Abstract

The outbreak of COVID-19 has been accelerating the digital transformation of financial institutions all over the world. Mobile banking APPs become an important channel to provide financial services in the Internet and Big Data era. Factors that restrict its development have attracted the close attention of scholars and practitioners around the world. Different from a general APP software, mobile banking APPs naturally have some financial attributes which set high requirements for personal privacy protection and other security issues. For this reason, this paper extends the original UTAUT2 model by incorporating a new constructor: perceived risks. The study carefully selects China Construction Bank’s mobile banking app (short as “the CCB APP”), as she is the biggest bank in China and has good novelty and representativeness in financial technology. This paper constructs an extended UTAUT2-based model using questionnaires and structural equation modeling the user behavior of CCB APP and tests the influencing factors of the proposed model through empirical analysis. Similar to other studies using the UTAUT2 model, the findings of this paper indicate that performance expectations, effort expectations, social influence, facilitators, and habits, all have a positive impact on CCB APP users’ intentions. Their intention to use was a mediating variable of user behavior, while facilitators directly influenced CCB users’ behavior. However, the study finds that perceived risk negatively affects the CCB users’ intention while hedonic motivation and price value do not significantly affect users’ decision-making process. Based on these findings, the misdirection should to be avoided in regard to financial APP development by financial institutions is discussed and the future research direction concerning mobile banking app adoption is illustrated.

Introduction

According to the “China Electronic Banking Survey Report (CFCA, 2020)” released by China Financial Certification Center, the proportion of personal mobile banking users reached 71%, a 12% increase year-on-year (Hua, 2021). Especially since the outbreak of COVID-19, mobile banking APPs have gradually become the main battlefield of financial empowerment in the era of digital economy.

The importance of promoting mobile banking APPs to go with the development of a digital economy is self-evident, and the study of user behavior from the user side has received increasing attention from scholars. It is found that: first, trust has a significant positive impact on users’ satisfaction when using mobile banking services (Geebren et al., 2021); second, due to the difficulty of information security and personal privacy protection, which is the main reason for users to refuse to use mobile banking APPs (Cavus et al., 2021); third, perceived usefulness, effort expectation, and social influence have a positive effect on users’ willingness to use mobile banking APPs (Siano et al., 2020); fourth, focuses on methodological innovation, such as adopting a combination of neural network analysis and structural equation modeling, to verify that user satisfaction and intention to use are two influencing factors that affect users’ actual usage behavior for mobile banking (Sharma & Sharma, 2019); fifth, in security research of mobile banking Apps, 61% of users are willing to pay for additional security (Snyder & Byrd, 2017).

In a study by Chinese scholars, it was found that: First, bank institutions in China have long focused on managing credit risk and business risk, and have comparatively less understanding of the risks associated with mobile banking APPs and new technologies (Zhejiang Regulatory Bureau of China Banking and Insurance Regulatory Commission, 2020). Second, mobile banking APPs become an important tool for online payments. General bank service users are aware that there are security risks or security vulnerabilities in the process of using it, which would cause users to worry about risks such as asset loss and information leakage (Shi, 2019). Third, a study on mobile banking users’ usage behavior in agricultural credit societies found that perceived risks significantly affect users’ willingness to use (Yuan et al., 2016).

Although perceived risk was considered, a systematic factor analysis based on UTAUT2 has not yet been conducted by scholars in China. Endogenous territorial limitations of the rural credit union system is not only related to the business strategies of local banks but also essentially involves their nature and positioning in the overall banking system, which is the logical starting point of the bank’s financial operations. Positioned as a mass cooperative financial organization, rural credit unions do not yet have the inherent strength and external environment to engage in cross-regional operations. This characteristic of using acquaintance credit as a bond also determines that its service targets are limited to specific regions, and it is not necessary or difficult to extend to cross-regional operations (Du, 2023).

The relevant literature in different countries has shown that the investigation of mobile banking APP users’ behavior has become a hotspot in the current research field. Secondly, the security perspective should be a major factor that cannot be avoided in future research on financial APPs regarding users’ behavior. Along with the rapid development of the Internet, the third-party payment platform has dramatically impacted the operation and development of commercial banks (Cui & Jin, 2017). This is because third-party payment platforms and commercial banks have severe overlaps and malicious competition in business, which directly increases the cost of customer acquisition for commercial banks and inhibits their income level (T. Xie & Liu, 2019), and is prone to systemic risks in the financial industry. In current China, the realization of shared prosperity has become a major practical problem for financial institutions in implementing the digital transformation strategy. In this regard, it is urgent to find ways to expand the scale of mobile banking app users to ensure that it can play an essential role in the financial empowerment of the digital economy and promote rural revitalization.

The key to scaling up the user use of mobile banking APPs lies in sorting out factors that constrain users’ intention to use them. This paper attempts to answer the following three research questions:

(1) What factors influence users’ intention to use the CCB APP?

(2) What is the role of each influencing factor on the user’s intention to use the APP?

(3) Based on this, what are the recommendations for improving mobile banking APP users’ intent?

The main contribution of this paper is:

At the academic level, because the mobile banking APP has financial attributes and high requirements for information security, users inevitably worry about the security of their property and privacy and other aspects when using the financial APP, so this paper introduces a risk perception perspective to enrich and improve the application scenarios of the UTAUT2 model in banking institutions and make up for the deficiencies of the information security dimension in the original UTAUT2 model;

At the practical level, the mobile banking APP of China Construction Bank, one of the four major banks in China, has a large user base as a specific research object. The financial investment in financial technology is higher in comparison with other banks, and it is more representative in terms of technological frontier and advancement. The research results have high practical reference value for the internal optimization or improvement of marketing measures of mobile banking APP.

Literature Review

Mobile Banking App and User Usage Behavior

A mobile banking APP is a third-party application of traditional banking business on the smartphone platform, an essential financial service in the Internet era, and an intermediary platform for information exchange and transactions between banks and customers (Hua, 2021). In essence, a mobile banking APP relies on a mobile phone as the carrier for information acceptance and processing. It breaks the time and space limitations of bank users in business processing with the help of a mobile network, which enriches the financial service channels and brings great convenience to users (Wang et al., 2018). It also makes it an important channel for online asset management services, customer service management, and other business between financial institutions and their customers (Zou, 2018).

User behavior refers to “the analysis of the composition and characteristics of users and the patterns exhibited by users in the process of use to determine or predict their intentions and needs” (Liu et al., 2020). The study of user behavior has been widely used in information security, online marketing, and opinion management (Zhang et al., 2015). According to the survey, the proportion of daily user usage behavior of a computer or mobile phone is 40.3% and 83%, respectively, and it was evident that mobile phone usage of users has a higher proportion (An, 2021). It can be seen that a mobile APP, as a mobile terminal, has become the most crucial application medium, and user usage behavior based on this medium should be the research focus. Unlike computer media, the user behavior of mobile terminals shows the characteristics of mobility, instantaneousness, and efficiency of social communication but also aims to meet the convenience of life and the pursuit of quality of life.

A mobile banking APP is not a simple online extension of a traditional offline banking business. There are significant differences. The differences come from: first, in terms of business efficiency enhancement, compared with the offline processing method of traditional banking business, mobile banking apps can significantly save the processing time of banking jobs so to enhance efficiency; second, in terms of non-contact service enhancement, the ongoing epidemic further strengthens the necessity of non-cash and non-contact financial services and other business, so to protect users’ health and safety.

UTAUT2: Unified Theory of Acceptance and Use of Technology 2

The extended integrated Unified Theory of Acceptance and Use of Technology 2 (UTAUT2) is an upgraded theoretical model of UTAUT proposed by Venkatesh, Thong, and Xu et al. by refining and optimizing the original UTAUT model to cope with the shortcomings of the original model (Venkatesh et al., 2012). The UTAUT2 model firstly inherits all core variables from the original UTAUT theory; secondly, it adds three core variables, namely hedonic motivation, price value, and habit; thirdly, comparing to the moderating variables part of the original UTAUT theoretical model, in this study, voluntariness is removed, gender, age, and experience are retained. From a systems perspective, the incorporation of the new core variables brought about differences in the composition of the variables, which in turn makes differences in the interrelationships of the variables, leading to the differences between the two theoretical models and ensuring the advanced nature of the UTAUT2 model used in this study.

Since its introduction, the UTAUT2 theoretical model has been acknowledged by scholars in many countries because of its progressive nature, highlighted by its wide application in various fields. First, in the field of AI APPs, Vimalkumar et al. (2021), in studying users’ intention to use digital voice assistants based on a theoretical basis—the UTAUT2 model, verified that all antecedent variables have significant effects on users’ intention to use the APP; second, in the field of mobile payment APPs, Oliveira et al. (2016) based on the UTAUT2 theoretical model, investigated the reasons affecting users’ use of mobile payments in the Portuguese region, and the results showed that users’ behavior of using mobile payments is influenced by performance expectations, perceived technological security, and other factors; third, in the field of social APPs, in a study of users’ information-sharing behavior on social networking sites by Dhir et al. (2018), the UTAUT2 theory was used as a research model to test 780 adolescents. Their study confirms that habit and hedonic motivation have a significant effect on users’ willingness to use.

Research Hypothesis Development

Performance Expectancy

Performance expectancy (PE) refers to the degree to which using technology will benefit users in performing certain activities (Venkatesh et al., 2003). This paper defines performance expectancy as the user’s belief that using the CCB app will bring them richer information, resources, and better services. The more users believe that the mobile banking app will help them conduct their business, the stronger their willingness to use it. Many studies have also confirmed that performance expectancy positively influences users’ willingness to use; Araújo Vila et al. (2021) in their study of factors influencing spa travel APPs, proved that performance expectancy has a significant positive effect on travelers’ purchase intentions. Penney et al. (2021) in their study on mobile money explored that performance expectations have a significant impact on predicting users’ behavioral intentions. Based on this, the following hypotheses are proposed:

Effort Expectancy

Effort Expectancy (EE) is the level of effort that users have to put in when using a new system or new technology (Venkatesh et al., 2003). This paper defines effort expectancy as how easy or difficult it is for users to download or use the banking app for certain services. It is generally believed that the easier the process of installing a mobile banking APP is, the less effort users have to put into it, and then the more users will be willing to use the APP. The relationship between effort expectation and willingness to use has also been confirmed by some scholars, such as in a study on researchers’ willingness to engage in online academic conference knowledge exchange in an epidemic situation, it is proved that effort expectancy has a significant positive effect on the willingness to engage in online academic conference knowledge exchange (Cai et al., 2021). In a study on the willingness of the public to use government microblogs in response to emergencies, it was confirmed that effort expectancy has a significant positive effect on the willingness of public use (Hou, 2017). The significant effect of effort expectancy on intention to use was confirmed in a study of executives’ acceptance of Blended Learning (Dakduk et al., 2018). Based on this, the following hypotheses are proposed:

Social Influence

Social Influence (SI) is the degree to which users perceive that how other people would think of them if they use a new technology or system (Venkatesh et al., 2003). This paper defines social influence as the extent to which the user’s close family and friends, social media, and the general social environment influence the user’s willingness to use. Social influence is a reflection of a person’s herd mentality, where individuals are vulnerable to environmental influences. For example, people would take devices from people surrounding them, especially their family and friends. Many studies have also demonstrated the relationship between social influence and user’s willingness to use some new information systems, such as in a study on the factors influencing the usage behavior of online office app users, it was confirmed that social influence has a significant positive impact on users’ behavior (Liu et al., 2020); Wu et al. (2021) in their research on smart cities, confirmed that social influence has a significant positive impact on users’ willingness to use health information technology behaviors. Social influence has a significant positive impact on users’ behavior in study of sustained mobile payment use in Sudan (Sleiman et al., 2022). Based on this, the following hypothesis is proposed:

Facilitating Conditions

Facilitating Conditions (FC) refers to the degree to which users perceive external support for using a technology or service (Venkatesh et al., 2003). This paper defines facilitating conditions as the convenience and technical support users need to use the CCB APP system. The relationship between facilitators and willingness to use has also been confirmed by some scholars, such as in a study on mobile payment, which confirmed that facilitators have a significant positive effect on users’ willingness to use (Patil et al., 2020); In a study on the acceptance of modern technology among the elderly, researchers find that facilitators have a significant positive effect on users’ willingness to use (Macedo, 2017). Based on this, the following hypothesis is proposed:

Hedonic Motivation

Hedonic Motivation (HM) refers to users’ fun or joyful experience in using a technology (Venkatesh et al., 2012). This paper defines hedonic motivation as the pleasurable experience and satisfaction users get when using the CCB APP. The mobile banking APP, as an alternative to traditional banking, can be operated by users through their smartphones. The entertainment activities included in the software, such as the chance to win random rewards by completing payments and participating in the golden egg draw, may bring novelty and pleasure to its users, eventually increasing the volume of total users. Many studies have also demonstrated the relationship between hedonic motivation and intention to use. For example, Baabdullah et al. (2019), in their study of the actual usage behavior of mobile banking users, confirmed that hedonic motivation has a significant positive effect on users’ actual usage behavior; Aria and Archer (2018) in a study of online medical healthcare systems in different contexts, confirmed that hedonic motivation has a significant positive effect on patient’s willingness to use online systems. Based on this, the following hypothesis is proposed:

Price Value

Price Value (PV) is when the benefits of using technology are perceived to be greater than the costs paid by the user, and the value positively impacts the intention (Venkatesh et al., 2012). This paper defines price value as the perceived benefit or cost reduction of using the software for users when they use the CCB app for business transactions. Many research scholars have already tested the relationship between price value and intention to use. For example, a study of online virtual try-on systems confirmed that price value is an essential predictor of users’ usage behavior (Qasem, 2021). A study of social networking sites confirmed that price value significantly positively affects students’ willingness to use social networking sites (Chang et al., 2022). Based on this, the following hypothesis is proposed:

Habit

Habit (HT) is the degree to which a user unconsciously uses technology or a system in continuous learning, and it reflects the unconscious behavior of the user (Venkatesh et al., 2012). In this paper, Habit is defined as the degree of unconscious use of the CCB app when it is available. A study on consumers’ willingness to share their feedback of branded products confirmed that habit has a significant positive effect on users’ perception of posting their experience on the website (Herrero & San Martín 2017). A study on mobile banking confirmed that habit significantly positive impact on users’ willingness to use (Baabdullah et al., 2019). Based on this, the following hypothesis is proposed:

Perceived Risk

Perceived Risk (PR) refers to users’ degree of expected uncertainty and loss when using a new system or technology. This study examines the impact of perceived risk on users’ willingness to use the CCB App by introducing the perceived risk variable, defined in this paper as the degree to which users perceive problems such as information leakage and insecurity of account funds when using the CCB App. When customers use a mobile APP for transferring money and remittance, it increases many risks that are not present in traditional offline transactions. These uncertain risk factors may cause loss of funds or privacy leakage in users’ accounts, and these problems vastly increase users’ perception of risk and reduce their willingness to use it. In a study of mobile banking, it was shown that perceived risk has a significant negative effect on users’ willingness to use (Chen et al., 2019; Singh et al., 2020), and their study on online food stores confirmed that perceived risk has a significant negative impact on consumer’s intention to use (Van Droogenbroeck & Van Hove, 2021). Based on this, the following hypothesis is proposed:

Intention to Use

According to the theory of planned behavior, a large part of the actual usage behavior of users is determined by their intention to use, which is defined in this paper as the user’s intention to use the CCB APP to pay or process other businesses. Some scholars have also demonstrated the relationship between usage intention and usage behavior. A study of the higher education ecosystem confirmed that the intention to use significantly affects users’ behavior (Malešević et al., 2021). Also, Pham et al. (2022), in their study of online banking services in Vietnam, verified that users’ intention to use has a significant impact on user behavior. From this, it can be predicted that users’ intention to use is the most direct factor affecting users’ behavior. The stronger their intention, the higher the probability of taking users’ actual behavior. Based on this, the following hypothesis is proposed:

Gender, Age, and Experience on Mobile Banking App Users’ Intention to Use

Gender

Gender is a statistical variable that measures the size of the population. Since users of different genders have different thinking patterns and cognitive levels, gender plays an influential role in users’ acceptance of technology and user behavior. In a study of e-government software adoption among Taiwanese residents, gender was confirmed to have a moderating effect between social influence and behavioral intentions (Lian, 2015); Ameen et al. (2018) in a study of smartphone use in the Middle East, confirmed that gender has a significant effect on users’ willingness to use. Based on this, the following hypothesis is proposed:

Age

Since users of different ages have different life experiences and mental maturity, age moderates users’ use of technology or behavior. Many studies have demonstrated the moderating effect of age on the relationship between behavioral intentions. A study by Chopdar et al. (2018) of mobile shopping app software, confirmed that age as a moderating variable has a significant effect on the intention to use in Italy. Based on this, the following hypotheses are proposed:

Experience

Experience refers to knowledge or skills gained through practice, and in this paper, the user’s experience is defined as the frequency with which the user uses the CCB App. Although a user’s specific behavior is to some extent determined by his will, the influence of subjective will diminishes as the user accumulates experience for a particular item. Experience is an essential moderating variable in the UTAUT2 theoretical model. Some scholars have also confirmed the moderating effect of experience on users’ behavioral willingness, such as Li et al. (2016) in their study on the future development of home e-commerce, which confirmed that the more experienced consumers are in online shopping, the stronger their willingness to buy furniture online. Based on this, the following hypothesis is proposed:

Research Model

The research model of this paper is shown in Figure 1.

UTAUT2 model based on perceived risk extension for CCB mobile app in China.

Research Design

Questionnaire Design

The study designed the measurement items based on the original item scale by Venkatesh et al. (2012). The questionnaire was divided into two sections. The first section included six questions about the demographic characteristics of the respondents, such as age, gender, occupation, etc.; the second section contained 30 questions, and three measurement items were designed under each variable, and its scale design was measured using a five-level Likert scale, which divided the measurement range into five levels “completely disagree, not very much agree, average, agree, and strongly agree.” as detailed in Table 1.

Design of Measurement Items for Variables Studied.

Data Collection

To ensure the validity and reliability of survey outcomes, the author visited several branches of the China Construction Bank in Jilin Provinces, China. With the permission of lobby managers, the author was approved to collect questionnaires from users online who had experience in using their mobile banking APP. To ensure the participation rate of the questionnaire, a bottle of drinking water was provided to users who participated in responding to the questions. At the research site, 432 questionnaires were distributed, and all were collected, with a final return rate of 100%. By screening the data, invalid questionnaires with incomplete answers, all identical answers, or short responding times were deleted. In the end, 403 valid questionnaires were obtained. The effective rate of the questionnaires was 93.29%, and the basic information of the sample data is shown in Table 2.

Statistical Analysis of Demographic Characteristics (N = 403).

Data Analysis

Reliability and Validity Analysis

The author conducted reliability and validity tests through SPSS 22.0 software to analyze the sample data obtained from the questionnaire. The results of data analysis showed that the recovered questionnaire data were suitable for factor analysis: Bartlett’s spherical test statistic was 5,353.790, and the corresponding probability significance (Sig) was .806, according to which it is known that the variables are strongly correlated with each other and therefore also suitable for factor analysis. The internal consistency reliability analysis of each variable was carried out by calculating Cronbach’s alpha coefficient, and Cronbach’s alpha coefficients of each dimension were above .7, indicating that their data were internally consistent. The details are shown in Tables 3 and 4.

KMO and Bartlett’s Test.

Reliability Tests.

Correlation Analysis

In this paper, validated factor analysis was conducted through structural equation modeling with two analysis software’s, AMOS 24.0 and SPSS 22.0 software, which included convergent and discriminant validity. From Table 5, it can be seen that the factor loadings of the measurement terms for each latent variable are greater than the theoretical value of .50 and significant at the p < .001 level, with CR values greater than 0.75, much higher than 0.60, and AVE values greater than 0.50. From Table 6, the results show that the correlation coefficients of any two observed variables in the scale are less than .6. Each data on the diagonal is the square root of the AVE value of each variable and are more significant than the square of the correlation coefficient of that variable with other variables. All the above data meet the basic test requirements, indicating that the survey scale has good discriminant validity.

Factor Load and Variable Combination Reliability.

Discriminant Validity of Measurement Scales.

Path Analysis and Hypothesis Test

The data of this study were analyzed using AMOS 24.0 software for structural equation modeling to verify the relationship between the variables. Based on the proposed research hypothesis, a complete structural equation model was constructed using AMOS 24.0 software based on the proposed conceptual model (see Figure 2), and the fitness index of this model is shown in Table 7.

CCB mobile app user intention model and standardization coefficients.

Fit Indices.

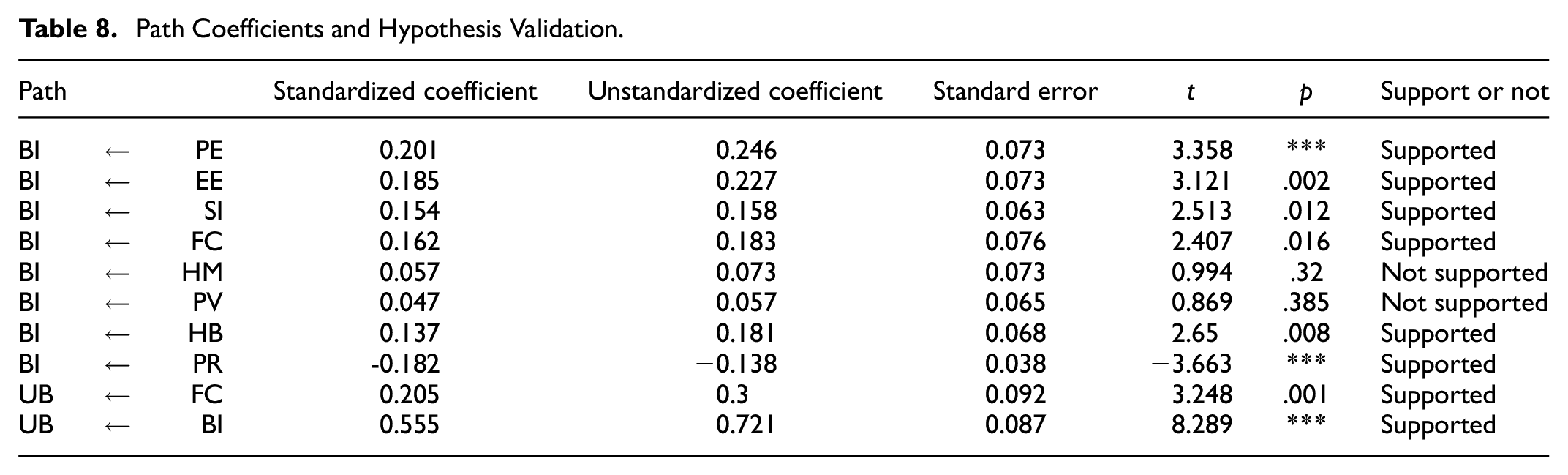

Table 7 shows that the theoretical model proposed in this paper meets the requirements in terms of the fitness index and the model fitness is good. From the Table 8, it can be seen that: first, performance expectation has a significant positive effect on users’ intention to use (β = .201, p < .05,) and H1 was supported; Second, effort expectation has a significant positive effect on users’ intention to use (β = .185, p < .05) and H2 was supported; third, social influence has a significant positive effect on users’ intention to use, H3 was supported; fourth, facilitation factors have a significant positive effect on users’ intention to use (β = .162, p < .05), H4 was supported; fifth, hedonic motivation does not have a significant positive effect on users’ intention to use (β = .057, p > .05), H6 was not supported; sixth, price value has a significant positive effect on users’ intention to use (β = .047, p > .05) does not have a significant positive effect, H7 was not supported; seventh, habit has a significant positive effect on users’ intention to use (β = .137, p < .05), H8 was supported; eighth, perceived risk has a significant negative effect on users’ intention to use (β = −.182, p < .05), H9 was supported; ninth, facilitators have a significant positive effect on users’ usage behavior (β = .205, p < .05) has a significant positive effect on user usage behavior, H5 was supported; tenth, User intention to use has a significant positive effect on user usage behavior (β = .555, p < .05), H10 was supported.

Path Coefficients and Hypothesis Validation.

Moderating Effects Analysis

The moderating variables in this paper were gender, age and experience, and analysis of covariance was conducted on each of the three moderating variables using SPSS software to clarify the effect of different control variables. If the control variables differ significantly in different regions, then the control variable is considered to have an effect, and vice versa.

From Table 9, it can be found that: firstly, the effect of gender as a moderating variable on the antecedent variable and willingness to use is not significant; secondly, the effect of age as a moderating variable on the antecedent variable and willingness to use is also not significant; thirdly, when experience is used as a moderating variable, the significance of the effect of the pathway on social influence, price value, habit, and perceived risk is less than .05, this result proves that experience has significant influence effect.

Analysis of Control Variables.

Discussion and Conclusion

By summarizing the above charts, it is evident that the test supports all of the research hypotheses proposed in this paper except for the partial paths of H6, H7, H11, H12, and H13.

First, according to the empirical data, the information and services brought by the CCB app positively influenced the users’ intention to use it. This finding is consistent with based UTAUT2 model on users’ intention to use virtual doctor appointments (Schmitz et al., 2022). As the CCB APP brings more convenient and diversified choices for users in handling banking and other related business. China Construction Bank, as one of the four central banks in China, also gives full play to the practical value of online internet finance, which not only meets the diverse needs of users but also makes them more time and effort efficient in providing services. In today’s fast-paced time, performance expectations have become a key factor affecting users’ willingness to use a certain product. In the future development, CCB APP designers should strengthen extensive data analysis, make adjustments to meet users’ differentiated needs, and carefully craft functions and modules on the home page so to cater to different user groups and facilitate the user experiences.

Second, the data collected above also suggests that the amount of effort invested by users in using the CCB APP positively influences their usage intention. This finding is consistent with a study based on the UTAUT model on the factors influencing the public’s use of government microblogs in emergencies (Hou, 2017). Due to the current high usage rate of mobile phone apps, the basic operations of various types of software tend to be consistent, and it is increasingly important whether the software is fully functional, whether business processing can meet users’ usage needs, and whether software operations are simple and effective. Therefore, optimizing users’ business processes, the simplicity, and convenience of payment links, and the diversity of business services require the ease of use of a mobile banking APP, which is an important factor in increasing users’ intention to use the CCB APP.

Third, users’ close relatives and friends, as well as social media, could positively impact their willingness to use (Jamshidi et al., 2023; Wu et al., 2021). Due to the ongoing epidemic in China, face-to-face interactions are limited. Mobile banking apps for online transactions and business processing are in line with the social development trend and are recognized by people as a newly-upraising business model. To take advantage of the social influence, the Bank can make better use of social platforms or celebrity endorsement effects to promote the banking APP, so that more people can know about and use the APP.

Fourth, the degree of users’ unconsciousness in CCB applications positively influences their intention to use them. This finding is consistent with the ICT-based UTAUT2 model study, which suggests that habit positively influences users’ usage behavior (Goncalves et al., 2018). Due to the current popularity of smartphones, online payment and business processing have become widely accepted ways to handle financial services. According to the results of the data analysis, the more users are accustomed to using the CCB App for payment and business processing, the stronger their willingness to continuously use the CCB App. To increase users’ habit of using the CCB APP, the Bank management team can use the method of sales training for branch service staff to guide users to operate and use the mobile banking APP to strengthen their habits without adding additional costs.

Fifth, data shows that risks, such as the security and privacy of the software in the process of using the CCB app, may affect the users’ willingness to use it to some extent. This research finding is in line with Patil et al. (2020) study. Due to the rapid development of the Internet, information security is becoming more and more important to users. It is completely not acceptable users do not trust the payment process and information technology of CCB and are worried that the process of payment and business processing within the CCB app will bring about security problems in their financial accounts due to the leakage of personal information. In that case, users will use traditional offline banking to conduct business. Due to the technical limitations of mobile communication, mobile operating system, and information encryption, it is not easy to guarantee 100% absolute security of the security technology adopted by the CCB mobile APP. Thus, the APP designer needs to make a great effort to programming in the field of information security. To protect users’ privacy and security, the Bank is suggested to appropriately join a third-party security testing so to alleviate users’ concerns in business processing or payment, enhance users’ trust in the technology adopted by CCB APP, and eventually increase their willingness to use it.

Sixth, the study also finds that fun activities within the CCB APP and the entertainment experience in the payment process do not show a significant positive effect on the users’ willingness to use the APP. The reason for this may be two reasons: first, because CCB APP is a kind of software combining payment and finance, users mainly focus on business functions such as financial payment and bank transfer, and often do not pay attention to the entertainment settings in the process; second, the market of entertainment APP software is prosperous, and it is difficult to cultivate entertainment functions embedded in CCB APP. This is consistent with the same results based on the UTAUT2 model for meal delivery APP software, which concluded that hedonic motivation has no significant effect on the willingness to use meal delivery apps (Lee et al., 2019). It can be seen that both meal delivery apps and mobile banking apps belong to a class of software with a clear direction of special functions. If it is difficult to achieve effective integration between entertaining and functioning at the same time. Therefore, the APP designers could put comparatively less time and effort into this aspect.

Seventh, the factors of the benefits or cost reduction that the software brings to the users in the process of using the CCB APP have little impact on the users’ intention. This finding is in line with Palos-Sanchez et al. (2019) study. Due to the progressive popularization of financial software and the low fees when transferring or making payments, users tend to ignore the importance of price value when choosing which software to use for payments and business transactions. In that case, the Bank can develop relevant promotional activities to increase the strength of the benefits, such as daily sign-up for seven consecutive days to get phone bill coupons, the first time to use CCB Dragon Payment to purchase goods can receive discounts. The APP designers can make moderate concessions to improve the software’s cost performance, attract more users to use the APP, and increase the user’s perception of price concessions.

Eighth, users are more willing to use the CCB mobile banking app after acquiring the skills or having the convenience of using it. This finding is in line with previous studies (Macedo, 2017). Moving into the era of big data, the widespread use of smartphones has facilitated the development of mobile banking and provided a convenient base for the users of the CCB APP. Therefore, when users become increasingly skilled in using mobile banking apps, the more they will experience the convenience and ease of life brought by the CCB APP, and the stronger the users’ intention to use it will be.

Finally, CCB APP users’ intention to use plays the role of mediating variables in performance expectation, effort expectation, social influence, facilitation factors, price value, hedonic motivation, habit, perceived risk, and CCB APP users’ usage behavior. This study’s results are consistent with previous findings that generally confirm that intention to use affects user behavior (Ali, 2016; Venkatesh et al., 2012).

Theoretical Implications

Due to the widespread use of Alipay and WeChat Pay, mobile banking-type APPs provided by many Chinese financial institutions generally have the issue of low usage volume, which will lead to the difficulty of directly empowering rural revitalization and shared prosperity through the digitalization of financial services. It can be seen that insufficient research on user behavior from the user side is a significant key to restricting the low penetration rate of mobile banking type APPs. Most of the findings of this study are corroborated with the results of previous studies, in which perceived risk negatively affects willingness to use, which inhibits the availability of mobile banking APPs, and because hedonic motivation and price value are difficult to significantly affect users’ willingness to use, which further increases the difficulty of mobile banking APP usage penetration. From the perspective of theoretical innovation, this paper proposes a UTAUT2 extension model based on a risk perception perspective, which not only enriches the explanatory power of the UTAUT2 model for mobile banking APP users’ usage behavior but also systematically sorts out the influencing factors that restrict mobile banking APP users’ willingness to use. Its findings can provide theoretical support for the digital transformation of financial institutions.

Practical Implications

The findings of this paper can directly provide valuable suggestions for commercial banks on how to design, develop and operate mobile banking APPs in the era of digital transformation. Specifically, the positive effect of performance expectation on users’ willingness to use is that users expect mobile banking APPs to provide more convenient services, such as opening live payment services in mobile banking APPs; second, the positive effect of effort expectation on users’ willingness to use is that APPs with cumbersome operation interfaces are not friendly to older and users with weak learning ability. Therefore, the process should be simplified, and the software interface should be clear and operable to reduce the learning cost of the user group; third, for the positive effect of social influence, word-of-mouth publicity could be done more frequently, and the recommendation mechanism should be designed to strengthen the word-of-mouth effect; fourth, for the negative effect of perceived risk, the information security mechanism should be optimized, such as creating the only official download channel to avoid the malicious installation of pirated software at source, and such as regular security upgrade management to ensure the timely repair of security vulnerabilities; fifth, for the hedonistic motivation and price value and other factors do not work significantly, designers can reduce the entertainment function in APP, prudent consideration of price incentives.

Limitations and Future Study

The research of this paper on mobile banking type APP only takes the China Construction Bank’s App as an example. More bank Apps could be included and examined for future studies. Its research findings have reference value for some financial institutions’ future or ongoing digital transformation. However, the research data in this paper are collected from an offline field to ensure its high quality. Due to the epidemic, the data only come from Changchun City, Jilin Province. Its research findings have geographical limitations and have not yet been covered all over the country. In addition, local village banks have different customer service targets, especially from the perspective of rural revitalization. The factors affecting users’ willingness to use the service may be different, which needs to be analyzed and proven in the subsequent research.

Footnotes

Author Contribution Statement

Jianhua Jiang: Conceptualization, Validation, Formal analysis, Writing—review & editing, Validation, Supervision, Final review.

Jianing Ma: Writing—review & editing, Questionnaire design, Data collection, Data analysis.

Xiaoqing Huang: Translation touch-ups, Supervision, Final review.

Jinping Zhou: Supervision, Final review.

Taibo Chen: Supervision, Final review.

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: The authors thank the financial support from the Foundation of the Jilin Provincial Department of Science and Technology (No.YDZJ202201ZYTS565). Jilin Office of Philosophy and Social Science (No. 2022B84).

Ethics Statements

Generated Statement: No animal studies are presented in this manuscript.

Generated Statement: No human studies are presented in this manuscript.

Generated Statement: No potentially identifiable human images or data is presented in this study.

Data Availability Statement

The data used in this study was collected through an online survey questionnaire. The dataset can be accessed by sending an email to the corresponding author. Access to data is available for researchers who request access and require researchers to provide their purpose of use.

In order to protect the privacy of participants, all personal information is anonymous. The future updates of the dataset will be conducted regularly, and detailed information can be inquired about by sending an email to the corresponding author.