Abstract

This study examines how financial constraints and total assets affect the corporate bankruptcy risk of listed firms in Vietnam. Specifically, we test whether larger firms are less financially constrained and have lower distress risk subsequently. This study employs the dynamic system Generalized Method of Moments to analyze an unbalanced sample of 1,990 firm-year observations from 2010 to 2019. The results indicate that larger firm size increases the Z-score index, implying that larger firms have lower bankruptcy risk. Our finding also reports that financial constraints reduce the Z-score index, suggesting that financially constrained firms have extremely high bankruptcy risk. Our findings also show the inverted U-shape relationship between financial constraints and distress risk. Our results support the too-big-to-fall theory, the trade-off theory, the agency theory, and prior literature. Finally, our study contributes practical implications for managing bankruptcy risks in emerging markets.

Introduction

Distress risk happens when firms have inadequate cash flow available to pay their creditors or if their liabilities exceed their assets (He et al., 2023). Corporate default risk can affect financial stability and the macroeconomy (Zhang et al., 2020) because financial sustainability is essential in measuring institutions’ survival and development. Altman (1968) developed the Z-score index to predict the possibility of corporate insolvency. This index can predict with up to 94% accuracy whether a sampled company will file for bankruptcy over the next 2 years. Altman (1968) indicated that all firms with Z-score scores greater than 2.99 do not go bankrupt in the next 2 years. Firms with a Z-score lower than 1.81 have serious distress risk within the next 2 years.

Recent literature reports mixed impacts of financial constraints on default risk. Musso and Schiavo (2008) argue that financial constraints increase the distress risk. Duong et al. (2022) report a causality between financial constraints and distress risk. Specifically, a higher distress risk leads to higher financial constraints, not the other way around. Chauhan and Banerjee (2018) indicated that highly leveraged firms are more vulnerable to failure, primarily when a financial shock occurs. Trade credit increases the probability of bankruptcy because trade creditors are frequently less eager to extend new loans to their clients during an economic downturn. Wahyudi (2014) suggests that an increase in leverage would be followed by default risk in financially constrained firms (Cai & Zhang, 2011). In addition, Yu et al. (2021) suppose that financing constraints mainly refer to businesses’ external financial friction while seeking external financing support. Credit-constrained businesses may be pushed to employ riskier and more expensive external financing, such as trade credit or credit cards, which raises the likelihood of default (Xu et al., 2022).

In addition, the previous studies reported the negative impacts of firm size on default risk, which supports the too-big-to-fall hypothesis. Darrat et al. (2016) demonstrated that larger companies might have the strength and capacity to bargain to prevent bankruptcy. Similarly, Dirman (2020) reports that more prominent firms are more likely to withstand challenging conditions and avoid insolvency. Zhu et al. (2021) report that larger firm size has protection against financial risk because larger firms can access external financing more easily than smaller firms.

However, the financial constraints may vary across firm sizes. Prior studies only considered the linear impact of financial constraints on default risk (Darrat et al., 2016; Komera & Lukose, 2014; Schwarz & Pospíšil, 2018; Yu et al., 2021) or the impact of firm size on default risk (Bhagat et al., 2015; Darrat et al., 2016; Zhu et al., 2021). Prior studies only focus on the relationship between financial constraints and bankruptcy in developed and emerging markets (Musso & Schiavo, 2008; Xu et al., 2022; Yu et al., 2021). Therefore, this study is the first to examine the nonlinear effect of financial constraints and firm size on default risk in Vietnam.

Besides that, previous studies used the pooled OLS method (Baghdadi et al., 2020; Bhagat et al., 2015; Dodoo et al., 2021) or simulated maximum-likelihood approaches (SML) to the estimation of the logit/probit regression models (Komera & Lukose, 2014; Wahyudi, 2014; Zhang et al., 2020) to test the impact of financial constraints and total assets affect default risk. This study closes the prior literature gap because it follows Appiah et al. (2023) to employ a two-step dynamic System Generalized Method of Moment (GMM). GMM method is more efficient than OLS (Greene, 2005) and SML (Inkmann, 2000) because it overcomes possible heteroscedasticity, omitted variables bias, and endogeneity issues. Finally, this study extends prior literature because we provide a robustness test in different consumer discretionary, consumer staples, industrial, and materials sectors.

This study is conducted in Vietnam because of the following reasons. Firstly, Vietnam is a frontier market with rapid growth and different market microstructures than emerging and developed nations. The Vietnamese economy has transitioned from a centrally planned system to a more market-oriented one (Vo & Bui, 2016). In addition, over 90% of Vietnamese firms are small firms with charter capital of less than 500,000 USD. These firms may consequently have higher financial constraints to accessing external capital than large firms (Nguyen & Kien, 2022), leading smaller firms to have higher distress risk.

Furthermore, the number of distressed firms surged significantly in Vietnam because of business disruptions during the Covid-19 pandemic. In particular, 101.7 thousand businesses were temporarily suspended and dissolved in 2020. Vietnam has 41.8 thousand enterprises exiting the market, particularly in the first 4 months of 2020, representing the highest number of bankruptcies in the last 10 years. This bankruptcy rate of businesses in Vietnam is extremely high, particularly during the Covid-19 pandemic (Duong et al., 2022). Our descriptive statistics report that the median Z-score of listed firms in Vietnam is 2.080, implying that distress risk among listed firms in Vietnam is apparent.

Our sample is an unbalanced panel with 1,990 firm-year observations, including all manufacturing firms listed on the Vietnam stock market’s Ho Chi Minh Stock Exchange (HOSE) and Hanoi Stock Exchange (HNX) from 2010 to 2019. We follow Altman (1968, 2013) to measure bank ruptcy risk (Z-score). We also follow Chan et al. (2010) and Duong et al. (2022) to calculate financial constraints (AKZ and Z_FC) and firm size (SIZE). We follow Duong et al. (2023) and Tran et al. (2023) to perform the dynamic system Generalized Method of Moments (GMM) to estimate the findings.

Our study generates the following remarkable findings. Firstly, empirical findings show that financially constrained firms have higher bankruptcy risks. When the financial constraint index increases by one point, the Z-score reduces to 1.33 scores. These firms must employ more expensive external financing options to raise capital. Moreover, financially constrained firms have less protection against economic shocks, which raises the likelihood of default. The result is consistent with Musso and Schiavo (2008), Xu et al. (2022), and Yu et al. (2021) and consistent with the trade-off theory and hypothesis 1.

Secondly, our finding indicates an inverted U-shaped relationship between financial constraints and default risk in Vietnam. Firms with lower operating cash flow, little cash, and a high leverage ratio encounter more financial constraints (Chauhan & Banerjee, 2018). These financially constrained firms also have increased the probability of defaults (Xu et al., 2022). However, when firms are excessively constrained, managers cannot access external debts to finance risky investments. Therefore, these firms must rely on internal resources rather than external debts so they have lower bankruptcy risks. Besides, managers avoid risky projects and non-value-adding activities to protect shareholders from potential asset depletion. Our finding supports the pecking order theory, agency theory, and hypothesis 2.

Thirdly, this study also shows that larger firms have lower default risk. Specifically, a percentage increase in the firm size increases the Z-score by 0.71% points, implying lower default risks. More prominent organizations are more likely to face challenging conditions, and the higher the company’s overall assets, the greater the potential to pay off corporate commitments in the future, allowing the company to avoid bankruptcy risk. Darrat et al. (2016) demonstrated that larger companies might have the strength and capacity to bargain to prevent bankruptcy risk. Therefore, our findings support hypothesis 3 and the too-big-to-fail theory.

Finally, we use the robustness check to ensure financial constraints and firm size on default risk are still robust when following Chan et al. (2010) using an alternative financial constraints index calculation (Z_FC) instead of AKZ. Thus, our study also follows Sayari and Mugan (2017) to test in different sectors. Although increased financial constraints may increase the likelihood of default risk for particular industry groups, such as Industrials and Services, it may reduce it for Consumer Staples. Our research also reveals a robust nonlinear relationship between financial constraints and default risk in Consumer Staples.

Our results provide practical policy implications to reduce the distress risks in emerging markets. Firstly, small and medium firm managers must clearly understand cash flow management and create an optimal capital structure to minimize distress risk. This will allow them to effectively increase leverage to support business growth and establish stable financial operations. In addition, managers must also develop risk management policies for firms, especially during economic downturns or periods of financial uncertainty. Finally, the Vietnamese government should prioritize the liquidity of listed companies by providing them with various financing options for easier access to capital, and the government can promote access to financing by expanding loan guarantee programs to encourage banks to lend to SMEs backed by government guarantees in case of default.

The remainder of the research is described below. Section “Literature Review” is a literature review; Section “Data and Methodology” is about data and methodology; Section “Empirical Results” provides empirical results; Section “Discussion” is the discussion and robustness tests; and Section “Conclusion and Recommendation” is the conclusion and recommendation.

Literature Review

Theories

According to the static trade-off theory, firms have optimal capital structures that they determine by balancing the costs and benefits of using debt and equity. One of the advantages of using debt is the benefit of a debt tax shield. One of the drawbacks of debt is the cost of potential financial distress, mainly when the firm relies on excessive debt. Managers must make a trade-off decision between the benefits of tax shields and the increasing financial distress risk. However, there are additional costs and benefits to using debt and equity. Agency costs are another significant cost factor. Agency costs result from conflicts of interest among the firm’s stakeholders and former information asymmetries (Jensen & Meckling, 1976). As a result of incorporating cost into the static trade-off theory, a firm determines its capital structure by balancing the tax benefits of debt against the costs of financial distress associated with too much debt and the costs of financial distress against the agency cost of equity.

The pecking order theory proposes that companies primarily rely on internal sources of financing before resorting to external funding. Almost all businesses have cash and short-term investments in internal funds; even when raising funds from outside, they prefer debt financing over equity financing. This may be at greater risk of bankruptcy if they encounter financial constraints because excessive debt can lead to high-interest payments and debt service obligations that strain a company’s cash flow, making it more vulnerable to bankruptcy if it cannot meet these obligations. Therefore, these excessively financially constrained firms have lower bankruptcy risk (Komera & Lukose, 2014).

In addition, agency theory argues that shareholders delegate management responsibilities to managers, expecting them to maximize firm profits for shareholders. However, managers have personal objects that may not align with shareholders’ interests (Jensen & Meckling, 1976). As a result, increasing assets will encourage managers to increase personal benefits, which raises the enterprise’s default risk. However, some managers also expect to maximize profits for firms, increase assets to provide sources to boot development and decrease financial constraints and default risk.

At the same time, the “too big to fail” principle supposes that more prominent firms have a more diversified business and multiple financing channels than small firms. Larger companies might have the strength and capacity to bargain to avert bankruptcy (Darrat et al., 2016).

Financial Constraints and Bankruptcy Risks

Chan et al. (2010) determined intuitive features that portray a high-value, financially constrained firm as having a low operating cash flow, paying low dividends, having little cash in hand, being highly leveraged, and having good investment opportunities. Musso and Schiavo (2008) find that financial constraints will impact default risk, increasing the probability of exiting the market for French manufacturing firms from 1996 to 2004. Chauhan and Banerjee (2018) focused on emerging markets and used leverage, likely a financial constraint in Indian manufacturing firms between 1993 and 2015. They indicate that firms having a high debt ratio pay higher interest rates due to riskier and more financial constraints (Musso & Schiavo, 2008). In addition, Yu et al. (2021) suppose that financing constraints mainly refer to difficulties accessing external financing in Chinese listed firms from 2001 to 2017. Credit-constrained businesses may be pushed to employ riskier and more expensive external financing, such as trade credit or credit cards (Xu et al., 2022), which raises the likelihood of default.

However, other studies report an inverse relationship between financial constraints and default risk. For instance, Komera and Lukose (2014) used logistic regression to examine the effects of firm-level financial constraints on the bankruptcy probabilities of 1,185 firms in India from 1992 to 2009. The results indicate a negative association between financial constraints and corporate bankruptcy risk. Under conditions of uncertainty and gloomy economic prospects, financially constrained firms often limit borrowing to minimize the corporate default risk. Schwarz and Pospíšil (2018) report that firms that filed for bankruptcy were not financially constrained before the 2008 financial crisis from 2006–2011 in the Czech Republic. Financially constrained companies must seek external funds and bear high financing costs, so interest rates positively relate to a firm’s default probability. However, another perspective of high short-term interest rates indicates that most firms are in a “fast-growing regime” with a low default probability. Moreover, Sayari and Mugan (2017) show the diverging impact of industry characteristics on firms and financial distress risk in the US market.

In difference from prior studies examining the relationship between financial constraints and bankruptcy in developed and emerging markets (Musso & Schiavo, 2008; Xu et al., 2022; Yu et al., 2021), there is no study investigating the impact of financial constraints on default risk, especially nonlinearity relationship of financial constraints on bankruptcy risk in frontier countries such as Vietnam. Therefore, the literature gap motivates us to research financial constraints’ impact on the default risk of firms listed in Vietnam and propose the following hypothesis:

Hypothesis 1: There is a positive relationship between financial constraints and bankruptcy risk.

Based on the mixed effects from previous studies establish a favorable association between financial constraint and bankruptcy risk (Musso & Schiavo, 2008; Xu et al., 2022; Yu et al., 2021), while other studies report a negative relationship between them (Komera & Lukose, 2014; Schwarz & Pospíšil, 2018). We conjecture that financial constraint has a threshold which, at that point, the financial constraint will decrease or increase. Therefore, we propose the following hypothesis.

Hypothesis 2: There is a nonlinear relationship between financial constraints and bankruptcy risk.

Firm Size and Bankruptcy Risks

Studies have shown that the evidence demonstrates a negative nexus between firm size and default risk. This finding supports the too-big-to-fall thesis, which presupposes that prominent firms have a more diversified company and many financing channels than tiny firms. Darrat et al. (2016) indicate that larger organizations can prevent bankruptcy by using their strength and capability to bargain. Luu Thu (2023) and Zhu et al. (2021) claim that the likelihood of a company experiencing financial distress decreases as the size of the company grows. This is because larger organizations have protection against the possibility of experiencing financial distress since larger firms are more transparent and have easier access to external finance than smaller enterprises. Zhang et al. (2020) suggested that smaller firms have higher default risk. However, large firms with more outstanding cash holdings can mitigate their default risk as they are unconstrained (Chan et al., 2010). Holding extra cash is a cushion to withstand future losses from the default. Dirman (2020) asserts that more prominent companies are more likely to endure trying circumstances and that the greater the total assets owned by the company, the greater the ability to pay off corporate obligations in the future, thereby enabling the company to avoid experiencing financial distress.

On the other hand, the size of the company has a positive impact on bankruptcy risk. Idrees and Qayyum (2018) discovered a greater chance of distress risk when firm size grows due to the presence of levered shares. Notably, an increase in firm size in asset base could be linked to debt-financed development beyond a trade-off between tax shield and bankruptcy-related costs, thereby increasing distress risk. Larger enterprises have more excellent debt ratios and are financially leveraged than smaller firms, which are more likely to be distressed. Oktasari (2020) indicates that the smaller the size of the company, the greater the tendency to experience financial distress because smaller companies tend to have more growth opportunities and, consequently, are more likely to face conflicts of interest between the principal and the agent. Consequently, smaller companies borrow more money to lower their agency cost of debt.

Hypothesis 3: A negative relationship exists between firm size and bankruptcy risk.

Data and Methodology

Data

We gathered the financial statements from Fiinpro and CafeF, prominent data providers in Vietnam. We follow Duong et al. (2022) to exclude companies with missing accounting and financial data. This research follows Altman (1968) in examining the bankruptcy risk of listed manufacturing firms. We also follow Duong et al. (2022) to eliminate observations with insufficient data to calculate variables and winsorize all variables at the 5% and 95% levels to minimize extreme values bias. Our data sample starts from 2010 to avoid the immense impact of the 2008 financial crisis, which may cause estimation biases. The final sample is an unbalanced panel with 1,990 firm-year observations, including 335 manufacturing firms listed on the Ho Chi Minh Stock Exchange (HOSE) and Hanoi Stock Exchange (HNX) from 2010 to 2019.

Variable Definitions

Dependent Variable (Bankruptcy Risk)

Numerous prior research provides various definitions of default risk. Singh (2023) claims that default risk is the inability of a firm to pay its maturing liabilities. He et al. (2023) state that default risk occurs when a firm has insufficient cash flow to pay the debt or liabilities exceed assets. Zhang et al. (2020) explain that corporate default risk can erode financial stability and the macroeconomy. To predict the potential of default risk or firm insolvency, Altman (1968) proposed the Z-score Model, where firms with Z-scores higher than 2.99 are unlikely to go bankrupt, and those with Z-scores lower than 1.81 have a high risk of bankruptcy within the next 2 years.

Independent Variable

Financial constraints (AKZ): Priors studies show a positive relationship between financial constraints and bankruptcy risk (Musso & Schiavo, 2008; Xu et al., 2022; Yu et al., 2021), while several studies show a negative impact of financial constraints on bankruptcy risk (Chan et al., 2010; Komera & Lukose, 2014). Many studies on financial constraints use accounting variables (Yuan et al., 2022) or text analysis (Buehlmaier & Whited, 2018; Hoberg & Maksimovic, 2015). Therefore, following Chan et al. (2010), this study uses changes in cash dividends to indicate a firm’s financial constraint status. It reflects low operating cash flow, low dividends, limited cash, high leverage, and attractive investment opportunities. We expect financial constraints to increase bankruptcy risk.

Firm size (SIZE): Zhang et al. (2020) argue that smaller firms are more likely to default. However, large firms with more outstanding cash holdings can mitigate their default risk as they are unconstrained (Chan et al., 2010). Therefore, we follow Duong et al. (2022) to measure firm size by the natural logarithm of the total asset and test whether larger firms have lower distress risk.

Control Variables

Asset turnover of operation (ATO): Luu Thu (2023) uses asset turnover of operation (ATO) as a proxy for low cost and indicates that firms with higher ATO experience lower bankruptcy risk. Therefore, we follow Luu Thu (2023) to calculate the ATO ratio as operating sales divided by the average operating assets and test whether an increase in asset turnover of operations leads to a decrease in bankruptcy risk.

Gross Profit Margin (GPM): We follow Wahyudi (2014) to measure the gross profit margin as revenue minus the cost of goods sold scaled by revenue. However, Wahyudi (2014) shows that gross profit margin does not significantly impact bankruptcy risk, so we use GPM as a control variable to test whether GPM negatively affects bankruptcy risk.

Return on asset (ROA): Baghdadi et al. (2020) suggest a negative relationship between return on asset and bankruptcy risk. Therefore, we follow Baghdadi et al. (2020) to compute the ROA as net profit divided by average total assets and test whether firms with higher ROA experience lower bankruptcy risk.

Research Model

We follow Darrat et al. (2016), Dirman (2020), Luu Thu (2023), and Zhu et al. (2021) to examine the relationship between firm size (SIZE) and bankrupt risk. They discover the negative impacts of firm size on bankrupt risk, which supports the too-big-to-fall hypothesis. Therefore, we construct a model (1) to test whether it affects. We also add control variables having impacts on bankrupt risk, including ATO (Luu Thu, 2023), GPM (Wahyudi, 2014), and ROA (Baghdadi et al., 2020).

In model (2), we replace SIZE with AKZ to examine the impacts of financial constraints and control variables on corporate default risk. Musso and Schiavo (2008), Xu et al. (2022), and Yu et al. (2021) argue that financial constraints increase the likelihood of default. In contrast, many previous studies have shown a negative relationship between financial constraints and default risk, typically Komera and Lukose (2014) and Schwarz and Pospíšil (2018). Therefore, we employ model (3) and model (4) to examine the nonlinear relationship between financial constraints and bankruptcy risk. In model (3), we add AKZ_SQUARE, and in model (4), we test the effect of U-relationship and firm size on bankrupt risk after controlling other variables. The econometric form of these models is specified as follows:

Where Z-SCOREi,t is the bankruptcy risk coefficient of companies, AKZi,t−1 is an indicator of financial constraints, and SIZEi,t−1 is the natural log of the total assets. In addition, the control variables include ATO, GPM, and ROA. We follow Duong et al. (2022) to dynamic system Generalized Method of Moments to estimate our regressions. αi is the firm fixed effect, and αt is the year fixed effect. µi,t is the residual value. All variable definitions are reported in Appendix A.

Research Methodology

Initially, we implement the Hausman Test and Redundant Fixed Effect Test to determine the most suitable estimation model between the Pooled Ordinary Least Square (OLS), Fixed Effects Model (FEM), and Random Effects Model (REM). However, it is essential to acknowledge that OLS, FEM, and REM are subject to endogeneity and heterogeneity issues, significantly impacting research findings (Dodoo et al., 2021; Greene, 2005). Hence, we then implement the Breusch-Pagan-Godfrey test to determine whether the selected estimation approach violates the heteroskedasticity issue. Suppose the test result indicates a heteroskedasticity issue. Therefore, we employ a two-step dynamic System Generalized Method of Moment (Sys-GMM) to resolve the presence of heteroskedasticity and overcome the endogeneity issues (Appiah et al., 2023). The GMM technique has several benefits, including using cross-correlation equations to improve efficiency and the optimum weight matrix to handle serial correlation and variable variance issues (Duong et al., 2023). Besides, GMM estimation can address issues concerning autocorrelation and omitted variable measurement errors (Appiah et al., 2020; Dodoo et al., 2021), resulting in more accurate and dependable study outcomes.

Furthermore, we conducted several tests to evaluate the appropriateness of the two-step dynamic System Generalized Method of Moment (Sys-GMM) estimation. These tests include the F-test, the Arellano-Bond test, and Sargan/Hansen test. The F-test is utilized to assess the statistical significance of the estimated coefficients. The Arellano-Bond test, however, enables us to investigate the presence of first and second-order autocorrelation problems. In addition, we conduct the Sargan/Hansen test to ensure that the variables chosen as instrumental variables are rational and appropriate. We test the sustainability of results by using another way to calculate the financial constraints variable (Z_FC) following Chan et al. (2010). Besides, we split the data sample by industry to examine the robustness.

Empirical Results

Descriptive Statistics

Table 1 reports descriptive statistics of variables. Table 1 indicates that the average value of the Z-score is about 2.46, the maximum value of the Z-score is about 7.38, and the minimum value is about 0.34. Altman (1968) suggests the company has an extreme default risk if the Z-score is less than 1.81. If the Z-score is between 1.81 and 2.99, the firms may have bankruptcy risk in the subsequent 2 years. If the Z-score exceeds 2.99, the business is in good financial health. The median Z-score in Vietnam is 2.08, implying that distress risk is evident for listed manufacturing firms in Vietnam. The mean value of the Z-score is quite similar to the same-country sample of Duong et al. (2022), which is 2.52. In addition, Table 1 also describes the average values of Z_FC, SIZE, ATO, GPM, and ROA are 0.48, 27.597, 1.25, 0.164, and 0.066, respectively.

Descriptive Statistics.

Note. Table 1 presents the descriptive statistics. Our sample includes 335 listed manufacturing firms in Vietnam from 2010 to 2019. All variable definitions are reported in Appendix A.

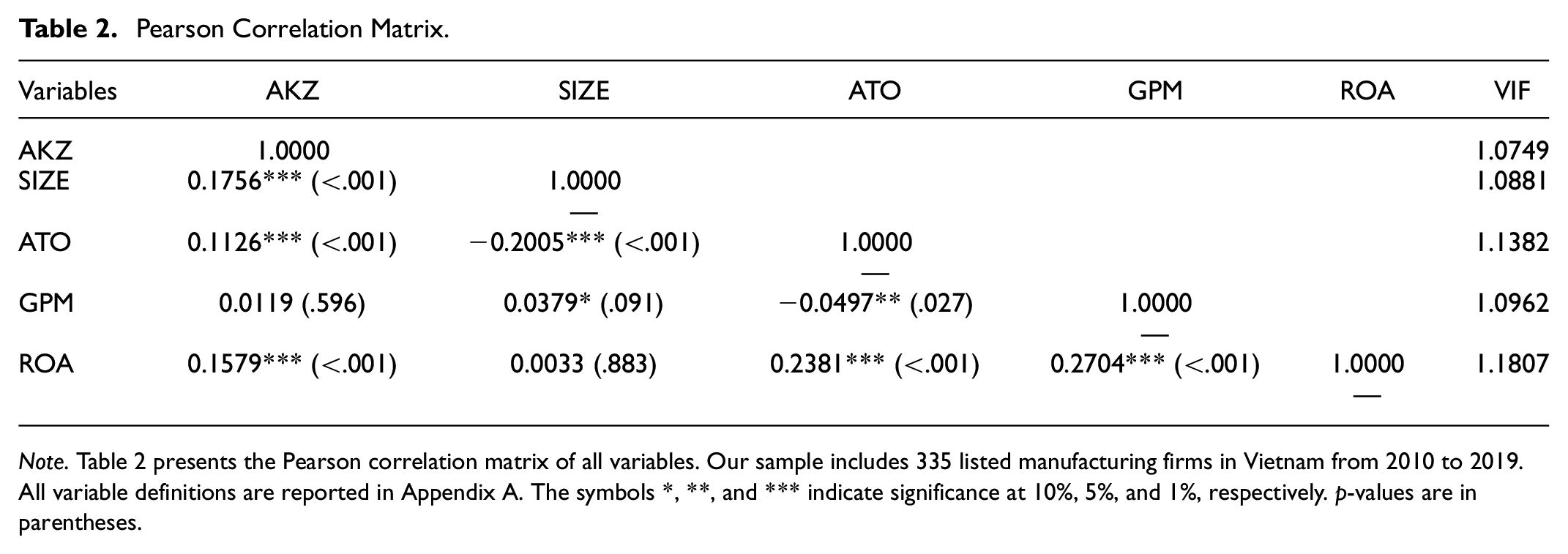

Pearson Correlations Matrix

Table 2 reports the Pearson correlation matrix between the variables. Table 2 reports weak correlations between independent variables because all the correlation coefficients are less than .5. However, we still conduct the variance inflation factor (VIF) test to ensure that multicollinearity is not a problem in this study. The result indicates that all variables are less than five, so we conclude that multicollinearity issues do not exist in our sample (Duong et al., 2023).

Pearson Correlation Matrix.

Note. Table 2 presents the Pearson correlation matrix of all variables. Our sample includes 335 listed manufacturing firms in Vietnam from 2010 to 2019. All variable definitions are reported in Appendix A. The symbols *, **, and *** indicate significance at 10%, 5%, and 1%, respectively. p-values are in parentheses.

The Regression Results of the Fixed Effects Model (FEM)

The Hausman and Redundant Tests are used to determine the best estimate methodology from the Pooled Ordinary Least Squares (OLS), Fixed Effects Model (FEM), and Random Effects Model (REM) in our examination of the causal association between financial constraints and firm size on bankruptcy risk. Following these tests, we conclude that the FEM is the best approach for assessing the connection between our variables.

Table 3 shows a negative relationship between financial constraints (AKZ) and bankruptcy risk but is only statistically significant in model (2). Table 3 also indicates a negative relationship between firm size (SIZE) and bankruptcy risk, but not significant statistic. In addition, our result reports no inversed U-shape between financial constraints and corporate bankruptcy risk.

The Fixed Effects Model (FEM) Regression Results.

Note. Table 3 presents estimation results from the Fixed Effect Models method (FEM). Our sample includes 335 listed manufacturing firms in Vietnam from 2010 to 2019. All variable definitions are reported in Appendix A. The symbols *, **, and *** indicate significance at 10%, 5%, and 1%, respectively. p-values are in parentheses.

Nevertheless, the Breusch-Pagan-Godfrey test in Table 3 reveals heteroskedasticity issues in all models. Greene (2005) also claims that the result of the FEM method is biased because it may violate the heterogeneity assumption. Therefore, we follow Appiah et al. (2023) to employ a two-step dynamic System Generalized Method of Moment (Sys-GMM) to resolve the heteroskedasticity and endogeneity issues. We report the GMM estimations in Table 4.

Estimation Results from the Two-Step Dynamic System Generalized Method of Moments.

Note. Table 4 presents estimation results from the GMM method. Our sample includes 335 listed manufacturing firms in Vietnam from 2010 to 2019. All variable definitions are reported in Appendix A. The symbols *, **, and *** indicate significance at 10%, 5%, and 1%, respectively. p-values are in parentheses.

The GMM Regression Results

Several diagnostic tests were performed to determine the suitability of our GMM regression findings. First, the F-test has a p-value of less than 1%, suggesting that the predicted coefficients are statistically significant. Second, the AR (2) test has a p-value more significant than 10%, indicating no quadratic autocorrelation. Thirdly, the coefficient of lag dependent variable and AR (1) are statistically significant, indicating that the instrument is valid. Finally, the Sargan/Hansen test yields a p-value of more than 10%, showing that the number of instrumental variables is adequate. These findings confirm the reliability and consistency of our GMM regression results.

Discussion

Table 4 reports a positive relationship between financial constraints and the bankruptcy risk of Vietnam-listed manufacturing firms. When the financial constraint index increases by one point, the Z-score reduces to 1.33 scores, implying serious bankruptcy risks. Financially constrained firms have to raise capital with higher financing costs, which raises the likelihood of default (Xu et al., 2022; Yu et al., 2021). Furthermore, as they increase their debt levels with higher financing costs, they also raise their bankruptcy risk because the more debt a firm has, the greater the financial distress costs it may face if it encounters economic or operational challenges. The result is consistent with Musso and Schiavo (2008), Xu et al. (2022), Yu et al. (2021), and the trade-off theory. Thus, our finding supports hypothesis 1.

Table 4 indicates an inversed U-shape between financial constraints and corporate default risk in listed manufacturing firms in Vietnam. Table 4 further reveals that the turning point for financial constraints is 2.844, meaning that manufacturing enterprises face a greater chance of bankruptcy when financial constraints reach 2.844. However, a point increase in financial constraints above 2.844 reduces the likelihood of manufacturing firms going bankrupt. Our findings are consistent with Chan et al. (2010), Komera and Lukose (2014), and the pecking theory that excessively constrained firms have lower bankruptcy risk because they depend on internal capital to grow the business rather than raising external capital. Therefore, these excessively financially constrained firms have lower bankruptcy risks. Besides, our research findings support the agency theory that excessive financial constraints compel firms to allocate resources efficiently. Managers avoid risky projects and non-value-adding activities to protect shareholders from potential asset depletion. Therefore, this encourages investments with positive cash flows, reducing the risk of excessive leverage and bankruptcy. Additionally, excessive financial constraints strengthen external monitoring by creditors, and lenders enforce governance, ensuring managers pursue value-maximizing strategies and avoid actions that could lead to bankruptcy. Therefore, our findings support hypothesis 2.

Table 4 also indicates an inverse relationship between firm size and default risks. Our findings demonstrate that increasing business size by 1% increases the Z-score by 0.71% points, suggesting lower bankruptcy risk. Larger firms are better protected against financial difficulty because they are more transparent and have greater access to external capital than smaller businesses. Furthermore, more prominent organizations are more likely to face challenging conditions, and the higher the company’s overall assets, the greater the potential to pay off corporate commitments in the future, allowing the company to avoid bankruptcy risk. Our result is consistent with Darrat et al. (2016), Dirman (2020), Luu Thu (2023), and Zhu et al. (2021). Besides, our findings are consistent with the too-big-to-fall theory, supposing that more prominent firms have a more diversified business and multiple financing channels than small firms. Darrat et al. (2016) demonstrated that larger companies might have the strength and capacity to bargain to prevent bankruptcy risk. Therefore, our findings support hypothesis 3 and the too-big-to-fall theory.

Table 4 reports a negative relationship between ROA and bankruptcy risk. The finding is consistent with Baghdadi et al. (2020) in that a higher ROA reduces the risk of a company defaulting by reducing operating expenses when assets are used effectively. Furthermore, Destriwanti et al. (2022) suggest that High ROA shows that the business has enough capital to make investments and pay off debts, which helps the company not face a lack of capital and leads to bankruptcy. In addition, the company’s stock with a high ROA ratio attracts a lot of investor interest, increasing the company’s value. Companies will receive funding from the stock market and make bank loans quickly.

Robustness Tests

Cleary (1999) claims that alterations in cash dividend distributions can serve as reliable indicators of a firm’s financial constraints. The coefficients of firm-specific variables in the formula for calculating the Z_FC variable indicate that Z_FC effectively reflects the financial status of corporations. Firms with high leverage, high growth, low profitability, and low financial slack are more inclined to curtail dividend payouts. Therefore, we use the robustness check to ensure our results are still robust when following Chan et al. (2010) using an alternative financial constraints index calculation (Z_FC) instead of AKZ.

Table 5 reports the persistent impact of financial constraints on bankruptcy risk after using Z_FC as the different estimation for financial constraints. Table 5 indicates an inverse U-shape between financial constraints and bankruptcy risk, meaning that financial constraints increased by the turning point at 0.646, and bankruptcy risk increased. The turning point is 0.646, implying that financial constraints increase, and the bankruptcy risk increases before the turning point. After the turning point, the bankruptcy risk decreases. Table 5 also shows the robust effects of firm size on bankruptcy. Our robust findings are consistent with our main findings.

Robustness Test Results from the GMM Estimations Using Z_FC as Financial Constraint Index.

Note. Table 5 presents robustness test results from the GMM estimations using Z_FC as the financial constraint index. Our sample includes 335 listed manufacturing firms in Vietnam from 2010 to 2019. All variable definitions are reported in Appendix A. The symbols *, **, and *** indicate significance at 10%, 5%, and 1%, respectively. p-values are in parentheses.

Table 6 reveals that the effect of financial constraints on the probability of default risk varies by industry characteristics (Sayari & Mugan, 2017). Although increased financial constraints may increase the likelihood of default risk for particular industry groups, such as Industrials and Services, it may reduce it for Consumer Staples. Specifically, financial constraints have a negative relationship with the Z-score, leading to an increase in default risk for firms in Industrials and Services. These findings are consistent with our main findings. However, financial constraints positively affect the Z-score for Consumer Staples firms. Specifically, financial constraints in Consumer Staples firms increase by one point, leading to an increase of 1.138 points Z-score, indicating a decrease in default risk for Consumer Staples firms. Industry-specific factors are possible explanations for this finding. Although facing financial constraints, Consumer Staples firms often have more control over their costs than companies in other sectors. Therefore, these firms may implement strict cost-cutting measures, including reducing discretionary spending, optimizing supply chains, and managing inventory efficiently. Besides, Consumer Staples products typically have inelastic demand, meaning people continue to buy these products even during economic downturns. Hence, Consumer Staples firms enhance their ability to generate cash flows, service their debt, and minimize bankruptcy risk. The results are also consistent with Sayari and Mugan (2017) and the trade-off theory.

Robustness test results across sectors by using the GMM estimation.

Note. Table 6 presents robustness test results across sectors using the GMM estimation. Our sample includes 335 manufacturing firms and 51 service firms in Vietnam from 2010 to 2019. All variable definitions are reported in Appendix A. The symbols *, **, and *** indicate significance at 10%, 5%, and 1%, respectively. p-values are in parentheses.

Table 6 also reveals a nonlinear relationship between financial constraints and default risk in Consumer Staples. Table 6 reveals that the turning point for financial constraints is 1.088, meaning that manufacturing firms face less chance of bankruptcy when financial constraints reach 1.088. However, a point increase in financial constraints above 1.088 increases the likelihood of manufacturing firms going bankrupt. This result conflicts with the main result because the Consumer Staples industry is stable, but competition can still be fierce. Financial constraints may limit a company’s ability to invest in marketing, research, or product development, potentially leading to a loss of market share and declining profitability. In addition, inflation or input cost increases can erode Consumer Staples firms’ profit margins. If they are unable to pass these cost increases onto consumers through higher prices cannot, it can negatively affect their financial health and increase default risk.

Conclusion and Recommendation

Our study examines how the nonlinear effect of financial constraints and total assets affects the corporate bankruptcy risk of listed firms in Vietnam. We used a two-step GMM estimation to analyze an unbalanced panel with 1,990 firm-year observations, including all manufacturing firms on the Hanoi Stock Exchange (HNX) and Ho Chi Minh Stock Exchange (HOSE) from 2010 to 2019.

Our study has the following results. Firstly, empirical findings show that financially constrained firms have higher bankruptcy risks. Our findings support trade-off theory and hypothesis 1. Secondly, our finding indicates an inverted U-shaped relationship between financial constraints and default risk in the Vietnam stock market. Our research also supports the pecking order theory, agency theory, and hypothesis 2. Thirdly, this study also shows that larger firms have lower default risk. Our findings support the too-big-to-fall theory and hypothesis 3. In addition, the first robustness test suggests that the findings are robust even if we employ an alternative financial constraint proxy. The second robustness test indicates a robust nonlinear relationship between financial constraints and default risk in Consumer Staples. Although increased financial constraints may increase the likelihood of default risk for Industrials and Services, it may reduce it for Consumer Staples.

Our results provide practical policy implications to reduce the distress risks in emerging markets. Firstly, small and medium firm managers must clearly understand cash flow management and create an optimal capital structure to minimize distress risk. This will allow them to effectively increase leverage to support business growth and establish stable financial operations. Specifically, firms can negotiate with creditors to restructure their debt in cases of high debt burden. This may involve extending maturities, reducing interest rates, or even writing off a portion of the debt to alleviate immediate financial pressure. Managers aim to optimize the utilization of capital sources for reinvestment, such as borrowing from banks, issuing securities like shares and bonds, or splitting shares. Companies can optimize their operations by reducing costs, improving efficiency, and reallocating resources to focus on core activities to enhance profitability and cash flow. Besides, maintain strong relationships with banks and financial institutions. Communicate proactively about the company’s financial health and plans for managing distress risk.

In addition, managers must also develop risk management policies for firms, especially during economic downturns or periods of financial uncertainty. Our results suggest that firms only borrow small percentages from banks and accumulate cash to ensure solvency and liability to reduce risk. Firms should conduct scenario planning and stress tests to assess the impact of various adverse economic scenarios on the company’s financials. Use this information to make informed decisions and develop contingency plans. In addition, managers should also develop a crisis management plan and communication strategies during a financial crisis. Maintain open and honest communication with stakeholders, including employees, investors, and creditors. In this period, companies can access government programs, like government grants and loan programs, that may be available to support businesses during challenging times.

Finally, the Vietnamese government should prioritize the liquidity of listed companies by providing them with various financing options for easier access to capital. The State Bank of Vietnam should increase its credit room for credible institutions, lowering loan costs for firms with good credit. Establish or improve a comprehensive credit information bureau to provide accurate and up-to-date credit information on businesses, which can help reduce information asymmetry between lenders and borrowers. The government should also establish a risk assessment and management framework for listed companies by categorizing businesses and creating appropriate credit policies for each industry and firm, providing tax incentives and regulatory support. This includes extending credit to firms with practical strategies and operations and limiting excessive lending to those unable to repay their debt. Furthermore, the government can promote access to financing by expanding loan guarantee programs to encourage banks to lend to SMEs backed by government guarantees in case of default. In addition, the government should improve bankruptcy laws to provide a more efficient and predictable framework for restructuring and insolvency proceedings, encouraging creditors to work with distressed firms.

This study has the following limitations. Our research is restricted to data since it only represents the Vietnamese context. Second, Vietnam belongs to one of the frontier countries, so that the results may differ from those of emerging and developed economies because of different market microstructure structures and regulations. For more comprehensive results, we recommend that authors interested in this topic further cross-country studies or investigate the linkages in frontier nations with economic instability due to crises and epidemics in the future.

Footnotes

Appendix

Variable Descriptions.

| Variables | Notation | Variable descriptions | Reference |

|---|---|---|---|

| Dependent variables | |||

| Bankruptcy risk | Z-score | The Z-score is a formula for calculating the financial health of a firm and a potent tool that projects the probability of a manufacturing firm starting bankruptcy. Altman’s (1968) Z-score model is as follows: Z-score = 1.2X1 + 1.4X2 + 3.3X3 + 0.6X4 + X5 Where: X1: Working capital/total assets. X2: Retained earnings/total assets. X3: Earnings before interest and taxes/total assets X4: Market value equity/book value of total debt X5: Sales/total assets. |

Altman (1968) |

| Z-score | The Z-score is a formula for calculating the financial health of a firm and a potent tool that projects the probability of a non-manufacturing firm starting bankruptcy. Altman’s (2013) Z-score model is as follows: |

Altman (2013) | |

| Independent variables | |||

| Financial constraint | AKZ | AKZ = −1 × CashFlow − 7.03 × Dividend − 1.59 × Cash + 1.14 × Leverage + 0.16 × MB | Chan et al. (2010) |

| Financial constraint | Z_FC | Z_FC = 0.0218 × Current − 0.0095 × FCCov − 0.5581 × NI − 0.2149 × Slack + 0.8034 × Growth + 1.6908 × Leverage | Chan et al. (2010). |

| Firm size | SIZE | The natural logarithm of the total asset | Duong et al. (2022) |

| Control variables | |||

| Asset turnover of operation | ATO | The ATO ratio is operating sales divided by the average operating assets. | Luu Thu (2023) |

| Gross profit margin | GPM | The gross profit margin is revenue minus the cost of goods sold scaled by revenue. | Wahyudi (2014) |

| Return on asset | ROA | Profit for shareholders is usually divided by total assets, a measure of the company’s profitability per dollar of assets. | Baghdadi et al. (2020) |

Acknowledgements

We also thank anonymous reviewers for their constructive feedback, which helps us revise our manuscript

Author Contributions

Hoa Thanh Phan Le (hoa.lpt@vlu.edu.vn) : analyzed and interpreted the data and wrote the first and final drafts of the manuscript. Tuan Nhat Pham (phamnhattuan@tdtu.edu.vn), Trang Ngoc Doan Tran (b2000200@student.tdtu.edu.vn) and Han Gia Dang (b2000354@student.tdtu.edu.vn): performed the experiments, contributed reagents, materials, analysis tools, or data. Khoa Dang Duong (duongdangkhoa@tdtu.edu.vn): conceived and designed the experiments, performed the experiments, analyzed and interpreted the data, and wrote the first draft of the manuscript.

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: This work was supported by Ton Duc Thang University and Van Lang University.

Ethical Approval

This study does not involve animals or humans.

Data Availability Statement

The data that support the findings of this study are available on request from the corresponding author.