Abstract

This study investigates the predictors of financial distress of banks in Sub-Saharan Africa. Specifically, we examine the relationship between bank financial distress and the 5Cs (i.e., Character, Capacity, Capital, Condition, and Collateral). We use logistic regression and panel data from 228 listed and non-listed Sub-Sahara Africa Banks over the period 2006 to 2016 to test the hypotheses. We find that the rating measures of capacity (cost to income), capital (leverage), and condition (loan loss reserves to gross loan and inflation) positively affect the financial distress of the banks in Sub-Saharan Africa. Control of corruption decreases the probability of financial distress; however, the collateral and character indicators do not predict the financial distress of the banks. This study adds to the debate on how Character, Capacity, Capital, Condition, and Collateral affect bank financial distress in Sub-Saharan Africa, a region with high bank insolvency but research remains scant.

Introduction

Fifty-five years post Altman’s (1968) and Beaver’s (1966) studies, the prediction of financial distress of banks in Sub-Saharan Africa, where there is frequent bank failure, remains an empirical question (Ozili, 2018). In particular, studies on bank failure prediction in developing countries, especially in Africa regions, focus on financial integration (Popiel, 1994), stability (Ozili, 2018), or country-specific (Babajide et al., 2015) using financial ratios. The few existing studies on the financial insolvency of banks in emerging markets and the few available empirical studies’ results are uncertain (Haris et al., 2022). These studies largely overlook fundamental causes of financial distress of firms, including macroeconomic (Acosta-González et al., 2019), non-financial (Altman, 2018; Appiah, 2011; Calice, 2014; Distinguin et al., 2010) and corporate governance (Appiah et al., 2015; Ciampi, 2015; Lakshan & Wijekoon, 2012; Manzaneque et al., 2016; Salloum & Azoury, 2012). Consequently, scholars (e.g., Trussel & Patrick, 2018) are calling for more studies on the probabilities of banks’ financial distress, especially in emerging markets, since a bank’s stability contributes significantly to avoiding severe economic turmoil (Haris et al., 2022).

We, thus, attempt to fill this gap by combining these neglected indicators to assess their effects on banks’ distress. Specifically, the study examines the probabilities of financial distress of banks in the Sub-Saharan Africa context using the 5Cs of credit rating measures (capacity, capital, collateral, conditions, and character) while controlling for corruption and regulatory quality. We find that the rating measures of capacity (cost to income), capital (leverage), and condition (loan loss reserves to gross loan and inflation) positively affect the financial distress of the banks in Sub-Saharan Africa. However, the collateral and character indicators do not predict the financial distress of banks in Sub-Saharan Africa.

Our contributions are twofold. First, this study examines the role of the 5Cs on bank financial distress, answering the call made by Zaki et al. (2011) for more research on the effects of 5Cs in settings where research is neglected but bank financial distress remains a trending topic. From this point, the present study complements the emerging body of work focused on the effects of the 5Cs on bank financial distress in developing economies (ElBannan, 2021; G. Gupta & Mahakud, 2022; Kanoujiya et al., 2021, 2022; Rastogi & Kanoujiya, 2022; Zaki et al., 2011). We provide evidence on how to assess the probabilities of banks’ financial distress in Sub-Saharan Africa, a region with high bank bankruptcy. Second, the study contributes towards policy reform by showing that Control of Corruption is a relevant indicator in understanding financial distress in the Sub-Saharan Africa context. Thus, a wake up call for policymakers, regulators, and investors to advance corruption control strategies, thereby reducing the probability of bank distress in the Sub-Saharan Africa region.

The study proceeds as follows. Sections “Literature Review” and “Method” provide the literature and methodology, respectively. The results and discussion of the findings are in Section “Results and Discussion,” and Section “Conclusions” provides the concluding remarks.

Literature Review

Motivation

The literature on corporate financial distress has largely ignored the 5Cs in both developed and developing countries. Beaver (1966), for example, concludes that the critical determinant of corporate failure was net cash flow from operations, while Altman’s (1968)Z-score proposed five financial explanatory variables (retained earnings to totals assets ratio, earnings before interest, working capital to total assets ratio, taxes to total assets ratio, the market value of preferred and common equity to total liabilities ratio, and sales to total assets ratio) as the predictors of corporate failure. Taffler (1982) later developed a similar Z-score model and concluded on different explanatory variables: profit before taxes to current liabilities ratio, current assets to total liabilities ratio, current liabilities to total assets ratio, and working capital to operating costs ratio.

Le and Viviani (2018) report that the critical accounting ratios that predict bank failure are liquidity, capital efficiency, and profitability ratios. Okezie et al. (2011) argued that capital ratios predict bank failure. Calice (2014) further finds evidence that low leverage indicates banks’ low possibility of financial distress. Appiah et al. (2015) also find that the most predictors of the financial failure of firms are earnings before interest and tax to total assets, working capital to total assets, total debt to total assets, quick assets to current liabilities, net income to total assets, and current assets to current liabilities. Distinguin et al. (2010) also find that the level and change of capital, asset quality, earnings, and liquidity ratios are crucial in assessing the probability of financial distress. Zaki et al. (2011) also find that the cost-income ratio, total asset growth ratio, equity to total asset, and loan loss reserve to gross loans ratios directly impact banks’ probability of financial distress. Furthermore, Carmona et al. (2019) find that low figures of retained earnings to average equity, risk-based capital ratio, and pre-tax return on assets contribute to banks’ failure. Kristóf and Virág (2022) also report that management capability, capital adequacy, and earnings predict banks’ failure in Europe.

Regarding macroeconomic measures, business failure is a function of high interest rates, inflation, GDP gap, money supply, and industrial production index (Hol, 2007; Liu, 2009). On corporate governance measures, Lakshan and Wijekoon (2012) find that an audit committee, official compensation of board members, and outside director ratio predict corporate financial distress. Firms with a higher outside directors’ ratio are less likely to suffer financial bankruptcy (Salloum & Azoury, 2012). Others document the significance of CEO duality, ownership concentration, and block shareholders in the financial distress syndrome (see Manzaneque et al., 2016).

Largely, corporate distress literature is dominated by ad hoc models due in part to the lack of economic theory that guides the selection of variables (see Appiah et al., 2015; Blum, 1974; Taffler, 1982). The ad hoc models include the CAMELS rating system, 5Cs, and Moody’s RiskCalc model (Zaki et al., 2011). Following Zaki et al. (2011), the present study adopted the 5Cs of credit rating of individuals and entities to select explanatory variables for the study. The 5Cs are Capacity, Capital, Collateral, Conditions, and Character. We turn next to our hypotheses development by discussing each in turn.

Capacity and Financial Distress

We use two proxies to measure the Capacity of Banks. Our first proxy is liquid assets to customers’ deposits and short-term funds (Kristóf and Virág, 2022; Zaki et al., 2011). Liquid assets are banks’ assets that change quickly into cash (Phan et al., 2022). Liquid assets include cash and bank balances, reserves with the central bank, and marketable securities (Herger, 2019). The ratio of liquid assets to customers’ deposits and short-term funds measures the short-term liquidity position of a bank (J. Gupta & Kashiramka, 2020; Zaki et al., 2011). Bhandari and Iyer (2013) argue that a higher ratio denotes that the bank is financially stable to meet current depositors’ financial demands, which decreases financial distress. We, therefore, hypothesize a negative relation between liquid assets to customers’ deposits and short-term funds and financial distress of banks.

Our second proxy for the capacity of the banks is the cost-of-income ratio (Kristóf and Virág, 2022, Zaki et al., 2011). This is a ratio of total costs to banks’ total revenue (Simoens et al., 2022). Cost comprises interest costs, general expenses, overhead and administrative costs, and total revenue is the sum of interest and non-interest income (Zaki et al., 2011). Cost-of-income ratio is an indirect way of assessing management efficiency in terms of the profitability of banks (Derbali, 2021). A low cost-of-income ratio indicates the efficient and effective management of the operations of banks through cost-cutting (Huljak et al., 2019). However, a high cost-of-income ratio means management inefficiency and threatens banks’ survival (Zaki et al., 2011). Hence, we hypothesize a positive relationship between the cost-of-income ratio and the financial distress of banks.

Capital and Financial Distress

Financial leverage is used to represent the capital indicator. Leverage denotes debt divided by the sum of equity and debt value at the end of the reporting year (Appiah, Gyimah, & Abdul-Razak, 2020; Appiah, Gyimah, & Adom, 2020). In theory, high corporate financial leverage pressures management to prevent waste and improve economic performance (Zhou et al., 2021). In practice, however, a high debt burden on the bank may constrain investment which could eventually cause financial distress (Kalash, 2021). Put differently, high financial leverage directly correlates with financial distress, and low financial leverage indicates a low probability of bank financial distress. Consequently, we hypothesize a positive relationship between financial leverage and financial distress of banks.

Collateral and Financial Distress

Collateral is proxied as total asset growth (Titman et al., 2013). Put differently, Collateral measures the annual increase in banks’ total assets. Assets of Sub-Saharan Africa banks consist of more personal investments in high-risk loans (Zaki et al., 2011), implying growth in these loans results in a higher probability of default (Kumar et al., 2018). Here, banks with higher total asset growth are more exposed, resulting in a higher probability of bank financial distress (Zaki et al., 2011). Thus, a positive relationship is hypothesized between total asset growth and financial distress of banks.

Condition and Financial Distress

We consider both firm and economic conditions that affect the financial distress of banks. Credit risks such as non-performing loans to gross loans (NPLTL) and loan loss reserve (LLR) are used to represent firm conditions. A non-performing loan to gross loan (NPLTL) is the sum of borrowed money in which the borrower has failed to meet scheduled payments for at least 90 days (Bholat et al., 2018). Banks consider such debts bad; hence provisions are made for loan loss reserves (Ozili & Outa, 2017). The higher the loan loss reserve provisions in banks’ financial reports, the higher the probability of financial distress. On the other hand, loan loss reserve (LLR) is the allowance or provision made against profit to safeguard against future probable non-performing loans and losses arising from renegotiated loan terms (Gutiérrez-López & Abad-González, 2020). A high loan loss reserve to gross loan ratio indicates that management expects a high loan default in the ensuing years (Chen et al., 2021). Thus, we hypothesize that both non-performing loan to gross loan and loan loss reserve to gross loan ratio positively affect financial distress of banks.

Regarding the economic condition, GDP per capita (GDPPC) measures a country’s economic performance that accounts for the population (Coscieme et al., 2020). If a nation’s economy grows faster than its population, the GDPPC increases, and the financial health improves due to a positive business environment (Inekwe et al., 2018). A continuous economic downturn or reduction in GDPPC increases the probability of corporate failure (Alifiah & Tahir, 2018). Also, high inflation (CI) significantly influences the occurrence of a banking crisis, while low inflation contributes to financial stability (N. Gupta & Kumar, 2022). Also, Brownbridge (1998) argues that high inflation increases the volatility of business earnings because it directly affects pricing policy, and the probability of businesses incurring losses increases (Msomi, 2022). Inflation increases the credit risk or the likelihood of loan default (N. Gupta & Kumar, 2022). When this crystalizes, it leads to the non-performing loan, directly influencing bank financial distress (Msomi, 2022). Finally, the exchange rate depreciation (CNERD) is a country’s local currency level against the US dollar over 1 year (Kalemli-Ozcan et al., 2021). According to Fidrmuc and Kapounek (2020), a high exchange rate depreciation weakens a bank’s financial position, especially if it holds a larger share of its liability in foreign currency. Also, Kaminsky and Reinhart (1999) point out that a high devaluation of local currency leads to a higher probability of bank financial distress. Sahut and Mili (2011) find that real exchange rate depreciation is a crucial predictor of the financial distress of banks. We, therefore, hypothesize that GDPPC, CI, and CNERD positively affect the probability of bank financial distress.

Character and Financial Distress

Agency and resource dependency scholars, respectively, advanced the theoretical case for the need for more independent non-executive directors to monitor self-seeking CEOs (Hermalin & Weisbach, 1988) and also lobby for support from critical resources providers (Appiah & Chizema, 2016). In this regard, the board chairman is selected from the independent non-executive directors to ensure enhanced independence of the board (Neves et al., 2022). In practice and theory, the monitoring and resource provision functions of the board are the keys to avoid bank financial distress (Appiah & Chizema, 2016; Hillman & Dalziel, 2003). This suggests a poorly composed board with compromised members and inadequate skills, individual fame, qualifications, work experience, social and communication skills is more likely to be ineffective in its oversight roles, implying the probability of financial distress tends to increase with the presence of CEO duality (Marie et al., 2021), lesser independent directors (Appiah & Amon, 2017; Jensen & Meckling, 1976; Puni & Anlesinya, 2020), lower board size (Badu & Appiah, 2017). Therefore, we hypothesize a positive relationship between CEO Duality and financial distress of banks. However, both board independence and board size negatively affect financial distress of banks.

Method

Design and Data

This study adopts the quantitative approach to examine the determinants of financial distress probabilities of banks in Sub-Saharan Africa. Data for 321 Africa banks are already available during the data-collecting procedure, including duplicate records due to the concurrent availability of consolidated/unconsolidated financial data and financial statements from Bankscope and the World Bank Databases. We find that most of the data beyond 2016 are unconsolidated, unaudited, or unavailable after screening the data. We remove the duplicated statements and focus on audited and consolidated financial information; a final usable sample of 228 banks over 11 years (2006 to 2016) is used for data analysis. The available datasets from the Bankscope Database and World Bank Database on Sub-Saharan Africa countries (number of banks) are Ghana (21), Nigeria (24), Cote D’Ivoire (19), Kenya (25), Uganda (16), Rwanda (8), Zambia (20), Sudan (15), South Africa (23), Tanzania (22), Mauritius (15), and Zimbabwe (20).

Econometric Models

The probability of bank distress can be assessed using either a static or dynamic approach (Tomas Žiković, 2018). Selection between these two approaches depends on whether the data is discrete or continuous. As the data from financial ratios, macroeconomic variables, cultural variables, and corporate governance variables are collected and reported annually, the analysis uses discrete-time data (Brekumi et al., 2023). The study adopts the logistic statistical technique used in previous studies (Zaki et al., 2011). Recent literature review indicates that the logistic regression model is one of the most standard models used in predicting corporate failure or success (Adeola et al., 2021; Gyimah & Adeola, 2021; Gyimah et al., 2019, 2020, 2023; Jalloh et al., 2019; Lakshan & Wijekoon, 2012; Manzaneque et al., 2016; Sahut & Mili, 2011; Tomas Žiković, 2018; Zaki et al., 2011). The financial distress model is as follows:

Note that Yit is the probability of financial distress (PFD) of banks i at time t, Sit is the score that constitutes an order of the ith financial institution according to its level of riskiness in time t.

where Xit−1 (m × 1) is the vector of bank-specific variables (which includes liquid asset to customer deposit and short-term funding, the cost-to-income ratio, leverage, total assets growth, and credit risk), Zit−1 (n × 1) is the vector of macroeconomic variables (which includes GDP per capita, inflation, and nominal exchange rate depreciation), β and γ (m × 1 and n × 1) are vectors of coefficients, and ε it is an error term with various assumptions of distributions made in equations (2) and (3). For financially distressed banks, i = 1; n in time t, Yit is a sequence of 1 for that particular year t and 0 for banks not experiencing financial distress in year t. We substitute equation (2) into equation (1) to derive equation (3) as:

It is also argued in the literature that character indicators or corporate governance mechanisms constitute one of the critical determinants of the financial distress of banks. Thus, equation (3) is adjusted to contain corporate governance variables.

Wit is a vector of corporate governance variables, including CEO duality, outside directors, board size, and board independence. Since the study is a cross-country one, cultural and governance differences may also influence the state of financial distress. Thus, the analysis controls for corruption and government effectiveness in the model.

Where Cit constitutes control of corruption and government effectiveness variables in equation (5). The study then uses logistic regression to estimate equation (5). We estimate the model with the following specifications using the STATA version 15.1 software:

Model Measures

The dependent variable is dichotomous, 1 for financially distressed, and 0 for financially healthy. The literature has already established that there is no universally agreed definition and measurement for financial distress (Appiah et al., 2015). This study adopts multiple criteria for measuring distress. A bank is distressed where (1) Altman’s (1983)Z score is less than 3, and (2) the Capital Adequacy ratio (Equity/Total Assets) is less than 10%. The capital adequacy ratio has been adopted as a technical measure of bank financial distress for the following reasons. First, all the Sub-Saharan Africa countries have enacted laws, highlighting insolvency is inevitable when a bank fails to meet the minimum capital adequacy ratio. Second, the Basel Committee on Bank Supervision has reiterated that capital adequacy is key in detecting bank distress. Moreover, Tomas Žiković (2018) concluded that the legal criterion for distress classification is inadequate in emerging economies because of lax enforcement of bankruptcy laws.

Regarding the explanatory variables, the capital credit rate is represented by leverage (LR), measured as the carrying amount of debt expressed as a ratio over the sum of equity and debt value at the end of the reporting year (Appiah, Gyimah, & Abdul-Razak, 2020). For the collateral variable, the growth of the total assets is the changes in the annual increase in total assets and the banks’ book value of total assets (Zaki et al., 2011). The credit risk equals the loan loss reserve to gross loan, and the non-performing loan ratio is the condition rating of the banks. The GDP per capita equals the gross domestic product per population, inflation is the consumer price index rate, and exchange represents the depreciation of the nominal exchange rate (Aslam & Haron, 2020; Calice, 2014). CEO Duality is a dummy variable indicating whether the CEO is the same as the chairperson of the board of directors, outside directors ratio equals the number of outside directors, board size represents the number of directors and board independence, a binary variable indicating the presence of non-executive directors (Aslam & Haron, 2020; Brekumi et al., 2023;Kyei et al., 2022; Lakshan & Wijekoon, 2012).

The study accounts for the effect of cultural and governance differences across countries with two control variables. The first is control of corruption, an indicator from the World Bank. The control of corruption ranges from −2.5 (least effective or most corrupt) to 2.5 (most effective or least corrupt), which measures the perceptions of how public power is used for personal benefit (Kanapiyanova et al., 2023). Second, the regulatory quality measure also ranges from −2.5 (least effective) to 2.5 (most effective), which measures the government’s ability to develop and apply sound policies and regulations to promote private sector development (Akorli & Adom, 2023). Negative control of corruption and regulatory quality could increase moral hazard, and decrease lending conditions and loan repayments which can increase the probability of bank distress (Kanapiyanova et al., 2023). Table AI (see Appendix) provides the measures for all the variables.

Results and Discussion

Descriptive Statistics of Variables

Table 1 presents the number of observations, mean, standard deviation, and minimum and maximum values of the study’s variables. On board size, the study reports approximately 10 board members with a spread of 5. Also, the outside director’s ratio ranges from no representation on the board to a maximum of 90%. On average, 28.28% of banks’ boards are outside directors. The GDP per capita average grows at 3.69% on the macroeconomic variables at a spread of 2.56%. The exchange rate of depreciation to the US dollar is at an average of 5.68%, with a high spread of 10.81%. Some economies experience a maximum exchange rate depreciation of 34.72%, while others rather have an appreciation of 19.27%. Inflation records an average figure of 9.83%, with a corresponding standard deviation of 4.50. The results indicate a maximum inflation of 22.11% and a minimum of 1.02%. Analysis of corruption and regulatory quality control reveals that control of corruption and regulatory controls are generally weak with an average of −0.623 and −0.422, respectively.

Descriptive Statistics of Variables (N = 228).

Note. aDummy variables: Only frequencies and percentages of the base levels are reported.

Credit risk is measured by loan loss reserve to gross loan (LLRGloan) and non-performing loans to total loan (NPLTL) ratio. The LLRGloan records an average of 8.1%, with a standard deviation of 9.23. The NPLTL ratio records a high average rate of 26.6%, with a wide spread of 72.36, indicating a high rate of non-performing loans across the region. Leverage ratio (LR) and liquid assets to customer deposit and short-term fund (LACF) represent the banks’ long-term and short-term liquidity, respectively. The leverage records a high average rate of 87.07 % with a standard deviation of 13.20, which indicates a highly geared situation. The short-term liquidity has an average of 42.36%, implying that banks could barely meet half of the short-term liquidity demand, and this is a credit risk situation, is due to high withdrawals by depositors.

From the results in Table 2, the mean bank’s size is 877.12 but with a significant standard deviation of 4,138.54, which shows a high spread, confirmed by a wide range of values between 13 and 57,295. Also, total assets growth (TAG) that connotes the collateral of the 5Cs has a mean of 33.94% but with a very high standard deviation of 116.22. Also, some banks record negative total asset growth, with a minimum of 61.05% and a maximum of 1,435.18%. The maximum asset growth looks abnormal, but further checks reveal that most financially distressed banks were later recapitalized. The cost-to-income ratio (CIR) is 103.51%, indicating that expenses or costs exceed income on average. Regarding CEO duality, only four banks representing 1.754% have CEOs that are the same as the chairperson of the board of directors, implying few variations in CEO duality between banks. Finally, for board independence, 27 banks representing 11.842% consist of non-executive directors, indicating that most banks (88.158%) do not have independent non-executive directors.

Comparative Statistics of Distressed and Non-Distressed Banks (N = 228).

Note. aDummy variables: Only the percentages of the base levels are reported.

p-value < .05.

Comparative Statistics

Table 2 presents the comparative descriptive and inferential results between financially distressed and healthy banks used for the study. We employ the t-test to assess the mean difference between the ratio measures, while a chi-square test is used to examine the significant differences across the dummies. From Table 2, except for board size, the t-test of other corporate governance variables is insignificant between distressed and healthy banks. The board size of financially healthy banks is larger than that of financially distressed banks. Further macroeconomic indicators show that GDP per capita, exchange rate depreciation, and inflation have insignificant differences between distressed and healthy banks. However, the averages of financial ratios show a significant difference between financially distressed and healthy banks. For instance, the loan loss reserve to gross loans ratio is significant at 10.6 among financially distressed banks but at a lower rate of 5.12 for financially healthy banks, suggesting that distressed banks tend to have a higher loan loss reserve than healthy banks in proportion to gross loans. Also, the leverage ratio means that healthy banks tend to have a lower percentage of 82.58 than distressed banks, 91.54. However, the t-test on non-performing loans suggests an insignificant difference between distressed and healthy banks. Lastly, both returns on equity ratio (ROE) and cost to income ratio (CIR) significantly differ between distressed and healthy banks. Distressed banks record an opposing average ROE of 20 and an average CIR of 121; both indicate a loss. On the contrary, the financially healthy banks report an average of 9.94 ROE and 86 of CIR, indicating profit. There are material differences between the financial ratios but little difference between corporate governance and macroeconomic variables of distressed and healthy banks in Sub-Saharan Africa.

Diagnostic Tests

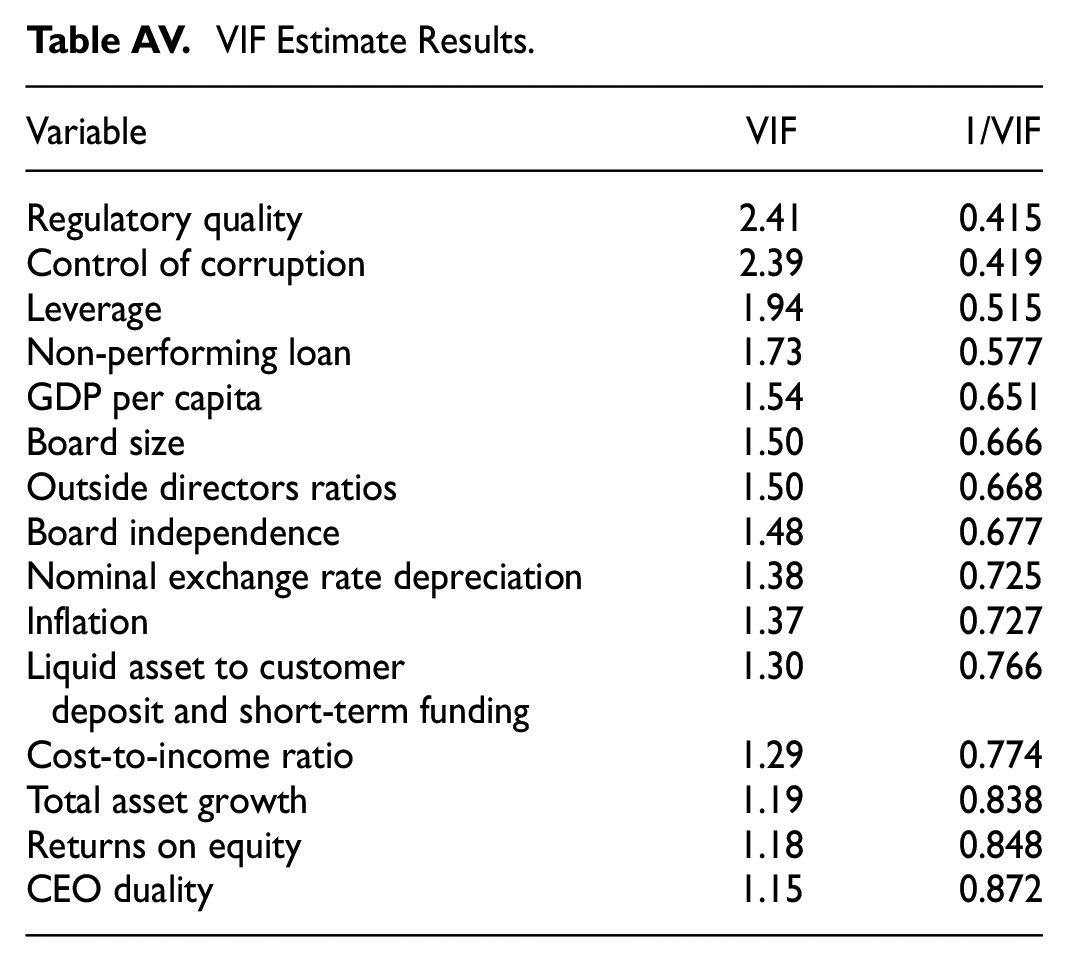

This results of multicollinearity, data normality, and heteroscedasticity. All the VIF record values are less than 10, suggesting no significant collinearity among the regressor (Adom et al., 2020; Gyimah & Lussier, 2021; Jalloh et al., 2019; Sakyiwaa et al., 2020). The VIF results show that there is no problem with multicollinearity (Gyimah et al., 2019). However, the pairwise correlation records a high coefficient of .77 between regulatory quality and control of corruption. We, therefore, drop regulatory quality and non-performing variables because loan loss reserve and control of corruption serve the same purpose in the models. Also, the null hypothesis of the Shapiro-Wilk W test indicates that our data has a normal distribution. Except for CEO duality which we drop, all other variables have a p-value of less than 5%.

One of the critical assumptions of regression estimation is that the error term has to be homoscedastic to ensure unbiased test statistics. Using the Breusch-Pagan/Cook-Weisberg to test for heteroskedasticity under the null hypothesis, we record a Chi-squared of 0.64 with a p-value of .425. We, therefore, accept the null and conclude that there is no heteroskedasticity between distress and the error term. The results for pairwise correlations (Table AII), Shapiro Wilk W test (Table AIII), Heteroskedasticity (Table AIV), and VIF (Table AV) are reported in the Appendix.

Regression Results

Table 3 provides the marginal effect of the logistic regression results without macroeconomic variables, and Table 4 provides the regression results, including the macroeconomic indicators. The results show that none of the character variables (corporate governance mechanisms) affects the probability of bank financial distress in Sub-Saharan Africa. The result is inconsistent with our formulated hypotheses based on extant literature suggesting that board independence, board size and outside directors are the contributing factors to the financial distress of banks in Sub-Saharan Africa. The comparative analysis in Table 3 shows the negligible difference between the financially distressed and healthy banks. Perhaps, the regulatory environment of the banks in the respective countries is not so robust in a way that creates opportunities for manipulation and suspicious deals creating corporate governance mechanisms that are ineffective and insignificant in determining the financial distress of banks in Sub-Saharan Africa. However, the control of corruption has a significant adverse effect on the financial distress of banks without macroeconomic indicators but has no effect when the macroeconomic indicators are introduced.

Results of Bank’s Financial Distress Without Macroeconomic Variables.

Results of Bank’s Financial Distress with Macroeconomic Variables.

The loan loss reserve also significantly influences the probability of banks’ financial distress with or without macroeconomic variables, confirming our hypothesis. Loans constitute a more significant proportion of the bank’s assets, and therefore customers’ default increases the liquidity, leading to financial distress. The leverage ratio also significantly influences banks’ probability of financial distress with or without macroeconomic indicators in Sub-Saharan Africa, confirming our hypothesis. Moreover, we find that the total asset growth positively affects the likelihood of financial distress but is insignificant whether macroeconomic indicators are present (p-value > .05), contradicting our hypothesis. Further, the liquid asset-to-customer deposit ratio does not influence the financial distress of banks in the selected Sub-Saharan Africa regions, contradicting our hypothesis. Finally, the cost-to-income ratio positively influences banks’ likelihood of financial distress in Sub-Saharan Africa, confirming our hypothesis. A low cost-to-income ratio indicates prudent management of a bank’s financial and non-financial resources through strategic measures such as cost minimization and efficiency in operations that lead to high profitability.

Discussion of Findings

We discuss the study’s findings based on the specific objectives, focusing on the logistic regression model results with the macroeconomic indicators and the 5Cs (capacity, capital, collateral, condition, and character). We use cost to income, and liquid assets to customer deposit and short-term funds to measure capacity (the first C). Based on the results in Table 3, we find that the cost-to-income ratio is significant in determining the probabilities of financial distress of banks in Sub-Saharan Africa. Our findings confirm the studies by Distinguin et al. (2010), Le and Viviani (2018), and Zaki et al. (2011) that found similar results. However, the liquid assets to customer deposits and short-term funds show an insignificant impact on the banks’ financial distress probability. This finding agrees with Calice’s (2014) study, where liquid assets to deposits and short-term funding ratios do not influence the probability of financial distress in emerging economies. The leverage ratio represents the measurement of capital (the second C). We also find that leverage has a significant positive impact on banks’ probability of financial distress. The findings agree with Calice (2014), Distinguin et al. (2010), Okezie et al. (2011), and Kalash (2021), that find leverage is a predictor of the financial distress of banks. Further, we find that the total asset growth as a proxy for the third C (collateral) has no significant impact on banks’ probability of financial distress, contradicting Zaki et al.’s (2011) findings that find a significant effect of total asset growth and the likelihood of bank failure in the UAE.

The loan loss reserve to gross loan ratio measures condition (the fourth C). Here, we find that the loan loss reserve to gross loan ratio positively influences banks’ probability of financial distress in Sub-Saharan Africa. The result confirms the findings of Babajide et al. (2015), Bholat et al. (2018), and Zaki et al. (2011), which find that non-performing loans or loan loss reserve to gross loans increases the probability of financial distress of banks.

Following a similar study by Zaki et al. (2011), we also use macroeconomic variables such as GDP per capita, nominal exchange rate depreciation to the US dollar, and inflation to measure conditions. Our results in Table 3 show that GDP per capita and nominal exchange rate depreciation to the US dollar have no significant impact on the probability of financial distress. However, we report a positive relationship between inflation and the financial distress of banks. Our finding supports the theory of inflation and bankruptcy by Gordon and Shoven (1982). Further, our results agree with Liu’s (2009) findings that report a positive nexus between inflation and business failure or distress.

The character variables such as outside director’s ratio, board size, and board independence display an insignificant impact on banks’ financial distress probability in Sub-Saharan Africa’s perspective. The findings agree with Lakshan and Wijekoon (2012) that board size does not appear to be a significant determinant of financial distress, but refute their findings that found that outside director’s ratio and board independence negatively affect financial distress of firms. Ciampi (2015) postulates that a firm with more than 50% outside directors increases the probability of distress. However, Salloum and Azoury (2012) contend that higher outside directors reduce financial distress. These results are due to weaknesses, the quality of outside directors, and low control of corruption in Africa that have weakened the independence of the board and corporate governance practices.

Conclusions

This study assesses the likelihood of banks’ financial distress using a dataset from 228 selected banks from Sub-Saharan Africa regions. The study analyzes a matched sample of 114 financially distressed banks and 114 healthy banks using minimum capital adequacy of 10% and Altman’s (1983) Z-score of below three as criteria for categorizing the financial distress of banks. We use logistic regression to assess the critical determinants of the financial distress of banks in Sub-Saharan Africa. We find that cost-to-income ratios, loan loss reserve to gross loan ratios, and leverage exhibit a significant positive impact on the financial distress of banks in the Sub-Saharan Africa regions. However, per prior studies, the liquid asset to customer deposit and short-term fund and total asset growth ratios are insignificant in predicting the financial distress of banks.

Further, GDP per capita and nominal exchange rate depreciation to the US dollar have no significant impact on banks’ probability of financial distress. Contrary to recent findings from emerging economies, the study provides evidence to support a significant positive effect of inflation on the likelihood of banks’ financial distress in Sub-Saharan Africa. Besides, our results indicate that control of corruption is fragile across Sub-Saharan Africa and is one of the most critical factors influencing the probability of banks’ financial distress. The study concludes that capacity rating variable (cost to income ratio), capital rating factor (leverage), and condition rating variables (loans loss reserve to gross loan ratios, leverage, and inflation) are the critical determinants of banks’ financial distress in Sub-Saharan Africa. However, the collateral and character indicators do not predict the financial distress of banks in Sub-Saharan Africa. Put differently, the character variables (such as CEO duality, board size, and board independence) and collateral variables (such as total asset growth and book value of total assets) do not matter in predicting the financial distress of banks in Sub-Saharan Africa. These findings may be due to regulatory, compliance, and corruption control weaknesses within the governance systems.

The study finds that the cost-to-income ratio significantly affects bank financial distress; therefore, banks should invest in strategies that help reduce costs and increase income. Banks should invest in technologies that help reduce labor costs and enhance efficiency. This should not be done by cutting labor headcount; instead, it should be directed at specific low-performing units or sections. Banks should also improve budgetary controls to avoid waste and maintain costs within the plan.

Furthermore, the study finds that loan loss reserve positively influences banks’ financial distress. Banks should therefore improve their credit control systems and risk management to minimize the rate of non-performing loans. Boards of banks should work to improve internal controls and supervision and avoid insider lending. Banks should raise the standards of credit and risk management systems. Moreover, the study finds that all the corporate governance mechanisms seem insignificant to banks’ financial distress. Central banks in Africa are solely responsible for managing and maintaining sound financial systems, and the doubt about the effectiveness of corporate governance mechanisms and weak corruption controls demands a different approach in the central banks’ supervisory role. Central banks should train and resource their supervisory to ensure that boards of banks are not rendered ineffective due to corruption. The central banks should pay particular attention to banks that record continuous negative returns to equity and high leverage levels. The central banks should have integrated systems that assist them in having direct data on banks for decision-making. Audit firms that compromise their independence should be banned from engaging by any other bank. The research also finds that inflation significantly directly influences banks’ financial distress. Governments should therefore take both monetary and fiscal policies to control inflation.

Furthermore, the study reveals that control of corruption has a significant negative impact on banks’ financial distress. The average value of −0.623 for control of corruption indicates that there is the least effective combating control in sub-Saharan Africa. Corruption contributes to financial distress in banks by undermining trust, distorting economic policies, and facilitating fraudulent activities. Implementing strict anti-corruption measures can help reduce financial distress and promote a healthier banking system. Therefore, the government should provide resources and training to anti-corruption agencies to improve corruption control. Also, global partners such as the World Bank and the International Monetary Fund should channel their support to improve good corporate governance across Sub-Saharan Africa.

Like all other studies, this study also has limitations. For instance, the study neglects other banks from North Africa countries, suggesting that the generalizability of our findings in Sub-Saharan Africa and beyond may be problematic. Future studies may consider analysis across Africa and focus on other corporate governance variables, financial ratios, profitability measures, and macroeconomic indicators. Future studies may also consider developing a model to predict the bank’s failure in Africa. Also, future studies should explore other corporate governance mechanisms that effectively influence the survival of banks across Africa. The findings have also set the debate on the impact of corruption on corporate governance mechanisms that future studies may consider. Assessing the probabilities of financial distress is a remarkable and debatable topic in finance. Thus, researchers may replicate the issue in other continents to add to the extant literature. The concluding word on the determinants of the probability of financial distress is not yet said; further study is welcome.

Footnotes

Appendix

VIF Estimate Results.

| Variable | VIF | 1/VIF |

|---|---|---|

| Regulatory quality | 2.41 | 0.415 |

| Control of corruption | 2.39 | 0.419 |

| Leverage | 1.94 | 0.515 |

| Non-performing loan | 1.73 | 0.577 |

| GDP per capita | 1.54 | 0.651 |

| Board size | 1.50 | 0.666 |

| Outside directors ratios | 1.50 | 0.668 |

| Board independence | 1.48 | 0.677 |

| Nominal exchange rate depreciation | 1.38 | 0.725 |

| Inflation | 1.37 | 0.727 |

| Liquid asset to customer deposit and short-term funding | 1.30 | 0.766 |

| Cost-to-income ratio | 1.29 | 0.774 |

| Total asset growth | 1.19 | 0.838 |

| Returns on equity | 1.18 | 0.848 |

| CEO duality | 1.15 | 0.872 |

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.

Data Availability Statement

Data sharing not applicable to this article as no datasets were generated or analyzed during the current study.