Abstract

This paper investigates the influence of non-financial firms’ involvement in shadow banking on the caliber of corporate innovation. It focuses on Chinese non-financial listed companies between 2012 and 2022 and delves deeper into the mechanism of economic policy uncertainty (EPU) in relation to the interplay between shadow banking and innovation quality. The findings reveal that firms participating in shadow banking activities experience a decline in innovation quality, with a more pronounced effect observed among state-owned enterprises (SOEs) and small and medium-sized enterprises (SMEs). Furthermore, EPU amplifies the negative impact of non-financial firms’ shadow banking on innovation quality. The outcomes of this study hold significant academic value and practical implications for curbing enterprise shadow banking, optimizing resource allocation structures, maintaining economic policy stability, and fostering high-quality businesses development.

Plain language summary

This research looks into how non-financial companies that do secret or unofficial banking (called shadow banking) affect their ability to create new and better products or services (known as innovation quality). It mainly focuses on Chinese non-financial companies listed on the stock market between 2012 and 2022. The study also explores how changes in economic policies (economic policy uncertainty, or EPU) connect to shadow banking and innovation quality. The results show that companies involved in shadow banking often see a drop in their innovation quality. This effect is stronger in companies owned by the government (state-owned enterprises, or SOEs) and in smaller businesses (small and medium-sized enterprises, or SMEs). Moreover, when economic policies are uncertain, shadow banking’s negative effects on innovation become worse. This study is important for understanding how to limit shadow banking, use resources more efficiently, keep economic policies stable, and help businesses develop better.

Keywords

Introduction

According to the World Intellectual Property Organization Innovation Index Report (2020), China ranks 14th globally in terms of innovation level, and in 2019, it secured the top spot for the number of Patent Cooperation Treaty (PCT) patent applications. However, despite the positive trend of increasing innovation scale, the quality of current innovation remains a concern. Key core technologies exhibit a high level of external dependence, highlighting the presence of a “bottleneck,” and there is still a gap between China’s innovation level and that of developed countries. Strengthening independent research and development (R&D) of core technologies and improving innovation quality are fundamental driving forces for both national and corporate competitiveness and long-term development. As the national innovation-driven development strategy advances, various sectors have begun to address the challenge of the “quantity over quality” innovation trap. Understanding the factors that influence innovation quality has become imperative. The existing research has predominantly focused on the influence of institutional support on enterprise innovation quality, considering factors such as innovation incentive policies, the level of financial development, and environmental regulations. These studies have found a significant influence of institutional support on innovation quantity, but there is room for improvement in understanding its effectiveness on innovation quality (Hsu et al., 2014). This suggests that enhancing innovation quality requires not only external environmental support but also the synergistic effect of internal driving forces within companies. The outcomes of this study hold significant academic value and practical implications for curbing enterprise shadow banking, optimizing resource allocation structures, maintaining economic policy stability, and fostering the high-quality development of businesses.

Amidst the promotion of robust development in the real economy, a counter-market economy phenomenon has emerged within Chinese enterprises. Instead of utilizing cash assets for their core production and operational activities, a significant number of real businesses have diverted substantial sums of money toward the financial market in pursuit of profits. Corporate capital, which should serve as the lifeblood for sustainable enterprise growth, is intended to flow into various business endeavors and investment and financing activities, leveraging transactional or precautionary motives. This infusion of capital is expected to provide market advantages, bolster enterprise value, and generate positive economic outcomes. However, a considerable number of enterprises, enticed by the allure of financial advantages, driven by speculative cash-holding motives, have diverted substantial cash assets into the financial market. These enterprises rely on the horse-trading effect inherent in financial resource allocation (Y. Q. Wang et al., 2015). They engage in shadow banking activities, seeking gains through capital arbitrage and assuming the role of “intermediaries” for funds.

Consequently, the prevalence of shadow banking among real enterprises has surged, leading them to become entangled in the swamp of “money speculation.” The involvement of non-financial enterprises in shadow banking, deviating from financial regulations and assuming the role of shadow banks, can adversely affect the substantial economy. This includes promoting the increase of investment requirements (Jafri, 2019), stock price crash risk (Han, Hsu, et al., 2023), reduced efficiency in the allocation of corporate resources (Dakua, 2019), and an increased vulnerability to stock price collapses (Si et al., 2021). These consequences ultimately disrupt normal production and operational activities, as well as impede the long steady development of enterprises. The innovation quality serves as a direct indicator of a company’s sound business condition and is closely linked to stakeholders’ expectations for the company’s future growth. Existing research on innovation quality in firms has mainly been conducted from a macroscopic perspective, such as innovation policy (Oughton et al., 2002), green credit policy (Zhang et al., 2022) and finance and economic development (Hsu et al., 2014). The micro-level aspects have explored topics such as social responsibility, asset allocation strategy (Han, Hsu, et al., 2023), institutional shareholding (Aghion et al., 2013), and industry-academia-research cooperation (Hansen et al., 2022).

Literature on the consequences of shadow banking by non-financial firms presents different perspectives. Engaging in shadow banking could potentially lower financing costs for firms, thereby enhancing their overall financing capacity (Allen & Gu, 2021). The development of shadow banking could contribute to achieving a balance between income and liquidity, providing financial support for firms to pursue innovation. Firms that utilize idle funds for shadow banking activities could benefit from improved capital efficiency and more rational allocation of funds. These well-managed and properly developed shadow banking activities could alleviate financing constraints and facilitate the transformation and upgrading of enterprises (Si & Li, 2022). Non-financial firms holding certain financial assets could reduce interest costs, improve financing capacity, hedge against asset-specific risks, and enhance shareholders’ interests (Baud & Durand, 2012; Demir, 2009). In an ideal scenario, such financial gains can strengthen the core business capabilities of the firm.

Research has shown that the shadow banking activities of non-financial enterprises, operating outside the realm of financial supervision and regulation, are associated with information asymmetry, high leverage, elevated risks, and contagion effects (Jianjun & Xun, 2016). These activities pose significant risks to both the companies involved and the broader economy. Driven by profit-seeking motives, enterprises allocate substantial capital to the financial market, resulting in a decline in innovation output and impeding enterprises’ upgrading and transformation (Bereskin et al., 2018). Furthermore, the shadow banking activities of non-financial firms often manifest as a “crowding-out effect,” diminishing the efficiency of corporate investments and increasing financial market volatility (Orhangazi, 2008; Tori & Onaran, 2018). In addition, it will impacts social welfare and increase the likelihood of risk. Furthermore, it reduces the efficiency of resource allocation (Han, Hsu, et al., 2023) and tends to exacerbate the evolution of financial risks (Hsu et al., 2014). The increase in the number and size of shadow banks can contribute to opportunistic behavior by management. Scholars have also argued that non-financial firms’ involvement in shadow banking can raise financing costs for other small and medium-sized enterprises (SMEs), disrupt social welfare, heighten audit and default risks for firms, and reduce the efficiency of corporate investments (Allen & Gu, 2021; Lu et al., 2015). These findings underscore the fact that shadow banking by non-financial corporations poses significant risks, leading to economic and financial harm.

In recent years, scholars have delved into the repercussions of economic policy uncertainty (EPU) from numerous viewpoints. In terms of macroeconomics, the discussions have revolved around subjects like GDP and carbon emissions (Khan et al., 2022), carbon pricing (Li et al., 2023), news related to climate change (Assaf et al., 2023), renewable energy sources (Yi et al., 2023), and energy markets (X. Wang et al., 2023). Within the microeconomic sphere, investigations have zeroed in on facets such as corporate digital transformation (Cheng & Masron, 2023), managerial sentiment (Ma et al., 2023), green innovations (Cui et al., 2023), audit quality alongside earnings management risk (Lee & Jeong, 2024), and the worth of advertising expenditure (Jabbouri et al., 2024). Nevertheless, there’s been scant investigation on how financialization within non-financial enterprises influences their innovation quality amidst economic policy uncertainty.

The existing literature has extensively examined the consequences of non-financial firms’ engagement in shadow banking. This paper takes a micro perspective to explore the intrinsic connection between “shadow banking” and “innovation quality.” By examining this relationship, it provides a fresh perspective on key issues such as low innovation quality, high debt, and the “de-realization to deficiency” problem faced by Chinese enterprises. Additionally, it aims to investigate the influence of economic policy uncertainty on the connection between nonfinancial corporations’ shadow banking and innovation quality. This research contributes to the standardization of enterprise innovation quality management mechanisms, helps address issues related to insufficient innovation power and low innovation quality, promotes transparency and regulation by government entities, enhances capital allocation efficiency, and provides innovative ideas for high-quality economic development and improved corporate innovation quality.

The remaining sections are structured as follows. Section “Theoretical and Hypothesis” provides theoretical analysis and the research hypothesis. Section “Sample Selection and Variable Definition” introduces sample selection and variable definition. Section “Empirical Analysis and Economic Explanation” discusses empirical analysis and economic explanations. Section “Heterogeneity Analysis” analyzes heterogeneity from the perspectives of scale and ownership. The final section “Research Conclusions and Policy Recommendations” concludes this study and proposes some policy suggestions.

Theoretical and Hypothesis

Shadow Banking of Non-Financial Firms and Innovation Quality

The increasing trend of shadow banking among non-financial corporations has emerged as a significant area of research in the field of financial investment. While on the surface, it represents the allocation of a greater proportion of financial assets on the balance sheets of real firms, its underlying nature lies in the growing influence of financial motives, markets, participants, and institutions in both domestic and international economies. Therefore, the shadow banking activities of non-financial firms fundamentally reflect macroeconomic operations at the micro level and highlight the increasingly prominent role of financial elements in the business development process of real firms. In practice, corporate innovation is characterized by its long-term nature, substantial investment requirements, and inherent risks. It involves a continuous process of accumulation, synergy, and optimization. However, this process often faces challenges such as financing constraints, technological limitations, inefficient resource allocation, and limited commercial application. As a result, their innovation quality is largely determined by sustained investment in R&D and effective innovation management. In summary, the rise of shadow banking among non-financial firms reflects the growing importance of financial elements in the business landscape.

At the same time, their innovation quality depends on overcoming various obstacles and leveraging continuous investment in R&D, as well as efficient innovation management practices. The current academic discourse surrounding the economic consequences of shadow banking by non-financial firms highlights both macro and micro-level effects. At the macro level, most studies take a negative stance, emphasizing that shadow banking activities divert resources from the real economy to the virtual economy, resulting in adverse impacts on economic growth, industrial upgrading, and technological innovation. However, the micro-level effects of non-financial firms’ shadow banking behavior remain subject to debate. Some argue that real enterprises allocate their financial assets to generate higher returns and improve investment efficiency by utilizing idle funds. This approach can reduce financing constraints, enhance operational performance, and contribute to the development of the core business. Conversely, others contend that allocating a significant amount of capital to financial assets instead of real investments can weaken firms’ operational capacity (Tori & Onaran, 2018), hinder technological innovation (Xie et al., 2022), and impede overall productivity. Consequently, the shadow banking activities of non-financial firms can negatively impact their production and business activities, potentially disincentivizing them from engaging in financial markets, particularly in terms of innovation quality.

The inhibition of innovation quality improvement by the shadow banking of non-financial firms primarily stems from the erosion of firms’ intrinsic motivation to invest in innovation. While the outward manifestation is the allocation of scarce funds to financial markets, leading to substitution between financial and innovation investments and a significant reduction in resource allocation for innovation (Kliman & Williams, 2015), the underlying cause lies in the short-term pursuit of high financial returns by corporate management. When capital is shifted from the real sector to the financial sector, yielding higher returns, the capacity for technological innovation is inevitably underinvested, resulting in a struggle to generate high-quality innovation performance. Overall, the shadow banking behavior of non-financial enterprises has complex implications, with potential negative impacts on firms’ innovation quality. By diverting resources from the real sector to the financial sector, it can crowd out investments in technological innovation and hinder the generation of high-quality innovation outcomes. Based on the aforementioned analysis, hypothesis H1 is presented in this paper:

H1: The shadow banking of non-financial firms reduces the quality of their innovation.

Economic Policy Uncertainty, Shadow Banking of Non-Financial Firms and Innovation Quality

The shadow banking activities of non-financial companies exhibit certain characteristics such as incomplete information, high-leverage, high-risk, and high contagiousness. If not managed properly, these activities can have a negative impact, particularly for enterprises with limited risk resilience. This negative impact can worsen the feedback loop between the financial market and the real economy, hindering the high-quality development of our economy (Qian et al., 2017). Non-financial companies engage in shadow banking through various means, such as cooperating with financial intermediaries or directly participating in financial activities. Cooperation with financial intermediaries involves activities like entrusted loans and entrusted wealth management, while direct participation encompasses traditional commercial credit, bridge loans, and innovative equity investments. Notably, entrusted loans have experienced rapid growth in China in recent years, representing a distinct form of shadow banking. In this arrangement, enterprises entrust banks to issue, oversee the utilization of funds, and assist in their recovery, enabling the reallocation of funds among enterprises. However, bridge loans, characterized by excessively high interest rates and supervision challenges, pose significant risks.

There are several key theories regarding the impact of EPU on non-financial firms’ involvement in shadow banking. Firstly, the real options theory suggests that EPU increases the business risk for non-financial firms. In the face of uncertainty, the value of a firm’s waiting option rises, leading to a reduction in fixed investment as firms become more cautious (Bloom, 2009; Rodrik, 1991). Secondly, macroeconomic uncertainty can widen the risk gap between financial and real investments, resulting in a higher risk-adjusted real rate of return on financial assets. This can incentivize non-financial firms to allocate more resources toward financial investments. Thirdly, when EPU intensifies, banks tend to decrease lending to SMEs and favor state-owned enterprises (SOEs) or large firms. This leaves SOEs or large firms with more idle funds, allowing them to engage in shadow banking activities, such as entrusted lending (Huang et al., 2015). Moreover, the real options theory has gained prominence in academic research as one of the widely accepted theories on uncertainty’s impact on corporate investment (Gulen & Ion, 2016). This theory is based on the assumption of investment irreversibility and suggests that firms, when facing increased uncertainty, reduce investment spending and defer investment decisions until more information becomes available. In particular, corporate R&D expenditure, characterized by earmarking and higher investment irreversibility compared to other investments, tends to decrease when firms encounter EPU, leading to a reduction in corporate innovation investment.

EPU refers to the presence of inconsistencies in industrial development, tax policies, and industry guidelines, which can increase the risk of business losses and bankruptcy. When EPU rises, firms become uncertain about the returns on their technological innovation, reducing their motivation to pursue market consolidation through R&D efforts. This, in turn, hampers firms’ incentives to innovate in their core business. As a result, the lower returns on R&D investment make shadow credit assets, which offer higher returns on investment, an attractive option for management to enhance profitability. Consequently, there exists a negative connection between the shadow banking activities of non-financial firms and the quality of innovation. With increased EPU, firms are less incentivized to engage in R&D innovation. However, the relatively higher returns associated with shadow banking activities make management more inclined to allocate funds to such activities, considering them a more profitable alternative. Therefore, the scale of shadow banking becomes a stronger indicator of financial activities rather than R&D innovation, leading to a decline in the quality of corporate innovation. Based on this analysis, hypothesis H2 is presented in this paper:

H2: As economic policy uncertainty increases, the dampening effect of shadow banking by non-financial firms on their quality of innovation will strengthen.

Sample Selection and Variable Definition

Sample Selection and Data Processing

This paper utilized an initial sample of listed companies in the Shanghai and Shenzhen A-shares from 2012 to 2022 to investigate the validity of the proposed hypothesis. The financial data of these listed companies were sourced from the Wind and CSMAR databases. To ensure the sample’s credibility and representativeness, the data underwent the following processing steps. Firstly, listed companies in the financial and public utility sectors, as well as those categorized as ST and *ST, were excluded. Secondly, companies with significant missing or abnormal values in their financial data were also removed. Additionally, to mitigate the impact of extreme values, a two-sided 1% tail reduction (Winsorization) was applied to all continuous variables. Following these data processing steps, a total of 17,495 firm-year observations covering the period from 2012 to 2022 were obtained for the analysis.

Dependent Variable

The innovation quality in this study was assessed using a measure known as “Innovation Quality” (LnCit), which was based on the methodology employed by Rong et al. (2017). LnCit represents the natural logarithm of the total number of citations received by a company’s patents in the subsequent year. A higher value of LnCit indicates a higher level of innovation quality.

Explanatory Variable

Corporate shadow banking (shban): In previous studies, researchers have commonly used two proxy variables, namely “substantive credit intermediation” and “shadow credit chain,” to represent the shadow banking activities of non-financial firms (Gu et al., 2024; Han, Feng, & Li, 2023). “Substantive credit intermediation” is derived by aggregating the sizes of entrusted loans, entrusted finance, and private lending. Entrusted loans are reflected in accounting accounts such as “other current assets,”“other non-current assets,” and “non-current assets with maturity within one year” (Han, Feng, & Li, 2023). The data on entrusted wealth management activities can be obtained from Guotaian’s database, while other forms of private lending, such as bridge loans, are often recorded under the accounting account of “other receivables.” Given the inherent secrecy of private lending, the “other receivables” account can serve as a proxy variable to measure private lending and complement the estimation of fund transfers among enterprises (Jiang et al., 2010). On the other hand, the “shadow credit chain” primarily involves non-financial enterprises participating in the credit creation chain of the shadow banking system by investing in financial products such as bank wealth management, brokerage wealth management, trust products, and structured deposits offered by mainstream institutions. The data on the “shadow credit chain” activities of non-financial firms can be obtained by examining the breakdown of the “other current assets” category in the financial statements’ notes (Han, Feng, & Li, 2023). In this paper, the proxy variables for shadow banking activities by non-financial firms were calculated as the sum of the sizes of the two types of shadow banking operations, expressed as a proportion of total assets.

Moderating Variable

Economic Policy Uncertainty (EPU): The China Economic Policy Uncertainty Index, referring to Baker et al. (2016) and Ashraf et al. (2022), was created using a keyword search approach applied to the South China Morning Post. This index has been extensively utilized and tested in academic circles, demonstrating a certain level of stability and validity. For this study, the data were obtained by manually calculating the annual arithmetic mean from the monthly data and subsequently dividing the values by 100 to maintain consistency with the empirical data.

Control Variables

In order to address the issue of omitted variable bias, this research incorporates findings from various scholars, including Love et al. (2007) and J. Wang et al. (2024). Several control variables were selected to mitigate this bias, namely firm size (Size), gearing ratio (Lev), return on net assets (ROE), the proportion of independent directors (Indep), dual role (Dual), percentage of top shareholder ownership (Top1), TobinQ, year of establishment (Age), management expense ratio (Mfee), total asset turnover ratio (ATO), cashflow ratio (Cashflow), growth in operating income (Growth), and the number of directors (Board). These control variables were chosen to ensure objectivity and scientific rigor in the research outcomes. Additionally, the paper includes fixed effects for year (Year) and industry (Ind), as defined in Table 1, to further enhance the reliability of the results.

Definition of Main Variables.

Model Construction

Based on the above-mentioned analysis, in order to explore the influence of non-financial firms’ shadow banking system on innovation quality, the following panel regression model was constructed using a fixed effects model:

where LnCit is a proxy variable for innovation quality, shban represents shadow banking of non-financial firms, and EPU represents economic policy uncertainty.

Empirical Analysis and Economic Explanation

Descriptive Analysis

Table 2 presents the descriptive statistics for the key variables. The mean value of LnCit, representing firm innovation quality, is 2.565, with a standard deviation of 1.618. These figures indicate substantial variations in innovation quality among the sampled firms. The maximum value of shadow banking (shban) for non-financial firms is 1.492, while the minimum value is close to 0, suggesting significant differences in shadow banking activities across the sample firms. The mean value of 0.144 indicates that shadow banking constitutes a considerable proportion of total assets for non-financial firms, potentially impacting their core operations. The average EPU index is 2.24, with a minimum value of 0.98, a maximum value of 3.784, and a standard deviation of 0.964. These findings illustrate substantial year-to-year variations in EPU.

Descriptive Statistics of Main Variables.

Multiple Regression Analysis

Shadow Banking of Non-Financial Firms and Innovation Quality: Baseline Regression

In this study, a panel fixed effects model is employed to examine the impact of non-financial firms’ involvement in shadow banking on innovation quality. The results of this analysis are presented in Table 3. Column (1) of the table displays the outcomes without the inclusion of any control variables. The coefficients associated with the effect of shadow banking on innovation quality are negative and statistically significant at the 1% level. This suggests that engaging in shadow banking activities by non-financial firms negatively affects their own innovation quality when not considering other control variables. This finding supports the research hypothesis H1 of the paper. Column (2) presents the results after incorporating the control variables. It can be observed that although the coefficient values slightly decrease, the sign remains unchanged. The coefficient pertaining to the impact of non-financial firms’ engagement in shadow banking activities on innovation quality remains significant. This indicates that the conclusion regarding the suppressive effect of shadow banking on innovation quality for non-financial firms is robust and reliable.

Baseline Regression Results for Shadow Banking of Non-Financial Firms and Quality of Innovation.

Note. ***, **, and * denote significance at the 1%, 5%, and 10% levels, respectively, the values in parentheses are t-values, as below.

Economic Policy Uncertainty, Shadow Banking of Non-Financial Firms and Innovation Quality

In order to delve deeper into the influence of EPU on the connection between shadow banking of non-financial firms and innovation quality, this paper introduces an interaction term between shadow banking of non-financial firms and EPU into the benchmark model. The regression results are presented in Table 4. The coefficient associated with the interaction term (shban × EPU) between EPU and shadow banking of non-financial firms is found to be significantly negative at the 1% level. This indicates that heightened EPU intensifies the adverse relationship between shadow banking of non-financial firms and innovation quality. Consequently, the research hypothesis H2 is supported by the findings.

Economic Policy Uncertainty, Shadow Banking of Non-Financial Firms, and Quality of Innovation.

Note. *** denote significance at the 1% level.

Robustness Test

Endogenous Problem Handling

Lagged Treatment of Explanatory Variable

To address the potential endogeneity issue arising from the reverse causality between “higher innovation quality leading to lower levels of shadow banking by non-financial firms,” this paper employs a one-period lagged regression approach for the explanatory variable. The regression results are presented in Table 5. Upon examining the results, it can be observed that the signs and significance levels of the variables have not significantly changed. This outcome provides stronger confirmation regarding the robustness and validity of the findings obtained in this study. By utilizing the one-period, two-period regression analysis, the paper effectively mitigates concerns related to endogeneity, thereby enhancing the credibility and soundness of the research outcomes.

Lagged Order Treatment of Explanatory Variable.

Note. *** denote significance at the 1% level.

Propensity Score Matching Method

In the first step, the dataset was divided into two groups based on the degree of shadow banking among non-financial firms. The treatment group (H_shban = 1) consisted of samples with a higher degree of shadow banking (shban ≥ 0.046), while the control group (H_shban = 0) consisted of samples with a lower degree of shadow banking (shban < 0.046). The median was used as the criterion for classification, and the control variables were employed as matching variables. In the second step, dummy variables were created to represent the groups, and propensity score values were calculated using a logit model. Three matching methods, namely one-to-one nearest neighbor matching, radius matching, and kernel matching, were utilized to match the samples based on the propensity scores. Finally, the matched samples were separately regressed, and the regression results are presented in Table 6. It can be observed that the coefficients associated with shadow banking by non-financial firms are all significantly negative. This indicates that the conclusions drawn in this paper’s hypothesis remain valid. The results support the notion that there is a negative connection between shadow banking by non-financial firms and innovation quality, even after employing propensity score matching to address potential selection biases.

Propensity Score Matching.

Note. *** denote significance at the 1% level.

Instrumental Variable Method

To mitigate the potential endogeneity issues stemming from omitted variables, this paper adopts a strategy of employing instrumental variables. The approach was inspired by the works of El Ghoul et al. (2011). Specifically, the instrumental variable (IV_shban) selected is the average value of shadow banking among other firms within the same industry as the focal firm. The rationale behind this choice is that the average shadow banking level of other non-financial firms in the same industry is likely to be correlated with the shadow banking level of the focal firm. However, it is assumed that this instrumental variable does not directly impact other firm behaviors, satisfying the two conditions required for a valid instrumental variable. In order to estimate the parameters of the instrumental variable, the two-stage least squares (2SLS) method was employed. This approach helps to attenuate the influence of endogeneity issues and provides more robust estimates of the relationships under investigation. By incorporating instrumental variables into the analysis, this paper aims to address the potential endogeneity concerns and enhance the validity and reliability of the research findings.

The regression results obtained from the 2SLS method are presented in Table 7. Column (1) displays the results of the first stage regression, which is a crucial step in the 2SLS approach. It can be observed that the estimated coefficients of the instrumental variables are significantly positive at the 1% level of significance. Furthermore, the Wald F-statistic associated with the first-stage regression is substantially greater than 10, indicating a strong correlation between the instrumental variables and the endogenous explanatory variables. This suggests there is no issue of weak instrumental variables in this analysis. Column (2) shows the regression results of the second stage of 2SLS, which suggests that the negative connection between shadow banking of non-financial firms and innovation quality still holds and the significance remains unchanged. It follows that the shadow banking of non-financial firms reduces their innovation quality, in line with the conclusions obtained in the previous section.

Regression Results for Instrumental Variables.

Note. *** denote significance at the 1% level.

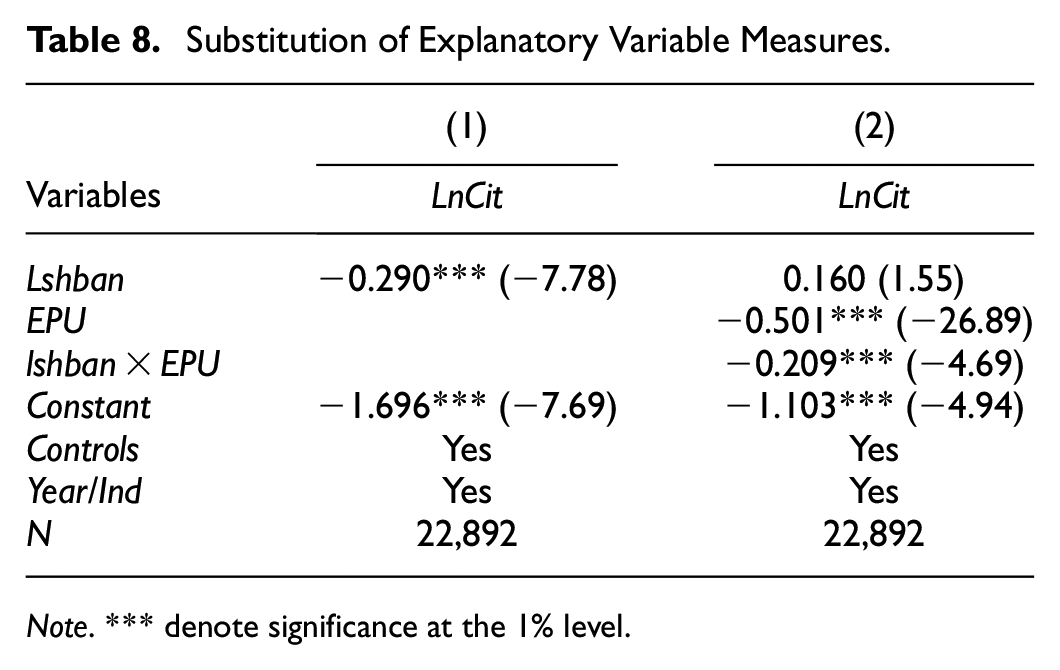

Metric of Replacement Variables

In the previous analysis, the measurement of shadow banking among non-financial firms was based on the sum of various financial indicators as a percentage of total assets. However, in this paper, a different measurement method is adopted. Specifically, let lshban = (other current assets + entrusted wealth management amount + other receivables)/total assets; it is utilized as a replacement explanatory variable. In addition, a cross product term is introduced in the analysis. Table 8 lists the regression results incorporating these modifications. It can be seen that the regression results remain largely unchanged after changing the variables.

Substitution of Explanatory Variable Measures.

Note. *** denote significance at the 1% level.

Replacement of Regression Method

Firstly, based on the descriptive analysis conducted above, it is evident that the innovation quality data for all enterprises analyzed in this study show positive values and follow a mixed characteristic resembling a continuous positive distribution. In order to further examine the impact of non-financial firms’ shadow banking on innovation quality, this paper employs the Tobit model. Additionally, to more effectively address endogeneity concerns, the higher-order joint fixed-effects approach of Moser and Voena (2012) is applied, specifically controlling for “time × industry.” The findings in Table 9 demonstrate that non-financial firms’ shadow banking undermines the quality of their innovation, which aligns with the findings discussed in the previous section.

Tobit Model + Higher Order Fixed Effects.

Note. *** denote significance at the 1% level.

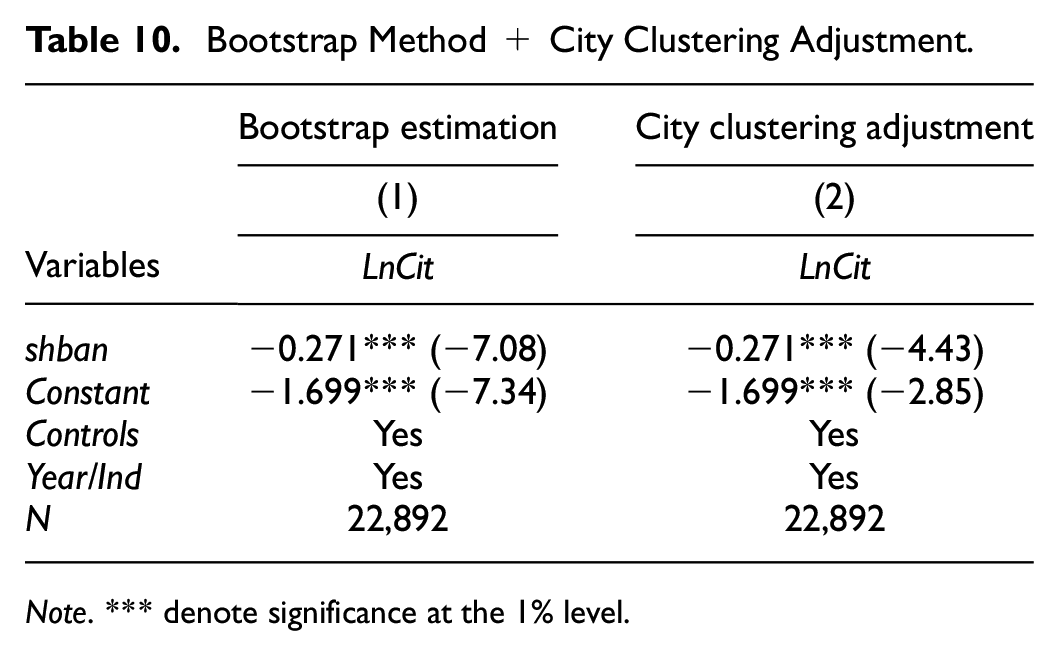

Secondly, in order to mitigate potential biases in statistical results stemming from sample self-selection, this study incorporates the Bootstrap self-sampling method for parameter estimation. This method enhances the validity and consistency of parameter estimation results by iteratively sampling from the original sample multiple times to attain an unbiased asymptotic distribution. Analyzing Column (1) of Table 10, it becomes apparent that the coefficient associated with the impact of non-financial firms’ shadow banking on innovation quality is significantly negative. This finding reinforces the notion that firms involved in shadow banking are capable of significantly diminishing innovation quality.

Bootstrap Method + City Clustering Adjustment.

Note. *** denote significance at the 1% level.

In addition, recognizing the potential mutual influence among listed companies within the same city regarding innovation quality, this study applies city-level clustering adjustment by employing clustered standard errors. The updated regression outcomes are presented in Column (2) of Table 10. The results reveal that the coefficient for the variable shban remains significantly negative at a 1% level of significance. This signifies that non-financial firms involved in shadow banking can indeed substantially diminish the quality of their innovations. These findings further strengthen the robustness and reliability of the previous conclusions.

Heterogeneity Analysis

Analysis Based on Different Ownership

In China, SOEs enjoy a closer relationship with the government and benefit from stronger financing advantages. These SOEs have greater access to the implicit guarantee of credit provided by the state or local government. They receive financial support from government agencies and can secure substantial amounts of funding from banks and other financial institutions, exceeding their actual business needs. In contrast to non-SOEs, SOEs possess significant political resources and often rely on the government as a “guarantor.” This eases their budget constraints and enables them to attract credit support from banks through government platforms. Consequently, SOEs can effectively overcome financing difficulties and avoid capital constraints. Therefore, despite investing a significant portion of their capital in shadow banking activities, SOEs have access to ample funds through government and bank support (platform support, and credit support) to sustain their investment in innovation R&D. Consequently, the inhibitory effect of shadow banking activation on innovation investment within SOEs is not significant, and the likelihood of business risks is extremely low. On the other hand, non-SOEs lack the inherent advantages of SOEs, and their investment decisions are highly susceptible to financing constraints and business risks. In summary, the negative impact of corporate shadow banking on innovation quality is not significant in the case of SOEs.

In order to examine the potential variations in the impact of shadow banking on innovation quality based on firm ownership heterogeneity, this study categorizes the sample firms into two groups: SOEs and non-SOEs. The regression results, presented in Table 11, shed light on this analysis. The findings indicate that the detrimental effect of shadow banking on innovation quality is more pronounced among non-SOEs. In essence, the impact of shadow banking is more pronounced in non-state-owned enterprises. These regression results suggest that heterogeneity in firm ownership significantly affects the relationship between shadow banking and innovation quality.

Regression Results for Different Ownerships.

Note. *** denote significance at the 1% level.

Analysis Based on the Impact of Different Scales

The influence of scale on business development should not be overlooked, as it can vary across different firms and affect their investment and financing behavior. In general, larger enterprises with substantial organizational structures and extensive business operations tend to face higher agency costs and more intricate internal control challenges. As a result, they are more inclined to participate in shadow banking activities, which can ultimately impact their innovation quality. In this study, the median firm size in the sample is used as the threshold to distinguish between large-scale enterprises and small-scale enterprises. Subsequently, separate regression analyses are conducted on each sub-sample. This approach facilitates a more focused examination of the relationship between scale, shadow banking, and innovation quality.

The regression results examining the impact of shadow banking by non-financial firms on innovation quality across different subsamples are presented in Table 11. The findings indicate that shadow banking activities by non-financial firms significantly diminish innovation quality, particularly in small-scale firms. This difference may arise due to several factors. Firstly, smaller firms typically operate with higher levels of risk and possess less transparent information, which inherently leads to underinvestment in innovation. Secondly, engaging in shadow banking amplifies the risk of default, while corporate innovation represents a high-risk, long-reward cycle of R&D. Consequently, shadow banking has a more pronounced detrimental effect on the quality of innovation for smaller firms.

Research Conclusions and Policy Recommendations

In the current era of state-driven high-quality development, enterprises play a crucial role in advancing the real economy. Quality innovation serves as a key driver for transforming the mode of economic development and achieving high-quality growth. However, in recent years, the financial industry has experienced rapid growth and higher investment returns, leading to an increasing number of real enterprises participating in shadow banking activities. This trend not only contributes to the “de-realization” of the real economy but also significantly impacts the innovation quality of these enterprises. Against this backdrop, this paper conducted an empirical analysis to examine the impact of shadow banking by non-financial firms on their innovation quality. The study utilized financial data from China’s A-share non-financial listed companies as the research sample, covering the period from 2012 to 2022. Additionally, the research delved into the influence of EPU on the connection between shadow banking and innovation quality for non-financial firms.

The findings presented in this paper demonstrated that when non-financial firms transitioned from industrial production to involvement in shadow banking, this transition adversely affected the quality of their innovation. Moreover, the negative impact of shadow banking on innovation quality was further amplified by EPU. These conclusions held true even when alternative indicators for the main variables were used, different modeling methods were employed, other shocks were controlled for, and potential endogeneity concerns were taken into account. Additionally, the analysis of heterogeneity revealed that the detrimental effect of shadow banking on innovation quality was particularly pronounced among SOEs and small-scale firms.

Based on the aforementioned findings, the following policy recommendations are proposed. Firstly, it is imperative for tangible enterprises to concentrate on their core business activities, augment investments in product innovation, and strive to improve management effectiveness and operational efficiency. Proactive measures must be adopted to mitigate the effects of “shadow banking” and other high-risk financial investment practices. Companies should also focus on strengthening their internal control and supervision systems to fulfill their supervisory role effectively. Managers should adopt a long-term strategic perspective rather than succumbing to short-term considerations.

Secondly, relevant government departments and policy implementation bodies should closely monitor companies’ investment activities and scrutinize their involvement in shadow banking. Strict controls should be implemented to limit the proportion of investments companies make in shadow banking, thus preventing excessive reliance on “shadow” practices that could hamper innovation quality. It is crucial to discourage disinvestment tendencies. Furthermore, the government should adjust and formulate economic policies in a timely manner to ensure their effectiveness, continuity, and sustainability in achieving desired economic objectives.

Thirdly, at the societal level, greater support for the financial market should be provided to expand financing channels and enhance fund distribution. Efforts should be made to overcome discriminatory practices driven by “intra-system” factors that hinder fair access to funds. The development and improvement of inclusive financial markets for all types of entities are essential to curb non-financial enterprises’ utilization of illicit channels like underground funds for engaging in “shadow banking.” This will help mitigate the negative impact on corporate innovation resulting from the accumulation of “bad news.” These measures hold positive implications for enhancing internal corporate governance efficiency, reducing information asymmetry, improving innovation quality, and maintaining financial market stability.

In addition, this paper has the following research shortcomings. For instance, the research presented here does not take into account the possibility that financial environment variability might yield different outcomes. Simultaneously, while examining the impact of shadow banking activities on the quality of innovation, the paper inadequately considers elements such as firm-specific characteristics, industry dynamics, etc., which could potentially influence their correlation. Furthermore, it fails to address how policy uncertainty might mediate the effect of shadow banking on the quality of innovation. These are aspects that the authors intend to further explore in their subsequent research.

Footnotes

Acknowledgements

We thank the editors and anonymous reviewers for their helpful suggestions.

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: This paper was supported by general research project of Southwest University of Political Science and Law “Research on the Promotion Mechanism of High-level Opening of Securities Industry for the Innovation and Development of Entity Enterprises” (Grant No. 2023XZZXYB-12); Southwest University of Political Science and Law School of Economics 2022 Bidding Project (Grant No. XYZB202217); Science and technology project of Chongqing Municipal Education Commission (Grant No. KJQN202200317).

Data Availability Statement

The data that support the findings of this study are available from the corresponding author upon reasonable request.