Abstract

This study investigates how corruption control influences the choice between high-tech and non-high-tech acquisition targets, using international data from 2000 to 2019. Grounded in the institutional theory and transaction cost economics, we hypothesize that stronger corruption control reduces transaction risks, making high-tech acquisitions more attractive. Our findings confirm a positive relationship between corruption control and high-tech acquisitions, but document an inverted U-shaped effect, indicating that beyond a certain threshold, the regulatory burden may deter high-tech investments. Further, we find that cultural distance shapes acquisition outcomes, reinforcing the cross-cultural management theory that power distance moderates the positive relationship between corruption control and high-tech acquisitions. The study contributes to the literature by highlighting the importance of institutional quality in shaping sector-specific acquisition strategies and offers practical implications for managers and policymakers.

“As long as politics is the shadow of big business, the attenuation of the shadow will not change the substance.”

Introduction

In recent years, the global mergers and acquisitions (M&A) landscape has transformed significantly, with technology-driven transactions surging to account for nearly 60% of all deals (Huang & Xie, 2023; Schweizer et al., 2023). This surge highlights the growing strategic importance of high-tech firms, which serve as critical engines of innovation, economic growth, and digital transformation. High-tech firms, characterized by substantial investments in R&D, robust intellectual property portfolios, and pioneering advancements in areas, such as artificial intelligence, biotechnology, and renewable energy, present acquirers with unparalleled growth opportunities. For acquiring firms, the potential to gain competitive advantage and drive innovation makes high-tech firms especially attractive targets in our knowledge-based economy (Bhussar et al., 2022).

However, acquiring high-tech firms, especially in cross-border contexts, brings with it complex challenges. High-tech firms rely heavily on intangible assets, such as patents and proprietary technologies, whose valuation is inherently uncertain and can lead to significant information asymmetry between buyer and seller (Chen et al., 2020). Burger et al. (2023) suggest that the high levels of uncertainty surrounding future cash flows and the difficulty in assessing intangible assets worsen the risks involved, as acquirers must often make decisions with incomplete information about the true value and growth potential of these firms. As a result, while high-tech acquisitions offer substantial growth prospects, they also expose acquirers to greater risks of adverse selection and misjudgment of firm value.

Despite the significant rise in high-tech acquisitions, understanding of how institutional quality, specifically corruption control, affects these transactions remains limited. Chen et al. (2024) focus on the impact of corruption culture and find that higher levels of corruption culture were associated with M&A deals of greater value. Also, firms exhibited a tendency to acquire targets that shared similar levels of corruption culture. Ueta (2024) emphasizes the impact of economic and political institutions on investor-community conflicts during acquisitions. Indeed, the institutional environment in target countries, particularly corruption control, can play a key role in shaping transaction costs and overall deal risk, particularly in sectors where transparency and institutional quality are crucial to due diligence processes. In environments with weak governance frameworks, high-tech firms, with their intangible assets and innovation strategies, are predominantly vulnerable to the risks that come with institutional imperfections. Corruption, as an indicator of institutional weakness, worsens these challenges by increasing the costs and complexity of due diligence, diminishing transparency, and ultimately impacting the strategic calculus of potential acquirers (Huang et al., 2023). This highlights the need to examine how institutional factors, such as corruption control, influence the decision to acquire high-tech versus non-high-tech firms, especially in cross-border settings where institutional quality is variable.

Addressing this gap, our study investigates the impact of corruption control on high-tech versus non-high-tech acquisition choices, grounded in institutional theory and transaction cost economics. Institutional theory (North, 1990) emphasizes the importance of formal and informal rules that structure economic activity, suggesting that high levels of corruption can distort the market and reduce transaction efficiency. Transaction cost economics theory (Williamson, 1979) further supports this view by positing that firms seek to minimize transaction costs in M&A decisions, which are significantly increased in corrupt environments. By focusing on how corruption levels influence high-tech acquisitions, this research provides new evidence on the association between institutional quality and sector-specific M&A strategies.

Prior studies have largely concentrated on firm-level factors that make high-tech firms attractive acquisition targets, such as R&D capabilities, innovation potential, and intellectual property assets (Desyllas & Hughes, 2009; Davis & Madura, 2015; Renko et al., 2022; Zhu et al., 2024). While these factors are essential to understanding firm attractiveness, they do not account for the broader institutional environment in which cross-border acquisitions take place. Specifically, there is limited investigation into how country-level institutional factors, such as corruption control, shape the selection of high-tech versus non-high-tech targets. This gap is particularly important given the rise of cross-border M&A in high-tech sectors, where institutional quality and transparency are critical for reducing transaction risks. Corruption, as a fundamental barrier to effective governance, affects transaction costs and due diligence efforts, thereby shaping acquirers’ strategic choices in complex sectors like high-tech.

Prior studies find that corruption increases operational costs (DiRienzo et al., 2007; Kyriacou et al., 2024), reduces announcement returns (Jiang & Lu, 2020), and may delay the completion of acquisition deals in cross-border contexts (Weitzel & Berns, 2006). These challenges are even more pronounced in high-tech industries, where the intrinsic intangibility of assets and high innovation dependency make transparency and institutional integrity essential. For instance, high levels of corruption can increase market imperfections, leading to increased information asymmetry and investor uncertainty (Huang et al., 2023; Jain et al., 2017; Khan et al., 2019). These imperfections, in turn, increase adverse selection risks in high-tech acquisitions.

Despite a considerable body of literature on the influence of corruption on international investment flows, such as studies linking corruption with foreign investment volumes (Godinez & Liu, 2015; Habib & Zurawicki, 2001), portfolio allocation (Jain et al., 2017), and shareholder value for acquiring and target firms (Nguyen & Phan, 2017; Nguyen et al., 2020; Yang et al., 2022), very little is known about how corruption affects the choice between high-tech and non-high-tech acquisitions. To the best of our knowledge, existing research has yet to fully explore how acquirers’ strategic planning is shaped by institutional imperfections like corruption, particularly in sectors where intangible assets play a dominant role. Building on the idea that corruption levels in the host country can exacerbate inherent information asymmetries within the high-tech sector, we hypothesize that acquirers may favor non-high-tech targets when corruption is high, as these transactions may pose lower risks of adverse selection and value misjudgment.

Using a comprehensive dataset of international acquisitions from 2000 to 2019, our results indicate a positive relationship between corruption control in the target country and the likelihood of high-tech acquisitions. Accordingly, when target countries exhibit strong corruption control, with low corruption levels and effective anti-corruption measures, acquirers are more inclined to pursue high-tech targets. However, this relationship follows an inverted U-shape; beyond a certain point, extremely high corruption control levels tend to shift preferences toward non-high-tech acquisitions. These findings are consistent across various testing methodologies and subgroups, underscoring the robustness of our results.

In addition, we find that acquirers are more likely to select high-tech targets when the host country’s corruption control is stronger than that of the acquirer’s home country, a trend likely influenced by information asymmetries across borders. Further, we examine how the interaction between corruption control in the host country and cultural distance, measured through power distance disparity (PDV) between the target and acquirer countries, affects acquisition choices. Drawing on arguments that high power distance cultures may tolerate greater inequality and corruption (Bontis et al., 2009; Dang et al., 2022), our findings reveal that as cultural differences between the host and home countries increase, the positive relationship between corruption control and high-tech acquisitions weakens, suggesting that cultural distance complicates the benefits of strong governance in high-tech M&A decisions.

This paper makes substantial contributions to the literature on corruption and high-tech acquisitions in three crucial ways. First, this study addresses a critical gap in the high-tech acquisition literature by examining how institutional quality, particularly corruption control, influences acquirers’ decisions. Prior research on M&A has largely focused on general economic, financial, or firm-specific factors, without fully exploring how corruption control affects the selection of high-tech firms as targets. High-tech firms, due to their intangible assets and high levels of uncertainty, are more vulnerable to market imperfections, especially in countries with weak institutional frameworks. While studies like Habib and Zurawicki (2001) find the impact of corruption on overall investment flows, few have examined its role in shaping sector-specific acquisition strategies, particularly in high-tech sectors. By focusing on this aspect, our study fills an important gap in understanding how acquirers navigate institutional deficiencies when targeting high-tech firms. The distinction between high-tech and non-high-tech acquisitions is essential as acquirers must navigate the trade-off between high growth potential and substantial risk in high-tech firms. Corruption can make high-tech acquisitions less attractive in environments with weak governance. Therefore, understanding how corruption affects these choices is valuable for both investors and policymakers. A second key contribution lies in the exploration of corruption control asymmetry between home and host countries. Unlike previous studies that treat corruption as static, this research introduces the concept of corruption control disparity, demonstrating that high-tech acquisitions are more likely when the target country has stronger corruption control compared to the acquirer’s home country. This highlights the importance of relative institutional quality in international M&A strategies. Further, our study integrates cultural dimensions, specifically power distance, into the analysis. We find that cultural factors moderate the relationship between corruption control and high-tech acquisitions.

These findings provide both theoretical and practical contributions for firm managers and policymakers. For managers, understanding how corruption control and cultural differences influence acquisition decisions can guide more informed strategies. From a policy perspective, improving institutional transparency and reducing corruption are critical to attracting high-tech investments, especially in emerging markets. This research has broader implications for global innovation and economic development. Countries with stronger corruption control are better positioned to attract high-tech investments, which drive innovation and contribute to long-term growth. Whereas, corruption stifles innovation and delays the development of competitive high-tech industries. Policymakers in emerging markets can use these insights to implement anti-corruption reforms that create more favorable conditions for high-tech investment.

The subsequent sections of this paper are organized as follows. Section “Literature Review and Hypothesis Development” reviews the related literature and develops hypotheses. Section “Data, Sample, and Variable Construction” describes data and methodology. Section “Empirical Results” reports empirical results. The conclusion of the paper is presented in Section “Conclusion.”

Literature Review and Hypothesis Development

Corruption and High-tech Acquisitions

Corruption is a core aspect of institutional weakness, exhibiting in forms, such as bribery, embezzlement, patronage, and nepotism, drawing considerable attention from economists and international organizations. In 2018, United Nations Secretary-General Antonio Guterres highlighted corruption’s pervasive impact, stressing that it transcends borders and wealth, erodes resources crucial for education and healthcare, deters foreign investment, and drains natural assets (United Nations, 2018). He highlighted the World Economic Forum’s estimate that corruption costs the global economy at least $2.6 trillion, or about 5% of global GDP (WEF, 2019). Numerous studies support these assertions, showing how corruption negatively affects economic activities, particularly in acquisitions. Rossi and Volpin (2004) find that lower-corruption environments, which suggest better institutional quality and shareholder protections, attract a greater volume of acquisitions. Corruption compromises transparency in the acquisition process, raising concerns among bidders and lowering acquisition volumes. Using a sample of Chinese firms, Huang et al. (2023) report that a decline in corruption boosts cross-region takeover activities by 40% and more than doubles the deal volume. Other research also indicates corruption’s adverse effects on shareholder value (Nguyen & Phan, 2017) and target premiums (Chen et al., 2024; Weitzel & Berns, 2006). Particularly, corruption-related business costs can exceed those from taxation (Shleifer & Vishny, 1993).

In the high-tech sector, acquisition decisions are predominantly sensitive to the host country’s corruption level, reflecting a balance between potential rewards and risks. In low-corruption environments, where transparency prevails, information asymmetry and agency problems are minimized, making high-tech acquisitions more attractive. High-tech industries, known for their high growth potential despite uncertainties in cash flow, offer substantial returns for acquirers (Kohers & Kohers, 2000). While many high-tech stocks are volatile and involve young firms with limited funding and uncertain future cash flows, periods, for instance, the late 1990s tech boom saw these firms trading at high premiums (Benou & Madura, 2005). For acquirers, a target country with low corruption, indicating robust control and minimal corruption perception, presents an ideal setting to pursue high-tech acquisitions.

As corruption levels increase, high-tech acquisitions face several significant challenges. Agency problems within high-tech firms become worsen in environments with weak legal and institutional frameworks, minimal corruption control, and high corruption perceptions. In these settings, local managers have greater opportunities for self-serving behavior, resulting in both direct costs (expenses that benefit managers but harm shareholders) and indirect costs (inefficiencies due to bribery-driven decisions). Funds and resources are often misallocated from productive areas to less promising ones. Previous acquisition studies have highlighted how corruption contributes to market imperfections, such as information asymmetry and investor uncertainty around a firm’s core business (Jain et al., 2017; Khan et al., 2019), which further intensify ambiguity for investors in high-tech sectors. To address these issues, acquirers frequently rely on investment banks as advisors, seeking to mitigate information asymmetry and reduce investor uncertainty (Benou & Madura, 2005).

A second challenge involves limited access to external capital markets. High-tech industries require significant investment in research and development (R&D) to support growth and address rapid product obsolescence, resulting in particularly high R&D spending (Cloodt et al., 2006; Hagedoorn & Duysters, 2002; Jiang & Jiang, 2024). However, high-tech firms often struggle to secure external capital, especially debt financing, due to the inherent risks associated with their investments. Duan (2023) finds that facing the increasing threat of patent trolls, high-tech firms are burdened with significant legal expenses, heightened cash flow instability, and rising anticipated costs of financial distress. In countries with weak institutions, characterized by insufficient governance, low investor protection, and limited corruption control, external capital markets are generally underdeveloped and costly to access, particularly for high-tech firms (Khanna & Palepu, 2000). As corruption levels rise in host countries, capital costs for tech-based firms also increase, escalating transaction costs and financial constraints for acquirers. Therefore, as corruption intensifies, it often becomes more prudent for bidders to avoid high-tech targets in these environments.

Theoretical Framework and Hypothesis Development

Institutional theory (North, 1990) offers a foundation for understanding how a country’s legal and governance structures, particularly in terms of corruption control, shape strategic decisions in acquisitions. The institutional environment is critical for reducing uncertainty and information asymmetry, two factors that play a big role in the valuation of high-tech firms. High-tech firms, heavily dependent on intangible assets, are particularly vulnerable to institutional weaknesses. In corrupt environments, where transparency is compromised, assessing these assets becomes difficult, worsening risks for acquirers. Corruption can impede due diligence processes, increase the likelihood of adverse selection, and lead to misjudgments about the target firm’s actual value and potential (Huang et al., 2023; Kyriacou et al., 2024). This makes high-tech acquisitions in corrupt environments inherently riskier, as acquirers may be forced to make decisions based on incomplete or unreliable information.

In contrast, target countries with robust corruption control offer a stable and transparent environment, mitigating the risks of asymmetric information and creating favorable conditions for high-tech acquisitions. Strong anti-corruption measures provide a governance structure that supports transparency and fairness. In these environments, acquirers have greater confidence in the accuracy of asset valuations and the integrity of the transaction, which reduces the potential for adverse selection. This theoretical framework highlights the critical role that institutional quality plays in making high-tech firms in well-governed countries more appealing acquisition targets.

To further explain this relationship, we turn to Transaction Cost Economics theory (TCE) (Williamson, 1985), which posits that firms engage in M&A to minimize transaction costs, especially when facing valuation uncertainties (Dang et al., 2022). High-tech acquisitions, due to their reliance on intangible assets, often involve significant transaction costs as acquirers work to verify asset values and reduce information asymmetry. Corruption in the target country exacerbates these transaction costs by increasing risks related to misrepresented information and hidden liabilities. The additional costs linked to potential fraud, regulatory hurdles, and incomplete information make high-tech acquisitions less attractive in corrupt environments.

On the other hand, in countries with strong governance and effective corruption control, transaction costs are lower, as acquirers can trust the reliability of the information provided by target firms. Institutional safeguards reduce the risks associated with intangible asset valuation, enabling acquirers to pursue high-tech acquisitions more confidently. By fostering transparency and accountability, corruption control mechanisms lower the barriers to high-tech acquisitions, aligning with acquirers’ strategic objectives to mitigate risk while accessing innovative assets. As a result, high-tech acquisitions become a more viable and appealing choice in well-regulated environments.

Together, institutional theory and TCE provide a structured rationale for our first hypothesis. They highlight how institutional quality, particularly corruption control, serves as a key determinant in high-tech versus non-high-tech acquisition decisions. In countries with stronger institutional frameworks, high-tech acquisitions are favored due to the reduced transaction risks and greater transparency. This leads us to propose that the level of corruption control in target countries positively influences the likelihood of high-tech acquisitions.

We further explore how institutional disparity between home and host countries affects cross-border acquisition decisions, drawing on institutional distance theory (Kostova & Zaheer, 1999). This theory suggests that differences in institutional quality, including variations in corruption control, regulatory frameworks, and governance standards, introduce challenges for foreign investors. As these disparities increase, cross-border transactions become more complex and uncertain, requiring firms to navigate unfamiliar regulatory environments and adapt to different legal practices (Dang et al., 2021).

In the context of high-tech acquisitions, the institutional quality of the host country, especially regarding corruption control, can significantly impact acquirers’ risk assessments. When the host country has superior corruption control compared to the acquirer’s home country, high-tech targets are perceived as lower-risk investments. Strong institutional frameworks in the host country reduce information asymmetry and enhance transparency, making high-tech acquisitions more attractive to acquirers. Firms from countries with weaker governance may thus see the host country’s robust institutions as a protective factor against the specific risks associated with high-tech transactions.

On the other hand, if the host country has weaker institutional quality than the acquirer’s home country, high-tech acquisitions become riskier. Increased corruption and inadequate governance can lead to increased transaction costs, greater information asymmetry, and potential value erosion. In such environments, acquirers may prefer non-high-tech targets or avoid acquisitions altogether to avoid the intensified complexities of due diligence and the challenges of managing intangible assets in a poorly governed setting.

Empirical studies have shown the impact of institutional disparity on M&A decisions. For example, firms from highly regulated countries often hesitate to invest in countries with lower regulatory standards due to concerns over operational inefficiencies, compliance challenges, and reputational risks (Shimizu et al., 2004; Xu & Shenkar, 2002). In high-tech sectors, where transparency and asset protection are critical, institutional disparity has even greater consequences.

The concept of corruption distance has been used in existing research to assess its effect on acquisitions. For instance, Godinez and Liu (2015) find that firms from low-corruption countries, often unfamiliar with the informal practices in high-corruption countries, show reduced FDI flows. However, limited research specifically examines how these disparities impact high-tech acquisitions, which is the gap our study aims to fill.

As corruption disparities increase, entering an unfamiliar, potentially corrupt environment becomes increasingly risky, particularly in high-tech acquisitions where information asymmetry is significant. In such settings, higher agency conflicts, misallocated resources, and increased transaction costs make high-tech targets less attractive to acquirers. Brouthers and Brouthers (2001) argue that institutional disparity, especially regarding corruption, raises transaction costs, making business in unconventional environments more complex. Similarly, Godinez and Liu (2015) find that substantial institutional differences complicate acquirers’ efforts to establish legitimacy and adapt to local norms, further discouraging high-tech acquisitions in these contexts. As a result, in high-disparity environments, acquirers may favor non-high-tech targets, which are less vulnerable to the compounded risks of an uncertain market. From these arguments, the second hypothesis is established as follows:

Cultural theory, particularly Hofstede’s Power Distance dimension, provides a useful framework for understanding how national culture shapes tolerance for corruption and affects cross-border acquisitions. National culture, defined as the shared values and beliefs within a society, is formed through socialization processes within families, educational institutions, and communities (Hofstede, 1980). Studies on cultural influence (e.g., Gunkel et al., 2014) frequently use Hofstede’s cultural dimensions, including individualism versus collectivism, masculinity versus femininity, power distance, uncertainty avoidance, and short-term vs. long-term orientation. For this study, we focus on power distance, a dimension with significant implications for corruption dynamics in M&A but limited examination in prior research.

Power distance, as defined by Hofstede (1980, 2001), measures the degree to which inequality and hierarchical authority are accepted within a society. In high power distance cultures, social hierarchies and unequal power distributions are often viewed as natural, fostering a greater tolerance for corruption. In these environments, individuals in high-ranking positions may see their status as a right to personal gain, leading to practices that exploit their roles (Getz & Volkema, 2001). On the other hand, lower-status individuals may engage in corrupt acts, such as bribery, to improve their standing, while non-public officials may also use bribes to navigate these hierarchical systems (Breuer & Knetsch, 2022). In contrast, low power distance cultures promote equality, transparency, and cooperation, viewing titles and status with less emphasis (Davis & Ruhe, 2003).

High power distance therefore fosters acceptance of inequality and, by extension, corrupt practices, which can weaken anti-corruption measures. This tolerance for hierarchical power makes power distance a critical moderator in M&A, especially when corruption control is considered. In high power distance countries, anti-corruption initiatives may be less effective, as cultural acceptance of hierarchical and unequal relationships can dilute the impact of strong governance. As a result, the positive relationship between corruption control and high-tech acquisitions may be weakened. In contrast, in low power distance countries, where equality and transparency are prioritized, strong corruption control is more likely to enhance the attractiveness of high-tech acquisitions.

Empirical evidence supports the influence of cultural distance on M&A. Brouthers and Brouthers (2001) and Dang et al. (2021) show that cultural differences, particularly in power distance, shape acquisition outcomes by influencing risk perception and the effectiveness of institutional governance. Building on these insights, we propose that when the power distance disparity between host and home countries is large, the positive impact of corruption control on high-tech acquisitions will be less pronounced. In contrast, a smaller power distance difference will likely amplify the benefits of strong corruption control. We expect that high power distance in the target country correlates with a greater tolerance for corruption, weakening the positive link between strong corruption control and high-tech acquisitions. Thus, as the power distance disparity widens, the positive relationship between corruption control and high-tech acquisitions will be diminished.

Motivated by these arguments, the following hypothesis is proposed:

Data, Sample, and Variable Construction

Data and Country Sample Selection

We conduct an analysis of international acquisitions spanning the period from 2000 to 2019, encompassing 38 different target countries. The choice of the period 2000 to 2019 is because it captures a significant timeframe in which the global economy experienced rapid technological advancement and increasing M&A activity in the high-tech sector. The early 2000s marked the acceleration of the digital revolution, with sectors such as information technology, biotechnology, and artificial intelligence seeing substantial growth. By analyzing data over this period, the study captures the effects of institutional improvements and anti-corruption reforms, especially after the representation of international governance standards by organizations such as the OECD (OECD, 2018) and the UN (United Nations, 2023). Further, this timeframe includes both periods of economic stability and financial crises, allowing our study to examine the differential effects of corruption control across various macroeconomic conditions. Also, the 38 target countries were selected based on two main criteria: (a) their active participation in cross-border M&A activity, particularly in high-tech sectors, and (b) the availability of reliable governance and corruption control data from established databases, including the World Bank’s Worldwide Governance Indicators and Transparency International’s Corruption Perception Index. These countries represent a diverse mix of developed and emerging markets, which allows the study to capture the effects of corruption control across different institutional contexts.

The data regarding acquisition transactions were sourced from the Thomson Reuters SDC Platinum database. Firm-specific financial data were gathered from the Worldscope Database, while country-level variables utilized for our analysis were sourced from the Fraser Institute, Worldwide Governance Indicators (World Bank), Transparency International, and World Development Indicators (World Bank).

Following prior empirical studies, we set specific inclusion criteria for our sample. Acquiring companies were required to secure a stake of at least 5% in target firms and to maintain a minimum 5% ownership post-acquisition, consistent with Bris and Cabolis (2008). To reduce sample selection bias, we excluded instances where multiple firms acquired the same target on the same day. To ensure economic relevance, we retained only transactions with a minimum deal value of US$1 million. After applying these criteria and excluding observations with missing data, our final sample comprised 75,412 completed acquisition deals across 38 target countries.

Variable Construction

This study examines the relationship between corruption control and high-tech acquisition activity, including potential variations across institutional and cultural contexts. Given the binary nature of the primary dependent variable (high-tech vs. non-high-tech acquisitions), we used Probit regression models, which are well-suited for estimating event probabilities based on independent variables like corruption control. The normal distribution assumption of Probit models aligns with the cross-country variations and binary outcomes of our data, allowing us to estimate how corruption control and other control variables affect the likelihood of high-tech acquisitions. We acknowledge that one limitation of Probit models is their susceptibility to omitted variable bias if key predictors of high-tech acquisitions are excluded. To mitigate this, we included a comprehensive set of firm- and country-level control variables to account for alternative explanations of acquisition decisions, thereby reducing the risk of bias from unobserved heterogeneity. Appendix B provides detailed definitions and sources for the variables. Our empirical model is as follows:

where,

Following methodologies used in prior research, such as Weitzel and Berns (2006), we employ one of the World Governance Indicators from the World Bank to measure corruption control at the country level, denoted as CCTRL. This variable serves as a proxy for the level of corruption control within a country, based on perceptions of how public power is used for private gain. It captures a range of corrupt activities, from minor incidents to significant abuses of power, including elite influence on state functions (Kaufmann et al., 2005). The CCTRL index ranges from −2.5 (low control) to +2.5 (high control), with higher values indicating stronger control over corruption.

To ensure the robustness of our findings, we also include an alternative measure, the Corruption Perceptions Index (CPER), released annually by Transparency International since 1996. The CPER assesses perceived corruption in the public sector, based on expert and business professional surveys conducted by Transparency International. It uses a scale from 0 to 100, where 0 indicates high perceived corruption and 100 indicates low perceived corruption. This widely used index provides an additional layer of analysis for evaluating corruption-related impacts in our study.

Prior studies have identified various deal-, firm-, and country-level characteristics associated with the likelihood of high-tech firms being acquired. To incorporate these factors, we include a set of control variables in our analysis. At the country level, economic conditions significantly impact the appeal of tech firms as acquisition targets (Davis & Madura, 2015). To capture these economic factors, we use several proxies: lnGDPcap represents the natural logarithm of GDP per capita as an indicator of a country’s economic prosperity, GDPgrt reflects GDP growth to indicate the rate of economic expansion, and MCAP/GDP denotes the stock market capitalization relative to GDP. We also consider economic freedom, measured by the EFQ variable from the Fraser Institute’s Economic Freedom of the World index, which ranges from 0 (lowest freedom) to 10 (highest freedom). Further, we include CITAX, which represents the level of taxation on income and capital gains, sourced from the Global Financial Development Database. Tax considerations can influence acquirers’ choices between high-tech and non-high-tech targets, particularly if they are assessing industrial relatedness. Devos et al. (2009) suggest that while operating synergies drive value in same-industry deals, financial (tax) synergies are more relevant in diversified mergers. Therefore, tax levels may play a role in target selection, especially in high-tech sectors, where industrial relatedness is a key consideration.

We also include variables that capture deal-specific characteristics, which may influence the choice between high-tech and non-high-tech targets. TOEHOLD is a continuous variable representing the percentage of the target firm’s shares held by the acquiring company at the time of the bid announcement (Andriosopoulos & Yang, 2015). RELATED is a binary variable that takes the value of one if the target and acquirer operate in the same industry, and zero otherwise. Many high-tech firms leverage acquisitions to outsource their R&D efforts (Higgins & Rodriguez, 2006), while larger high-tech firms often acquire smaller, innovative companies to enhance internal R&D and diversify their technological capabilities (Renko et al., 2022). SHARES denotes the percentage of the target firm’s shares sought by the bidder, while CASH is a binary variable that equals one for all-cash deals and zero otherwise. Cash-financed deals introduce issues of information asymmetry and adverse selection, as acquirer shareholders may be concerned about overpayment due to potential overvaluation of the target (Rappaport & Sirower, 1999). This concern is heightened in high-tech industries, where asset valuation is more uncertain, making it challenging to accurately signal worth to acquirers (Capron & Shen, 2007). AcqVALUE represents the transaction value of the deal, expressed as the natural logarithm of the transaction amount in US$ million. Larger deals typically attract greater attention and can have a more substantial effect on market valuation (Andriosopoulos & Yang, 2015). We also control for year (δt), industry (γs), and geographic (Ωg) effects in our empirical models.

Sample Characteristics

Table 1 provides an overview of the characteristics of completed transactions within our dataset. Generally, successful deals are predominantly found in the top quartile, accounting for 74,649 out of 79,632 transactions. Approximately 27.78% of the M&A deals involve target companies operating in related industries, indicating a degree of industry-related acquisitions. Cash is the chosen mode of payment in 43.55% of the deals, while in 17.01% of cases, the acquiring firm holds a share of the target stake at the time of the announcement. Furthermore, bidders seek approximately 67.11% of the target firm’s shares on average, and the mean transaction value stands at US$256.11 million. Notably, 28.41% of the acquisitions pertain to high-tech target companies, while high-tech bidders are involved in 24.43% of the deals.

Characteristics of Completed Acquisitions.

Note. This table provides an overview of the deal-specific characteristics and institutional environments of target countries involved in mergers and acquisitions (M&A) from 2000 to 2019. The table categorizes data by quartiles based on the number of deals and highlights key variables such as the percentage of related deals, cash payments, toehold ownership, the average share sought by bidders, and the mean transaction value. Further, it reports the proportion of high-tech acquired firms and high-tech bidders across quartiles. Countries in the top quartile exhibit a higher frequency of deals, larger transaction values, and a greater proportion of high-tech acquisitions, reflecting their institutional advantages and appeal for technology-driven investments.

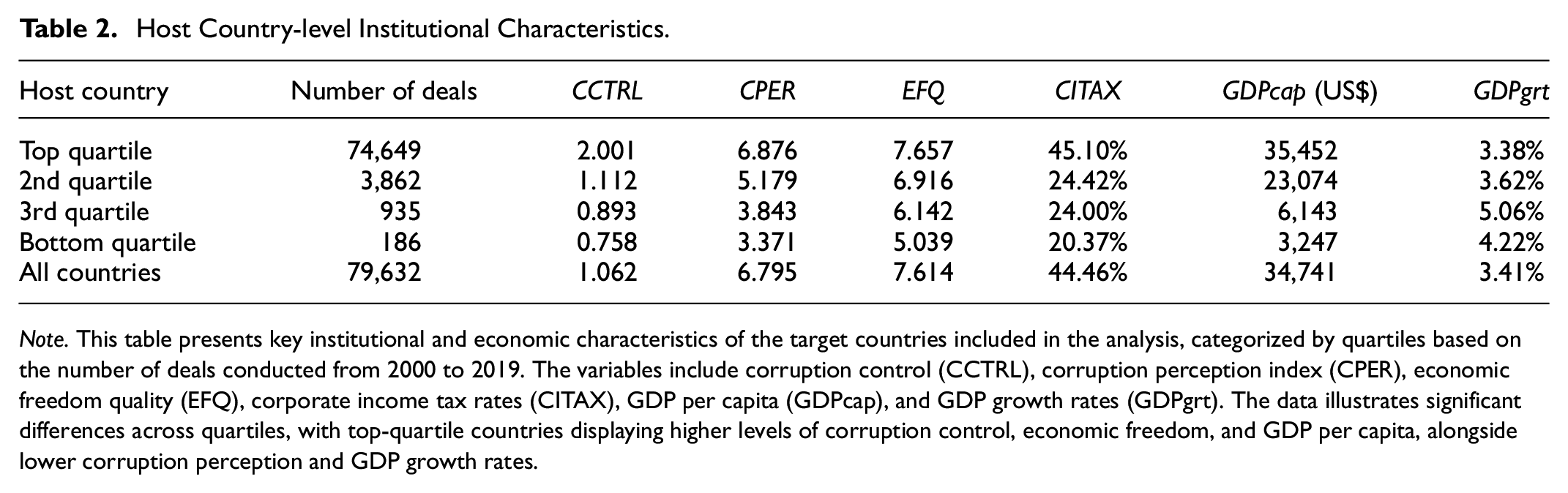

Table 2 provides essential descriptive statistics for the institutional and economic variables of the target countries. The data is categorized by quartile, based on the number of deals. It is evident that host countries in the top quartile demonstrate the highest levels of corruption control and economic policy uncertainty. On average, these countries exhibit greater GDP per capita, higher economic freedom, and tax rates, as well as lower GDP growth rates.

Host Country-level Institutional Characteristics.

Note. This table presents key institutional and economic characteristics of the target countries included in the analysis, categorized by quartiles based on the number of deals conducted from 2000 to 2019. The variables include corruption control (CCTRL), corruption perception index (CPER), economic freedom quality (EFQ), corporate income tax rates (CITAX), GDP per capita (GDPcap), and GDP growth rates (GDPgrt). The data illustrates significant differences across quartiles, with top-quartile countries displaying higher levels of corruption control, economic freedom, and GDP per capita, alongside lower corruption perception and GDP growth rates.

We also report the characteristics of acquisitions across developed and emerging markets, illustrating the differing economic and institutional settings that impact M&A decisions (Appendix A). For developed countries, such as the United States and Japan, the data shows a high volume of deals and significant average deal values. These countries exhibit high scores in corruption control and economic freedom, with substantial market capitalization to GDP ratios, which reflect stable investment environments with robust institutional quality. This stability and transparency are particularly advantageous to high-tech acquisitions, as investors perceive these environments to be less risky, with lower levels of information asymmetry and stronger governance mechanisms to protect intangible assets, which are critical in high-tech sectors. On the other hand, in emerging markets, such as China, India, and Malaysia, the characteristics highlight the challenges and opportunities unique to these regions. Although emerging markets present lower corruption control and economic freedom scores, they tend to have higher growth rates and attractive entry points due to lower valuations compared to developed economies. However, the lower scores in corruption control, combined with higher perceived corruption, signal potential risks related to governance, resource allocation, and information asymmetry. This combination creates a more complex environment for high-tech acquisitions, where transaction costs and risks associated with managing intangible assets may discourage investors.

Empirical Results

Target Country’s Corruption Control and High-tech Acquisitions

To test the first hypothesis regarding the impact of host country’s corruption control (Target CCTRL) on the likelihood of high-tech acquisitions, we conducted a regression analysis using equation (1) for the entire dataset. The results of this analysis are presented in Table 3. The Target CCTRL coefficient is positive and highly significant at the 1% level in all columns. For instance, in Column (1), the coefficient for CCTRL is 0.213 (with a t-statistic of 13.58). This indicates that an increase in the target country’s level of corruption control by one standard deviation (which is 0.48, standard deviation of the CCTRL variable in the whole sample) results in a rise of 10.22 (=0.48 × 0.213) percentage point in high-tech acquisitions. This provides strong support for the first hypothesis (

Target Country Corruption and High-tech Acquisitions.

Note. This table presents the probit regression results examining the influence of corruption control in target countries (CCTRL) on the likelihood of high-tech acquisitions. The dependent variable is a binary indicator that equals 1 for high-tech acquisitions and 0 for non-high-tech acquisitions. Key independent variables include CCTRL (corruption control index), CCTRL2 (to capture the potential non-linear effects), and deal-specific controls such as RELATED (whether the acquirer and target operate in the same industry), CASH (indicator for all-cash deals), TOEHOLD (percentage of target shares already held by the acquirer), SHARES (percentage of shares sought), and AcqVALUE (natural logarithm of transaction value). Country-level controls include economic freedom (EFQ), market capitalization to GDP (MCAP/GDP), corporate tax rates (CITAX), GDP per capita (lnGDPcap), and GDP growth rate (GDPgrt). We also control for year (δt), industry (γs), and geographic (Ωg) effects in our empirical models. z-ratios are shown in parentheses. The symbols ***, **, and * indicate significance at the 1%, 5%, and 10% levels, respectively.

Further, one of the findings of the study is the inverted U-shaped relationship between corruption control and high-tech acquisitions, suggesting that after a certain threshold, increases in corruption control may lead acquirers to favor non-high-tech firms. This phenomenon can be understood through the lens of diminishing returns to transparency. In environments where corruption control is moderate or weak, improving institutional integrity can reduce transaction costs and information asymmetry, making high-tech acquisitions more attractive due to the high value of their intangible assets. However, as corruption control becomes remarkably strong, the regulatory burden and compliance costs might also increase. Acquirers may then perceive non-high-tech firms, where innovation and R&D risk are lower, as more attractive options because the heightened regulatory oversight could make high-tech acquisitions more complex or expensive. We have also connected this finding to relevant prior literature. For example, studies in institutional economics (e.g., Rodrik, 2007) suggest that beyond a certain point, regulatory stringency might deter foreign investment in industries with high uncertainty, such as high-tech.

These results remain consistent when accounting for other country-level characteristics (Columns [2] through [4]), providing additional confirmation of our findings.

The results using perception of corruption (CPER) as an alternative measure of corruption control, presented in Table 4, further substantiate our core findings. Across all three columns, the Target CPER coefficient is positive and highly significant at the 1% level, indicating that a greater perception of corruption in the target country initially correlates with a higher likelihood of high-tech acquisitions. This aligns with our first hypothesis that acquirers are attracted to high-tech targets in countries with more perceived corruption, potentially due to favorable conditions for accessing innovative assets at competitive valuations.

Robustness Check With Alternative Independent Variables.

Note. This table presents robustness checks using an alternative measure of corruption control, the Corruption Perception Index (CPER), to evaluate its impact on high-tech acquisitions. The dependent variable remains a binary indicator, with 1 representing high-tech acquisitions and 0 for non-high-tech acquisitions. Key variables include CPER (perceived corruption index), CPER2 (capturing non-linear effects), and control variables such as RELATED (industry relatedness), CASH (payment method), TOEHOLD (percentage of pre-bid ownership), SHARES (share percentage sought), AcqVALUE (deal size in log form), and additional country-level factors like EFQ (economic freedom), MCAP/GDP (market capitalization to GDP), CITAX (corporate tax rates), lnGDPcap (GDP per capita), and GDPgrt (GDP growth rate). We also control for year (δt), industry (γs), and geographic (Ωg) effects in our empirical models. z-ratios are shown in parentheses. The symbols ***, **, and * indicate significance at the 1%, 5%, and 10% levels, respectively.

We also find that the Target CPER2 coefficient is negative and significant at the 1% level in all columns, suggesting an inverted U-shaped relationship. This pattern indicates that while moderate levels of perceived corruption may create strategic opportunities for acquirers, particularly in high-innovation industries, excessive levels ultimately discourage high-tech transactions. As corruption perception crosses a critical threshold, the risks associated with high-tech acquisitions, such as increased information asymmetry, agency conflicts, and transaction costs, begin to outweigh the potential benefits.

To further assess the robustness of our findings, we conducted additional tests to examine how a country’s level of corruption control influences the selection between non-high-tech and high-tech targets in diverse economic contexts, specifically comparing developed and developing markets.

We initially evaluate the combined effect of corruption control and economic development on the acquirer’s choice of high-tech targets. We performed separate regressions of equation (1) for target companies located in developed economies and those in developing markets. As shown in Columns [1] and [2] of Table 5, the coefficients for the CCTRL variable and its squared term are consistent with our primary findings, indicating that stronger corruption control in host countries positively impacts the likelihood of high-tech acquisitions across both market types. Also, the negative and significant coefficients for the squared term confirm a diminishing effect, suggesting that after a certain threshold, the impact of corruption control on high-tech acquisitions decreases.

Results for Sub-samples.

Note. This table presents the probit regression results for sub-samples of target countries, distinguishing between developed and developing markets. This table explores how the level of corruption control in the target country influences the likelihood of high-tech acquisitions in these different economic contexts. The dependent variable remains a binary indicator (1 for high-tech acquisitions, 0 for non-high-tech acquisitions). Key variables include CCTRL (corruption control), CCTRL2 (capturing the non-linear effect), and various control variables such as RELATED (industry relatedness), CASH (payment method), TOEHOLD (percentage of shares already held by the acquirer), SHARES (percentage of shares sought), and AcqVALUE (transaction value in logarithmic form). Additionally, country-level controls like EFQ (economic freedom), MCAP/GDP (market capitalization to GDP), CITAX (corporate income tax), GDPcap (GDP per capita), and GDPgrt (GDP growth rate) are included. We also control for year (δt), industry (γs), and geographic (Ωg) effects in our empirical models. z-ratios are shown in parentheses. The symbols ***, **, and * indicate significance at the 1%, 5%, and 10% levels, respectively.

Second, it is likely that the potential for sample selection bias arises due to the high representation of U.S. firms in our sample (see Appendix A). To address this, we re-estimate equation (1) using only the non-U.S. subsample. The results, presented in Column [3] of Table 5, confirm that corruption in the target country continues to be a significant factor influencing the choice of high-tech acquisitions, indicating that this relationship holds consistently, regardless of whether the target firm is based in the U.S. or elsewhere.

Third, during crises, acquirers may be more risk-averse and prioritize targets in less volatile sectors such as non-high-tech, given the increased uncertainty surrounding high-tech firms’ future cash flows and the potential for rapid technological obsolescence. Also, financial crises often lead to tighter credit conditions, making it more difficult for acquirers to finance high-tech deals, which tend to require larger upfront investments in R&D and intangible assets (e.g., Bloom, 2009; Duchin & Schmidt, 2013). On the other hand, in non-crisis periods, when market conditions are more stable, acquirers may be more willing to pursue high-tech acquisitions, as the potential for innovation-driven growth is more attractive. Further, during non-crisis periods, the availability of external financing is typically greater, allowing acquirers to invest in high-risk, high-reward sectors like high-tech. We regress equation (1) for the two crisis and non-crisis subsamples. The results in Columns [4] and [5] of Table 5 indicate that the relationship between the intention to acquire a high-tech target and the corruption control level in the target country still holds for the two subsamples. Overall, the financial crisis has not affected our analysis results.

Further, as another complementary analysis, we regress equation (1) for the subsample of high-tech acquirers and non high-tech acquirers. As reported in Columns [1] and [2] of Table 6, the significant positive coefficients for Target CCTRL across the specifications suggest that acquirers, regardless of operating in high-tech or non high-tech industries, tend to prefer high-tech targets if the corruption levels of host countries decrease, reflecting through strong control of corruption and high corruption perceptions.

Results for High-tech versus Non High-tech Acquirers.

Note. This table presents the probit regression results comparing high-tech versus non-high-tech acquirers, exploring how the level of corruption control in target countries affects acquirer preferences. The dependent variable is a binary indicator (1 for high-tech acquisitions, 0 for non-high-tech acquisitions), and the key independent variable is CCTRL (corruption control index), along with CCTRL2 (to capture the non-linear relationship). Control variables include RELATED (industry relatedness), CASH (payment method), TOEHOLD (pre-acquisition ownership percentage), SHARES (percentage of shares sought), and AcqVALUE (transaction value in logarithmic form). Country-level controls such as EFQ (economic freedom), MCAP/GDP (market capitalization to GDP), CITAX (corporate tax rates), GDPcap (GDP per capita), and GDPgrt (GDP growth rate) are also included in the model. We also control for year (δt), industry (γs), and geographic (Ωg) effects in our empirical models. z-ratios are shown in parentheses. The symbols ***, **, and * indicate significance at the 1%, 5%, and 10% levels, respectively.

Country-level Transparency Difference and High-tech Acquisitions

Also, we posit that the higher the difference in the levels of corruption control between target and acquiring firm countries, the lower the probability of a transaction being made in the high-tech industry. Similar to equation (1), we use Diff_CCTRL (the difference in the level of corruption control between target and acquiring firm countries) as the main test variable. Specifically:

Table 7, Columns [1], [2], and [3] show the regression results, highlighting that Diff_CCTRL is positively associated with the likelihood of high-tech acquisitions. This positive association indicates that when the target country’s corruption control is stronger than that of the acquirer’s home country, there is a preference for high-tech targets. Accordingly, a greater level of corruption control in the target country compared to the bidding country reduces perceived risks associated with high-tech assets, making such transactions more attractive. These findings are consistent with existing literature and support Hypothesis (

Corruption Difference and High-tech Acquisitions.

Note. This table examines the impact of the disparity in corruption control levels between the target and acquirer countries on the likelihood of high-tech acquisitions. The dependent variable is a binary indicator (1 for high-tech acquisitions, 0 for non-high-tech acquisitions), and the primary independent variable is Diff_CCTRL (the difference in corruption control levels between the target and acquirer countries). Additional control variables include RELATED (industry relatedness), CASH (payment method), TOEHOLD (percentage of shares held by the acquirer before the deal), SHARES (percentage of shares sought), and AcqVALUE (logarithmic value of transaction size). Country-level variables such as EFQ (economic freedom), MCAP/GDP (market capitalization to GDP), CITAX (corporate tax rates), GDPcap (GDP per capita), and GDPgrt (GDP growth rate) are also incorporated. We also control for year (δt), industry (γs), and geographic (Ωg) effects in our empirical models. z-ratios are shown in parentheses. The symbols ***, **, and * indicate significance at the 1%, 5%, and 10% levels, respectively.

Transparency, High-tech Acquisitions, and the Role of Power Distance in Acquisitions

In this section, we introduce an interaction between corruption control variables and power distance to assess whether differences in power distance between host and home countries influence the relationship between host country transparency and the choice of high-tech targets. Power distance is operationalized using the Hofstede Power Distance Index, which scores countries on a scale from 0 to 100, with higher scores indicating greater acceptance of hierarchical structures and unequal distributions of power. We hypothesize that the positive relationship between host country institutional transparency, measured by corruption control, and the selection of high-tech targets will be weaker when target countries exhibit significantly higher power distance than the acquirer’s home country. Expanding on equation (1), we include Diff_PDI, representing the difference in power distance between the host and home countries, to capture this moderating effect. We run the following regression model:

In Table 8, we present the regression results for the interaction between the corruption control in the host nation (Target CCTRL) and the power distance difference proxy (Diff_PDI) on the likelihood of high-tech acquisitions. The Target CCTRL variable remains positively correlated with the probability of transactions occurring in the high-tech industry, even after accounting for the impact of host country-specific characteristics (Column [1]) and all host-home country-specific characteristics (Column [2]). This suggests that a stronger corruption control in the host nation is associated with a higher likelihood of high-tech acquisitions.

The Role of Power Distance.

Note. This table explores the interaction between corruption control in the target country and the power distance difference (Diff_PDI) between the target and acquirer countries, and its impact on the likelihood of high-tech acquisitions. The dependent variable is a binary indicator (1 for high-tech acquisitions, 0 for non-high-tech acquisitions). Key independent variables include CCTRL (corruption control), Diff_PDI (the difference in power distance between the target and acquirer countries), and the interaction term CCTRL × Diff_PDI. Control variables such as RELATED (industry relatedness), CASH (payment method), TOEHOLD (percentage of shares already held by the acquirer), SHARES (percentage of shares sought), and AcqVALUE (transaction value in log form) are included. Country-level controls like EFQ (economic freedom), MCAP/GDP (market capitalization to GDP), CITAX (corporate tax rates), GDPcap (GDP per capita), and GDPgrt (GDP growth rate) are also considered. We also control for year (δt), industry (γs), and geographic (Ωg) effects in our empirical models. z-ratios are shown in parentheses. The symbols ***, **, and * indicate significance at the 1%, 5%, and 10% levels, respectively.

The coefficients for power distance difference proxies (Diff_PDI) are negatively significant. This indicates that acquirers are unlikely to choose high-tech target firms when the power distance difference between the target country and the bidding country becomes larger. This supports the idea that higher power distance in the target country relative to the bidding country hinders innovative opportunities and technological knowledge in high-tech target firms, making high-tech acquisition deals less attractive to acquiring firms.

When interacting the Target CCTRL variable with the power distance difference proxy (Diff_PDI), the coefficients for interaction terms between the Target CCTRL and Diff_PDI are statistically negative across all specifications. This result aligns with the hypothesis (

Conclusion

This research investigates the impact of a target nation’s level of corruption control on the choices made by acquirers between high-tech and non high-tech targets in international acquisitions over 2000 to 2019. After accounting for various deal-specific and country-level factors, we find that acquiring firms tend to prefer high-tech targets when conducting deals in host nations with strong institutional transparency and corruption control. This suggests that a high level of corruption control in the target country positively influences the likelihood of high-tech acquisitions. However, as corruption control in target countries continues to increase, the preference for high-tech deals diminishes. This indicates that there is a threshold beyond which the benefits of strong corruption control in target countries are not as pronounced for high-tech acquisitions. The study also finds that a significant difference in corruption control between the target country and the acquirer country negatively impacts high-tech acquisitions. Larger gaps in corruption control levels reduce the likelihood of high-tech acquisitions. Lastly, the interaction between target country corruption control and the power distance difference between host and home countries plays a role. When cultural differences, particularly power distance, are greater, the positive relationship between target country corruption control and high-tech acquisitions weakens or even becomes negative.

This study contributes to the literature on institutional theory and cross-border M&A by showing that institutional quality, particularly corruption control, plays a critical role in shaping high-tech acquisition decisions. The identification of an inverted U-shaped relationship adds a new dimension to the understanding of how improvements in governance can have both positive and negative effects on acquisition strategies, depending on the sector and the level of regulation. This finding challenges the simplistic assumption that stronger governance always leads to increased investment and suggests that there may be diminishing returns to institutional improvements in highly regulated environments.

From a practical perspective, these results have implications for businesses, investors, and policymakers. Managers should incorporate assessments of target countries’ corruption control and overall institutional quality into their strategic decision-making processes. The results suggest that investing in high-tech firms is more attractive in countries with moderate to strong corruption control. However, beyond a certain threshold, the complexity of regulatory compliance in highly transparent environments might increase transaction costs, making non-high-tech firms more appealing. Managers should balance the benefits of reduced information asymmetry with the potential costs of increased regulatory oversight. Also, for firms seeking high-tech acquisitions in emerging markets, improvements in institutional quality, such as corruption control, can signal reduced risks and greater opportunities. Managers should be prepared to seize these opportunities as countries implement reforms to improve transparency and governance.

For policymakers, the study highlights the importance of improving corruption control to attract high-tech FDI. Governments should prioritize anti-corruption reforms and institutional transparency as part of their broader economic development strategies. By fostering a stable and transparent institutional environment, policymakers can make their countries more attractive to high-tech investors, which in turn can drive innovation and economic growth. Further, while reducing corruption is critical, policymakers should be cautious about creating overly burdensome regulatory environments that may deter high-tech investments. There is a delicate balance between ensuring transparency and maintaining a business-friendly environment, particularly for industries that require flexibility, such as high-tech. Excessive regulation could stifle innovation by making it more difficult for foreign firms to enter these markets.

While this study offers valuable contributions, it is important to acknowledge several limitations that provide suggestions for future research. First, while the study focuses on cultural distance through the lens of power distance, it does not address other cultural dimensions, such as individualism or uncertainty avoidance, which could significantly affect firms’ risk assessment and M&A decision-making processes in high-tech industries. Future research could explore these additional cultural factors by investigating how individualism influences firms’ openness to cross-border collaborations or how uncertainty avoidance impacts decision-making under risky conditions, particularly in high-stakes environments like high-tech acquisitions. Comparative studies across industries or geographic regions could also provide valuable insights into how different cultural dimensions interact with corruption control to shape acquisition strategies. Second, this study focuses on acquisition decisions but does not examine their long-term effects. Future research could explore how corruption control influences post-acquisition outcomes, such as operational integration, cultural alignment, and financial performance of acquired firms, especially in environments with varying levels of corruption. Specifically, future research could use longitudinal data to track key performance indicators over time, examining whether firms operating in corrupt environments face greater challenges in integrating acquired assets or achieving strategic objectives. Also, comparative analyses between acquisitions in corrupt and non-corrupt regions could provide insights into the mechanisms through which corruption control mitigates risks and enhances post-acquisition success.

Footnotes

Appendix

List of Variables.

| Variable | Description and source |

|---|---|

| Dependent variable | |

| HTECH | This dummy variable receives the value of one if an acquisition occurs in the high-tech industry and zero if the acquirer chooses the non high-tech target for transaction i in year t (Source: SDC Platinum). |

| Cross-country corruption-related variables | |

| CCTRL | This index measures the level of corruption control within a country, capturing perceptions of the extent to which public power is used for private gain. It reflects both minor and large-scale corruption, as well as state capture by elites and private interests. The index ranges from −2.5 to +2.5, with higher values indicating lower levels of corruption (Source: Worldwide Governance Indicators, World Bank). |

| CPER | This index measures perceived levels of public sector corruption, ranking 180 countries and territories based on assessments by experts and business leaders. It uses a scale from 0 to 100, where 0 indicates high levels of corruption and 100 signifies a very low level of corruption, or a “very clean” status (Source: Transparency International). |

| Other cross-country variables | |

| EFQ | This index assesses a country’s overall quality of economic freedom, evaluating its performance across five key areas: (1) government size, (2) legal structure and property rights security, (3) access to stable monetary systems, (4) freedom to engage in international trade, and (5) regulation of credit, labor, and business sectors (Source: Fraser Institute). |

| PDI | Power distance is operationalized using the Hofstede Power Distance Index, which scores countries on a scale from 0 to 100, with higher scores indicating greater acceptance of hierarchical structures and unequal distributions of power. |

| MCAP/GDP | The stock market capitalization to GDP ratio (Source: Global Financial Development Database). |

| CITAX | This variable relates to the tax level on income and capital gains (Source: World Development Indicators, World Bank). |

| GDPgrt | Annual percentage growth rate of Gross domestic product (Current US$) (Source: World Development Indicators, World Bank). |

| lnGDPcap | Gross domestic product per capita (Constant 2005 US$) in logarithm (Source: World Development Indicators, World Bank). |

| Deal-specific and firm-level variables | |

| RELATED | An indicator variable taking on the value of one if the target and the acquirer are in same areas of operations and zero for unrelated acquisitions (Source: SDC Platinum). |

| CASH | An indicator variable taking on the value of one if an acquisition is paid by cash and zero if it is paid by acquirer’s stock or a mixed cash and stock payment (Source: SDC Platinum). |

| SHARES | The percentage of the target firm’s shares sought by the bidding firm (Source: SDC Platinum). |

| TOEHOLD | The percentage of target equity held by the bidder before the acquisition (Source: SDC Platinum). |

| AcqVALUE | The value of the transaction (US$ million) in logarithm (Source: SDC Platinum). |

Acknowledgements

We wish to thank Mieszko Mazur and Edward Jones, and the participants at the 2021 Financial Markets and Corporate Governance Conference, and seminar at the University of Danang - University of Economics, for very valuable comments and suggestions.

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: This research is funded by Funds for Science and Technology Development of the University of Danang under project number B2023-DN04-10.

Ethics statement for animal and human studies

Not applicable

Data availability statement

The data that support the findings of this study are available from the corresponding author upon reasonable request.