Abstract

Green and sustainable corporate development promotes economic, environmental, and social sustainability. It significantly enhances long-term corporate profitability and mitigates climate change. An essential avenue toward fostering green sustainable development among enterprises lies in the organic amalgamation of digital technology with the real economy, commonly called digital-real integration. Hence, a comprehensive exploration of digital-real integration and its impact on the green sustainable development of enterprises becomes imperative. This study endeavors to address this need by constructing a two-sector four-factor model focusing on production and R&D. It examines both factor-based integration and technology-based integration of digital technologies to assess their influence on the green sustainable development of enterprises, alongside scrutinizing the bias of technological progress from both theoretical and empirical standpoints. This paper employs panel data from Chinese A-share listed companies covering the period from 2000 to 2022 to develop a model for empirical analysis. The findings reveal that both factor-based fusion and technology-based fusion positively contribute to the green sustainable development of enterprises. However, factor-based fusion exhibits an inverted U-shaped curve relationship, a significant positive promotional effect is observed only when the critical threshold is not exceeded. Furthermore, through a lens of heterogeneity, enterprises grappling with poor revenue status, technological backwardness, inadequate internal control, and non-compliance with the SDG policy may encounter challenges in executing digital-realistic fusion. Subsequent investigations indicate that digital-realistic integration results in a bias toward digital capital and skilled labor, favoring technological advancement. In light of these findings, we propose the following policy recommendations: (1) expedite innovation and optimize the industrial framework; (2) implement tax incentives and fiscal policies to enhance the company’s revenue profile and promote technological advancement; and (3) establish mandatory environmental regulations to ensure the company’s compliance with its sustainable development objectives. These strategies offer a noteworthy Chinese paradigm that could be adapted for fostering sustainable development in developing countries.

Plain language summary

Green and sustainable corporate development promotes economic, environmental, and social sustainability. An essential avenue toward fostering green sustainable development among enterprises lies in the organic amalgamation of digital technology with the real economy, commonly called digital-real integration. This study endeavors to address this need by constructing a two-sector four-factor model focusing on production and R&D. It examines both factor-based integration and technology-based integration of digital technologies to assess their influence on the green sustainable development of enterprises, alongside scrutinizing the bias of technological progress from both theoretical and empirical standpoints. This paper employs panel data from Chinese A-share listed companies covering the period from 2000 to 2022 to develop a model for empirical analysis. The findings reveal that both factor-based fusion and technology-based fusion positively contribute to the green sustainable development of enterprises. However, factor-based fusion exhibits an inverted U-shaped curve relationship, a significant positive promotional effect is observed only when the critical threshold is not exceeded. Furthermore, through a lens of heterogeneity, enterprises grappling with poor revenue status, technological backwardness, inadequate internal control, and non-compliance with the SDG policy may encounter challenges in executing digital-realistic fusion. Subsequent investigations indicate that digital-realistic integration results in a bias toward digital capital and skilled labor, favoring technological advancement. In light of these findings, we propose the policy recommendations, offering a noteworthy Chinese paradigm that could be adapted for fostering sustainable development in developing countries.

Keywords

Introduction

The Sustainable Development Goals (SDGs) have long been a topic of great concern for governments and academics alike (Bautista-Puig et al., 2024; Sorooshian, 2024). They represent a direction that humanity strives to achieve, emphasizing the promotion of green transformation within enterprises and the coordinated development of the economy and the environment (Abbas, 2024; Zhuo et al., 2024). Over the past three decades, China has emerged as a significant player in the global economy, with companies playing a pivotal role in enhancing economic performance (Ciravegna & Michailova, 2022; Ndubisi et al., 2021; Zameer et al., 2020). According to iFinD data as of March 1, 2024, among over 5,000 listed companies in the A-share market, 44 companies are projected to have generated revenues exceeding 10 billion yuan in the previous year (J. Li et al., 2024). Noteworthy among them are Greenland Holdings, Green Electric Appliances, TCL Technologies, and Guizhou Moutai, with revenues of 360, 207.5, 175.45, and 149.5 billion yuan, respectively. These companies boast operations spanning across every province in China as well as in overseas markets. However, scholarly literature highlights that despite their contributions to economic development, these companies have significantly impacted local energy consumption, air quality, and ecological balance (Chai et al., 2021; Chien et al., 2021). Amidst these challenges, the Chinese government is actively implementing policies and regulations to align with the United Nations Sustainable Development Goals (SDGs) program (Lin, 2021; Odoch et al., 2021; Xiao et al., 2024). This initiative aims to expedite the transition to renewable energy sources and address issues related to resource wastage and environmental degradation (Cantarero, 2020; S. Xu, 2021). A recent illustration of this effort is the issuance of the “Opinions on Strengthening Ecological and Environmental Zoning Control” by the General Office of the State Council of China on March 6, 2024. This policy reinforces measures for preventing and mitigating water pollution and environmental risks within enterprises, while also optimizing industrial layouts and fostering green, low-carbon, and recycling-oriented development strategies. Such initiatives may stem from governmental apprehensions that relocating heavy industrial enterprises to regions with superior ecological conditions could potentially harm local environments. However, notwithstanding these efforts, as documented in the China Environmental Yearbook (2022), enterprises in specific regions of China continue to grapple with significant challenges to green and sustainable development. These challenges include issues such as excessive energy consumption, inefficient production capacities, and the relative scarcity of natural resources (Cheng et al., 2020; L. Xu & Tan, 2020; Z. Yang & Solangi, 2024). Consequently, there arises a pressing need for comprehensive and in-depth research into the green sustainable development of enterprises, with a focus on exploring viable pathways for fostering harmonious coexistence between enterprises and the ecological environment, all while advancing economic prosperity.

China’s real economy is experiencing rapid development, with manufacturing serving as its cornerstone (Hao et al., 2023; Ren et al., 2021). Since 2010, China’s manufacturing industry has consistently held the top position globally in terms of output value for 13 consecutive years, earning it the moniker “world factory” (X. Li et al., 2020; Y. Li et al., 2020; K. Li et al., 2022; Tan et al., 2024). However, numerous challenges persist in the transformation of the manufacturing sector, including issues such as market risks and disruptions in the industrial and supply chains in the post-epidemic era (Cai & Luo, 2020; Karmaker et al., 2023; Paul et al., 2021). The phenomenon of being “big, but not strong, comprehensive, but not excellent” stands as a central impediment to the industry’s advancement (X. Li et al., 2020; Y. Li et al., 2020; Dong et al., 2021; K. Li et al., 2022). Emphasized in the report of the 20th National Congress of the Communist Party of China (CPC) is the concept of digital-real integration, which advocates for the deep integration of the digital economy with the real economy to propel the digitalization of the manufacturing sector (D. A. Gao et al., 2024; D. Gao, Zhou, Mo et al., 2024; D. Gao, Zhou, Wan, 2024; J. Su et al., 2021; Zhang et al., 2021). Digital-real integration refers to the profound integration and development of the digital economy alongside the real economy (Ouyang, 2024). This process encompasses the application, penetration, and transformation of digitalization within the non-digital real economy, thereby enabling the digital economy to enhance the growth of the real economy. The concept of digital-real integration can be understood from three perspectives: First, the integration and application of digital technology within the real economy; Second, the integration and application of the digital economy with the real economy; and third, the integration and application of various elements of digitization (Xi, 2024)—such as the Internet, 5G, cloud computing, data resources, and digital talent—into the non-digital real economy (Javaid et al., 2024). Positioned as a novel production factor, digital technology emerges as the linchpin in driving the digital transformation of enterprises and the advancement of the real economy. The seamless fusion of digital technology with the real economy emerges as a vital mechanism for promoting environmentally friendly and sustainable enterprise development (X. Chen et al., 2023; Xue et al., 2022).

The genesis of the relationship between digital technology and economic progress can be traced back to the 1980s, marked by the renowned economist Solow’s formulation of the “production paradox of information technology,” which posited that while information technology boasts diverse applications, it fails to enhance productivity (Solow, 1987). However, by 2000, Solow contended that the “Solow Paradox” no longer held. This shift is attributed to the networking, complementarity, and diffusion characteristics inherent in digital technology, which can be seamlessly integrated with production factors like human capital and fixed capital (Andrews et al., 2018; Kauffman & Techatassanasoontorn, 2005). This integration facilitates the widespread dissemination of digital factors across temporal and spatial boundaries at minimal cost, thereby augmenting enterprise productivity (Bharadwaj et al., 2013; Teece, 2018). Consequently, this enhanced productivity translates into reduced energy consumption per unit of output, thereby fostering the green and sustainable development of enterprises. Furthermore, digital technology can serve as a vital component in the production process itself, acting as a production factor. Some scholars contend that a substantial portion of a nation’s productivity growth stems from increased investment in digital technologies, particularly computers, which are integrated into both hardware and software research and development centers (Caselli & Coleman, 2001; Skare & Riberio Soriano, 2021). They argue that such investments have a more pronounced impact on economic growth than any other factor (Matthess & Kunkel, 2020; Zhang et al., 2021). However, other researchers have examined “Solow’s paradox” using the CES production function and have found no significant relationship between the digital economy and economic growth (Irtyshcheva et al., 2021).

Technological progress does not uniformly affect the marginal output of each intermediate input factor. When technological progress accelerates the marginal output of a specific factor, it is termed biased technological progress for that factor (Korinek & Stiglitz, 2020; Markauskas & Baliute, 2021). Acemoglu (2002) posits that technical progress bias refers to the disparity in the growth rates of the marginal output of each factor, with bias favoring the factor experiencing faster growth. Correspondingly, enhanced technical progress denotes the absolute increase in the marginal output of a factor. Presently, scholarly research on technical progress bias predominantly focuses on two aspects. Firstly, scholars endeavor to measure the bias of technological progress, with a prevailing consensus that technological progress exhibits a bias toward capital (Feng et al., 2022; Zhen et al., 2021; Zhu et al., 2021); Research on the economic effects of digital-real integration primarily focuses on income distribution and positive growth (Bai et al., 2020; Lee et al., 2022).

However, existing literature reveals a contentious debate regarding whether digital-real integration fosters green sustainable development for enterprises. The measurement of this integration often overlooks the role of digital technology as a novel factor of production and fails to delve into the asymmetric impact of digital-real integration, specifically, the characteristics of technological progress bias. Consequently, this study seeks to address these gaps by examining the implications of digital-real integration on enterprise green sustainability, taking into account both the technological and factor attributes of digital technology. Hence, the primary objective of this study is to address existing gaps by investigating the impact of digital-real integration on corporate green sustainability. This analysis considers the technological and factorial attributes of digital technology and proposes policy recommendations aimed at mitigating the challenges associated with digital-real integration and green sustainability. Additionally, the study offers a significant Chinese paradigm that can be utilized to advance sustainable development in developing countries.

In terms of marginal contribution, the study makes a dual contribution: (1) From a research perspective, it concurrently considers the technical and factor attributes of digital technology on enterprise green sustainable development. It delves into the repercussions of shifts in the bias of technological progress on enterprise development patterns, thereby enhancing research within the realms of new factors affecting technological progress structure and new technologies influencing green and sustainable enterprise development. (2) From a theoretical perspective, it analyzes how changes in technological progress bias affect enterprise development patterns, which supplements the influence of new factors on the structure of technological progress and the impact of new technology on green sustainable development within enterprises. By furnishing empirical evidence, it advocates for the amalgamation of mathematical modeling with real-world applications to catalyze structural transformations in technological progress and foster green and sustainable enterprise development. Additionally, it offers a model for reference, particularly applicable to developing countries.

Theoretical Analysis and Research Hypothesis

Digital-Real Integration Approach with Nested CES Production Function Modeling

To explore the relationship between digital-real integration and enterprise green sustainable development, it is essential first to establish a suitable theoretical framework that effectively integrates these two concepts into the research paradigm. The crux of digital-real integration lies in the proliferation of digital technologies, including big data and artificial intelligence, within the real sector of the economy. This symbiotic relationship between digital technologies and the real economy engenders a virtuous cycle, fostering the advancement of both domains (Kristoffersen et al., 2020; Sun et al., 2024). Building upon this premise, our study delineates two distinct forms of digital-real integration based on the functionality of digital technologies (refer to Figure 1): factor-based integration and technology-based integration. Factor-based convergence entails the involvement of digital capital as an intermediary factor in production (Zhou & Gao, 2023), where digital capital denotes the capital investment derived from the utilization of digital products within the real sector of the economy (Litvinenko, 2020). Conversely, technological convergence entails the direct utilization of digital technology within the real economy, such as through the Internet and the telecommunications industry (X. Li et al., 2020; Y. Li et al., 2020). Factor-based convergence directly influences the real economy through digital capital, whereas technological convergence indirectly impacts the real economy through skilled and unskilled labor (Dubey et al., 2023; Lau et al., 2022).

Digital-real integration method.

To comprehensively address both factor-based and technological integration, this study draws upon Acemoglu’s (2002) seminal work to develop a two-sector model encompassing production and research and development (R&D). In this model, technology is epitomized by machines deployed in production, with the machines being vented to intermediate producers by a technology monopolist operating within the R&D sector. To ensure consistency in the treatment of labor and capital factors, this study incorporates insights from Havranek et al. (2021) and N. Chen et al. (2022), who categorize labor into skilled and unskilled segments based on educational attainment and differentiate capital into digital and ordinary forms (excluding digital capital). Additionally, this research adopts Sato’s (1967) framework to establish the nested constant elasticity of substitution (CES) production function, as outlined in Equation 1 below. It is important to note that we did not include the four types of production factors—namely, general capital, numerical capital, skilled labor, and unskilled labor—in the same equation when formulating the function. This decision was primarily due to the differences in the elasticity of substitution among these factors, which precludes the use of identical coefficients. Furthermore, in real-world business decision-making, it is common practice to establish the ratios of numerical capital to general capital and skilled labor to unskilled labor initially. This approach is more representative of practical scenarios. After determining these ratios, we subsequently consider the inputs of conformity capital and labor, aligning more closely with actual conditions.

Where

Factor-Based Integration in the Context of Technological Progress Bias

In the context of digital-real integration as a factor-based phenomenon, we introduce ordinary capital (G) and numerical capital (I) as intermediate inputs, with capital K serving as the final output. In this scenario, the production function can be expressed as follows:

Where

Since the market is competitive, profit maximization equations can be derived for ordinary and numerical manufacturers:

Among them, the

It is observable that the demand for machines escalates with the prices of the two factors

The R&D department prioritizes the present value of profits over current profits, leading to the formulation of the net present value of profits as follows:

Where r represents the discount rate and V signifies the present value of profits. In a steady-state economy, where future profits equate to current profits and the discount rate remains constant, V equals 0. Consequently, the net present value of profits can be reduced to:

Hence, Equation 15 provides the ratio of the Net Present Value (NPV) of profits for technology vendors:

When deriving Equation 15 concerning the numerical capital input I, we arrive at the ratio of the NPV of the two profits to the numerical capital input, depicted in Equation 16:

Analysis of Equation 16 reveals that with the escalation of factor-based integration—signifying an increase in the volume of digital capital input—the ratio of NPV profits of technology vendors corresponding to ordinary and digital capital amplifies. Consequently, technology vendors intensify research and development efforts on ordinary capital, thereby reinforcing technological advancements. However, the impact of technological bias remains uncertain. Subsequently, we will incorporate technology-based integration modeling into this framework.

Technology-Based Integration in the Context of Technological Progress Bias

In scenarios where number-reality integration takes the form of technology-based integration, skilled and unskilled labor can be construed as intermediate inputs, with labor denoted as L serving as the final output.

Assume that the skilled labor factor s can use digital technology to produce a segment of the intermediate input U of unskilled labor, and that s stands as the sole source of production for the intermediate input S of skilled labor, we can delineate U into components handled by the unskilled labor factor

There are three types of machines involved here, the first being skilled labor factor s producing skilled labor intermediate inputs used in the production of skilled labor intermediate inputs U, in the amount of

Since markets are competitive, it can be concluded that input producers maximize their profits:

By combining the above equations for each of

The marginal cost of the machine, which is priced by the technology vendor in a manner consistent with the above, yields a profit function for the technology vendor:

And it in turn leads to the following NPV for the technology vendor:

The focus of digital technology applications lies in the replacement of skilled labor with unskilled labor. When comparing the first type of manufacturer with the third type, we can determine the present value of net profit as follows:

By deriving Equation 32 concerning the degree of application of digital technology, denoted as m, we ascertain the effect of m on the ratio of the present value of the two net profits:

From Equation 33, we observe that as the degree of technology-based integration, denoted as the degree of application of digital technology m, increases, the NPV ratio of profits for technology vendors decreases. Consequently, vendors intensify their R&D investment in unskilled labor, thereby promoting technological advancement. However, the impact of technological skewness remains unclear and warrants further verification. This ambiguity stems from the fact that current digital technology primarily enhances the efficiency of repetitive tasks without significantly augmenting creative production activities. Consequently, the R&D endeavors of vendors predominantly target the enhancement of unskilled labor. Furthermore, we intend to conduct additional research on digital-real integration and corporate green sustainability from the perspective of technological progress bias.

Digital-Real Integration and Enterprise Green Sustainable Development Under the Perspective of Technological Progress Bias

Building upon this foundation, we can subsequently incorporate digital-real integration and enterprise green sustainable development into the existing research framework. To encapsulate the integration of digital-real aspects integration and corporate green sustainability from the perspective of technological progress bias, we model the decision-making behavior of technology vendors by augmenting technological progress. This augmentation involves incorporating augmented technological progress with ordinary-type capital into the production function, along with enhanced technological progress of skilled and unskilled labor with ordinary-type capital to the production function

Taking the logarithm of Equation 34 gives:

It may be assumed that

This is obtained by substituting Equation 38 into Equation 37 and simultaneously solving for time:

The same treatment for Equations 35 and 36 can be obtained:

Bringing Equations 40 and 41 to Equation 39 yields:

The green and sustainable development of enterprises is contingent upon the enhanced technological progress of intermediate inputs amidst a constant growth rate of factor inputs. This underscores the notion that investments in digital capital and advancements in digital technology applications can augment the technological progress of ordinary capital and unskilled labor. Consequently, Hypothesis 1 can be formulated as follows:

Hypothesis 1: Both factor-based integration and technology-based integration can contribute significantly to the green and sustainable development of enterprises.

Furthermore, augmented technological progress serves as the intermediary construct for establishing digital-real integration from the perspective of technological progress bias. Here,

And the marginal output of each factor is as follows:

From Equations 43 and 44, it becomes apparent that technology bias is influenced by enhanced technological progress and the elasticity of substitution. Moreover, as derived above, factor-based convergence amplifies the enhanced technological progress of ordinary capital,

Hypothesis 2: Factor-based convergence tends to favor digital capital under the technological progress bias perspective, thereby fostering green and sustainable corporate development.

Hypothesis 3: Under the lens of technological progress bias, technology-based integration inclines toward skill-based labor, thus fostering green and sustainable corporate development.

The research framework of this study encompasses the following (Figure 2):

Main research framework of this study.

Empirical Design and Research Method

Data Sources

The research methodology employed in this study combines both theoretical and empirical analyses. Theoretical analyses are utilized to derive three research hypotheses, which are subsequently tested through empirical analyses to assess the validity of the theoretical framework and the research hypotheses. The empirical data utilized in this study originate primarily from three reputable databases: the China Business Enterprise Registration Database, the CSMAR database, and the Wind database. Specifically, the explanatory variables for this study are sourced from the CSMAR database. Among the core explanatory variables, factor-based integration data are obtained from the Wind database, while technology-based integration data are drawn from the CSMAR database. Additionally, the Technological Progress Bias data are calculated by the authors. The control variable is derived from the China Business Enterprise Registration Database and the CSMAR database. Considering the constraints of data availability, the research focuses on panel data extracted from Chinese A-share listed companies spanning the period from 2000 to 2022. The data undergo several treatments, including the exclusion of ST and ST* companies, elimination of entities with missing key indicators or less than 10 years of observations, supplementation of sparse missing values through linear interpolation, and application of a two-sided 1% shrinkage treatment to mitigate the influence of outliers.

Selection of Variables

Dependent Variable

The dependent variable under scrutiny in this investigation is corporate green sustainable development (Gsd). Gsd is operationally defined as the logarithmic summation of economic, social, and environmental performances, drawing on the conceptualizations presented by Taliento et al. (2019) and Karaman et al. (2020). Herein, economic performance is represented by corporate net profit, social performance by corporate social donations, and environmental performance by the negative of corporate energy consumption.

Core Independent Variables

(1) Factor-based integration (Inv). From the preceding mathematical exposition, it becomes evident that factor-based integration primarily pertains to numerical capital. Following the framework proposed by Brynjolfsson et al. (2002), this study adopts the logarithm of the ratio of the nominal value of shares to fixed assets of listed companies to capture numerical capital values. Building upon this variable, the nominal value of a listed company’s stock can, to a certain extent, reflect the enterprise’s digital capital strength. Generally, a stronger digital capital endowment correlates with a higher nominal stock value. To mitigate the issue of heteroskedasticity in this study, the analysis will employ the logarithm of the ratio of the nominal value of the company’s stock to its fixed assets.

(2) Technology-based Integration (Use): Building upon the theoretical underpinnings elucidated earlier, it becomes apparent that technology-based convergence predominantly revolves around the deployment of digital technologies within enterprises. In this study, we draw upon the works of Lewis and Young (2019) and Wang et al. (2023) to gage this convergence. Specifically, we quantify it by assessing the frequency of pertinent terms within the annual reports of listed companies, encapsulating information related to digital technologies such as Artificial Intelligence (AI), Cloud Computing (CC), Blockchain (BC), big data (BD), and digital technology applications (DT), subsequently taking the logarithm of these word frequencies.

(3) Technological Progress Bias (Bias): As posited by Jiang and León-Ledesma (2018), the outcomes were assessed employing a second-level nested four-factor CES production function, thereby gaging the elasticity of substitution.

Control Variables

Informed by extant literature on the green sustainable development of enterprises (Le, 2022; Shahzad et al., 2021; Xie & Zhu, 2020), and cognizant of the pragmatic sustainable development imperatives faced by enterprises, this study incorporates six control variables into the model. These primarily encompass enterprise size (Size), asset-liability ratio (Lev), total asset turnover ratio (Rou), enterprise innovation ability (Inn), enterprise goodwill (Hou), and environmental regulation (Reg). Among these, firm size is represented as the logarithm of the firm’s total operating income; the gearing ratio is articulated as the proportion of the firm’s total liabilities to total assets; total asset turnover is delineated as the ratio of current assets to total assets; firm innovation capacity is defined as the ratio of R&D investment to the firm’s total costs; firm goodwill is captured as the logarithm of net goodwill; and environmental regulation is expressed as the ratio of the firm’s investment in environmental pollution control to total assets. All descriptive statistics are detailed in Table 1.

Descriptive Statistics.

Building Empirical Models

Drawing upon theoretical underpinnings, this study formulates the following foundational regression model:

Where

To delve deeper into the impact of number-reality integration on the green sustainable transformation of enterprises through technology bias, this study will construct and validate the following mediating effect equations.

Empirical Results and Analysis

Analysis of Baseline Regression Results

This study investigates the impact of digital-real integration on the green sustainable development of enterprises through regression analysis employing Equation 49. Initially, the independent and core dependent variables are regressed individually, followed by the incorporation of control variables and quadratic terms of the explanatory variables. The first three columns of Table 2 present the regression results of factor-based integration (Inv) on corporate green sustainable development (Gsd), while the last three columns depict the regression outcomes of technology-based integration (Use) on Gsd.

Benchmark Regression Results for Digital-Real Integration and Green and Sustainable Development in View of Factor-Based Integration and Technology-Based Integration.

Note. T-statistics are in parentheses and ***, **, indicate 1%, 5% significance levels, respectively.

The regression results reveal a significant positive correlation between Inv and Use on Gsd, evident without the inclusion of control variables, indicating statistical significance at the 1% level and confirming H1. However, the significance of Use shifts after controlling for additional variables, suggesting its impact on Gsd is mitigated by these controls. Subsequently, incorporating the quadratic term into the original equation reveals that the quadratic term of elemental fusion lacks statistical significance. Conversely, Use remains statistically significant, with the coefficient of the primary term being significantly positive and that of the quadratic term being significantly negative. This implies that Inv exhibits a linear positive correlation with Gsd, while Use demonstrates a nonlinear relationship, displaying an inverted U-shaped pattern characterized by an initial rise followed by a decline, in other words, a significant positive relationship exists under specific circumstances; however, once the threshold is surpassed, the relationship shifts to a negative association (D. A. Gao et al., 2024; D. Gao, Zhou, Mo et al., 2024; D. Gao, Zhou, Wan, 2024). This phenomenon may be attributed to the variations in technology-based integration among companies, which can exert heterogeneous effects on digital-real integration and green sustainability. It is frequently observed that a higher degree of technological bias does not necessarily lead to greater benefits, resulting in an inverted U-shaped relationship (D. A. Gao et al., 2024; D. Gao, Zhou, Mo et al., 2024; D. Gao, Zhou, Wan, 2024). In light of our preliminary findings, it becomes evident that the direct integration of digital elements with the real economy, particularly through intermediate goods inputs and production, holds promise in advancing the green and sustainable development goals of enterprises. Conversely, while digital technology boasts efficient and clean attributes absent in traditional technologies, its efficacy remains contingent upon human capital, limiting the potential for increased marginal output. Due to the different research perspectives in this study, this has different conclusions from previous studies by scholars (Sun et al., 2024; X. Yang et al., 2024).

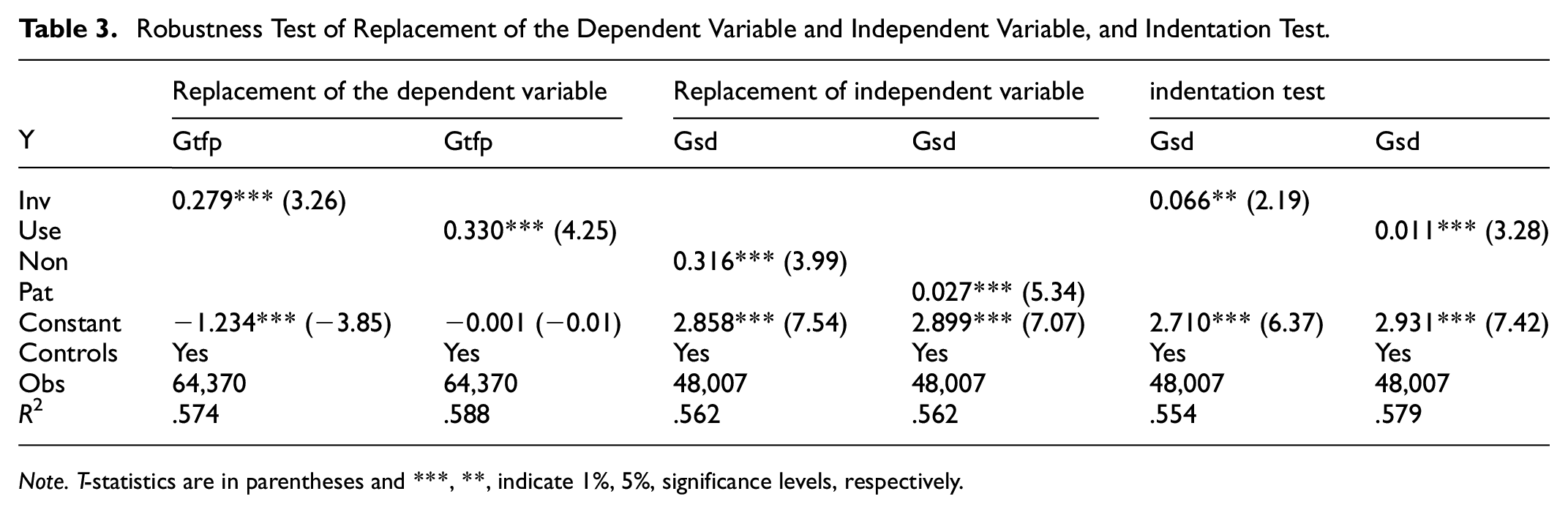

Robustness Tests

Given the potential for errors in measuring explanatory and response variables, which could influence regression results, this study employs several techniques to mitigate their impact. Specifically, we utilize the replacement of the dependent and independent variables, alongside a reduced-tail treatment of data within the 5% quartile to conduct tests. Notably, we substitute enterprise green total factor productivity (Gtfp) for the dependent variable, recognizing its significance as a measure of enterprise green sustainable development. Additionally, we replace elemental fusion with the proportion of intangible assets (Non) and technological fusion with the logarithm of the number of utility model patents granted (Pat). The robustness test results, presented in Table 3 below, indicate that individual coefficients remain significant at the 1% level irrespective of the replacement variable or the reduced-tail test, and the robustness of our findings is corroborated, providing additional support for H1. In other word, Both factor-based integration and technology-based integration can contribute significantly to the green and sustainable development of enterprises.

Robustness Test of Replacement of the Dependent Variable and Independent Variable, and Indentation Test.

Note. T-statistics are in parentheses and ***, **, indicate 1%, 5%, significance levels, respectively.

It is important to note that, although several robustness tests were conducted, the strategies employed to address model specification, measurement error, and omitted variable bias were not sufficiently comprehensive. Therefore, we implemented additional methods, including the incorporation of potential omitted variables, the exclusion of data from the epidemic period, and the substitution of the model, to enhance the robustness and reliability of the underlying regression results. First, regarding potential omitted variables, we draw on the study by Y. Su and Wu (2024) and include firm growth as a potential omitted variable among the control variables. A firm exhibiting stronger growth is likely to have developed a sustainable long-term strategy, while a firm with weaker growth may adopt less sustainable practices. To measure firm growth, we utilize the ratio of the market value of a firm’s assets to its total assets (Tobq). Second, the impact of epidemics can adversely affect firms’ business performance, leading to non-sustainable outcomes. Consequently, we exclude data from the years 2020 to 2022 and retain data from 2000 to 2019 for our robustness tests. Finally, Table 2 presents the results both with and without the addition of control variables, employing fixed-effects models; we also utilize a random-effects model to verify the reliability of the model results. Following further robustness testing outlined in Table 4, we find that after considering the three methods—addressing potential omitted variables, excluding the epidemic effect, and replacing the model—the baseline regression results remain supported. This suggests that our conclusions are robust and provide additional support for the hypotheses.

Robustness Test of Omitted Variables, Impact of the Epidemic and Random Effects Model.

Note. T-statistics are in parentheses and ***, indicate 1%, significance levels, respectively.

Endogeneity Test

Given the necessity to address endogenous causality in empirical analysis, this study employs an instrumental variable approach to mitigate this concern. Specifically, we opt to utilize the lagged first order (L.Inv and L.Use) of independent variables for 2SLS regression. The regression results for the lagged first order of the independent variables are presented in Table 5 below. As shown in Table 5, the p-values for the Endogeneity test of endogenous regressors and the Underidentification test were both .000. The Kleibergen-Paap Wald test statistics (F-values) were 74.17 and 225.64, respectively. Additionally, the Stock-Yogo critical value at the 15% level was 8.96. It is evident that the dependent variable exhibits endogeneity and thus necessitates testing. The selected variables pass both the unidentifiable test and the weak instrumental variable test, thereby affirming the validity of the instrumental variables. Furthermore, the results indicate a positive and significant relationship between the instrumental variables and both the endogenous and dependent variables. It suggests that our underlying conclusions remain robust after addressing the endogeneity test.

Endogeneity Test with Lagged First Order of Independent Variables as Instrumental Variables in View of Factor-Based Integration and Technology-Based Integration.

Note. T-statistics are in parentheses and ***, * indicate 1%, 10% significance levels, respectively.

Moreover, this study incorporates the Bartik instrumental variables method for endogeneity testing. Given that the crux of factor-based convergence lies in the amalgamation of digital capital with the real sector of the economy, and recognizing the role of the post office as a digital infrastructure in the early public sector, which stimulates additional investment in digital capital—a correlate of factor-based convergence (Dubey et al., 2023; Reggi & Gil-Garcia, 2021)—we utilize the national total number of post offices in the year preceding the sample’s time horizon, that is, 1999, as an instrumental variable for factor-based integration (Post). The core concept of technological convergence resides in the application of digital technology within the tangible economic sphere. Hangzhou, being the leading city in China’s digital economy development, has attained a pivotal role in digital technology advancement (Gong et al., 2020; Zhu & Chen, 2022). Consequently, this paper selects the inverse of the spherical distance between the provincial capital city where the enterprise is registered and Hangzhou as a technological convergence instrumental variable (Dist). Moreover, to weigh factor-based integration and technology-based integration, exogenous weights are necessary. Building upon Akerman et al. (2022), this study employs the Internet penetration rate of listed companies as the weight (Internet). This weight is then multiplied by the preceding two instrumental variables to derive two Bartik instrumental variables (Post-Internet and Dist-Internet). The results of the 2SLS regression are presented in Table 6. As observed in Table 6, the p-values for the Endogeneity tests concerning endogenous regressors were .0066 and .0007. The p-value for the Underidentification test was .000, while the Kleibergen-Paap Wald F-values were 23.486 and 66.798. Furthermore, the Stock-Yogo critical value at the 15% level remained at 8.96. We affirm the validity of the instrumental variables, establishing a statistically positive and significant relationship between the instrumental variables and both the endogenous and dependent variables (p < .01). This result further validates the benchmark regression results.

Endogeneity Test of Bartik’s Instrumental Variables Approach.

Note. T-statistics are in parentheses and ***, indicate 1%, significance levels, respectively.

Heterogeneity Test

After the aforementioned empirical investigation, which highlights the positive impact of digital-real integration on fostering green sustainable development within enterprises, it is imperative to acknowledge that each enterprise is influenced by its unique characteristics and policy factors, warranting further exploration. Therefore, this study endeavors to analyze the three dimensions of “cannot integrate,”“not able to integrate,” and “don’t want to integrate.” of real enterprises around digital-real integration.

Enterprises of “Cannot Integrate.”

Due to variations in the enterprise’s internal dynamics and its level of internal control, the digital-real integration realms may not be feasible. Financial constraints pose a significant challenge to enterprises, as allocating more liquidity toward digital-real integration can exacerbate financial strain, potentially leading to bankruptcy due to disruptions in the capital chain. Furthermore, inadequate internal control mechanisms hinder the ability of enterprises to reach consensus on critical decisions, thereby impeding the implementation of digital-real integration strategies. In this study, we operationalize the business status using the current assets ratio (Flo) and quantify the degree of internal control through the internal control index (Con), utilizing their respective mean values as thresholds to delineate heterogeneity. Table 7 examines the heterogeneity among enterprises that “cannot integrate,” revealing that those with poor operational performance and weak internal controls struggle to positively influence sustainable development outcomes.

Heterogeneity Analysis of Enterprises that “Cannot Integrate.”

Note. T-statistics are in parentheses and ***, indicate 1%, significance levels, respectively.

Enterprises of “Not Able to Integrate.”

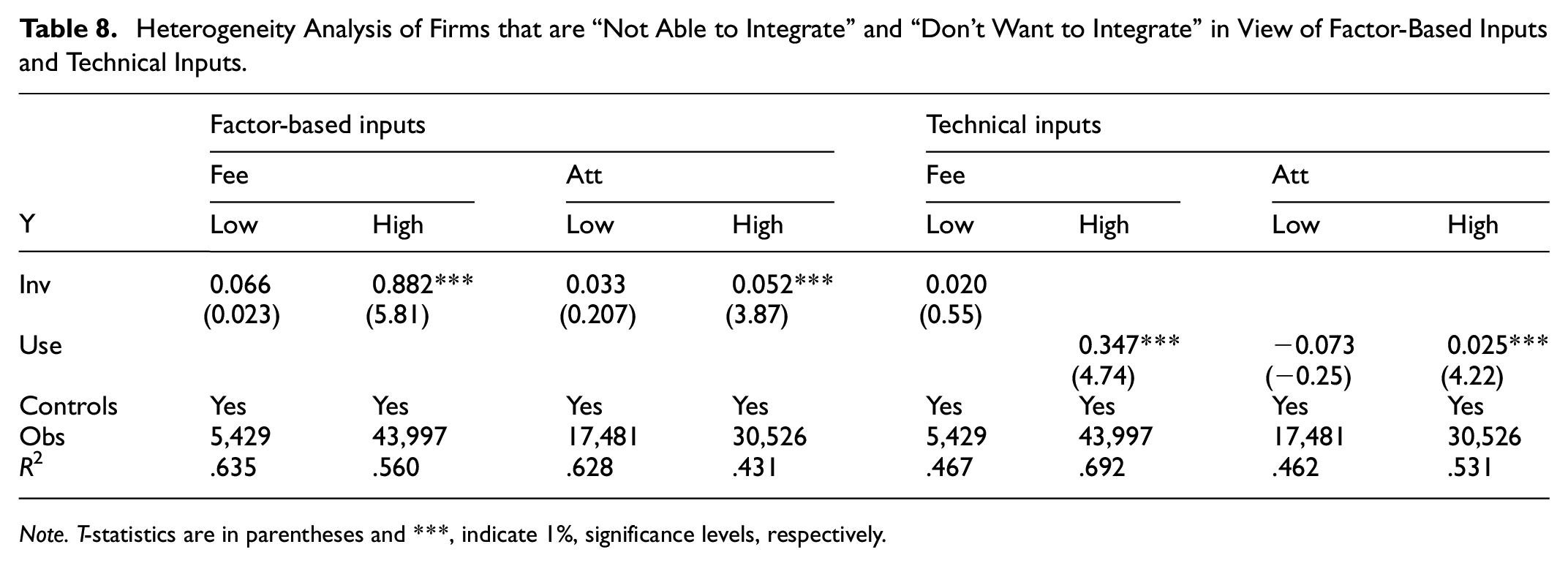

Enterprises frequently encounter challenges in achieving integration due to technological lag. Therefore, this paper employs the R&D expense ratio (Fee) as a metric to gage the extent of integration challenges. Utilizing its mean value as a reference point, Table 8 explores the heterogeneity among enterprises that exhibit reluctance to integrate. It can be found that firms that are “not able to integrate” can hardly have a positive and significant impact on Gsd.

Heterogeneity Analysis of Firms that are “Not Able to Integrate” and “Don’t Want to Integrate” in View of Factor-Based Inputs and Technical Inputs.

Note. T-statistics are in parentheses and ***, indicate 1%, significance levels, respectively.

Companies of “Don’t Want to Integrate.”

For enterprises categorized as “don’t want to integrate,” their ability to positively and significantly influence Green Sustainable Development (GSD) is notably constrained. This study employs adherence to the GRI Sustainability Reporting Guidelines as a criterion to ascertain whether a company falls into the category of “don’t want to integrate.”Table 7 above scrutinizes the heterogeneity among enterprises falling into the “unwilling to integrate” classification, yielding consistent findings with those of companies displaying reluctance toward integration.

Further analysis reveals that the elemental and technological amalgamation inherent in digital-real integration yields a notable and positive impact on the green and sustainable development trajectory of enterprises. This fundamental observation underscores the focal point of this paper on digital technology’s role in enterprise development. Building upon the theoretical framework expounded earlier, the study explores how digital technology engenders asymmetric growth in intermediate inputs, thereby altering marginal output dynamics. By investigating the influence of digital-real integration on technology bias, this study proceeds to examine its implications for green sustainable enterprise development. Empirical testing, as per Equation 50, is conducted, with results presented in Table 8. Integrating the findings from Table 9 with previous regression analyses, it emerges that factor-based integration fosters a bias toward digital capital in technological progress, while technology-centric integration tends to favor skilled labor in technological advancement. The observed outcome aligns with the theoretical framework discussed earlier, attributable to the substitution effect induced by digital factor-based fusion, replacing repetitive mechanical tasks traditionally undertaken by unskilled labor. Moreover, this fusion enhances the efficacy of skilled labor, thereby fostering the advancement of green and sustainable enterprise development. In sum, the validation of Hypotheses 2 and 3 is confirmed.

The Role of Technology Bias in Digital-Real Integration and Sustainable Green Development of Enterprises.

Note. T-statistics are in parentheses and ***, indicate 1%, significance levels, respectively.

To bolster the robustness of this inference, we conducted a two-sided 5% quantile shrinkage test and implemented a variable replacement procedure, substituting the technology-based fusion with the Internet penetration rate of listed enterprises. The resulting test outcomes are detailed in Table 10 below. Factor-based convergence engenders a bias toward digital capital in technological advancement, whereas technology-based convergence exhibits a bias toward labor, thereby bolstering green and sustainable enterprise development and corroborating prior research findings.

Robustness Test of the Further Analysis: Replacement of Core Variables and Indentation Test.

Note. T-statistics are in parentheses and ***, indicate 1%, significance levels, respectively.

Conclusions and Recommendations

Conclusion

The pivotal role played by the integration of digital technology development and the real economy cannot be underestimated. Consequently, this study delves into the impact of factor-based integration and technology-based integration within the digital-real integration paradigm on the green and sustainable development of enterprises, elucidating the phenomenon through the lens of biased technological progress. Furthermore, it endeavors to explore the nuanced role of technological progress bias therein. Henceforth, this study formulates a two-sector four-factor CES production function, incorporating ordinary capital, digital capital, skilled labor, and unskilled labor as intermediate inputs. Theoretical postulations derived from this framework are subsequently substantiated through empirical analysis.

Following this investigation, we can find that: (1) Both factor-based fusion and technological fusion exert positive influences on enterprises’ endeavors toward green and sustainable development. Technological fusion tends to exhibit diminishing marginal efficacy. (2) Heterogeneity analysis exposes various factors impeding enterprises’ integration within the digital and real realms. Such factors include intrinsic business conditions and levels of internal control, rendering certain entities “cannot integrate.” (3) Technological backwardness serves as a deterrent for enterprises categorized as “not able to integrate.” (4) Notably, the absence of reference to the GRI Guidelines for Sustainability Reporting emerges as a significant obstacle for those enterprises disinclined toward integration. (5) Both factor-based integration and technology-based integration precipitate digital-capital-biased technological advancements alongside skill-based labor-biased technological progress. The robustness of these conclusions has been rigorously tested, affirming the veracity and precision of the findings.

Policy Recommendations

Building upon these conclusions, this study forwards three key policy recommendations. (1) There is a call to foster digital-real integration among enterprises, necessitating the design of systems that expedite digital technology innovation and the utilization of digital equipment. This entails enlarging the scope of factor-based and technological integration within the real economy, complemented by appropriate policy incentives and fiscal measures. Enterprises should integrate their digital development strategies into their overarching sustainable development strategies. By implementing digital transformation, they can enhance their levels of green product innovation, green process innovation, and green management innovation. This approach aims to strengthen the enterprises’ green core competitiveness, thereby improving financial performance while simultaneously reducing negative environmental impacts. Ultimately, this strategy seeks to achieve the sustainable development goal of harmonious coexistence between enterprises and the natural environment. (2) Given the asymmetric development spurred by technological progress and the increasing demand for digital capital-biased and labor-biased technological advancements, there is a pressing need to accelerate innovation, strategically plan industrial layouts, and elevate the skill proficiency of the workforce through educational interventions. These efforts aim to propel digital-real integration and bolster the pace of green development within enterprises. The government should enhance the influence of strategic planning on industrial layout, promote green technological innovations among enterprises, and implement cleaner practices in existing areas. Furthermore, it is essential to facilitate the transition of enterprises from crude oil production processes to green product design, the use of environmentally friendly material inputs, and the programing of recycling and disposal strategies. Concurrently, governments must strengthen the protection of property rights and establish a conducive external environment for the market, thereby fostering technological advancement with a bias toward digital capital and labor capital. (3) Numerous enterprises encounter challenges of “cannot integrate,”“not able to integrate,” and “don’t want to integrate” predominantly attributable to poor revenue status and technological backwardness. Consequently, further utilization of tax incentives and fiscal policies is advocated to stimulate corporate revenue enhancement, foster technological advancement, and leverage mandatory environmental regulations to cultivate corporate adherence to sustainability. The government can improve the financial support policy system to incentivize the transformation of polluting enterprises into green enterprises. By integrating environmental risks into the digital economy regulatory system, the fiscal support policy creates a shackle on the financing and financial subsidies obtained by high-polluting enterprises, and guides enterprises to participate in clean production and green projects. At the same time, the system of financial support assessment and evaluation criteria has been improved, and enterprise self-assessment and external supervision have been strengthened.

Limitations and Future Outlook

This study acknowledges several limitations. Firstly, the data sources utilized in this research are primarily the Wind database, the CSMAR database, and the China Business Enterprise Registry database, which encompass data on listed enterprises. Consequently, information pertaining to numerous unlisted enterprises is excluded. Secondly, although our robustness tests reveal certain issues, these do not compromise the validity of the final benchmark regression results.

To address these limitations, future research should enhance the selection of data sources by including a broader sample that encompasses all enterprises, not solely those that are publicly listed. Additionally, a focused examination of micro, small, and medium-sized enterprises (MSMEs) is warranted, as their business activities significantly influence both environmental outcomes and the sustainable development of the economy. Furthermore, employing advanced machine learning techniques, such as Latent Variable Models (LMM), could facilitate more rigorous robustness tests, thereby enabling a more precise identification of causal relationships.

Footnotes

Acknowledgements

The authors would like to thank the reviewers and the editor for their expertise and valuable input.

Ethical Considerations

Not applicable.

Consent to Participate

Not applicable.

Consent to Publication

Not applicable.

Author Contributions/CRediT

All authors contributed to the study’s conception and design. Material preparation, data collection, and analysis were performed by Haonan Chen, Zhi Li and Xiaoning Cui. The first draft of the manuscript was written by Haonan Chen and Xiaoning Cui and all authors commented on previous versions of the manuscript. All authors read and approved the final manuscript.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Data Availability

The data are available from the corresponding author upon reasonable request.