Abstract

The study aims to examine the degree of Sustainable Digital Financial Inclusion (SDFI) of women workforce of Banking sector and IT sector. Banking sector imparts the knowledge of Digital Banking (DB), and IT sector develops DB applications. This research is motivated by the void left by previous researchers in understanding the determinants of Digital Banking Adoption Intention (DBAI) by female employees; as their digital inclusivity influences the DFI of common women. The study uses UTAUT2 model and PLS-SEM was applied on the 257 responses collected through structured questionnaires. Results show that female bankers have higher SDFI as compared to female IT employees due to mediation of DBAI between Drivers influencing DB and SDFI. The study contributes by clubbing the technological and financial sector. The study suggests the higher management of Banks and IT firms for recruitment and training of women personnel in DB adoption and DB application development, respectively.

Plain language summary

The study aims to find the degree the of SDFI of female employees of Indian banking sector and IT sector with the mediation of Digital Banking Adoption Intention (DBAI). Study finds that although both sector have equal contributing factors technology adoption of Digital Banking, female employees of Banking sector have higher SDFI mediated by DBAI.

Introduction

Mannan and Farhana (2023) identified Digital Banking (DB) as a potential gateway for Digital Financial Inclusion (DFI), which is not only restricted to financial sector, but spreading to all sectors of the society. Financial Institutions have been using Digital Financial Services (DFSs) for a long time to provide timely financial services. The rising demand for financial innovation has prompted other sectors to enter the market to make profits, raising the standard of DFSs (Irimia-Diéguez et al., 2023). The growing demand for innovative DFSs prompted TechFins to enter the financial sector. According to Koskipää (2022), TechFins are Information and Technology (IT) firms that provide financial services in addition to their core business, such as Amazon and Alibababa. According to Boissay et al. (2021) digital payments were the first DFSs offered by TechFins, which later expanded to credit, insurance, and investment products. To (2023) praised TechFins (IT firms) for changing the traditional financial services landscape and enhancing DFI by providing convenient, efficient, and personalized financial services, resulting in customer satisfaction and retention. While, M. K. Jain (2019) found traditional banks to have a competitive advantage over IT firms due to their extensive experience in financial services and customer trust in banking processes. According to Murad and Ahmad (2023) employees’ adjustment and adaptability to DB influences client’s technology adoption behavior. As significant number of banking tasks have been computerized, IT employees have become an integral part of the banking sector, where they are responsible for IT related tasks of Banks’ network, databases, and servers; protecting Banks’ privacy from cyberattacks (Mentoria, 2022). This explains the role of IT sector and Banking sector in providing DFSs, leading to DFI. However, a substantial amount of literature fails to investigate the importance of banks and IT firms in DFI. Authors were unable to locate any study that compared DFI levels among employees of both sectors.

Harasim (2021) asserted that the combination of Banks and TechFins is either competitive or coopetition. Cuadros-Solas et al. (2023) held a firm position on the competition between banks and TechFins, where the latter overtakes bank customers and reduces bank profitability. While Smyrnova (n.d.) supported the collaboration of Banks and TechFins, in which Banks hire the Financial Software Developer, who works on the development and updating of software used in the financial industry, ranging from credit software to financial fraud detection software. Boissay et al. (2021) advocated for collaboration between the IT and financial industries because technology firms have a greater reach to the unbanked population, greater access to customer data, and more capital. The efficiency of financial services improves with the assistance of technology firms and software or application developers, positively influencing the DFI, according to Boissay et al. (2021). The dual role of competition and collaboration of banks and IT firms (who serve as TechFins) necessitates an examination of their role in DFI in society.

People’s financial inclusion will remain inadequate unless banking services are widely available and used appropriately. Kaur and Ali (2021) investigated bank employees’ perceptions of DB adoption, claiming them to be the front-line representatives. Furthermore, employees’ adaptation to innovative financial technology enables them to provide customized services, which leads to customer satisfaction (Lydiana et al., 2023). When comparing female workforce participation in both sectors, Vidya (2023) stated that a report on “Business Responsibility and Sustainability Reporting” revealed that the IT sector had the highest female participation rate, followed by the financial sector. In contrast, career advancement in the IT sector in India is found to be lower than in the financial sector. Studies of Thakur et al. (2016); Chamboko et al. (2021); Tiwari et al. (2022) confirmed the critical role of female banking agents in spreading the need for financial inclusion to other women. Their research found that rural women are more comfortable in conducting financial transactions with female agents. Similarly, in the IT sector, Rossi and Harl (2023) advocated for greater female participation in the IT workforce in order to innovate a plethora of diverse products tailored to their intellect, thus satisfying the feminine digital needs. This illustrates the critical role of female employees in raising the DFI level in society by raising their own DFI level. However, the degree of DFI of female workforce in both sectors has remained unanswered. Their own inclination and adoption of DFSs via DB can encourage clients to use DB, ultimately improving DFI in society. Therefore, there is an urgent need to examine the DFI levels of female bank employees and female IT employees. Given the importance of both sectors in DFI, and the vitality of female workforce participation, authors conducted a women-specific sectoral comparison of DFI. Considering the research problem, the authors seek answers to the following research questions:

RQ1: How do technology adoption factors influence the Digital Banking Adoption Intention (DBAI) by female employees of both sectors?

RQ2: Further, how does the DBAI, as a mediator, influence Sustainable DFI (SDFI) of female personnel?

RQ3: Is there difference in SDFI level of female employees of both sectors due to difference in their DBAI?

This was accomplished by incorporating Perceived Innovativeness into the Extended version of the Unified Theory of Acceptance and Use of Technology (UTAUT2). “Digital India” was launched in 2015 with the goal of “Anytime-Anywhere Banking,” which became possible with phony smart phone and internet penetration. Demonetization of 2016 caused a severe shortage of physical currency, forcing Indians to use DB channels. Years later, the Covid-19 pandemic compelled individuals and organizations to use online banking. Hence, this study uses DB adoption as a parameter to examine the SDFI level of female workforce. Ikdal et al. (2017) explains that SDFI occurs when accounts are affordable to customers while also bringing profits to financial institutions. A structured questionnaire was used to collect data from female employees in both sectors. The difference in DB adoption by female employees in both sectors reflects their difference in SDFI level.

This is one of the earliest studies its kind to compare the DFI of two important and competitive industries. Also, the study conducts a comparative analysis of the DFI level of women employees in both sectors. The study is intended for bank management and IT organizations to assist their female employees in becoming more inclined to adopt and use DB channels, and motivating them to discuss the benefits of DB to other women. This could help Indian women improve their DFI. The study’s findings may aid the government in developing policies to encourage greater collaboration between banks and IT firms in the development of simple and beneficial financial applications.

A Review on Evolution of Technology Acceptance Models

Theory of Reasoned Action developed by Ajzen and Fishbein (1975) stated that a person’s attitude and the subjective norms imposed by society determine the person’s behavior and result in a specific action. Davis (1989) criticized it for being less effective in understanding a person’s behavior when using technology in an organization. This prompted Davis (1989) to develop the Technology Adoption Model, in which Perceived Ease of Use and Perceived Usefulness played a significant role in influencing a person’s technology adoption decision. Venkatesh and Davis (2000) extended the model by incorporating Subjective Norms, Social Influence, and Voluntariness to adopt technology, along with previous constructs. Later, Venkatesh et al. (2003) developed the UTAUT model initially emphasizing on extrinsic motivation of organizational users. Further, Venkatesh et al. (2012) developed UTAUT2 in response to the spread of IT from organizations to consumers, in which they incorporated three other constructs: Hedonic Motivation, Price Value, and Habit. According to Venkatesh et al. (2016), the UTAUT2 extensions produced a significant improvement in the variance explained in behavioral intention (56%–74%) and technology use (40%–52%).

To understand consumer technology adoption behavior, any single model is insufficient and would require more than one model (Manrai et al., 2021). Furthermore, Alkawsi et al. (2021) discovered that the UTAUT2 model’s constructs to be customer-oriented and having personalized touch in technology acceptance in an organizational context. Thus, the authors believe that the UTAUT2 model is more comprehensive in terms of social, psychological, and economic aspects of technology adoption.

UTAUT2 is used in this study to understand the adoption of DB technology among female employees, incorporating “Personal Innovativeness” (PI). Hilal and Varela-Neira (2022) defined PI as an individual’s proactive personality. They emphasized the importance of a person’s outward personality in technology adoption, as these individuals see Mobile Banking technology as an opportunity to improve individual and organizational performance. Their innovative behavior has a significant and positive impact on Behavioral Intention (BI) to adopt technology.

Review of Literature

Table 1 presents the results of studies focusing on SDFI and sustainable development. Table 1 has been framed in line with the methodology of Hazaea et al. (2023).

Sample of Studies on Sustainable Financial Inclusion/DFI.

Source. Created by the authors.

Research Model and Hypotheses Development

Figure 1 depicts the conceptual research model.

Conceptual Research model.

Performance Expectancy (PE)

“To what extent an employee perceives using the system will help him achieve employment efficiency benefits” is the operational definition given Amrouni et al. (2019) for PE. Yuliana and Aprianingsih (2022) linked the PE variable to Perceived Usefulness of Technology Adoption Model. In a study of Omani employees, Alraja et al. (2016) discovered that PE had a positive and significant relationship with BI to usee-government services, where employee performance is related to the growth and productivity of the organization. Gupta et al. (2023) demonstrated a positive relationship between PE and technology purchasing; the greater the benefits received from using the technology, the greater the desire to purchase and use the technology.

According to Orser and Riding (2018) women business owners lack the ability to use IT for financial decision-making, resulting in loss of commercial opportunities. Regarding FinTech, Kurniasari et al. (2023) emphasized the positive influence of PE on FinTech service adoption in private organizations. Furthermore, in the case of Block-chain technology used in the banking sector, employees regard their PE as a major determinant of adopting the relevant technology (Jena, 2022).

H1a: PE is the Driver influencing DBAI.

H1b: There is a significant difference in PE among women employees of Banking sector and IT sector.

Effort Expectancy (EE)

Amrouni et al. (2019) defined EE as “the level of ease with using the system.” Consumers use apps and websites with simple designs. Also, they choose apps with clear navigation icons from a pool of apps that perform similar tasks (Shaw & Sergueeva, 2019). EE is a significant factor in technology adoption because consumers prefer to use simple interfaces to avoid human errors that result in monetary loss (Hamid et al., 2022). In Saudi Arabia, Bajunaied et al. (2023) discovered a significant positive impact of EE on customer BI to adopt FinTech.

Manrai et al. (2021) explained the positive impact of EE on technology adoption by women in India’s semi-urban areas by stating that women may be more likely to purchase technology if the interface of application software is clear and requires fewer steps to complete. Bastari et al. (2020) found that user-friendly application websites increased employee trust in technology adoption. In the case of FinTech, ease of use is demonstrated when customers do not need to learn additional skills to use the FinTech (Tun-Pin et al., 2019).

H2a: EE is the Driver influencing DBAI.

H2b: There is a significant difference in EE among women employees of Banking sector and IT sector.

Social Influence (SI)

Venkatesh et al. (2003) used the term “SI,” referring to the effect of one’s close relationships’ views on technology adoption and usage. According to Gharaibeh et al. (2020), social circles are complex relationships of relatives, friends, and colleagues that have either a positive or negative effect on the intention to adopt technology. According to Shaw and Sergueeva (2019), SI is the desire to impress others by purchasing the latest technology, even though the use of technology must be conducted alone and the benefit of its use is enjoyed solely. According to a study conducted by R. Jain et al. (2022) on employees of Social Development Organizations, adoption of technology by one member of the organization influences the adoption intention of others. SI was credited by Irimia-Diéguez et al. (2023) as the creator of a favorable or unfavorable attitude toward FinTech adoption, which leads to adoption intention.

Nath et al. (2013) upheld the dominant role of superiors in positive IT communication in Indian banks to achieve organizational goals. Kumar and Ayedee (2021) endorsed the role of business owners or managers as a motivator for employees to adopt technology, as employees look up to the seniors for their perspectives on technology. A study on women-owned Small and Medium Enterprises by Alam et al. (2022) discovered that female leaders require more social media to expand their business, as they rely heavily on social relationship management to sustain their business.

H3a: SI is the Driver influencing DBAI.

H3b: There is a significant difference in SI among women employees of Banking sector and IT sector.

Facilitating Conditions (FCs)

FCs were defined by Nath et al. (2013) as the technological facility or prevalence of technical infrastructure to support the use of Information Systems. Internet access, mobile device access, and appropriate file sizes are examples of viable infrastructure (Ambarwati et al., 2020). Poor network connectivity or frequent errors on mobile banking systems may reduce consumer interest in DB technology (Marpaung et al., 2021). Expert advice, easy internet access, and the availability of smart devices are the factors that drive FCs to adopt FinTech services (Bouteraa et al., 2023).

According to Garg (2022), women are more considerate of FCs because they place more emphasis on external factors when adopting new technology. Regarding Block-chain technology, Mansoor et al. (2023) asserted that FCs such as banking infrastructure, regulatory framework, and compliance standards have a positive impact on bankers’ intention to use and subsequent actual use of Block-chain technology for remittances. According to Bajunaied et al. (2023), FCs have a significant positive impact on BI’s adoption of FinTech.

H4a: FCs is the Driver influencing DBAI.

H4b: There is a significant difference in FCs among women employees of Banking sector and IT sector.

Hedonic Motivation (HM)

According to Shaw and Sergueeva (2019), consumers use apps with simple and enjoyable user interfaces. According to Moorthy et al. (2020), consumers use Mobile Banking apps more frequently if their designs are unique, appealing, and enjoyable to use. Entertaining features of Mobile Banking apps have a positive and long-lasting effect on consumer minds, leading to a significant and positive effect on BI to adopt DB (Marpaung et al., 2021). In the case of employees, Nguyen and Malik (2022) defined extrinsic motivation as the tangible rewards whereas intrinsic motivation is the enjoyment or sense of fulfilment gained from using technology. Ouattara (2017) found that HM has a significant and positive impact on the adoption of IT in small and medium-sized businesses in Ontario. Wibowo and Sobari (2023) claimed in a study on Quick Response Code Indonesian Standard (QRIS) services; one of the mobile banking services, that HM has a significant positive effect on QRIS because users feel happy while using the technology’s simple features.

Ling and Yazdanifard (2014) confirm women as hedonic purchasers, that is people who buy technology because they have a social attachment to it. They discovered that women behave happily when purchasing any online product or technology. Bajaj et al. (2023) confirmed this by stating that women attach emotional values to technology and are risk avoiders. They buy technology based on information availability, and convenience.

H5a: HM is the Driver influencing DBAI.

H5b: There is a significant difference in HM among women employees of Banking sector and IT sector.

Price

The price paid to purchase technology (cost of the device, data, and other service charges) has a significant impact on the intention to adopt technology. Gharaibeh et al. (2020) stated that a user adopts technology when the benefits received outweigh the cost. This could be explained by the belief that there is a negative relationship between the device’s price and BI (Al-Saedi et al., 2020). According to Nguyen and Malik (2022), the cost of technology from the perspective of employees is the time and effort required to use technology. Almaiah et al. (2022) claimed a significant effect of price on BI to adopt Internet Banking.

DiCaprio et al. (2017) attributed less FinTech adoption to a lack of financial identification, financial dependence on male members, less financial knowledge, and financial risk aversion among women-led firms. According to Ameen et al. (2018), women consider smartphone prices to be higher because they rely financially on men. Price reductions would encourage women to adopt and use mobile technology for financial services. According to Lee et al. (2022), even though DFSs are less expensive, women perceive it to be expensive and prefer cash over DB.

H6a: Price is the Driver influencing DBAI.

H6b: There is a significant difference in Price among women employees of Banking sector and IT sector.

Habit

Ambarwati et al. (2020) defined “habit” as a user’s automatic behavior based on prior learning. When a consumer uses DB for a longer period and for multiple times, it develops a favorable opinion and positive behavior toward DB, eventually leading to a favorable habit to use DB (Galhena & Gunawardena, 2022). According to Chang et al. (2019), increased and repetitive use of technology develops a habit that replaces EE, resulting in easy accessing of internet and completing online transactions. This leads to increased technology usage and better technological experience. Qamar and Qureshi (2022) discovered a significant and positive impact of Habit on the continued intention to use mobile banking among Pakistani mobile banking users.

Yen and Wu (2016) discovered Habit to be a significant predictor of BI to use Mobile Financial Services in their study of Taiwan women due to the easy communication features of mobile devices. Özsungur (2019) discovered that Habit has a significant and positive effect on BI to use technology among Turkish women entrepreneurs. Manrai et al. (2022) concluded that Indian women have a habit of using cash instead of FinTech payment services. FinTech adoption may break this cash-oriented habit by encouraging women to explore other financial services, eventually leading to a cashless habit.

H7a: Habit is the Driver influencing DBAI.

H7b: There is a significant difference in Habit among women employees of Banking sector and IT sector.

Personal Innovativeness (PI)

Patil et al. (2020) defined PI as an individual’s “novelty-seeking tendencies” or eagerness to “try something new.” Considering FinTech Services, Setiawan et al. (2021) define PI as one’s own initiative to use FinTech services. Wirani et al. (2022) asserted a positive relationship between PI and BI in adopting FinTech, where users with an innovative personality are the early adopters of the services. According to Bouteraa et al. (2023), the higher an individual’s level of inventiveness, the more positive their attitude toward FinTech services. Solarz and Adamek (2022) asserted a positive relationship between PI and DBAI in the case of DB (a type of FinTech). This was expanded by Pea-Assounga and Yao (2021), who claimed that PI has a significant influence on bank employee performance, which determines the bank’s overall efficiency. Biscione et al. (2021) concluded that female-led firms have a higher likelihood of introducing technological innovation. They claimed that female managers have a greater influence on a company’s technological innovation. However, Yuan and Ma (2022) discovered that female employees in IT companies are less innovative due to their lower acceptance in the technological sector. They claimed that female employees’ PI attitudes are influenced by social relationships and the assistance of coworkers in innovative tasks.

H8a: PI is the Driver influencing DBAI.

H8b: There is a significant difference in PI among women employees of Banking sector and IT sector.

Digital Banking Penetration (DBP) and Digital Banking Usage (DBU)

Sarma and Pais (2011) explained that internet access (penetration) as an important factor leading to DFI. Thulani et al. (2014), Abor et al. (2018), Ghosh (2020) concluded that usage of mobile is more significant in DFI. Lenka and Barik (2018) established the fact that people use mobile devices more for financial transactions. High correlation is seen in mobile and internet use reflecting a high combined contribution to the model of DFI. Both the mobile usage and internet penetration when taken separately as independent variables show a positive impact on FI. Thulani et al. (2014) concluded that this positive effect is less visible in female headed houses. Guerra-Leal et al. (2021) in Mexico; Antonijević et al. (2022) in a survey of 144 nations, claimed a lesser share of women in access of DB. Also, in the usage of DB, women were the poor performers claiming to have lesser DFI level. Antonijević et al. (2022) claimed that women are more comfortable to make cash transactions, thereby decreasing their DFI level.

H9a: DBP has a significant effect on DBAI.

H9b: There is a significant difference in DBP among women employees of Banking sector and IT sector.

H10a: DBU has a significant effect on DBAI.

H10b: There is a significant difference in DBU among women employees of Banking sector and IT sector.

Determinants of Sustainable DFI

Pazarbasioglu et al. (2020) identified three stages of DFSs development: increased access to transaction accounts, increased utilization of transaction accounts for digital payments, and improved DFSs by moving beyond digital payments. Increased access to DFSs allows for increased consumption and investment, resulting in economic growth and Asia-Pacific Economic Cooperation [APEC] (2022). Augustine (2023) elaborated that increased use of DFSs improves DFI in addition to providing security for digital platforms.

According to Alkhazaleh and Haddad (2021), Customer Satisfaction (CS) has a direct and positive impact on customer commitment to FinTech usage. Furthermore, Uddin and Nasrin (2023) asserted that CS has a significant and positive influence on Continued Intention to Use Mobile Financial Services. They claimed that CS is more about technology performance than about expectations. CS encourages customers to use technology indefinitely in order to receive better services for a longer period of time, which leads to SDFI. Bhat and Darzi (2014) discovered that females are oblivious to satisfaction derived from DFSs due to their lack of confidence in dealing with complaints.

H11a: Future Use of DB leads to SDFI.

H11b: There is a significant difference in Future Use of DB among women employees of Banking sector and IT sector.

H12a: Frequent Use of DB leads to SDFI.

H12b: There is a significant difference in Frequency of using DB among women employees of Banking sector and IT sector.

H13a: Increased Use of DB leads to SDFI.

H13b: There is a significant difference in Increment in usage of DB among women employees of Banking sector and IT sector.

H14a: CS derived from DB leads to SDFI.

H14b: There is a significant difference in CS among women employees of Banking sector and IT sector.

Hypotheses Development Linking Drivers with DBAI and SDFI

Daka and Phiri (2019) found PE, EE, FCs as significant Drivers of e-banking adoption intention. Hassan et al. (2022) in a study covering Bangladesh also found UTAUT 2 factors to be significant Drivers of on mobile FinTech adoption intention. Considering the women employees in architecture field, Mittal and Bhandari (2021) validated the UTAUT2 Drivers to be significant for technology adoption. Setiawan et al. (2021) also found the UTAUT2 factors to be significant in FinTech adoption intention among Indonesian women.

H15a: Drivers of DB have significant effect on DBAI.

H15b: There is a significant difference in relation of Drivers and DBAI among women employees of Banking sector and IT sector.

Ojo (2022) emphasized on fifth Sustainable Development Goals (SDG 5) that relates to gender equality, where SDG 5a, relates to implementing certain rights over land ownership, access to financial services, etc., and SDG5b relates to promoting ICT adoption and usage among women. Pal et al. (2023) explained Sustainability as the continued intention to use mobile payment technology, which leads to long term FI termed as SDFI.

H16a: DBAI have significant effect on SDFI.

H16b: There is a significant difference in relation of DBAI and SDFI among women employees of Banking sector and IT sector.

H17a: Drivers to DB have significant effect on SDFI.

H17b: There is a significant difference in relation of Drivers and SDFI among women employees of Banking sector and IT sector.

In Ghana, Odei-Appiah et al. (2022), supported the significant effect of adoption intention of FinTech on Actual Usage and thereby significant effect on DFI. Neelam and Bhattacharya (2023) in a study on urban poor households of India found that UTAUT2 factors had a significant effect on adoption intention of mobile finance, where intention was a mediator in mobile finance usage, indicating a significant mediation role of intention on DFI. According to Asif et al. (2023), intention to use FinTech products was the prominent cause of FI of Rural India.

H18a: DBAI acts as a mediating variable between Drivers and SDFI.

H18b: There is a significant difference among women employees of Banking sector and IT sector regarding impact of Drivers on SDFI with the mediation of DBAI.

For clear understanding, the proposed relations of all the hypotheses of the study have been depicted in Table 2.

Proposed Relation.

Source. The authors’ compilation.

Research Methodology

Measurement Scales

The study follows a cross-sectional research design. The research model consists of eight latent constructs to measure the exogenous latent variable “DBAI” ultimately impacting the dependent variable SDFI. DBP and DBU measure the degree of DBAI of respondents. Since, the aim of study has been to examine and compare the DFI level of women personnel of IT sector and Banking sector, thus women employees of both sectors were targeted.

Authors divided the questionnaire into three sections (Appendix A). First section focused on respondents’ demographic information, comprising of age, income, and education. Second section comprises of constructs of UTAUT2 that demanded answers on the 5-point Likert scale, ranging from Strongly Disagree (1) to Strongly Agree (5). Each construct was accompanied by a brief description to make it easy for the respondents to understand the constructs. The questionnaire was drafted in English. The constructs are as follows: PE (three items) and EE (three items) derived from Davis (1989). PI (three items) adopted from Agarwal and Prasad (1998). SI (three items), FC (four items), HM (three items), Habit (three items), and Price (three items) derived from Venkatesh et al. (2012). DBAI as related to BI (three items) adopted from Ajzen and Fishbein (1975).

Third section measured the DBAI was measured through DBP (three items) and DBU (five items) derived from Ravikumar et al. (2019), and SDFI. SDFI through constructs: Future Use of DB (one item) adopted from Sharif and Raza (2017); Frequent use of DB (one item) adopted from Tandon et al. (2016); Increased use of DB (one item) adopted from Adapa and Roy (2017); and CS (seven items) adopted from Zouari and Addelhedi (2021).

Sample and Data Collection

Women employees of three public sector Banks: State Bank of India (SBI), Punjab National Bank (PNB), Bank of Baroda, and three private sector Banks: Axis Bank, HDFC Bank, and ICICI Bank, made the sample as the Banks were selected according to market capitalization (April, 2023). Similarly, women employees of the IT firms: TCS, Infosys, Wipro, HCL Technologies, Tech Mahindra, and L&T Infotech, were selected as these IT companies were ranked topmost according to market capitalization (April, 2023). These top IT firms are not only in the software development services but are also participating DFSs. TCS has it renowned TCSBaNCS software used by SBI for retail banking. Infosys developed its software FINACLE used by ICICI Bank, Axis Bank, HDFC Bank. Wipro provides Core Banking Solution for one of the Regional Rural Bank in India. L&T Infotech provides L&T Finance; HCL provides HCL Finance; Tech Mahindra provides Mahindra Finance.

Pilot study was conducted to check for face validity, content validity, and reliability of the questionnaire. After recommended changes, the questionnaire was refined and distributed among women workforce of both sectors. A random sample selection was made. Structured questionnaires were distributed to 300 women personnel (150 each from both sectors); out of which the authors received 257 completed questionnaires, yielding a response rate of 85.67%. One hundred and thirty women employees belonged to IT sector (50.58%) and 127 from Banking sector (49.42%). The collected responses were coded and tested for reliability in SPSS version 21 where data was found to be highly reliable with Cronbach’s alpha score of .901. Table 3 displays the demographic profile of the respondents. Majority of women from both sectors belong to age group of 26 to 40 years, earning less than 0.5 million per annum, and majority of women belong have completed their post-graduation.

Demographic Profile of Respondents.

Source. The authors’ compilation.

Data Analysis

For data analysis Partial Least Squares Structural Equation Modelling (PLS-SEM) has been applied. SEM is applied to study the relationship between multiple variables, as this technique helps to understand the cause-and-effect relation between multiple independent variables and dependent variables (Hu et al., 2019).

Assessment of Measurement Model

Measurement model is assessed through Internal Consistency, Convergent validity, and Discriminant Validity (Alkawsi et al., 2021).

Internal Consistency is a reliability check to ensure that all the questionnaire items measure their respective constructs which they are supposed to measure. Table 4 displays that Cronbach’s alpha and CR of women employees of both sectors if above .7 and .8 respectively, implying that data has good internal consistency. Average Variance Extracted (AVE) measures Convergent Validity assessing the degree to which constructs are different from each other in the instrument. AVE values of all constructs in Table 2 are higher than 0.50 reflecting more than 50% of variations in the respective constructs were because of their indicators (Fornell & Larcker, 1981). Square root of AVE in Table 4 represents discriminant validity implying that all constructs are different from each other, having values above .50.

Reliability and Validity Score.

Source. Created by the authors.

Convergent validity is represented through outer loadings of the constructs, as depicted in Table 5, where Outer loadings of more than 0.70 suggest satisfactory indicator reliability and is preferred. However, as per Hulland (1999); Hair et al. (2019), outer loadings of 0.4 or higher is acceptable. As these two factors (PI and SI) are important, so we have retained them for analysis. In Table 5 maximum indicators have outer loadings of above 0.70 except SI and Price, explaining that they contribute less in the measurement of Drivers influencing DB of female employees of both sectors.

Outer Loadings.

Source. Created by the authors.

According to Fornell-Larcker criteria, the square root of AVE, as a measure of Discriminant validity, should be greater than the correlation of latent constructs, in Table 6.

Fornell-Larcker Criteria.

Source. Created by the authors.

Assessment of Structural Model

R-square value of each endogenous latent variable assesses the structural model by estimating the relationship between independent variable and dependent variable. According to Table 7, R-square of 0.700 implies that Drivers of DB cause 70% variation in DBAI for female employees of Banks as compared to 0.445 that is 45.5% variation in DBAI for female employees of IT sector. Similarly, DBAI causes 76.7% variation in SDFI of female bank employees as compared to female IT employees (61.2%). Adjusted R-square values also highlight the same situation.

R Square and Adjusted R Square.

Source. Created by the authors.

Table 8 presents the f-square values which implies the change in R-square value when an exogenous variable is removed. The threshold limits of f-square effect size set by Cohen (2013): ≥0.02 is small; ≥0.15 is medium; ≥0.35 is large. Removal of DBAI and Drivers has less effect on SDFI in case of bank employees.

F Square Values.

Source. Created by the authors.

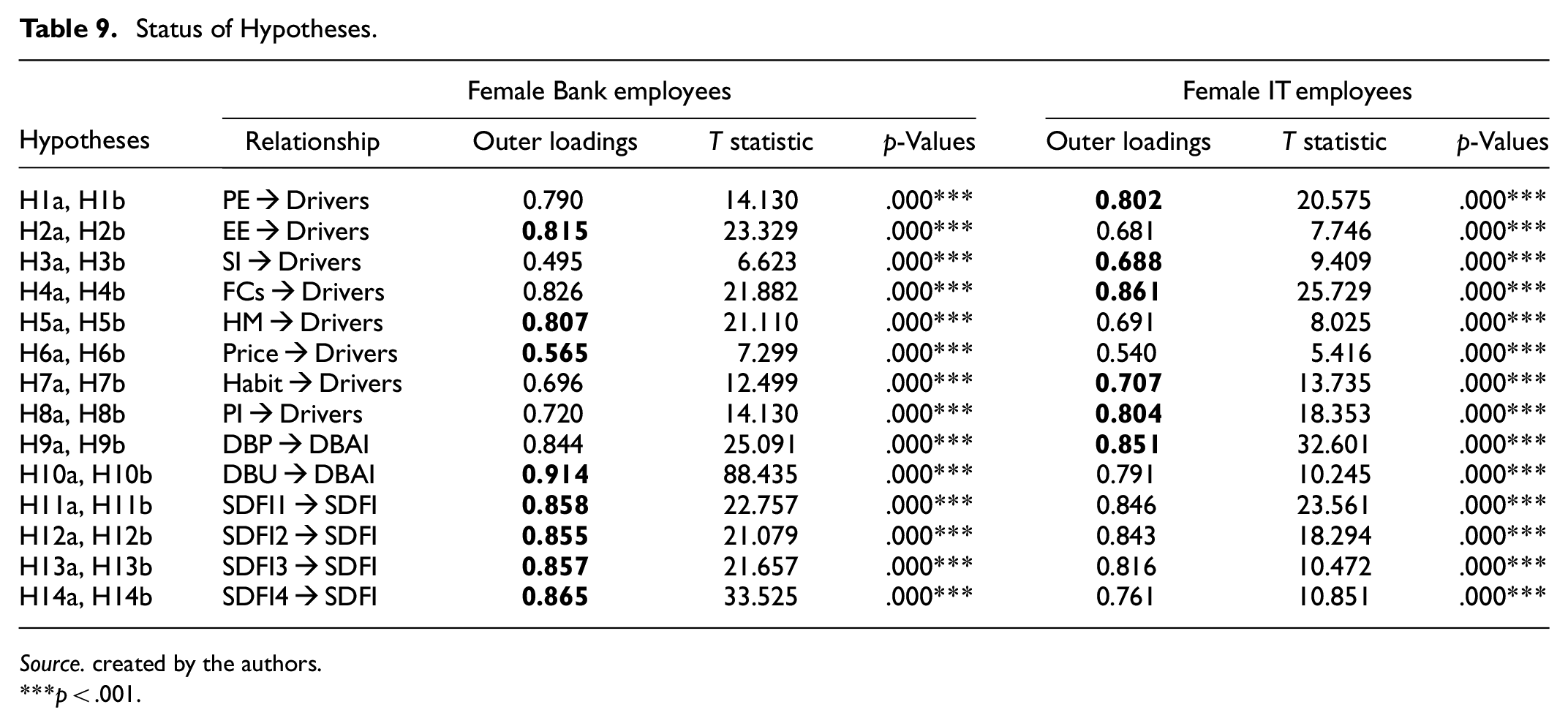

Hypotheses Testing

Since t-statistic and p-values of all hypothetical relations are more than 1.96 and 0.05 respectively in Table 9, thus all the hypotheses are significant. The higher loadings have been reflected in bold. All relations are significant for female workforce of Banking sector and IT sector, implying that all UTAUT2 factors have a significant role as Drivers of DB adoption. Further, outer loadings would be used to gauge the primarily contributing Drivers of DB adoption. Four factors in both sectors: Banking sector (EE, HM, Price, and PI), and IT sector (PE, SI, FCs, and Habit) have major contribution as Drivers influencing DB adoption. DBP has higher contribution in DBAI in IT sector, while DBU is found to be higher in Banking sector. But, all the variables of SDFI have higher contributions in women employees of Banking sector. Table 10 provides for path coefficients of female employees of both sectors. It shows that in the absence of mediating variable (DBAI), SDFI of female employees of Banking sector is higher than those of IT sector. Also, with the mediation of DBAI, SDFI of female bank employees (0.851) is higher than those of IT sector (0.758). this implies that women employees of Indian Banks take the lead as compared to women employed in IT firms.

Status of Hypotheses.

Source. created by the authors.

p < .001.

Mediation Effect of Paths.

Source. created by the authors.

***p < .001.

The above results of the study are depicted through resultant model of PLS-SEM (Figure 2) which provided a pictorial comparison of their SDFI levels. Figure 2 presents the comparative results of female employees of Banking sector and IT sector.

Resultant model.

Discussion

Owing to significant role of Banking sector and IT sector in DFI, and in view of scarcity of research on examining the role of both sectors in DFI; motivated authors to make a sectoral comparison in context of SDFI. As female employees play a major role in influencing other women to adopt DB channels and enhance their SDFI level, thus authors aimed to examine the degree of SDFI of employees themselves through mediation of DBAI. UTAUT2 model was applied on 257 responses (130 from banking sector and 127 from IT sector). Results found that although DBAI significantly mediates the relation of Drivers and SDFI but it has complementary mediation for female workforce of both sectors. Explanatory power of the model improved by including DBAI as a mediating variable to 76.7% (female bank employees) and 61.2% (female IT employees). These open avenues to examine the mediation of such behavior-related variables between technology adoption and SDFI.

Findings of the study concluded that PE is the Driver influencing DBAI for both set of employees, supporting H1a. This is line with the studies of Alraja et al. (2016); Kurniasari et al. (2023). The statistics for female bank employees (β = .790, p = .000) and for Female IT employees (β = .802, p = .000) vary. This shows that PE has a higher contribution as Drivers of DBAI in case of female IT employees, indicating the significant difference in PE among female employees of both sectors; thereby accepting H1b. Despite the higher experience on providing financial services to customers through banking software’s, female bankers have less PE. It is contrary to result of Jena (2022). Higher PE among IT professionals has been supported by Tiwari et al. (2023) by stating that IT employees need to keep abreast their skills for technological achievement, job satisfaction in the IT sector.

The results of the study accept EE as the Driver influencing DBAI (supporting H2a) finding its support from Bastari et al. (2020); Bajunaied et al. (2023). Statistics of female bank employees (β = .815, p = .000) and female IT employees (β = .681, p = .000) vary. The statistics supports H2b where EE as Driver of DBAI is higher in case of female bank employees. This is supported by Jena (2022) who stated that bank employees perceive effortlessness in using technology to avoid risk.

SI has a significant impact as Driver of DB on DBAI for both set of respondents, accepting H3a. The positive and significant effect of SI on technology adoption has been supported by Kumar and Ayedee (2021). Statistics for female bank employees (β = .495, p = .000) and female IT employees (β = .688, p = .000) vary. The effect of SI on DBAI is higher in case of female IT employees in comparison to female bankers, supporting H3b. This can be gauged from the result of Zhang et al. (2015) who supported the social interaction among team members of IT sector, and considered it to be important for their project’s success. Mergener and Trübner (2022) stated that employees living with their families feel less isolated. Nestway (2021) mentioned the cities of Mumbai, Delhi, and Bangalore as the most preferred cities for software engineers. This might be the reason of higher loading of SI in case of female IT professionals as living far from their families, render them to believe peers and seniors for latest technology adoption.

Findings of the study support H4a claiming that FCs referring to institutional infrastructure to support the DBAI has significant effect for female employees of both sectors. However, the statistics of FCs among female bank employees (β = .826, p = .000) and female IT employees (β = .861, p = .000) differ. This depicts that FCs contribution in technology adoption is higher among female IT employees as compared to female bank employees, accepting H4b. This could be due to the lack of bank’s IT infrastructure to support DB. ETBFSI Research (2023) held the frequent server issues and technical glitches as dominant reason for low digital infrastructure of banks. It occurs when there is high volume of customers transactions and the subsequent failure of IT infrastructure after reaching its capacity. Thus, technology adoption requires good digital back-up which is found to be poor in Banks, causing lower FCs’ contribution in DBAI in female bank employees.

Study finds HM to be a significant driver influencing DBAI for employees of both sectors, thereby accepting H5a. We find its evidence from studies of Nguyen and Malik (2022); Marpaung et al. (2021). But, the statistics of female bank employees (β = .807, p = .000) and female IT employees (β = .691, p = .000) differ. This depicts that contribution of HM on DBAI is lot higher among bank staff, leading to acceptance of H5b. This could be explained by the role of banks in generating trust among public to use DFSs by providing good performance (Afif et al., 2023). They explained banks to function and perform well to survive as intermediary between economy and public.

The study supports H6a, indicating Price to be a significant driver influencing DBAI for employees of both sectors. This is line with the studies of DiCaprio et al. (2017); Nguyen and Malik (2022). The effect of Price for DBAI is found to be higher among female bank employees as compared to female IT employees. The loadings have minimal difference between female workforce of both sectors where bankers (β = .565, p = .000) and IT professionals (β = .540, p = .000) are different. This accepts H6b. this finds support from Khullar (2021) who reported that although employees of IT firms gradually earn well with the passage of time, but bank employees receive perks of housing and allowances, irrespective of low salary. This might be the reason that female employees of Banks find price of DB to have a significant effect on their DBAI as salary is required to pay for data and not the perks.

Study finds Habit to have significant effect as driver on DBAI for employees of both sectors, supporting H7a. This is line with the studies of Galhena and Gunawardena (2022); Qamar and Qureshi (2022). But the different statistics of female bank employees (β = .696, p = .000) and female IT employees (β = .707, p = .000) makes H7b acceptable, depicting that Habit has a lot higher contribution in case of IT employees than bankers. This was supported by Hamid et al. (2022) who stated that the more the users adopt mobile banking applications, the more the software developers need to improve the applications’ interface to provide facilities to customers. Thus, Habit to use DB has higher role in case IT employees as they are the developers of the apps that lets them use the apps instantly and at-ease, which is not in case of bankers as they must learn the apps themselves and then communicate further to customers.

PI is also found to be significant predictor of DBAI for both set of respondents, accepting H8a finding its support from studies of Yuan and Ma (2022); Wirani et al. (2022). However, there is significant difference in PI among female bank employees (β = .720, p = .000) and female IT employees, (β = .804, p = .000) being its loading much higher in case female IT employees. This accepts H8b that claims significant difference in PI among both set of respondents. Gulshan and Singh (2022) attributed the need of innovativeness among IT employees as their work profile demands repetition of tasks of testing, production support, and maintenance, resulting in monotonous routine of employees. As the jobs of IT are creativity-demanding and stressful, thus IT professionals continuously strive to enhance their innovation level.

To assess the difference in DBAI, two parameters: DBP and DBU were examined. The results show that DBP and DBU have significant effect on DBAI of employees of both sectors, leading to acceptance of H9a, and H10a. The results show that DBP is higher among IT employees while DBU is higher among Bank employees. This accepts H9b, and H10b as the statistics in case of DBP of female banks employees (β = .844, p = .000) differ from that of female IT employees (β = .851, p = .000). The results of DBU among bank staff (β = .914, p = .000) is different from that of IT staff (β = .791, p = .000). This can be interpreted from the higher contribution of loadings of Usage in case of bank employees and that of penetration in IT sector. Female bank employees have been reported to have higher Usage of DB channels due to higher loading values of EE (Al Tarawneh et al., 2023), HM (Marpaung et al., 2021), Price (Alsheikh & Bojei, 2012), and Personal Innovativeness (Bouteraa et al., 2023). Higher DBP in case of IT employees can be due to contribution of factors in penetration of DB channels, such as, PE (Osman and Leng, 2020), SI (Kumar & Ayedee, 2021), FCs (Bouteraa et al., 2023), and Habit (Galhena & Gunawardena, 2022).

The four indicators of SDFI: Future Use, Frequent Use, Increased Use, and CS represented the continued intention to use DB and CS received from using DB. Research found that all four constructs have significant effect on SDFI for female professionals of both sectors, accepting H11a, H12a, H13a, H14a. We find its support from Pazarbasioglu et al. (2020); Augustine (2023); Alkhazaleh and Haddad (2021); Uddin and Nasrin (2023). Also, the beta coefficients (β) of all four indicators of SDFI are higher in female bank employees (0.858; 0.855; 0.857; 0.865) as compared to IT employees (0.846; 0.843; 0.816; 0.761), accepting H11b, H12b, H13b, H14b. This signifies that higher is the continued intention and satisfaction derived by female workforces from DB, higher will be their influence on other women to engage in DB modes.

Results present significant effect of Drivers on DBAI (accepting H15a), significant effect of DBAI on SDFI (accepting H16a), significant effect of Drivers on SDFI (accepting H17a) for female employees of both sectors. The results are in line with studies of Hassan et al. (2022); Mittal, and Bhandari (2021); Pal et al. (2023). However, the statistics of Drivers influencing DBAI (bank employees:0.837, IT employees:0.667); DBAI influencing SDFI (bank employees:0.380, IT employees:0.258); Drivers influencing SDFI (bank employees:0.533, IT employees:0.586) are different. This supports H15b, H16b, H17b. This implies that Drivers have a significant positive influence over DBAI, and SDFI. Also, DBAI have positive significant influence on SDFI for employees of both sectors. Further, the mediation analysis shows that DBAI significantly mediates the relation between Drivers and SDFI for both set of respondents, accepting H18a. But, the effect of Drivers on SDFI are significantly reduced due to mediation of DBAI for female bank employees (0.318) and female IT employees (0.172). This implies that DBAI has partially mediating effect on relation between Drivers of Db adoption and SDFI. Although the mediation effect is higher among bank employees as compared to IT sector, claiming significant difference in mediation result in both sectors, accepting H18b. This explains that adoption intention acts a strong mediator in explaining SDFI level of bank employees, in line with studies of Kaddumi et al. (2023) who held FinTech adoption intention having significant effect on banks profitability level.

Implications

Theoretical Implications

Few researchers have applied UTAUT2 on employees of an organization to understand their intention towards technology adoption. The study contributes by applying UTAUT2 on female employees of Indian banking sector and IT sector, contributing to understanding the women’s perception of technology adoption. The study firstly adds to literature by comparing the SDFI level of female employees of these two important and competitive sectors, and merging the areas of technology adoption intention and financial inclusion, which in the view of authors has been a limitation in the previous studies. The study finds that female employees of banking sector lead in SDFI than their IT counterparts. Three constructs: EE, HM, and Price have higher contribution as Drivers of DB adoption in DBAI in case of female bank employees. While, five constructs viz., PE, SI, Habit, FCs, and PI have higher contribution in case of female IT employees. Despite this, SDFI of female bankers is more than IT employees owing to higher loadings of variables of SDFI.

Managerial Implications

DBAI significantly mediates the relation between Drivers to DB adoption and SDFI for female employees of both sectors: banking sector and IT sector. But the mediation effect is higher among female bank employees. Bank management need to understand that though the technology adoption factors significantly affect SDFI but their intention to adopt DB has a higher effect on their SDFI level. This should be considered by the bank management to provide specific training to female employees regarding multiple digital platforms so they can further cater to women customers. This step may enhance DFI level of women in the nation. Similarly, the higher management of IT firms where women employees make a significant proportion of their employees database, should recruit, and train more women in the application development roles. This will help to develop female friendly application and websites.

Limitations and Directions for Future Research

Though the study contributes to existing knowledge of DFI, its limitation may open avenues for future research work.

The study lacks in geographical outreach and is undertaken in Northern India. Thus, the study may not be generalizable, although it can be inferred that North India represents India, in terms of the IT and Banks considered in the current study, hence the study may be valid for India as a whole. However, future researchers can focus on IT companies and Banks from other regions too to increase applicability. Also, the study participants may be increased. The study employs cross sectional research design, but motivates future researchers to follow longitudinal study to gauge the changing behavior of employees after technology adoption and thereby change in their DFI level. The construct of PI may be enhanced in future studies by incorporating dimensions of innovativeness. As the study provides with a complementary mediation of variables, thus more factors to UTAUT2 model may be inculcated. This study can be used in future to analyze the Gender Digital Divide existing among organizations. The study in future can be extended to actual usage of DB and be restricted to intention.

Conclusion

Extensive studies have focused on DB adoption and its effect on DFI among public. Lately, few studies contributed by examining the perception of employees of Indian financial sector on technology adoption. But authors failed to find any study on technology adoption among employees of IT employees. Banks and IT firms have enormously contributed to DFI among public. Bank employees have framed policies to enhance DFI while IT employees have developed softwares to engage public in DB transactions. But authors did not find any study examining the adoption of DB among employees of these two important and competitive sectors that promote DFI in the nation. Also, authors found this research gap as an opportunity to gauge into female employees’ DFI level. Understanding women’s perception may help to frame policies to render DB services such as to raise DFI level of other women.

To achieve this objective, authors used UTAUT2 model incorporating PI. Results suggest that SDFI of female bank employees is higher than SDFI of female IT employees owing to higher contribution of variables of SDFI in case of banks. The study also found mediation of DBAI on SDFI to be more among bank employees. The study contributes by extending the model of UTAUT2 in the financial domain. The model is used to make a comparative study of two sectors equally contributing to DFI among economy. DFI needs to be sustainable for economic progress of a nation. Thus, the study is unique in extending the DFI to SDFI by adding constructs of future DB usage, Increased DB usage, Frequent usage, and CS (SDFI4), that depict Continued Intention to use technology. Although CS has been given importance previously to understand the continued intention to use technology, but the study adds to literature by collaborating CS with other constructs too.

Despite the contribution, the study lacks in generalization due to limited geographical coverage. This paves way for future studies. Authors suggest to incorporate more variables in the model to get a deeper analysis of DB adoption. Gender perspective can also be added in the model. The model helps to frame women-oriented policies to raise their SDFI. Also, results motivate application designers to develop DB application to be tailored according women’s needs.

Footnotes

Appendix A: Measurement Items

Acknowledgements

The authors are obliged to the respondents for timely and honest completion of the questionnaires. Authors thank the reviewers for their useful comments.

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.

Data Availability Statement

The data would be made available on request to the corresponding author.