Abstract

This study aims to examine the managerial and organizational factors affecting ICT adoption in SMEs, and the link between ICT adoption level and firm performance. In this context, a survey was performed with owners, top-level managers, middle-level managers, and first-line managers of SMEs. The study was carried out in three phases. First, after assessing the ICT adoption level for each participating SME, the effect of owner and manager-related characteristics and organizational attributes on the level of ICT adoption was examined. Second, an analysis was performed to find out if there is a relationship between ICT adoption levels and organizational innovation types. Finally, the effect of ICT adoption level on firm performance and the mediating effect of organizational innovativeness types on this link were investigated. Data obtained from 393 owners and managers of 203 SMEs were analyzed through SPSS. Analysis results show that the owner’s/manager’s education level and awareness of the benefit of ICT are positively related to ICT adoption level. In contrast, awareness of the costs of ICT is negatively related to ICT adoption in SMEs. Moreover, the results reveal that internal integration and strategic integration level ICT adoption on firm performance is mediated by organizational innovativeness. These findings stand to help SMEs strategically plan their ICT adoption phases based on their organizational needs.

Plain language summary

This study explores the managerial and organizational characteristics of small and medium-sized enterprises (SMEs) and their impact on the adoption of information and communication technology (ICT). Additionally, the research investigates the role of organizational innovativeness in the link between ICT adoption and firm performance. A survey involving owners and managers at various levels in 203 SMEs was conducted. In the initial analysis, the study examined whether owner and manager characteristics, including education, age, tenure, and ICT awareness, influence the extent of ICT adoption. Furthermore, the researchers analyzed the impact of organizations’ lifespan, size, and revenue on the level of ICT adoption. Second, the study explored the relationship between ICT adoption levels and the type of organizational innovativeness. Finally, it examined how the level of ICT adoption affects firm performance, taking into account the role of organizational innovativeness. The findings suggest that the education level of owners/managers and their awareness of ICT benefits positively influence ICT adoption, while awareness of ICT costs has a negative impact. This implies that when the awareness levels of business owners and managers regarding the benefits of ICT increase, and when they are more educated, the level of ICT usage in their companies is positively affected. However, an increase in awareness levels about the costs associated with ICT leads to a negative impact on ICT adoption. The study reveals that, among the levels representing ICT adoption, only internal integration and strategic integration have an indirect impact on the performance of companies. The reason for this indirect effect is that internal integration and strategic integration, as a result, enhance organizational innovativeness, leading to improved performance. The specific types of innovation causing this effect are (1) product and (2) process-market innovativeness of organizations.

Introduction

Small and medium-sized enterprises (SMEs) play a crucial role in both developed and developing economies, contributing significantly to employment, GDP, and overall socio-economic development (Rollin et al., 2022). While digitalization and the use of ICT contribute to SMEs reducing transaction costs, improving service quality, integrating with customers and other stakeholders, increasing effectiveness and efficiency, and achieving sustainable growth and competitive advantage, they also require them to deal with several obstacles.

SMEs encounter obstacles that hinder their efficiency from digitalization and ICT use, such as limited ICT knowledge, lack of specialized skills, and insufficient financial and human resources (Eze et al., 2018). Besides, the Covid-19 pandemic has further emphasized the importance of ICT adoption and digitalization for SMEs. At the same time, in developing countries, the inadequacy of infrastructure, constraints on senior management support, insufficient financial and human resources, a generally negative attitude toward digitalization, and the experience and commitment of managers (Ibrahim et al., 2018), limited financial support, political instability, and lack of external support/consultancy and related costs (Y. Wang, 2016) are among the critical factors that hinder the use and adoption of ICT. Besides, due to their positioning in the value chain and need for economies of scale, SMEs need help integrating recent digital technologies. The success of an enterprise in ICT adoption and digitalization depends on its capabilities and dynamic managerial characteristics (Alexopoulos et al., 2022).

Social performance improvement positively affects innovation performance. Awan (2019) demonstrated that relational governance fosters innovation performance; consequently, the firm’s willingness to adapt and carry out knowledge practices to indicate that firms are driven to guarantee a long-term relationship can significantly impact the enhancements in innovation performance. Integration along the supply chain, increased collaboration, joint decision-making mechanisms, and information exchange are only possible based on digital networks. Xia et al. (2024) also confirmed that the digitalization of business processes as a part of digital transformation has a direct influence on organizations’ innovativeness. Furthermore, Vilkas et al. (2022) proved that digitalization is positively related to product innovations in manufacturing firms.

Prior studies have mainly focused on the Technology-Organization-Environment (TOE) framework by Tornatzky and Fleischer (1990) to understand firm-level ICT adoption and examined a wide range of factors. Studies examining the relationship between firm size and ICT adoption have mixed findings. Among the factors related to owners/managers, lack of awareness has been identified as one of the most critical barriers, especially for developing countries (Elhusseiny & Crispim, 2022; Singh et al., 2022). There are also conflicting findings regarding the effect of demographic factors related to owner/manager on ICT adoption (Kusuma et al., 2020; Lu et al., 2019). For example, Kusuma et al. (2020) found significant differences based on age and year in business, but Lu et al. (2019) and Alma and Coskun (2018) found no significant differences based on age in terms of ICT adoption.

The conceptual models specifically proposed for SMEs (Alma Çallı et al., 2019; Taylor, 2019) put forward factors such as firm size, age, and leaders’ attitudes as determinants of ICT adoption. Alma Çallı et al. (2019) suggested a comprehensive model and proposed that factors such as lifespan, size, revenue and owner/manager-related factors such as education, age and ICT awareness affect the extent of ICT adoption and digitalization. As Taylor (2019) suggested, these conceptual models need to be explored and tested in different contexts. Potential determinants such as ICT awareness level, firm size, and age, which were revealed as findings of qualitative studies (Özşahin et al., 2020) and the findings that past studies have reached contradictory results for different contexts, need to be tested empirically.

In this study, demographic characteristics of SMEs, including lifespan, size, and revenue, were considered. Additionally, owner/manager-related characteristics, including education, age, and ICT awareness, were taken into account as determinants of ICT adoption. In addition, unlike previous studies, this study deals with ICT adoption from a multidimensional perspective. ICT adoption in SMEs was evaluated by considering the dimensions of communication, internal integration, integration with customers (mainly focusing on external integration), inter-organizational integration, and strategic integration, as suggested by Özşahin et al. (2022).

H. Wang et al. (2024) pointed out that although previous studies had shown a connection between digitalization and innovations, more in-depth studies are still required. Tsou and Chen (2023) investigated the mediating role of organizational innovativeness on the relationship between the usage of digital technology and business performance. Because their study focused on finance firms, the results are context-specific. Besides, a stream of research proved that ICT adoption/digitalization positively affects firm performance (Rollin et al., 2022). However, some studies demonstrated that ICTs enhance production costs and, in return, decrease firm performance (Santos-Jaén et al., 2022; Thatcher & Oliver, 2001).

However, it is widely acknowledged that ICTs and information systems enable the production of more innovative solutions by speeding up and facilitating knowledge management activities, collaboration, and cooperation. Innovations provide meeting customer requirements (Doğan & Doğan, 2020; Limsangpetch et al., 2022) and growth and development of businesses (Kim et al., 2023). Therefore, the arguments above can be combined to examine better the relationships between ICT adoption, organizational innovativeness, and firm performance. The impact of organizational innovativeness on the relationship between digital technology utilization and firm performance has not been investigated empirically by a comprehensive framework (Tsou & Chen, 2023). To the best of our knowledge, the only study (Tsou & Chen, 2023) investigated the mediating role of organizational innovativeness on the relationship between the usage of digital technology and business performance. However, since their study focused on finance firms, the results are context-specific. Sijabat (2022) examined the relationship between digitalization, knowledge management, and performance and knowledge management’s role as a mediator. Nevertheless, some methodological limitations exist, such as sample size and measurement of digitalization using a unidimensional scale.

Consequently, to fill the research gaps, this study aims to investigate the effect of SME owners’ and/or managers’ and organizational characteristics on the level of ICT adoption and to examine whether there is a relationship between ICT adoption levels of SMEs and organizational innovativeness types. Specifically, the aim is to examine the effect of ICT adoption level on firm performance and the mediating effect of organizational innovativeness types on this link.

Literature Review and Hypotheses Development

Technology-Organization-Environment (TOE) Framework

Even though ICT is now widely used by businesses, there are still differences in applications and overall outcomes between different firms. ICT adoption and its effects on business performance are both considered to be significantly influenced by firm size. According to Duc and Nguyen (2023), large companies employ technology more effectively because of their advantages in size and capital. For various reasons, including limited resources, SMEs may find it challenging to deploy ICTs (Taylor, 2019). Although studies on ICT adoption are based on various theories to explain and examine information technology and systems adoption, the technology, organization, and environment (TOE) framework (Tornatzky & Fleischer, 1990) has been frequently used for organizational-level examinations. TOE framework posits that technological, organizational, and environmental factors influence the organizational processes (Tornatzky & Fleischer, 1990).

The TOE framework has been extensively utilized to study SMEs’ ICT adoption behavior and decisions (Ghobakhloo & Ching, 2019; Giotopoulos et al., 2022; Maroufkhani et al., 2020). Giotopoulos et al. (2022) stated that the TOE framework is commonly regarded as the most suitable and robust theoretical model for organizational-level analyses.

Accordingly, different factors have been examined as antecedents of ICT adoption. Having a dominant role, owners/managers in SMEs lead the development of the organizational culture toward IT utilization (Fink, 1998). Because of the highly centralized organizational structures of SMEs (Tan et al., 2010), the capabilities, tendencies, willingness, and readiness to change of the owner/manager determine the extent of innovations and technology adoption decisions (Abdullah et al., 2012; Birley, 1982; Cannon, 1985; Thong, 1999). The previous studies have also examined demographic characteristics comprising age, education, and year of business experience. Previously, Kusuma et al. (2020) found significant differences in ICT practices based on age, year in business, and managerial status, while no significant differences were detected based on gender and educational qualifications.

In addition to basic demographic factors, Barba-Sánchez et al. (2007) mentioned the influence of training, experience, and psychological factors that differentiate entrepreneurs. The findings of Roberts et al. (2021) show that decision-makers are impacted by various psychological factors, including their attitudes toward technology, personal motivations, risk perceptions, and technical competence. Adoption of technological innovations becomes easier when a cause-effect relationship is established regarding the results of a technological solution design, and managers are aware of the opportunities to be presented (Annosi et al., 2019). According to Annosi et al. (2019), owners’/managers’ beliefs about the advantages of the technology and their knowledge nurture the new technology adoption. Lu et al. (2019) also confirmed that perceived benefits are related to technology adoption.

Kossaï et al. (2020) found that firm size is one of the significant factors impacting the adoption of advanced manufacturing ICTs in the electronics sector. While some studies have reported that firm size will make technology adoption more effective, some studies have stated that it will be easier for small firms to benefit from technology due to flexibility (Duc & Nguyen, 2023). According to Duc and Nguyen (2023), despite several theoretical studies in the literature, their conclusions are more complex and inconsistent. Even while SMEs have raised their ICT investments, particularly in developing nations, the benefits of economic benefits might not be achieved (Barclay & Duggan, 2008; Kraemer et al., 2005).

In developing country SMEs, common barriers include inadequate technological infrastructure, lack of management vision, financial constraints, unbalanced investment and return benefits, and lack of awareness about technological solutions. Lack of awareness and management vision were found to be the most critical barriers (Singh et al., 2022). Lack of skilled managers, lack of management support, lack of financial resources, and lack of skilled employees are among the barriers that are more common in developing countries compared to developed countries (Elhusseiny & Crispim, 2022). Although the study of Singh et al. (2022) was performed in MSMEs in India, which demonstrates similarities with other developing countries regarding the business environment and global pressures, the authors call for future research examining the effect of proposed barriers in other developing countries.

For developing country SMEs, a behavioral model of ICT adoption was proposed by Taylor (2019). However, that conceptual model reveals potential determinants and needs to be studied empirically. Taylor (2019) calls for future studies to empirically test the conceptual model in different contexts and examine variables that may have different moderating and mediating roles. A qualitative study conducted on 51 SMEs previously indicated the entrepreneur’s ICT awareness level, firm size and age as factors affecting ICT adoption in these enterprises (Özşahin et al., 2020). Similarly, the conceptual model proposed by Alma Çallı et al. (2019) mentioned demographic characteristics of SMEs (lifespan, size, revenue) and owner/manager characteristics (education, age, and ICT awareness) as determinants of ICT adoption. However, these findings need to be tested empirically. In a study conducted on a limited sample, while there were no significant differences in the ICT adoption of SMEs in terms of the age of the owner/manager, significant differences were found in terms of education level, company size, and ICT investments (Alma & Coskun, 2018). Besides, the lack of consensus on the outputs of previous studies examining firm size and ICT adoption has been attributed to the influence of particular contextual factors (Cataldo & McQueen, 2014; Revilla & Fernández, 2012). For this reason, researchers such as Duc and Nguyen (2023) stated that it is necessary to examine the relationship between size, ICT adoption, and performance from a different perspective, especially in companies operating under similar conditions, such as developing country SMEs.

Therefore, the following hypotheses are proposed based on the above literature and explanations.

H1: Lifespan of the organization has impact on ICT adoption level

H2: Size of the organization has impact on ICT adoption level

H3: Revenue of the organization has impact on ICT adoption level

H4: Education of the owner/manager has impact on ICT adoption level

H5: Age of the owner/manager has impact on ICT adoption level

H6: Tenure of the owner/manager has impact on ICT adoption level

H7: ICT awareness (benefits) of the owner/manager has impact on ICT adoption level

H8: ICT awareness (costs) of the owner/manager has impact on ICT adoption level

ICT Adoption & Organizational Innovativeness

ICT Adoption

According to Özşahin et al. (2022), ICT adoption has been investigated by several scholars using unidimensional scales. However, ICT adoption has proven to be multidimensional, and adoption and use of ICT in businesses take place in stages, depending on the sophistication and extent of integration. Depending on the studies of Alma et al. (2018), Kotelnikov (2007), Redoli et al. (2008), Shiels et al. (2003), and Venkatraman (1994), an assessment framework was previously proposed for examining the level of ICT adoption in SMEs. According to that framework, ICT adoption includes the following dimensions: communication, internal integration, integration with customers (mainly focusing on external integration), inter-organizational integration, and strategic integration (Özşahin et al., 2022).

Communication is characterized by the use of communication mechanisms and the Internet. Internal integration means using digital networks for the continuous flow and sharing of information within the enterprise more regularly. The existence of the intranet, enterprise resources planning systems, and associated hardware-software mechanisms demonstrate that the enterprise has achieved internal integration. While external integration primarily means integrating customer-related processes and supporting them with ICT, inter-organizational integration expands the scope of this integration. Inter-organizational integration allows all partners in the value chain to provide information flow between them and the business enterprise digitally. At the level of strategic integration, which is the final step, the mechanisms used for strategic decision-making, especially advanced data analytics applications and decision support systems, are observed (Özşahin et al., 2022).

Organizational Innovativeness

The ability of a company to bring new goods or approaches to improve its performance is referred to as innovativeness. Therefore, the word “innovativeness” is employed in this study to define a company’s capacity for innovation. This capacity is measured by how a new or significantly enhanced product, process, marketing strategy, or organizational technique has been introduced into the company’s operations to improve performance (Makanyeza et al., 2023).

Organizational innovativeness encompasses different types of innovativeness, innovative practices and behaviors within the organizations (Klimas, 2015). C. L. Wang and Ahmed (2004) proposed five primary aspects, including “product innovativeness,”“market innovativeness,”“process innovativeness,”“behavioural innovativeness,” and “strategic innovativeness” that define an organization’s overall innovativeness.

Previously, Vilkas et al. (2022) proved that digitalization positively correlates with product innovations in manufacturing firms. Additionally, it was indicated that the degree of digital maturity affects how well a company performs in digital innovations (Çallı & Çallı, 2021). A company’s digital orientation and capability have a positive effect on its digital innovation capability, and digital innovations have a mediating role in the link between digital capability, technology orientation, and firm performance (Khin & Ho, 2019).

Digital transformation is commonly acknowledged as the primary force behind capturing innovation possibilities and generating value (Vial, 2019) as a result of enhancing collaboration and knowledge management (H. Wang et al., 2024). Previous studies have proved that digitalization has a significant impact on knowledge management practices (Sijabat, 2022). Utilizing a knowledge-based view (KBV), knowledge enables one to assess the success of digitalization and boost corporate performance. Based on KBV, knowledge generates innovation and enhances competitiveness (Viswanathan & Telukdarie, 2021; Yli-Renko et al., 2020). According to Xia et al. (2024), the digitalization of business processes as a part of digital transformation has a direct influence on organizations’ innovativeness. Tacit knowledge from different units is collected, integrated, and shared, and explicit knowledge formation is supported.

Knowledge management techniques are consistently promoted and believed to enhance corporate performance through their capacity for creativity (Lai et al., 2022). Since digital procedures make it easier to be close to consumers, company digitalization can increase business performance, especially among MSMEs (Domi et al., 2020). Such a focus on the consumer motivates MSMEs to create distinctive strategies for satisfying customers’ requirements, boosting sales, and maximizing profitability (Sijabat, 2022). On the other hand, there are also mixed findings in the literature. According to the study of Fu (2022), intra-organizational and inter-organizational knowledge sharing via ICT utilization affects administrative or technological innovativeness differently.

H. Wang et al. (2024) indicated that although existing research revealed the relationship between digitization and innovations, more comprehensive and detailed studies are needed. In addition, although (Tsou & Chen, 2023) explored the mediating effect of organizational innovativeness on the link between digital technology use and firm performance, the findings are specific to context as their study was conducted on finance firms. Therefore, the following hypothesis is proposed.

H9: ICT adoption (basic communication, internal integration, external integration, inter-organizational integration, and strategic integration) has a positive effect on organizational innovativeness

Firm Performance

Organizations’ ability to support their business processes with ICTs considerably impacts the firm performance (Domi et al., 2020). Aguegboh et al. (2023) explored how implementing ICT immediately affects bank performance. However, that study focused specifically on the banking industry and examined the adoption of ATMs. Similarly, Santos-Jaén et al. (2022) focused on a particular industry and proved that ICT adoption positively impacts firm performance in the hotel industry. For the SMEs in the manufacturing sector, Ab Wahab et al. (2020) also explored a positive relationship.

Sijabat (2022) concluded that the performance of Indonesian micro, small, and medium enterprises has been significantly and favorably impacted by business digitalization. Business analytics adoption enhances business process performance, and business process performance is related to firm performance. Business process performance was explored to have a mediating role in the relationship between business analytics adoption and firm performance (Aydiner et al., 2019).

The positive effect of digitalization on firm performance was also confirmed by Anbree et al. (2022). Nevertheless, digitalization was measured using a unidimensional construct, and data were gathered from seven SMEs. Li et al. (2023) explored that digitalization significantly affects the growth performance of manufacturing firms in China. However, ICT adoption or digitalization is a phenomenon that requires investigation from a broader perspective and assessing the complexity of implementation. Rollin et al. (2022) explored a positive link between ICT adoption and SME performance from the aspect of owners/managers in Uganda. While some researchers argue that it has a direct effect on competitive advantage (Hinze & Sump, 2019), some researchers argue that by revealing more innovative solutions, ICTSs will increase production costs and therefore decrease firm performance (Santos-Jaén et al., 2022; Thatcher & Oliver, 2001).

While Alma Çallı and Çallı (2021) also explored a positive relationship between digital maturity and firm performance, Wroblewski (2018) did not find a significant effect of digital maturity on performance. As a result of the controversy in the findings of previous studies and the lack of consensus regarding the direction of the relationship (Sirirak et al., 2011), there are still several systematic gaps in the literature about the relationship between ICT adoption and SME performance (Santos-Jaén et al., 2022). Therefore, the following hypothesis is proposed.

H10: ICT adoption (basic communication, internal integration, external integration, inter-organizational integration, and strategic integration) has a positive effect on firm performance

In the age of digitalization, the use of ICTs, knowledge management systems, and knowledge management activities significantly affect the performance of organizations (Agrawal et al., 2022). Organizations must evolve for survival, and their leaders and employees must be innovative to adjust the organization to outside changes and satisfy societal requirements (Tsou & Chen, 2023). Therefore, the following hypothesis is proposed in this study.

H11: Organizational innovativeness has a positive effect on firm performance

Mediating Role of Organizational Innovativeness

The hypotheses proposed above can be combined to explore the mediating role of organizational innovativeness. As the use of ICT in companies becomes more sophisticated, the development of innovations based on digitalization is also supported. Although technology is a prerequisite and requirement in companies, organizational innovativeness is necessary for sensing and implementing digitally-enabled growth opportunities (North et al., 2019). According to the digital maturity model developed by North et al. (2019), technology is a tool in the digital transformation journey. It supports digitally-enabled business models, processes, technology innovations, and organizational innovativeness. Organizational innovativeness developed through ICT contributes to the firm’s generation of digitally enabled innovations (Tsou & Chen, 2023). Besides, ICT adoption enhances local knowledge diffusion, networks, and collaboration capability, influencing innovativeness (Makanyeza et al., 2023).

Integration and communication with external parties develop the capability to innovate and boost the performance of innovations. Inter-organizational cooperation was also found to be an effective strategy that enhances innovations (Kim et al., 2023). Without digital technologies and digitization, both inter-organizational and intra-organizational communication and collaboration cannot be expected to take place. An organization may utilize ICTs to rearrange current business processes and establish new, effective organizational practices, facilitating product or service innovation to support firm performance (Li et al., 2023). This is possible when ICT adoption and innovativeness are well aligned inside the company. A prior study examined the mediating effect of innovations on the link between organizational culture and performance in the banking sector (Imran et al., 2022). From a broad perspective, culture is an important indicator of digital maturity (North et al., 2019), and ICT adoption is closely related to innovative culture. However, ICT adoption is more related to the technical aspect of digital transformation, and studies examining the relationship between the extent of ICT adoption, organizational innovativeness, and firm performance are limited.

Knowledge management, including knowledge gathering, storage, dissemination, and implementation, is closely linked with firm performance through the mediating impact of innovativeness. Previous studies revealed a positive relationship between knowledge management, organizational innovativeness, and firm performance (Limsangpetch et al., 2022). There is no comprehensive framework with empirical support that identifies the effect of organizational innovativeness on the link between digital technology use and firm performance (Tsou & Chen, 2023). Sijabat (2022) investigated the link between digitalization, knowledge management, and business performance and explored the mediating effect of knowledge management. However, the study has some methodological limitations, such as sample size and measurement of digitalization using an unidimensional scale. Marchiori et al. (2022) found that innovativeness has a mediating role in the link between IT capabilities and organizational performance. However, the focus of that study was different and used a capabilities-based approach.

SMEs, critical in value creation and employment, cannot achieve the expected outcomes and produce innovations, especially in developing countries. It has been determined that using a high level of ICT in Sri Lanka effectively achieves high innovation performance. However, the use of ICT and innovation performance are moderate. Thus, future studies might examine the mediating role that innovations play in the relationship between ICT usage and company performance (Weeramanthri et al., 2022). Because of this research gap, this work aims to examine if organizational innovativeness can be viewed as a transcendental instrument that determines the significance of this relationship by analyzing the indirect influence of ICT adoption on SMEs’ performance. Therefore, the following hypotheses are proposed.

H12a: Organizational innovativeness mediates the effect of basic communication component of ICT adoption level on enterprise’s overall performance

H12b: Organizational innovativeness mediates the effect of internal integration component of ICT adoption level on enterprise’s overall performance

H12c: Organizational innovativeness mediates the effect of external integration component of ICT adoption level on enterprise’s overall performance

H12d: Organizational innovativeness mediates the effect of inter-organizational integration component of ICT adoption level on enterprise’s overall performance

H12e: Organizational innovativeness mediates the effect of strategic integration component of ICT adoption level on enterprise’s overall performance

Methodology

Research Model & Hypotheses

Based on previous studies and research gaps, the proposed research model includes firm lifespan, size, and revenue as organizational characteristics and education, age, tenure, and ICT awareness (benefits and costs) as individual factors. The effects of these factors on the level of ICT adoption are examined. Further, the relationship between the level of ICT adoption and firm performance is analyzed, and the mediator effect of organizational innovativeness on this relationship is examined. The preliminary research model is presented in Figure 1.

Research model.

For the operationalization of this research model, a 15-item scale from the study of Tan et al. (2010), accepted as a reliable measurement of ICT awareness, was used to measure ICT awareness. In terms of ICT awareness, participants’ perceptions of possible benefits and barriers to ICT adoption are measured. The 16-item innovativeness scale of C. L. Wang and Ahmed (2004) was adapted to measure enterprises’ innovativeness. 6-items-overall performance scale was adapted from Khandwalla (1977). Scales measuring ICT adoption level, ICT awareness and innovativeness, incorporating dimensions of behavioral innovativeness, product innovativeness, process innovativeness, market innovativeness, and strategic innovativeness, which is commonly used in ICT and digitalization-related studies. 6-items-overall performance scale, widely used to evaluate the overall performance of firms in literature, was adapted from Khandwalla (1977). Scales measuring ICT adoption level, ICT awareness and innovativeness were based on a five-point Likert Scale.

ICT adoption’s multidimensionality was previously proven by researchers (Alma et al., 2018; Kotelnikov, 2007; Redoli et al., 2008; Shiels et al., 2003; Venkatraman, 1994). Based on those studies, communication, internal integration, integration with customers (mainly focusing on external integration), inter-organizational integration, and strategic integration dimensions were suggested by Özşahin et al. (2022) for examining the level of ICT adoption in SMEs. Accordingly, 30 items were measured utilizing a five-point Likert-type scale.

Research Setting

The Marmara Region, the most industrialized region in Turkey with the highest number of SMEs, was chosen to draw the study sample. Thus, non-probability sampling was employed by applying a convenience sampling approach. Whereas non-probability sampling has limitations because of subjectivity in the sample selection process and constraints regarding the representation of the population, when working with large populations, it is acceptable as randomization is not achievable (Etikan et al., 2016).

Data Collection

Owners, top-level managers, middle-level managers, first-line managers, and white-collar employees were asked to complete the questionnaire (519 people in total). However since owners and managers expected to be more knowledgeable about the business operations and strategy of their companies, their answers were considered for the analysis. In order to reflect more reliable information regarding the business enterprises, at least two responders from each SME are asked to complete the questionnaire. Nineteen forms were omitted because they failed to conform to the requirements, and 107 forms belonging to white-collar employees were excluded. Thus, data obtained from 393 owners and managers of 203 SMEs were analyzed through the SPSS. Descriptive statistics of the sample are presented in Table 1.

Descriptive Findings of the Sample.

Analysis and Findings

Data Analysis

Besides descriptive analyses, exploratory factor analysis and reliability analyses, correlation and regression analyses were utilized.

Reliability and Validity of the Scales

In order to assess the suitability of data for factor analysis, KMO (Kaiser Meyer Olkin) and Bartlett’s tests were conducted. KMO values exceeding 0.90 and statistically significant Bartlett’s values (p < .001) indicate the sampling is adequate for factor analyses (For KMO and Bartlett’s test values, see Appendix 1).

Firstly, exploratory factor analyses (EFA) were conducted on data obtained from 393 respondents to reveal the factor structure of the measures. Factor analysis was performed on 15 items of ICT awareness, 30 items of ICT adoption, and 22 items of organizational innovativeness and overall performance scales separately. The items with factor scores less than 0.50 and cross-loadings were removed for better factor structure. Hence, five items of ICT adoption with low factor loadings (less than 0.50) and three items with cross-loadings were eliminated. The remaining 22 items were loaded on five different factors without any cross-loadings. All items of ICT awareness were loaded on their respective two factors without cross-loadings. On the other hand, 22 items adopted from the literature to measure innovativeness and firm performance have been run together for EFA. Except for two items (Inv15 and Inv16), all items were loaded on their estimated factorial components without cross-loadings. So, the items of the strategic innovativeness dimension failed to form a factor. The items of market innovativeness and process innovativeness combined and loaded on the same factor. Thus, EFA results revealed a three-dimensional-organizational innovativeness model, as depicted in Appendix 1, although initial conceptual organizational innovativeness scale had five dimensions based on the literature. This may result from focusing on micro, small and medium-sized firms in a developing country context. Small firms are inherently less likely to be sophisticated in understanding and demonstrating innovations than large-scale firms in developed nations.

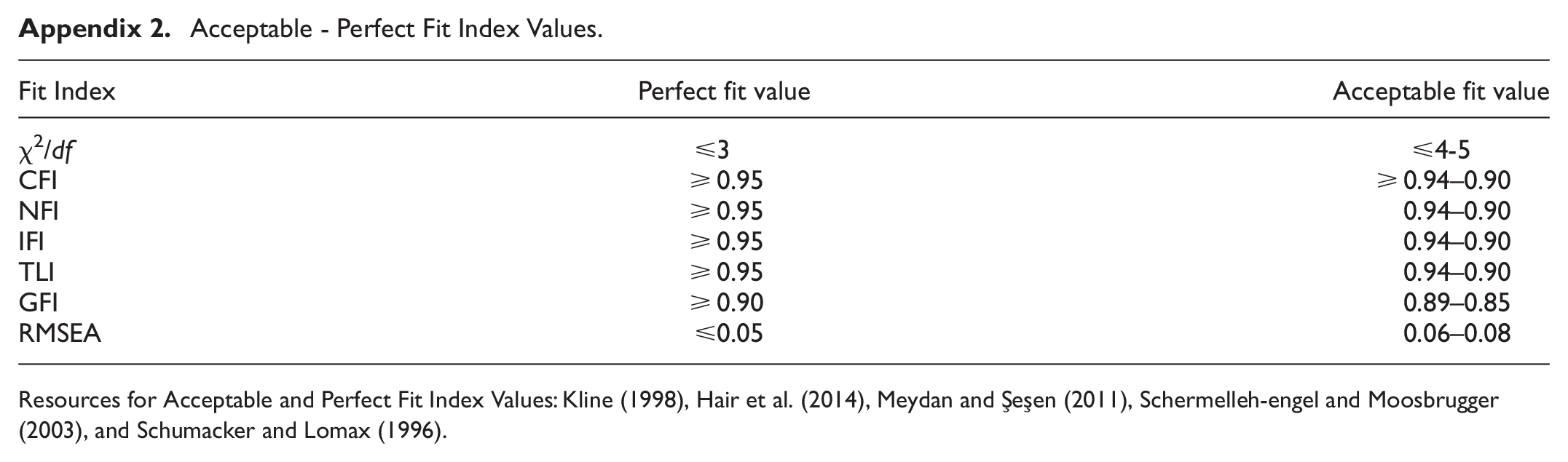

As the following step, CFA (Confirmatory factor analysis) with Maximum likelihood (ML) estimation method was also conducted on extended data obtained from 500 respondents to confirm EFA results and to test the revealed factor structure models for the constructs. Those 500 respondents include not only managers or owners of SMEs but also white-collar employees of SMEs. Before CFA, missing values were replaced by using the linear interpolation method. Parallel to the literature, the goodness of fit index (GFI), comparative fit index (CFI), incremental fit index (IFI), normed fit index (NFI), and Tucker-Lewis index (TLI), were considered for CFA. If all these indexes (CFI, GFI, NFI, IFI, TLI) are above 0.90, it indicates the perfect fit value and the model is ideal (Hair et al., 2014). However, some other researchers indicate that values above 0.85 are also acceptable fit indices, as represented in Appendix 2 (Schermelleh-engel & Moosbrugger, 2003; Schumacker & Lomax, 1996). As demonstrated in Table 2, most values are above 0.90, indicating better factor structures for each construct. Root mean square residual of approximation (RMSEA) was also considered, which indicates a better fit if it is lower than 0.08. RMSEA values depicted in Table 2, which are below 0.080, indicate also better-fit indices for all constructs. Moreover, to assess the reliability of measurements, Cronbach’s alpha and construct reliability (CR) coefficients were considered as it was suggested by Hair et al. (2014). Cronbach’s alpha reliability and construct reliability (CR) coefficients exceeding .70, depicted in Table 2, indicate the reliability of measurements. Moreover, as Hair et al. (2014) stated, higher CR coefficients (mostly exceeding 0.80) also indicate that internal consistency exists. Besides, the square root of AVE (average variance extracted) values exceeding 0.50, which are presented in Table 2, indicate the discriminant validity of the constructs (Fornell & Larcker, 1981; Hair et al., 2014).

CFA and Reliability Analysis Results.

Note. BC = basic communication; INTI = internal integration; EXTI = external integration; IOI = inter-organization integration; STRI = strategic integration; PB = perception on ICT benefits; PC = perception on ICT costs; INVB = behavioral innovativeness; INVMP = process-market innovativeness; INVP = product innovativeness; FP = firm performance.

Hypothesis Testing

Hierarchical regression analyses were conducted on 203 observation data to test the research model and hypotheses. Data obtained from 393 respondents were aggregated into 203 firms before regression analyses were conducted. Moreover, four sub-dimensions of innovativeness were combined to form a higher-order construct—organizational innovativeness.

Identifying the ICT adoption level predictors constitutes the research model’s first part. Researchers proposed that organizational characteristics of SMEs in terms of size, lifespan, industry and annual revenue of SMEs (H1-H2-H3), demographic characteristics of owners/managers of SMEs in terms of age, education (H4-H5-H6) and ICT awareness of owners/managers of SMEs (H7-H8) affects the ICT adoption level of SMEs. To test those hypotheses, linear regression analyses were executed. The results of regression analyses indicated that the owner’s/manager’s education level is positively related to four components (β = .475, p = .000 for basic communication; β = .361, p = .000 for internal; β = .187, p = .040 for inter-organizational and β = .213, p = .016 for strategic integration) of ICT adoption level (Table 3). Moreover, regression analysis findings on Table 4 revealed that the owner’s/manager’s awareness of ICT benefits and costs has significant effects on components of ICT adoption level. The awareness related to ICT benefits has a positive impact on basic communication (β = .188 p = .010), internal integration (β = .366 p = .000), external integration (β = .332 p = .000), inter-organizational integration (β = .306 p = .000) and strategic integration (β = .386, p = .000), whilst awareness related to ICT costs affects basic communication (β = −.356 p = .000), internal integration (β = −.355 p = .000), inter-organizational (β = −.199, p = .007) and strategic integration (β = −.257 p = .000) negatively. Briefly, higher awareness of owners/managers on ICT benefits increases the ICT adoption level, while their awareness on ICT costs decreases the ICT adoption level of the SMEs overall.

Demographics Characteristics –ICT Adoption Relations.

*p ≤ .05. **p ≤ .01. ***p ≤ .001.

ICT Awareness-ICT Adoption Relations.

*p ≤ .05. **p ≤ .01. ***p ≤ .001.

To examine the relationships among the components of ICT adoption level, organizational innovativeness and overall firm performance, hierarchical regression analyses were performed. Baron and Kenny (1986) framework was followed to test the mediator roles of organizational innovativeness on the effects of ICT adoption level components on firm performance. Accordingly, the findings of hierarchical regression analyses depicted in Table 5 indicate the mediating role of organizational innovativeness on the effects of internal and strategic integration components of ICT adoption on firm performance. Therefore, H12b and H12e are supported. Sobel (1982) test results also showed that the indirect effects were statistically significant (z = 5.50, p = .000 for integral integration and z = 5.18, p = .000 for strategic integration).

Regression Analysis Results on The Mediator Effect of Organizational Innovativeness on ICT Adoption Components and Firm Performance Relationship.

*p ≤ .05. **p c .01. ***p ≤ .001.

To test the robustness of the mediation analysis, an alternative mediation model was also tested in which organizational innovativeness was the independent variable, internal and strategic integration were mediator variables, and firm performance was the dependent variable.

The results of alternative mediation analyses showed that the significant effect of organizational innovativeness on firm performance does not change significantly with the inclusion of internal integration and strategic integration components into regression analyses (Table 6), which indicates that the alternative mediation model is not significant. Hence, the robustness of the model indicating the mediator effect of organizational innovativeness on relationships between ICT adoption level and firm performance was validated.

Alternative Mediation Analyses Results.

*p ≤ .05. **p ≤ .01. ***p ≤ .001.

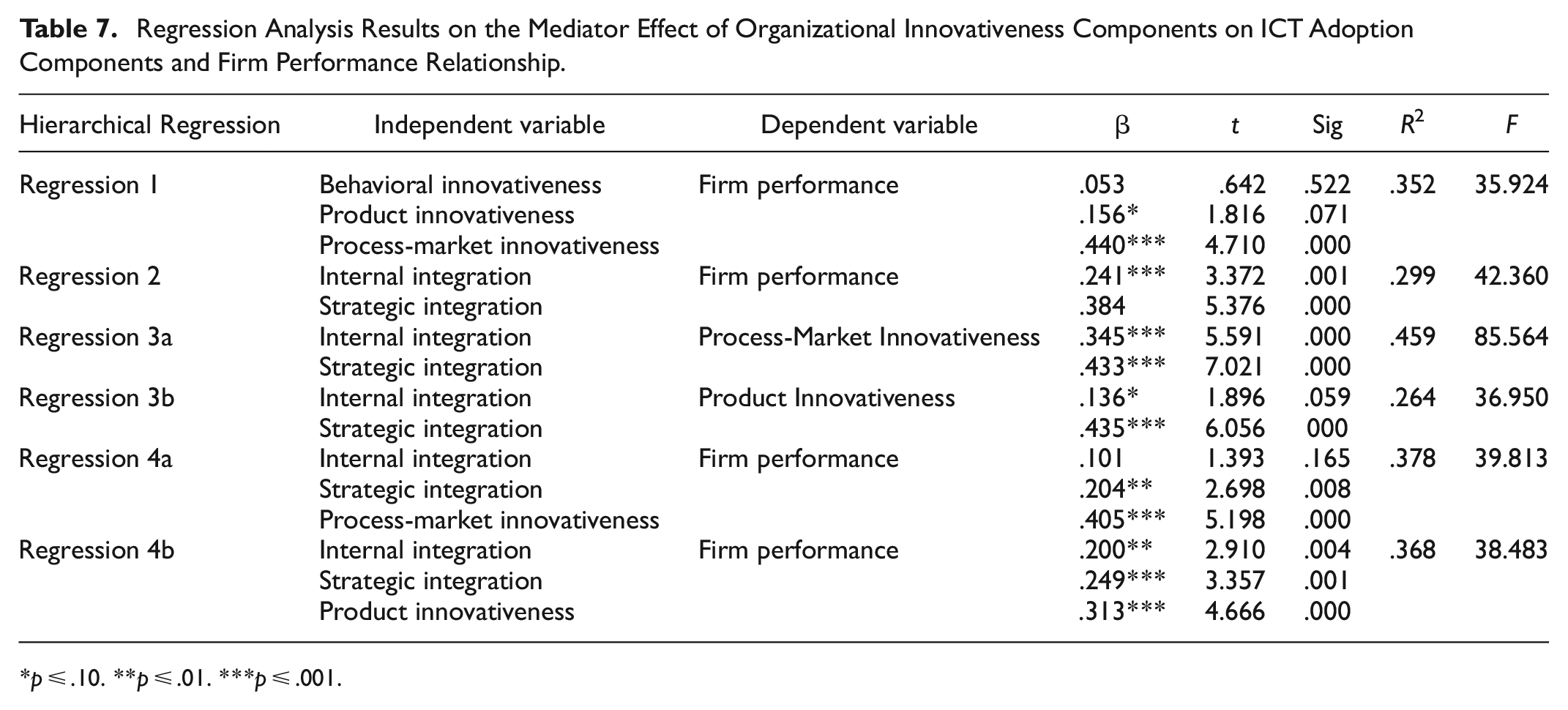

In order to identify which components of organizational innovativeness mediate the effects of internal integration and strategic integration components of ICT adoption level on firm performance, the components of organizational innovativeness were analyzed one by one. In this context, first the effects of organizational innovativeness components on firm performance were examined through a regression analysis, which revealed the significant effects of product innovativeness and process-market innovativeness on firm performance (β = .156, p ≤ .10 and β = .440, p ≤ .001 respectively). Thus, product innovativeness and process-market innovativeness components of organization innovativeness were approached in order to search for the mediating effects on relationships between ICT adoption levels and firm performance.

As depicted in Table 7-Regression 4a, the effects of internal integration and strategic integration on firm performance decrease significantly with the inclusion of process-market innovativeness in the regression analysis (β = .101, p = .165 for internal integration and β = .204, p = .008 for strategic integration), which indicates the mediating role of process-market innovativeness on the link between internal integration and strategic integration and firm performance. Sobel (1982) test results also showed that the indirect effects were statistically significant (z = 5.69, p = .000 for integral integration and z = 5.32, p = .000 for strategic integration). On the other hand, the effects of internal integration and strategic integration on firm performance decrease but not significantly with the inclusion of product innovativeness in the regression analysis, which means the partial mediating role of product innovativeness on the relations of internal integration (β = .200, p = .004) and strategic integration (β = .249, p = .001) to firm performance (Table 7). SOBEL tests were also conducted on 203 observation variables to examine the indirect effect of internal and strategic integration components of ICT adoption level on overall firm performance. Sobel (1982) test results (z = 5.69, p = .000 for internal integration and z = 5.32, p = .000 for strategic integration) indicates the indirect relationships between internal and strategic integration components of ICT adoption and firm performance, which may also provide evidence for mediating effects of process-market innovativeness and product innovativeness. As a result, summary of hypotheses testing is presented in Table 8.

Regression Analysis Results on the Mediator Effect of Organizational Innovativeness Components on ICT Adoption Components and Firm Performance Relationship.

*p ≤ .10. **p ≤ .01. ***p ≤ .001.

Summary of Hypotheses Testing.

Figure 2 presents the research model after the findings of the regression analyses.

Research model.

Discussion and Conclusion

Results and Discussions

This study examined the factors that were previously proposed as determinants of ICT adoption in SMEs. The conceptual model proposed by Alma Çallı et al. (2019) was used as a foundational model since it is comprehensive and uses the TOE framework, which is widely used for understanding ICT adoption in organizations. Besides, as Taylor (2019) stated, testing and verifying prior conceptual models in different contexts is necessary. Accordingly, this study is expected to make a theoretical contribution to the literature in this manner.

Firm revenue, education, and ICT awareness of the owner/manager were explored as factors affecting ICT adoption in this study, supporting the conceptual model presented by Alma Çallı et al. (2019). The hypotheses were confirmed for all components of ICT adoption. In this context, the findings of this study related to ICT awareness are in line with the findings in the qualitative study of Özşahin et al. (2020). It is an important finding that, contrary to our hypotheses, organizational variables such as company size, lifespan and variables such as age and tenure of the company owner/manager do not have a significant effect on ICT adoption. In this context, it is expected that the complex findings of past studies on the relationship between company size and ICT adoption will be clarified to some extent. The findings of this study contradict the argument of Duc and Nguyen (2023), who suggest that firms that are larger in size use technology more effectively. Additionally, this finding is not in line with the results of Kossaï et al. (2020) and Özşahin et al. (2020) Besides, contrary to what conceptual models suggest (Alma Çallı et al., 2019; Taylor, 2019), the effect of size on ICT adoption has not been theoretically confirmed. Previously, Alma and Coskun (2018) empirically suggested that size is effective, but that study is based on a very limited sample. Additionally, the sector and technology examined in the study of Kossaï et al. (2020) may have caused differences since ICT adoption in advanced manufacturing and the electronics sector were investigated. In this context, it is clear that sectoral characteristics and specific technology adoption may have caused differences. It is important that studies conducted on different sectors according to their level of digitalization reveal a different perspective in terms of interpreting the overall situation. Again, as put forward by Duc and Nguyen (2023), although past studies have revealed the existence of the size-ICT adoption relationship, some important studies have revealed that it is easier for small companies to benefit from technology due to their flexibility and agility. Accordingly, since this study evaluates the sophistication of digitalization, complex digitalization projects that may lead to more organizational complexity in relatively large companies may have caused this finding. This finding also seems to contradict the study of Neirotti et al. (2018), which explored firm size as an indicator of ICT-based capabilities. In this regard, the argument of Cataldo and McQueen (2014), Revilla and Fernández (2012), who suggested that contextual factors cause differences between studies, was supported.

In addition, the findings of Singh et al. (2022) stating that lack of awareness of owner/manager is one of the most common barriers to technology adoption in developing country SMEs, were also supported. The study of Singh et al. (2022) was carried out in Indian MSMEs, and the authors stated that studies conducted in different developing countries will contribute to the literature. In this respect, this finding is important and reveals the importance of ICT awareness of owners/managers for enhancing the adoption and use of ICT in developing countries that show some similarities. In addition, regarding technology adoption decisions, (Abdullah et al., 2012; Birley, 1982; Cannon, 1985; Thong, 1999) that put forward the argument that the owner/manager’s tendency, attitude, and willingness to use technology are effective in their decisions have been confirmed. This finding is also in parallel with Roberts et al. (2021) and Annosi et al. (2019). However, Annosi et al. (2019) specifically focused on technology 4.0 in agricultural SMEs which demonstrate lower levels of awareness as authors stated. However, this study made a distinction related to cost-benefit awareness and concentrated on a wide range of sectors.

Depending on the considerable role of owners in determining ICT adoption decisions, owners’/managers’ perceptions of the benefits and costs of the ICT adoption would lead to the adoption of ICTs that may require remarkable changes in the organization. Hence, owners’/managers’ awareness of benefits promoting a high level of engagement in organizational ICT practices is a critical factor for understanding and fostering ICT adoption in SMEs. On the other hand, the perception of owners/managers that ICT adoption will bring different obstacles, costs and disadvantages for the business has been identified as a negative influencer of ICT adoption. Accordingly, for promoting and enlarging the scope of ICT practices, awareness related to costs is also a considerable determinant that should be focused on and understood from the aspect of owners/managers.

Lack of financial resources was also identified by Elhusseiny and Crispim (2022) as one of the most common barriers to ICT adoption in developing countries compared to developed countries. In this direction, in this study, firm revenue, which is linked with a company’s financial resources, was among the significant indicators of ICT adoption. Also, in relation to this, Lu et al. (2019) confirmed that ICT use of SMEs is associated with annual sales turnover, and they did not find a significant difference between firms in terms of age. However, the findings of that study are specific to the construction sector. The financial constraints and unbalanced investments were also proposed by Singh et al. (2022) as common barriers in developing country SMEs. However, Elhusseiny and Crispim (2022) and Singh et al. (2022) conducted reviews and produced conceptual arguments which require empirical investigation. Again, in this study, in contrast to the studies of Alma Çallı et al. (2019), Özşahin et al. (2020), factors such as lifespan and age of the owner/manager were not identified as factors affecting ICT adoption. In this context, the findings of this study also contradict the study of Kusuma et al. (2020), who found age and year in business as determinants of ICT adoption in SMEs.

These inconsistent findings may be attributed to the conceptualization and measurement of ICT adoption. Past studies have generally tended to explore the use of different technologies within the organization rather than a holistic ICT implementation. Therefore, demographic differences can be expected to be more influential in investment decisions related to the application of specific technologies. In connection with this, this study, focusing on the extent of ICT adoption and its components, produced different results as expected. Duc and Nguyen (2023) stated that the relationship between firm size, ICT adoption, and performance should be investigated in various contexts, such as different developing country SMEs operating under similar conditions. Therefore, particular contextual elements are believed to cause differences between the findings of prior studies and this research.

It was also explored that ICT adoption has a positive effect on firm performance. Nevertheless, associated hypothesis was partially accepted. It was found that only internal integration and strategic integration dimensions has a positive influence on firm performance. This outcome is in line with the studies of Vilkas et al. (2022), Xia et al. (2024) revealing positive link between digitalization and innovativeness. Domi et al. (2020) also indicated that digital procedures can increase business performance, particularly in MSMEs. However, there are controversial findings. For instance, according to Fu (2022), intra-organizational and inter-organizational knowledge sharing via ICTs influences administrative and technological innovativeness differently. This finding highlights that different levels and different dimensions for ICT adoption have different effects on innovativeness, as it was previously emphasized in this research. A significant link between external integration and organizational innovativeness was not explored. It may be problematic for SMEs with limited resources to achieve full integration at the external integration level. Efforts to ensure coordination and synchronization with digital networks with external partners can have a negative impact on organizational innovativeness by reducing company agility. This argument can also apply to the relationship between ICT adoption and firm performance since it was found that only internal integration and strategic integration has a positive influence on firm performance. Strategic integration is related to use of decision support mechanisms and use of analytic solutions such as business analytics. The finding related to the positive impact of strategic integration on firm performance is consistent with Aydiner et al. (2019), who discovered that business analytics is related to firm performance. This finding is also in line with Ab Wahab et al. (2020), Santos-Jaén et al. (2022). Additionally, this specific finding supports the study of Aguegboh et al. (2023) proposing that ICTs immediately affect bank performance. Further, our finding is consistent with Sijabat (2022), Anbree et al. (2022), Li et al. (2023), and Rollin et al. (2022). Nevertheless, this finding contradicts the outcomes of researchers such as Wroblewski (2018). Researchers Santos-Jaén et al. (2022), Sirirak et al. (2011), and Thatcher and Oliver (2001) have suggested that there are different ideas and gaps in the literature regarding the direction and impact of this relationship.

However, previous studies concentrated on particular industries. Besides, consideration of sophistication of ICT practices and multidimensionality of ICT adoption is critical. Because, while for internal and strategic integration dimensions ICT adoption increases firm performance, a significant effect for other dimensions was not detected. That particular outcome is consistent with Santos-Jaén et al. (2022), Thatcher and Oliver (2001) since they indicated that ICTs may increase production costs and, therefore, decrease firm performance. External integration and inter-organizational integration may cause more complexities and dramatic change in the organization as a result of redesing of the business network and working together with other partners. Integration of the supply chain may cause new challenges for SMEs since organizational information systems should be opened, harmonized and integrated with other partners. In this case, environmental and organizational barriers may have been in the foreground and caused this outcome for SMEs in developing countries. Additionally, the mediating role of innovativeness was explored in this study. For this reason, it turns out that the effect of ICT adoption on firm performance is realized by increasing the firms’ innovations. In this respect, this study differs from studies that confirm the direct effect of digitalization on performance. In this regard, the findings of this study are actually parallel to the arguments of Vilkas et al. (2022), Xia et al. (2024), Ying et al. (2022), Çallı and Çallı (2021), Yang et al. (2020), and Vial (2019) confirming the connection between digitalization and organizational innovativeness. Besides, this outcome strengthens the existing body of literature suggesting that ICTs enhance innovativeness via developing knowledge diffusion, networks, cooperation, and communication (Li et al., 2023; Kim et al., 2023; Makanyeza et al., 2023).

Another significant finding is that the effect of organizational innovativeness on firm performance was detected. In this regard, this finding is consistent with the findings of Doğan and Doğan (2020) and Limsangpetch et al. (2022). Nevertheless, the most remarkable finding of this study is the mediating role of organizational innovativeness on the link between ICT adoption and performance. Examining in detail, only two components of ICT adoption (

Conclusion

Theoretical Implications

Understanding different factors determining ICT adoption in SMEs is essential for driving ICT utilization and improving its sophistication. Previous literature using the TOE framework has mostly focused on the determinants of the adoption of particular digital technologies. Hence, this study contributes to the field by examining the extent of ICT adoption in SMEs through a comprehensive assessment framework. Besides, previous studies have mostly examined the combined effect of sub-dimensions of organizational innovativeness and have neglected the mediating impact of different dimensions.

Although a considerable number of studies have utilized the TOE framework, determinants may be specific to the context, including sample characteristics and the adopted technology. This study adds to the ICT adoption literature in the context of developing country SMEs by successfully testing the TOE framework with organizational and individual characteristics. Although organizational characteristics such as size and lifespan have been widely examined and previously found antecedents of ICT adoption, this study did not find these factors as determinants of ICT adoption. Besides, exploring the significant role of the owner/manager and his/her attitudinal characteristics in ICT adoption decisions is a remarkable finding. For the context examined, owner/manager-related characteristics were found to be more critical for understanding and driving the ICT adoption in SMEs. Perceptions of the owner/manager related to the benefits and costs of ICT adoption are an important psychological factor. It is a valuable outcome for many organizations that encounter resistance to technology adoption but have to implement it for competitiveness. Owner’s/manager’s education is also an important driver of ICT adoption. Lack of education might affect perceptions of ICT adoption’s risks and benefits. These outcomes are also consistent with Roberts et al. (2021), who emphasized that a lack of technical understanding led to inaccurate risk perceptions among decision-makers who needed to fully comprehend the technology’s purpose, usefulness, or possible more enormous ramifications for their firm. This finding also aligns with Annosi et al. (2019), which stated that managerial cognition and perceptions related to external environment influence are linked with technology adoption.

A requirement of extending TOE by investigating the consequences of ICT adoption was also discovered since it is expected that the extent of ICT adoption and sophistication of ICT applications might influence performance differently. The literature reports that past research has widely investigated the link between ICT adoption and performance. However, it is necessary to reveal possible indirect ICT adoption effects and explain how different levels of ICT adoption enhance performance. For instance, the previous finding by Tsou and Chen (2023) was confirmed, demonstrating the significant mediating effect of organizational innovativeness on the link between digital technology use and firm performance and providing further understanding of how different levels of ICT use and adoption affect different types of innovativeness and performance.

Given the prior studies that conceptually propose that organizational innovativeness affects performance, different types of organizational innovativeness as mediating factors were considered and empirically tested for its mediating effect on the link between ICT adoption and performance. Dimensions of innovativeness, including product and process & market innovativeness, were found as significant mediating factors. Another important finding is that only internal and strategic integration among the sub-dimensions of ICT adoption is associated with innovation and performance. Internal integration for this study was conceptualized as using and combining internal sources and capabilities for keeping and creating knowledge.

When it comes to strategic integration, according to Shiels et al. (2003), strategic integration integrates the characteristics of internal, external, and inter-organizational levels. It requires utilizing digital technologies to improve communication and information exchange within the organization and its business network. Accordingly, based on the conceptualization of this study, strategic integration is characterized by data integration from internal and external systems for analyzing customer and market data and decision-making for strategic issues. Therefore, strategic integration is expected to trigger and increase product, process & market-based innovations and enhance performance through innovativeness. Besides, different dynamic capabilities of the organizations might also affect the link between different levels of ICT adoption and innovativeness. For instance, Shen et al. (2021) discovered that organizations’ coordination and integration capabilities have a moderator effect and support enhancing innovation performance. Therefore, the impact of different types of dynamic capabilities organizations own might have caused this outcome. Specifically, when an organization creates a more suitable environment for employees to engage in innovative behaviors, it becomes easier to improve firm performance.

Practical Implications

From the managerial aspect, findings demonstrate that the tendency of organizations should be toward increasing the implementation of diverse digital technologies for achieving internal integration and then carrying this integration outside the organization to achieve a high level and comprehensive integration with all their partners in the ecosystem. This provides a learning capability which facilitates capturing new resources and ideas and combining them with internal capabilities. According to Shen et al. (2021), a high level of learning capability gives the opportunity to eliminate R&D costs and create new products. Managers’ in-depth understanding of ICT adoption and organizational innovations is required for firm performance. Process, product, and market innovations are important aspects that should be focused on. Owners/managers should hold a positive attitude toward ICT adoption with developing understanding regarding the benefits of a high level of ICT adoption and develop a strategy for change management to enhance innovations.

For promoting the adoption of ICTs in SMEs, perceptions, technical knowledge, and education for driving their perceptions should be taken into account. Government institutions dealing with SMEs, SMEs themselves, ICT consultants, and vendors can benefit from this research’s outcomes. SMEs’ digitalization rate can be enhanced by establishing suitable and appropriate strategies. This study suggests that SME owners/managers should concentrate on promoting innovative orientation. Entrepreneurial spirit and fostering an organizational culture of embracing proactiveness and innovativeness can enhance the level of ICT adoption and benefit from digitalization. Increasing innovations of SMEs should also be within the scope of government initiatives and programs. Initiatives for building networks among owners/managers can enhance knowledge dissemination and awareness of owners regarding the benefits of creative and innovative business ideas. Peer support and guidance can drive to establish new strategic positioning and motivate behavioral changes. Additionally, the reasons behind owners’ negative beliefs and attitudes are important. Support and incentives should be provided for anticipating these reasons and increasing owners’ awareness regarding the implementation of new technology and innovative practices. Special efforts can be put into providing training programs specifically designed for owners and organizations.

More tailored support for the technical skills and education of owners/managers can be provided to enhance their perceptions of addressing the digital gap among SMEs. Awareness and training programs presenting knowledge through online platforms can support owners in enhancing their digital skills.

Limitations and Future Directions

Even though research outcomes contributed to acquiring new insights, this study has some limitations that future studies can answer. First, a longitudinal study design could be better at anticipating causality than a cross-sectional study design. Additionally, this study focused on SMEs in Turkey using convenience sampling, which makes the generalization of the findings to other contexts ambiguous. This study focused on a subset of individual and organizational characteristics due to discovering some research gaps. For instance, to the best of our knowledge, this is the first study investigating the mediating impact of different types of organizational innovativeness on the link between different levels of ICT adoption and performance. Hence, this study’s scope was defined to address those issues. However, integrating a different mix of variables and examining different relationships between variables are among the future research goals of researchers. Findings might guide future research aiming to establish and test different research models. The model proposed might be adopted for different contexts and for cross-cultural studies. Of course, repeating a similar study with a more extensive data set would produce more reliable results. This can be considered an exploratory study to determine the framework.

Footnotes

Appendices

Acceptable - Perfect Fit Index Values.

| Fit Index | Perfect fit value | Acceptable fit value |

|---|---|---|

| χ2/df | ≤3 | ≤4-5 |

| CFI | ≥0.95 | ≥0.94–0.90 |

| NFI | ≥0.95 | 0.94–0.90 |

| IFI | ≥0.95 | 0.94–0.90 |

| TLI | ≥0.95 | 0.94–0.90 |

| GFI | ≥0.90 | 0.89–0.85 |

| RMSEA | ≤0.05 | 0.06–0.08 |

Resources for Acceptable and Perfect Fit Index Values: Kline (1998), Hair et al. (2014), Meydan and Şeşen (2011), Schermelleh-engel and Moosbrugger (2003), and Schumacker and Lomax (1996).

Author Note

This study is the extended version of the conceptual study presented as a short paper in the 12th IADIS International Conference Information Systems.

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.

Data Availability Statement

Data sharing not applicable to this article as no datasets were generated or analyzed during the current study.