Abstract

The objective of this study is to investigate the impact of school ties between top management executives, such as the Chief Executive Officer and Chief Financial Officer, and external parties, including auditors, on a company’s earnings management practices. This study uses fixed effect regression method to test the hypotheses, whether school ties between top management executives and audit partner will affect on the practical earnings management. The authors obtained sample from Indonesia Stock Exchange Commission during 2010 to 2022 and includes several causality tests to robust the empirical result from current study. Our findings suggest a noteworthy positive association between school-ties linking the Chief Executive Officer (CEO) and the Auditor with Earnings Management. However, our analysis reveals that other combinations of school ties exhibit an opposite effect. The findings of this study suggest that ties between internal and external parties within a company may be a factor that investors should carefully consider when evaluating the accuracy and reliability of financial reports. As such, it may be prudent to avoid investing in such companies. Despite prior research extensively examining the measurement of accrual-based earnings management, the literature lacks discussion regarding its association with the potential influence of ties. Thus, this study aims to fill this gap by investigating the relationship between top management school ties and earnings management.

Introduction

The investigation of ties that exist within a company has garnered considerable interest in the academic literature. For instance, J. J. Wang et al. (2020) examined the relationship between a company’s internal and external connections in enhancing performance through the utilization of institutional advantages and external resource capabilities (G. Wang et al., 2013). Such bonding is critical for companies to capitalize on new opportunities and adapt to changes in the environment, leading to short-term access to institutional resources. Other studies, including Gao et al. (2017), J. Wu (2011), J. A. Zhang and Cui (2017), and K. Zhang and Truong (2019), explored the impact of bonding on negative audit opinions and higher audit fees. Increased audit fees were found to be positively associated with auditors who provide modified audit results, leading to new audit quality concerns and discretionary accruals (Guan et al., 2016). Hwang and Kim (2009) conducted an archival study and found that CEO-board social ties not only affected compensation but also resulted in less effective board oversight.

In both China and Korea, the similarity of school alma mater plays an important role in building social relations (Chang et al., 2017). Previous research, for example, used the likeness of school alma mater bonds to be used as measurement and testing related to decisions made by company management and their external parties (Lennox & Park, 2007; Menon & Williams, 2004; Naiker & Sharma, 2009). They began to link the consequences of the social relationship between the CEO and CFO and the board of directors, audit committee members, and external auditors on financial reporting quality and audit quality, assuming that the CEO and CFO are the two most important executives (Harymawan, Minanurohman, et al., 2023; Hoitash et al., 2016) an agency perspective that can increase information asymmetry between management and the board of directors. Still, until now, no one has tested the results of management, such as earnings management or the quality of earnings that can be generated due to ties within the company.

Although the study has extensively explored the measurement of accrual-based earnings management, the literature has overlooked its relationship with the possibility of interference from ties. While Dechow et al. (1995) showed that management could not manipulate revenue, they could still use discretionary income, such as credit sales, to manipulate earnings, which the original model could not detect. Management estimates of earnings typically converge toward zero (Dechow et al., 1995). Additionally, the presence of a CFO in a board position may foster the development of social ties that could potentially lead to losses. Cohen et al. (2017) examined the CEO-audit committee relationship, which created a negative perception among investors about the committee’s independence and effectiveness, and led them to question the acceptability of earnings management practices.

Earnings management (EM) refers to the actions taken by managers to increase (or decrease) reported earnings. This concept identifies two important components of EM: consequences and intentions (Fischer & Rosenzweig, 1995). EM results in increased asymmetric information between managers and investors. Furthermore, EM behavior can harm investors and even affect the real operating efficiency of the company. The emergence of EM reduces the quality and reliability of information in financial statements. EM aims to achieve optimal short-term earnings rather than being closely tied to product innovation and company operations. Therefore, EM can pose a potential risk to the future development of the company (Teoh et al., 2016).

The statement suggests that the relationship between top management ties (Chief Executive Officer, Chief Financial Officer) and external parties (Auditor) may have an impact on earnings management practices. This relationship is plausible due to three underlying factors (Chen et al., 2015). Firstly, we posit that the existence of strong ties may undermine supervision, leading to a negligent attitude toward the results without thorough examination. Secondly, such ties may enable the leakage of confidential information, facilitating the manipulation of earnings management practices. Thirdly, the relationship between professionals may lead to a state of helplessness or lack of independence, jeopardizing ethical decision-making. These factors have motivated our research to explore the potential impact of such ties on earnings management practices (Bamber et al., 2010).

The structure of this paper is as follows: In Section 2, we present a thorough review of the relevant literature. In Section 3, we provide an overview of the research methodology that we employed. Section 4 contains a detailed analysis of the results we obtained, followed by a discussion of these findings. Finally, in Section 5, we draw our conclusions and provide recommendations for future research.

Literature Review and Hypothesis Development

Institutional Setting: The Indonesian Earnings Management Studies

The close relationship between top management and auditors is believed to harm auditor independence which contributes to the occurrence of financial scandals and it is doubtful that the reliability of audit results affects earnings quality. Therefore, regulations related to the consideration of auditor independence are intended to improve audit quality and prevent close relationships between auditors and management/directors because the independent attitude is abstract, difficult to measure, and must be obeyed by auditors. Regulations related to auditor independence are aimed at enhancing the quality of audits and preventing the existence of close relationships between auditors and management/directors. This is because the independent attitude of auditors is abstract and difficult to measure, making it necessary for auditors to strictly adhere to the rules and regulations that govern their independence.

Earnings management is a common phenomenon in Indonesia, as it is in many other countries. Indonesian companies have been found to engage in various earnings management activities, including income-increasing activities such as accruals management and income-decreasing activities such as real activities manipulation. Several factors have been identified as contributing to the prevalence of earnings management in Indonesia. One of the factors is the lack of strong regulatory oversight, which creates an environment where companies may engage in unethical practices without fear of significant consequences. Another factor is the pressure to meet financial targets, particularly in the short term, which can lead to managers manipulating earnings to avoid negative consequences, such as a decline in stock prices or loss of investor confidence. To address this issue, the Indonesian government has implemented various regulations aimed at improving financial reporting transparency and reducing the incidence of earnings management. For example, the Financial Services Authority (OJK) has issued regulations that require companies to disclose more detailed information about their financial statements, including any unusual or non-recurring items that may impact their earnings. The Indonesian Institute of Accountants (IAI) has also implemented standards aimed at improving the quality of financial reporting, including the adoption of International Financial Reporting Standards (IFRS) in 2012. Despite these efforts, earnings management remains a significant issue in Indonesia, and further research is needed to understand the nature and extent of this phenomenon and to develop effective strategies to address it.

In Indonesia, Indonesia’s Republic Law no. 5 of 2011 concerning the Explanation of Public Accountants states that in providing guarantee services, public accountants and accounting firms must maintain independence from conflicts of interest with clients. Conflict of interest in this regulation means that a public accountant or related party has a financial interest or has significant control over the client or obtains economic benefits from the client. Another consideration that is free from conflicts of interest such as a public accountant or related party has a family relationship with a leader, director, administrator, or person holding a key position in finance and/or accounting to clients such as husband, wife, children, parents, or relatives. Biological, but in a deeper relationship such as the similarity of the school alma mater has not been determined. This research may provide other considerations regarding regulations that are suitable for targets in Indonesia.

The Contemporary Studies of School-ties on Firm-Executives and Opportunistic Behavior

One recent study on the contemporary of school ties on firm-executives and opportunistic behavior is “School ties, social capital, and opportunistic behavior: Evidence from Chinese listed companies” by Huang et al. (2012). The study investigates the effect of school ties between executives and the controlling shareholders on opportunistic behavior in Chinese listed companies. The authors use a sample of 1,715 Chinese listed companies and find that school ties between executives and controlling shareholders have a positive effect on opportunistic behavior, as measured by related-party transactions and earnings management. The presence of independent directors on the board helps alleviate the negative impact of social ties on opportunistic behavior in Chinese listed companies, as revealed in the study. This research adds to the existing literature on the connection between social ties and opportunistic behavior by providing evidence from the Chinese context. The findings hold significance for corporate governance and suggest that having independent directors can mitigate the adverse effects of school ties on opportunistic behavior (P. Wu et al., 2015).

Several recent studies, including Lau et al. (2016), Guan et al. (2016), and Griffin et al. (2021), have investigated the relationship between earnings management and the school ties of top management, including in Indonesia. For instance, Harymawan et al. (2021) found that companies with top executives who have school ties with auditors tend to engage in earnings management practices to artificially inflate their reported earnings. Another study by Oswal et al. (2020) examined the impact of school ties between top executives and politicians on earnings management in Indonesia and discovered a positive association between the two. Similarly, Kumala and Siregar (2021) observed a negative impact of school ties between top executives and auditors on earnings quality in Indonesia. Additionally, Prastiwi et al. (2021) explored the effect of school ties on the effectiveness of internal control systems and found that companies with school ties between top executives and internal auditors tend to have weaker internal control systems, which can contribute to increased earnings management. Collectively, these studies indicate that school ties between top executives and auditors or politicians can lead to higher occurrences of earnings management and weaker internal control systems, ultimately resulting in lower earnings quality. Further research is necessary to delve into the mechanisms behind these relationships and identify potential solutions to address the issues of earnings management and weak internal controls.

Earnings management has persistently plagued Indonesia’s corporate environment, resulting in a significant number of financial reporting fraud cases in the past (Kuang et al., 2022). Researchers have increasingly focused on studying earnings management in Indonesia to comprehend the extent and nature of the problem and explore potential remedies. Various studies have employed diverse research methods and investigated different factors that may influence earnings management. For example, some studies have examined the impact of corporate governance, ownership structure, and audit quality on earnings management, while others have explored the role of cultural factors such as ethical values and moral intensity in shaping earnings management behavior. Despite the growing body of research, there are still gaps in understanding earnings management in Indonesia. Future studies could assess the effectiveness of current regulations and policies in preventing earnings management and fraudulent financial reporting (Harris & Bromiley, 2007). Furthermore, research could investigate the impact of technology and digitalization on earnings management within Indonesia’s corporate environment. Additionally, studies may delve into the role of auditors in detecting and preventing earnings management and explore methods to enhance auditor independence for improved audit quality. Finally, the consequences of earnings management on various stakeholders, including shareholders, creditors, and employees, as well as the broader economic implications of fraudulent financial reporting, warrant further examination.

Hypothesis Development

According to existing literature, the role of top managers is essential in determining a company’s success (Eisenhardt & Schoonhoven, 1990; McGee et al., 1995). Independent board members play a crucial role in ensuring fair CEO compensation practices and preventing excessive salaries (Hwang & Kim, 2009). In transitional economies that lack formal institutional support, top managers often rely on personal relationships with managers from other companies (business relationships) and government officials (political ties) to compensate for the institutional vacuum (Peng & Heath, 1996; Xin & Pearce, 1994). Within this context, top managers may depend on personal relationships with managers from other companies and government officials to navigate the business environment. In China, this is referred to as “guanxi,” while in South Korea, it is known as “jeong.” These relationships are built on mutual trust and reciprocity, providing businesses with access to resources, information, and opportunities that may otherwise be inaccessible (Rajeevan & Ajward, 2020). However, relying on personal relationships and political ties also carries risks. It can lead to cronyism, corruption, and limited opportunities for those without access to these networks. Furthermore, these relationships can be fragile and susceptible to changes in the political or business environment. Therefore, while personal relationships and political ties can be advantageous in transitional economies, it is crucial to establish formal institutional support and develop a robust legal framework that provides long-term stability and predictability for businesses (Karpoff et al., 2017).

Inter-firm relationships among top managers can create collaboration opportunities and implicit collusion while reducing competitive costs and uncertainty (Lau et al., 2016). These business ties can also provide legitimacy and transactional security for companies through the trust established in these relationships (Abdullah & Tursoy, 2021; Acquaah & Eshun, 2010; Cahyono & Sawarjuwono, 2022). However, it is important to acknowledge that these ties may also result in group bias and personal gains at the expense of shareholders (Fracassi & Tate, 2012). Collaboration and coordination between firms can lead to economies of scale, more efficient resource utilization, and improved information sharing. Additionally, these business ties can enhance legitimacy and transactional security by facilitating business transactions and recommendations between top managers. Nevertheless, it is crucial to recognize that these ties may also result in group bias and prioritize personal gains over the interests of the company and its shareholders (Huang et al., 2012; Kuang et al., 2022; Kumala & Siregar, 2012). Top managers may prioritize their personal relationships and alliances, potentially leading to collusive practices such as price fixing or market division, benefiting themselves but harming competition and consumers (Chiu et al., 2013; Ngelo et al., 2022; Xie et al., 2003). Therefore, striking a balance between the benefits and risks of inter-firm relationships among top managers is crucial. While these relationships can provide collaboration opportunities and transactional security, it is vital to ensure they do not lead to collusion or group bias, and that the interests of shareholders and consumers are safeguarded (Bertrand & Schoar, 2003; Cohen & Zarowin, 2010; Hoitash et al., 2016; Park & Shin, 2004). This can be achieved through regulatory oversight, corporate governance, and transparency in business practices.

While we remain optimistic about the potential interest among researchers in exploring this field, we find it encouraging that educational ties between top management and external auditors do not appear to influence earnings management (Klein, 2002). This presents an opportunity to examine the impact of school-ties on high earnings management and low reporting quality (Bruynseels & Cardinaels, 2014; Kontesa et al., 2021). Furthermore, the presence of school-ties can be informative in terms of the likelihood of financial statement restatements, as well as the potential for increased pressure to engage in more aggressive earnings management practices (Harymawan et al., 2022). The latter scenario can lead to negative outcomes for investors, including a lack of profitability and difficulties in obtaining reliable information. In some cases, it may even lead to reporting inaccuracies or fraudulent practices. Based on these observations, we propose the following hypothesis:

Apart from the top management (CEO and CFO), other employees in the company also play a significant role in determining earnings management and participate in decision-making processes. The CEO and CFO can collaborate to achieve their primary goals, and the most substantial collaboration is the closest collaboration that can represent cooperation and obscure its direct influence (Cahyono, Haider, & Sawarjuwono, 2023; Feng et al., 2011). However, their relationship must be avoided from the existence of professional bias with auditors that can develop from the same educational background. In Indonesia, most accounting firms only establish kinship rules between the signing auditor (partner) and top management, but there are social ties that can build and strengthen the relationship between the signing auditor and top management (Hambrick & Mason, 1984). According to Guan et al. (2016), social ties born from an educational background also involve in decision-making. The relationship between auditors and top management as alumni provides an opportunity to interact about their school values (Meek et al., 2007). Based on these findings, we hypothesize that combining the CEO and CFO with auditors would lead to better decision-making processes regarding earnings management. Hence, the following hypotheses as stated:

Data and Research Methodology

This study used a variety of secondary research sources, including the Annual Report, ORBIS, LinkedIn, Google Scholar, Google, and the KAP Official Website. We collected data on 1,580 companies listed on the Indonesia Stock Exchange from 2010 to 2021. The data obtained from IDX can be cross-checked with financial service regulatory authorities to verify its availability and accuracy. Cross-checking the data obtained from IDX with financial service regulatory authorities can help ensure that the information is up-to-date, reliable, and meets compliance standards (Viana et al., 2022). This verification process can be particularly important for businesses and investors who rely on this data to make informed decisions. It can also provide transparency and accountability in the financial industry, which is crucial for maintaining trust and stability in the market. Therefore, it is advisable to regularly cross-check data obtained from IDX with financial service regulatory authorities to minimize the risk of errors or inaccuracies. Due to the COVID-19 pandemic, we divided our samples according to the crisis and non-crisis economy. We tested separately the samples that were in conditions of an economic crisis caused by COVID-19, while we tested the other samples directly. Thus, the results of testing the study can control for sample differences between crisis and non-crisis periods.

The sample was obtained by eliminating companies with missing data in any of the variables used, as presented in Table 1. Table 1 contains several panels that show the distribution of the sample based on different variables. Panel A presents the distribution of the sample based on missing data in any of the variables used. Panel B shows the sample distribution based on the year of observation. Panel C presents the distribution of the sample based on industry and whether the CEO and CFO have similar school ties or not. The table indicates that companies with similar CEO and CFO school ties accounted for 63.16% (998) of the sample, while those without such ties accounted for 36.84% (582). Therefore, the sample size and distribution provide a comprehensive basis for analyzing the relationship between school ties and earnings management in Indonesian companies.

Sample Selection and Firm Distribution by Industry and Period.

To define the dependent variable, Guan et al. (2016) adopted the concept of school-ties, which refers to the similarity of the educational backgrounds of individuals in different positions, regardless of their study programs or graduation periods. A dummy variable was created to indicate the presence (1) or absence (0) of school-ties between two juxtaposed positions. As for the independent variable, we measured earnings management using Dechow’s model, which assumes that accrual recognition shifts over time. This model allows for adjustments to be made to reported earnings in order to reflect the company’s performance more accurately and timely. The cash flow model, as proposed by Dechow and Dichev (2002), is considered the most important method for matching accruals with cash flows. In this model, the firm’s accruals are estimated as the residual of an equation where changes in the firm’s current working capital accruals are a function of the firm’s past, current, and future cash flows.

where ΔWCit is the change of working capital for a firm i in year t; OCFt − 1 is the operating cash flows at the end of year t − 1; OCFt is the operating cash flows at the end of year t; OCFt + 1 is the operating cash flows at the end of year t + 1. ΔWC is defined as (Δaccounts receivable + ΔInventory—Δaccounts payables—Δtaxes payable + Δother assets), while average total assets scale all variables in Eq. (1).

The control variables were selected based on previous research, including the number of directors (DIRSIZE) (Roiston & Harymawan, 2022), number of commissioners (COMSIZE) (Guan et al., 2016; Ningsih et al., 2021), and independent directors (INDCOM) (Muttakin et al., 2018) to represent good corporate governance. Firm size (FIRMSIZE) (Abdullah et al., 2023) and leverage (LEV) (Cahyono, Harymawan, & Kamarudin, 2023) were chosen to represent company characteristics, while return on assets (ROA) (Ningsih et al., 2021) and loss (LOSS) were selected as profitability ratios to represent company performance, as in Guan et al. (2020). The definitions of the variables used in this study for further information are listed in Table 2.

Variable Definitions and Measurement.

This study was then tested using the fixed effect regression model from STATA 14.0 software to test the relationship between the dependent variable and the independent variable and involve the control variable in it.

Result and Discussion

Empirical Result: Descriptive Statistic and Pearson Correlation

Table 3 provides an overview of the descriptive statistics for all the variables of interest, as well as the control variables used in this study. The sample size for this study is 1,580 observations. Earnings management, as measured by the Dechow model (Dechow et al., 1995), is represented by a mean of 0.059. TIES_CEOCFO, TIES_CEOAUDITOR, and TIES_CFOAUDITOR, which represent the CEO-CFO, CEO-Auditor, and CFO-Auditor school-ties, respectively, have different means of 0.012, 0.037, and 0.059.

Statistic Descriptive.

Table 4 presents the Pearson correlation results between the variables analyzed in this study. Our findings indicate that Earnings management, proxied by the Dechow model (DECHOW), is positively and significantly correlated with TIES_CEOAUDITOR, FIRMSIZE, and ROA. This is in line with our hypothesis that school-ties between CEOs and auditors may lead to increased earnings management practices by the company. Additionally, the positive correlation with ROA supports our assertion that earnings management may be linked to our primary variable.

Pearson Correlations.

Note. p-Values in parentheses.

p < .1. **p < .05. ***p < .01.

Table 5 Panel A shows the univariate tests of the company’s firm characteristics with and without the CEO and CFO school-ties. In this test, we can see that from TIES_CEOAUDITOR and TIES_CFOAUDITOR, companies that have a CEO and a CFO school-ties show the same mean. However, in contrast to the comparison shown on the side of companies with no school-ties between the two, companies without a CEO and CFO school-ties show a higher number than companies with school-ties. Panel B shows the univariate tests of the company’s firm characteristics with and without the CEO and Auditor school-ties. From this point of view, DECHOW shows the significance of the figures shown in their coefficients. Significantly, companies with CEO and Auditor school-ties will tend to have higher TIES_CFOAUDITOR than companies without school-ties. The rest did not show significance, but they showed varied conditions in each of its variables. Panel C shows the univariate tests of the company’s firm characteristics with and without the CFO and Auditor school-ties. From the perspective of TIES_CEOAUDITOR, companies with CFO and Auditor school-ties will be significantly higher than companies that do not have school-ties. Our assumption may be justified from this test because the important is companies with top management will work together and support each other so that bonds with auditors still have a higher chance of being built between the three in each combination.

Univariate Tests.

Note.t statistics in parentheses. *p < 0.1. **p < 0.05. ***p < 0.01.

Main Result: Top Management School-ties and Earnings Management

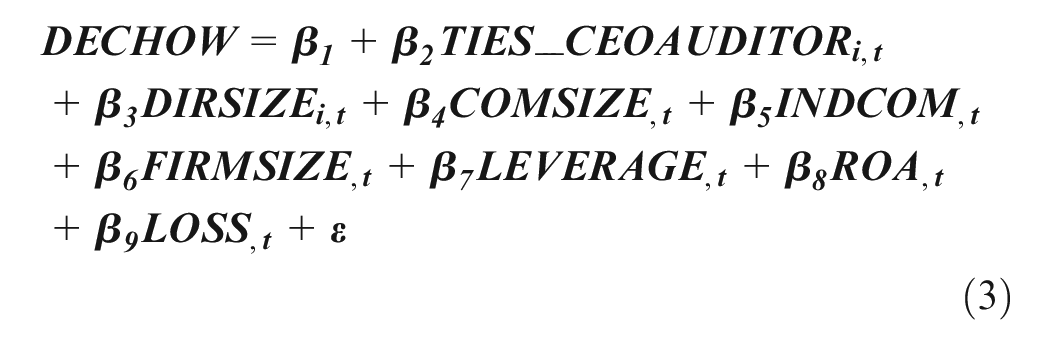

This section examines the formulation of the first hypothesis that CEO and CFO school-ties have a positive relationship with earnings management. To test hypothesis 1, I specified a regression model linking dependent variable, test variable, and batteries of control variables as follows:

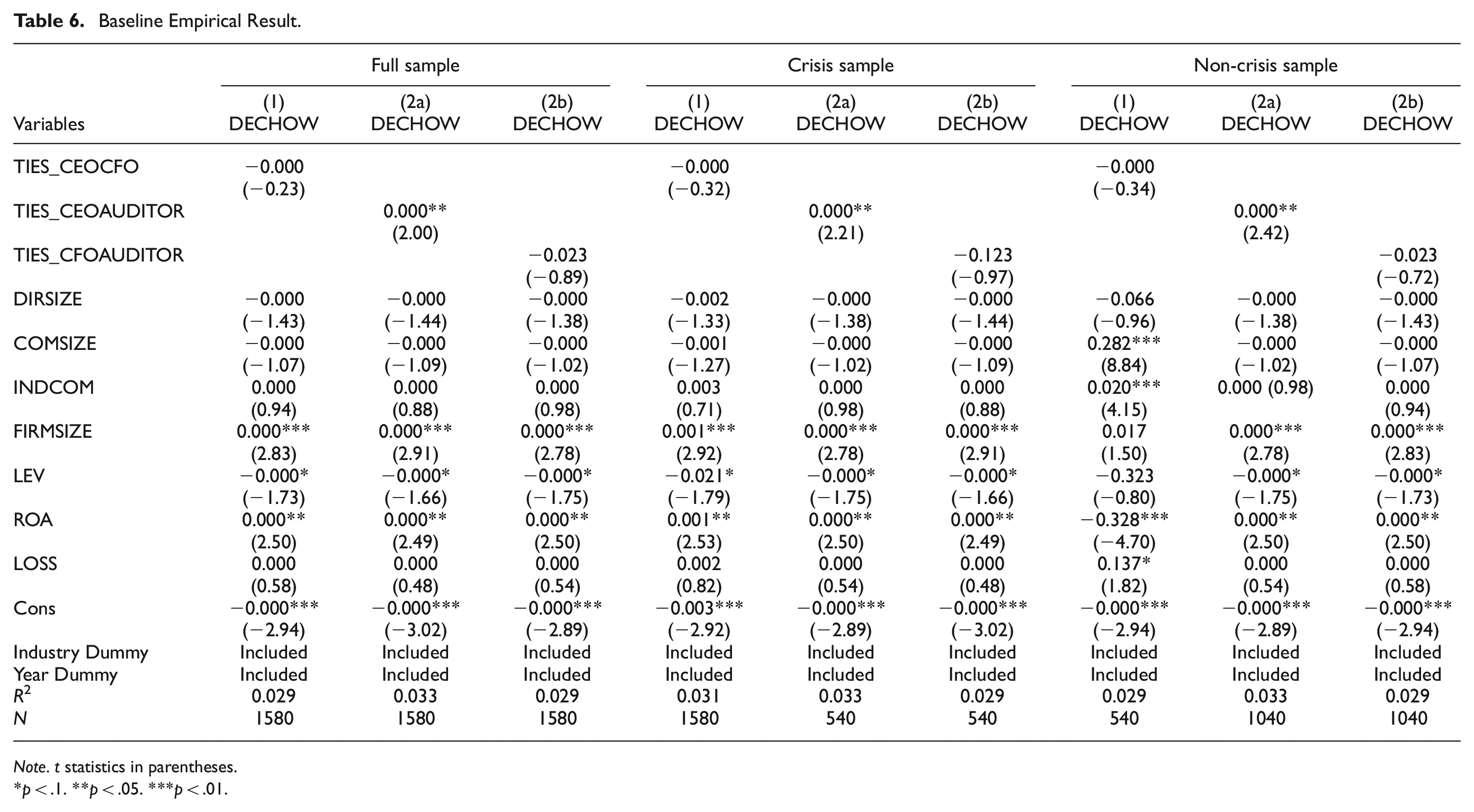

In the regression model results, Table 5 (equation 1) presents the hypothesis test 1, which indicates that the TIES_CEOCFO coefficient is −0.000 and statistically insignificant (z = −0.23). This means that there is no association between CEO and CFO school-ties and an increase in earnings management, leading to the rejection of the first hypothesis. It is possible that school-ties could enhance access to information and facilitate communication and negotiations. However, when it comes to earnings management, there may be other factors at play that result in a negative relationship. Our findings do not provide a definitive explanation for this, but it is possible that a critical point in the combination of school-ties could shed more light on this issue.

The literature has contributed to our understanding of how social networks, such as school-ties, can influence various outcomes in different settings. Research has demonstrated that school ties can play a role in facilitating access to valuable resources, information, and employment prospects. Particularly within the labor market, school ties have been shown to improve the effectiveness of connecting employers with suitable employees, while also fostering social cohesion and trust within the workplace (Sihombing et al., 2023). However, the potential negative consequences of school-ties have also been documented. For example, school-ties may contribute to the perpetuation of social inequality, by giving preferential treatment to individuals with privileged backgrounds. They can also limit diversity and innovation, by favoring conformity and groupthink over individual creativity and dissent. In the specific case mentioned, the combination of school-ties seems to play a role in an unexplained phenomenon (Sáenz González & García-Meca, 2014). This highlights the need for further research on the dynamics and effects of social networks, particularly in complex and dynamic settings such as the one in question. Exploring the critical point in the combination of school-ties that might shed more light on the issue is a promising avenue for future inquiry. By deepening our understanding of how social networks operate and interact with other factors, we can develop more effective strategies to harness their potential benefits while mitigating their potential drawbacks.

Main Result: Top Management and Auditor School-ties and Earnings Management

Our second test examines the relationship between top management and external parties, specifically auditors. We have two parts to our hypothesis 2. Hypothesis 2a focuses on the impact of CEO and Auditor school-ties on earnings management. To test this, we specified a regression model with the dependent variable as the test variable and a set of control variables. The model is as follows:

The results presented in Table 6 (equation 2a) support hypothesis 2a, indicating a statistically significant coefficient of TIES_CEOAUDITOR at the 5% level (z = 2.00), with a value of 0.000. This suggests that companies with school-ties between CEOs and auditors have a positive association with earnings management, which can compromise the independence of auditors and negatively impact the quality and reliability of financial reporting. This finding is in line with previous research by Guan et al. (2016), who argued that school-ties between auditors and the board of directors can lead to higher levels of earnings management. Furthermore, high levels of earnings management may indicate low reporting quality (Bruynseels & Cardinaels, 2014). Thus, regulators should consider implementing policies to mitigate the potential negative impact of these relationships on financial reporting practices, and investors should exercise caution when analyzing financial information from companies with school-ties.

Baseline Empirical Result.

Note. t statistics in parentheses.

p < .1. **p < .05. ***p < .01.

Main Regression Analysis

Guan et al. (2016) made a notable contribution to the existing body of knowledge on corporate governance and financial reporting by shedding light on the potential risks associated with school ties between auditors and corporate boards. Their study reveals that these ties can give rise to conflicts of interest and compromise the independence of auditors, ultimately leading to an increase in the manipulation of financial statements. This finding holds particular significance in the context of high-profile corporate scandals like Enron and WorldCom, where the presence of auditor-board relationships played a role in enabling financial misconduct and fraudulent activities. The research conducted by Guan et al. emphasizes the critical importance of maintaining a robust system of checks and balances within corporate governance, which includes independent audit committees and external auditors, to safeguard the credibility and accuracy of financial reporting. Their work also highlights the need for further research into the factors that influence auditor independence and the effectiveness of regulatory mechanisms designed to prevent earnings management. By shedding light on the potential risks associated with school ties between auditors and the board of directors, Guan et al.’s research contributes to a broader understanding of the complex dynamics at play in corporate governance and financial reporting.

Our second hypothesis (2b) aims to investigate the potential impact of school-ties between a company’s CFO and its auditors on earnings management. To test this hypothesis, we employed a regression model that linked the dependent variable (earnings management), the test variable (CFO-auditor school-ties), and various control variables. The regression model was specified as follows:

Our hypothesis 2b, which suggests that companies with CFO and Auditor school-ties are associated with high earnings management, is rejected based on the results of this test. The coefficient of −0.023 is not significant (z = 0.89). We further analyzed the reasons for this finding and concluded that the CEO and Auditor school-ties might be sufficient to represent the company’s goals in improving earnings management. The CEO, as the top manager, has enough control over colleagues both inside and outside the company, even without the involvement of the CFO and the Auditor with school-ties (Alkebsee et al., 2022; Ramos et al., 2023).

As a result, the lack of association between CFO and Auditor school-ties and earnings management is not a cause for concern. Furthermore, this finding highlights the importance of considering the specific roles and responsibilities of different members of top management when analyzing the impact of school-ties on earnings management. It suggests that the CEO may play a more critical role in determining the company’s reporting practices than the CFO or Auditor, even if they have school-ties with each other or with the CEO. Overall, our study emphasizes the need for investors and regulators to be aware of the potential impact of school-ties on earnings management behavior in companies. While the CFO and Auditor school-ties did not show a significant association with earnings management, the CEO and Auditor school-ties did show a positive relationship. This suggests that companies with these relationships may be more prone to engaging in earnings management practices, which can have negative consequences for investors and the market as a whole. As such, we recommend that investors exercise caution when relying on financial reporting from companies with CEO and Auditor school-ties, and that regulators consider broader policies to address the potential negative impact of these relationships on the reporting practices of companies.

Robustness Test

Previous research indicated that there was a positive association between the shared educational background, or alma mater, of top management and auditors, and earnings management practices in companies. However, these findings may have been affected by endogeneity issues, where the observed relationship is influenced by other factors. To obtain a more representative sample that accurately reflected the test results, we utilized Coarsened Exact Matching (CEM) methodology. Secondly, we tested for unreal variables that could impact the relationship between the independent and dependent variables by employing a two-stage testing model.

Coarsened Exact Matching Method

To address the endogeneity problem, we utilized coarsened exact matching (CEM) to group suitable samples based on their similar characteristics (Blackwell et al., 2009). Table 7 displays a matching summary resulting from the coarsened exact matching treatment. Panel A indicates that the resulting matched sample comprised 468 observations with a similarity in the CEO’s alma mater, and 330 observations without the similarity in the CEO’s alma mater. Similarly, panel B shows that the matched sample comprised 438 observations with a similarity in the CFO’s alma mater, and 360 observations without the similarity in the CFO's alma mater. Lastly, panel C displays that the matched sample comprised 458 observations with a similarity in the auditor’s alma mater, while the unmatched sample had a total of 340 observations with an unequal alma mater. By using coarsened exact matching, we were able to effectively group the samples based on their similar characteristics, reducing the potential impact of endogeneity on our results.

Coarsened Exact Matching Summary.

Table 8 presents the results of the sample match test, which was performed using the coarsened exact matching method. The results show that there were no significant changes from the baseline tests, and the conclusions remain consistent with the previous tests. Therefore, the sample match test supports the findings of the baseline tests, confirming the robustness of our results.

Coarsened Exact Matching (CEM) Regression Result.

Note. t statistics in parentheses.

p < .1. **p < .05. ***p < 0.01.

Heckman Two-Stage Model

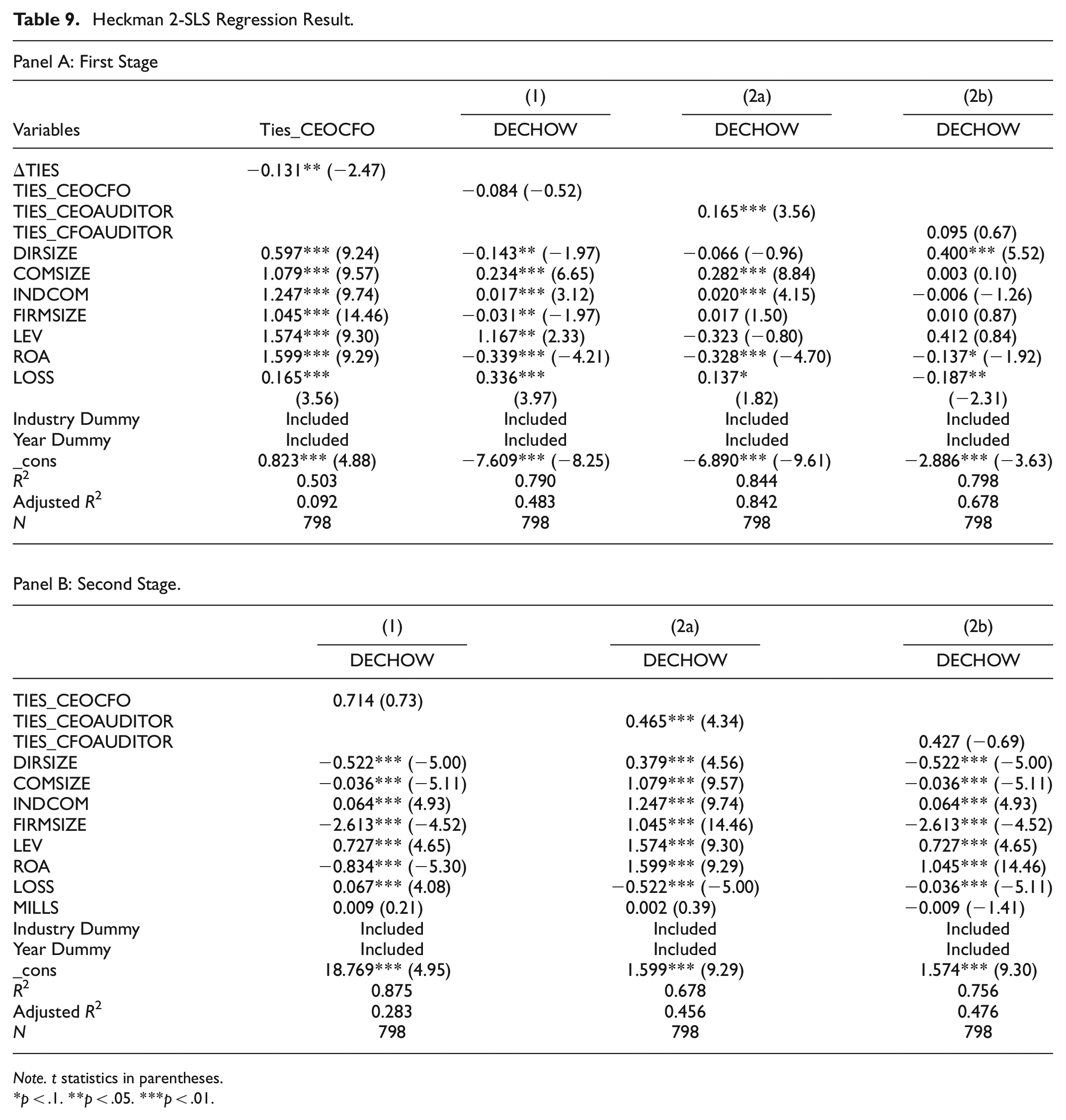

To address endogeneity problems caused by unobservable factors, researchers often use two-stage Heckman testing models. The two-stage Heckman (1979) model involves two equations: a selection equation and a regression equation. The second stage estimates the regression equation using a linear or non-linear model that accounts for the selection bias. Guan et al. (2016) proposed a two-stage Heckman test to address endogeneity problems in international business research. They argued that unobserved factors, such as cultural and institutional differences, can create selection bias in international business studies. By using the two-stage Heckman model, they were able to account for these unobserved factors and obtain more accurate estimates of the relationship between the independent and dependent variables. In the first stage, we tested factors outside the model by developing a new variable, TIES, as a free variable to see how it affects independent variables TIES_CEOCFO, TIES_CEOAUDITOR, and TIES_CFOAUDITOR. In the second phase, we re-estimated models 1, 2a, and 2b, including mills variables obtained from the first stage of testing. As a result, as shown in Table 9, it remains unchanged after the model is controlled by MILLS.

Heckman 2-SLS Regression Result.

Note. t statistics in parentheses.

p < .1. **p < .05. ***p < .01.

Additional Analysis

Additional tests were carried out using several treatments, firstly we divided the samples based on audit agencies auditing in the company and secondly, we tested based on a sample of companies that adopted a high-tech role and did not. Qin et al. (2021) shows that earnings management behavior is often reinforced by the ability of companies to adopt technology. In addition, it is possible that companies audited by top accounting firm have little chance of doing profit management compared to non-top accounting firm.

Sub Sample: Big 4 and Non-Big 4 Accounting Firm

Previous studies have found that earnings management behavior is more likely to occur when companies are audited by firms affiliated with top KAP (KAP refers to the accounting profession’s “knowledge, ability, and professionalism”) compared to non-top KAP (Fang et al., 2022; Harymawan, Anridho, et al., 2023; Ngelo et al., 2022). As a result, companies may feel that they need to meet or exceed earnings expectations to maintain their reputation and avoid negative consequences. The test results as shown in Table 10, remain and do not change, when the company is in the condition of being audited by KAP Big 4 and non-Big 4.

Additional Analysis School Ties Top Management and Auditor on Big 4 and non-Big 4.

Note. t statistics in parentheses.

p < .1. **p < .05. ***p < .01.

Sub Sample: High and Low Technology

Previous research has suggested that earnings management behavior is more prevalent in companies that operate in high-tech industries compared to those that do not (Bruynseels & Cardinaels, 2014; Kontesa et al., 2021). Therefore, it is important for high-tech companies to prioritize transparency and ethical behavior in their financial reporting practices, and for auditors to remain vigilant in detecting and preventing earnings management. This can help to maintain investor confidence and ensure the long-term sustainability and success of these companies. The test results are shown as in Table 11, fixed and show that in high-tech companies have differences with low-tech companies.

Regression Result School Ties Top Management and Auditor on High and Low Technology.

Note. t statistics in parentheses.

*p < .1. **p < .05. ***p < .01.

Conclusion

This study investigates the potential impact of school-ties between top management and auditors on earnings management. Surprisingly, our results indicate that the existence of school-ties between the CEO and Auditor is positively associated with higher levels of earnings management, as measured by the Dechow model. In contrast, there is no evidence of a significant relationship between school-ties of the CFO and CEO, or the CFO and Auditor, and earnings management (Alkebsee et al., 2022; Chiu et al., 2013; Cohen & Zarowin, 2010; Fang et al., 2022; Ramos et al., 2023). We speculate that companies with school-ties may be more likely to engage in fraudulent behavior and compromise the independence of professional work. Therefore, it is crucial for companies to maintain a balance between personal relationships and professional ethics. This study sheds light on the importance of promoting transparency and accountability in the corporate environment to prevent any potential misuse of personal ties. Companies can implement internal controls and ethical guidelines that prohibit the abuse of personal relationships for financial gain. Moreover, the role of auditors in ensuring the integrity of financial reporting should not be overlooked. Regulators should also consider strengthening regulations to uphold the independence of auditors and prevent any conflicts of interest that may emerge from personal relationships.

This study addresses a research gap by investigating the influence of school-ties on earnings management in Indonesian companies, an area that has received limited scholarly attention (Alkebsee et al., 2022; Ramos et al., 2023). Our findings indicate that the presence of school-ties between top management and auditors is associated with a heightened propensity for earnings management, thereby posing potential drawbacks for investors. Such practices can impede investors’ ability to comprehend and make well-informed decisions, resulting in reduced profitability and challenges in acquiring accurate information. Furthermore, the potential for sustained fraudulent practices cannot be disregarded under these circumstances. Consequently, we advise investors to exercise caution when relying on financial reports from companies involved in school-tie relationships. Additionally, we recommend that regulators adopt comprehensive policies to tackle the potential adverse impact of professional relationships on companies’ reporting practices. These policies may encompass stricter disclosure requirements, more rigorous auditing standards, and enhanced monitoring of financial reporting practices. Furthermore, companies should be encouraged to adopt codes of ethics that explicitly address the potential conflicts of interest that may arise from personal relationships among top managers and auditors. It is also important for companies to promote a culture of transparency and accountability. This can be achieved by creating an independent audit committee that is responsible for overseeing the financial reporting process and ensuring the accuracy and integrity of financial statements. The audit committee should be comprised of independent directors who are not affiliated with the company or its top managers.

Collectively, our paper expands the social network literature to the arena of earnings management. Our findings demonstrate that external social networks (CEO, CFO, and audit partner) are important determinants of earnings management, both based on accrual and real activity, and they complement our understanding of the important role played by social networks in facilitating information exchange and disseminating corporate practices across firms. Overall, we advance the involvement of various external parties at the intersection of social network and corporate earnings management literature, and we believe that evidence from this research can help standard setters and regulators better understand business practices and reporting behavior of companies in the social network context. Finally, we need to note that our study and findings are based on a sample of companies in Indonesia, which has a different governance structure than some countries. Social networks can fundamentally differ across different countries, and our findings may not apply to other countries. Readers should be cautious about the generalizability and implications of our research to other countries.

Footnotes

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.

Data Availability Statement

Data sharing not applicable to this article as no datasets were generated or analyzed during the current study.