Abstract

In recent times, women have been increasing their participation in company management positions, occupying positions on the board of directors, and making strategic decisions with a view to the international expansion of the firms. However, the evidence of the participation of women in the processes of internationalization of companies is not conclusive or adequate for emerging economies, such as those in Latin America. Based on this premise, we conducted this research using data from 1,246 firms included in the Fifth Longitudinal Survey of Chilean Companies. These companies are categorized into four industries: 98 in extractive, 149 in manufacturing, 285 in Commercial, and 714 in services. A Tobit regression model to estimate the influence of the presence of women in senior management and gender diversity on boards on the export intensity of the company. The main findings show that women in the position of CEO and a higher percentage of women on boards of directors do not affect the export intensity of the company. They also show that the relationship between foreign ownership and export intensity was positive and, finally, that export intensity did not depend on gender diversity in high-level administrative positions. An important limitation of this research is not having a data panel for each company to estimate their evolution over time thus, as well as information related to compensation contracts for management teams. For future research, we are interested in studying the effect of ownership on the internationalization process.

Introduction

During the last decades, increasing market liberalization and privatizations have rapidly increased the internationalization of firms, especially in emerging markets (Agnihotri & Bhattacharya, 2015; McCormick & Somaya, 2020; Ramamurti & Singh, 2009). The discussion on the determinants of firms’ internationalization has generated a growing interest in explaining its causes and associated benefits (Casillas & Moreno-Menéndez, 2017; Falahat et al., 2020; Jiang et al., 2020; Paul et al., 2017; Zhao & Zou, 2002). An essential issue in this field is the contribution of smaller firms (SMEs) to economic and social development through the internationalization of their operations, as well as the internationalization needs of their businesses as a source of growth and/or competitive advantage (Ahmed & Brennan, 2019; Arregle et al., 2017; Breuillot et al., 2022; Calabrò & Mussolino, 2013; Pukall & Calabrò, 2014; Zahra, 2003).

The research on a firm’s internationalization is a developed field rooted in well-known theories from different disciplines (Beugelsdijk et al., 2018; Niittymies & Pajunen, 2020). However, findings and constructs in this field primarily emerge from developed countries; hence, they may not adequately explain the internationalization dynamics in emerging economies, such as those in Latin America (Agnihotri & Bhattacharya, 2015; Spencer Ruff, 2018). On the other hand, understanding firms’ internationalization is incomplete if social changes and institutional conditions are not considered, such as political regulations, market openness, business culture, and social norms (Beugelsdijk et al., 2018; Morrish & Earl, 2020; Park, 2018).

Moreover, these considerations work in two ways: the firm’s domestic country and host contexts. Previous research has demonstrated that the ownership structure and the composition of the company’s board of directors are relevant attributes in the design and development of export strategies (Lukason & Vissak, 2020; Nam et al., 2018; Sareen, 2018; Vega Salas & Deng, 2017). So as to optimize these factors, companies should constantly refine their governance mechanisms, particularly property concentration and board composition, to reduce agency conflicts (Lukason & Vissak, 2020), as well as foster growth in both domestic and international markets (Nas & Kalaycioglu, 2016).

However, there is still a lack of evidence on the impact of the board’s characteristics, such as gender diversity and foreign property, on the firm’s internationalization (Dias et al., 2021; Dixon et al., 2017; Nas & Kalaycioglu, 2016). In the recent time, women have been increasing their participation in leadership positions in business, as entrepreneurs, board directors, and CEOs (Alarcón & Cole, 2023; Moreno-Gómez et al., 2018). Therefore, more frequently, executive-level women take part in strategic decisions that concern the firm’s international expansion (Chadwick & Dawson, 2018).

Women’s opportunities for promotion and representation in leadership, particularly in Latin American companies, remain notably low. Globally, the proportion of women in leadership positions is significantly lower than that of men, reaching 24%. A comparative analysis of regional disparities reveals that European nations lead with 35% female representation, followed by Africa with 27%, Asia-Pacific emerging markets with 26%, North America with 23%, and Latin America with 18% (Avolio & Laura, 2017; Leyva-Townsend et al., 2021).

Women-led firms operating in countries with high levels of gender discrimination are more likely to internationalize their operations, because expanding into foreign markets can mitigate, to some extent, the discriminatory barriers they face in their own countries (Anggadwita & Indarti, 2024; Pindado et al., 2023). While women-led firms are less likely to initiate exporting activities, once involved in international trade, the gender of the CEO does not significantly impact the intensity of their export engagement (Bannò & Filippi, 2024).

On the other hand, economic globalization has increased the labor and investment exchange, promoting foreign investments in domestic markets. This global mobility led to many challenges in equilibrating foreign business culture and domestic management practices (Beugelsdijk et al., 2020; Meyer & Xin, 2018). Foreign investment may change the social norms of business concerns in terms of women’s participation in leadership positions, considering the differences in gender development between countries (Chakabva & Tengeh, 2023; Gulzar et al., 2019).

Despite the increasing body of literature on women’s leadership, there is no conclusive evidence regarding the specific impact of female CEOs or female board members on the export intensity of smaller firms. This might be explained by their underrepresentation in the labor market (Husted & de Sousa-Filho 2019).

Based on these arguments and the inconclusive findings regarding CEO gender and company ownership in developing economies like Chile (which has become one of the most prosperous in Latin America), we propose the following research questions. How does gender diversity in top management positions influence the internationalization of a company? and How does foreign ownership moderate the impact of gender diversity in top management on a company’s internationalization?

This research implements a Tobit regression model to estimate the influence of the presence of women in top management and gender diversity on the board of directors on the firm’s export intensity. We evaluate the results considering different firm sizes and industries and conduct a moderation analysis using interaction effects of the variables. The study was carried out on a sample of 1,246 Chilean firms of varying sizes and sectors representing the Chilean business ecosystem. The findings show that the women in the CEO position and a higher percentage of women in board directors do not affect the firm’s export intensity. The relationship between foreign property and export intensity was positive, that is, greater foreign ownership increases a company’s export intensity. These findings propose that the export intensity does not depend on gender diversity in top management positions, that is, female CEOs and directors may have the same preferences as men in the internationalization decision-making process. The positive relationship between foreign property and export intensity suggests that the alien investors may imprint their globalized business vision on domestic firms and encourage their internationalization expectations.

Our findings contribute to internationalization literature, imprinting a social perspective of a firm’s internationalization process. The evidence related to the effect of women’s participation in top management business positions on the decision-making process is mixed. Still, we observed a prevalence of the myth that women are less likely to undertake the riskiest actions, such as making internationalization decisions and increasing the firm’s export intensity. In this vein, we discard a significant relationship between gender and firm internalization, suggesting that women may have the same preferences as men in the internationalization decisions. On the other hand, the positive relationship between foreign ownership and export intensity identified in this study is helpful for public policymakers in emerging economies. Increasing export activity and international exchange of resources may be necessary to stimulate foreign investment in domestic firms to enhance the knowledge of global markets and successful internationalization processes.

The rest of the paper is organized as follows. Section 2 defines the literature review and hypotheses are formulated based on the relevant literature. Details of the research design are provided in Section 4. An empirical analysis is presented in Section 5, including details of additional testing and robustness testing. Conclusions are provided in Section 6.

Literature Review

Theoretical Development on Firms’ Internationalization as a Field of Research

Internationalization of the firm is a heterogeneous research field because of the diversity of theories used to explain a company’s internationalization process (Eduardsen et al., 2023; McCormick & Somaya, 2020). In this vein, the international expansion of business involves many issues, such as foreign investment strategies, competitive advantages, dynamic capabilities, and strategic considerations (Breuillot et al., 2022; Falahat et al., 2020; Jiang et al., 2020). Therefore, various approaches are necessary to study the different phenomena related to internationalization. At the end of the 1960s, the first theories explaining the internationalization of companies emerged, considering direct foreign investment as a consequence of the relative differences in profitability and interest rates between countries (Spencer Ruff, 2018). In this early stage of research, the internationalization strategies related to technology transfer, organizational capabilities, and reciprocal commerce interaction between developed and emerging economies were not considered in depth (Brush & Manolova, 2004; Tiessen et al., 2001).

Other theories explain internationalization as a diversification strategy to deal with investment risks that depend on the risk aversion profile adopted by the company (Aliber, 1970; Ragazzi, 1973; Tobin, 1958). Also, the literature based on new proposals on the internationalization of companies, especially SMEs, has experienced significant growth and increasing complexity (Arregle et al., 2017; Casillas & Moreno-Menéndez, 2017; Pukall & Calabrò, 2014). In this vein, the research has been expanded to explain the internationalization process beyond the imperfections of capital markets (Spencer Ruff, 2018; Wadeson, 2020). Thus, theories have emerged referring to the life cycle of companies and gradual internationalization (Upsala model) associated with better experiential knowledge of international markets that allow for reducing the risks associated with this decision (Cuervo-Cazurra, 2012; Wadeson, 2020).

The existence of market failures that lead to transactions between countries has motivated other theoretical frameworks that consider these transactions as subject to a high level of uncertainty and based on complex and heterogeneous products (Mariotti & Marzano, 2020). The resource-based view also has been applied to study firms’ internationalization, arguing that multinational companies with organizational capabilities and strategic resources will be more likely to invest in international markets if they can obtain superior and sustainable performance (Ramon-Jeronimo et al. 2019). On the other hand, the theory based on Dunning’s eclectic paradigm (OLI model) proposes that a company will internationalize its operations when it meets three conditions simultaneously: (a) ownership advantages, (b) location advantages, and (c) internationalization advantages (Dunning, 1988, 1997; 2000).

The theories applied to explain the firm’s internationalization process recognize the importance of the firm’s international expansion as a source of competitive advantage and better performance (Boso et al., 2019; Sun et al., 2019). The internationalization of companies requires taking challenges and risks; in this vein, the evidence shows that before internationalizing their businesses, companies must reach a certain level of economies of scale and experience to participate in the changing international market adequately (Minetti et al., 2015; Nam & An, 2017). Moreover, previous studies identify that the internationalization of a company is determined by its level of productivity, size, and the existence of entry barriers in international markets and can be measured based on the export intensity of goods and/or services (Bernard & Jensen, 2004; Kneller et al., 2008; Wagner, 2021).

Previous research has demonstrated that export intensity is explained by firm size and ownership concentration (Filatotchev et al., 2008; Gaur & Delios, 2015; Lukason & Vissak, 2020; Robson & Freel, 2008). In this vein, it is evidence that ownership concentration allows greater control over managers; thus, owners can focus on strategic decisions that promote greater long-term efficiency (Bhaumik et al., 2017; Farooque, 2021; Shleifer & Vishny, 1997; Wellalage & Locke, 2011). Moreover, various studies have found that a more concentrated ownership structure positively and significantly affects the firm’s internationalization process (Fernández & Nieto, 2006; Gomez-Mejia et al., 2010; Karaevli & Yurtoglu, 2021; Lukason & Vissak, 2020).

On the other hand, Vega Salas and Deng (2017) finds that the concentration of ownership, especially in emerging countries, may favor the existence of agency problems between majority and minority shareholders or between agent and principal. The internationalization process of companies increases the complexity of their business and control and requires companies to have corporate governance practices that reduce the associated risks (Dixon et al., 2017; Lukason & Vissak, 2020; Sanders & Carpenter, 1998). Evidence shows that the internationalization process is favored by the management of Corporate Governance (CG) since it seeks to promote better conditions that increase competitiveness (Maia et al., 2013; Nas & Kalaycioglu, 2016).

As described above, firms’ internationalization processes have been analyzed under several approaches. However, it is necessary to extend the internationalization literature toward a more inclusive approach highlighting the social norms that predominate in the assumptions of firms’ internationalization decision dynamics (Ahmed & Brennan, 2019; Beugelsdijk et al., 2018; Niittymies & Pajunen, 2020). Another essential issue to consider in a firm’s willingness to export is the effects of foreign property on the relationship between gender diversity in the top management and the firm’s internationalization (Kabir & Thai, 2021; Pergelova et al., 2018). The foreign investor may imprint their beliefs on gender diversity in the business management style, according to their experiences in their own country (Ain et al., 2022).

Involvement of Female Directors and CEOs in the Firm’s Internationalization Decisions

Recently the literature has turned to identifying the barriers that affect companies led by women when they attempt to internationalize their operations, highlighting the fact that women are less predisposed to implement high-growth strategies than their male counterparts, due to certain family and/or work considerations that could intentionally encourage their participation in local companies (Akter et al., 2019; Cliff, 1998; Kepler & Shane, 2007). Thus, it is less likely that women will take on risks than their male counterparts and, given that internationalizing operations implies risks, it is possible they may decide not to expand their companies (Aculai et al., 2006; Boustanifar et al., 2022). In this vein, the literature describes women as cautious, conservative, and risk adverse (Hurley & Choudhary, 2020; Marlow & McAdam, 2012; Marlow & Swail, 2014; Pergelova et al., 2018).

For its part, the extant discrimination against professional women in Latin America obligates them to demonstrate greater experience and qualifications than their male counterparts to obtain the position of CEO in a company (Moreno-Gené & Gallizo, 2021; Singh et al., 2008). Also, the existence of gender quotas on boards of directors is observed as an impairment to their management capacities by the presidents of boards of directors (Atinc et al., 2022; Casaca et al., 2022; Zehnder, 2016).

Gender diversity on the board and in the management of companies promoting internationalization strategies may generate benefits (Berenguer et al., 2016). For example, it may enrich the decision-making process, allowing better decisions to be made, promoting corporate innovation, enabling better analysis of complex problems, and producing more knowledge, ideas, and information that favor the boards’ abilities to deal with non-routine problems (Chen et al., 2018; Huse & Solberg, 2006; Kamenou-Aigbekaen, 2019; Kanadlı et al., 2018; Kirsch 2018; Levi et al., 2014).

In addition, the inclusion of female directors provides a positive image for the firm that can enhance competitive advantage and improve ties with external stakeholders, contributing to the firm’s legitimacy by promoting gender equality in response to social diversity norms (Hillman et al., 2002; Hillman et al., 2007; Isidro & Sobral, 2015; Knippen et al., 2019). However, Carter et al. (2010) find that gender diversity could have inconclusive effects that depend on certain internal and external conditions that affect the company.

On the other hand, Lukason and Vissak (2020) and Reavley et al. (2005) do not find evidence that the participation of women on the board of a company positively influences its internationalization. Similar results are found by Grondin and Schaefer (1995) for a sample of Canadian SMEs, Westhead et al. (2001) for a sample from the United Kingdom, and Berenguer et al. (2016) in a sample of Spanish small and medium enterprises. Moreover, some studies suggest that more female directors can negatively affect the firm’s performance and internationalization by affecting the decision-making process (Benito-Ossorio et al., 2020; Joshi et al., 2006; Richard et al., 2004; Triana et al., 2014).

As pointed out, a firm’s internationalization decisions increase business complexity and involve several risks; therefore, the decision-makers risk preferences influence the firm’s international expansion (Boustanifar et al., 2022; Minetti et al., 2015; Nam & An, 2017). In this vein, the effects of female directors and CEOs on firms’ risk attitudes and internationalization are not conclusive (Ossorio, 2017). Evidence shows that women in management tend to take more risks in their decisions than men (Charness & Gneezy, 2012; Jurajda & Janhuba, 2018; Poletti-Hughes and Briano-Turrent, 2019). On the other hand, an extensive body of literature suggests a negative association between a female CEO and firm risk attitudes (Carter et al., 2017; Dowling & Aribi, 2013; Mateos de Cabo et al., 2012; Zalata et al., 2019). On the other hand, Benito-Ossorio et al. (2020), in a study of board gender diversity and cross-border mergers and acquisitions, found that more female directors reduced the firm’s likelihood to acquire a foreign target. Based on these findings and considering that internationalization is a risky choice, the following hypotheses are proposed.

H1. The presence of women in the company’s executive management negatively affects the company’s export intensity.

H2.A higher presence of women on a company’s board of directors negatively affects the company’s export intensity.

Foreign Ownership in the Company, Internationalization Decisions, and Female Leadership

There is little evidence in developing countries of the effects of property structure, as a whole, and foreign property in particular, as drivers of the relationship between internationalization and performance (Bykova & Lopez-Iturriaga, 2018; Narteh & Acheampong, 2018; Onjewu et al., 2024). Evidence seeks to explain the export intensity of firms with foreign investors in the firm’s ownership, suggesting that firms that are more concentrated and with a high presence of foreign directors tend to export more (Nam et al., 2018; Webster et al., 2022; Woo, 2020).

Filatotchev et al. (2008), find a positive relationship between foreign ownership, managerial independence in decision-making, and export intensity, using a sample from Poland, Hungary, Slovenia, Slovakia, and Estonia. This is due to the fact that when foreign investors participate on the board it is more likely that companies will adopt international standards of governance and commercial practice, which facilitates entry into international markets (Gulzar et al., 2019; Park, 2018).

Those companies that count on the participation of foreign investors on their boards generally possess intangible assets that can provide a competitive advantage in the international market that could facilitate their internationalization processes (Boso et al., 2019; Filatotchev et al., 2007). Webster et al., (2022), find that foreign property positively and significantly affects company performance, as well as productivity and level of exports for a sample of African companies.

From resource theory, it is observed that when the objective of a foreign investor is to leverage resources and capabilities of the subsidiary in other countries and create economies of scale, which otherwise would not be available domestically, then ensuring total control over the internationalization strategy and decisions can become a critical success factor (Andersen, 1993; Gereffi, 2019; Shahbaz et al., 2015). Bykova and López-Iturriaga (2018) find, for a sample of Russian manufacturing companies, a positive and significant relationship between exports and company performance, which can be explained from the advantages of the participation of foreign companies in ownership.

However, Rojec et al. (2004) find that export intensity is due to foreign ownership and structural differences between domestic and foreign companies in those companies where foreign investors participate. For their part, Singla et al. (2017) find that foreign investors adjust their preferences and/or decisions according to the dominant national family owners and, thus, this participation would not directly affect the internationalization process of the company. Along the same lines, Calabrò and Mussolino (2013) and Jackson and Strange, 2008, study the effects of resource transfer between affiliated, subsidiary and/or joint-venture companies when there are local and foreign investors among their owners. The main effects are associated with issues of financial – accounting control (Henry et al., 2007; Panicker et al., 2019) and the misappropriation of funds of minority shareholders (Bona-Sanchez et al., 2017). Therefore, and given these corporate governance practices, a negative and adverse effect is observed in internationalization (Agnihotri & Bhattacharya, 2019). According to the above arguments, the following hypothesis is proposed.

H3. The participation of foreign investors in the company’s ownership moderates the effects of the presence of women in the company’s executive management on the company’s export intensity.

H4. The participation of foreign investors in the company’s ownership moderates the effects of the presence of women on a company’s board of directors on the company’s export intensity.

Methodology

Sample

This research uses data from the Fifth Longitudinal Business Survey (INE, 2018), which includes relevant information from more than 6,000 Chilean firms. The final sample considered 1,246 businesses since they have complete data for all variables included in this study. On average, the firms have 21 years of operation, and 34.2% are involved in some innovation activity. Women-led businesses represent 17.2% of the sample, and the average percentage of women on the board of directors is 12.9%, which shows the gender disparity in access to top management positions. The firms that export (goods and/or services) are 20.1% of the sample, and the average sales for export transactions represent 9.7% of total business sales. Descriptive statistics are presented in Table A1.

Variables

This study uses one dependent variable, two independent variables, one moderator variable, five control variables (Éxposito et al., 2022), and two terms of interaction effects. The dependent variable is the export intensity measured by the percentage of the firm’s total sales produced by export (goods and/or services) transactions, expressed in rates. The independent variables are female CEO and gender diversity on boards of directors. The female CEO is a dichotomous variable that takes the value of one if the firm is led by women and zero otherwise. The board’s gender diversity is measured by the percentage of women directors over total board directors, expressed in rates. The foreign participation in ownership is included in the model as a moderator variable and represents the proportion of the firm under a private foreign owner.

The moderation analysis considers two constructed variables, the interaction effects of foreign participation in ownership on (a) the relationship between female CEO and export intensity and (b) the relationship between gender diversity on the board of directors and export intensity. We include innovation activities, capital intensity, and age as control variables. Innovation is a dichotomous variable that takes the value of one if the firm is involved in some innovation activity and zero otherwise. Capital intensity is measured as the ratio between asset value and salary costs; thus, a higher level of capital intensity represents higher capital consumption than labor. The firm’s age is the years of operation; additionally, we include the age squared measure to control the possible non-linear effect of the firm’s age on export intensity.

Methods

First, we analyze the pairwise correlations between variables and find significant correlations in most cases; however, most of these correlations are lower than |0.16| (see Table A2), highlighting the statistical significance between the variables of board diversity, foreign ownership, innovation, firm age, and capital intensity.

Following Tobin (1958), we use the Tobit model for its original purpose, that is, a suitable method when the outcome variable is left-censored at zero. In some cases, the variable under study exhibits specific upper and lower limits that affect its distribution, resulting in a degree of truncation. Additionally, due to the transient nature of the data, where firms may enter or exit the sample (Pham, 2017), we further account for potential censoring using the Tobit regression model to estimate the propensity to export (Manogna & Mishra, 2022).

Our dependent variable is export intensity which cannot take negative values because it represents the proportion of the firm’s total sales produced by export transactions; the lowest value that the variable can take is zero in the case of those firms that do not export; therefore, we have 251 uncensored observations.

In order to understand the results better, we test the hypotheses across different firm size ranges, using quartiles to estimate the impact separately across four industries: extractive, manufacturing, commercial, and service. This approach was chosen due to the relative importance of these industries and the feasibility of effectively categorizing the data within these groupings. This criterion classified the firms into four groups according to their sizes, with the largest size being 24.56 (natural logarithm of asset value). The quantiles considered the following intervals:

Therefore, we specified the following models considering first a pooled estimate and subsequently by quartile and by industries, respectively. This approach has been proposed in order to estimate the effects of variables that influence export intensity according to the firm’ size (Expósito et al., 2022), allowing us to evaluate hypotheses 1 and 2.

In our analysis,

Where

In order to analyze the differential effects of variables on export intensity across different industries, model (1b) is proposed, where the subscript z represents each of the industries that take part in the analysis.

Where

Moderation Effect Analysis

To estimate the effects between the variables that define export intensity, we consider the moderating effects of the representation of foreign investors in companies (Expósito et al., 2022; Vega Salas & Deng, 2017), and thus, evaluate the proposed hypotheses 3 and 4. Following our first proposed Tobit regression model equation, we evaluate hypotheses 3 and 4 across different ranges of firm sizes and industries. We proposed the following equation model to conduct the moderation analysis, where the subscript

Where

Where

Since

Robustness Check

To confirm the stability of our solution to equation (1), we run a robustness check using the Poisson regression model. The Poisson regression model maintains the restriction of

Results

As mentioned above, to test the hypotheses and estimate the firm’s level export intensity, we first propose a pooled dataset of firms (1a). Then, to assess the impact of firm size, we estimate model (1b). The pooled estimation indicates that CEO gender (F) and board diversity (D) are not significant factors in internationalization. This finding aligns with the studies by Lukason and Vissak (2020) and Reavley et al. (2005), which suggest that female-led firms do not significantly differ from those led by male CEOs in terms of exporting (see Table 1).

Tobit Regression Model Results by Quartiles.

Note. *, **, *** significance level at 0.10, 0.05, 0.01.

However, when analyzing the data by quartiles and estimating the effects of CEO gender (F) and Board of Directors diversity (D), it is observed that only CEO gender has a positive and significant influence on the internationalization process of the Model 1/Q2 company (0.350, ρ < .05). This result aligns with the findings of (Isidro & Sobral, 2015; Hillman et al., 2002; Hillman et al., 2007; Knippen et al., 2019), who suggest that female CEO leadership can positively impact internationalization. Therefore, we reject hypothesis 1.

Regarding hypothesis 2 of this research, which states a negative relationship between female board representation and export intensity our analysis of both pooled and quartile-level data does not yield any significant result (See Table 1), despite the findings in the existing literature. However, the results are in line with those of Allen et al. (2007), Dowling and Aribi (2013), Grondin and Schaefer (1995), Reavley et al. (2005), Westhead et al. (2001), and Zalata et al. (2019), who also find have found no significant relationship between the presence of women on the board of directors and export intensity. Therefore, there is no evidence to reject hypothesis 2.

Additionally, the results obtained for hypotheses 1 and 2 may be explained by the lower participation of women in top management positions, such as CEO or board members in Latin American and Caribbean companies compared to other regions like North America and Europe (Marquez-Cardenas et al., 2022). Similarly, Ramón-Llorens et al. (2017) find no observable effect of CEO gender on firm internationalization. Furthermore, Arenas-Torres et al. (2021), in a study of Chilean companies, conclude that the participation of women on boards and in leadership positions does not result in significant differences compared to their male counterparts. Despite recent legislative efforts aimed at promoting gender diversity, the observed effects remain marginal (Reguera-Alvaradorga et al., 2017).When analyzing the effects of foreign ownership, a positive and significant relationship is observed both in the pooled data and across all quartiles. In the estimation (1a), a coefficient of 0.534 (ρ < .01) is reported, with a standard deviation of 0.081 (See, Table 1). In the estimation of (1b), the results also indicate a positive and significant relationship (see Table 1) for Model 1/Q1 (0.855, ρ < .01), Model 1/Q2 (0.492, ρ < .01), Model 1/Q3 (0.270, ρ < .1), and Model 1/Q4 (0.435, ρ < .01). The results are in line with those proposed by Shahbaz et al. (2015), Bykova and Lopez-Iturriag (2018), and Gereffi (2019), who similarly report a positive and significant relationship between export level and the participation of foreign investors in ownership.

Regarding control variables, innovation (I) and firm age were found to be relevant determinants of firm internationalization when analyzing the pooled data (see Table 1). However, when examining the effects by quartile, it was found investment had a positive and significant impact only on the first quartile Model 1/Q1 (0.410, p < .01), while firm age exhibited a positive and significant relationship for Model 1/Q2 (0.027, p < .05); Model 1/Q3 (0.026, p < .1); and Model 1/Q4 (0.024, p < .1) and these findings align with (Éxposito et al., 2022).

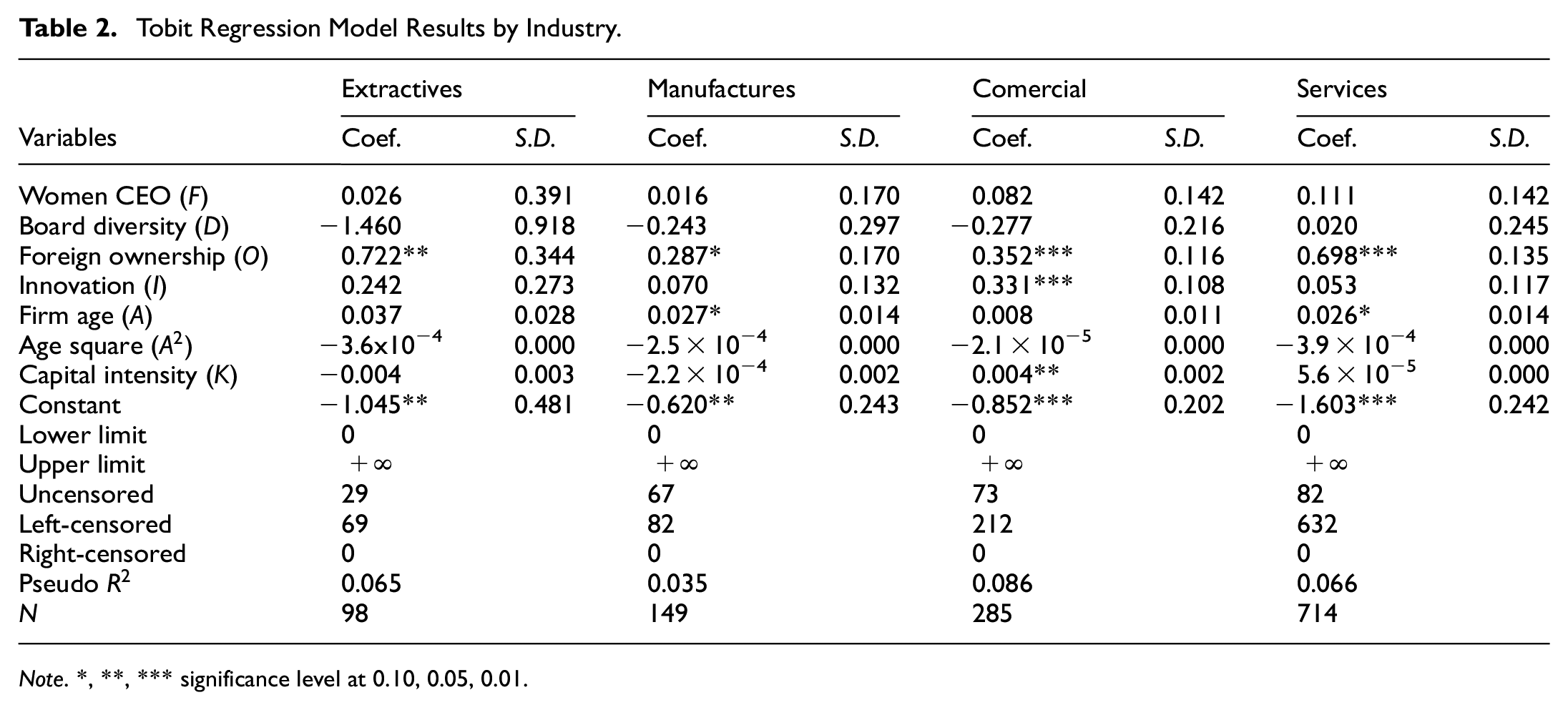

When estimating model (1a) by industry, a similar impact is observed for CEO gender (F) and board diversity (D), as neither of these variables significantly affects export levels. However, a positive and significant relationship is also found for the Foreign Ownership (O) variable in all industries (see Table 2). Notably, extractive industries show the strongest impact (0.722, ρ < .05), followed by services (0.698, ρ < .01), commercial (0.352, ρ < .01), and manufacturing (0.287, ρ < .10).

Tobit Regression Model Results by Industry.

Note. *, **, *** significance level at 0.10, 0.05, 0.01.

While foreign ownership (O) positively impacts export intensity, there is no evidence to suggest that the presence of a female CEO (F) and the interaction with

Tobit Regression Model Results, Interaction Effects by Quartiles.

Note. *, **, *** significance level at 0.10, 0.05, 0.01.

Tobit Regression Model Results, Interaction Effects by Industry.

Note. *, **, *** significance level at 0.10, 0.05, 0.01.

With respect to the variable,

Discussion and Conclusion

The development of the determinants of internationalization is an established area in developed countries, but the proposed theories are not adequate for emerging economies (Panicker et al., 2019). For this reason, this study has focused on studying those variables that explain internationalization for a sample of 1,246 Chilean SMEs firms of varying sizes and sectors representing the business ecosystem in an emerging economy.

The results show that for small-medium size companies, a positive and significant effect is observed for the participation of women on the executive management on the export intensity of the company. Contrary to previous literature, our findings suggests that women in the top management position are willing to undertake internationalization processes, taking the risk associate with this type of operations (Akter et al., 2019; Poletti-Hughes & Briano-Turrent, 2019). In this vein, the notion that women are more risk averse than men is questionable from a strategic point of view (Charness & Gneezy, 2012; Jurajda & Janhuba, 2018). Thus, women CEOs may have similar expectations of business international expansion than men CEOs, and the negative effect of female gender on internationalization, find in previous studies, may be generated by other conditions (Akter et al., 2019; Carter et al., 2010; Moreira et al., 2019).

According to Ossorio (2017), the gender diversity may stimulate the firm’s internationalization but may increase the firm’s risk aversion decreasing the risky invests like internationalization. This duality represents a challenge to determine the real effect of board gender diversity in firm’s internationalization. Our results do not show a significant relationship between the share of women in directors’ board and the export intensity.

Therefore, our findings are in line with the not conclusive effect of board diversity on internationalization decision and we propose that may exist institutional, social, or cultural conditions that shape the decision-making process to export in a gender diverse board (Berenguer et al., 2016; Giraldez-Puig & Berenguer, 2018; Ossorio, 2017). This could be explained by Expósito et al. (2022) who find that there are no significant differences in export propensities between male and female CEOs for a sample of European companies, as the export orientation was the same for the two of them.

A non-significant causal relationship between gender diversity in top management positions and export intensity is observed in smaller-sized Chilean companies, which could be explained by the lower participation of women in Latin-American firms compared to developed countries (Márquez-Cardenas et al., 2022; Zehnder, 2016).

Previous evidence has been demonstrated that firms with high presence of foreign directors tend to export more (Nam et al., 2018; Woo, 2020). In this vein, foreign ownership may change the relationship between female CEO’s and directors and export intensity. Although, the relationship between foreign property and export intensity was positive, that is, greater foreign ownership increases a company’s export intensity, we found a negative effect of foreign ownership on the relation between board diversity and export intensity in the medium-size companies.

Property concentration and foreign investment favors internationalization in Latin American countries (Aguilera & Crespi-Cladera, 2016; Vega Salas & Deng, 2017; Webster et al., 2022). These factors can facilitate access to foreign markets, allowing smaller-sized companies to expand their reach. Additionally, they can lead to better management practices, intellectual capital development, and improvement in production quality (Atkin et al., 2017; Sanyaolu et al., 2022; Teplova et al., 2022).

Therefore, in companies with high levels of foreign ownership, the high presence of women in board of directors negatively affects the export intensity. However, the presence of women directors does not affect the export intensity; moreover, we cannot find a change in the significance on this relation when the foreign ownership variable was introduced. Finally, our results do not show differences in the models between industries.

Our results allow us to contribute to the literature of processes of internationalization and its causes from a gender perspective as it deals with the effects of a woman in the CEO position or participating in the executive management of the organization. The findings show that women in the CEO position and a higher percentage of women in board directors do not affect the firm’s export intensity, except in the case of small-medium size companies. Interestly, our research suggests that the companies with a female CEO’s may show higher levels of export intensity than the firms led by men. These findings propose that the export intensity does not depend on gender diversity in top management positions, that is, female CEOs and directors may have the same preferences as men in the internationalization decision-making process.

Finally, we estimate that this research could contribute to explaining the level and quality of the growth of some companies that have or are developing internationalization strategies and that seek to promote certain strategies for gender equality in their organizations.

Limitations and Future Research Agenda

An important limitation of this research is not having a data panel for each of the companies to thus estimate their evolution over time, as well as information related to compensation contracts for management teams. For future research, we are interested in studying the effect of ownership and membership in an economic group on the internationalization process.

Footnotes

Appendix

Robustness Check. Poisson Regression Model.

| (a) Poisson regression model by quantiles | ||||||||||

|---|---|---|---|---|---|---|---|---|---|---|

| Variables | Model 1 | Model 1/Q1 | Model 1/Q2 | Model 1/Q3 | Model 1/Q4 | |||||

| Coef. | S.D. | Coef. | S.D. | Coef. | S.D. | Coef. | S.D. | Coef. | S.D. | |

| Women CEO ( ) | 0.104 | 0.240 | −0.790 | 0.902 | 0.655 | 0.399 | −0.353 | 0.626 | 0.074 | 0.399 |

| Board diversity ( ) | −0.195 | 0.411 | 1.109 | 0.973 | −0.463 | 0.757 | 0.335 | 0.932 | −0.273 | 0.878 |

| Foreign ownership ( ) | 0.943*** | 0.197 | 2.211*** | 0.570 | 0.767** | 0.384 | 0.434 | 0.427 | 0.722** | 0.357 |

| Innovation ( ) | 0.469** | 0.184 | 1.353** | 0.577 | 0.307 | 0.372 | 0.101 | 0.395 | 0.430 | 0.301 |

| Firm age ( ) | 0.039** | 0.019 | 0.114 | 0.151 | 0.043 | 0.037 | 0.013 | 0.040 | 0.056 | 0.035 |

| Age square ( ) | −3.2x10−4 | 0.000 | −0.004 | 0.005 | −3.2x10−4 | 0.000 | −8.9x10−5 | 0.001 | −5.5x10−4 | 0.000 |

| Capital intensity ( ) | 6.6x10−6 | 0.001 | −0.066 | 0.151 | −0.036 | 0.030 | −0.004 | 0.009 | −0.001 | 0.001 |

| Constant | −3.429*** | 0.317 | −4.745*** | 1.237 | −3.099*** | 0.642 | −2.737*** | 0.686 | −3.199*** | 0.651 |

| Pseudo | 0.043 | 0.209 | 0.057 | 0.012 | 0.044 | |||||

| N | 1,246 | 312 | 311 | 311 | 312 | |||||

| (b) Poisson regression model by industry. | ||||||||||

| Extractive | Manufacturing | Commercial | Service | |||||||

| Variables | Coef. | S.D. | Coef. | S.D. | Coef. | S.D. | Coef. | S.D. | ||

| Women CEO ( |

−0.226 | 0.707 | 0.176 | 0.433 | 0.171 | 0.640 | 0.397 | 0.397 | ||

| Board diversity ( |

−1.349 | 1.372 | −0.150 | 0.737 | −0.796 | 0.933 | 0.321 | 0.738 | ||

| Foreign ownership ( |

0.818* | 0.469 | 0.310 | 0.446 | 0.755* | 0.452 | 1.558*** | 0.344 | ||

| Innovation ( |

0.336 | 0.421 | 0.056 | 0.349 | 0.800* | 0.432 | 0.172 | 0.342 | ||

| Firm age ( |

0.068 | 0.063 | 0.055 | 0.042 | 0.009 | 045 | 0.020 | 0.037 | ||

| Age square ( |

−0.001 | 0.001 | −0.001 | 0.001 | 9.9 × 10−5 | 0.001 | −3.8 × 10−4 | 0.001 | ||

| Capital intensity ( |

−0.006 | 0.005 | 0.002 | 0.004 | 0.009** | 0.005 | 0.001 | 0.001 | ||

| Constant | −2.288*** | 0.834 | −2.559*** | 0.718 | −3.452*** | 0.809 | −3.915*** | 0.532 | ||

| Pseudo |

0.062 | 0.022 | 0.072 | 0.074 | ||||||

| N | 98 | 149 | 285 | 714 | ||||||

Note. *, **, *** significance level at 0.10, 0.05, 0.01.

Acknowledgements

Not applicable

Ethical Considerations

An ethics statement (including the committee approval number) for animal and human studies. If this is not applicable, please state this instead.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Data Availability Statement

The data for the study is not available due to restrictions from the organization.