Abstract

This study provides valuable insights into understanding how salesperson behavior, whether technical knowledge (TK) or adaptive selling behavior (ASB), influences a customer’s attitude toward the salesperson (AS). We analyzed the relationships between investment bank customers and the bank in Chile using a cross-sectional sample of 115 customers. Multi-group structural equation modeling (SEM) analyses were performed to test the moderating effects of customer gender and age. The empirical analysis shows that a salesperson’s TK and ASB contribute significantly and positively to AS. Furthermore, there’s a synergistic effect between these two independent factors, indicating a reinforcement effect. The effect of TK on AS is significant for both males and females. In this line, no studies have jointly analyzed the effects of TK and ASB on AS from the customer perspective. About the moderation analysis, this pioneering article finds (1) moderating effects of age in the relationship between TK and AS in magnitude and between ASB and AS, which is significant only in the older customer groups (>50 years), and (2) moderating effects of gender in the relationship between ASB and AS, where it is only significant in female customers that consider relevant the adaptability in the investment context. These results reveal the relevance of aligning salespeople and customer demographic patterns. Therefore, these findings have critical implications for investment banking in developing sales strategies and cultivating customer relationships.

Keywords

Introduction

A salesperson’s actions affect customer attitudes toward said salesperson and the organization (Fergurson et al., 2021). For example, a salesperson’s level of technical knowledge can drive higher sales performance (Groza et al., 2016) and focus effort on suitable activities and customers (Peesker et al., 2022). According to Pousa et al. (2020), sales performance can be boosted when customers receive offers better suited to their needs and perceive that salespeople are genuinely concerned about them. In addition, strong customer loyalty and faithfulness have a positive effect on the customer’s opinions about the enterprise and on passing them to the other groups of stakeholders, which creates a positive reputation (Özkan et al., 2020). In the long term, a positive corporate image is crucial for consumers when purchasing.

For the above reasons, the banking industry requires salespeople to have better problem-solving skills and to provide quality-oriented service (Tseng, 2019). In addition, banks need to strengthen personnel capability and have more trained staff, as frontline employees are critical players in obtaining and retaining customers (Darzi & Bhat, 2018), strategical to balance customer cost acquisition (van der Borgh et al., 2019). Gender diversity has become a relevant factor since team sales and profits increase when the proportion of women increases from low to mid-level (Shin et al., 2023), especially in industries where customer trust in a salesperson is a determinant of a high standard of service (Tosun, 2020; Wijaya et al., 2022).

The banking industry is an appropriate setting to study how the technical knowledge (TK) and adaptive selling behavior (ASB) of the salesperson play a critical role in improving a customer’s attitude toward the salesperson (AS), given the complex nature of financial mechanisms. In this context, it is relevant to denote that attitude refers to a favorable valuation of an assessment of the relationship between the two roles (Bhandary et al., 2023a). Financial advice is an intangible service based on the credibility of the sales agent, their level of financial knowledge, and selling adapted to the customer’s requirements. However, like other industries, digital transformation has affected it, which has driven a change in customer communication patterns by seeking more personalized, faster information, with multi-channel sales and the use of platforms (Giovannetti et al., 2022), especially in the younger segments. These changes require that organizations be able to hire salespeople who already have adaptive resources for each client (e.g., technological knowledge, ability to deal with uncertainty and role conflict, confidence in technologies, and optimism; Guenzi & Nijssen, 2021).

Previous studies have focused on the salesperson’s myriad (Alavi et al., 2019; Kimura et al., 2019). Therefore, the main objective of this research is to explain how TK and ASB influence AS from the customer’s perspective. We also study the moderating effects of customer gender and age on the relationships between these variables as proposed in the conceptual model. Multi-group structural equation modeling (SEM) analyses were performed. Therefore, this article examines all these variables (AS, TK, ASB, gender, and age) together to apply them to the banking industry and confront the challenges of moderating conditions in the context of sales in this industry (Kwak et al., 2019).

This research used a sample of customers of a Chilean investment bank. This industry thus offers an ideal testing condition as the Chilean banking system is widely recognized for its financial strength and high quality of service (Jiménez-Hernández et al., 2019). In addition, Chile is one of the countries in the region with the highest level of financial inclusion, where more than 90% of the Chilean population (over 15 years of age) has access to banking products such as debit cards (Diario Financiero, 2024).

To achieve these research objectives, the following research questions (RQs) are proposed:

RQ1: How do technical knowledge and adaptive selling behavior influence the customer’s attitude toward salespersons in the banking investment industry?

RQ2: How do age and gender moderate the associations between technical knowledge and adaptive selling behavior with customers’ attitudes toward salespersons in the banking investment industry?

This article makes several contributions to the theoretical and managerial perspectives on salesperson effectiveness. First, this study explains how a customer’s perception of a salesperson’s TK affects their AS. Second, this paper focuses on the customer’s evaluation of ASB instead of most of the research on salesperson managers. In this sense, explain how customers’ perception of ASB affects their AS. Finally, this work also studies the effects of TK and ASB on AS, where the customer’s gender and age could influence that. In this way, consider the moderating effect of gender and age on previous relationships.

The rest of the article is structured as follows: Section 2 provides the research’s conceptual framework and hypotheses. Section 3 details the research methodology. Section 4 presents the results. Section 5 discusses our evidence based on theoretical and managerial implications identified in the field. Finally, the article presents the main conclusions and identifies future research avenues.

Conceptual Framework

To develop the hypothesis between the constructs used in this study (salesperson’s technical knowledge, adaptive selling behavior, and customer’s attitudes toward the salesperson) for the proposed, we adopt the theoretical lens of the Knowledge-Based View (KBV), widely applied in sales management literature (K. Y. Chen & Lee, 2017; Paswan & Panda, 2020; Xu et al., 2023). In light of this theoretical approach, knowledge represents a critical source for developing more elaborate and contingent scripts and approaching different events and situations in a sales context, becoming a crucial driver of salesperson performance (Sangtani & Murshed, 2017).

The KBV suggests that knowledge development mechanisms influence the ability of a company to recognize and implement the appropriate management actions to develop effective customer relationships (Yli-Renko et al., 2020). In this way, firms have the role of knowledge generators and incubators for their salespeople (Chowdhury et al., 2022). Consequently, knowledgeable salespeople are more skilled in managing and controlling the experience journey of each customer (Peñalba-Aguirrezabalaga et al., 2021). Accordingly, and in line with this underlying theory, literature shows that knowledge interacts with adaptive-selling theory. Adaptive selling refers to “the alteration of sales behaviors during a customer interaction based on the information and nature of the selling situation.” (Weitz et al., 1986), approaching to fit customers’ needs and preferences (Alnakhli et al., 2020). An adaptive seller can use new information, adjust their selling approach, and tailor their discourse to suit the situation (Itani et al., 2020) and marketplace changes (Hochstein et al., 2019).

Thus, we specifically use this theoretical lens to outline the role of technical knowledge and adaptive selling behavior play in customer attitudes toward salespersons (H1 and H2), considering the moderator effects of age (H3 and H4) and gender (H5 and H6). The model also includes two control variables: customer income and salesperson experience. Figure 1 presents the hypothesized model. In addition, it also includes two control variables: customer income and salesperson experience.

Conceptual model.

Customer Attitude Towards the Salesperson (AS)

In commercial banks, the better the service quality, the greater the customer’s perceived value (Zietsman et al., 2019). In this respect, Janakiraman et al. (2019) point out that customer attitudes toward the salesperson are crucial in determining satisfaction, and salespersons also have an essential role in receiving more robust quality evaluations in service organizations, especially when there is an established relationship with the customer. The salesperson needs to analyze the consumer’s characteristics, be a good listener, understand the customer, and build more personal communication to reduce failures (Nuryakin & Sugiyarti, 2018).

M. Kim et al. (2019) suggest that in this industry, managing customer relationships is part of the role of salespeople. However, it takes time to develop these skills, and salespeople gain the necessary experience in an advanced stage of their careers (Pousa et al., 2017). Chang and Hung (2018) indicate that customers find themselves in a vulnerable position due to the natural complexity of the industry, which requires quality interaction with salespeople who possess practical communication skills to receive and correctly understand the information provided.

Furthermore, even though the banking industry has been changing with the advancement of new technologies, the concept of “personal support,” through the co-creation of value, continues to be a main factor in the quality of customer service, facilitating the positive impacts of the sale (Alnakhli et al., 2021); future behavioral intentions are strongly correlated with customers perceiving empathy and understanding on the part of their bank.

The Effect of TK on AS

Salespeople with more selling skills and knowledge become more market-oriented, which means they integrate “product knowledge” and “customer preferences” to create greater customer value (Y. C. Chen et al., 2018). To understand customer preferences, salespeople must behave like consultants who listen carefully to customers and deliver value-added solutions to address customers’ problems, making them trusted advisors (Itani et al., 2019). Furthermore, listening helps salespeople understand customer differences and vary their sales styles, considering the situation. In addition, the meta-analysis of variables that can predict sales performance by (Verbeke et al., 2010) suggests that a salesperson’s overall knowledge plays a central role in the sales act through their ability to transfer information, especially in adaptive selling, determining performance relationships. In this way, technical knowledge might trigger value creation or moderate the strength of the relationship with customers (Alnakhli et al., 2021).

In this line, salesperson’s knowledge can be structured into declarative and procedural categories, regarding selling context and circumstances (Volpers et al., 2024). The former relates to attribute-based information and recalling relevant facts, while the latter refers to skills in selling tactics, techniques, and strategies (Nguyen et al., 2018). This integration is reflected in their tacit knowledge; and their ability to integrate declarative and procedural knowledge (Leach et al., 2021). Since different knowledge types exist, companies must consider the salesperson’s knowledge level and quality to drive challenges and seek customer solutions to their needs (Epler & Leach, 2021). Groza et al. (2016) further state that a person’s level of knowledge in a selling context can lead to better sales performance. For this reason, they suggest that organizations should increase training programs for their salespeople.

In this line, (Bonney et al., 2022) state that salespeople with specific knowledge can influence or guide customers in their buying decision process. However, in retrospect, Anaza and Nowlin (2017) state that accumulating unnecessary information transforms knowledge from a positive characteristic into an obstacle. This knowledge deficit can explain the lack of flexibility in sales and customer experience (Pappas et al., 2023).

In this sense, today’s dynamic sales environment requires that salespeople possess a high degree of technical knowledge that they can use effectively in their customer relationships (Kalra et al., 2021). Therefore, this study considers several aspects of technical knowledge, such as competitors’ products, services, sales policies, and product lines, including product features, benefits, and knowledge of a company’s procedures. Hence:

H1. TK is positively associated with AS.

The Effect of ASB on AS

Better perceptions of adaptive sales increase satisfaction with the sales staff and suppliers (influencing their loyalty), thus ensuring stability in the buyer-seller relationship (Román & Juan Martín, 2014). In this relational selling context, Shannahan et al. (2017) state that customer-salesperson interactions can reduce uncertainty and co-generate valuable information for the salesperson to improve sales. For this reason, it is essential to consider a salesperson’ ability to develop their potential (Lussier et al., 2021).

Despite the emergence of relational selling as an alternative sales strategy and the growing evidence that relates ASB to better sales performance, it is relevant to consider the different sales situations that salespeople may face. Considering this, managers must learn to coach salespeople properly, as it is crucial to decide on relational versus transactional sales strategies (Autry et al., 2013). Moreover, in an adaptive selling context, the approach employed in a “buying situation” is critical to success, and the relationship length positively affects this context (Amenuvor et al., 2022).

A salesperson’s performance and effectiveness are driven by situational selling context and greater (functional) customer orientation, increasing the captured value (Mullins et al., 2020). The findings of Tseng (2019) were that highly customer-oriented employees can achieve greater customer satisfaction. They said employees’ ability to solve problems since they tend to offer solutions according to client needs. However, users can also assess a salesperson’s performance based on their perception of the established interaction and whether it achieves the objective in the customer’s ecosystem, considering the characteristics of the buying situation (Paesbrugghe et al., 2020). Therefore, the following hypothesis is formulated on the customer’s perception:

H2. ASB is positively associated with AS.

Age as a Moderating Variable

In investment banking, which has a wide and diverse range of customers, the age variable is essential to customer perceived value and behavioral intention during decision-making (Molinillo et al., 2021). Another study evaluating digital payment systems’ financial well-being experiences revealed that customer experience differs based on gender and age categories (Dzogbenuku et al., 2022).

It has been shown that the consumer’s age affects the association between variables related to consumer behavior (Rather & Hollebeek, 2021). A study by Cambra-Fierro et al. (2017) found that older customers are likelier to be loyal. Different age groups have different needs based on their technological profile, eagerness for social connections, expectations, engagement, and relevance in specific industries and/or services (Kamath et al., 2020). Moreover, the results of the research on customer valuation by Rambocas et al. (2018) indicate that satisfaction is more of a switching deterrent for older customers than for younger customers.

In the purchase behavior context, Guan et al. (2022) research reveals how younger consumers garn product information from multiple sources and channels to make their purchasing decisions. Furthermore, the research by Chawla and Joshi (2018) emphasizes the need for compatibility between the banking services offered and a customer’s lifestyle and age in designing suitable services that will meet the specific needs of customer segments. Therefore, the third and fourth hypotheses of this study are as follows:

H3. Age moderates the relationship between TK and AS.

H4. Age moderates the relationship between ASB and AS.

Gender as a Moderating Variable

In line with studies detailing the significant moderating effect of age and gender on consumer intentions, it is essential to understand the influence of gender differences on user interaction (Merhi et al., 2020). In this sense, men are more achievement-oriented than women in their purchases and tend to become easily uninterested, bored, or angry if they spend too much time on the process. Moreover, men are more likely to embrace digital services, while women are more security-conscious (Dzogbenuku et al., 2022).

Women seem more concerned with maintaining relationships than engaging in autonomous interactions. Role Theory predicts that female consumers are keen to preserve relationships with their service providers and that variations in customer satisfaction tend to affect male consumer loyalty more(J. Kim, 2021).

Male consumers want a comfortable experience (in layperson’s terms, less hassle), but women tend to focus on the quality of their interactions with the service’s employees (Teeroovengadum, 2022). In this context, the limited evidence shows that gender strongly moderates the post-sales perception of the customer of the banking service provided (Martins Gonçalves & Sampaio, 2012).

The study by Kamath et al. (2020) shows that customer experience can build strong loyalty among customers, especially male customers. Moreover, men are more inclined to use new payment technologies (Kalinić et al., 2020). However, for female customers, the quality of interaction with their bank significantly predicts their satisfaction (Teeroovengadum, 2022). Considering this evidence, it becomes interesting to analyze their role in the context of technical knowledge and adaptive selling. Hence:

H5. Gender moderates the relationship between TK and AS.

H6. Gender moderates the relationship between ASB and AS.

Methodology

Questionnaire Development and Measurement Scales

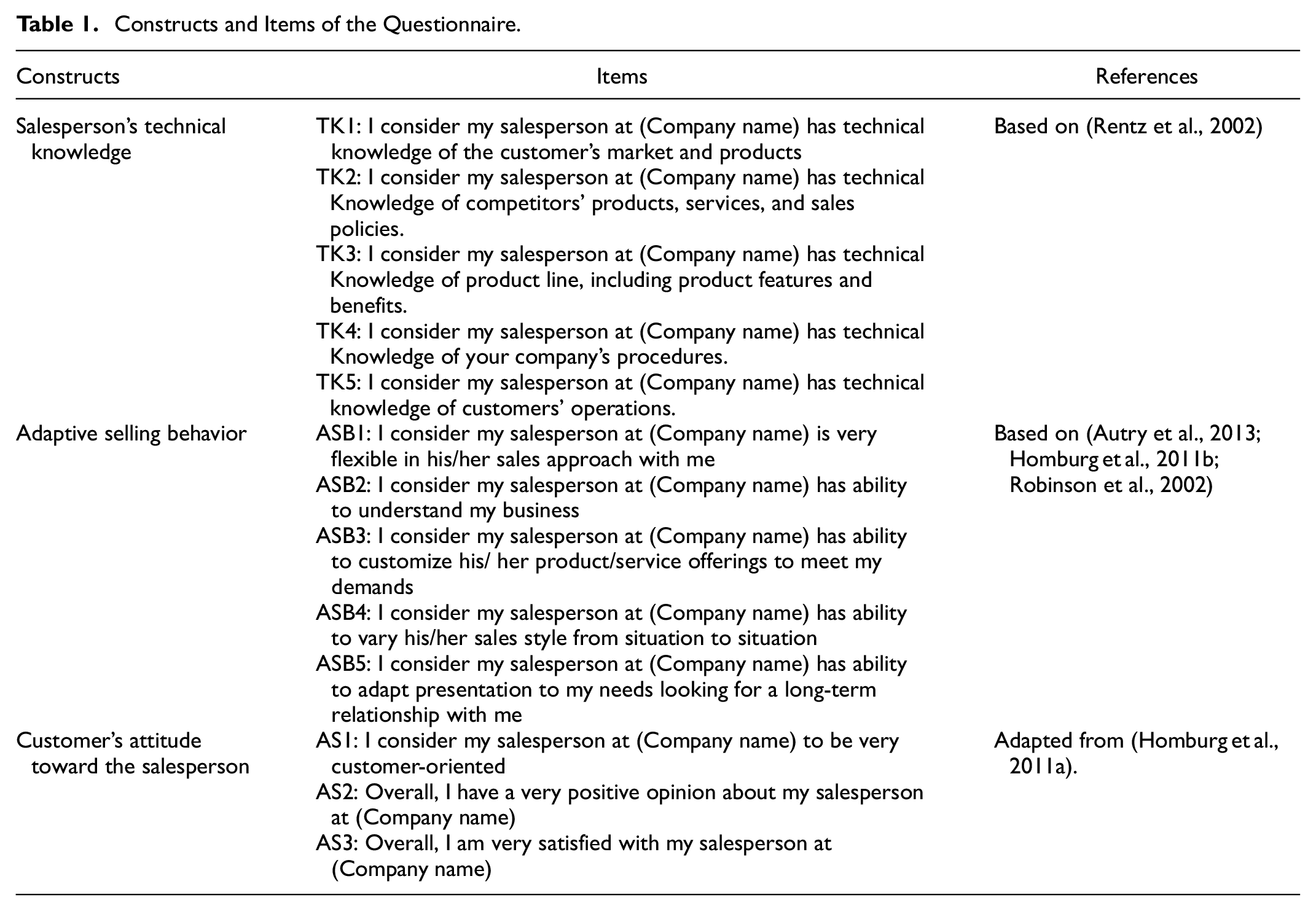

The original scale was designed as a unit measure for salespeople. The terms were changed for customer response. This procedure resulted in a rephrasing of the items compared to the original scales. Salesperson’s technical knowledge refers to the adaptability and selling skills to predict objective performance. TK was measured by three items adapted from (Rentz et al., 2002). Adaptive selling behavior focuses on the resources-based allocation of the customer value to the firms that sell goods and services. ASB was measured through five items adapted from (Autry et al., 2013; Homburg et al., 2011b; Robinson et al., 2002). Customer attitudes toward salespersons consider the salesperson’s attitude, satisfaction, and commitment. AS was measured by three items from (Homburg et al., 2011a). Respondents expressed their attitudes and opinions regarding the questions and sentences on a 7-point Likert scale (1 = completely disagree; 7 = completely agree). See Table 1.

Constructs and Items of the Questionnaire.

Data Collection

The data in this study were obtained from clients of a Chilean investment bank. In this sense, the selected bank customers possessed a level of seniority and familiarity with investment products, as they had maintained a business relationship with the bank for at least 5 years, differentiating from regular bank customers. The customers and individuals utilizing the bank’s standard products were subjected to the same stimuli to ensure consistency. Considering this filter, the survey was distributed to 2,569 bank customers, resulting in a final response rate of 6.58% (169 individuals). Nonetheless, the sample size was reduced to 115 participants who provided comprehensive data and exhibited a minimal standard deviation to minimize potential biases. The respondents were fully aware that their participation was strictly for academic purposes, and each participant signed a Confidentiality Agreement to ensure the privacy of their responses. The customers’ ages ranged from 18 to 65, with an average age of 48.6, a median of 48, and 59.1% were male. 54.2% of respondents had more than 5 years of tenure with the bank. The sample characteristics are depicted in Table 2.

Characteristics of the Sample.

Statistical Analysis

The hypothesized model was tested using structural equation modeling via covariance-based SEM (CB-SEM) using AMOS 26 software, a tool based on this approach (Dash & Paul, 2021). CB-SEM is a covariance-based procedure that considers the constructs as common factors that explain the covariation between their associated indicators (J. F. Hair et al., 2021), considering a minimum range of 5 to 10 observations by item for the measurement (J. Hair et al., 2010). This procedure determines the model parameters to reproduce an empirically observed covariance matrix (Reinartz et al., 2009). In this way, CB-SEM is the appropriate method when the research objective is theory testing and confirmation of assumed relationships, instead of PLS-SEM, which is more suitable when the purpose is prediction (Dash & Paul, 2021). CB-SEM is more stringent than PLS-SEM and adequate for descriptive models (Zhang et al., 2021). Thus, CB-SEM is suitable to analyze the hypothesized model of this study, considering (1) the objective to confirm the hypothesized relationships from a theoretical standpoint, (2) is a descriptive model, (3) the model complexity (i.e., it involves 11 items for three constructs), and (4) the sample size (achieving the required range of observations). Furthermore, the analysis included multi-group SEM to examine the potential moderator role of age and gender.

Results

Measurements Assessments of the Variables

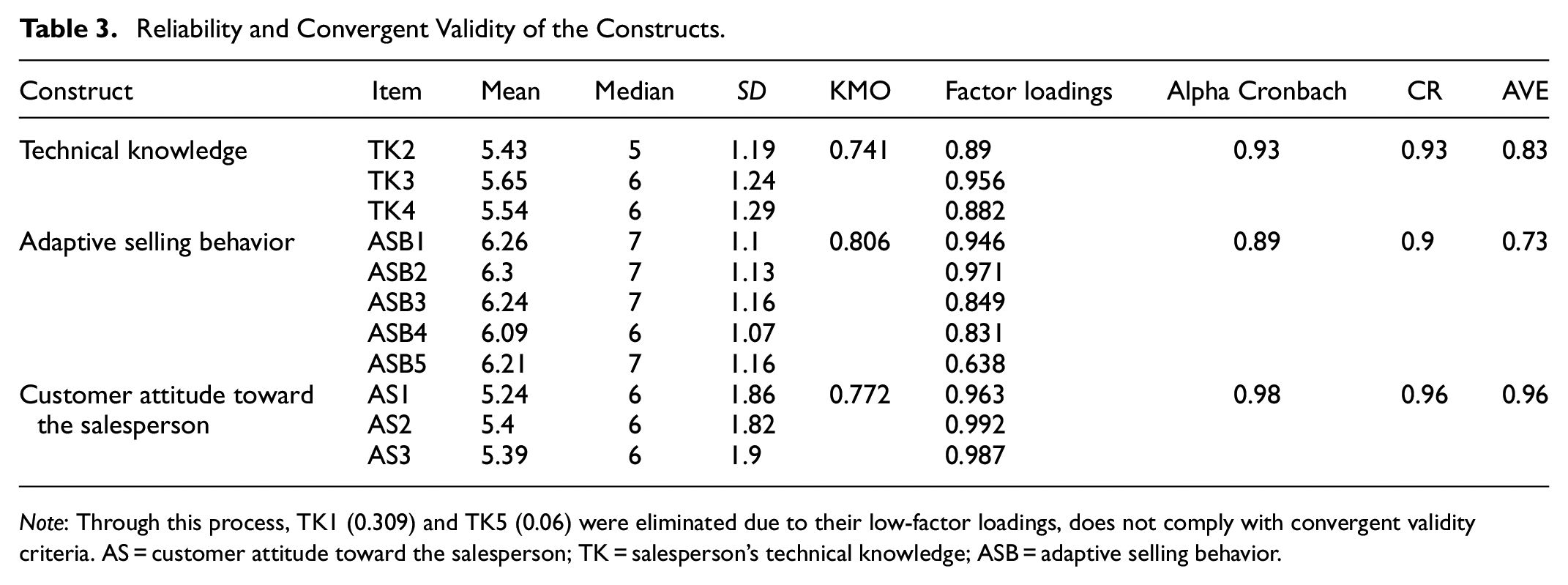

The variables measurements consider the basic central tendency (mean and median) indexes and variability (standard deviation). To assess the reliability of the measured constructs, consider the construct reliability. The reliability of the constructs was measured using Cronbach’s alpha (α) index (range from 0 to 1) and composite reliability (CR) values. Both measures present values higher than the threshold value of 0.7, denoting good reliability and supporting the convergent validity of the constructs (J. F. Hair et al., 2017). To assess the convergent validity, including the standardized factor loading (on their respective constructs). The obtained values were higher than the 0.5 thresholds, and the convergent validity of the constructs was supported (Fornell & Larcker, 1981; J. F. Hair et al., 2017). Finally, as a summary indicator of convergence, AVE values were higher than the threshold value of 0.5, supporting the convergent validity (see Table 3).

Reliability and Convergent Validity of the Constructs.

Note: Through this process, TK1 (0.309) and TK5 (0.06) were eliminated due to their low-factor loadings, does not comply with convergent validity criteria. AS = customer attitude toward the salesperson; TK = salesperson’s technical knowledge; ASB = adaptive selling behavior.

Discriminant validity was estimated to ensure the measures’ adequacy of the constructs using the Fornell-Lacker criterion (Shiu et al., 2011), comparing the square root of the AVE of constructs with the bivariate correlation among the constructs. According to Table 4, discriminant validity was supported (correlation values are less than the AVE square root for each construct).

Discriminant Validity Using the Fornell-Lacker Criterion.

Note. Bold values indicates the square root of each construct AVE (represented in the diagonal) is greater than the correlation with any other construct, establishing the discriminant validity.

In addition, the heterotrait – monotrait (HTMT) ratios are less than 0.629 (see Table 5), less than the threshold of 0.85 (Henseler et al., 2015). Therefore, the discriminant validity has been reached through these measures.

Discriminant Validity Using Heterotrait – Monotrait (HTMT) Ratio.

In reviewing the questionnaire, it was important to rule out the presence of Common Method Bias (CMB). Common Method Variance (CMV) was evaluated using the Harman single-factor test, which resulted in a variance value of 48.08%. When the percentage is below 50%, there is no CMB in measuring the research indicators (Pangarso et al., 2020). We also used the Common Latent Factor (CLF) to determine whether a common factor could significantly influence the results (Podsakoff et al., 2003). Even after applying the CLF, the results indicated that the CR and AVE scores were sufficiently strong for each construct. In addition, the CLF showed differences below 0.2 (AS = 0.13; TK = 0.14; ASB = 0.18), so the CMB did not significantly affect the measurement model. In addition, we estimate the variance inflation factor (VIF) to evaluate the presence of multicollinearity. The highest score was 1.048, which is far below the suggested threshold of 5 (O’brien, 2007).

Confirmatory Factor Analysis (CFA) was used to check the validity of the measurement model developed in the previous section. The

Hypotheses Testing

The influence of TK on AS is positive and significant (β = .626, p-value < .01, see Figure 2). Additionally, the results for the effect of ASB on AS showed a positive and significant relationship (β = .118, p-value < .01), thus supporting H1 and H2. Finally, the effect of interaction between TK and ASB was slightly positive and significant (β = .130, p-value < .01). The model also used the customer income variable and salesperson experience as control variables. The first of such variables was to discard any effect from the economic situation, while the second of those variables discarded the effect of bias from the salesperson’s characteristics. Neither variable was significant.

General model.

The Moderating Effects of Age

Three groups (18–34 years, 35–50 years, and older than 50 years) were selected to analyze the role of age as a moderating variable in the measurement model. The effect of age on the model’s two independent variables was estimated by comparing the β coefficients in the subsamples (see Figure 3). Consequently, statistical differences between the groups can be seen.

Age effect on proposal model.

TK was significant in the three groups. Nevertheless, its weight in the older group (β = .378) was significantly lower in comparison to the other groups (βs ≥ 0.576). The age variable for ASB was only significant in customers above age 50, indicating the variable’s relevance for this group. The results thus suggest that the ASB only influenced the sample’s older people (β = .334) and that TK was less relevant in said group (β = .378). Considering the concept of Hayes and Montoya (2017), where a moderating variable can modify the relationship between two variables (strengthening, weakening, or reversing relations). Based on the results obtained in this study, H3 and H4 are supported by the data. These results are in Figure 3; details are provided in Tables 6 and 7.

Invariance Analysis of Age.

Significance of the Age Moderator.

Note. TK = salesperson’s technical knowledge; ASB = adaptive selling behavior.

The Moderating Effects of Gender

Two groups (male and female) were selected for the measurement model to test the moderating influence of the gender variable in the model. Then, an invariance analysis revealed a relevant difference between the groups, expressed in the following values:

The effect of gender was estimated using the β coefficient to compare the subsamples (see Figure 4). TK is significant for both groups, with a slightly higher value for men (β = .669) than for women (β = .611), so there were no significant differences between the two groups. The effect of ASB on AS was not significant in the male group compared to the female group, where it was significant and had a positive value (β = .134). Therefore, these results disprove H5 but support H6. See Figure 4 and Tables 8 and 9 for further details. Table 10 provides a summary of supported and disproved hypotheses.

Gender effect on proposed model.

Invariance Analysis of Gender.

Significance of the Gender Moderator.

Note. TK = salesperson’s technical knowledge; ASB = adaptive selling behavior.

Summary of Results.

In summary, H1 and H2 are supported, exhibit the relevance of technical knowledge and adaptive selling behavior to generate a favorable customer attitude, and are the foremost step to cultivating effective relationships. The results of moderation analysis show that age moderates the relationships between TK and ASB with AS (supporting H3 and H4), revealing the differences in their valuation. In the case of gender, there are observed differences in their moderator role. In the relationship between TK and AS, gender does not moderate this relationship, showing an equal relevance (disproving H5) exhibiting the transversality relevance of technical knowledge in this industry. In contrast, gender does moderate the relationship between ASB and AS, becoming significantly only for the female group, presenting as a crucial characteristic in the customer-salespeople relationship.

Discussion

Theoretical Contributions

This article provides valuable theoretical contributions to the literature by generating knowledge about the customer attitude toward salespersons, evaluating the role of technical knowledge and adaptive selling behavior of salespersons, relevant and essential for the design of customer experience in services (Fergurson et al., 2022) and understand their pivotal role in the investment-focused banking industry. Specifically, this research shows that technical knowledge’s direct effect on customer attitudes toward salespersons is significant in the evaluated context. Previous research in the banking service context suggests that salesperson attributes contribute to contact frequency and client knowledge, augmenting sales effectiveness and longstanding customer relationship (A. Shetty & Basri, 2018), supporting H1.

More specifically, some scholars consider that salespeople are the brokers’ knowledge of complex goods and services, influencing customer learning (Bonney et al., 2022). Accordingly, this research contributes to the adaptive-selling theory, which has shown that adaptive selling behavior is indispensable if companies want to obtain positive customer attitudes toward salespersons in the investment banking industry. The H2 result is consistent with previous research that evidences the direct and positive effects on customer’s perceptions of satisfaction with the product, developing relational-based selling (Ramos et al., 2023) and positive valuation (Bateman & Valentine, 2021), always that adaptive selling behavior has a knowledge focus and not an improvisational orientation (Charoensukmongkol & Suthatorn, 2021). These findings reinforce the central role of these variables within the context of the investment banking industry, where the customer has higher technical demands (Tosun, 2020), considering the knowledge-based view perspective.

This article includes age and gender as moderators of the investment banking industry. These variables provide empirical evidence about the factors that influence customer perceptions of salespersons’ knowledge and adaptive selling behavior. Age plays an important moderating role in the relationships between TK and ASB with AS, within the realm of investments. The results show that age moderate TK effects on AS between the three groups (18–35 years, 35–50 years, and >50 years). Specifically, the weight attributed to the younger groups (≤50 years) is significantly higher compared to the weight assigned to the older group (>50 years), supporting H3. Overall, the outcomes imply that TK holds the potential to enhance AS more effectively among younger customers. This result is consistent with the study by Guan et al. (2022), which found that younger consumers spend time and effort actively seeking more information from different sources to make their purchasing decisions. Younger customers requesting more information and accessing a more significant number of information sources may need salespeople with a higher level of TK. Customers value the guidance of salespeople about the products, where the given data reveals their level of expertise and knowledge (Arditto et al., 2020) and competence (Høgevold et al., 2021). In addition, the moderation analysis determined that the effect of ASB on AS is only significant among clients over 50 years of age, supporting H4. This result emphasizes that learning about the relationship between types of customer needs and sales encounters is more effective in adaptive selling employment (Alavi et al., 2019; Ryari et al., 2021). In addition, this perception of a salesperson’s adaptive selling behavior influences the quality of customer experience and the possibility of building strong loyalty (Kamath et al., 2020), considering the complexity of customer characteristics (Habel et al., 2021).

The gender variable presents another theoretical contribution of this research where gender positively moderates the relationship between ASB and AS in the female gender group, supporting H6. The need for adaptive support from salespeople to technical customer needs can explain this finding (Teeroovengadum, 2022), considering the financial resources involved in this industry. In addition, it must be noted that there is an increased level of female participation in acquiring banking-related products tailored to their preferences and needs (Hendriks, 2019) and more sensitivity to knowledge stimuli (Zhou & Charoensukmongkol, 2022). In contrast, the situation is quite different when analyzing gender’s moderating effect on TK. Their effect is significant and similar between the two gender groups (male and female). One possible explanation for this is the similar level of importance the groups assigned to the credibility and trust in the banking institutions (Kalinić et al., 2020), disproving H5.

Additionally, when the industry has technical characteristics, customers tend to have prior experience and knowledge, regardless of gender (Merhi et al., 2020). This result is particularly true for decisions on long-term investments. Therefore, through the hypothesized model, this research provides a complete overview of how TK and ASB affect AS in the investment banking sector, pioneering this theoretical statement.

Managerial Implications

This research makes valuable contributions to empirical evidence by testing the model using the customers of a Chilean bank focused mainly on investments. The Chilean banking system is widely recognized for its well-established reputation for financial stability, advanced technological integration, and quality of service. Consequently, an important managerial implication that surfaced from this research is the need for managers to reassess the relationship between customer-oriented salespeople and their customers. The salespeople must increase TK and ASB (which affect the customer’s attitude toward the salesperson) to close a sale effectively.

In conclusion, companies should maintain long-term relationships with valued customers to ensure profitability, where salesperson adaptation to clients’ needs is crucial to nurturing a long-term customer-company relationship (Omoregie et al., 2019). In this line, salespersons with a high level of TK are more likely to develop more sophisticated courses of action in a sales context. So, a more knowledgeable salesperson will attain better results in complex situations. Kwak et al. (2019) point out that sales managers who use an ASB sales strategy must pay attention to how much and what type of adaptation and training is required because this will eventually make a difference and affect performance. Effective listening skills help the salesperson to adapt better to different sales situations and add value to the transaction. This aspect is decisive since client knowledge of the banking industry influences the degree of interaction intensity and satisfaction with their bank (Herjanto & Amin, 2020).

Management should focus on having a workforce with strong customer skills to be better prepared to face service failures. For example, the sales performance of customer-oriented salespeople with an ASB is superior (Pousa et al., 2020). Organizations should implement salesforce strategies focusing on providing service and generating sales to develop salesperson ambidexterity. According to the research of Agnihotri et al. (2017), salesperson ambidexterity had an impact on both adaptiveness and role conflict.

The results of this study suggest fostering positive customer attitudes is influenced by gender and age, and it is more important to monitor and encourage salespeople to develop TK among younger customers. Conversely, the results suggest monitoring and encouraging salespeople to develop ASB among female and older customers. These findings underscore the need to adapt salespeople strategies according to the specific characteristics of their customer base.

Conclusions

Key Takeaways

This article analyzes the influence of salesperson’s technical knowledge and adaptive selling behavior on customer attitudes toward salespersons using the CB-SEM method through AMOS software. This research attempts to provide an overview to help the investment banking industry identify how to approach the sales process effectively with their client portfolios. From a conceptual standpoint, the study highlights the relevance of technical knowledge in salespersons, reflected in their intellectual capabilities and expertise (Bhandary et al., 2023b) about financial products and services and the adaptive selling relevance on technical industries (Charoensukmongkol & Suthatorn, 2021) like investment banking. These factors are substantive and must be developed by financial institutions, considering their relevance to customer perceptions in aspects such as loyalty (B. Shetty et al., 2018). In addition, this research illustrates the role of age and gender in these relationships, influencing the quality of information and service perceptions (Molinillo et al., 2021)Therefore, the outcomes of this research could potentially help investment banking industry managers concentrate their efforts on developing sales strategies based on technical formation and sales encounter training to address different types of customer needs and requirements.

Limitations and Future Directions

This study has some limitations. First, this research uses a sample from customers of a banking organization specializing in long-term investments in Chile. Generalizations might be limited because self-reported surveys may generate results higher or lower than reality in this industry (Dandis et al., 2021). Second, the product analyzed is standard and needs a consultative sale where the salesperson’s knowledge is relevant in advising the client on the best investment alternatives according to their profile. Third, this study does not consider the personality of the salespeople, emotions, or stress, which can influence their capabilities and the client’s perception of a salesperson. Fourth, as concerns the findings of this study, incorporating variables such as trust and customer engagement can be highly valuable in expanding customer behavior understanding (Park & Tran, 2018). Finally, to begin generalizing the research results, the effects caused by cultural differences and the realities of other industries and countries must be analyzed and examined, for example, local management practices (Onyemah et al., 2021).

Footnotes

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.

Ethical statement

Ethical review and approval of this study were waived because express consent was obtained from the participants and approval was obtained from the collaborating universities in this study. Respondents are aware that the data is used exclusively for academic purposes. In turn, each participant had to read the reason for this research and then confirm their participation and consent.

Data Availability Statement

Data sharing not applicable to this article as no datasets were generated or analyzed during the current study.

{kind=link}

{kind=link}