Abstract

This study aims to determine factors that influence Mongolian customers’ intention to use cryptocurrency, which is a virtual currency created by fast-growing technology. For the theoretical framework, the extended Unified Theory of Acceptance and Use of Technology (UTAUT2) along with received risk and financial literacy was used. Data in this study were collected by conducting survey questionnaires from cryptocurrency users of cryptocurrency platforms in Mongolia. Analyzing the data which consists of 720 valid datasets was accomplished by using SmartPLS software. The results of partial least squares structural equation modeling (PLS-SEM) showed that behavioral intention to use cryptocurrency is significantly and positively influenced by performance expectancy, price value, perceived risk, hedonic motivation, and facilitating conditions. In contrast, financial literacy has a significant negative impact on the behavioral intention to use cryptocurrency. The other two variables, effort expectancy and social influence, have no impact on cryptocurrency use. The proposed model explains 59.3% of the total variance in intention to use cryptocurrency among Mongolian customers. The outcomes of our study hold noteworthy implications for policymakers, individual users, and stakeholders within the cryptocurrency domain, as well as researchers engaged in scholarly investigations within this field.

Introduction

In contemporary times, our global society is increasingly intertwined with the fabric of technology. This rapid technological development and achievement have impacted people to adopt and accept the technology. The fast-growing technology has created a new product named cryptocurrency, which is a peer-to-peer virtual cash model that allows users to pay others without any financial institution. Cryptocurrencies, such as Bitcoin and Ethereum, have gained significant attention as a potential alternative to traditional fiat currencies. The decentralized nature of these digital assets allows for transactions to occur without the need for intermediaries, which has the potential to revolutionize the financial industry.

The cryptocurrency market has increasingly expanded over the last few years. As of September 2023, over 23,000 cryptocurrencies are in the transaction. The largest market share being Bitcoin (38.4%), followed by Ethereum and Tether USD. In 2023, there are approximately 420 million cryptocurrency users globally, indicating a 36.88% year-over-year (YoY) increase (Triple-A, 2023). This surge corresponds to a daily average of 400,000 bitcoin transactions. As of May 2023, Asia takes the forefront with 260 million users, showcasing an impressive 100% surge compared to the preceding year’s figure of 130 million. Following closely, North America secures the second position with 54 million users, witnessing a modest increase of 3 million from the previous year’s count of 51 million. Conversely, Africa experiences a 28% decline, seeing a reduction from 53 million to 38 million users. European users also register a decrease, declining from 43 million to 31 million during the same period (Finbold, 2023).

The total value of cryptocurrencies in the world is estimated to be over $3.5 trillion USD. This figure includes the market capitalization of all cryptocurrencies in circulation, such as Bitcoin, Ethereum, Binance Coin, and others in 2023. The first largest cryptocurrency by market capitalization is Bitcoin (BTC), with a market cap of over $1 trillion USD. It was created in 2009 by an anonymous person or group using the pseudonym Satoshi Nakamoto. Second largest cryptocurrency is Ethereum (ETH), with a market cap of over $400 billion USD. It was launched in 2015 and is designed to support smart contracts and decentralized applications. Afterward, Binance Coin (BNB)—with a market cap of over $80 billion USD. Binance Coin is a cryptocurrency created by the Binance exchange. It is used to pay transaction fees on the Binance platform and also serves as a trading pair for other cryptocurrencies. Therefore, Solana (SOL), with a market cap of over $70 billion USD, is a relatively new cryptocurrency that was launched in 2020. It is designed to be a fast and scalable blockchain platform for decentralized applications. Cardano (ADA)—with a market cap of over $60 billion USD, Cardano is a blockchain platform that was launched in 2017. It is designed to be a more secure and sustainable alternative to other blockchain platforms, such as Ethereum.

As a new market, overcoming various challenges, the market value of cryptocurrencies in Mongolia has exceeded ₮380 billion, and crypto exchanges have about 850,000 customers. In the last 24 hr, IHC (IHC) was the highest traded coin, measuring up to 10.3%. In addition, coins such as TRD (TRD) and SPC (SPC) were actively traded (Lemon Press, 2023). The average daily transactions are valued at 410 million MNT. As of September 2023, 41 domestic and 170 international coins and tokens have been registered and there are 12 internal cryptocurrency platforms. The key feature of these exchanges is their 24/7 trading capability and immediacy. One of the most well-known exchanges available to Mongolian investors is Binance, which is a global cryptocurrency exchange that supports trading in a wide range of cryptocurrencies. Although Binance does not have a physical presence in Mongolia, it is available to Mongolian investors through its online platform. Another option for Mongolian investors is BitMax, which is a cryptocurrency exchange that supports variety of cryptocurrency trade, including Bitcoin, Ethereum, and Litecoin. BitMax is registered in the Cayman Islands and has a global presence, but it is available to Mongolian investors through its online platform. There are also plans to launch a new cryptocurrency exchange called Ardex, which is being developed by a Mongolian startup called Ard Holdings. It will reportedly support trading in both fiat and cryptocurrencies. While the cryptocurrency market in Mongolia is still at its developing stage, there are signs of increasing interest and adoption of cryptocurrencies among Mongolian investors and businesses. It will be interesting to see how the market continues to evolve in the coming months and years.

Mongolia currently lacks dedicated regulations for cryptocurrencies. Over the past 5 years, concerns have arisen regarding the legal regulation of cryptocurrencies. According to the Financial Action Task Force (FATF), the legal regulation and development of cryptocurrencies in Mongolia is insufficient, or that key regulatory bodies are making steps to guarantee policy implementation in line with Recommendation 15 (FATF, 2018). Furthermore, the Central Bank of Mongolia stated that cryptocurrency is risky, there is no legal regulation, and it cannot be used for payments. First of all, cryptocurrencies and coins are not money and are not official means of payment. In addition, citizens risk losing all their invested money or becoming a victim of money laundering or fraud. These are not legal means of payment on the territory of Mongolia, and are not related to electronic money defined in the Law on National Payment System and are not allowed. Therefore, regulators have repeatedly warned to be very careful (Central Bank of Mongolia, 2018). In January 2022, the Central Bank of Mongolia issued a statement, warning citizens about the risks associated with investing in cryptocurrency. The statement cautioned that cryptocurrencies are not legal tender in Mongolia, and that investing in them carries a high risk of financial loss. The Bank of Mongolia also emphasized that it does not regulate or supervise cryptocurrency-related activities. Despite these warnings and regulatory gaps, there is a surge in cryptocurrency activities in Mongolia. There are numerous incidents of people losing money in cryptocurrencies due to a low regulation and a lack of financial awareness about cryptocurrencies. The rising incidents of financial losses within the cryptocurrency market underscore the urgency of exploring this research topic, emphasizing the need for enhanced regulatory measures and increased financial awareness to mitigate the associated risks in Mongolia. Nevertheless, there have been ongoing governmental deliberations regarding the potential introduction of cryptocurrency regulations in the future. The Ministry of Electronics, Development, and Communications is actively engaged in developing and implementing a legal framework known as the “Virtual Asset Service Provider” law.

Consequently, this study was undertaken to discern the influencing factors behind cryptocurrency adoption among Mongolian consumers, with a particular emphasis on risk perception and financial literacy. Comprehending user acceptance and adoption of cryptocurrencies becomes paramount, especially for policymakers, industry stakeholders, and researchers’ intent on fostering the utilization of digital assets. The scarcity of research in Mongolia about cryptocurrency adoption further accentuates the need for this study. The existing gap in understanding the dynamics of cryptocurrency adoption by Mongolian customers necessitates investigation, and the formulation of a promising conceptual model to address this gap is crucial for advancing scholarly understanding in this context. In this research, the data was collected using a stratified random sampling method, targeting Mongolian cryptocurrency users across different demographic categories to ensure representativeness. In behavioral studies, particularly those involving the extended Unified Theory of Acceptance and Use of Technology (UTAUT2) model, a larger sample size is advantageous for achieving more precise parameter estimates and better model fit indices.

Academic researchers have increasingly recognized the significance of understanding the intricate factors that influence individuals’ decisions in adopting and utilizing cryptocurrencies. Recent studies, such as those by Li & Wang (2021), highlight the multifaceted nature of these behavioral intentions, emphasizing the role of trust, perceived risk, and technological factors. Investigating these intentions contributes not only to the field of behavioral finance but also informs the development of robust theoretical frameworks that capture the evolving dynamics of the cryptocurrency market. Moreover, as the cryptocurrency landscape continually evolves, the practical implications are substantial. Policymakers, financial institutions, and cryptocurrency developers can leverage insights from behavioral studies to formulate effective regulatory measures, design user-friendly interfaces, and tailor financial products that align with user expectations (Huckle, 2019). This research is crucial in ensuring the sustainable integration of cryptocurrencies into the broader financial ecosystem, offering nuanced perspectives on the motivations and concerns of investors and users in this rapidly changing digital financial landscape.

After this introduction, Section 2 provides theoretical framework, analysis of existing literature on customers behavioral intention to use cryptocurrency and research gap of the study. Section 3 explains variables and how hypotheses are developed, and describes the proposed conceptual model. Section 4 explains the mehodology and scale items of constructs to measure the conceptual model. In Section 5 hypotheses are tested, and Section 6 provides discussion and implications about the behavioral intention to use cryptocurrency. Section 7 and 8 provide limitations and future directions with conclusion.

Literature Review

Cryptocurrencies offer a versatile means of pricing goods and services, enabling seamless cross-border transactions and currency conversions. Cryptocurrencies have grown rapidly and are now popular assets in global financial markets (Bialkowski, 2020; Fangh et al., 2021; Li et al., 2021), attracting media attention, individual investors, institutional investors, and regulators, as well as becoming an important and current topic in several fields of academic research (Angerer et al., 2021).

While numerous studies have delved into the economic and technological aspects of cryptocurrencies, there remains a dearth of research exploring user acceptance and adoption. A crucial economic dimension of cryptocurrencies lies in their potential as a unit of account. Technology plays a pivotal role in facilitating the adoption of cryptocurrencies, providing the essential infrastructure for supporting digital assets. However, it is important to note that the adoption of technology is influenced by an individual’s demographics and personality traits (Tapscott & Tapscott, 2016). Furthermore, technology readiness significantly impacts an individual’s inclination to embrace or reject new technological advancements (Parasuraman, 2000).

Theoretical Framework

The Unified Theory of Acceptance and Use of Technology (UTAUT) and its updated version, UTAUT2, are theoretical models that offer insights into the adoption and utilization of new and emerging technologies. The UTAUT model was initially developed by Venkatesh et al. (2013) with the aim of explaining customer behavior and identifying the factors that influence the adoption of novel technologies and products using the partial least square method. Since its inception, the UTAUT model has found widespread application in various domains, particularly in conjunction with information technology or information systems, to understand technology adoption. In recent years, researchers have directed their attention toward studying the adoption of cryptocurrencies, which represent a novel and rapidly growing technological product. Consequently, the UTAUT model has been employed in investigating the factors influencing cryptocurrency adoption, attracting considerable interest within the research community.

The UTAUT model, proposed by Venkatesh et al. (2003), encompasses four primary constructs: performance expectancy (PE), effort expectancy (EE), social influence (SI), and facilitating conditions (FC). Performance expectancy relates to users’ perception of the technology’s usefulness, where individuals find value in technology that enhances their performance. Effort expectancy denotes the ease of use associated with the technology, as users are more inclined to adopt technology they perceive as user-friendly. Social influence gages the impact of individuals’ social circles, including friends, family, colleagues, and other social groups, on their decision to adopt technology. Facilitating conditions play a crucial role in facilitating consumers’ adoption and utilization of technology, encompassing factors such as the availability of necessary resources, infrastructure, training, and technical assistance.

In a separate study conducted by Jia et al. (2020), the UTAUT model was employed to examine the adoption of mobile payment and cryptocurrency specifically in China using multivariable-adjusted analysis. The findings of the study revealed that the constructs of performance expectancy, effort expectancy, social influence, and facilitating conditions exhibited significant predictive power in relation to the adoption of mobile payment and cryptocurrency within the Chinese context.

The UTAUT2 model, introduced by Venkatesh et al. (2012), serves as an enhanced version of the UTAUT model, aiming to provide further clarity regarding technology acceptance from the customers’ standpoint. UTAUT2 incorporates additional constructs, namely hedonic motivation (HM), price value (PV), and habit (H). Hedonic motivation assesses the level of enjoyment or pleasure derived by users from utilizing the technology. Price value pertains to the perceived value for money associated with the technology, influencing users’ adoption decisions. Habit, on the other hand, reflects the extent to which users have become accustomed to and habituated to using the technology over time. These additional constructs in UTAUT2 contribute to a more comprehensive understanding of technology acceptance and adoption from the customers’ perspective.

In a study conducted by Tsai et al. (2020), the UTAUT2 model was employed to explore the factors influencing the intention to use cryptocurrency among consumers in the United States using logistic regression analysis. The findings of the study revealed that several constructs of the UTAUT2 model, including performance expectancy, effort expectancy, social influence, facilitating conditions, hedonic motivation, and self-efficacy, emerged as significant predictors of the intention to use cryptocurrency. These results highlight the importance of these factors in shaping consumers’ inclination to adopt and utilize cryptocurrency as a form of digital currency.

In the field of studying cryptocurrency adoption, the application of UTAUT and UTAUT2 models has proven to be highly valuable for comprehending the factors that influence the acceptance of this innovative technology. By examining the fundamental constructs of these models, researchers can gain valuable insights into why certain users may be more inclined to adopt cryptocurrencies compared to others. As the usage of cryptocurrencies continues to expand, it is expected that these models will remain essential tools for researchers in this field.

To summarize, the utilization of UTAUT and UTAUT2 models in the investigation of cryptocurrency adoption offers a robust framework for comprehending the factors that shape the acceptance of this emerging technology. Numerous studies have implemented these models and have discovered that factors like performance expectancy, effort expectancy, social influence, and facilitating conditions play significant roles in predicting the intention to use cryptocurrencies. Moving forward, additional research may be needed to explore the applicability of these models to other emerging technologies and to uncover how they can be adapted to different contexts.

Investors or Customers Behavioral Intention to Use Cryptocurrency

Investigating behavioral intentions contributes to the broader field of behavioral finance, offering valuable data on how psychological factors such as perceived risk, trust, and perceived usefulness influence decision-making in the context of cryptocurrency investments (Barberis & Thaler, 2003). Furthermore, as the cryptocurrency market evolves rapidly, comprehending user intentions can inform strategic business decisions for cryptocurrency startups and established financial institutions looking to integrate blockchain technologies. Especially, a nuanced exploration of investors’ and customers’ behavioral intentions toward cryptocurrency usage serves as a foundational step in fostering the sustainable development and integration of cryptocurrencies into the global financial landscape.

In the study conducted by Nadeem et al. (2021), the focus was on understanding the determinants influencing individuals’ intentions to adopt Bitcoin. The research findings emphasize the crucial role-perceived ease of use and utility, both of which exhibit a positive impact on the desire to use Bitcoin. To gather relevant data for this investigation, the researchers employed a survey methodology. Additionally, a preliminary pilot study involving 50 participants was conducted as an initial exploration, laying the groundwork for the subsequent comprehensive investigation. This preliminary phase not only provided valuable insights into factors such as perceived ease of use and utility but also set the stage for a more in-depth examination of individuals’ willingness to adopt and use Bitcoin. Rooted in survey methodology and preliminary pilot research, the study contributes meaningful insights into the key drivers influencing individuals’ intentions regarding Bitcoin adoption.

Another study by Nadeem et al. (2021) studied factors influencing cryptocurrency use including ease of use, perceived userfulness and security. The study involves 385 Chinese respondents. The study’s findings of structural equation modeling (SEM) indicate a positive correlation between the perceived ease of use and perceived usefulness. Notably, the perceived usefulness serves as a mediator in the connection between the perceived ease of use and the intention to use Bitcoin. Additionally, the results underscore the significance of transaction processing and perceived ease of use in influencing perceived usefulness. However, the variables of security and control demonstrate an insignificant impact on perceived usefulness.

Teker and Deniz (2021) investigated the demographics and investment patterns of cryptocurrency users, determining that the majority were within the ages of 25 and 34, most of whom were university graduates. Notably, investors presented a considerable interest in bitcoin foreign currency exchange, fueled by strong profit performance. As a result of factor analysis, the study emphasized the importance of social media outlets as investors’ major source of market information. The study, which included 428 individual investors, provides a statistically robust framework for shining light on crucial facets of the bitcoin ecosystem and its growing dynamics. The study concluded that cryptocurrency market is riskier or more vague than the stock market.

In the study conducted by Pham et al. (2021) highlights two key determinants influencing the inclination to invest in cryptocurrency. The study’s sample consisted of 275 Italian investors, providing a diverse pool for a comprehensive exploration of factors influencing cryptocurrency investment in the Italian context. This study incorporated behavioral factors originating from the theory of planned behavior, as well as variables derived from the financial behavior literature. Analysis revealed that attitude, unlawful attitude, subjective norms, perceived behavioral control, herding behavior, and perceived risk all exert a positive influence on investment intentions. Notably, socio-demographic characteristics and financial literacy do not impact the intention to invest in cryptocurrencies. This study stands as the inaugural examination of the interplay between behavioral and socio-demographic factors in shaping investors’ intentions to engage in cryptocurrency investments.

In their latest investigation Nazim et al. (2021) conducted an examination of the factors influencing the behavioral desire to adopt blockchain technology. Their findings of factor analysis using SPSS software reveal that social influence, enabling conditions, and effort expectation are the primary determinants in this context, with particular emphasis placed on effort expectancy as the most crucial factor. The study derived these insights from a sample of 150 respondents to whom questionnaires were administered, reflecting a meticulous approach to data collection. This research contributes to the understanding of the dynamics surrounding blockchain technology adoption, highlighting the significance of social influence, enabling conditions, and, notably, effort expectancy in shaping individuals’ behavioral inclinations.

Zhao and Zhang (2021) delved into the dynamics of cryptocurrency investment, revealing significant insights. Their findings indicate a favorable association between both investment experience and financial literacy with cryptocurrency investment. Notably, investment experience emerged as the more impactful factor in shaping cryptocurrency investment decisions. The research employed a robust dataset to explore the nuanced relationships between investment experience, financial literacy, and engagement in cryptocurrency investment. This study contributes valuable perspectives to the evolving field of cryptocurrency research, shedding light on the differential influences of investment experience and financial literacy.

Abramova et al. (2021) undertook an in-depth exploration into the security and risk perceptions of crypto-asset users and their consequential impact on crypto wallet decisions and security procedures. The most important outcomes of the research illuminate the existence of diverse attitudes among crypto-asset users concerning security and risk. These individual variations were found to play a pivotal role in shaping decision-making processes related to crypto wallet usage and the adoption of security measures. The study surveyed a substantial sample of 395 crypto-asset consumers, employed a novel approach combining extensive and varied sampling techniques. This methodology enabled a comprehensive analysis, providing valuable insights into the intricate interplay between security perceptions, risk considerations, and the behavioral choices of crypto-asset users. The findings contribute to a nuanced understanding of the factors influencing the security practices and decision-making of individuals engaged in the crypto-asset domain.

In the study conducted by Mahomed (2017), a comprehensive examination was undertaken to understand the factors influencing the adoption of cryptocurrencies, particularly focusing on Bitcoin, within the context of South Africa. The study, based on a sample of 280 participants from South Africa, contributes valuable insights into the complexities of consumer usage patterns and sheds light on strategic considerations for promoting cryptocurrency adoption. The results of structural equation modeling (SEM) suggest that facilitating conditions exert the most significant explanatory impact on the actual usage of cryptocurrency, surpassing behavioral intention. Within the realm of behavioral intention, hedonic motivation emerges as the strongest predictor, followed by perceived trust and social influence. Notably, both effort expectancy and performance expectancy were found to be non-significant, in contrast to the prevailing trends observed in much of the existing literature within related fields.

Research Gap

While numerous studies have extensively examined the economic and technological dimensions of cryptocurrencies, a notable gap persists in the research landscape concerning user acceptance and adoption. In view of the fact that cryptocurrency is a new notion, a few Western experts have made an effort to explain consumer behavior. Cryptocurrency markets are dynamic and influenced by user participation. Analyzing behavioral intentions helps anticipate market trends, enabling investors, policymakers, and industry stakeholders to make informed decisions. The current study tries to contribute to this gap by researching individuals’ behavioral intention to use cryptocurrency.

The lack of extensive research in Mongolia regarding cryptocurrency adoption underscores the significance of this study. The existing knowledge gap concerning the intricacies of cryptocurrency adoption by Mongolian customers calls for exploration, and the development of a robust conceptual model to address this gap is vital for advancing scholarly comprehension in this domain. Our study is the first attempt at investors behavioral intention of cryptocurrency adoption in Mongolia as there are no international research on the financial direction of cryptocurrency, especially people’s behavior intention toward cryptocurrency in Mongolia.

The application of UTAUT and UTAUT2 models in studying cryptocurrency adoption provides a robust framework for understanding the determinants influencing the acceptance of this evolving technology. However, numerous studies employing these models have mainly identified factors of performance expectancy, effort expectancy, social influence, and facilitating conditions as pivotal in predicting the intention to use cryptocurrencies. There is a necessity to extend the model by incorporating additional variables such as risk, trust, security, and financial literacy. To fill this gap, our study sought to enhance the UTAUT2 model by integrating variables of perceived risk and financial literacy. This decision was prompted by the absence of a robust legal environment in Mongolia and the prevalent participation of individuals in the lack of adequate financial knowledge.

Conceptual Model

In keeping with Venkatesh et al. (2003 and 2012), performance expectancy, effort expectancy, social influence, facilitating conditions, hedonic motivation and price value have been considered for examining cryptocurrency adoption by Mongolian customers. The current research does not consider habit due to Mongolian customers not having rich experience in using cryptocurrency. Cryptocurrency has been newly introduced to Mongolian users, which is not enough time for customers to have habitual behavior. To broaden the UTAUT2 model, received risk and financial literacy have been included (Figure 1). In the Mongolian context, the absence of legal frameworks and regulations governing cryptocurrencies, coupled with a surge in financial losses within the cryptocurrency market, underscored the imperative to introduce factors such as received risk and financial literacy.

Proposed conceptual model.

Performance Expectancy

The UTAUT model’s fundamental concept, performance expectancy (PE), measures how users believe that utilizing technology will enhance their performance or make their activities simpler. PE, therefore, represents the user’s view of the technology’s utility. According to Venkatesh et al. (2012), PE was a major factor indicating consumers were more willing to adopt technology if they felt it improved their performance. According to Wu and Wu (2019), PE was a significant predictor of users’ intention to use, indicating that users who thought the technology would improve their performance were more inclined to adopt it. Thus, the following hypothesis is proposed:

H1. Performance expectancy will positively influence Mongolian customers’ intention to use cryptocurrency.

Effort Expectancy

The term “effort expectancy” (EE) describes how easily a technology may be used. In their investigation of the adoption of information technology using the UTAUT, Venkatesh et al. (2003) discovered that EE was a major predictor of users’ desire to use technology. As a result, Hughes et al. (2019) discovered that EE was a major construct of users’ intention to use, indicating that people were more inclined to accept technology if they thought it was simple to use. Several researchers have looked at how effort expectancy affects performance expectancy in relation to the adoption and use of cryptocurrencies. For instance, a study by Tarhini et al. (2021) found that perceived ease of use (effort expectancy) had a significant positive impact on users’ perceived usefulness (performance expectancy) of cryptocurrency. Furthermore, research by Tarhini et al. (2021) demonstrated that effort expectancy also had a significant indirect effect on cryptocurrency adoption through its impact on performance expectancy. Specifically, the authors found that users’ perception of the ease of use of cryptocurrency positively influenced their perception of its usefulness, which in turn, positively influenced their intention to adopt cryptocurrency. Similarly, a study by Lin et al. (2021) found that perceived ease of use was a significant predictor of users’ intention to adopt cryptocurrency. These studies suggest that effort expectancy is a crucial factor in determining users’ perceptions of the usefulness and benefits of cryptocurrency, as well as their intentions to adopt and use it. Therefore, efforts to enhance the ease of use of cryptocurrency platforms and improve user experience could play a vital role in promoting the adoption and use of cryptocurrency. Thus, the following hypotheses are proposed:

H2. Effort expectancy will positively influence Mongolian customers’ intention to use cryptocurrency.

H3. Effort expectancy will positively influence performance expectancy of cryptocurrency use.

Social Influence

Social influence (SI) is the term used to describe social norms and the opinions of others on the adoption of technology. SI measures how much a person is impacted by those around them, including friends, family, coworkers, and other social groups. According to Venkatesh et al. (2003), SI refers to the degree to which an individual perceives that others believe a person should use the new system or technology. Several studies have investigated the influence of social factors on the adoption of cryptocurrency. A study by Xie et al. (2022) used the UTAUT model to investigate the adoption of cryptocurrency among US college students. The study found that social influence had a particularly strong impact on the adoption of cryptocurrency among college students. Similarly, other studies by showed that social influence played an important role in the adoption of cryptocurrency, which found that individuals who were more exposed to information about cryptocurrency through their social networks were more likely to adopt it (Choi et al., 2019; P. Wang et al., 2019; Yan & Bao, 2020; T. Zhou et al., 2019). Thus, the following hypothesis is proposed:

H4. Social influence will positively influence Mongolian customers’ intention to use cryptocurrency.

Facilitating Conditions

Facilitating conditions (FC) is an essential construct of the UTAUT and UTAUT2 models, widely used to explain user’’ technology adoption behavior. These models argue that a key factor in assisting consumer’’ adoption and use of technology is the availability of necessary resources and infrastructure, such as supporting technology, training, and technical assistance. FC play an important role in the adoption of cryptocurrency as they make it easier for users to access and use the technology.

Numerous studies have found a positive association between facilitating conditions and users’ intention to use cryptocurrencies. For example, studies by Atzori (2015) revealed that facilitating conditions were significant predictors of cryptocurrency adoption in various contexts. Facilitating conditions such as ease of use, usability, and infrastructure positively influence the intention to use cryptocurrency. These findings have proved the importance of facilitating conditions in investigating the adoption of cryptocurrency. Thus, the following hypothesis is proposed:

H5. Facilitating conditions positively influence Mongolian customers’ intention to use cryptocurrency.

Hedonic Motivation

Hedonic motivation refers to the emotional or subjective benefits that individuals derive from using a technology. J. H. Lee (2019) found that hedonic motivation was a significant predictor of user’’ intention to use cryptocurrency in South Korea. The study found that users were motivated to use cryptocurrency for entertainment and enjoyment, as well as for the perceived social status associated with owning and using cryptocurrency. Similarly, other studies found that hedonic motivation is a positively significant predictor of user’’ intention to use cryptocurrency (D. Lee & Park, 2021; Wang et al., 2019; Zhou et al., 2019). Therefore, the following hypothesis is proposed:

H6. Hedonic motivation will positively influence Mongolian customers’ intention to use cryptocurrency.

Price Value

The price value of cryptocurrency refers to the exchange rate or market value of a cryptocurrency. Several studies have examined the impact of price value on users’ intention to adopt cryptocurrency. A study by D. Wang et al. (2021) examined the factors that influence users’ intention to use cryptocurrency in Taiwan. The study found that price value was significant predictors of users’ intention to use cryptocurrency. Similarly, other study found that the price value of Bitcoin had a significant positive impact on users’ intention to adopt the cryptocurrency, which revealed the users perceived Bitcoin as a valuable investment opportunity and were motivated to adopt the cryptocurrency due to its potential for high returns (Kshetri & Voas, 2018; Yli-Huumo et al., 2016).

There are several studies that indicated that users were more likely to adopt cryptocurrency when they perceived it as a valuable investment opportunity, and when the price value of the cryptocurrency was increasing (J. Li et al., 2019; Liao et al., 2020; Ma et al., 2020; Mensah et al., 2019; Shin & Shin, 2021; Wang et al., 2019; Yoo & Jang, 2019; Zhang et al., 2019; Q. Zhou et al., 2020). So, the price value of cryptocurrency is an important factor in users’ adoption decisions.

H7. Price value will positively influence Mongolian customers’ intention to use cryptocurrency.

Received Risk

According to Faqih (2016), received risk (RR) is the uncertainty of using or buying a product. Several studies found that perceived risk is a significant factor in users’ intention to adopt the technology. Alalwan et al. (2018) found that perceived risk was a significant predictor of users’ behavioral intention to adopt mobile banking. A review by Liao et al. (2020) focused specifically on studies that used UTAUT2 to investigate the adoption of cryptocurrency exchanges. The review found that perceived risk was a significant predictor of users’ intention to use cryptocurrency exchanges. X. Li and Wang (2021) conducted a literature review on factors affecting cryptocurrency adoption using the UTAUT2 model. The review included studies that investigated the role of perceived risk in the adoption of cryptocurrencies. The authors identified 17 studies that met their inclusion criteria and found that perceived risk was consistently identified as a significant factor influencing cryptocurrency adoption. Users’ intention to use cryptocurrencies was significantly negatively impacted by received risk, demonstrating that greater levels of received risk are associated with decreased intention to use cryptocurrency. Therefore, there is no specific regulation for cryptocurrency in Mongolia and cryptocurrency is warned as a risky investment by the Bank of Mongolia. Thus, it is necessary to involve risk in this study. Thus, the following hypotheses are proposed:

H8. Received risk will negatively influence Mongolian customers’ intention to use cryptocurrency.

H9. Received risk will negatively influence performance expectancy of cryptocurrency use.

Financial Literacy

As financial literacy is an important skill for better financial decisions and using technology, it was selected as an influencing factor. Hastings (2013) found that experience and knowledge of technology had a significant positive effect on users’ intentions to adopt and use cryptocurrency. The authors suggest that users’ experience and knowledge of technology could contribute to a greater understanding of the benefits and risks of cryptocurrency and increase their confidence in using it. Jung et al. (2019) studied the factors affecting the adoption of cryptocurrency using the UTAUT2 model. The study found that financial literacy was a significant predictor of users’ intention to adopt cryptocurrency, along with other UTAUT2 factors such as performance expectancy and social influence. Hsieh and Li (2020) investigated the factors influencing the intention to use cryptocurrencies as a payment method using the UTAUT2 model. The study found that financial literacy had a positive effect on users’ intention to use cryptocurrencies. Based on these findings, the following hypothesis is proposed:

H10. Financial literacy will positively influence Mongolian customers’ intention to use cryptocurrency.

Methodology

Sampling Methodology

In order to collect data to examine the conceptual model, prepared questionnaires were given to Mongolian customers. It is important to mention that our questionnaires have reached all cryptocurrency platforms’ users and 720 valid questionnaires were completed by Mongolian customers. Although there are many methods for choosing the optimal sample size, the most widely used in practice, the basic assumption of sampling is to assume that the original population is normally distributed, and the sample size is selected by simple random sampling that the formula is shown in Equation 1.

Where,

The determination of an optimal sample size through the sampling procedure yielded a figure of 385. In the course of our study, a total of 720 valid responses were collected, thereby indicating a level of data sufficiency commensurate with the research requirements.

To further validate the optimal sample size, we also calculated the sample size using the following formula. The sample size of 720 respondents was selected based on several statistical principles and widely accepted guidelines for determining adequate sample size in behavioral research.

A common formula for determining sample size in quantitative research is based on Cochran’s formula for large populations:

where,

✓

✓

✓

✓

The Cochran formula for infinite populations was initially used to calculate the required sample size for large populations. However, given that the number of cryptocurrency users in Mongolia is finite and highly concentrated in Ulaanbaatar, this formula was adjusted with the finite population correction to yield a more precise sample size.

Given the lack of prior studies that accurately estimate the proportion of Mongolian customers with the intention to use cryptocurrency, we utilized

Our calculation indicates that a minimum of 385 respondents would suffice for a representative sample. Although, to ensure higher reliability and mitigate potential non-response biases, we chose to collect data from 720 respondents, which also adheres to the widely accepted statistical guideline of ensuring at least 10 respondents per variable for structural equation modeling (SEM), as recommended by Kline (2015).

Furthermore, Hair et al. (2010) recommends a sample size ranging between 200 and 400 for structural equation modeling (SEM) analysis. However, since cryptocurrency adoption involves a variety of constructs and behavioral factors, we chose a larger sample size to increase the power of the analysis and ensure that the results remain valid across different population subgroups.

Measurement Scale and Statistical Method

In this study, we used a five-point Likert scale, a common tool in quantitative research. This scale allows participants to express their agreement or disagreement effectively. It’s valued for normalizing responses and reducing the impact of extreme answers, which is crucial in behavioral finance research. Responses are recorded on a scale of 1 to 5, with “1” indicating “strongly disagree” and “5” indicating “strongly agree,” offering a clear and structured way for participants to convey their attitudes and opinions. This ensures comprehensive and precise data collection.

To analyze cryptocurrency adoption, we used the partial least squares structural equation modeling (PLS-SEM) technique which is mainly used among researchers on this topic. PLS-SEM is a holistic modeling approach that empowers researchers to assess the interconnections among variables and assess the validity and reliability of any research framework (Hair, 1998). As recommended by Hair et al. (2021) and Nitzl and Chin (2017), in this study we applied simplified variance-based SEM approach (PLS) because of the following reasons:

- PLS exhibits flexibility in its approach, imposing minimal constraints on measurement scales, sample size, and the distribution of residuals.

- In PLS analysis, the assumption of complete independence among variables is not required, thereby enhancing the reliability of the results.

- PLS demonstrates robustness when dealing with data skewness and the omission of an independent variable.

Furthermore, PLS-SEM was chosen as the primary statistical method for data analysis due to its flexibility and ability to handle complex models involving latent variables, as is the case in this study. According to Hair et al. (2019), PLS-SEM is particularly advantageous when the research model is predictive and the objective is to maximize the explained variance of dependent variables, which aligns with our study’s aim of predicting cryptocurrency adoption. This method was selected over covariance-based SEM (CB-SEM) due to its ability to work effectively with smaller sample sizes and non-normal data distributions (Chin, 1998; Hair et al., 2019).

PLS-SEM also allows for the simultaneous estimation of both the measurement model (i.e., the relationships between observed variables and their underlying constructs) and the structural model (i.e., the relationships between the constructs themselves; Hair et al., 2017). This dual focus enables us to assess the reliability and validity of the constructs used in the extended UTAUT2 model while also testing the hypothesized relationships between variables such as performance expectancy, perceived risk, and behavioral intention.

Given that our study represents one of the early investigations in the field of cryptocurrency use among Mongolian customers, we opted to employ partial least squares structural equation modeling (PLS-SEM). PLS-SEM was chosen for its capacity to directly create independent latent variables through cross-products involving the response variables. Hair et al. (2014) have advocated for the use of PLS path modeling in the initial stages of theoretical development to assess and validate exploratory models.

As shown in Table 1, 28 scale items have been used in the current study to measure the constructs in our model. The main constructs of UTAUT2 (PE, EE, SI, FC, HM, PV, and BI) were measured by the same items used by (Venkatesh et al., 2012). Received Risk (RR) was measured by the three items taken from (Faqih, 2016). Financial literacy was measured by the two items taken from (Hastings, 2013).

Constructs.

From this investigation, the reliability and validity of the constructs were thoroughly examined using a range of statistical tests, ensuring that the measurement model is robust and capable of producing reliable results (Table 2). Specifically, the following measures were employed to assess the strength of the model:

✓

✓

✓

✓

✓

✓

Explanation of the Tests Used in the Research, Formulas, and Evaluation Criteria.

Source. Author estimates.

In addition to these fit measures, the following reliability and validity indicators were used to strengthen the assessment of the measurement model:

✓

✓

✓

✓

✓

✓

Results

Respondents’ Profile and Characteristics

As shown in Table 3, 40% of participants were male, and the rest were female. In case of the age group, it was noticed that the age group up to 25 captured the largest percentage of the total sample (83%). With reference to the monthly income level, the majority of the respondents (56%) had a monthly income level up 500,000 MNT, followed by those (20%) who had a monthly income ranging from 1 to 2 million MNT. Therefore, most of the respondents have a Bachelor degree (92%).

Consumer Profile.

Source. Author estimates.

Normality

A skewness-kurtosis approach was adopted to test univariate normality for each variable (Byrne et al., 2010). The statistical values of skewness and kurtosis describe the shape of distribution of data. Skewness measures the degree of asymmetry in the distribution and kurtosis measures the degree of peakedness or flatness of a distribution. As shown in Table 4, all values support the normality: skewness below cut-off point 3, and kurtosis below cut-off point 8 (Kline, 2005).

Assessment of Normality.

Source. Author estimates.

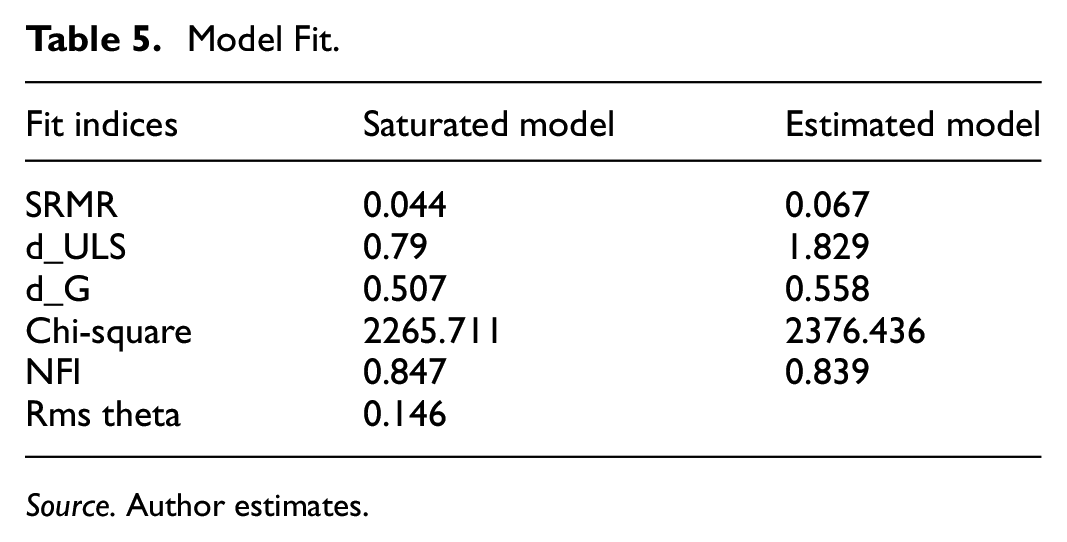

Model Fit

Using SmartPLS 3, the main fit indices including SRMS, d_ULS, d_G, Chi-square, NFI, and Rms Theta have all been tested to evaluate the model fit. As shown in Table 5, fitness indices have adequate goodness of fit to the data (Byrne et al., 2010; Hair et al., 2012).

Model Fit.

Source. Author estimates.

It is important to note that the appropriate threshold for a “good” RMS Theta may vary depending on the specific research context and the number of indicators used. As a general guideline, an RMS Theta value of 0.3 or less is often considered acceptable.

Structural Model Assessment

In our model assessment, we conducted a thorough evaluation of several key indicators to ensure the robustness of our research framework. These indicators included item loadings (Loading), average variance extracted (AVE), Cronbach’s alpha, rho_A, composite reliability (CR), Variance Inflation Factors (VIFs), and Cross loadings as summarized in Tables 6, 7.

Validity, Reliability and Multicollinearity.

Source. Author estimates.

Cross-Loadings for the Measurement Model.

Source. Author estimates.

Firstly, we examined the item loadings, and our results revealed that all indicator loadings exceeded the recommended threshold of 0.7. This observation signifies that our model demonstrated strong internal consistency, as advocated by Gefen et al. (2000). The consistently high values of the indicator loadings reflect the reliability and coherence of the latent constructs within our research framework.

Secondly, we assessed the AVE for all items, and we found that they consistently surpassed the widely accepted threshold of 0.5. This achievement supports the notion of convergent reliability, in line with the criteria proposed by Bagozzi et al. (1998), Fornell and Larcker (1981). The high AVE values indicate that a substantial proportion of the variance in our constructs is explained by their respective indicators, further reinforcing the robustness of our measurement model.

Furthermore, to evaluate the internal consistency of our construct measures, we employed Cronbach’s alpha, for which the recommended threshold is .7. Our results confirmed that all constructs met this criterion, underlining the reliability of our measurement instruments, as recommended by Hair et al. (2012).

Subsequently, we investigated composite reliability (CR) to assess internal consistency. Our findings revealed that all constructs exceeded the threshold of 0.7, aligning with Hair et al. (2012) recommendation. The high CR values reinforce the reliability and consistency of our measurement model.

Additionally, Rho_A measures the internal consistency or reliability of a measurement scale or construct, which is an essential aspect of assessing the validity of research measures, which ranges from 0 to 1, with higher values indicating greater internal consistency or reliability of the measurement scale or construct (Hair et al., 2012).

Moreover, we examined VIFs and found that all items met the acceptable value of less than 10, indicating acceptable level of multicollinearity (Kutner et al., 2005; O’brien, 2007).

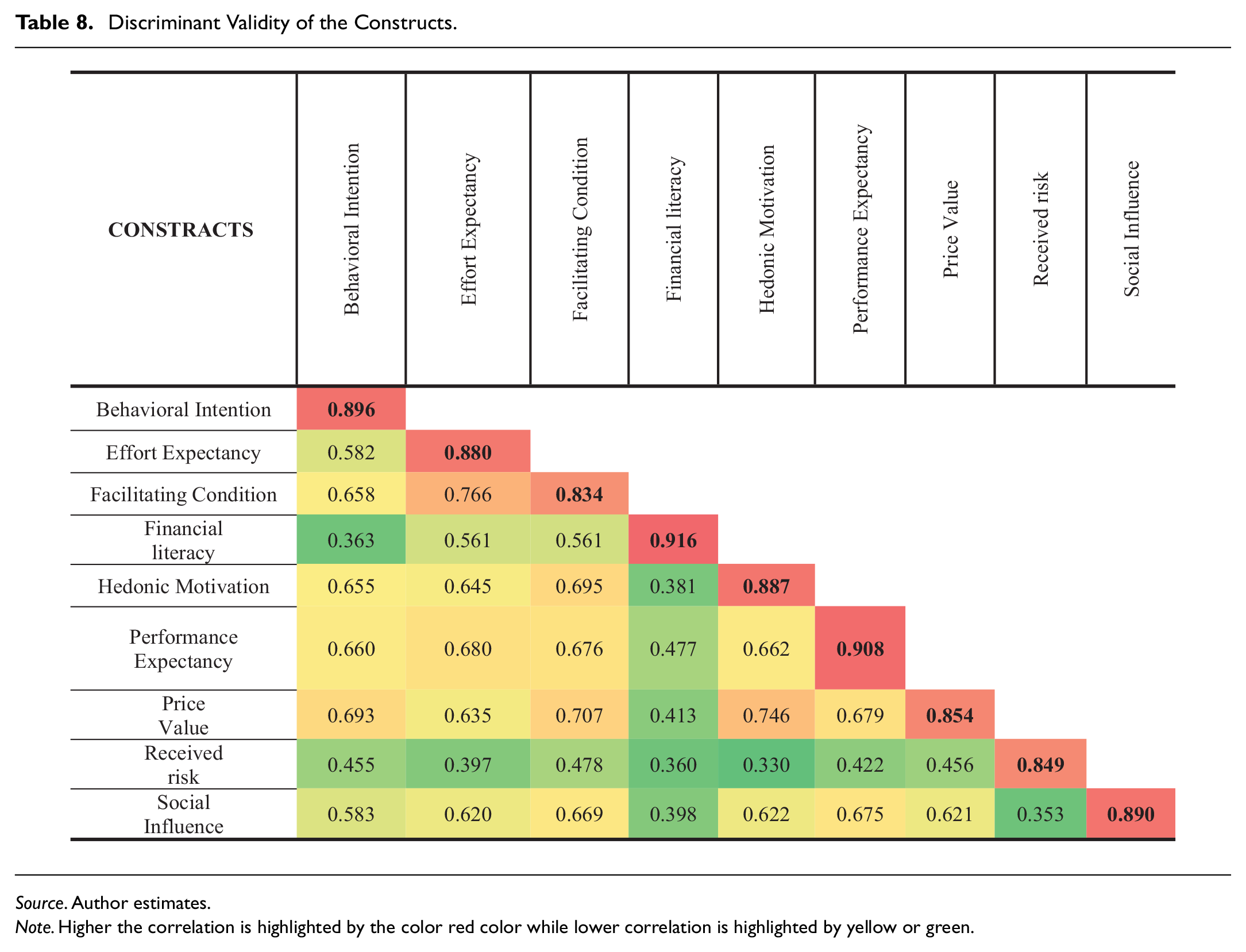

Then we tested discriminant validity using the Fornell and Larcker (1981) to determine whether the variable’s measures differed from other variables. The diagonals are the square root of the AVE of the latent variables and indicate the highest in any column or row. It indicates that there is discriminant validity (Table 8). These results collectively affirm the adequacy of validity in our research. In summary, the measurement model demonstrates adequate reliability, convergent validity, and discriminant validity.

Discriminant Validity of the Constructs.

Source. Author estimates.

Note. Higher the correlation is highlighted by the color red color while lower correlation is highlighted by yellow or green.

Our comprehensive model assessment, which considered a range of criteria, demonstrates the internal consistency, reliability, and convergent validity of our research framework. These findings affirm the robustness of our measurement model and provide confidence in the soundness of our study.

Then R2 was used for goodness of model fit, and in our model 59.3% for cryptocurrency use, and 48.9% for performance expectancy. It is important to note that the main constructs of UTAUT2 without received risk and financial literacy were able to predict about 58.2% of variance in cryptocurrency use. Therefore, structural models which include received risk and financial literacy have more power to explain the behavioral intention to use cryptocurrency.

Afterward, bootstrapping analysis was managed to determine the significance of coefficients (Table 9). As a result, cryptocurrency use significantly predicted by UTAUT2 factors: performance expectancy (

Path Coefficient and Their Significance.

Source. Author estimates.

, **, * represent 1%, 5%, 10% significantly level, respectively.

Discussion and Implications

The rapid advancement of technology has given rise to the revolutionary concept of cryptocurrencies—peer-to-peer virtual cash models that operate independently of financial institutions. Bitcoin and Ethereum, among thousands of others, have emerged as potential alternatives to traditional fiat currencies, garnering substantial attention in the financial landscape. The growth of the cryptocurrency market has been nothing short of remarkable, with over 23,000 cryptocurrencies in circulation by September 2023. Bitcoin, as the frontrunner, holds the largest market share, followed closely by Ethereum and Tether USD. The soaring popularity of cryptocurrencies is evidenced by the staggering number of users worldwide, reaching approximately 420 million by 2023, engaging in a massive 400,000 bitcoin transactions daily. In Mongolia, cryptocurrency is at early stage of implementation and customers are interested in this digital asset because of its potential opportunity to earn profit and transfer money. There is no law of cryptocurrency and the Bank of Mongolia issued a statement, warning citizens about the risks associated with investing in cryptocurrency. Therefore, studying the factors influencing cryptocurrency adoption provides valuable insights into the evolving landscape of digital finance, enabling stakeholders to navigate the challenges and seize the opportunities presented by this transformative technology.

The study focused on investigating the factors influencing the behavioral intention to use cryptocurrency among Mongolian customers. Given the limited research in the Mongolian context, the study utilized an extended version of the Unified Theory of Acceptance and Use of Technology 2 (UTAUT2) as the theoretical foundation, incorporating received risk and financial literacy. The proposed model accounted for 59.3% of the variance in Mongolian customers’ intention to use cryptocurrency. As cryptocurrency adoption is relatively new in the country, and customers have not had sufficient experience to develop habitual behavior, we did not consider the habit construct. Ten hypotheses were introduced to consider the various factors that may shape Mongolian customers’ inclination to adopt and utilize cryptocurrency.

The study’s findings reveal that the price value of cryptocurrencies exerts a significant influence on the intention of Mongolian customers to utilize them. As the exchange rate and market value of cryptocurrencies increase, customers in Mongolia are more inclined to adopt them as valuable digital assets. This trend is driven by the allure of high returns and the rising price value of cryptocurrencies, aligning with prior research conducted by D. Wang et al. (2021) and Q. Zhou et al. (2020). The result is also consistent with Yli-Huumo et al. (2016), Kshetri and Voas (2018), Liao et al. (2020), Shin et al. (2011), and Zhang et al. (2019). Mongolian users exhibit enthusiasm for engaging in the cryptocurrency market due to the potential to generate quick profits.

The survey results affirm the positive impact of performance expectancy on Mongolian customers’ intention to use cryptocurrencies, which is supported by prior studies (Venkatesh et al., 2012; Wu & Wu, 2019). As stated by Venkatesh et al. (2012), Performance Expectancy (PE) emerged as a significant determinant, suggesting that consumers were more inclined to adopt technology when they perceived it to enhance their overall performance. Mongolian individuals are drawn to cryptocurrencies due to their perceived ability to enhance performance and simplify various activities. It indicates that Mongolian customers may perceive digital assets as an opportunity to streamline financial activities, manage assets, and earn profits, which increases their intention to use cryptocurrency.

Moreover, our result shows that received risk positively influences performance expectancy, as well as behavioral intention. This implies that Mongolian customers are willing to invest in cryptocurrencies despite the potential financial risks, solely driven by the pursuit of profits through buying and selling these digital assets. This aspect warrants careful attention from policymakers and regulatory institutions. This discovery stands in contrast to previous studies (Abramova et al., 2021; Barberis & Thaler, 2003; Jiang et al., 2021; Liao et al., 2020; Tarhini et al., 2021; Teker & Deniz, 2021) leading us to posit that Mongolian customers engage in cryptocurrency investments due to their inherent curiosity. Furthermore, their inclination toward cryptocurrency adoption is shaped by their relatively limited financial knowledge concerning risk, combined with a predisposition for risk-taking behavior. This unique result might be explained by the socio-economic context of Mongolia, where individuals may have fewer investment opportunities and view cryptocurrency as a lucrative, albeit risky, alternative. This finding supports the assertion by Tarhini et al. (2021) that consumers in certain markets may accept higher risk levels when the anticipated rewards are perceived to outweigh the risks. Thus, Mongolian customers are not concerned about risk while they participate in the cryptocurrency market. As a result, the risk warning statement issued by the Bank of Mongolia may not effectively influence their decision-making. Policymakers should prioritize understanding the behavior of cryptocurrency users and tailor their policies based on the actual risk perception these users exhibit.

Interestingly, the study reveals a negative association between financial literacy and the intention of Mongolian customers to use cryptocurrencies. Individuals with lower financial literacy are more likely to adopt and utilize cryptocurrencies. The findings indicate that Mongolian customers exhibit a common inclination toward using cryptocurrencies primarily as a means to pursue profit, regardless of their level of financial knowledge. This prevailing tendency represents a risky decision-making pattern, which may potentially lead to substantial financial losses in the future. This result contrasts with the outcomes of prior studies by Hastings (2013), Jung et al. (2019), Hsieh and Li (2020), where higher financial literacy typically led to more cautious and informed investment decisions.

This negative association may be explained by the speculative nature of cryptocurrency investments. Less financially literate individuals may be more drawn to the allure of quick profits and may not fully understand the associated risks, leading them to invest more impulsively. This pattern presents a potential risk for policymakers, as a lack of financial literacy could lead to ill-informed decision-making and financial losses for many users. The result suggests that educational initiatives around financial literacy should be a priority in Mongolia, especially in the context of cryptocurrency adoption.

In addition, the provision of facilitating conditions, such as access to smartphones, apps, computers, internet, 4G, and 5G services, has a positive impact on Mongolian customers’ intention to use cryptocurrencies. Notably, the young demographic, representing approximately 70% of the Mongolian population, exhibits a higher inclination toward adopting technology, innovation, and the internet of things. The result is consistent with Mahomed (2017) and Atzori (2015).

Consequently, hedonic motivation plays a crucial role in influencing Mongolian customers to embrace cryptocurrencies, as they are drawn to the entertainment and joy associated with these digital assets, which is supported by prior studies (J. H. Lee, 2019; D. Lee & Park, 2021; Mahomed, 2017; Wang et al., 2019; Q. Zhou et al., 2020).

The survey results revealed that both effort expectancy and social influence do not have a significant direct impact on the behavioral intention of Mongolian customers to use cryptocurrencies. The reasonable level of smartphone and internet penetration in Mongolia can be seen as a contributing factor to the ease of cryptocurrency adoption among the Mongolian customers. This suggests that this demographic faces no significant challenges in utilizing cryptocurrencies, indicating the removal of barriers that may have hindered adoption in the past. These findings align with previous research, which posited that as technologies mature, users tend to take such services for granted, leading to minimal effort required for their use (Venkatesh et al., 2003). It posited that as technology becomes more familiar and integrated into daily life, users require less effort to adopt it. The relatively high level of smartphone and internet penetration in Mongolia likely reduces any perceived complexity in using cryptocurrency, thus diminishing the impact of effort expectancy on behavioral intention. This result suggests that Mongolian customers do not find the effort required to use cryptocurrency to be a significant barrier, nor are they strongly influenced by the opinions of their social circles when deciding whether to adopt cryptocurrency. Similarly, the minimal effect of social influence suggests that Mongolian customers are more individualistic in their decision-making process regarding cryptocurrency usage, relying less on external pressures from family, friends, or influencers. This stands in contrast to studies in other regions, where social networks significantly influence cryptocurrency adoption (e.g., Nazim et al., 2021). It reflects a growing trend of self-directed financial decision-making among Mongolian users, particularly in a nascent market like cryptocurrency, where personal exploration may play a more prominent role.

Effort expectancy has a positive indirect impact on the intention to use cryptocurrencies via performance expectancy. This suggests that if Mongolian customers feel that it is simple to use cryptocurrencies, they will perceive them as useful and beneficial. The statistical findings from our study indicate that the impact of effort expectancy on intention to use cryptocurrencies is fully mediated by the performance expectancy. This can be attributed to the reduced effort needed to comprehend and employ cryptocurrencies. Consequently, these factors may elevate the expectations of Mongolian individuals regarding the potential benefits and overall effectiveness of adopting cryptocurrencies. This result is consistent with the prior study by Tarhini et al. (2021), who found that effort expectancy had a significant indirect effect on cryptocurrency adoption through its impact on performance expectancy.

Prior studies by Nazim et al. (2021), Mahomed (2017), Venkatesh et al. (2003), Xie et al. (2022), Yan and Bao (2020), Choi et al. (2019), Zhou et al. (2019), Wang et al. (2019) revealed that individuals who were more exposed to information about cryptocurrency through their social networks were more likely to adopt it. However, in our study, social groups such as families, workmates, friends, and social influencers do not play a significant role in influencing their decision to use cryptocurrencies. These findings indicate that Mongolian individuals tend to be self-oriented decision-makers, relying less on external influences when making decisions about cryptocurrency usage.

In this study, the inclusion of received risk and financial literacy in the structural model enhances its explanatory power for the behavioral intention to use cryptocurrency was proven by the R2 coefficient used to assess the goodness of fit for the model, with 59.3% of the variance in cryptocurrency use. The main constructs of the UTAUT2 model, without considering received risk and financial literacy, were able to predict approximately 58.2% of the variance in cryptocurrency use. As a result, this research makes a valuable contribution to the existing literature by extending the application of the UTAUT2 model within the context of a developing country, Mongolia. The study offers substantial insights and implications for policymakers and regulatory bodies in formulating appropriate policies and legal frameworks concerning cryptocurrencies. Moreover, cryptocurrency platforms stand to benefit from our findings, as they can utilize the understanding of consumer behavior provided by this study to shape their strategic approaches effectively.

Limitations and Future Research Directions

Although this study has found some important results over the area of behavioral intention to use cryptocurrency, it is restricted by the number of limitations.

The primary research method employed in this paper was a survey questionnaire. While surveys are valuable for collecting quantitative data and capturing a broad range of perspectives, it’s essential to recognize that they have their limitations. To enhance the depth and breadth of understanding, future research can benefit from incorporating alternative research methods, such as interviews, case studies, and experimental research. Interviews offer a qualitative approach to data collection, allowing researchers to engage in direct conversations with participants. This method can yield rich insights and in-depth understanding, which may uncover nuances and perspectives not easily captured through surveys alone. Case studies are particularly useful when the aim is to explore complex, real-world scenarios in detail. Researchers can select specific cases or examples related to the research question and thoroughly analyze them. On the other hand, experimental research involves controlled settings and manipulation of variables to establish cause-and-effect relationships. While it may require more resources and planning, experimental research can provide robust evidence for causal relationships within the research domain. By integrating these alternative research methods, researchers can enrich their investigations, ensuring a more comprehensive and multifaceted exploration of the research topic. Each method brings its own strengths and can help mitigate the limitations of any single approach. The sequential use of multiple research methods can enhance the validity and reliability of the findings.

Moreover, it’s important to note that this study exclusively focuses on cryptocurrency users in Mongolia. The findings might vary if the survey had a broader geographical scope or if comparisons were made with users in other developing nations. As Exton and Doidge (2018) have shown, perceptions can differ significantly based on the country of study. Therefore, future research should encompass a more diverse range of countries to capture a broader perspective on cryptocurrency use and perceptions.

Additionally, the largest segment of the respondents in the current study was young, had a lower and middle income, and had bachelor’s and below education level. Thus, the future studies ought to involve other segments of the population of Mongolia. To increase and ensure a more diverse demographic representation, a stratified sampling method can be used in the future studies, by dividing the population into subgroups and then randomly selecting participants from each subgroup.

Furthermore, the results of this study are based on the cross-sectional data, longitudinal study could provide more understanding regarding the topic. As we mentioned before, habit is excluded from the model. Once the Mongolian customers get used to cryptocurrency in their daily lives, it becomes possible to include the habit as one of the constructs for future studies. The inclusion of the “habit” variable is crucial in understanding behavioral intention to use cryptocurrency for several reasons. Habit represents repetitive, automatic behaviors developed through past experiences, and its incorporation into the model can provide a more comprehensive understanding of user behavior. In the context of cryptocurrency usage, habitual actions may significantly influence individuals to continue engaging with these digital assets, even in the absence of conscious decision-making. By accounting for habit, researchers can capture the inertia that individuals may experience in their cryptocurrency-related activities, offering insights into the sustained use of these financial technologies.

Recommendations for Future Research and Practice

The negative relationship between financial literacy and the intention to use cryptocurrency suggests a need for targeted educational programs. These initiatives should aim to increase awareness about the risks associated with cryptocurrency investments and provide consumers with the knowledge to make informed decisions. Policymakers and financial institutions should collaborate to design financial literacy programs that cater to the unique characteristics of cryptocurrency.

With cryptocurrency adoption growing in Mongolia, it is essential that regulatory bodies develop clear and robust legal frameworks to protect consumers from fraud and other risks. The findings that Mongolian users are willing to take financial risks despite warnings from the Bank of Mongolia indicate that stronger regulations are necessary to safeguard consumers without stifling innovation. In doing so, policymakers can foster a more secure and trustworthy environment for cryptocurrency transactions.

The significant impact of price value on behavioral intention suggests that cryptocurrency platforms in Mongolia could benefit from emphasizing the financial potential of digital assets. Marketing campaigns that highlight the value proposition of cryptocurrencies, particularly in terms of investment returns, could attract more users. However, these campaigns must also emphasize the risks to avoid misleading consumers.

Future research should delve deeper into the cultural and psychological factors that influence cryptocurrency adoption in Mongolia. The unique relationship between risk perception and behavioral intention in this study indicates that Mongolian users may approach investment decisions differently from users in other countries. Investigating how cultural values, such as risk-taking behavior or individualism, affect cryptocurrency use could provide valuable insights for both researchers and practitioners.

As noted in the limitations, a longitudinal approach would allow researchers to track changes in users’ behavioral intentions over time. Future studies should examine how factors such as market fluctuations, regulatory changes, or increased user experience impact the adoption of cryptocurrency in Mongolia. This would provide a more dynamic understanding of the factors influencing behavioral intention.

Conclusion

Behavioral intention to use cryptocurrency is an attractive area of research, however, there are a quite few studies relating to this topic in the Mongolian context. Thus, this study investigated the main factors that influence behavioral intention to use cryptocurrency among Mongolian customers using a promising conceptual model. In selecting the theoretical foundation, the most appropriate model was the extended UTAUT2 by Venkatesh et al. (2012) along with received risk and financial literacy. The proposed model explains 59.3% of the total variance in Mongolian customers’ intention to use cryptocurrency.

The selection of PLS-SEM, bootstrapping, and relevant model fit indicators was deliberate and aligned with the goals of this study. These techniques were chosen to provide a robust and comprehensive analysis of the factors influencing cryptocurrency adoption, while also addressing the specific characteristics of the data and the theoretical framework employed. The methodological choices are grounded in the literature and provide a solid foundation for the validity and reliability of the findings.

The findings of this study are significant in several respects. First, the strong influence of Performance Expectancy and Price Value on the behavioral intention to use cryptocurrency is consistent with prior research in other contexts (e.g., Venkatesh et al., 2012; Q. Zhou et al., 2020). This confirms that Mongolian customers view cryptocurrencies as a tool that can enhance their financial performance and as a valuable asset, particularly when market values are rising. The allure of potentially high returns serves as a powerful motivator for cryptocurrency adoption, consistent with findings from D. Wang et al. (2021).

The positive relationship between Perceived Risk and behavioral intention is notable, as it contrasts with many studies that have found risk perception to be a deterrent to adoption (e.g., Abramova et al., 2021; Barberis & Thaler, 2003). In Mongolia, this relationship may reflect a unique risk-taking culture or a perception that the potential rewards outweigh the risks. This phenomenon may also be driven by the limited investment opportunities in Mongolia, where cryptocurrency presents an alternative means of achieving financial growth.

The negative impact of Financial Literacy on behavioral intention underscores the speculative nature of cryptocurrency investments in Mongolia. Less financially literate individuals may be more likely to engage in risky investments without fully understanding the complexities or potential downsides of cryptocurrency, aligning with findings by Hastings (2013). This trend points to a need for greater education on the risks and benefits of cryptocurrency to prevent potential financial losses among users.

The absence of significant relationships for Effort Expectancy and Social Influence suggests that Mongolian customers, particularly in urban areas like Ulaanbaatar, do not face significant barriers in terms of effort or peer influence when adopting cryptocurrency. The high rate of internet penetration and smartphone use may explain the diminished role of effort expectancy, as cryptocurrency transactions are relatively easy for tech-savvy users to manage. Similarly, the self-directed nature of cryptocurrency investment in Mongolia may reduce the role of social influence, suggesting that individuals rely more on personal judgment than on the opinions of friends, family, or colleagues.

The findings of this study provide important insights into the factors influencing the behavioral intention to use cryptocurrency among Mongolian customers. These insights have significant practical implications for various stakeholders in the cryptocurrency domain, including policymakers, cryptocurrency platforms, financial institutions, and individual investors. The discussion below elaborates on how the results of this study can be applied by these stakeholders to foster a more secure and sustainable environment for cryptocurrency adoption in Mongolia.

Policymakers should take note of the significant positive influence of perceived risk, as this finding suggests that Mongolian consumers are willing to engage in cryptocurrency despite being aware of the risks involved. This presents an opportunity for regulatory bodies to develop more comprehensive legal frameworks that address the specific risks of cryptocurrency transactions, such as fraud, market volatility, and the lack of consumer protection. The Bank of Mongolia has already issued warnings about the risks of cryptocurrency, but this study shows that risk perceptions alone are not deterring consumers from engaging in the market.

Policymakers should also consider the negative impact of financial literacy on cryptocurrency adoption. This finding suggests that less financially literate individuals are more likely to invest in cryptocurrencies, potentially without fully understanding the risks. To mitigate potential negative outcomes, educational programs focused on financial literacy should be implemented to ensure that consumers are making informed decisions. Studies have shown that increased financial literacy is associated with better financial decision-making (Lusardi & Mitchell, 2014). Therefore, government and regulatory bodies should prioritize the development of educational initiatives that increase awareness about the complexities of cryptocurrency investments.

For cryptocurrency platforms operating in Mongolia, the results of this study provide valuable insights into consumer behavior and motivations. The positive relationship between price value and behavioral intention indicates that Mongolian users are highly sensitive to market conditions and are motivated by the potential for high returns. Platforms could leverage this finding by emphasizing the investment potential of cryptocurrencies in their marketing strategies, while also educating users about the risks involved. By providing tools and resources that allow users to better understand price fluctuations and make informed decisions, platforms can foster trust and engagement among users, contributing to a more stable and loyal customer base.

Additionally, the role of hedonic motivation in driving cryptocurrency adoption suggests that platforms could capitalize on the entertainment and excitement associated with cryptocurrency trading. Incorporating gamification elements or providing interactive features that engage users could further enhance their motivation to participate in cryptocurrency markets. Previous research has demonstrated the effectiveness of gamification in increasing user engagement with financial technologies (Hamari et al., 2014), and cryptocurrency platforms could benefit from applying similar strategies.

Moreover, financial institutions have an important role to play in educating their customers about the risks and benefits of cryptocurrency. By providing transparent and easy-to-understand information, banks can help mitigate the potential risks associated with investing in digital currencies. For example, incorporating risk assessment tools into banking apps that provide real-time insights into the volatility of cryptocurrency markets could help customers make more informed investment decisions.

The findings of this study also hold important implications for individual investors in Mongolia. As cryptocurrencies become more widely adopted, it is crucial for investors to recognize the risks associated with these volatile assets. The study shows that while perceived risk positively influences the intention to use cryptocurrency, this does not necessarily mean that users fully understand or can mitigate those risks. Therefore, individual investors should be encouraged to conduct thorough research and seek expert advice before making significant investments in cryptocurrencies.