Abstract

Although prior research has explored the influence of board’s external connectedness on corporate fraud in the U.S., how such influence works in economies with concentrate ownership like China remain largely unexplored. The highly concentrated ownership in China not only exacerbates principal-principal conflicts but also lead to the formation of director subgroup within the board and the separation of board’s external social networks. To explore the impact of board’s social network on corporate fraud in such a unique context in China, it is important to adopt a subgroup-level network lens. Filling this gap, using a binary probit regression model with partial observability on 1,530 Chinese publicly listed companies with corporate violation announcements data from 2003 to 2013, this study analyzes the impact of two director subgroup interlocking networks on corporate fraud occurrence and fraud detection. The empirical results show that high centrality in the dependent director subgroup interlocking network contributes to fraud deterrence, and the high centrality in the independent director subgroup interlocking network facilitates both fraud deterrence and fraud detection. This study contributes to corporate governance research by exploring the influence of social networks on corporate fraud with a subgroup-level network lens in China. Meanwhile, the formulation of two parallel director subgroup interlocking networks introduces a novel analytical framework for future interlocking directorship research in scenarios where the board is subject to a structured division.

Plain language summary

Previous research has examined how a company’s board connections affect corporate fraud in the U.S., but the impact of these connections in China, where ownership is highly concentrated, has not been thoroughly studied. In China, concentrated ownership can intensify conflicts among major shareholders and lead to the creation of distinct director subgroups within the board, each with its own external social network. To understand how these networks influence corporate fraud in China, it’s crucial to focus on the level of each subgroup. This study bridges that gap by analyzing data from 1,530 Chinese publicly listed companies with corporate violation announcements from 2003 to 2013. Using a binary probit regression model that accounts for partial observability, we explore the effects of interlocking networks of two director subgroups on both the occurrence of corporate fraud and its detection. Here’s a simplified summary of our findings: A more central position of the dependent director subgroup’s network is linked to a reduced likelihood of corporate fraud, suggesting that these connections can help deter fraudulent activities. Meanwhile, a more central position of the independent director subgroup’s network not only helps deter fraud but also aids in its detection if it occurs. This research contributes to the field of corporate governance by revealing how social networks can influence corporate fraud at a more detailed, subgroup level in China. Additionally, by proposing the concept of two parallel director subgroup interlocking networks, we offer a new framework for future research on the role of interlocking directorships in scenarios with structured board divisions.

Keywords

Introduction

Corporate fraud is a pivot subject in corporate governance research as such misconduct leads to significant negative consequences for stakeholders (Zahra et al., 2005), securities market (Free & Murphy, 2015), and society (Yu, 2013). As the cornerstone of corporate governance, the board of directors plays a significant role in the commission, deterrence, and detection of corporate fraud. Prior research has explored the impact of the board’s internal attributes such as composition, compensation, and reputation on corporate fraud (Agrawal & Chadha, 2005; Archambeault et al., 2008; Fich & Shivdasani, 2007; Fracassi & Tate, 2012). As the behaviors of organizations are profoundly influenced by their social embeddedness (Borgatti et al., 2009), many studies attempted to explore the impact of board’s external networks on corporate fraud by adopting a network lens (Bao et al., 2019; Chahine et al., 2021; Chiu et al., 2013; Khanna et al., 2015; Zhao & Zhu, 2023) and most of them centered around the U.S. firms. The answer to this question might provide an informal governance measure to curb corporate fraud through the management on board’s social network (Guo et al., 2022).

As corporate fraud is the manifestation of agency issues, the motives and triggers of fraud varies significantly with institutional contexts, particularly the ownership structures (Coffee, 2005). In economies with dispersed ownership like the U.S, type-I agency conflicts are prevalent, where CEOs may instigate fraud for personal gain against the supervision of board of directors (Johnson et al., 2009); conversely, in economies with concentrated ownership like China, type-II agency conflicts are prevalent, where large shareholders may collaborate with complicit directors to exploit minority shareholders with fraudulent activities (Berkman et al., 2009; La Porta et al., 1999). As the fraud mechanisms and patterns differ across these settings due to distinct motivations and triggers, the conclusion draws from research in the U.S may not be directly applicable to concentrated ownership economies like China without careful consideration. Although Zhao and Zhu (2023) conducted a study about the impact of interlocking networks on corporate fraud in China and found a significant deterring effect of board’s social embeddedness, they still treat the board as a unified entity, whereas the highly concentrated ownership and its influence on board structure in China has been ignored. Owing to the controlling shareholders’ dominance on board and the mandatory introduction of the independent director system in China in 2003, the board in Chinese companies is not an intact group, but rather the composite of two distinct, cohesive subsets, namely, the dependent director subgroup and the independent director subgroup, and their roles and influence on corporate fraud are largely different. Therefore, the overall influence of board’s social connectedness on corporate fraud in China is the aggregate of the individual impacts of each director subgroup’s social networks. However, existing studies failed to incorporate the divergent board structure into their analysis, we are not aware of the individual impact of each director subgroup’s social network, and this oversight could result in misconceptions and potentially harmful corporate governance policies. So, the central question of this paper is: what is the individual impact of each director subgroup’s social network on corporate fraud in China?

To answer this question, this study conducts empirical analysis on 1,530 publicly listed companies in China with data released by the China’s securities regulatory authorities over the period from 2003 to 2013, and tries to find out the impact of two director subgroup interlocking networks on corporate fraud. Given that the conventional probit model is not well-suited to handle the partial observability inherent to corporate fraud cases, as highlighted by Poirier (1980), we have employed a bivariate probit model that is specifically designed to account for this complexity. The study finds that the centralities of a focal firm’s dependent director subgroup and independent director subgroup in their respective interlocking network are negatively associated with the focal firms’ propensity to commit fraud, while the centrality of the focal firm’s independent director subgroup in its interlocking network has a positive correlation with the probability of fraud detection should any fraudulent behavior occur. This finding underscores the distinct roles that the dependent and independent director subgroups play in the context of corporate fraud in China.

This finding is logically congruent with Zhao and Zhu’s research (2023) but provide a deep layer of insight into the micro-mechanism that how board’s social connectedness influences corporate fraud at a sub-group level in China. Largely, this study has two theoretical contributions. First, it enriches the literature of corporate governance by extending research on social network’s impact on corporate fraud to sub-group level and concentrated ownership economies context. By delineating the scope of existing theories, this study sheds light on the nuanced influence that interlocking directorship networks can exert on the likelihood of a focal firm engaging in fraudulent activities within a concentrated ownership economy and offers a more precise framework for assessing the risk and dynamics of fraud in such settings. Second, dividing the interlocking directorship networks into two subgroup networks based on the systematic divisions in the boardroom, this study implies a new avenue for further research on how to adopt the subgroup-level network as an effectual analysis unit for studying inter-organizational networks’ impacts on board members’ activities. In addition, the findings of this study indicate that increasing the social connectedness of directors is beneficial to curb corporate fraud in China, especially for independent directors.

The rest of the paper is organized in five sections as follows. In the Theoretical and practical background section, we introduced the history and situation of corporate fraud and corporate governance in China and illustrated that the board structure in China is comprised of two distinct director subgroup and therefore there are two parallel director subgroups interlocking networks. In the Hypothesis development section, we proposed three hypotheses regarding the impact of director subgroups interlocking network on corporate fraud occurrence and detection. In the Research design section, we introduced the data, sample, variables, and the bivariate probit model with partial observability in our study. In the Empirical findings section, we demonstrated the descriptive statistics, results of basic regression and robustness test of our model. In the Discussion and conclusion section, we summarized the study’s contribution, implication as well as its limitations and avenues for further research.

Theoretical and Practical Background

Corporate Fraud and the Introduction of the Independent Director System in China

In the 1990s, owing to the transitional processes of economic restructuring and state-owned enterprise reform, Chinese listed companies had exhibited highly concentrated ownership, extensive state control, pervasive business group structure and weak legal protection for their minority shareholders (Clarke, 2006). Among these phenomena, the exclusive dominance wielded by controlling shareholders over the board and management stands out as particularly pronounced. In addition to directly designating directors, the controlling shareholders would usually arrange their business partners to join the board for resource dependence (Pfeffer & Salancik, 2003). Consequently, the board would be molded to represent the interests of controlling shareholders and their affiliated partners. Meanwhile, to reduce agency costs, the controlling shareholders often appoint their own directors to occupy critical management positions such as CEOs, thereby deeply controlling the management layer. In this way, the controlling shareholders could easily manipulate the listed companies to pursue their own private interests, even at the expense of the minority shareholders (Clarke, 2006). As a result, largely different from the traditional principal-agent conflicts between shareholders and management in dispersed ownership economies such as the U.S. (Fama & Jensen, 1983), the principal-principal conflicts between the controlling and minority shareholders became the primary agency issue in China (Young et al., 2008).

During the early 2000s, corporate fraud related to the controlling shareholders’ unrestrained abuse of power and exploitation of the minority shareholders frequently occurred (Z. Q. Li et al., 2004). To curb the rampant corporate fraud, the China Securities Regulatory Commission (CSRC) drew experience from the U.S., decided to introduce the independent director system in China (Hou & Moore, 2010; Yuan, 2007). In August 2001, the CSRC formally issued the “Guidance on the Establishment of Independent Director System in Listed Companies,” which mandated that all listed companies must appoint more than one-third of their board seats to independent directors by June 30, 2003, and required the independent directors to take on extra responsibilities to protect the interests of the minority shareholders. According to these stipulations, the independent directors were not allowed to hold shares or stock options of the focal firm and can only receive modest fixed subsidies (Clarke, 2006). Moreover, the independent directors had been legally granted several special rights to curb insider control, including the rights to veto large-scale related-party transactions and to express independent opinions on corporate decisions (F. Jiang & Kim, 2020).

Therefore, the boardroom in Chinese listed companies comprised two types of directors after 2003: the dependent directors, 1 who act consistently with the interests of the controlling shareholders and their affiliated partners, and the independent directors, who are expected to curb insider controlling and protect the interests of the minority shareholders. This difference has profoundly impacted the structure of interlocking directorship networks in China in the next ten years, before further corporate governance reforms took places in 2013.

Director Subgroup and Director Subgroup Interlocking Networks in China

Within the scholarly discourse on interlocking directorships, there is a consensus that an interlocking directorship serves as a bridge that channels resources, information and opinions across different boards and firms (Gulati & Westphal, 1999; Podolny, 2001). Essentially, this consensus is based on an implicit assumption that a board is a cohesive group, in which all directors actively engage with one another and are inclined to exchange and share resources, information, and perspectives. However, when the board’s cohesion is compromised, certain directors may become be reluctant to interact with other directors and refuse to share. In this way, the exchange of resources, information, and opinions among board members and between their respective companies could be impeded, disrupting the seamless flow of knowledge and collaboration that interlocking directorships are typically intended to foster.

As discussed above, due to the dominance of the controlling shareholders on boards and the mandatory introduction of the independent director system in China, the identities, responsibilities, and interests of independent directors are significantly different from or even in conflict with those of dependent directors. As outsiders to the focal firm, independent directors are excluded from the insider clique in which dependent directors and affiliated management have already established close relationships (Mizruchi, 1993; Yi & Ellis, 2000). Meanwhile, the interactions between dependent and independent directors are merely confined to a few board meetings in which independent directors’ primary task is to inspect and scrutinize the corporate proposals presented by dependent directors. As the decision makers, dependent directors would be subjected to evaluative oversight by independent directors who serve as the decision controllers (Gulati & Westphal, 1999). Thus, distrust and tension between the independent and dependent directors would arise (Sitkin and Stickel, 1996), which could hinder their ability to form a unified and cohesive group.

Consequently, within the same boardroom, dependent and independent directors would naturally form two distinct, cohesive subsets. To coordinate and pursue their interests, the dependent directors would interact with each other frequently and would gradually form a stable interest union (Pfeffer & Salancik, 2003). Influenced by the differential mode of association in Chinese social relationships (Fei et al., 1992), the closed formal relationships among the dependent directors would intertwine with their informal relationships, and as a result, a stable guanxi exhibiting multiplicity and reciprocity would be established (Yi & Ellis, 2000). On the other side, since independent directors are required by the CSRC to take training courses and pass the qualification tests on business ethics, demeanor codes, and commercial laws, those directors are conscious of their identity, rights, and responsibilities, which would lead to unambiguous expectations and rapid feedback among this group, and thus facilitate the formation of fast trust (Meyerson et al., 1996). Despite the limited interaction time, independent directors, through their participation in specialized board committees such as the remuneration and nomination committee, are compelled to collaborate closely. The complexity of their tasks, which demand a broad spectrum of professional expertise, necessitates their collaboration while fulfilling their duties (Finkelstein & Mooney, 2003).

In accordance with the theory of social categorization, individuals like and trust others who have similar attributes, and their interpersonal interactions would gradually form the boundary between insider and outsider through self-categorization (Hogg & Terry, 2000). Thus, following cooperative interactions, the dependent and independent directors would form common expectations, take collective actions, and eventually converge into two cohesive board subsets or subgroups, respectively (Carton & Cummings, 2012; Koskinen & Edling, 2012). Hence, two parallel interlocking networks composed of different types of director subgroups among the firms emerge, namely, the dependent director subgroup interlocking network (DDSIN) and the independent director subgroup interlocking network (IDSIN). 2 The two interlocking networks—DDSIN and IDSIN—differ in their goal-directedness during formation (Kilduff & Tsai, 2003) and in the types of resources they exchange (Gulati, 1999). The DDSIN is founded on the principles of interest coordination and resource dependence. The goal of this network is to pursue economic benefits, and the resources exchanged are substantial ones such as financial support, business cooperation, and commercial intelligence. Comparatively, the IDSIN is founded on the principles of social identification and professional collaboration. The goal of this network is to ensure that corporate actions and decisions are legitimate and beneficial for all shareholders, and thus the resources exchanged in this network are symbolic ones such as reputation, knowledge, and information.

Hypothesis Development

Since some fraudulent activities might escape from exposure, corporate fraud is a partially observable phenomenon, and the observed fraud is only a part of all the committed fraud that has been later detected. Accordingly, there are two distinct aspects of observable fraud for in-depth research: fraud commission and fraud detection (Khanna et al., 2015; Kuang & Lee, 2017).

Since the dependent directors in China occupy critical management positions, corporate fraud cannot occur without their participation and acquiescence. Therefore, different from CEOs playing a major role in corporate fraud in the US (Chahine et al., 2021), the primary culprit of fraud commission in China is the dependent director subgroup (Clarke, 2006).

In contrast, the independent directors take on the responsibility of curbing insider controlling, in line with the CSRC’s requirements. Therefore, the independent director subgroup would exert a counterbalancing impact on fraud commission by constraining the behaviors and decisions of the dependent director subgroup during the board meetings. If fraudulent activities eventually occurred and were noticed by the independent director subgroup, the directors would need to avoid being held accountable and show their innocence through casting opposing or abstaining votes, issuing critical opinions or even resigning from the focal firm (Gao et al., 2017; W. Jiang et al., 2016; Tang et al., 2013). In this way, the independent director subgroup can signal a warning to the public, media and regulatory agencies, eventually incurring investigation and fraud detection.

As those two types of director subgroups are imbedded in their interlocking networks, we contend that the network positions of dependent director subgroups might influence a focal firm’s likelihood of fraud commission, while the network positions of independent director subgroups might simultaneously influence the likelihood of fraud commission and detection in the event that fraud occurs.

Fraud Commission and the Network Positions of Dependent Director Subgroups

To explore the influence of the director subgroup’s interlocking network on corporate fraud commission, we contextualize our analysis through the lens of the fraud triangle. As the most used theoretical framework in fraud research, the fraud triangle has provided strong explanatory power on the occurrence of fraud by elucidating the three conditions that lead to fraud: (a) the incentive that motivates fraud; (b) the convenient opportunity for fraud; and (c) the ability of fraudsters to rationalize their fraudulent behaviors (Free & Murphy, 2015). As most corporate fraud in China is the result of deliberate collusion among dependent directors and management, individuals participating in collective fraudulent activities can easily soothe their sense of guilt given the diffusion of responsibility in groups (Feidman & Rosen, 1978). Therefore, the rationalization factor is relatively insignificant in China. As a common practice in the analysis of fraud commission, we focus on the two fundamental factors: the incentive and opportunity to commit corporate fraud (Dellaportas, 2013).

Since the dependent director subgroups are the primary culprits of fraud in focal firms (Clarke, 2006), their network positions in the DDSIN may significantly influence the likelihood of fraud commission in terms of the incentives. First, the central position in a network implies power and status (Brass, 1992), and thus the dependent director subgroups with a central position can have more opportunities to access resources via the DDSIN. In this way, a central dependent director subgroup would be easier to benefit from legitimate approaches without violating the official rules (Keister, 1998; Mahmood et al., 2011). When confronted with business adversity, the central dependent director subgroup can receive more material support, such as financial assistance, business cooperation, critical intelligence, and inter-firm commitments (Argote & Ingram, 2000; Engelberg et al., 2012; O’Hagan & Green, 2004). Therefore, the operational crisis stimulating fraud commission is relatively less likely to occur in a firm with a dependent director subgroup holding a central position in the DDSIN.

Second, once the fraudulent activity was exposed, the dependent director subgroup would encounter not only legal punishment but also permanent reputation penalties (Kang, 2008). Since reputation is very valuable providing long-term sustainable benefits, the loss of reputation related to fraud commission is enormously impactful. As an actor’s network centrality implies a high reputation (Balkundi et al., 2011), the losses incurred by fraud exposure would be more significant for the dependent director subgroup with a central position in the DDSIN than the one without. In addition, since most fraudulent activities are conducted covertly and require only collusion with insiders and collaboration rather than an external relationship in the spotlight (Kong et al., 2019), the external connectedness of central dependent directors would not significantly increase the opportunities to commit fraud. Taking into consideration of both the benefits and losses of committing fraudulent activities, the firm whose dependent director subgroup has a central position in the DDSIN would be less incentivized to commit fraud than the ones with peripheral subgroups. Therefore, we hypothesize:

Fraud Commission and the network Positions of Independent Director Subgroups

Although some scholars argue that the redundant external connectedness of independent directors might exhaust their energy and reduce their assiduity (Fich & Shivdasani, 2006), the hypothesis that busy independent directors are less effective in performing duties has not been supported in some empirical research (Ferris et al., 2003). Meanwhile, as the CSRC has mandated that each independent director should not take more than five directorships simultaneously, the multiple directorships of an independent director are normally fewer than three (Clarke, 2006). Thus, as the counterbalancing force on fraudulent activities, the independent director subgroup could significantly influence the dependent director subgroup’s propensity to commit fraud by minimizing their opportunity to do so in China.

On the one hand, the independent director subgroups with central positions in the IDSIN are more capable of performing their monitoring functions. The subgroup members (independent directors) with their ample social connections are more efficient at supervising corporate behavior, because they have better access to information on peer firm practices, industrial trends and market conditions (Nicholson & Kiel, 2004). Consequently, the well-connected independent director subgroup could exercise high-quality and strict supervision to constrain the opportunistic behaviors of the insiders (Coles et al., 2014). On the other hand, the independent director subgroups with central positions also have more independence and stronger motivation to curb fraud. Although independent directors receive only fixed subsidies, their concerns about the reputation would encourage them to assiduously perform their duties, especially the directors (as a subgroup in the boardroom) who occupy the central position in the IDSIN (Faleye et al., 2018; Shane & Cable, 2002). Additionally, the ample connections and interactions among independent director subgroups would also strengthen their relevant social identification, thereby strengthening their awareness of responsibilities (Hogg & Terry, 2000). Accordingly, a lower likelihood of fraud commission in a firm can be anticipated if its independent director subgroup holds a central position in the IDSIN. Therefore, we hypothesize:

Fraud Detection and the Network Positions of Independent Director Subgroups

In China, as civil litigation related to corporate fraud is rare, fraud detection is mainly performed by regulatory agencies through routine inspections and investigations that are triggered by accusations, anonymous reports, and media coverage (Hou & Moore, 2010). Therefore, the exposure of suspicious information and its visibility is critical in fraud detection (Johansson & Carey, 2016).

Once a company has committed fraud, the independent directors’ reputations will be at stake, and it would incur administrative or legal penalties as well. However, according to the conventional practices of the CSRC, once independent directors can prove that they have responsibly performed their duties, even if the firm has been judged to have violated laws and regulations afterwards, the independent directors could still get exemptions and be declared innocent. 3 Generally, if the independent directors are aware of suspicious corporate behaviors and decisions, they might cast opposing or abstaining votes in board meetings (W. Jiang et al., 2016), express critical opinions on corporate decisions (Tang et al., 2013), or even resign from the focal firm (Gao et al., 2017) to demonstrate their conscientiousness and responsibleness. These events would send a signal of suspicion to the public, media, and regulatory agencies, and would eventually incur relevant investigations.

As discussed above, the independent director subgroups with high centrality in the IDSIN have more experience in sensing potential corporate fraud, and they have a higher level of concern for reputation. Therefore, they are more capable and willing to prove their innocence and disseminate the information of suspicion to the public. Meanwhile, those subgroups are more visible and prominent to the public, media, and regulatory agencies, facilitating the signal reception around suspicion and subsequent fraud detection. Consequently, the firms with a central independent director subgroup in the IDSIN can have a high likelihood of fraud detection if fraud occurs. Therefore, we hypothesize:

Research Design

Data and Sample

We conducted the empirical research from 2003 to 2013 in China. In 2003, the independent director system was formally established by CSRC, and the systematic division within board of director and the formation of director subgroup emerged.

In 2013, the newly elected Central Committee of the Communist Party of China (CPC) introduced the “eight-point frugality code” and launched a nationwide campaign against corruption. Subsequently, a series of significant reforms were initiated, targeting anti-corruption measures, corporate governance. A notable aspect of these reforms was the increased involvement of the CPC in corporate governance, which lead to two distinct waves of resignations among independent directors who were previous officials or leaders in government, CPC or university (F. Wang et al., 2018; Zhang, 2018). Given that approximately one-third of Chinese listed companies are state-owned enterprises (SOEs), and most of these companies have CPC branches, the regulations had a substantial impact on the corporate governance mechanisms and the social connectivity of boards. Since then, instances of corporate fraud have become less prevalent, and the influence of both dependent and independent directors has been diminished, particularly in SOEs, due to the presence of CPC branches (Zhang, 2018).

This shift has made the dynamics of corporate fraud occurrence and detection more intricate than before, and it has also altered the social network structure of interlocking directorate network. Consequently, we have chosen 2013 as the cutoff point for our research to avoid the confounding effects of external policy interventions. We believe that the period spanning from 2003 to 2013 offers an optimal window for examining the influence of director subgroup interlocking networks on corporate fraud, with minimal interference from external factors.

As the companies listed on the Growth Enterprise Board have special listing conditions, this study focuses only on those companies listed on the Main Board and the Small and Medium-sized Enterprises Board of the China A-share stock market. We excluded financial companies due to their abnormality.

The information on corporate fraud was collected from the Corporate Violation Research Dataset in the China Securities Market and Accounting Research (CSMAR) database. This dataset has collected information about corporate violations by A-share listed companies from enforcement announcements issued by the CSRC and the Shanghai/Shenzhen Stock Exchange since 1994. According to the CSRC, corporate violations are classified into three categories: (a) information disclosure violations, such as “fictitious profit,”“fictitious asset,”“false records (misrepresentation),”“major omissions,”“delayed disclosure,”“false disclosure,”“fraudulent listing,” and “improper handling of general accounting”; (b) operational violations, such as “investment violations,”“unauthorized use of funds,”“assets occupation of the company,” and “illegal guarantees”; (3) individual violations, such as “insider dealing,”“illegal trading of share,” and “stock price manipulation” committed by the individual senior members of the firm. As the individual violations do not pertain to corporate behavior, we excluded individual violations from our sample to remain consistent with our research objectives. Since some companies committed more than one fraud in a given year, we merged those data into one firm-year observation. In this way, we obtained 1,139 firm-year violation observations from the original sample of 18,714 firm-year observations of 1,530 Chinese A-share listed companies in the period from 2003 to 2013.

To establish the two distinct director subgroup interlocking networks, we collected personal information on all directors of listed companies from the Wind financial database. We identified each director using their gender, age, education level, and career experience and then labeled them with unique numbers for recognizing the correct individual in the interlocking directorships. Afterwards, we transformed the two-mode data on the “director-company” affiliation relationship into one-mode data on the “director subgroup–director subgroup” interlocking relationship. Focusing on interlocking directorships among director subgroups of the same type, we established the DDSIN and the IDSIN. Additionally, we acquired information on the financial status, internal governance, and stock market performance of the firms from the CSMAR database.

Model Specification and Variable Definition

Model Specification and Dependent Variables

The dependent variables are to reflect the likelihood of fraud commission and fraud detection by the focal firm in the given year. However, as some fraudulent activities could evade detection and exposure, corporate fraud is only partially observable (Feinstein, 1991; T. Y. Wang, 2013). Therefore, it is impossible to directly measure the realization of fraud commission and fraud detection. To address this issue, the bivariate probit model with partial observability is a proper solution (Khanna et al., 2015; Kuang & Lee, 2017).

In the bivariate probit model, the two latent variables reflecting the probability of fraud commission and fraud detection are denoted as COMMIT* and DETECT*. They are influenced by explanatory variables as follows:

where XC and XD are the vectors of variables explaining the probability of fraud commission and fraud detection, respectively, and μ and v are zero-mean disturbances with a bivariate normal distribution with the correlated coefficient ρ. The effective identification of the parameters requires that XC and XD cannot be the same.

Following the prior literature, two indicator variables COMMIT and DETECT are created, where COMMIT = 1 if COMMIT* > 0, otherwise COMMIT = 0. Similarly, DETECT = 1 if DETECT* > 0, otherwise DETECT = 0. As COMMIT and DETECT cannot be observed directly, the observable corporate fraud is denoted as OBSERVE. This variable is equal to one if the focal firm has committed fraud in the given year and has been detected, and equals zero if the focal firm has not committed fraud or a fraud occurrence has not been detected (i.e., OBSERVE = COMMIT × DETECT).

The empirical model for OBSERVE is as follows, where Ф is the bivariate standard normal cumulative distribution function:

Using the maximum-likelihood method, the log-likelihood function for the model is:

In accordance with the logic of the bivariate probit model with partial observability, any pair of variables for which their product equals the value of observable fraud (OBSERVE) can be designated as COMMIT and DETECT, respectively. Therefore, the simplest way to set those two latent variables is to make each of them equal to the binary variable OBSERVE.

Independent Variables

In the literature on social network analysis, four types of network centrality are commonly used to measure the network position, including the degree centrality, closeness centrality, betweenness centrality, and eigenvector centrality, of the focal nodes (Wasserman & Faust, 1994). 4

Wasserman and Faust (1994) argued that because different kinds of centrality reflect different aspects of network attributes of the focal nodes, the chosen measure should align with the research objective and network attributes. According to the attributes of these two director subgroup interlocking networks, we selected closeness centrality to measure the network position of the dependent director subgroups in the DDSIN and betweenness centrality to measure that of the independent director subgroups in the IDSIN.

For the DDSIN, the average annual value of the network density is 0.00036, and the average annual value of the degree centrality of the subgroups is only 0.639, which indicates that this is a loose network with short-distance connections. Considering that this network is built on interest coordination and resource dependency, the resources contained in this network are substantive resources that are difficult to transmit through indirect and distant paths. As closeness centrality represents the extent to which the focal node is closely connected to other nodes, it can reflect the attenuation of connections over distances and emphasize the value of close relationships. Therefore, closeness centrality is a proper indicator for the dependent director subgroups’ network positions.

In contrast, for the IDSIN, the annual average value of the network density is 0.0016, and the annual average value of the degree centrality of each subgroup is 2.978, which indicates that this is a relatively dense network with long-distance connections. Taking into consideration that this network is built on social identification and professional collaboration, the resources contained in this network are symbolic resources that can be easily transmitted through indirect and long-distance connections.

Since betweenness centrality represents the extent to which the focal node acts as the information transmission pivot point, it can reflect the influence of long-range connections. Therefore, betweenness centrality is a proper indicator for the independent director subgroups’ network positions.

Since network centrality is a dimensionless quantity without practical meaning, we standardized the two independent variables and minorized them at the upper- and lower-one percent levels. The standardized closeness centrality of the dependent director subgroup is marked as IN_NET, and the standardized betweenness centrality of the independent director subgroup is marked as ID_NET.

Control Variables

We also included measures of the operational situation, corporate governance characteristics, and visibility of the firm as the control variables.

In terms of operational situation, we controlled for common indicators reflecting firm economic conditions and ownership structure at the firm level (T. Y. Wang et al., 2010; Wu, 2016). The set of variables related to a firm’s economic condition include firm size (LnASSETS), leverage (LEVERAGE), accounting performance (ROA), Tobin’s Q (TOBINQ), average sales growth rate over the past 3 years (GROWTH_3), firm age (FIRMAGE) and the industrial Tobin’s Q (INDUSTRYQ). The set of variables related to a firm’s ownership structure include the Herfindahl index of the five largest shareholdings (H5INDEX), the shareholding ratio of the state (STATE_HOLD) and the shareholding ratio of the institutional investors (INSIT_HOLD).

In terms of corporate governance, we controlled for common indicators reflecting the characteristic of the board, CEO, and auditors. As board monitoring plays a vital role in curbing corporate fraud, we controlled for board size (LnBDSIZE), board meeting frequency (LnBDMEETING), and the number of specialized board committees (LnCOMMITTEE) in their logarithmic forms. We also controlled the ratio of independent directors in the boardroom (IDRATIO), the tenure of the current board chair (CHAIRTENURE) and whether the board chair held the position of CEO (CEODUALITY) in the given year, as these proxies reflect the power of the chairperson in the focal firm. Additionally, as the audit quality impacts the difficulty of fraud commission, we included a dummy variable, AUDITOR_BIG4, to control whether the auditor belongs to one of the global Big 4 audit firms (i.e., PWC, DTT, KPMG, and EY), which is commonly seen as a signal of high audit quality. The specifications of variables are presented in Appendix 1.

In terms of a firm’s visibility, we controlled for indicators reflecting the characteristics of the focal firm’s shares and attention from securities analysts, as abnormal transactions and stock price fluctuations draw extra attention from the regulatory agency and might lead to investigations. Therefore, we include a set of variables in the model, namely, the annual turnover ratio of the stock (TURNOVER), fluctuation of stock price (VOLATILITY), and the annual return of the stock (RETURNRATIO). Additionally, we used the logarithm of the number of securities analysts who followed the focal firm (LnATTENTION) to proxy the external oversights, as analysts’ attention reflects the extent to which the focal firm’s abnormal performance would be noticed.

We also included variables reflecting whether the firm had committed fraud in the past (PAST_VIOLATE) and whether the firm experienced consecutive losses in the past 2 years and were marked as special treatment (ST) in the given year. As the scrutiny of corporate fraud in the two exchanges might be different, we also controlled for the stock exchange in which the focal firm is listed (SHEXCHANGE). In addition, to control the influence of different industrial environments on the probability of fraud commission and detection, we employed the incidence rate of fraudulent firms in the focal industry in a given year (VIO_INDUSTRY) as a control variable. Finally, we winsorized the primary continuous control variables at the upper- and lower-one percent levels.

As the precise estimation of a bivariate probit model requires different variables in the fraud commission equation and the fraud detection equation, we put only those variables that have direct influences on fraud commission or fraud detection in each equation, respectively. As a result, we used the centrality of director subgroups, internal governance variables and the firm’s operational variables in the fraud commission equation, as those factors reflect the incentive and opportunity for fraud commission. Using similar logic, we designated the centrality of director subgroups and the firm’s visibility variables in the fraud detection equation, because most fraud detection is triggered by abnormal salience in the sight of the public, media, and regulatory agencies.

Empirical Findings

Descriptive Statistics

From 2003 to 2013, there were 1,139 firm-year fraud observations of nonindividual corporate violations reported in 918 enforcement announcements issued by the CSRC and stock exchanges in China. In the full sample, there were 733 observations in the Shenzhen Stock Exchange and 366 observations in the Shanghai Stock Exchange. In total, 1,056 observations involved “information disclosure violation” (marked as type I fraud), and 588 observations involved “operational violation” and “other” (marked as type II fraud). The detailed sample distribution by year, exchange, and fraud type can be found in Table 1.

Sample Distribution.

Note. Type I frauds indicate those frauds related to information disclosure violation, Type II frauds indicate those frauds related to operational violations and other. SZ and SH indicates Shenzhen Stock Exchange and Shanghai Stock Exchange respectively. It could be seen that the Type I frauds are more likely to occur than Type II frauds, and firms listed in Shenzhen stock Exchange are more likely to commit frauds and be detected than those firms listed in Shanghai stock Exchange.

The descriptive statistics and correlation coefficients matrix of the variables are provided in Table 2. There is no strong correlation between variables. Moreover, the variance inflation factors (VIFs) of all variables are less than three, indicating the multicollinearity issue is not significant.

Descriptive Statistics and Correlation Coefficients Matrix.

Note. Each correlation coefficient greater than 0.03 is significant at the level of 0.01. On average, approximately 6.1% of firms committed fraud each year, and the average proportion of independent directors is 35.9%. Additionally, 3.6% of firms in the sample suffered losses over two consecutive years and were marked as ST. Also, as we winsorized IN_NET and ID_NET at the upper and lower 1% levels, their standard errors and means deviate from 1 and 0. The correlation coefficients are below 0.4 for all pairs of variables except for a value of 0.53 between LnASSETS and LnATTENTION and a value of 0.42 between LnASSETS and AUDITOR_BIG4. These results are because large firms receive more attention from securities analysts and their extensive audit work requires a qualified audit firm.

Regression Results

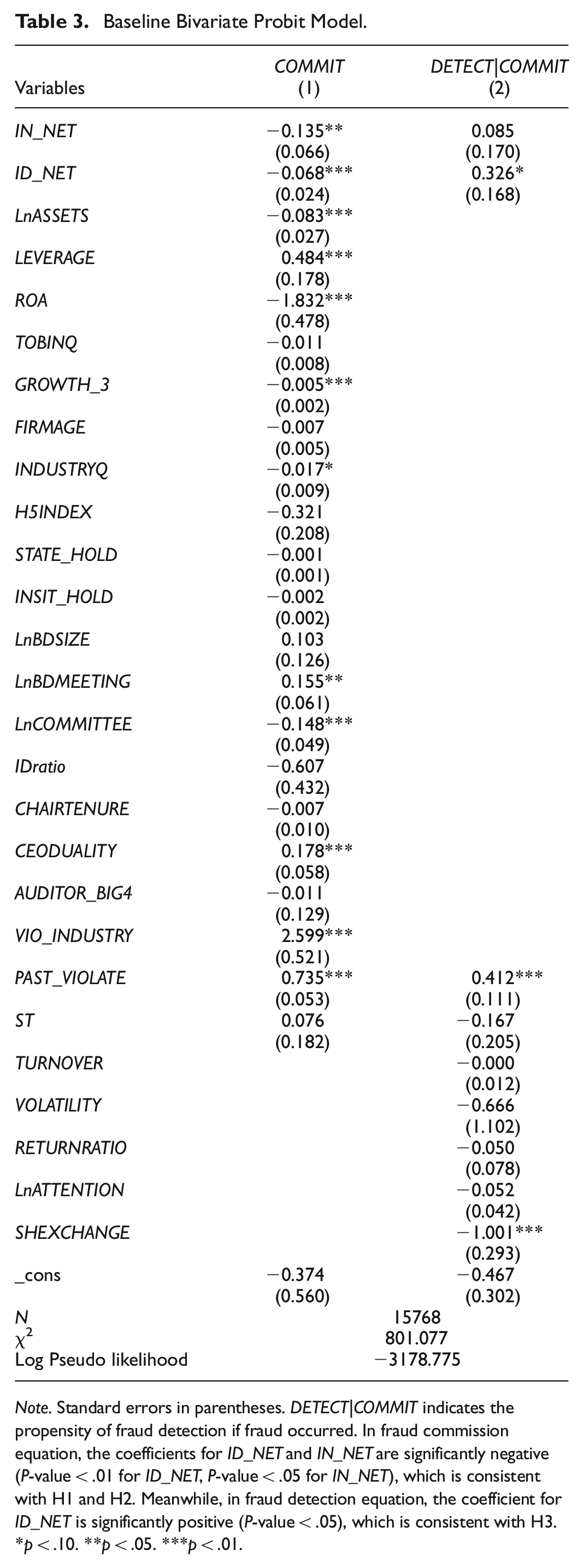

Table 3 reports the results of the baseline bivariate probit regressions on the association between director subgroup centrality and corporate fraud. The model provides adequate power in explaining the probability of fraud commission and fraud detection.

Baseline Bivariate Probit Model.

Note. Standard errors in parentheses. DETECT|COMMIT indicates the propensity of fraud detection if fraud occurred. In fraud commission equation, the coefficients for ID_NET and IN_NET are significantly negative (P-value < .01 for ID_NET, P-value < .05 for IN_NET), which is consistent with H1 and H2. Meanwhile, in fraud detection equation, the coefficient for ID_NET is significantly positive (P-value < .05), which is consistent with H3.

p < .10. **p < .05. ***p < .01.

In column (1) of Table 3, the fraud commission equation, the coefficients on the centrality of dependent director subgroups and independent director subgroups are both significantly negative (P-value < .01 for ID_NET, P-value < .05 for IN_NET), which is consistent with H1 and H2, which hypothesize that the central network position of the dependent and independent director subgroups have significant influence on the reduction of fraud commission incidence.

The results of fraud detection are presented in column (2) of Table 3. The coefficient of the centrality of the independent director subgroup ID_NET is significantly positive (P-value < .05), indicating that a higher likelihood of fraud detection is related to pivotal independent director subgroups. The result is consistent with H3.

Regarding the control variables, our results are consistent with the previous literature (Khanna et al., 2015; T. Y. Wang et al., 2010). Firms with larger scale, higher growth rate, higher market value, more profit, and more board committees are less likely to perpetrate fraud. However, firms with larger board sizes, more board meetings, higher financial leverage, previous fraudulent activities, and CEO duality have a higher risk of fraud commission. Furthermore, firms in declining industries indicated by a lower INDUSTRYQ or in industries where more fraudulent activities occur have a higher tendency toward fraud commission. In addition, fraud committed by companies listed on the Shanghai Stock Exchange are less likely to be detected than fraud committed by those listed on the Shenzhen Stock Exchange.

In summary, the results demonstrate that the association between the centrality of director subgroups and the likelihood of fraud commission is significantly negative for both dependent director subgroups and independent director subgroups, while the probability of fraud detection is significantly positively related to the centrality of independent director subgroups. These results support all three of our hypotheses.

Robustness Tests

To check the robustness of the results, various tests were carried out.

Alternative Model Specification

In the baseline model, we employ control variables related to a firm’s operational situation and corporate governance in the fraud commission regression and used control variables related to a firm’s external visibility in the fraud detection regression. As a robustness check, we also included corporate governance variables in the detection regression and included year dummies in the fraud commission regression while keeping the other control variables unchanged. The results are reported in Table 4.

Robust Test: Alternative Model Specification.

Note. Standard errors in parentheses. DETECT|COMMIT indicates the propensity of fraud detection if fraud occurred with alternative specification, we also included year dummies in the fraud commission equation and included corporate governance variables in the detection regression, while other control variables stay unchanged. The results are consistent with baseline model.

p < .10. **p < .05. ***p < .01.

The results show that, with the alternative model specifications, the sign and significance of coefficients of the centrality of the dependent and independent subgroups in the commission and detection regression remain unchanged, and that of the control variables are also consistent with the baseline model.

Alternative Measure of Dependent Variables

In the baseline model, the dependent variable OBSERVE is measured as whether the focal firm conducted fraudulent activities in the given year. Fraudulent activities could be categorized as “information disclosure violation,”“operational violation” and “others.” To check the robustness of our model, we excluded the fraudulent activities categorized as “others” as their detailed information are unclear and then re-estimated the model. The results are reported in Table 5.

Robust Test: Alternative Measure of Dependent Variable.

Note. Standard errors in parentheses. DETECT2|COMMIT2 indicates the propensity of fraud detection if fraud occurred We excluded the fraudulent activities categorized as “others” from the previous dependent variable OBSERVE for their detailed information are unclear. Accordingly, we obtained two new latent variables COMMIT2 and DETECT2 as the dependent variables in fraud commission equation and detection equation. The results are consistent with the baseline model.

p < .10. **p < .05. ***p < .01.

The coefficients of IN_NET and ID_NET in the fraud commission regression are significantly negative, while the coefficient of ID_NET is significantly positive in the fraud detection regression. In summary, the results are consistent with the baseline model.

Alternative Measure of Independent Variables

In the baseline model, we employed closeness centrality to measure the network position of dependent director subgroups and betweenness centrality to measure that of independent director subgroups. To avoid bias related to the selection of the measure, we also applied alternative measures.

First, we used a synthetic index of four centrality measures as our independent variables. We conducted a principal component analysis (PCA) on the four common indicators of network centrality (degree centrality, betweenness centrality, closeness centrality, and eigenvector centrality) of dependent director subgroups in DDSIN and independent director subgroups in IDSIN. We designated the factors with the largest loadings as IN_NEW and ID_NEW. We also included IN_NEW and ID_NEW as the new independent variables and re-estimated the regressions with the same specification as the baseline model.

The results reported in Table 6 are largely consistent with the baseline model: the coefficients of IN_NEW and ID_NEW in the fraud commission regression are significantly negative. However, the coefficient of ID_NEW is not significant in the fraud detection regression.

Robust Test: Alternative Measure of Independent Variables-PCA Method.

Note. Standard errors in parentheses. DETECT|COMMIT indicates the propensity of fraud detection if fraud occurred by conducting PCA on four network centralities of director subgroup (degree centrality, betweenness centrality, closeness centrality, and eigenvector centrality), we designated the factors with the largest loadings as the new independent variables IN_NEW and ID_NEW and then re-estimated the model. The results are largely consistent with the baseline model, except that the H3 is not supported.

p < .10. **p < .05. ***p < .01.

Second, following the research of García Lara et al. (2007), we employed proxy variables to mitigate potential estimation bias related to the correlation between IN_NET, ID_NET and the control variables. First, we regressed IN_NET and ID_NET on different sets of control variables separately with the OLS model, which are reported in the first four columns in Table 7. Specifically, we included the same sets of control variables as in the commission equation of the baseline model to estimate IN_NET and ID_NET, and then acquired the residuals of the two estimations and denoted them as IN_R1 and ID_R1. After this, we repeated the same procedure in the detection equation and acquired IN_R2 and ID_R2. As those residuals capture the part of network centrality that is orthogonal to the current control variables, they could reflect the exogenous effects of network centrality more accurately. Next, we included IN_R1 and ID_R1 in the commission equation and IN_R2 and ID_R2 in the detection equation and conducted the same regression as the baseline model. The results are reported in column (5) to column (6) of Table 7.

Robust Test: Alternative Measure of Independent Variables-Proxy Method.

Note. Standard errors in parentheses. DETECT|COMMIT indicates the propensity of fraud detection if fraud occurred F and R2 for the first four columns, and χ2 and Log Pseudo likelihood for the last two columns. First, we regressed IN_NET and ID_NET on control variables in fraud commission equation and fraud detection equation separately and acquired the residuals IN_R1, ID_R1, IN_R2, and ID_R2. Second, we included those residuals as independent variables in the model and then re-estimated the regression. The results are consistent with the baseline model.

p < .10. **p < .05. ***p < .01.

As expected, the results are consistent with the baseline model. The coefficients of IN_R1 and ID_R1 are significantly negative, and that for ID_R2 is significantly positive in the detection regression.

Endogeneity Issues

There may be potential endogenous issues stemming from selection bias as firms with high propensities to commit fraud are more likely to appoint directors with particular network attributes. To mitigate this concern, we conducted the regression on a subsample in which the selection bias is unlikely to occur.

In China, dependent directors are the primary participants of fraudulent activities. Since the composition of dependent directors reflects the power balance and resource dependence relationship between controlling shareholders and other large shareholders, it is uncommon to displace dependent directors because of their particular network attributes alone. However, as independent directors act as the counterbalancing force constraining insider controlling, the controlling shareholders would invite those people with fewer directorships to become independent director because they are less influential and easier to be manipulated. Therefore, the potential selection bias would largely occur in the appointment of independent directors.

Accordingly, we focused on the subsample in which the network attributes of the independent director subgroups remained unchanged to exclude the possibility of selection of less connected independent directors by controlling shareholders. As the degree centrality of a director can be directly observed, it would be the primary reference for controlling shareholders in appointing specific independent directors. Thus, we conducted the same regression as the baseline model on a subsample in which the degree centrality of the independent director subgroups in the given year remained unchanged compared with that of the prior year.

As reported in Table 8, the results on the subsample show that the significance and sign of the coefficients of IN_NET and ID_NET in the commission equation and that of ID_NET in the detection equation are largely consistent with the baseline model. The results indicate that our findings are robust after controlling for the endogeneity issue.

Robust Test: Endogeneity Issue: Regression on a Subsample With Unchanged Degree Centrality of Independent Director Subgroup in the Prior Year.

Note. Standard errors in parentheses. DETECT|COMMIT indicates the propensity of fraud detection if fraud occurred To mitigate the concern of endogeneity issue, we conducted the regression on a subsample in which the degree centrality of independent director subgroups remained unchanged with that in the prior year to exclude the possibility of appointment manipulation by controlling shareholders. Accordingly, the sample size decreased to 7,076. The results are largely consistent with the baseline model, except that the H3 is not supported.

p < .10. **p < .05. ***p < .01.

Discussion and Conclusion

Conclusion

As a prominent corporate governance issue, corporate fraud has been studied extensively. However, further research adopting a social network perspective that involves the impact of a corporate board’s external connections is relatively rare, and most of them were conducted on companies in the U.S. Although Zhao and Zhu (2023) have explored the influence of interlocking networks on corporate fraud in China and found a significant deterring effect of board’s social network, their research still have adopted the conventional view regarding the board of director as an intact group, whereas the impact of highly concentrated ownership structure on board structure in China has not been fully reflected. Owing to the compulsory introduction of the independent director system in 2003, the board of directors in Chinese listed companies has in fact been partitioned into a dependent director subgroup and an independent director subgroup, and the interlocking connections among the disparate subgroups of various firms lead to the formation two parallel subgroup interlocking networks. Thus, the primary purpose of this paper is to explore how director subgroup interlocking networks impact corporate fraud in China respectively. Deploying the bivariate probit model with partial observability, we find that the firm whose dependent director subgroup or independent director subgroup holds a central position in its interlocking network (DDSIN or IDSIN) has a low propensity of fraud commission, and that the latter has a high likelihood of fraud detection.

We believe that the external networks of dependent director subgroups help constrain fraud commission by decreasing the incentive to commit fraud, whereas the external networks of independent director subgroups help curb fraud commission by reducing the opportunities for fraud commission and increasing the possibility of fraud detection.

Theoretical Implication

In general, this study has two major theoretical contributions.

First, this study contributes to corporate governance research by exploring the impact of boards’ social networks on corporate fraud in concentrated economy with a subgroup lens. Although corporate fraud has been studied extensively, relevant research from the social network perspective is relatively new, and most existing studies are limited to the US. As the patterns and features of corporate fraud vary according to different ownership concentrations (Coffee, 2005; Soltani, 2014), the discoveries in the US cannot be simply generalized to other countries. By examining relevant hypotheses in China, we find that the dependent director subgroup interlocking network contributes to fraud deterrence, he independent director subgroup interlocking network facilitates both fraud deterrence and fraud detection. These findings are largely different from Kuang and Lee’s findings (2017) on the U.S. companies that the boards’ external connectedness is detrimental to corporate governance but are consistent with Zhao and Zhu’s findings (2023) on Chinese listed companies that boards’ social networks deter fraud occurrence. However, with a subgroup lens, our study provides a more thorough and detailed explanation and points out the similarities and differences between dependent director interlocking network and independent director interlocking networks and their individual impact on corporate fraud. Therefore, this study has discovered the micro-foundation of how board’s social network influence corporate fraud in China and provided a more comprehensive panorama regarding the relationship between a board’s external network and corporate governance issues across different economies.

Second, this study contributes to social network analysis literature by introducing a novel practice for establishing interlocking directorship networks when there is systematic division in the boardrooms. Different form prevalent practices in previous interlocking directorate research, owing to the unique board composition in China, our study identified two types of cohesive director subgroups and accordingly established two parallel director subgroup interlocking networks with different goals and resources. Currently, as many concentrated ownership economies have adopted the independent director system to curb insider controlling, the systematic division between independent director and dependent director in boardrooms is common in other countries such as Korea (Min, 2018) and India (Rajagopalan & Zhang, 2008). Thus, our study provides a novel analytical framework to precisely reflect the essential structure of interlocking directorship in concentrated ownership economies and systematic division in board. In general, this new practice extends the scope of interlocking directorship research and provides insights for studies on interlocking directorship in concentrated ownership economies.

Practical Implication

This study also has important practical implications. As the formal governance measures on corporate fraud prevention in China is ineffective due to the weak rule of law, the finding of this study provides an informal governance measure to curb corporate fraud through the management on board’s social network (Guo et al., 2022). First, as firms that are peripheral in both the IDSIN and DDSIN have less resource channels to cope with competitive adversity and receive little internal constraints on fraud commission, they are the breeding grounds for potential fraud. However, as these peripheral firms lack visibility, they received only limited attention. Therefore, Chinese securities regulators, securities analysts, and the media should increase the scrutiny of these peripheral firms. Second, Chinese securities regulators should encourage the formation of multiple directorships for independent directors. As independent directors would curb fraud commission due to reputational concerns, their social connectedness would strengthen their motivation and ability to constrain fraud commission and facilitate fraud detection. Because additional monitoring mechanisms would bring about unintended implementation costs and unexpected problems, encouraging multiple directorships by independent directors is an efficient way to constrain corporate fraud in China at relatively low cost.

Limitation and Future Direction

This study is not without limitations. First, as the cross-type interlocking directorship is unexplored, future study may investigate the characteristics, formation, and influence of this unique interlocking directorship. Besides, as our analysis on the formation of board subgroups is largely theoretical, more detailed evidence is needed for future research. Thus, more relevant variables can be involved, and even qualitative exploration can be adopted by further studies. Meanwhile, since this study’s data were collected in China before complex corporate governance reform took place since 2013 to reduce interference, its external validity in other time period and other concentrated ownership economies such as Indian, Korea and Russia can be further tested.

Footnotes

Appendix 1

APPENDIX II

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: This study is supported by XJTLU Key Programme Special Fund (KSF-E-60) and XJTLU Research Development Fund (RDF-17-02-48), Key Program of National Natural Science Foundation of China (71932009), IBSS Development Fund and Zhejiang Provincial Philosophy and Social Sciences Planning Project (24NDJC069YB).

Data Availability Statement

Data sharing not applicable to this article as no datasets were generated or analyzed during the current study.