Abstract

The purpose of this study is to analyze the impact of corporate governance and policies on financial sustainability in the presence of earnings management as the moderator in an emerging economy-Pakistan. The study’s population is the manufacturing industry of Pakistan that has 25 sectors and 295 firms listed with the Pakistan stock exchange PSX. Data was collected from Thomson Reuters Datastream for all the 295 firms. Panel data analysis was carried out to examine the impact of the variables of interest. Analysis reveals that out of the two independent variables; that is, corporate governance and policies, the former has a significant impact on financial sustainability. Furthermore, in direct relation earnings management is negatively affecting the financial sustainability of the corporates and the impact is significant with the p-value of .044. Earnings management as a moderator also has a negatively significant impact on the relationship between corporate governance, policies, and financial sustainability with a p-value of .042. This study would help the government and policymakers in making sustainable policies and frameworks.

Plain Language Summary

The purpose of the study is to highlight the impact of corporate governance, policies on financial sustainability and taking earnings management as the moderator. Regression analysis and panel data analysis is conducted to test the model. Results show that corporate governance has a significantly positive impact on the financial sustainability whereas earnings management has a significantly negative impact when take direct or as a moderator. As moderator it weakens the relationship between corporate governance and financial sustainability. This study would help the government and the policymakers in making the framework and sustainable policies. This study has only taken data from Pakistan, to increase the generalizability of the study data from other emerging countries could be taken.

Introduction

The financial crisis 2007 to 08 is one of the many incidents that has compelled the corporates to plan for a longer term. Nowadays corporates are looking for corporate sustainability, aiming to stay in the market for a longer period of time. Corporate Sustainability (CS) as defined by Brundtland’s report 1987: “development that meets the needs of the present without compromising the ability for future generations to meet their own needs.” In another definition, Corporate sustainability is explained as “the ability of a firm to nurture and support growth over time by effectively meeting the expectations of diverse stakeholders,” (Neubaum & Zahra, 2006).

In addition, keeping the long-term survival vision in front, the financial perspective for sustainability is also necessary (Grewatsch & Kleindienst, 2017). There are three elements of sustainability that is, environmental, social, and economic aspects (GRI, 2013) but after the financial crises, financial sustainability has gained importance (Afonso & Jalles, 2015). Organizations now have to develop sustainable policies which can enhance the financial health of the organizations in the longer term (Cabaleiro et al., 2013). Moreover, better corporate governance is required for better financial sustainability as it is the framework through which division and exercise of power is regulated (Licht, 2013). Concept of sustainable growth asks for a balance approach toward the policies of growth and operations, investment, and financing policies (Mubeen & Hanif, 2017).

Over the years, corporates are focusing more on long-term policies and strategies in order to stay in the market and to cater the needs of all the stakeholders. Due to this shift from short-term to long-term perspective, corporates need to understand whether the operations and policies developed are effective and could assist them to be financially sustainable or not? For that reason and to see the impact of financial sustainability, the economic aspect of variables influencing the corporates needs to be studied (Lopez et al., 2007). Additionally, the concept of financial sustainability has limited research with scanty literature available, making this an explorable domain in a developing country like Pakistan. In addition, to implement UN 2030 agenda for sustainable development (SDGs) all the stakeholders are making notable efforts but still, Pakistan is lagging behind the neighboring countries, that is, India and Bangladesh.

It is the need of the hour to investigate policies and their interventions that could be implemented for better planning, governance, performance, earnings management, and long-term financial sustainability (Lu et al., 2021) . In this study, this interconnected framework of the impact of corporate governance and policies on financial sustainability is analyzed in the light of earning management as a moderator. The study is conducted in an emerging nation Pakistan, to add to the literature from developing nations, and to help the stakeholders achieve the SDGs agenda as well. This study would be amongst the foremost studies to analyze the impact of corporate governance and policies on financial sustainability in the light of earnings management in an emerging country.

Review of the Literature

Corporates enter the market with the goal to stay and survive for a longer term, in order to create value and a win-win situation for themselves and all the stakeholders. Now corporates around the globe are more vigilant toward the present and future generations, such vision about all the stakeholders has an impact on the economy at a macro level (Busch & Lewandowski, 2018; Hoffman & Georg, 2013; Horváthová, 2010; Iwata & Okada, 2011; King & Lenox, 2001; Konar & Cohen, 2001; Lee et al., 2015; Lannelongue et al., 2015). Doing good to get good is the essence of survival presently.

Previous literature has shown that corporate sustainability is a complex concept (Aras & Crowther, 2009), many studies have measured CS with CSR (Abner & Ferrer, 2019; Akben-Selcuk, 2019; Baird et al., 2012; Ararat, 2008; Alexander & Buchholz, 1978), and many have measured CS with the three dimensions of CS that is, economic, social and environmental (Grewatsch & Kleindienst, 2017; Krechovska & Prochazkova, 2013; Kurapatskie & Darnall, 2013; Lassala et al., 2017), on the other hand, one of the three dimensions has also been taken to measure CS (Ahmed & Tirmizi, 2020; Bolívar, 2016; Lizinska & Czapiewski, 2018). Despite extensive research going on around the world related to CS still, this field is an emerging field with respect to academic research (Liang & Renneboog, 2020).

The concept of financial sustainability has become a recent concern for the government and corporates (Bolívar, 2016). Corporates are making policies that can help them improve their financial health and enhance their chance of long-term survival (Cabaleiro et al., 2013). The concept of financial sustainability was first introduced by (Hicks, 1945). A review of the literature shows that studies have been conducted to see the financial sustainability at local government level (Cabaleiro et al., 2013; Munoz-Canavate & Hipola, 2011). Being an important component of corporate sustainability, financial sustainability is a long-term balance between growth and development, operational, and financial plans. Therefore, a tradeoff between risk and return is required to survive for a longer period of time (Raza et al., 2020). Poor financial decisions or plans can easily lead to disaster not only for the corporates but for all the stakeholders like government, banks, creditors, suppliers, and at the macro-level disaster for the economy as well (Muhairi & Nobanee, 2019).This situation can be improved with the help of good corporate governance, as better governance can translate corporate policies into corporate sustainability (Wijethilake, 2017). As corporate governance has a positive influence on corporate sustainability (Crifo et al., 2019; Licht, 2013). After the financial crises like Enron, WorldCom, financial crisis 2007 to 08 and other economic crunch, stakeholders around the world and organizations themselves are implementing strict CG principles in order to protect their investors’, stabilize the organizations and to earn more on their investments so to reduce agency cost (Aras & Crowther, 2009). Furthermore, research has also shown the positive impact of corporate governance on firm performance and sustainability (Correa et al., 2020; Hamad et al., 2020; Lazaroiu et al., 2020; Zhang et al., 2020). Investors would pay more for an organization with good corporate governance standards (Beiner et al., 2004). Various studies show the importance that has been given to CG by investors, other stakeholders, organizations, and academicians (Correa et al., 2020; Hamad et al., 2020; Zhang et al., 2020). Corporate governance principles if instigated properly can not only help the organizations to create long term value in the form of corporate sustainability but also assist them to keep a balance between the economic and social benefit. Moreover, corporates are now more mindful of the expectations of society regarding social and environmental risk (Benn & Dunphy, 2007). Furthermore, corporate governance helps in transforming the economic goals of the organizations in order to align them with the sustainability principles for social and environmental justice.

On the other hand, the agency cost associated with conflict of interest between investors and managers can go to a level where it can hamper the growth of the firm and can have a negative impact on firm performance and sustainability (Shleifer & Vishny, 1997). Another negative impact of corporate governance can result in earnings management, according to Healy and Wahlen (1999) earnings management is the conviction of managers to deceive stakeholders about the financial and economic performance in order to benefit more. Mechanism for corporate governance and its quality also determine the level of earnings management (Peasnell et al., 2005). Emerging countries are more prone to earnings management than the developed countries (Li et al., 2011; Shaikh et al., 2019). Earnings management when taken as moderator studies have proved that it has a negative impact between CSR and profitability (Suteja et al., 2016).

Rapid growth in technology and the social scenario has changed the way firms were operating in society. Now broader corporate issues like the rights of people, effect on climate, and air pollution caused due to corporates have enhanced their role in the economy and society. In this situation, the catchphrase for a firm is to do good to make good. To do good firms need financial resources, investment in CSR, or other environmental drives. These investments do have an impact on the operating costs, profits, and incentive to participate in earnings management.

The main objective to engage in earnings management is to boost the firm’s prospects and value in order to meet the high expectations of the shareholders. Another reason could be that managers’ salaries are associated with the firm performance (Bergstresser & Philippon, 2006). Studies have also shown that earnings management can have negative impact on the sustainability of a firm (Chen & Hung, 2020). As the short-term goals of the managers and the shareholders would hamper the long-term interest of all the stakeholders (Lizinska & Czapiewski, 2018). The mechanism for corporate governance and its quality also determines the level of earning management (Peasnell et al., 2005).

Sustainability is a concept that comes with many special issues, foremost, and highly important is to maintain a balance or magnitude, like the magnitude of policy objectives affecting different sectors, government, various stakeholders, different generations, global concern verses local opportunities, economic verses social or environmental goals, long term gains verses short term benefits. Sustainable development asks for policies that can result in inclusive and long-term growth and development (UN, 2015). Moreover, government policies establish a base for a better business environment for all the organizations (Stern, 2015). These policies not only provide the environment for businesses but also add to social responsibility and value addition so drifting toward stakeholders’ model rather than traditional shareholder approach (Schoenmaker, 2017). For financial sustainability coordinated and comprehensive policies and protocols are the need of the time that can safeguard the consumers’ rights, give clarity of existence, back the development of the market, and which can together help to shift from shareholder approach to stakeholder approach (Portilla et al., 2020).

Based on the review of the literature following hypotheses are developed:

H1: Corporate governance has a positive impact on the financial sustainability of the firms

H2: Polices have a positive impact on the financial sustainability of the firms

H3: Earnings management has a negative impact on the relationship between corporate governance, policies, and financial sustainability as a moderator.

Theoretically, an organization should not only operate for maximization of the profit but also for the interests of all the other stakeholders whether internal or external, as defined by the Stakeholder theory. For an organization to operate successfully for a longer period it is necessary to take care of the interest of all stakeholders (Clarkson et al., 2011). Moreover, the concept of sustainable growth asks for a balanced approach toward the policies of growth and operations, investment, and financing policies (Mubeen & Hanif, 2017). Stakeholder theory supports the framework developed for the study as the organizations are created with a vision of long-term success and survival, for that they need to add value and increase the worth of the business by satisfying all the concerned stakeholders. On the contrary, unsustainable growth can take an organization toward financial misery and ultimately toward bankruptcy. Financial sustainability is the requirement of every organization irrespective of size or geographies to survive and sustain itself in the competitive environment (Dhannapal & Ganesan, 2010). Based on the review following theoratical framework is developed as shown in Figure 1:

Theoretical framework.

Econometric Model:

Equation for the Model:

For Moderation:

Methodology

The quantitative research method is used in the study. Data collected is number-based, and analysis is done using the mathematical-statistical modeling (Kabukcu & Chabal, 2021). To get the purpose of this study the methodology adopted is as follows:

Sample and Data

This study uses a panel dataset of annual frequency for the following reason: the more complicated behavioral models can be constructed and tested with the help of a panel dataset as compared to time series or single cross-sectional data sets (Mughal et al., 2021). The study utilized unbalanced panel data set of annual frequency ranging from 2005 to 2019. The secondary data is collected from all the firms listed in PSX under the manufacturing sector of Pakistan. In total, there are 379 firms in the manufacturing sector of Pakistan, and the current study dataset of 295 firms is used due to the non-availability of data. There is a total of 3,814 observations. Data has been collected from reputable Thomson Reuters Datastream for 15 years, that is, from 2005 to 2019. Whereas data related to policies designed by the government and sectors are collected from economic surveys of Pakistan (various years), websites of industrial associations, and sector-wise reports.

Variables

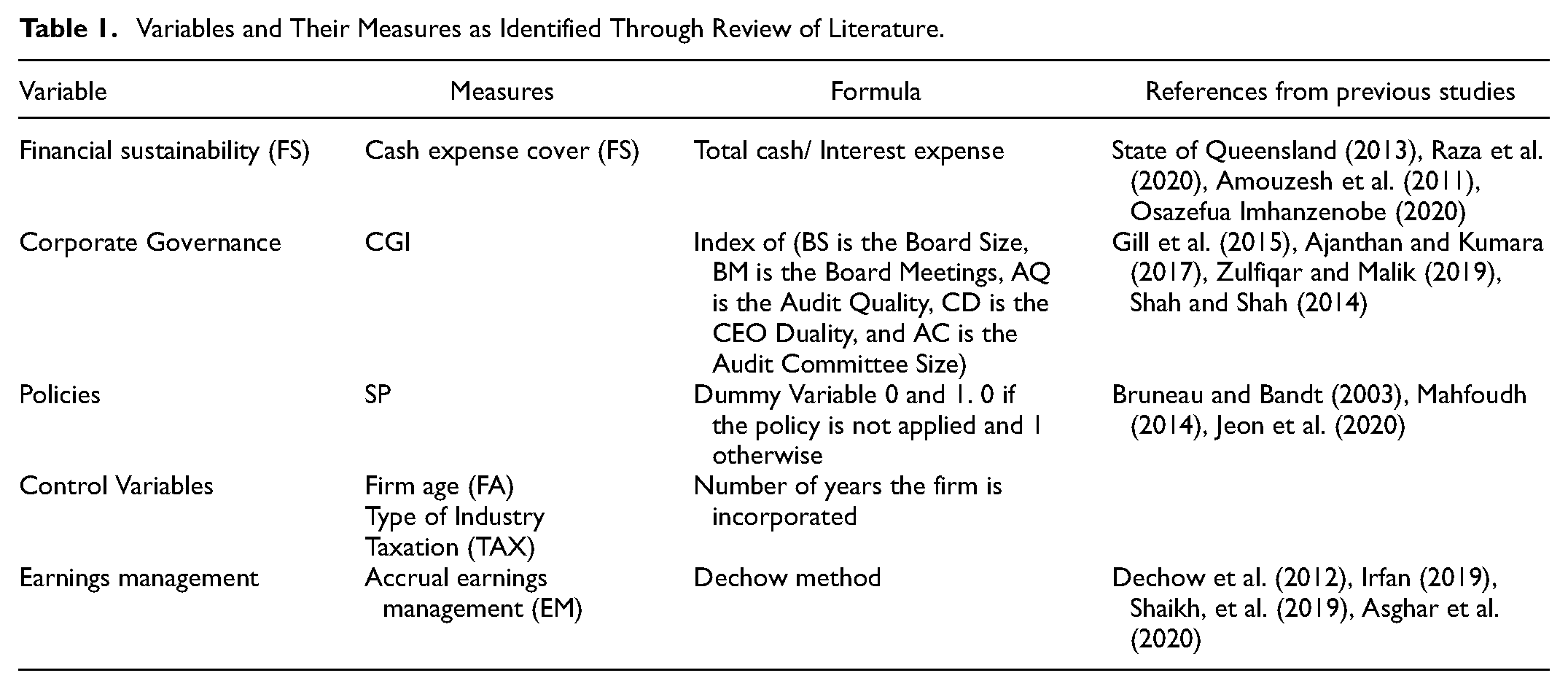

Corporate Governance Index CGI

To develop the CGI for the data sample, data regarding following determinants were collected:

BS is the Board Size, BM is the Board Meetings, AQ is the Audit Quality, CD is the CEO Duality, and AC is the Audit Committee Size

These five components are used to develop the CGI covering the three main themes as identified by Javed and Iqbal (2007) which are board, ownership and transparency or audit. Data related to all the firms were collected then index was develop in Stata software using additive index factor analysis. Index is developed to cater all the elements of corporate governance as it could be measured through various aspects.

The variables and their measures used in the study are shown in Table 1:

Variables and Their Measures as Identified Through Review of Literature.

Analysis

The study is conducted under the epistemology philosophy to obtain them using the science of instigation and the progress of human cognition and laws (Couper, 2020; Wu, 2011) . In a quantitative study, the answers to the research questions are sorted out quantitatively (Allwood, 2012). A problem is quantified by systematically collecting data, analyzing, and interpreting it in a more comprehendible mode. Quantitative analysis also helps to get valid and reliable results.

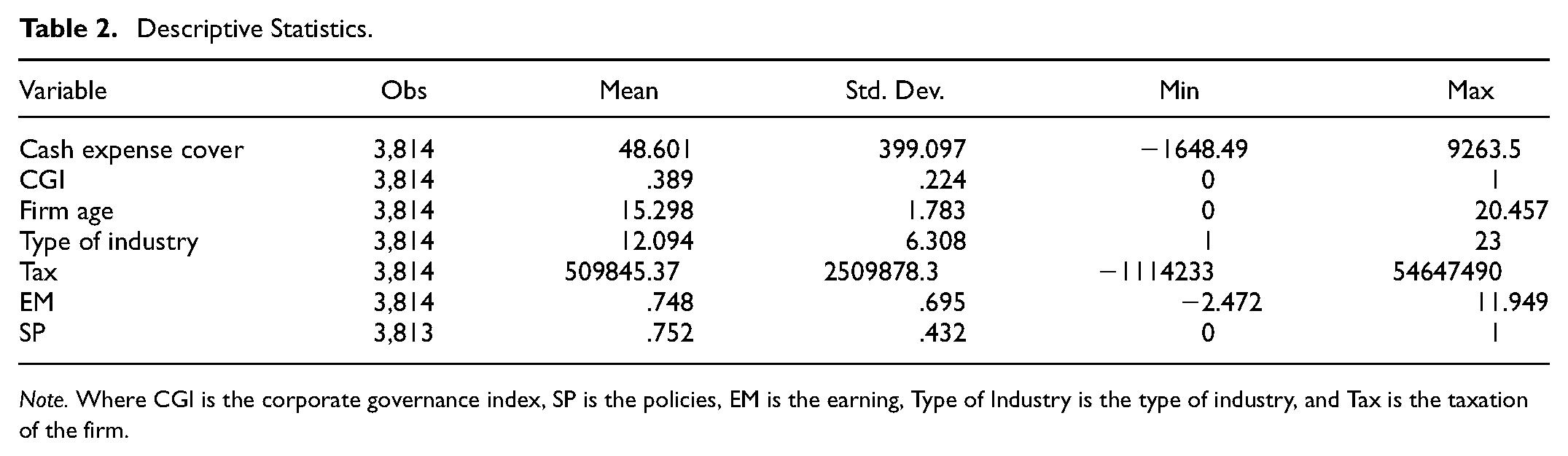

The findings are achieved by application of appropriate data analysis technique that involves the following steps. First and foremost, descriptive statistics to get a preliminary picture of the data as shown in Table 2 and Figure 2. The descriptive analysis is done to check each variable’s minimum, maximum, mean, and standard deviation (Kollias & Messis, 2021).

Descriptive analysis of the data in tabular form is as follows:

Descriptive Statistics.

Note. Where CGI is the corporate governance index, SP is the policies, EM is the earning, Type of Industry is the type of industry, and Tax is the taxation of the firm.

Descriptive analysis.

Linear regression was performed on the data and results are shown in Table 3, cash expense cover was used as the dependent variable to measure the financial sustainability whereas corporate governance index, sectoral policies and accrual earning management were taken as the independent variables along with the control variables: firm age, taxation and type of industry. Following equations were used to perform the regression analysis:

OLS Equation:

Where CGI is the corporate governance index, SP is the policies, EM is the earning management, Firm Size is the size of the firm, Type of Industry is the type of industry, and Tax is the taxation of the firm.

Linear Regression.

Note. CGI is the corporate governance index; SP is the policies; EM is the earning management, Firm Size is the size of the firm; Type of Industry is the type of industry; and Tax is the taxation of the firm.

p < .1. **p < .05. ***p < .01.

Linear regression is carried out to see the strength of relation between the endogenous and the exogenous variables as shown in Figure 3. Results show that CGI, EM and type of industry have a significant impact on the dependent variable financial sustainability with p-values of .021, .044, and .045. However, policies do not have a significant impact on financial sustainability of the firms under study. Impact of CGI is positive as the coefficient and the t-value have positive values whereas, negative values of coefficient and t-value for EM indicate a negative impact on the financial sustainability. Model is fit as the F value is significant. This analysis also helped to see the robustness as the coefficient sign of the dependent variable is not changing with the inclusion and exclusion of the variables.

Linear regression.

The residuals are also normally distributed as evident from the graph represented below in Figure 4:

Residuals normality.

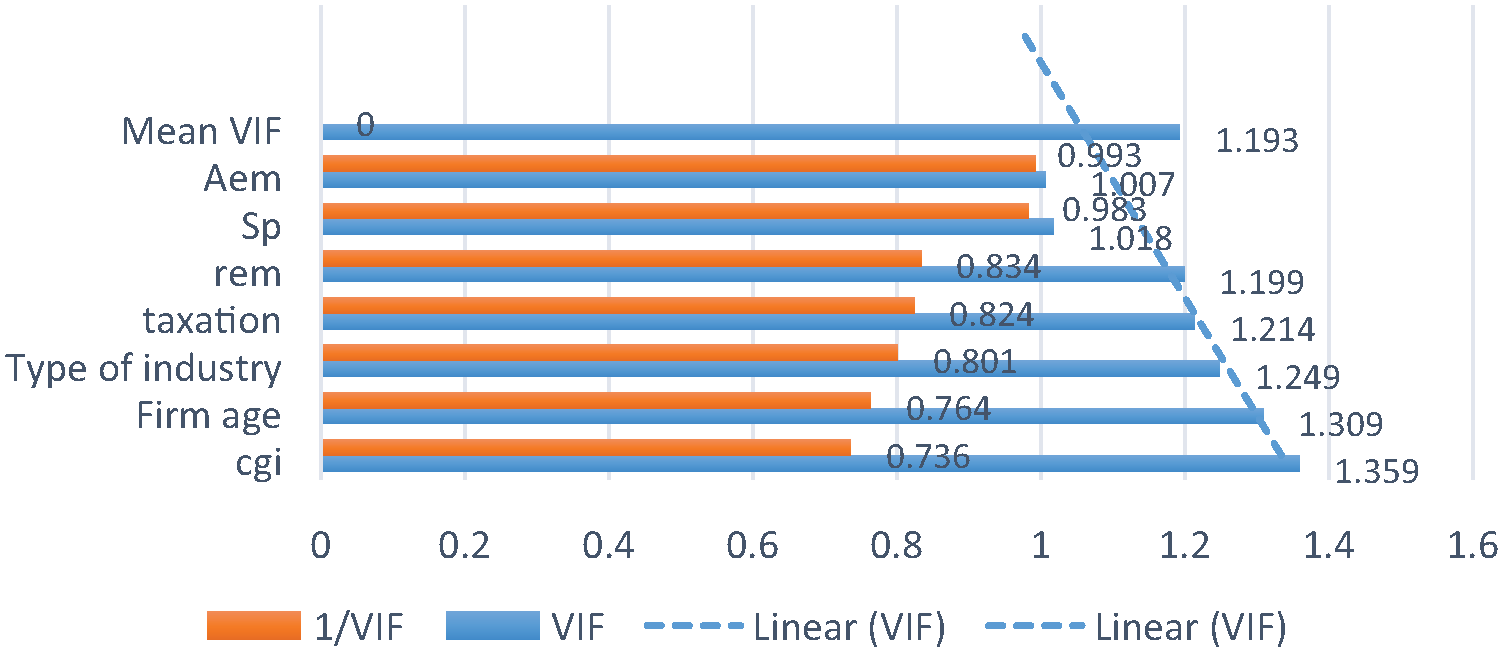

Moreover, test for Multicollinearity (VIF test) shown in Table 4 and heteroskedasticity (White test) shown in Table 5 are also fulfilling the regression assumptions, results of which are as follows:

Variance Inflation Factor.

As all the values are below 10 so variables are not having the Multicollinearity problem as shown in Figure 5.

Multicollinearity.

To test the presence of heteroskedasticity and the robustness of the model, White’s test was conducted and the results for the test are as follows:

White’s test for Ho: homoskedasticity against Ha: unrestricted heteroskedasticity chi2 (34) = 22.15 Prob > chi2 = 0.9413 Cameron & Trivedi’s decomposition of IM-test

IM Test.

As the probability value is more than 5% which means there is heteroskedasticity, again fulfilling the assumption for regression.

Linear regression was taken with Earning Management as the moderator the results are as follows in Table 6:

Regression With Moderator.

Note. Where CGI is the corporate governance index, SP is the policies, EM is the earning management, Firm Size is the size of the firm, Type of Industry is the type of industry, and Tax is the taxation of the firm.

p < .1. **p < .05. ***p < .01.

The result shows that earnings management does have a significant and negative effect when acting a moderator whereas the direct effect of earnings management also had a significantly negative effect on financial sustainability. Again policies are showing a significant impact on the financial sustainability.

In the next step panel data analyses was performed for which fixed effect and random effect were conducted.

Equation for Panel Data Analyses:

Fixed Effects Model:

Where:

Random Effects Model:

Whereas:

Hausman (1978) specification test.

As the value from Hausman test is more than 0.05 it means the random effect is accepted. According to random effect shown in Table 7, only CGI has a significantly positive impact on financial sustainability with a p-value of .049 at a confidence interval of 5%, whereas policies do not have any significant impact on financial sustainability with a p-value of .911. Moreover, earnings management has a significantly negative impact on the financial sustainability with a p-value of .025 significant at 5% confidence level.

Regression Results.

Note. Where CGI is the corporate governance index, SP is the policies, EM is the earning management, Firm Size is the size of the firm, Type of Industry is the type of industry, and Tax is the taxation of the firm.

p < .1. **p < .05. ***p < .01.

Conclusion

The analysis shows that corporate governance plays a significantly positive role in the financial sustainability of all the corporates operating in Pakistan as shown in the studies (Beiner et al., 2004; Correa et al., 2020; Zhang et al., 2020). Corporate governance helps to enhance the survival of the corporates by incorporating the concept of value creation for all the stakeholders. Whereas policies are not demonstrating any significant impact on financial sustainability for the corporates operating in Pakistan. The reason behind this could be the inconsistency in policies with every changing government as they alter the policies according to their specifications. The importance of policies is well proved in the literature, so there is a need to design policies that could enhance sustainability of the corporates, sectors, and the whole economy.

Moreover, the direct impact of earnings management also shows the significantly negative effect, if the corporates indulge in earnings management practices, their long term survival would be compromised. Whereas the moderating effect of earnings management is also showing a negatively significant impact and is further proving that such practices are harmful for the endurance of corporates.

One of the limitations of this research is that data is collected from one emerging country, future researchers could collect data from other emerging countries in order to generalize the findings. In addition, further research related to financial sustainability by incorporating different independent variables could assist in achieving the SGDs.

Footnotes

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.

Data Availability Statement

Research Data that support the findings of this paper is openly available.