Abstract

The main purpose of this study is to examine how female representation on the Board of Directors (BOD) and the role of female chief accountants moderate earnings management (EM) concerning firm performance around listing events in Vietnam. Additionally, we aim to investigate whether a substitute (stand-alone) or complementary relationship exists between AEM and REM in both upward and downward forms. While accruals earnings management (AEM) is computed based on accruals proxies, the three measures are aggregated into comprehensive metrics for Real Earnings Management (REM). To achieve these objectives, three hypotheses have been developed after a thorough review of the literature. Panel data has been collected from 222 firms that newly listed over a 4-year span around the listing events. This study demonstrates that the presence of women on BOD significantly and positively moderates the association between positive real-accruals earnings management and firm performance, but this effect is not observed in firms with negative REM or AEM. Our research additionally reveals that there is no moderating role of female chief accountant in these relationships. However, the presence of a female chief accountant positively impacts firm performance only in the positive AEM model. Additionally, we provide evidence that firms may employ individual EM strategies rather than complementary ones, with each type having a positive impact on firm performance.

Introduction

Earnings management (EM) is a persistent financial reporting phenomenon that aims to achieve specific goals while presenting a consistent image of stability in a company’s performance. This phenomenon has been noted in various equity issuance scenarios, including initial public offerings (IPOs) and seasoned equity offerings (SEOs). Numerous academics have made valuable contributions to the field of earnings management, particularly concerning its impact on a company’s performance. Previous studies exploring the phenomenon of earnings management have recognized that managerial manipulation of earnings can have a substantial impact on a firm’s performance (Boachie & Mensah, 2022; Chakroun & Ben Amar, 2022; Chiraz & Anis, 2013; Gunny, 2010; Kumar et al., 2021; Mensah & Onumah, 2023; Nguyen & Thi Duong, 2022). However, there are mixed findings in the literature regarding the association between firm performance and EM. For example, a negative effect of EM on firms’ profitability can be found in the study of Ardekani Aref Mahdavi and Mohammad (2012), Chakroun and Ben Amar. (2022), and Kumar et al. (2021), while Lee et al. (2006), Gunny (2010), Kasznik (1999) reported evidence of a positive association between EM and firm’s performance.

Moreover, two common methods of managing earnings are documented in the literature and have attracted the attention of many scholars—accrual earnings management (AEM) and real earning management (REM). While REM is accomplished by changing real operational activities, such as changing the timing or structure of operations, investments, or financial transactions, AEM is related to accounting practices or estimates employed for reporting specific transactions in financial statements. It is widely acknowledged that earnings manipulation is not without cost and this cost can vary between these methods. Moreover, due to differences in a firm’s circumstances, their motivations for choosing between these two earnings management methods are likely to differ (Braam et al., 2015; Gao et al., 2017). Hence, managers may select for either real activities manipulation or accruals manipulation techniques (Zang, 2012). However, most prior studies on EM and its impact on firm performance have exclusively focused on one type of earnings management, even though both types are likely to be employed (Boulhaga et al., 2022; Cohen et al., 2008; Schipper, 1989). Given the difference between REM and AEM, there is a growing demand for research that explores the effects of both types of EM on firm performance.

Over the past decade, there has been a notable global trend toward enhancing the presence of women on corporate boards. This trend is supported by the belief that companies with female executives tend to make more favorable decisions for their shareholders (Huang & Kisgen, 2013). As noted by Ferrary and Déo (2023), the fundamental premise is that gender diversity influences firm performance by bringing varying skills, expertise, experiences, beliefs, values, and leadership approaches and cognitive structures to the firm. Some studies have proposed that the presence of women on board of directors (BOD) tend to have a positive effect on firm performance because of their insights and innovative ideas (Ferrary & Déo, 2023; Gavious et al., 2012; Safiullah et al., 2022; Smith et al., 2006). In contrast, some other studies, such as Bin Khidmat et al. (2020), Kabir et al. (2023), have claimed that representation of women on BOD could reduce the profitability of a financial statement. The empirical evidence concerning the impact of gender diversity on firm performance, is still emerging and has produced varied results (Arioglu, 2020; Mensah & Onumah, 2023). This suggests the need for further research in this area.

From a different perspective, according to Srinidhi et al. (2011), boards controlled by women are likely to be in an enhanced situation to oversee and enhanced supervision of managers’ reporting, which, in turn, could lead to improvements in earnings quality. It is also suggested that the presence of women on BOD is associated with a greater capacity to oversee the earnings process and withstand scrutiny from the company when it comes to potential earnings manipulation aimed at enhancing firm performance. According to Fan et al. (2019), Triki Damak (2018), Kaplan et al. (2009), women directors are more conservative and professional judgment and monitoring abilities than men, as a result, financial reporting quality is likely to be enhanced (Ginesti et al., 2018; Pucheta-Martínez et al., 2016, and therefore improve firm’s profitability (Mensah & Onumah, 2023). Nevertheless, given the inconclusive findings in previous research, there remains a lack of consensus regarding the impact of female directors on mitigating EM (Sun et al., 2011). Therefore, the question arises about the moderating role of gender diversity in the relationship between EM and firm performance.

All the above reasons are motivations to conduct this study, which has the potential to make valuable contributions to the current body of literature in various ways:

(1)

Moreover, since 2006, the Government has made significant efforts to reduce gender inequality and promote women’s roles by introducing new key laws, such as the Law of Gender Equality. However, women continue to face barriers in a variety of occupations with the number of women business leaders being outnumbered by men in key executive roles (Obermann et al., 2021; Vu, 2018).

Given these circumstances, Vietnam is an excellent context for investigating EM practices and firm performance around listing, moderated by gender diversity. Furthermore, this study employs both AEM and REM methodologies as measurements of earnings management, thereby offering a more comprehensive perspective on EM.

(2)

(3)

The motivations of this research may be summed up in following two objectives:

(1) To examine whether gender diversity, characterized by the presence of women on the Board of Directors and a female chief accountant, moderates the relationship between AEM (or REM) and firm performance around listing events.

(2) To investigate whether there exists a substitute (stand-alone) or complementary relationship between AEM and REM, and their combined impact on firm performance, considering the influence of gender diversity in both forms of each type of EM.

The remainder of this paper is organized as follows: Section 2 presents the literature review and hypotheses. Section 3 discusses the methodology, including the sample, data, and research models. Section 4 presents the results and discussion. Finally, Section 5 provides the summary and conclusion.

Literature Review and Hypotheses Development

Earnings Management, Gender Diversity and Firm Performance

Earnings Management and Firm Performance

It has long been established by prior research that the objective of EM is to influence investor perceptions, especially in the context of decisions related to corporate events such as IPOs, SEOs, and new listings. The asymmetric information theory and agency theory have often been used to explain this phenomenon. In the context of equity offerings, an agency relationship arises when two parties, namely the principal (shareholders) and the agent (managers), have conflicting interests. The conflict arises when managers seek to maximize their own gains, which may not align with the best interests of shareholders. Given the significant information asymmetry that exists during equity issuance events, managers possess more extensive knowledge and information about the internal workings of a firm compared to investors. This advantage enables managers to prioritize their own interests over those of shareholders. In accordance with agency theory, managers (issuers) are strongly motivated and have opportunities to offer shares at higher prices or to improve their chances of being listed by inflating earnings through accounting methods or using real activities. In this context, managers are presented with opportunities and motivation to inflate their earnings, particularly to attain pre-established goals related to firm performance. As the results, the examination of the relationship between EM and firm’s performance has been heavily tested but continues to be an ongoing debate.

With AEM, a growing body of research has emerged exploring the relationship between AEM and firm performance in various markets and various events, but it has provided mixed results or insignificant results. Prior studies in French (Chakroun & Ben Amar, 2022; Chiraz & Anis, 2013), in Malaysia (Ahmad-Zaluki, 2009; Ardekani et al., 2012), in the United States (Anderson et al., 2013), in Pakistan and India (Hunjra et al., 2015), in Taiwan (Tang & Chang, 2015), have provided evidence to support the negative relationship between AEM and firm performance. On the contrary, others have come to the opposite view, such as in the United States (Chou et al., 2010; Lee et al., 2006), as well as sub-Saharan African countries (Boachie & Mensah, 2022; Mensah & Onumah, 2023), or have found insignificant results, as seen in the studies of Mohd Fatzel et al. (2022) and Okafor et al. (2018). Interestingly, mixed results have been provided in the study of Almasarwah et al. (2021). When EM is measured by AEM and REM (abnormal cash flow and abnormal production), it exhibits a strong positive correlation with firm performance. However, the REM measured by abnormal discretionary expenses demonstrates an insignificant connection with firm performance.

With REM, more recent studies shift the focus away from AEM. These studies examine the probability of managers distorting earnings by manipulating real transactions around corporate events. For example, according to Graham et al. (2004), a total of 78% of the companies in the sample acknowledge reducing expenses in areas such as research and development, promotion, or maintenance to achieve a specific earnings goal. Hence, managers use real earnings to meet profit targets. As the result, the positive association between REM and subsequent performance can be found in the study of Gunny (2010). Similarly, in a different context, extending prior research on REM and firm performance, by using the data from the Karachi Stock Exchange, Tabassum et al. (2015) found that REM seems helpful and appealing in current situation but may create problems in the future. In their study, they use ROA as an indicator for assessing firm performance. Their research offered additional confirmation that companies operating within a pricing regime characterized by stronger pricing-period accounting performance are not only tend to be more involved in REM but also experience positive consequences of it on future firm performance. In contrast, Kumar et al. (2021), Wang and Zheng (2020) found that REM activities negatively affect both accounting and market performance.

Gender Diversity and Firm Performance: The Moderating Role of Gender Diversity in the Relationship Between Earnings Management and Firm’s Performance

Agency theory and gender theory have been employed to explain the influence of gender diversity on firm performance. The fundamental tenet of agency theory, which underlies the role and designation of the board of directors, focuses on its effectiveness in mitigating managerial opportunism, thereby impacting firm performance (Aggarwal et al., 2019). Consequently, boards with gender diversity exhibit a stronger tendency to reduce agency costs & asymmetric information as well as boost firm performance (Ain et al., 2020; Loukil et al., 2020; Valls Martínez & Cruz Rambaud, 2019). Thus, the presence of women on the board may potentially be linked to a favorable association with the firm’s value (Lückerath-Rovers, 2013).

From the perspective of the gender theory, women are often expected to display qualities such as warmth, kindness, courtesy, and strong interpersonal skills, while men are commonly perceived as resilient, influential, assertive, and focused on achieving their goals. Hence, women can introduce a range of fresh viewpoints, ideas, backgrounds, values, and work principles that have the potential to improve board decision-making and overall effectiveness. These qualities can ultimately contribute to strengthening governance frameworks and improving firm performance (Kabir et al., 2023). Kaplan et al. (2009) contend that women demonstrate a greater commitment to reporting when faced with an unfamiliar reporting structure compared to men. Additionally, Gavious et al. (2012) and Smith et al. (2006) found that female directors contribute positively to the overall effectiveness and productivity of boards, as well as the performance of the company. Conversely, the rising trend of greater female representation on boards might pose certain disadvantages for corporations. According to Kabir et al. (2023), Vo Thi Thuy and Bui Phan Nha (2017), gender-diverse board would exert a negative impact on firm performance. Additionally, the study conducted by Marinova et al. (2016) and Simionescu et al. (2021) identified non-statistically significant relationships between board gender diversity and firm performance.

Recently, there has been a growing amount of research examining the role of gender diversity in the association between EM and firm performance. Prior studies have indicated that the presence of female leaders is likely to stimulate both formal and informal discussions within BOD, leading to increased accountability for managerial decisions. Hence, it can improve firm reporting (Adams & Ferreira, 2009; Nielsen & Huse, 2010). Using data from 10 different European countries to identify whether EM and gender diversity complement in explaining firm performance, Janssen (2019) demonstrated that EM both mediates as well as moderates the relationship between gender diversity and performance of firms without a gender quota. In a different context, Mensah and Onumah (2023) found that gender diversity does play a significant role in determining firm performance, and it also has a substantial moderating effect on the relationship between EM and firm performance.

The approach adopted by the previous studies exhibits three gaps. First, there is extensive literature on one form of EM and its relationship with firm performance. However, our understanding of both types of EM and how they affect firm performance remains limited. Furthermore, as discussed, most of the research has been conducted in the context of equity offerings in developed markets, where firms typically go public without significant delays. There is a scarcity of research in the context of developing markets, where the time gap between the IPO date and the listing date is often extended and varies in practice. Finally, from the foregoing, it becomes evident that the diversity of gender has as impact on the relationship between EM and firm performance. However, this relationship remains inconclusive due to mixed findings, which include positive, negative, or no relationship. Therefore, gender diversity may play an important role in moderating the impact of AEM and REM on firm performance during the listing process. The above arguments led to the following hypotheses as follows:

H1: Firm performance is positively related to AEM, moderated by gender diversity around listing events

H2: Firm performance is positively related to REM, moderated by gender diversity around listing events

Complementary or Substitute (Stand-Alone) Between REM and AEM

Recently, an increasing number of empirical studies have been examining whether firms use AEM and REM as a substitute or complementary tool in their strategic earnings reporting, yielding conflicting perspectives.

According to the substitute approach, as outlined by Zang (2012), Gao et al. (2017), Owusu et al. (2022), Cohen and Zarowin (2010), Cohen et al. (2008), authors argue that managers balance between REM and AEM by considering their respective costs. They adjust the extent of AEM in response to the level of REM employed. This approach implies that managers select a specific EM method that offers a comparative advantage in terms of cost-benefit, while disregarding other available methods to coordinate and achieve the maximum impact of strategic earnings reporting, whether it involves boosting or reducing income.

From the complementary approach, Mizik and Jacobson (2007), Li (2019), Chen et al. (2012), and Buanaputra (2021) show managers use both REM and AEM jointly and simultaneously to manipulate earnings upward. Moreover, it presents evidence suggesting that the utilization of AEM and REM may coordinate to maximize the effectiveness of earnings reporting strategies.

Regardless of whether managers employ REM and AEM in conjunction to enhance earnings or as substitutes to stabilize earnings in their financial reporting decisions, both approaches necessitate further examination. Our research question pertains to whether there is a substitute (stand-alone) or complement between the two EM methods and their impact on firm performance, as well as on the upward and downward trend of REM and AEM.

Based on the preceding discussions, this study develops next following hypotheses.

H3:Firm performance is related to firms employing a stand-alone AEM or REM versus firms simultaneously using both AEM and REM strategies, with moderation by gender diversity around listing events

Methodology

Data Source

This study analyzes data from newly firms listed on the HoChiMinh stock exchange (HOSE) during period from 2009 to 2019, covering 4 years around listing events: the year prior to listing, the listing year, and the two subsequent years following the listing. In order to compute EM in pre-listing year, sufficient financial statements data from 2 years prior to the listing events is required, considering that data before 2009 may be unavailable. Additionally, for EM of the two subsequent years following the listing, the sample data of newly listed firms ends in 2019 to allow sufficient time for collecting financial statements for the 2 years after listing. Data related EM, gender diversity and firm performance were manually collected from annual report and financial statements that are available on the HOSE webpage, as well as FIINGROUP Vietnam data source.

Consistent with the views of Algharaballi (2013), Roosenboom et al. (2003), there are necessary at least six observations in each industry-year to estimate EM. Hence, firms with missing required data in two sectors including communication service companies and information technology companies have been eliminated from the initial sample. Moreover, financial sector firms have also been eliminated due to their unique industry characteristics and accounting regulations. After the data elimination process, the final sample consists of 222 newly listed firms, totaling 888 firm-year observations in eight (8) sectors including: materials, consumer staples, consumer discretionary, real estate, industrials, utilities, energy, healthcare, as presented below (Table 1):

Sample Selection.

Empirical Method

Real Activities Manipulation Measure

REM involves a range of operational choices made during the year. In accordance with Roychowdhury (2006), this study focus on three categories of REM, which include accelerating discretionary expense, timing of sales, production costs.

First, decreases in discretionary expenses: From the perspective that reducing expenses can result in higher earnings, this type can be expressed as a linear equation involving sales, as shown in the following equation:

Second, by accelerating the timing of sales through increased discounts or more flexible credit conditions, these policies will temporarily increase sales volumes, thereby boosting earnings in the short term. However, lower cash flow can be observed during that period. Drawing from the research of Roychowdhury (2006) and Cohen and Zarowin (2010), this type of REM can be measured as the normal CFO levels, which can be expressed a linear equation in the following equation:

Third: production costs, to report of lower cost of good sold through increased of production, thereby having higher operating margin. The normal level of product cost is estimated as following equation:

In above equations, CFOi,t is net cash flows from operating activities in year t of firm i; REVit is sales in year t;

Abnormal discretionary expenses (DISXi,t), abnormal CFOi,t: and abnormal PRODi,t are estimated by calculating the difference between their actual values and the degree of DISX, CFO, and PROD, respectively. These degrees are computed using the estimated coefficients from each equation. Consistent with the views of Gao et al. (2017) and Li (2019), firms can manage their earnings through REM by using all these characteristics. In order to gain a comprehensive understanding of the effects of REM, these three characteristics are combined into one metric of REM. This involves multiplying abnormal discretionary expenses and abnormal cash flows by negative one, and then adding them to abnormal production costs. A higher value of this metric indicated a greater likelihood of the firm being involved in REM practices.

Accruals Earnings Management Measure

Drawing on previous literature, our study used the modified Jones model proposed by (Armstrong et al., 2008; Teoh et al., 1998a, 1998b) to estimate discretionary accruals as an indicator of EM behavior. Furthermore, within the specific context of Vietnam and listing events, Anh Huu and Chi Thi (2021) conducted a study utilizing 4 models that rely on both total accruals and current accruals. Their findings suggest that Vietnamese companies primarily aim to boost their previous year earnings by utilizing current accruals, rather than using total accrual models.

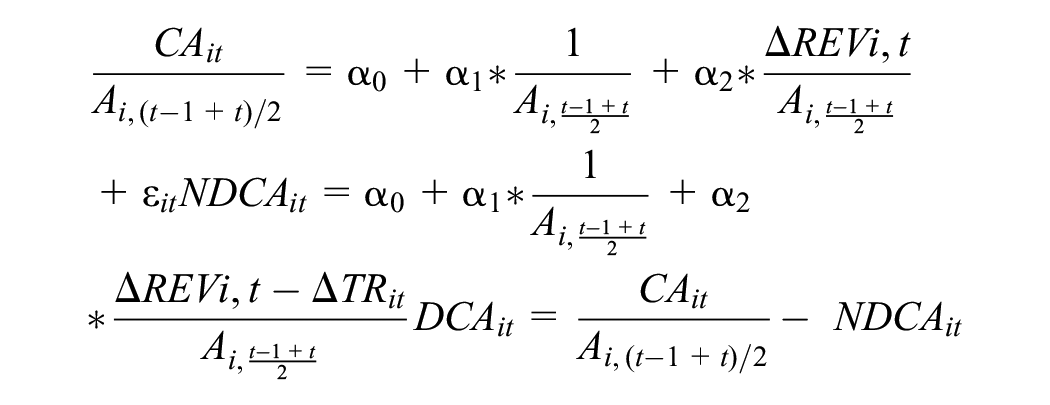

In a nutshell, consistent with earlier studies discussed in the literature review, this study employs DCA (Discretionary Current Accruals) to measure EM (Anh Huu & Chi Thi, 2021; Armstrong et al., 2008; Duong Thi, 2023; Teoh et al., 1998a, 1998b), which are examined using the equation below:

Current Accruals Model

Current accruals measurement

Where:

CAi,t: Current accruals for company i in year t;

DCAit: discretionary current accruals of firm i in year t

NDCAi,t: nondiscretionary current accruals of sample firm i in year t

ΔREVi,t : The change in revenues for company i in year t;

Firm Performance Measure

Return on total assets (ROA) is a widely adopted accounting-based indicator for measuring firm performance, as demonstrated in studies by Rowe and Morrow (2009) and Al-Matari et al. (2014), Nguyen and Thi Duong (2022). Consequently, this ratio has been extensively employed in the context of EM research, as evidenced by studies conducted by Gharbi and Othmani (2023), Gunny (2010), Mangala and Dhanda (2019), Mensah and Onumah (2023), and Nguyen and Thi Duong (2022). Considering these perspectives, ROA has been used in our study as measures of firm performance, be calculated as follows:

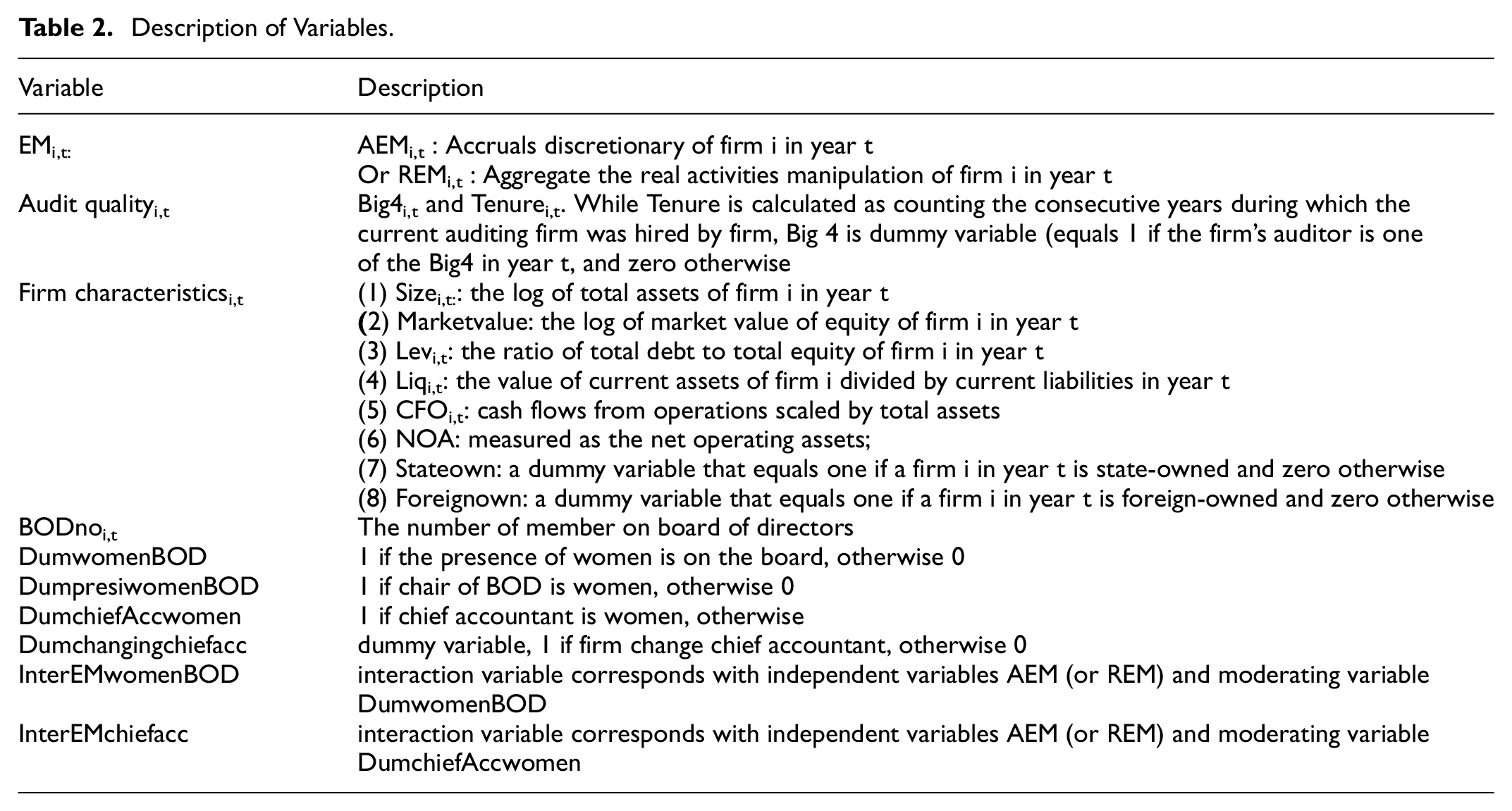

Gender Diversity

In our study, gender diversity has been measured at two levels. First, following the approach of previous literature, gender diversity is measured as dummy variables representing the presence of women on BOD. Moreover, our study contributes to existing knowledge by considering the role of the female chief accountant in the relationship between earnings management (EM) and firm performance. This is achieved by adding a dummy variable for the female chief accountant.

Measuring Control Variables

To control the diversity of firm performance based on firm characteristics, in light with prior literature, this study includes several control variables in the regression Model 1 and Model 2, including firm size, market value, leverage, liquidity, cashflow from operation (CFO), Net operating assets, state-owned, foreign-owned (Ferrary & Déo, 2023; Gaio & Pinto, 2018; Gong et al., 2008; Lee et al., 2006; Loughran & Ritter, 1997; Nguyen & Thi Duong, 2022).

According to Beatty and Zajac (1987), leaders change such as change CEO can explain the variance in firm performance. A widely recognized inverse correlation exists between firm performance and CEO turnover, as evidenced in studies such as Allgood and Farrell (2000)and Parrino (1997). The authors argue that poor firm performance can serve as motivation for firms to change their CEO (Conyon & He, 2008; Dardour et al., 2018). Hence, in addition to traditional factors, the replacement of leaders should be considered as a variable that has an impact on firm performance. In addition, the role of a chief accountant might not be common in numerous countries, but in Vietnam, it carries substantial significance in overseeing a company’s financial matters and is mandated by law (Le, 2024). They play a crucial role in shaping strategic financial planning and decision-making, as well as in implementing financial transactions and preparing financial statements in accordance with accounting regimes and accounting standards. In a similar way, we conjecture that chief accountant in poorly performance are more likely be replaced. Combining these two arguments, the changing chief accountant is added as control variables in our models.

In addition to internal factors, audit quality has also been adopting as external control variable in this study (Elewa & El-Haddad, 2019; Monametsi & Agasha, 2020).

Empirical Models

In the first stage, the hypothesis regarding the role of gender in the relationship between REM (or AEM) and firm performance was tested as following model:

Model 1

In the second stage, to investigate how gender diversity can moderate relationship between both types of REM and AEM and firm performance, we employ the subsequent regression models as follows:

Model 2

Where:

All other variables are defined as previously described in Table 2.

Description of Variables.

AEMREMBODi,t is interaction variable corresponds with independent variables AEM and REM and moderating variable DumwomenBOD

AEMREMChiefi,t is interaction variable corresponds with independent variables AEM and REM and moderating variable DumchiefAccwomen

Results and Discussion

Descriptive Statistics

The ROA values for all sample firms are higher than 0, implying that all firms can generate greater profits from their assets during the sample period. Table 3 also reveals that both REM and AEM exhibit positive mean and median values, with average AEM and REM levels at 0.0262 and 0.1082, respectively.

Descriptive Statistics.

Regarding auditor quality, the average for the Big 4 is 0.2207, indicating that 22.07% of the sampled firms were audited by one of the Big 4 auditing firms. Moreover, the average auditor tenure suggests that these sampled firms have maintained their partnerships with auditors for over 3 years on average. In addition, the average NOA stands at 0.6625, while it drops to 0.5120 at the 25th percentile. This signifies that firms typically have net operating assets exceeding half of their total assets.

The statistics for sampled firms indicate an average board of directors’ size of approximately 5.5 members. On average, 57.21% of BOD members and 45.72% of chief accountants are female, suggesting that the relatively of board members and chief accountants in listed firms in the Vietnamese market are female. In contrast, the percentage of female presidents of the BOD is merely 7%.

Table 4 also demonstrates that the study’s empirical models are unlikely to encounter issues related to Pearson and Spearman correlation coefficients, as none of the correlation coefficients among the independent variables exceeds the threshold of .80. Thus, multicollinearity is not deemed an issue in our regression model. In addition, the table reveals a positive association between two types of EM and ROA, supporting the well-documented proposition that EM is positively related to firm performance. Notably, the correlation coefficient between REM and AEM is negative, indicating an inverse relationship between them. Together, these findings demonstrate the connection between EM and firm performance, suggesting significant implications for selecting estimation techniques in the next section.

Pearson Correlations.

Multiple Regression Analysis

The findings show that the BreuschPagan (LM) test in all models are significant with Prob value 1% (except for the model with negative REM and negative DCA). These tests suggest that it is preferred to use the random-effects model or fix-effects model. The Hauman test is then used to identify whether Fixed Effects Model or Random Effects Model is more appropriate. Subsequently, the Wooldridge test is used to check for autocorrelation in panel data. If there is existence of problems of autocorrelation in data, FE or RE (within) regression with AR(1) disturbances is used to address that problem. Our study presents the final selected model after conducting all tests.

To explore potential variations in the impact of EM on firm performance moderated by gender diversity based on the direction of EM, the study sample has been divided into two groups: one composed of firms with positive EM, and another composed of firms with negative EM.

Firm Performance is Positively Related to AEM, Moderated by Gender Diversity

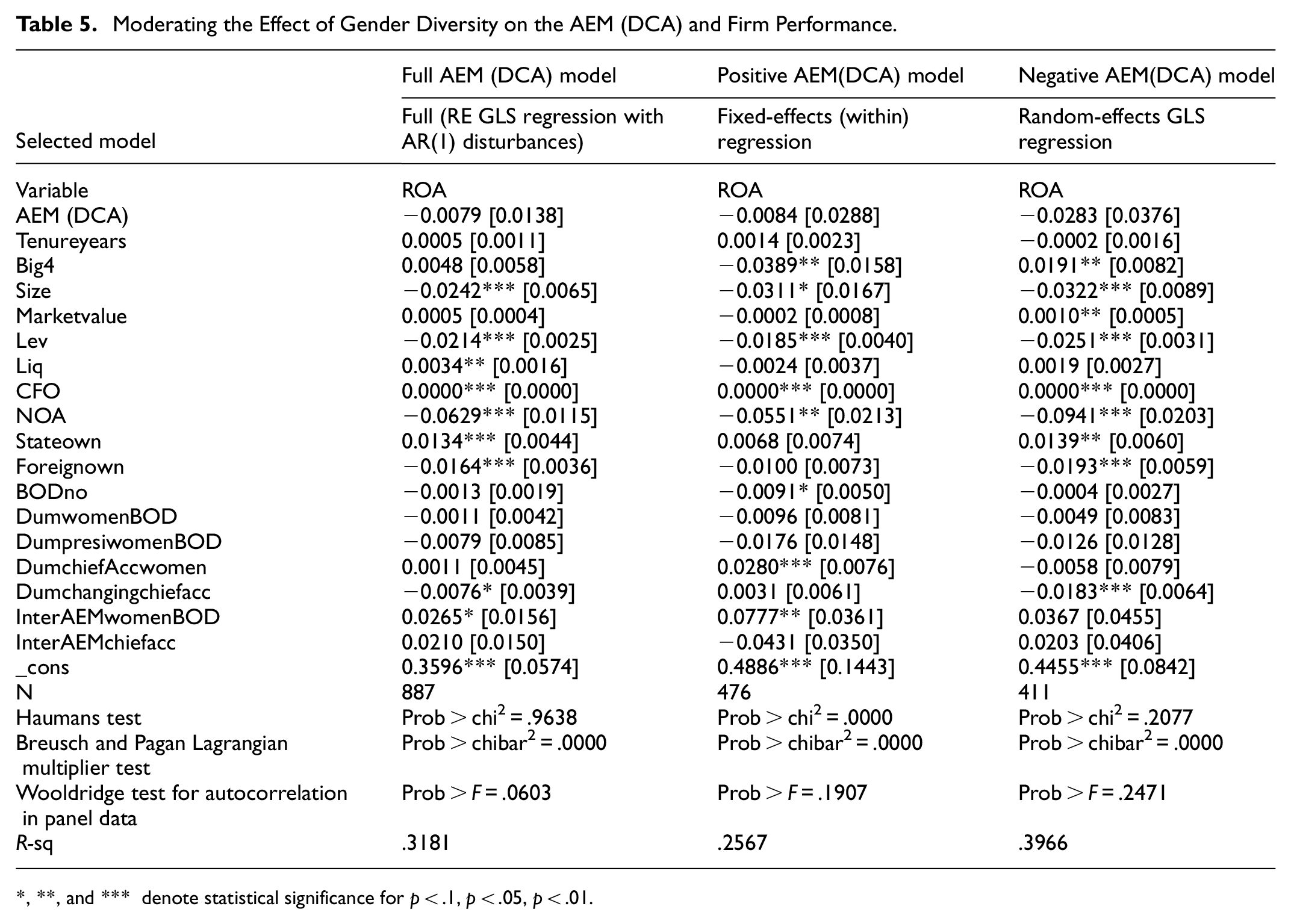

Table 5 provides the findings for full sample of AEM(DCA), positive AEM(DCA) and negative AEM(DCA). As revealed by the random-effects model in full model, the findings show that AEM and the presence of women on BOD, as well as a female chief accountant, are statistically insignificant associated with ROA. This suggests that AEM, the representation of women on BOD and as the chief accountant are not linked to firm performance. In contrast, the change in chief accountant is negatively significant at 10% level. In addition, the coefficient of InterAEMwomenBOD is significant in the expected positive direction, indicating that women on BOD have a moderating effect on the relationship between AEM and firm performance.

Moderating the Effect of Gender Diversity on the AEM (DCA) and Firm Performance.

*, **, and *** denote statistical significance for p < .1, p < .05, p < .01.

When considering different forms of EM and splitting the sample firms into two groups we can observe the differences between these two groups and compare them to the entire sample. Table 5 demonstrates that while the coefficient for the relationship between Dumchief Accwomen and the ROA in the positive AEM model is positively significant at 1% level, Dumchangingchiefacc has a significantly negative impact on the ROA in the negative AEM model. This suggests that firms will perform better when they have a female chief accountant, but only in the group of firms with positive AEM. Consistent with those generated by the entire sample, changing chief accountant in firms with negative AEM might hinder their financial performance.

However, the role of gender diversity on BOD and chief accountant cannot be fully explained without considering its interaction with AEM. As observed in the results presented in Table 5, the association between AEM and firm performance is stronger in firms with female representation on the BOD, but only in cases of positive AEM, not in cases of negative AEM. These findings indicate that female representation on BOD is related to higher practices of AEM, which subsequently has a favorable impact on firm performance. Therefore, they provide support for hypothesis H1, but only in firms with positive AEM.

Following Janssen (2019) and Mensah and Onumah (2023), our findings appear to support that board gender diversity would significantly moderate positive accruals current discretionary, and consequently, enhance the firm performance. This finding aligns with the agency theory’s assertion that a gender-diverse board can be effective in overseeing managerial opportunism, leading to positive contributions to corporate results.

Firm Performance is Positively Related to REM, Moderated by Gender Diversity

Table 6 provides the findings of full sample of REM, positive REM, negative REM. As seen in the results of Table 6, gender diversity on BOD, women chief accountant do not appear to be direct determinants of firm performance in all models. However, a negative relationship between changing the chief accountant and firm performance is found in the full model.

Moderating the Effect of Gender Diversity on the REM and Firm Performance.

*, **, and *** denote statistical significance for p < .1, p < .05, p < .01.

Furthermore, the results of positive REM model are consistent with those generated by positive DCA model. The interaction effect of gender diversity on BOD in the relationship between REM and firm performance yields a significant positive effect, which serves to establish and enhance the performance effects of REM when firms use positive REM. Therefore, greater reliance is placed on the results of the positive REM model, which supports H2.

Neither gender diversity nor EM directly influences firm performance in all models. These findings are also consistent with several studies by Mohd Fatzel et al. (2022), Okafor et al. (2018), which demonstrate that EM has an insignificant relationship with firm performance. However, the impact of EM on firm performance can be fully explained by examining its interaction with gender diversity on BOD. Hence, our study proposes that the representation of women on BOD significantly and favorably moderates the association between positive real- accruals earnings management and firm performance. Theoretically, the presence of women on the BOD can bring diverse perspectives, varied backgrounds, and unique values, which can enhance the decision-making process and boost the overall efficiency of boards, leading to improved firm performance (Bin Khidmat et al., 2020). In support of gender theory, we propose the importance of having representation of females on the BOD, ensuring that women’s unique skills and competencies can positively influence firm performance. Our research suggests that the presence of females on the BOD enhances the beneficial effects of EM practices. Our findings from the Vietnamese context align with studies from other developed markets conducted by Adams and Ferreira (2009) and Gharbi and Othmani (2023), indicating that the role of female on BOD in EM monitoring seems to result in efficiency outcomes of EM practices, thereby contributes to performance enhancement in firms around listing. Moreover, our findings suggest that gender diversity on boards plays a significant and positive role in moderating the connection between both types of EM and firm performance. This outcome reinforces the agency theory’s argument that a gender-diverse board is effective in overseeing managerial opportunism, thus leading to favorable firm performance. Finally, in agreement with, Mensah and Onumah (2023) and Zalata et al. (2021)), the mechanism through which board gender diversity might impact firm performance could also involve its monitoring of EM around listing.

Our study also finds that female chief accountant has a positive effect on firm performance only in the positive AEM model, not in REM models. These findings are relevant to the unique context of Vietnam, where the chief accountant plays a crucial role in recording economic transactions, using accounting methods in accordance with regulations and regimes to prepare financial statements. Therefore, to enhance firm performance, the female chief accountant might utilize AEM rather than REM. This implies that REM can only be implemented through real activities such as sales policies and financial policies, which require involvement from higher positions such as the BOD and are beyond the chief accountant’s responsibilities. The results provide empirical evidence that firms using AEM to boost earnings, those with female chief accountant, will demonstrate higher performance compared to firm with non-female chief accountant.

Firm Performance is Related to Firms Employing a Stand-Alone AEM or REM Versus Firms Simultaneously Using Both AEM and REM Strategies, With Moderation by Gender Diversity

In addition to testing the impact of one type of EM on firm performance, we explore how firms concurrently utilize both accrual-based and real earnings management strategies (interaction term AEM × REM) as well as moderate those relationship by using gender diversity. To further support the findings of the full sample regression, especially regarding the interaction of gender diversity with the effectiveness of both types of EM, the full sample is divided into four groups. Group one consists of firms with positive AEM and negative REM, group two comprises firms with positive REM and negative AEM, group three includes firms with negative REM and negative AEM, and group four consists of firms with positive REM and positive AEM. However, it’s important to note that the p-value of the regression model for group four is 12.56%, which suggests that these results do not provide sufficient evidence to support a significant relationship between EM and firm performance in firms with both positive REM and AEM. Therefore, we present the results for the selected three groups in Table 7.

Moderating the Effect of Gender Diversity on Two Types of Earnings Management and Firm Performance.

*, **, and *** denote statistical significance for p < .1, p < .05, p < .01.

As illustrated in Table 7, AEM has a positive and significant relationship at 1% level in full model and model of group 1, whereas there is no significant association between REM and firm performance in full sample. Moreover, there is no evidence to suppose that firms simultaneously use both AEM and REM.

For firms that rely more on current accruals and less on REM, the results in Table 7 are consistent with expectations. The coefficient of AEM is positively related to firm performance at the 10% level, while REM shows no significant relationship with firm performance. Most importantly, the coefficient of AEMREMBOD is positively significant at the 5% level, its estimated magnitude is slightly higher than those for the individual AEM. Representation of female on BOD have been found to positively moderate the direct relationship between both AEM, REM and firm performance. This indicates that in firms with female on BOD, the magnitude of its estimated coefficient of AEM exceeds the degree of negative REM. As a result, the coefficient for the interaction term is positive. This finding supports the perspective that an increase in managerial AEM leads to an increase in firm performance in the year when AEM is implemented.

For firms that rely more on real earnings management and less on accruals earnings management, while AEM has an insignificant relationship with ROA, REM shows a significantly positive coefficient at a 1% level. Interestingly, in the positive AEM model, the interaction term of AEMREMBOD shows a significantly positive coefficient at the 5% level, but in the model with positive REM, there is an insignificant relationship with ROA. It can be inferred that if firms inflate their REM, its performance becomes better. In addition, there is no evidence to conclude that firms simultaneously adopting AEM and REM enjoy higher firms’ performance than firms adopting either accrual-based or real earnings management alone.

However, this association is statistically insignificant for firms with both negative REM and AEM. Firms presenting negative EM, there was no evidence to support a relationship between EM and firm performance. As expected, the findings indicate that firms are more likely to manipulate earnings upward to improve their performance.

In conclusion, firms tend to favor one type of EM, each type has a positive impact on firm performance. In addition, when firms choose to employ AEM and have women on the BOD, despite the existence of negative REM the influence of AEM on performance outweighs the impact of negative REM, even if it exists. In contrast, when firms prefer to use real earnings, there is no evidence to support the simultaneous use of both AEM and REM.

Robustness Check

To further confirm our findings, a robustness examination has been performed in our study by using another proxy of AEM. Existing research also employs a measure of AEM derived from the total accruals model. In alignment with prior literature, this study utilizes the modified Jones model to calculate discretionary accruals (DA), known as the most effective model to detect AEM (Dechow et al., 1995; Teoh et al., 1998a, 1998b) as follows:

Where

The results of the robustness tests align with the main findings of H1 and H3 (Tables 8 and 9). In Table 8, where discretionary accruals of AEM are used as a measure of EM, the findings still suggest that the presence of women on the BOD significantly and positively moderates the association between positive AEM and firm performance.

Moderating the Effect of Gender Diversity on the AEM (DA) and Firm Performance.

Moderating the Effect of Gender Diversity on Two Types of Earnings Management and Firm Performance (When AEM Measured by DA).

*, **, and *** denote statistical significance for p < .1, p < .05, p < .01.

Additionally, hypothesis H4 is confirmed. As shown in Table 9, firms tend to favor one type of EM to enhance performance, with each type having a positive impact on firm performance, and women on BOD plays an important role in maintaining an appropriate level of earnings management by making trade-off selections between AEM (DA) and REM. Moreover, in the context of positive AEM and negative REM model, the presence of a female chief accountant positively impacts firm performance, while it does not show the same effect in REM models.

Conclusion

The purpose of this study is to examine how female representation on BOD and chief accountant moderate the relationship between EM and firm performance around listing events in Vietnam and to investigate whether a substitute (stand-alone) or complementary relationship exists between AEM and REM in both upward and downward forms. While AEM is computed based on current accruals and discretionary accruals proxies developed by Teoh et al. (1998a, 1998b) and Dechow et al. (1995), the three measures into comprehensive aggregate metrics of REM are employed (Gao et al., 2017; Li, 2019). To achieve these objectives, the three hypotheses have been developed after a thorough review of the literature. Panel data has been collected from 222 newly listed over a span of four (4) years around listing: the year before listing, a listing year, and two (2) subsequent years, from 2009 to 2019. Our study has partly contributed significantly to the literature review on EM and provides valuable empirical evidence for future studies, as follows:

First, while most prior studies examining the relationship between EM and firm performance focus on one technique of EM (REM or AEM), our study re-explores this relationship by adopting both AEM and REM strategies while considering the potential impact of gender diversity. In addition, by considering different forms of EM that stem from firm-invariant motivations in manipulating earnings (upward or downward), we expect to achieve a more reliable conclusion about this relationship. Interestingly, this relationship has been examined in the context where listings and IPOs are distinct processes, and the actual listing date takes place significantly after the issue date.

Our findings appear to support the idea that two types of EM have no influence on firm performance in all models. However, the impact of EM on firm performance can be explained by examining its interaction with gender diversity on BOD. Hence, our study proposes that presence of women on BOD significantly and positively moderates the association between positive real-accruals earnings management and firm performance. These results seem to align with agency theory, suggesting that gender diversity on board can effectively oversee managerial opportunism and contribute positively to firm performance (Mensah & Onumah, 2023; Tang & Chang, 2015). Representation of female on BOD are empowered enough to affect board decisions and contribute favorably toward firm performance around listing events.

In addition to BOD gender, our study further contributes to knowledge by considering the role of the chief woman accountant in the relationship between EM and firm performance. Our research additionally reveals that there is no moderating role of female chief accountant in these relationships. However, the presence of a female chief accountant positively impacts firm performance only in the positive AEM model. It implies that the female chief accountant may prefer employing AEM instead of REM. This suggests that REM can solely be executed through real activities such as sales policies and financial strategies, which require involvement from higher positions such as the BOD and are beyond the chief accountant’s responsibilities.

Second, firms in the Vietnamese market exhibit REM as well as AEM around listing events to beat earnings targets. To investigate whether firms employ both AEM and REM simultaneously and their association with firm performance, our study builds upon this research by examining the moderating effect of gender diversity. We provide evidence that firms may employ individual EM strategies rather than complementary ones, with each type having a positive impact on firm performance.

In addition, consistent with previous findings, it is apparent that board gender diversity on BOD plays a role in the EM–-firm performance nexus when firms use a positive stand-alone EM rather than in the joint effect of accrual-based and real earnings management. Interestingly, the study further reports a significant positive impact of the moderation effect of women on the BOD on the relationship between both types of EM and firm performance. This supports even in the presence of negative REM, firms with women on the BOD are more likely to properly utilize positive AEM, which would help moderate the positive impact of AEM on firm performance.

This study has important implications for researchers and investors. For researchers interested in investigating earnings management, it is crucial to focus on both earnings management strategies and their respective forms (upwards and downwards). Additionally, consideration should be given to the rewards of a stand-alone strategy of accrual-based and real earnings management, rather than a joint effect strategy. This study is also beneficial and informative for investors who must be aware of the impact of EM on firm performance. Especially, with representation of women on BOD, positive EM roles could serve as an effective tool to improve firm performance. Moreover, firms using AEM to boost earnings, those with female chief accountant, will demonstrate higher performance compared to firm with non- female chief accountant.

Although the study has made valuable contributions to the EM literature, this study suffers from limitations. First, this study has been conducted exclusively within the context of newly listed firms in Vietnam, focusing solely on non-financial firms. Moreover, only one dimension of firm performance has been considered. Hence, other proxies of firm performance may also be used in future studies. Second, the existence of endogeneity can be found in the study of earnings management and firm performance. Despite our efforts to address this issue by utilizing alternative measurements of AEM and employing robust statistical techniques, the potential for endogeneity remains a concern. Consequently, readers are advised to interpret our findings with care, acknowledging the potential constraints that endogeneity poses on the internal validity of our research. For future research, to tackle this issue, extending the time frame could be beneficial, allowing for the application of dynamic endogeneity through the incorporation of specific lag periods. Finally, this study employs a dummy variable as the sole measure of gender diversity. In line with Zalata et al. (2021), it’s worth noting that certain characteristics and skills of female members on BOD may influence their effectiveness in monitoring earnings management. Thus, further research can investigate these aspects.

Footnotes

Funding

The author disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: This research is funded by National Economics University, Hanoi, Vietnam

Declaration of Conflicting Interests

The author declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Data Availability Statement

Data sharing not applicable to this article as no datasets were generated or analyzed during the current study.