Abstract

This study investigates how the social connections of independent directors influence the disclosure of corporate social responsibility (CSR) information. Using data from Taiwanese firms listed on the stock market between 2013 and 2019, we employ the propensity score matching (PSM) method to compare the social networks of independent directors in firms that disclose their CSR reports with those that do not. Our findings reveal that disclosing CSR reports positively affects the centrality of independent directors’ social networks. In other words, directors who participate in CSR reporting have greater influence and better access to information within their social circles. This effect is particularly pronounced for firms with more analysts following them. Additionally, our study demonstrates that having more central and well-connected independent directors, along with increased analyst coverage, leads to greater CSR disclosure by firms. These results highlight the importance of diverse and robust social capital in enhancing transparency and promoting sustainable development for organizations.

Introduction

Different theories and factors shape corporate social responsibility (CSR) and corporate governance. One such factor is the social network of independent directors, which reveals their connections to other directors. This network facilitates firms in accessing external resources and adhering to unwritten norms. Freeman (1977) proposed a method to gauge the significance of a director within their social network. This measurement reflects the extent of their influence over available resources. The approach employs three key metrics, degree centrality, betweenness centrality and closeness centrality (Freeman, 1977; J. Zhang & Luo, 2017). These centrality measures reveal the ease or difficulty for a firm to acquire external resources. Additionally, they assist firms in mitigating risks, bridging information gaps, making informed decisions, and fostering creativity. Ultimately, these strategic efforts can contribute to increased profitability.

Another critical factor influencing corporate behavior is the attention of financial analysts. These analysts play a pivotal role in gathering and disseminating information within the financial market. They meticulously study firms’ value and future prospects, offering their views and forecasts. Their assessments can significantly impact stock prices and funding costs. By sharing their insights with the financial market, analysts contribute to narrowing information gaps and reducing information asymmetry (Naqvi et al., 2021). Moreover, analysts act as vigilant overseers, ensuring that managers utilize financial resources and human capital effectively. Their scrutiny enhances transparency and accountability within organizations (Brauer & Wiersema, 2018).

According to social capital theory, social capital encompasses the bonds and trust between individuals, influencing their behavior and actions (Coleman, 1988). It also encompasses the social network connections among individuals, rooted in shared norms of mutual benefit and trust (Ferraris et al., 2020; S. K. Singh et al., 2021). In this context, CSR, social networks, and analyst attention can all be viewed as forms of social capital, with interrelated dynamics. Numerous studies have demonstrated that CSR practices, board composition, and analyst coverage impact corporate performance. Regarding independent directors serving on boards, existing research often examines their roles (Gutiérrez & Sáez, 2015) or assesses their value (Giannarakis et al., 2020; Nguyen & Nielsen, 2010). However, the connection between independent director networks and CSR tends to focus on how these directors influence CSR initiatives (Barka & Dardour, 2015; Chiu et al., 2013). Notably, there has been limited discussion about whether participants in CSR activities consider the benefits of their social network positions when selecting independent directors.

This research investigates into the intricate relationship between CSR involvement and the social networks of independent directors. CSR involvement significantly enhances a firm’s image, reputation, performance, and overall value, as evidenced by prior studies (Cornell & Shapiro, 1987; Du et al., 2010; Fourati & Dammak, 2021; Servaes & Tamayo, 2013). The centrality of independent directors reflects their leadership, popularity, and reputation within the corporate context, drawing from theories such as Bourdieu (1986), Kaczmarek et al. (2014), and Masulis and Zhang (2019). Additionally, it investigates whether analyst coverage plays a moderating role in this dynamic.

Notably, Taiwan has publicly underscored the significance of CSR development. This emphasis has catalyzed the formulation of relevant policies and guidelines aimed at fostering corporate engagement in CSR initiatives. Since 2014, the Taiwanese government has leveraged legislation to encourage listed companies, meeting specific criteria, to prepare annual CSR reports. Furthermore, beginning in 2025, these companies will be mandated to integrate CSR reports into their annual reports. Remarkably, Taiwan stands as the pioneering in Asian region to implement such compulsory regulations. This progressive approach is further bolstered by proactive advocacy from Non-Governmental Organizations (NGOs) and enterprises’ unwavering commitment to transparent management and environmental sustainability.

Therefore, our study focuses on samples from Taiwan-listed firms during the period spanning 2013 to 2019. Employing social network analysis, we assess the centrality of independent directors and investigate the relationship between their CSR involvement and social networks. Additionally, we examine the impact of analyst coverage on the social networks of independent directors. These networks, in turn, play a crucial role in shaping social and environmental performance while mitigating information asymmetry within firms. Naqvi et al. (2021) have demonstrated that firms with greater transparency tend to attract heightened analyst attention.

Our findings reveal a positive impact of CSR involvement on independent directors’ social networks. Moreover, we observe a distinct positive effect on the social networks of independent directors in firms actively engaged in CSR initiatives. Notably, this effect is more pronounced in high analyst coverage firms compared to those with lower analyst coverage. These results offer valuable insights for stakeholders, enabling them to understand the motivations and benefits behind a firm’s CSR activities.

This research underscores the importance of regulators and policymakers encouraging firms to disclose their CSR reports and activities. Such transparency not only enhances social and environmental performance but also contributes to overall corporate governance quality. Independent directors play a pivotal role in overseeing and advising management on CSR matters. Leveraging their social networks, they can access valuable resources and information for the firm. Furthermore, analysts wield influence over firms’ CSR disclosure behavior. Their attention and feedback, along with the dissemination of CSR information to the public, shape firms’ practices. Stakeholders should closely monitor the social networks of independent directors and the analyst coverage of firms. These factors serve as indicators of the firm’s transparency and accountability.

This paper is structured as follows. Section 2 offers an overview of the related literature and articulates our hypotheses. Section 3 engages in a discussion concerning the sample, CSR measures, independent director social network centrality, and other control variables. Section 4 presents our research design, followed by an exposition of our empirical results. Section 5 encapsulates our key findings and conclusions.

Literature Reviews and Hypothesis

Independent Directors’ Social Networks

This study examines the role of social networks in promoting information exchange among independent directors in society. Serving as complex communication platforms, social networks create synergistic benefits for collaborative initiatives. Through the dissemination and reciprocation of information, directors can surmount their informational limitations. Traditional geosocial science research utilizes social network analysis to understand the structure and dynamics of these networks (Freeman, 2004).

Sociologists have significantly advanced the social network approach by integrating theoretical frameworks and applying them to both formal and informal social relationships. They’ve emphasized structural features like the relative positions of nodes within the network and introduced concepts like block modeling and multidimensional scaling to refine social network techniques (Wasserman & Faust, 1994). The social network theory identifies three key centrality measures: degree, betweenness, and closeness, which reveal the advantageous positions often held by opinion leaders (Freeman, 1977). Degree centrality quantifies an individual’s ties within a network, betweenness centrality assesses how frequently an individual connects other nodes in the network, and closeness centrality reflects how efficiently an individual can reach everyone else. These measures provide valuable insights into the dynamics of social networks and the influential roles played by specific individuals.

The Resource Dependency Theory (RDT) suggests that firms, viewed as open systems, obtain crucial resources through reciprocal exchanges and mutual trust with other firms (Bryant & Davis, 2012; Pfeffer & Salancik, 1978; Zaman et al., 2022). Independent directors, who serve on multiple boards, can offer benefits such as new knowledge, diverse information, reduced environmental uncertainty, and signals of quality improvement (Drees & Heugens, 2013; Xie et al., 2021; Zona et al., 2018). According to RDT, firms rely on external resources and engage in transactions to mitigate environmental uncertainty and dependence (Zaman et al., 2022). However, these transactions may lead to agency problems when the interests of principals and agents diverge, as pointed out by Fama and Jensen (1983). Agency Theory (AT) recommends monitoring and controlling agent behavior to align incentives and minimize opportunism (Bebchuk et al., 2017). On the other hand, Social Capital Theory (SCT), as highlighted by Coleman (1988) and Nahapiet and Ghoshal (1998), provides a perspective on how the social networks of firms and their agents influence their resource dependence and agency relationships. SCT posits that social networks are a valuable source of social resources that can enhance performance and well-being (Aklamanu et al., 2016; X. Zhang et al., 2017). For instance, firms and agents with higher social network centrality can access more diverse and unique information, and acquire more knowledge, respectively, reducing their environmental uncertainty and dependence, and benefiting the firms they serve (Xie et al., 2021; Zona et al., 2018).

While Social Capital Theory (SCT) recognizes the advantages of social networks, it also acknowledges the associated costs and risks, such as obligations, conflicts, opportunism, and free-riding, which can potentially impact the performance and well-being of individuals and organizations negatively (Adler & Kwon, 2002; Granovetter, 1973; Mond, 2022). For instance, firms with a higher degree of social network centrality might face increased competition and pressure from their external partners, leading to increased environmental uncertainty and dependence, as noted by Hillman et al. (2009). Similarly, agents with a high degree of social network centrality might prioritize their own interests or those of their other affiliations over the principals they represent, resulting in agency problems (Raymond, 2006; Stevenson & Radin, 2009). SCT can shed light on how the social networks of firms and their agents can both support and impede their resource dependence and agency relationships. It also provides suggestions on how firms and their agents can manage their social networks to optimize resource acquisition, governance, and performance. For instance, firms and their agents can balance their social network centrality and diversity to access more information and resources without becoming overly dependent on or creating conflicts with their external partners (Burg et al., 2022). Furthermore, by fostering trust and reciprocity with their external partners, firms and their agents can reduce opportunism and enhance cooperation (Alghababsheh & Gallear, 2021; Gulati & Nickerson, 2008). Numerous studies have confirmed that independent directors with a higher degree of social network centrality can benefit the board of directors in various ways, such as obtaining information, disseminating information, and accessing resources (Nicholson et al., 2004; A. V. Shipilov et al., 2010; A. Shipilov & Gawer, 2020).

CSR and Independent Director’s Social Networks

Corporate governance, a set of mechanisms that guide and control a firm (D. Singh & Delios, 2017), is designed to align with the interests of various stakeholders, including the board of directors, senior management, shareholders, among others. The social network of independent directors (Braun et al., 2019) fosters a conducive environment for the firm by offering rich experience, knowledge, and external connections (Intintoli et al., 2018), which influence the firm’s decision to engage in CSR. The central issue is how the network of independent directors impacts the board’s decision-making process. Through the reliable and cost-free function of information dissemination and diffusion (Chiu et al., 2013; Guo & Hao, 2021), the firm can enhance its CSR performance. SCT defines social capital as the aggregate of material or human capital that can be accessed through one’s position in the social network (Adler & Kwon, 2002; Cai et al., 2021). The value of social capital resides in the exchange of key information accessible in social networks (Asamoah et al., 2020; Foa & Foa, 1980). Thus, the more central the position of the firm’s independent director social network, the more accurate and timely information can be obtained. This capability is vital for creating more opportunities for the firm to meet stakeholder needs.

The social impact hypothesis, proposed by Cornell and Shapiro (1987), posited that CSR can bolster the firm’s external image, reputation, and consumer trust, and diminish its implicit liabilities, leading to improved financial performance. The social network of independent directors is a crucial factor influencing the firm’s CSR participation. Independent directors, who are external directors not holding shares in the firm, can offer unbiased and beneficial policies for the firm. Their social network connections are significant and serve as indicators of their leadership, popularity, or reputation. Social network centrality, an important indicator of who holds a key position in the network, is associated with more power, influence, and convenience from the network (Hochberg et al., 2007).

Independent directors with higher centrality are closer to the network center and can access more information and resources that can assist the firm in engaging in CSR. This suggests that the social network centrality of independent directors is positively correlated with the firm’s CSR participation. Therefore, this study proposes that the higher the social network centrality of independent directors, the higher the firm’s CSR participation. Consequently, we hypothesize that:

Hypothesis 1 (H1): The social networks of independent directors positively influence CSR participation.

Analyst Coverage and Independent Director’s Social Networks

Analyst coverage and director networks are important to corporate governance and financial decision-making. Analysts, by providing external oversight and disclosing information, bridge the information gap between firms and investors. They leverage their expertise to evaluate a firm’s past and future performance and share this information with stakeholders.

Analyst coverage has dual impacts. On one hand, it can reduce information asymmetry, decrease the cost of capital, and lessen the chances of fraud. On the other hand, it can lead to excessive optimism, short-termism, and agency issues. For example, investors may overvalue the stock price beyond its fundamental value (Chen et al., 2015). Additionally, managers might forgo long-term investments to meet short-term earnings targets, negatively affecting resource allocation efficiency (Irani & Oesch, 2016). Derrien and Kecskes (2013) demonstrated that firms with less analyst coverage encounter higher financing and investing costs, limiting their investment opportunities and profitability. Furthermore, Galanti et al. (2022) argued that analysts mitigate the problem of information asymmetry by disseminating public information such as earnings forecasts and investment recommendations, thereby reducing the cost of capital.

Analysts’ attention can also influence investor sentiment. Overexposure to firms covered by analysts may lead investors to pursue overvalued stocks, yielding lower future returns compared to less-covered and undervalued firms. Director networks also have a dual impact on firms. They can enhance board effectiveness, facilitate knowledge transfer, and improve firm performance. However, they can also lead to conflicts of interest, entrenchment, and cronyism. The interplay between analyst coverage and director networks can be intricate and context-dependent. Some studies suggest that analyst coverage can bolster director networks by offering additional monitoring and feedback. Conversely, other studies propose that analyst coverage can supplant director networks by diminishing the need for internal governance mechanisms.

Previous research has explored the individual effects of analyst coverage and director networks on corporate governance and outcomes. Analysts perform an external monitoring function, while directors offer internal oversight (Derrien & Kecskes, 2013; Galanti et al., 2022). Based on the interplay and complementary roles of analysts and directors, we propose the following hypothesis:

Hypothesis 2 (H2): There is a positive correlation between analyst coverage and the social networks of independent directors.

The Relationship of CSR, Analyst Coverage and Independent Director’s Social Networks

CSR is a practice that aims to generate value for both the firm and its stakeholders, which include society, the environment, and others, by implementing sustainable and ethical practices. CSR aims to optimize the value distributed among stakeholders while considering the social, environmental, and governance impacts of the firm’s activities over a specific period. As such, a CSR report can serve as a communication tool with stakeholders about the firm’s surplus profits (Gray et al., 1995; Viererbl & Koch, 2022). The independent board of directors mitigates agency issues and ensures the effectiveness of the firm’s CSR activities. These independent directors advocate not only for shareholders’ interests but also for those of other stakeholders (Haniffa & Cooke, 2005; Zaid et al., 2020). They oversee the firm to promote investment in sustainable solutions, decrease information asymmetry, and safeguard the firm’s reputation. Analysts, as experts in gathering, analyzing, and disseminating corporate information, provide unbiased information with a sense of social responsibility, which also acts as a supervisory function for stakeholders.

Reguera-Alvarado and Bravo-Urquiza (2022) discovered a positive correlation between CSR reporting and board size. This can be explained by the RDT proposed by Pfeffer and Salancik (1978), which posited that organizational behavior is influenced by external resources. The external resource of the independent director serves as social capital, which can provide the firm with a broader range of perspectives and roles in fulfilling CSR. A financial analyst assists firms in making business or investment decisions based on their knowledge of the industry and market trends.

Previous research found a positive correlation between CSR participation and analyst coverage, reflecting the firm’s reputation and investor recognition (Chun & Shin, 2018; Jo & Harjoto, 2014). Furthermore, sound corporate governance, such as having independent directors with professional knowledge and extensive social networks, can enhance board function and attract more attention from financial analysts. These financial analysts then offer informed guidance to the firm and investors on economic trends and financial strategy. This study seeks to explore the relationship between analyst coverage, the social networks of independent directors, and CSR participation. It aims to establish this connection empirically. Therefore, we propose the following hypotheses:

Hypothesis 3: Analyst coverage exerts a positive influence on CSR participation, and it also enhances the positive relationship between the significance of independent directors’ social networks and CSR participation.

Data and Descriptive Results

Data

We collect data from the Taiwan stock exchange’s Market Observation Post System (MOPS) to obtain a sample of public firms in Taiwan from 2013 to 2019. Financial firms and firms with incomplete data in the annual firm-level accounting data from the Taiwan Economic Journal (TEJ) dataset are excluded. This results in an unbalanced panel of 634 firms for our final sample. Information on the characteristics of independent directors is obtained from the TEJ corporate governance database. We quantify the connectedness of independent directors by calculating three types of social network centrality (degree, betweenness, and closeness) for each firm annually.

To represent a firm’s participation in CSR, we use a dummy variable that indicates whether a firm has issued a CSR report in a given year, which we source from MOPS. Our study investigates the influence of independent directors’ centrality and analyst coverage on CSR participation. Analyst coverage is defined as the number of analysts tracking a firm. In line with previous studies on CSR and related topics (Gentry & Shen, 2013; Thomas et al., 2018), we control for Return on Assets (ROA), firm size, book-to-market ratio, and leverage in our analysis, as these factors are known to influence CSR participation. ROA is calculated as net income over total assets, firm size is determined by the logarithm of total assets, book-to-market ratio is the book value over market value, and leverage is the total debt over total assets.

Independent Director Social Network Centrality Measures

We use data from the TEJ corporate governance database to establish measures of independent director networks for each firm-year in our sample. Two independent directors from different firms are deemed connected if they serve on the same board. By leveraging the start and end dates of each independent director’s tenure, we create a distinct adjacency matrix for each year from 2013 to 2019. This depicts the network structure for each year in our sample. As per Freeman (1978), there are three distinct centrality measures: degree, betweenness, and closeness.

Degree measures, the number of direct connections that each director has with other directors in the network. Degree centrality is based on Nieminen (1974), as the degree of adjacency between a director (pk) and other directors (pi):

Betweenness measures, the number of shortest paths between two directors in the network that pass through a director. Betweenness centrality was developed by Anthonisse (1971) and Freeman (1977). They considered the ability of a director (pk) to act as a bridge that has the potential to control information flow. Let gij be the number of possible paths between pi and pj. 1/gij = the probability of a path between pi and pj, and gij (pk) = the number of paths between pi and pj via pk. Then, the probability of a path between pi and pj through pk is bij (pk) = 1/gij× gij (pk), so pk becomes a bridge for other directors. The probability =

Closeness measures, the distance that a director needs to take within their network to reach any other director. This measure captures the connection to influential directors. Closeness centrality is derived by Sabidussi (1966). It reflects, how easy it is for a director (pk) to reach other directors (pi) in the network. If d(pi, pk) = the distance between pi and pk, then the closeness centrality of pk =

Empirical Setting and Estimation Technique

This study employs the Propensity Score Matching (PSM) approach to investigate whether firms engaged in CSR differ from those that are not, in terms of the social network of their independent directors. The PSM approach can effectively adjust for selection bias when assessing the impact of social networks on CSR participation. The decision to produce a CSR report may not be arbitrary, as firms that report on CSR may possess different characteristics from those that do not. The influence of director social networks on CSR is akin to a “treatment effect” as we aim to determine the outcome if a treated firm (a CSR reporter) with specific characteristics had not been treated. However, treated firms are typically self-selected based on certain criteria, which can bias a simple average comparison between the treatment and control groups.

The PSM approach compares treated firms with a chosen group of non-CSR report firms that share similar characteristics, instead of comparing with all non-CSR reporters. This process involves a two-stage matching method. In the initial stage, we employ the Logit model to estimate the impact of characteristic variables (such as firm performance, firm size, book-to-market ratio, financial leverage, and analyst coverage) on CSR. This results in the derivation of the matching coefficient, also known as the propensity score. The model for estimating the propensity score is as follows in Equation 1.

To compare the impact of CSR reporting on the centrality of independent directors, we first need to match the samples based on their propensity scores. The propensity score is the probability that a firm may issue a CSR report, expressed as:

In our examination of how the social network centrality of independent directors impacts a firm’s CSR reporting, we make use of a panel data model along with the Instrumental Variable (IV) technique. This methodology aids us in identifying the causal connection between social network centrality and CSR reporting. The relationship is articulated through the log-linear equation presented as Equation 2.

The dependent variable, CSR, is a binary variable that is set to 1 if a firm issues a CSR report in a given year, and 0 otherwise. The primary explanatory variable is Centrality, which quantifies the social network centrality of independent directors. We utilize three distinct measures of Centrality: Degree Centrality (DC), Betweenness Centrality (BC), and Closeness Centrality (CC). Additional explanatory variables include Analyst Coverage (Coverage), Return on Assets (ROA), Firm Size (Size), Book-to-Market Ratio (BM), and Leverage (Leverage). We employ the 1-year lagged values of Centrality as instrumental variables for the current values of Centrality. The equation is estimated for the entire sample and two subsamples based on analyst coverage. Table 1 outlines the definitions and explanations of the variables utilized in the analysis.

Variable Definition.

Descriptive Statistics

We examine the social networks of independent directors in firms that issue a CSR report (referred to as the “Treat” groups) and those that do not (referred to as the “Benchmark” groups). Network strength is measured using degree, betweenness, and closeness. Table 2 presents the summary statistics and the mean differences between the two groups. The Treat group exhibits higher network strength, firm size, book-to-market ratio, leverage, and analyst coverage compared to the Benchmark group. The differences are statistically significant for all variables except for ROA. This suggests that CSR reporting is linked with increased influence, resources, risk, and attention. Table 3 provides the correlation coefficients of the variables. The most robust correlation is observed between firm performance and analyst coverage, while the weakest correlation is between firm performance and the book-to-market ratio. The remaining correlations are moderate. CSR reporting exhibits a weak correlation with network strength.

Statistics for Disclosure and Non-Disclosure of CSR Reports, 2013 to 2019.

Note.(1) Figures in parentheses are standard errors. (2) ***, **, and * represent statistical significance at the 1%, 5%, and 10% levels, respectively.

Correlation Matrix.

***, **, and * represent statistical significance at the 1%, 5%, and 10% levels, respectively.

Do CSR Report Induce More Independent Directors’ Social Networks?

Empirical Results

Logit Model

We estimate the probability of publishing a CSR report for each firm using a Logit model. Firms are then matched based on this probability, and divided into two groups according to analyst coverage. We then investigate the impact of this division on CSR reporting. Table 4 presents the results for all firms and each group. For instance, in the case of DC, column (1) reveals that with each additional independent director, the likelihood of a CSR report being published increases by 46%. This aligns with Hypothesis 1, suggesting that the social network of independent directors plays a crucial role in CSR reporting. The stronger their network, the higher the probability of CSR reporting.

Propensity of CSR Disclosure to Engage in Independent Director Centrality – Logit Model.

Note. (1) Figures in parentheses are standard errors. (2) ***, **, and * represent statistical significance at the 1%, 5%, and 10% levels, respectively.

Table 4 Columns (1) to (3) suggest that for all firms, a unit increase in analyst coverage boosts the likelihood of CSR reporting by 10.73% to 12.02%. Columns (4) and (7) show that for firms with extensive analyst coverage, the addition of one director to their network raises the probability of CSR reporting by 61%, as opposed to a 32% increase for firms with limited analyst coverage. These findings align with Hypothesis 2, suggesting that the social networks of independent directors are more robust in firms with high analyst coverage compared to those with low analyst coverage. The results from Table 4 also support Hypothesis 3, indicating that analyst coverage has a positive effect on CSR participation and enhances the positive relationship between the centrality of independent directors’ social networks and CSR participation.

Other factors such as performance, size, book-to-market ratio, leverage, and analyst coverage also influence CSR reporting. However, the relevance of these factors varies between groups. For example, firms with high analyst coverage place more emphasis on performance, book-to-market ratio, and leverage, while firms with low analyst coverage prioritize size and analyst coverage.

Treatment Effect

We employ a matching process based on propensity scores from the Logit model to pair firms that report on CSR with those that do not. These scores mirror the observable characteristics’ similarity between the two groups. Subsequently, we compare the social network centrality (degree, betweenness, and closeness centrality) of independent directors among the matched firms. The outcome variables in this study are the centrality measures.

Table 5 presents the matching analysis results for all firms, demonstrating the impact of CSR reporting on the social network centrality of independent directors. We observe that CSR reporting has a more pronounced effect on the social network centrality of independent directors in firms with high analyst coverage compared to those with low coverage. Specifically, for firms with high analyst coverage, CSR reporting boosts degree, betweenness, and closeness centralities by 94.36%, 49.08%, and 1.8% respectively, in contrast to non-reporting firms. For firms with low analyst coverage, CSR reporting increases degree and betweenness centralities by 44.15% and 11.82% respectively, but does not significantly affect closeness centrality.

Treatment Effect of CSR Disclosure.

Note. (1) Figures in parentheses are standard errors. (2) Propensity score calculation includes company performance, company size, book-to-market ratio, financial leverage, and analyst coverage. (3) ***, **, and * represent statistical significance at the 1%, 5%, and 10% levels, respectively.

These findings confirm Hypothesis 2, suggesting that analyst coverage positively influences independent directors’ social networks. Analysts perform an external monitoring role, while directors oversee internally (Derrien & Kecskes, 2013; Galanti et al., 2022). This implies that CSR reporting amplifies the social connections and influence of independent directors, particularly in firms under greater external scrutiny and pressure from analysts. CSR reporting signals these companies’ commitment to stakeholder interests, thereby enhancing their social reputation.

The matching analysis confirms that CSR reporting significantly and positively impacts the social network centrality of independent directors across all firms, especially those with high analyst coverage. The treatment effects of CSR reporting vary from 66.99% to 1.1% across different dimensions of social network centrality. This evidence suggests that CSR reporting effectively strengthens the social network centrality of independent directors, which can potentially enhance the firm’s governance and performance.

Assessing the Matching Quality

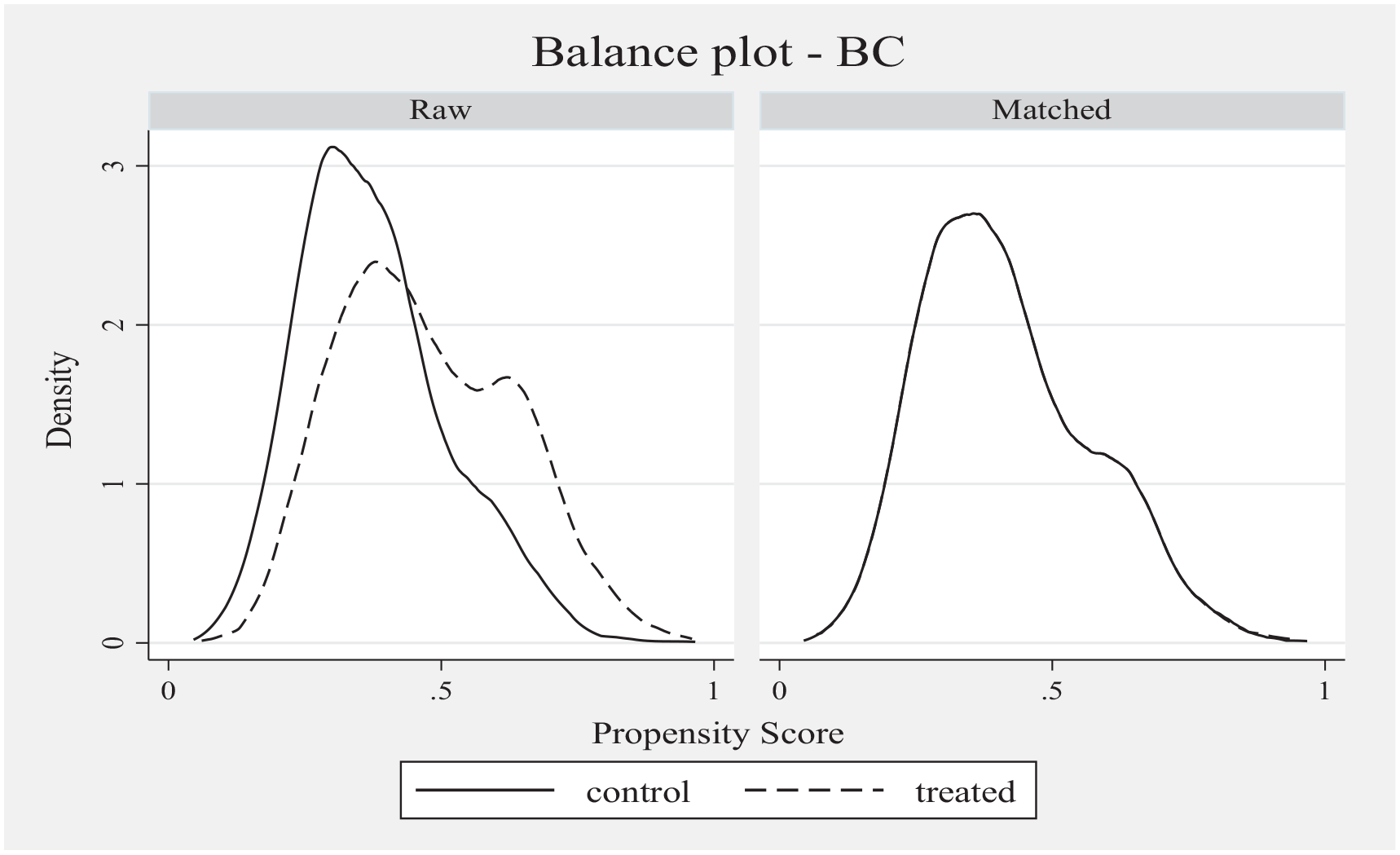

We employ the PSM method to create a control group of firms that do not report on CSR, but share similar observable characteristics with firms that do report CSR. The PSM method is based on the assumption that the matching process eradicates any systematic differences in covariates between the treatment and control groups. As a result, any remaining differences in the outcome variables can be attributed to the treatment effect of CSR reporting (Heckman et al., 1997). To validate this assumption, we examine the balance of covariates utilized in the propensity score estimation post-matching. Figures 1 to 3 display the density balancing plots for both the control and treated groups, before and after the matching process. The similarity in plots for the matched sample implies that the covariates have been effectively balanced through matching based on the predicted propensity score.

Density balancing plot-propensity score kernel with regression-adjustment for degree centrality.

Density balancing plot-propensity score kernel with regression-adjustment for betweenness centrality.

Density balancing plot-propensity score kernel with regression-adjustment for closeness centrality.

Table 6 presents the results of the balance check. It shows the mean values of covariates for the treatment and control groups and the p-values of the t-tests for their equality. It also shows the standardized bias for each covariate before and after matching, respectively. The standardized bias measures the percentage difference in the means of covariates between the two groups. A lower standardized bias indicates a better balance. We find that after matching, there is no significant difference in the mean values of any covariate between the treatment and control groups. The standardized bias for each covariate is also reduced substantially after matching, indicating that the matching procedure is effective in creating a balanced sample.

Matching Covariates Balancing Property – Kernel.

Further Investigation Into the Marginal Effect of Independent Directors’ Social Network Centrality on CSR

We then use the panel IV estimator to investigate the causal effect of independent directors’ centrality on CSR reporting. Table 7 provides the estimates of the equation in Equation 2 for the whole sample and two subsamples divided based on analyst coverage. We use DC, BC, and CC as alternative measures of Centrality, while controlling for other firm characteristics such as Size, BM, ROA, Leverage and Coverage.

Marginal Effect of Independent Directors’ Centrality on CSR.

Note. (1) Figures in parentheses are standard errors. (2) ***, **, and * represent statistical significance at the 1%, 5%, and 10% levels, respectively.

Table 7 reports the marginal effect of independent directors’ centrality on CSR. We find that DC and BC exert positive and significant impacts on CSR reporting for all firms, as well as for both low and high analyst coverage groups. This reaffirms the PSM results that independent directors’ centrality fosters CSR reporting. The elasticity of CSR reporting with respect to DC is 11.15%, BC is 10.47%, and CC is 13.94% for all firms. This further validates Hypothesis 1, indicating that the strength of the social network among independent directors is pivotal for CSR reporting. The more robust their social network, the higher the likelihood of them reporting CSR.

Table 7 also reveals that analyst coverage has a positive and significant effect on CSR reporting for all firms. This aligns with previous literature indicating that CSR reporting serves to reduce information asymmetry and agency costs between managers and stakeholders (Jo & Harjoto, 2014). The marginal effects of analyst coverage on CSR reporting range from 2.59% to 2.91% for the whole sample, depending on the centrality measure. We also find that the effect of analyst coverage is more pronounced for low coverage firms than for high coverage firms. The marginal effects of analyst coverage on CSR reporting range from 3.99% to 4.37% for low coverage firms and from 2.35% to 2.38% for high coverage firms, respectively. This is in line with Hypothesis 3, suggesting that analyst coverage positively influences CSR participation. This implies that firms with low coverage face more social pressure to engage in CSR reporting and disclose their social performance to stakeholders.

Moreover, the elasticity of CSR reporting with respect to DC is 15.12%, BC is 19.26%, and CC is 17.81% for high analyst coverage firms, and DC is 6.92%, BC is 5.26%, and CC is 12.97% for low analyst coverage firms. This is also consistent with Hypothesis 3, suggesting that analyst coverage amplifies the positive relationship between independent directors’ social network centrality and CSR participation. This implies that centrality is more critical for CSR reporting of high analyst coverage firms, which is consistent with the PSM results.

In relation to the other variables, we observe that Size exerts a positive and significant influence on CSR reporting exclusively for firms with low analyst coverage. This suggests that larger firms, subject to less external scrutiny, are more prone to engage in CSR reporting. ROA has a positive and significant impact on CSR reporting across all firms, particularly those with high analyst coverage, indicating a greater propensity for profitable firms to report their CSR activities. Both BM and Leverage have positive and significant effects on CSR reporting for all firms. This suggests that value firms and those with high leverage employ CSR reporting as a strategy to alleviate their bankruptcy risk and augment their market share (Bae et al., 2019).

Conclusion

Prior research on CSR have primarily focused on its impact on various aspects of corporate performance, value, risk, and governance. It has been established that firms that engage in CSR activities can gain public trust and improve their performance (Eberhard & Craig, 2013). Additionally, they can reduce their financing costs, increase their firm value, and decrease their firm risk (El Ghoul et al., 2018).

In this study, we utilize the social capital theory and the stakeholder theory to examine the relationship between CSR involvement, the social network of independent directors, and the analyst coverage of firms. We suggest that these elements form a part of the social capital that firms can gather and use to meet the needs of their stakeholders. We use PSM methods to confirm our hypotheses and show that firms involved in CSR activities tend to have independent directors who hold a more central position in the social network. This can bring more external and valuable information to the firms. We also show that analyst coverage moderates the positive effect of CSR involvement on the social network centrality of independent directors. This positive feedback loop links the firm’s acquisition of social capital and stakeholder satisfaction to its sustainable development.

Our findings reveal that CSR reporting significantly and positively impacts the social network centrality of independent directors across all firms (Alves, 2021; Zou et al., 2019). We also discover that this impact is more pronounced for firms with high analyst coverage compared to those with low analyst coverage (Albuquerque et al., 2019; Becchetti et al., 2015). This indicates that CSR reporting bolsters the social ties and influence of independent directors, particularly for firms subjected to greater external scrutiny and pressure from analysts (Hinze & Sump, 2019; Naqvi et al., 2021).

Our results suggest that CSR reporting can serve as a strategic management tool for firms aiming to achieve sustainable development and meet stakeholder expectations. We advocate for government and regulatory bodies to encourage CSR reporting, implement CSR audits, and oversee CSR-related activities. We also recommend stakeholders to assess the motives, financial information, and actual effects of CSR reporting to make informed investment decisions and judgments.

This study has a limitation in that it solely uses the issuance of a CSR report as a measure of CSR involvement. It does not consider the various dimensions and levels of CSR involvement and their impact on the social network centrality of independent directors, due to the availability of data. A potential avenue for future research is to differentiate between various types of CSR involvement and examine their distinct impacts on the social network centrality of independent directors. For instance, future studies could investigate how CSR involvement in different areas, such as environmental, social, or governance, influences the social network centrality of independent directors in diverse ways, provided data is available.

This study also suggests that government and regulatory bodies should stimulate firms to report their CSR activities and disclose their social performance to stakeholders. This can boost the social capital and reputation of firms, as well as the social network centrality of independent directors, which can enhance the firm’s governance and performance. This positions Taiwan as an interesting case study.

Taiwan’s innovative initiative mandates corporate sustainability disclosures, offering new research opportunities. This initiative, significant for examining the transition from voluntary to mandatory reporting, will require all Taiwanese firms to disclose industry-specific sustainability indicators from 2025. The aim is to promote sustainable development and increase corporate transparency, providing valuable information for stakeholders. Future research may explore how mandatory reporting influences executives’ commitment to sustainability. Detailed disclosures could reveal unexpected corporate leaders and laggards. Comparative studies could assess long-term impacts on priorities and accountability. The period leading up to 2025 presents an opportunity to observe changes in Taiwanese business sustainability practices, potentially shaping global best practices for mandatory disclosures.

Footnotes

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.

Data Availability Statement

Data sharing not applicable to this article as no datasets were generated or analyzed during the current study.