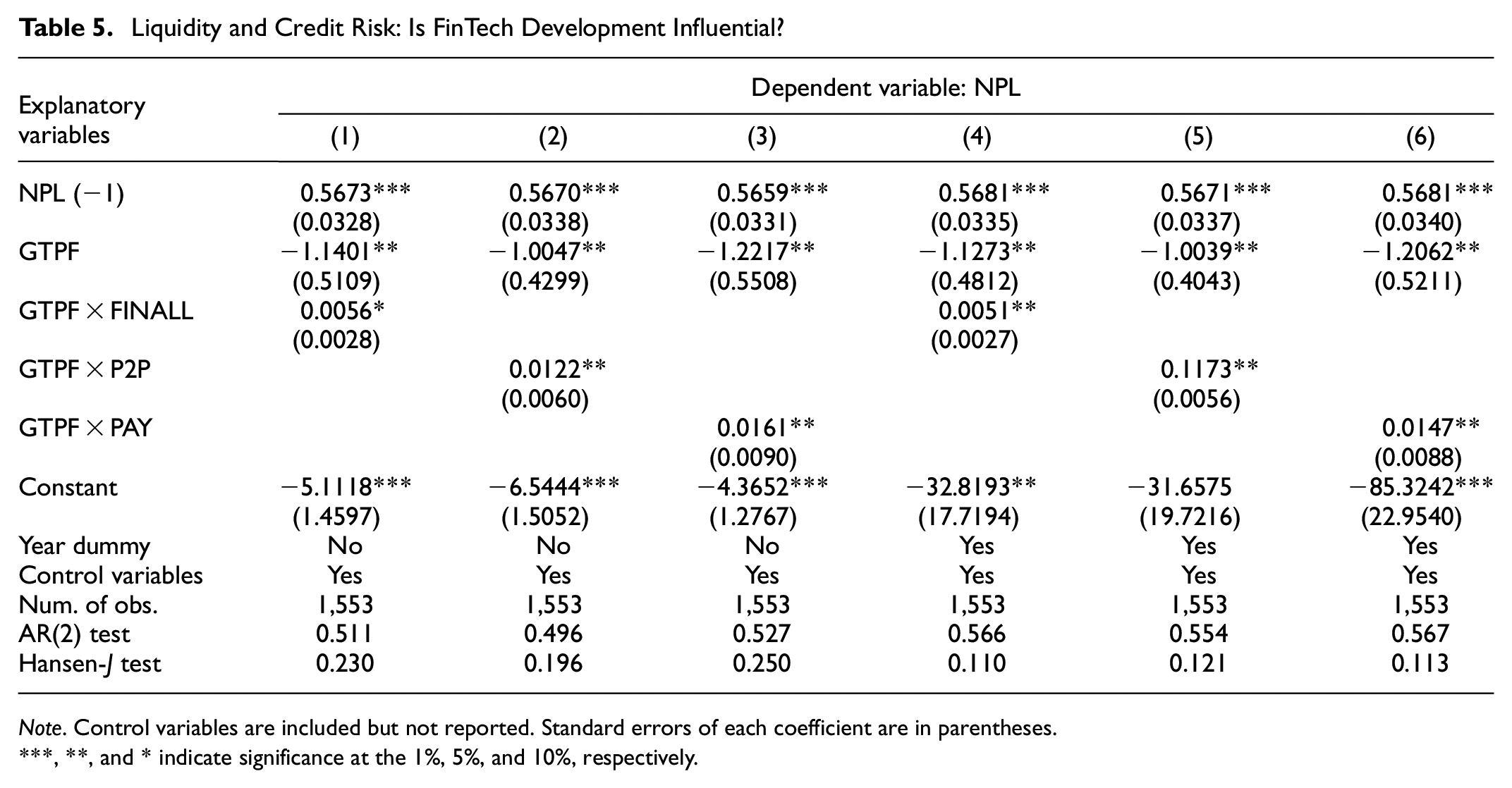

Liquidity and Credit Risk: Is FinTech Development Influential?

In the current digital era, FinTech is a significant player in promoting financial inclusion. While it disrupts the traditional banking industry and increases bank risks, it also complements and collaborates with it to reduce risk. This study investigates whether FinTech has any impact on the relationship between liquidity and credit risk. The findings suggest that the interaction between GTPF and financial innovation has a positive effect on NPL (β = .0051; .1173 and .0147, respectively) and significantly affects NPL at the 5% level of significance (Table 5). This indicates that FinTech’s competition heightens bank risk, where excess liquidity aggravates the risk-taking moral hazard in a bank. This finding aligns with previous research by Acharya and Naqvi (2012), Thakor (2012), Wagner (2007), and Buchak et al. (2018) which also identify the adverse impact of excess liquidity on bank risk. The practical implication of the empirical analysis is that the competition brought by FinTech may heighten bank risk, particularly in the context of excess liquidity aggravating the risk-taking moral hazard. This finding is consistent with previous studies, which have also identified the adverse impact of excess liquidity on bank risk. Therefore, banks need to be cautious in adopting financial innovation and ensure that they maintain adequate liquidity to mitigate potential credit risk. The study highlights the importance of balancing the benefits of FinTech in promoting financial inclusion with the potential risks it may pose to the banking industry.

Liquidity and Credit Risk: Is FinTech Development Influential?

Note. Control variables are included but not reported. Standard errors of each coefficient are in parentheses.

, **, and * indicate significance at the 1%, 5%, and 10%, respectively.

In this study, we conducted further investigations on the role of FinTech development and its impact on the relationship between liquidity and credit risk. To achieve this, we categorized the bank samples based on size (large vs. small banks), ownership (government vs. private banks), and period (crisis vs. normal period). Our findings show that FinTech development has a significant influence on the relationship between liquidity and credit risk, particularly in small and private banks. Moreover, when we separated the large and small banks, our results (as reported in Table 6) indicate that the interaction between GTPF and FinTech positively affects NPL in small banks (β = .0056; .0119 and .0175, respectively) and significantly affect NPL at the 5% and 10% level of significance, but there is no significant effect in large banks. This finding is consistent with Khan et al. (2017) and supports the “too big to fail” hypothesis. Secondly, when we separated government and private banks (as presented in Table 7), our study shows that GTPF and FinTech affect NPL in private banks positively, with no significant effect on government banks. This result suggests that FinTech development influences the relationship between liquidity and credit risk in private banks, particularly in the peer-to-peer lending (P2P) category. Therefore, the practical implications of the empirical analyses in this study suggest that policymakers and bank managers need to be cautious in promoting FinTech development and consider its impact on different categories of banks. Specifically, small and private banks are more susceptible to the negative impact of FinTech on the relationship between liquidity and credit risk. Therefore, policies and regulations that aim to promote FinTech development need to be implemented carefully to avoid excessive risk-taking behavior in banks, particularly in the P2P lending category. Moreover, our findings suggest that government banks may be less affected by FinTech development, which highlights the potential role of government intervention in managing bank risks associated with financial innovation. Overall, the results of this study can inform policymakers and bank managers in Indonesia and other developing countries in managing the risks and opportunities associated with FinTech development.

Liquidity and Credit Risk: Is FinTech Development Influential? Large Banks Versus Small Banks.

Note. Control variables are included but not reported. Standard errors of each coefficient are in parentheses. Large = Banks with core capital of more than IDR 5 trillion (BUKUIV and BUKUIII); Small = banks with a core capital of less than IDR 5 trillion (BUKUII and BUKUI).

, **, and * indicate significance at the 1%, 5%, and 10%, respectively.

Liquidity and Credit Risk: Is FinTech Development Influential? Government Banks Versus Private Banks.

Note. Control variables are included but not reported. Standard errors of each coefficient are in parentheses. Government = bank owned by the government; Private = bank owned by private.

, **, and * indicate significance at the 1%, 5%, and 10%, respectively.

To further investigate whether FinTech development influences the relationship between liquidity and credit risk, we categorized the samples into two periods: crisis (global financial crisis in 2008 and 2009) and normal period (Table 8). Our analysis shows that during the crisis period, FinTech development increases credit growth but has a negative impact on credit risk or bank NPL, and vice versa during a normal period. This finding is consistent with previous studies by Cornetta et al. (2011) and Khan et al. (2017) that show a decrease in bank risk during the global crisis due to low liquidity risk resulting from more significant deposits taken by the bank. However, during a normal period, FinTech development encourages an increase in credit growth and bank NPL, which is consistent with the research by Acharya and Naqvi (2012) and Wagner (2007). Overall, our study highlights the significant influence of FinTech development on the relationship between liquidity and credit risk in different banking sectors and periods. During the crisis period, FinTech development can decrease bank NPL due to lower liquidity risk resulting from significant deposits taken by the bank. However, during a normal period, FinTech development may increase bank NPL and credit growth, particularly in small and private banks, suggesting that banks should maintain adequate liquidity to mitigate credit risk. These findings highlight the importance of monitoring the impact of FinTech development on the banking industry and implementing appropriate risk management strategies to ensure financial stability.

Liquidity and Credit Risk: Is FinTech Development Influential? Crisis Versus Normal Period.

Note. Control variables are included but not reported. Crisis = the period of global financial crisis (2008/2009). Standard errors of each coefficient are in parentheses.

, **, and * indicate significance at the 1%, 5%, and 10%, respectively.

Robustness Checks

This section presents a series of robustness checks aimed at verifying whether the baseline results still hold when alternative measurements of credit risk, bank liquidity, and econometric methodology are employed. The findings are consistent with those of the baseline model.

Firstly, consistent with Khan et al. (2017) and Delis et al. (2014), we perform robustness checks using LLP (Loan Loss Provision) as an alternative measurement of credit risk (Table 9). The results show that GTPF has a positive and significant effect on LLP, indicating that banks maintain LLP when there is a potential decline in credit quality. Thus, higher LLP indicates that a bank has taken on higher-risk assets.

Liquidity and Loan Loss Provision (Robustness Checks with Alternative Measurement of Credit Risk).

Note. LLP = loan loss provision. Standard errors of each coefficient are in parentheses.

, **, and * indicate significance at the 1%, 5%, and 10%, respectively.

Secondly, in line with Khan et al. (2017), Imbierowicz and Rauch (2014), and Hassan et al. (2019), we perform robustness checks using LIQ (the ratio of current assets to total assets) as an alternative measurement of bank liquidity (Table 10). The results indicate that LIQ has a negative and significant effect on NPL, suggesting that higher liquidity helps reduce bank risk.

Liquidity and Credit Risk (Robustness Checks with Alternative Measurement of Bank Liquidity).

Note. LIQ = ratio of current assets to total assets. Standard errors of each coefficient are in parentheses.

, **, and * indicate significance at the 1%, 5%, and 10%, respectively.

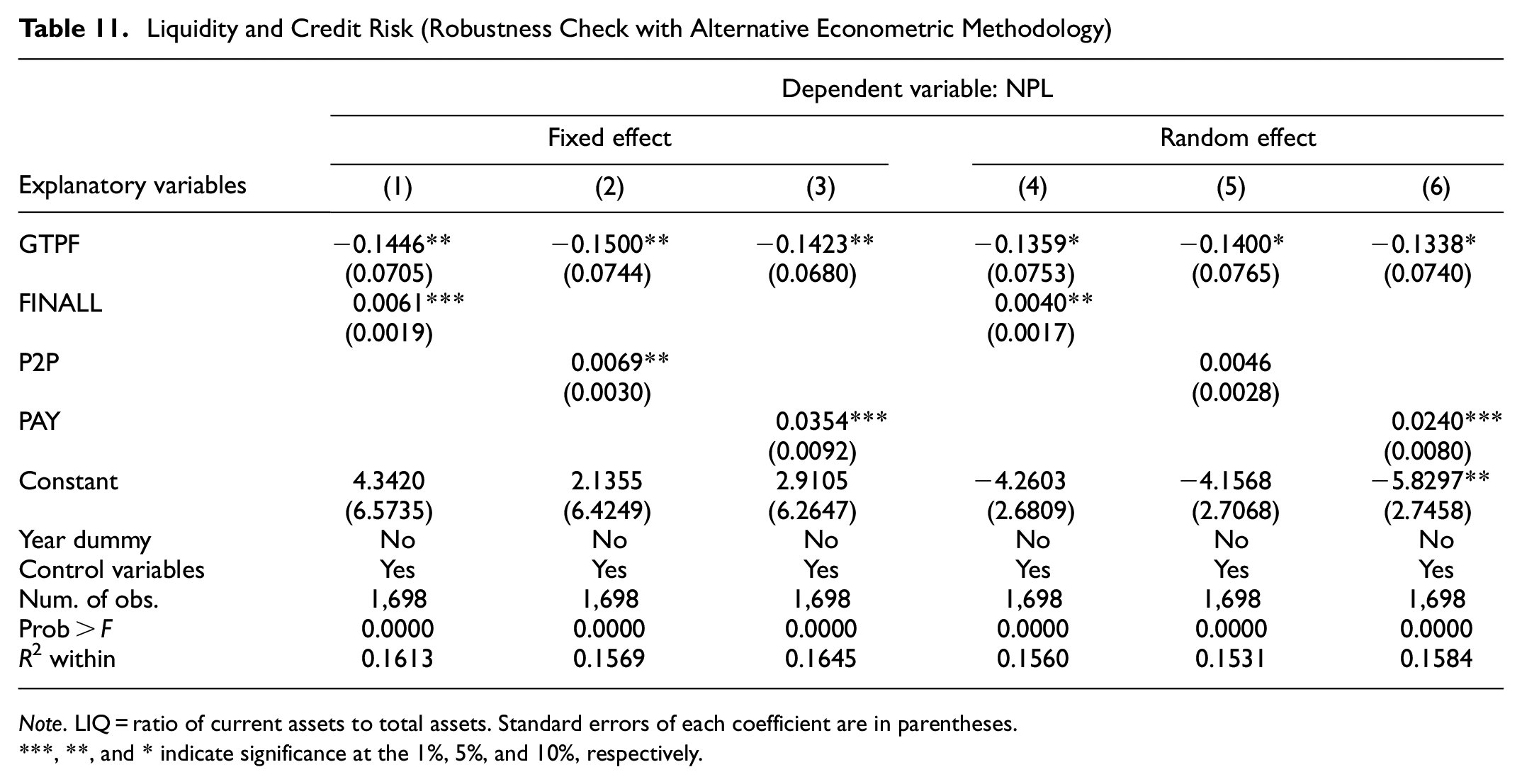

Thirdly, in our quest for robustness and a thorough examination of the liquidity-credit risk relationship, we conducted additional analyses employing fixed effect and random effect, as suggested by Danisman and Demirel (2018) and Phan et al. (2020). The incorporation of fixed effects allows us to control for time-invariant variables specific to each bank, offering a nuanced perspective on how these unchanging factors may influence the observed relationship. Simultaneously, random effects provide insights into unobserved heterogeneity across banks, capturing variations that might not be explicitly accounted for in our baseline regression. The results from these robustness checks, as presented in Table 11, affirm the stability and reliability of our primary findings, particularly emphasizing the negative and significant effect of Third-Party Fund (GTPF) growth on non-performing loans (NPL). Importantly, this consistency across different econometric methodologies reinforces the credibility of our conclusions, assuring that the observed impact of liquidity on credit risk is not an artifact of specific modeling choices. Additionally, our analysis delves into the specific impact of the payment (PAY) FinTech category, revealing a positive and significant association with NPL. This finding suggests that the development of payment FinTech might introduce disruptive elements, influencing the credit risk landscape within the banking sector.

Liquidity and Credit Risk (Robustness Check with Alternative Econometric Methodology)

Note. LIQ = ratio of current assets to total assets. Standard errors of each coefficient are in parentheses.

, **, and * indicate significance at the 1%, 5%, and 10%, respectively.

Conclusion

This study investigates the impact of bank liquidity on credit risk and the role of FinTech development in this relationship. Using a two-step GMM system, the empirical results reveal that higher bank liquidity lowers credit risk. However, FinTech development, as a competitive force, increases credit risk in highly liquid banks. Notably, the effects of FinTech development are significant in small banks (BUKU 3 and BUKU 4) and private national banks, particularly in the peer-to-peer lending category. Additionally, FinTech development shows a unidirectional correlation between liquidity and credit risk in normal periods compared to crisis periods.

The study provides important policy implications for designing an inclusive financial framework in the digital era, particularly regarding FinTech development. Policymakers, bank managers, and other stakeholders need to be cautious in promoting FinTech development and consider its impact on different categories of banks. While FinTech can enhance financial inclusion, it may also heighten bank risk, particularly in the context of excess liquidity aggravating the risk-taking moral hazard. Small and private banks are more susceptible to the negative impact of FinTech on the relationship between liquidity and credit risk. Therefore, policies and regulations that aim to promote FinTech development need to be implemented carefully to avoid excessive risk-taking behavior in banks, particularly in the P2P lending category. Moreover, government intervention may be necessary to manage bank risks associated with financial innovation, particularly for government banks that may be less affected by FinTech development. The results of this study can inform policymakers and bank managers in managing the risks and opportunities associated with FinTech development, ensuring financial stability and promoting inclusive growth.

For future research, it is recommended to explore the impact of FinTech on other aspects of banking, such as bank profitability and efficiency. Further research could also investigate the role of government intervention in promoting FinTech development and managing bank risks associated with financial innovation. Additionally, future studies could examine the impact of FinTech development on other categories of banks, such as banks adopting mobile banking and banks affiliated with FinTech companies. Moreover, given the unidirectional correlation between FinTech development and liquidity-credit risk relationship during normal periods compared to crisis periods, future research could investigate the impact of external shocks on the relationship between FinTech development and bank risks, particularly during the COVID-19 pandemic. Finally, it would be beneficial to explore the impact of other types of financial innovation, such as blockchain and digital currencies, on the banking industry.

Footnotes

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: This research was initially funded by Mulawarman University, Samarinda, Indonesia. Further development of the final manuscript was assisted by dissemination funding support from the Regional Research and Innovation Agency of East Kalimantan Province.

Data Availability Statement

Data sharing not applicable to this article as no datasets were generated or analyzed during the current study.