Abstract

Much of the university spin-offs (USOs) literature either focuses on the influence of parent universities or the external environments on enterprise performance in economies with one aspect almost always neglected, that is, the role of USOs’ corporate governance. In this study, we examine the effects of USOs’ corporate governance structure which includes equity structure, board size and organizational form, on enterprise performance in a Chinese context, as well as the moderating effect of human capital on the relationship between board size and enterprise performance. This study takes 150 enterprises in 42 universities in Hubei Province as samples in 2017 using the weighted least square (WLS) method. The research finds evidence of positive relationships between equity structure and enterprise performance, as well as between board size and enterprise performance. However, a positive effect is not found between organizational form and enterprise performance, which shows a prominent negative effect. Moreover, human capital which is partially positive, influences the relationship between board size and enterprise performance. Therefore, these findings add some potentially noteworthy dimensions to the USOs literature that are especially important to USOs’ policy makers and other stakeholders.

Introduction

With the advent in the era of the knowledge economy, universities are increasingly making a contribution to the social and economic development through different conduits such as creating university spin-offs (USOs), which are defined as new firms based on university-developed knowledge, either founded by entrepreneurial academics or with an equity participation of the parent university, or both (Ben-Hafaïedh et al., 2021; Fini et al., 2011; Fryges & Wright, 2014; Tagliazucchi et al., 2021). USOs can provide both highly skilled human capital and continuous support of knowledge creation and knowledge spillovers. Consistent with the opinion of entrepreneurial knowledge spillover theory (Acs et al., 2009), this leads to a positive spillover of innovation and economic growth to the local environment (Audretsch et al., 2014; Yuan et al., 2023a, 2023b). Commercializing ideas generated from incumbent organizations (such as universities) by creating a new company, entrepreneurs turn into channels for knowledge spillover as well as for innovative activities while improving economic performance through resource allocation (Meoli et al., 2017).

USOs can be divided into two types from a Chinese context: University-Led and Individual-Led (Xia et al., 2010). University-Led refers to enterprises developed by a government-university partnership or at least a non-inventor agency designated by the university, while Individual-Led refers to enterprises developed by academic inventors. USOs discussed in this article are the University-Led type because they usually have some unique properties. Firstly, board members in USOs usually need to hold dual positions both in universities and enterprises. Most USOs do not set up a shareholders' meeting due to the small number of shareholders. Secondly, the business purpose of USOs is different from other enterprises as they are established as an organization not merely for profit (Zheng, 2018), but their primary function is to commercialize technology with the strengths of talents and technologies that serve society (J. Li & Yu, 2013; Zhu, 2013). Thirdly, in particular, the business model of USOs is based on the combination of commercialization and institutional goals, where USOs have already become part of the university administration structure. This implies that USOs should obey not only the prevailing market system and laws, but also the rules and regulations of parent universities (Fang, 2017; Yan & Peng, 2019).

Despite spin-offs often outperforming other types of new firms in terms of employment and firm value (Acedo et al., 2006; Chatterji, 2009; Dahl & Reichstein, 2007; Fackler et al., 2015), numerous spin-offs are still struggling with low enterprise performance (Harrison & Leitch, 2009; Wennberg et al., 2011). China’s USOs have been improving their performance through continuous system reforms, and while growth ability has been greatly improved, there are still many problems of corporate governance in USOs, such as unclear property rights, incomplete management systems, chaotic financial management and imperfect oversight systems (Lin, 2019; F. Wang, 2017; Zhong, 2016). These lead to USOs’ enterprise performance results which are inferior compared to enterprises in the domain.

Hence, as many scholars have reached a consensus on the idea that USOs promote economic development (Audretsch & Lehmann, 2005; Meoli et al., 2017; Sciarelli et al., 2020), they began to think about the development of USOs, for example, discover what factors determine the momentum and competitiveness of USOs. Creating high-performance USOs has become a key strategic focus for many universities and policymakers (Pitsakis et al., 2015), and has been extensively researched (Fini et al., 2011). In general, a USO’s performance (e.g., lower risk rates, higher corporate valuations) is influenced by the size, institutional characteristics and support from resources (e.g., talents, finance and social relations) of parent universities (Andersson & Klepper, 2013; Colombo et al., 2009; Link & Scott, 2005; Siegel et al., 2004; Xia et al., 2010), which are influential factors from the parent universities’ organizational-level. Additionally, a USO’s performance is affected by external environments too, such as local-context support mechanisms, regional market conditions and local laws and policies (Cui et al., 2011; Diánez-González & Camelo-Ordaz, 2015; Kroll & Liefner, 2008; Michael et al., 2007; Mustar & Wright, 2009; Rasmussen et al., 2014; Xia et al., 2010).

Unfortunately, although existing studies on USOs have found that corporate governance is related to corporate performance (Gao & Wang, 2006; Selarka, 2014; Yang, 2014; Yang et al., 2007; Zhang, 1996), the research on the role of corporate governance variables at the company level is not as in-depth. The core of modern enterprises and corporate governance is the premise and guarantee for the high-quality development of enterprises. It cannot only alleviate agency conflicts, but also play a positive role in inhibiting the opportunistic behavior of management. Therefore, there may be internal management confusion, damage to shareholders' and employees' rights and interests that once ignored corporate governance. As a result, the polarization of employees' business level and work attitude is intensified, the separation between owners and control rights is deepened, and the risk of group governance is relatively higher. Enterprises must pay attention to corporate governance. The differences in governance concepts, capabilities, and levels directly affect the company's decision-making capabilities, operational efficiency, and organizational capabilities. This in turn affects performance where the overall development of Chinese USOs is not ideal from the practical point of view, and corporate governance is one of the main reasons leading to this problem (Jia, 2012). Therefore, this study addresses the following research question: How does the corporate governance structure of USOs influence enterprise performance in the Chinese context?

The paper is structured along the following lines: “Theoretical Analysis and Hypothesis” section provides a brief review of the literature on corporate governance structure and puts forward the hypothesis. “Methodology” section explains the data source and constructs models. “Results” section analyzes the empirical results. The final section discusses and concludes the paper.

Theoretical Analysis and Hypothesis

Corporate Governance Structure

Agency theory refers to the reshuffling of the management of the target company through mergers and acquisitions to solve agency problems of the target company (Nyberg et al., 2010; Solomon et al., 2021). Agency theory pointed out that the separation of control and ownership results in the divergence of interests between shareholders and managers (Ballantine et al., 1932). The goal of shareholders is to gain investment returns but managers usually have other goals, such as enhancing power and reputation. Furthermore, Ballantine et al. (1932) revealed that the separation of ownership and control has an adverse effect on the corporate governance structure. Efficient and effective corporate governance may help reduce agency costs caused by the separation of ownership and control by adjusting the interests between shareholders and managers. This in turn helps to facilitate the progress of corporate governance reform to improve enterprise performance (Owusu, 2012).

Corporate governance structure refers to the institutional arrangement in which corporate shareholders (owners) supervise, motivate, control and coordinate the company's management and performance in order to achieve their own operational objectives (Gyimah et al., 2021; Yunpeng & Zhentao, 2019). It can directly reflect the development direction of the enterprise and the relationship between different stakeholders. OECD referred corporate governance structure as a series of relationships among a company’s board of directors, management team, shareholders and other stakeholders. It provides the structure through which the objectives of the company are set and the means of attaining those objectives and monitoring performance are determined. Zhang (1996) argued that corporate governance structure refers to a set of legal, cultural and institutional arrangements related to the distribution of corporate control rights and residual claims. Therefore, efficient and effective corporate governance is conducive to long-term development of the enterprises by boosting stability and enterprise performance (Beiner et al., 2006; Black et al., 2006; Mallin, 2008). Firstly, efficient and effective corporate governance can broaden the financing channels of enterprises and increase opportunities for enterprises to obtain external financing. Secondly, it can optimize the distribution of capital, labor, other resources and reduce the cost of resource distribution. Thirdly, this can allow corporate governance to assist companies in avoiding a financial crisis and respond more efficiently to crises. Fourthly, it helps to improve the relationship between all stakeholders, thus improving labor relations (Bebchuk et al., 2009). Furthermore, efficient and effective corporate governance can effectively reduce agency costs and conflicts of interest as well as mobilize employee enthusiasm (Figure 1).

Corporate governance structure and enterprise performance.

The corporate governance structure includes three levels of institutional arrangements: owner, management and governance (Chen & Wang, 2008). In this research, we choose equity structure, board size and organizational form related to these three levels in order to test the impact of corporate governance structure on enterprise performance.

Equity Structure and Enterprise Performance

Equity is often emphasized as a relatively strong connection between co-partners that promotes resource and knowledge transfer by reducing transaction costs and improving organizational relations (Rachelle, 2007). In the context of this study, equity constitutes a strong formal connection between USOs and their parent universities, including a continuous exchange of resources and interests (Andy et al., 2003; Bray & Lee, 2000; Dante & Scott, 2003).

A high equity ratio of a parent university in a USO shows a strong formal connection for several reasons. Firstly, with the increase of the equity ratio of parent universities in USOs, parent universities have stronger control and influence over USOs thereby strengthening the coordination ability of the two parties. Secondly, due to the fact that most USOs’ managers are playing a dual role in both the parent university and spin-off, it is conducive to the linkage of interests between the two parties thereby reducing potential interest conflicts. In addition, parent universities can obtain remuneration from spin-offs for the use of universities-invented intellectual property (Bray & Lee, 2000; Maryann et al., 2002). Hence, holding equity ownership usually keeps parent universities and their respective spin-offs consistent in transforming technologies and product innovation (Maryann et al., 2002). Furthermore, given the particularity of academic knowledge, equity-based linkages between universities and spin-offs can reduce information asymmetries and increase trust between the two sides, so as to create optimal conditions for parent universities to accept endowments and incentivize spin-offs to accept knowledge transfer, promote resources transfer and knowledge sharing (Grant, 1996; Sleptsov et al., 2013).

In general, parent universities’ equity ownership in USOs legitimizes universities to provide resources to spin-offs, such as the provision of tangible resources (e.g., labs and equipment) and intangible resources (e.g., knowledge, technology, relationship networks) (Rasmussen & Borch, 2010; Sarah et al., 2013), which can deepen the degree of connection and trust between parent universities and USOs so that interests align and work together for the high-quality development of USOs. We thus hypothesize the following:

Hypothesis 1: Parent universities’ equity ratio in USOs is positively related to enterprise performance of USOs.

Board Size and Enterprise Performance

Different from other countries’ USOs, the organizational attribution and growth process of USOs in China are derived from the characteristics of China’ s university administrative governance (K. Gao & Wang, 2020). As a result, most board members are selected by allocating existing administrative staff, who normally do not have any private industry managerial experience (Meoli et al., 2017). Consequently, it is difficult for board members to provide practical support in the business restricting USOs’ ability to adapt to any sudden market changes in a timely manner. Chacanti et al. (1985) take retail bankruptcy companies as a research sample and found that companies’ bankruptcy probability is inversely proportional to the board size. The reason is that the diverse expertise brought by the large-scale board of directors improves the accuracy of the board’ s decision-making and then reduces the probability of bankruptcy. Therefore, given the current situation that Chinese USOs’ board members are not professional in enterprise management, a large-scale board may bring more expertise and new ideas to USOs, helping boards arrive at making more accurate decisions which then improves the efficiency of corporate governance.

Moreover, according to the resource dependence theory, the board size can be used as a measure of an organization’ s ability to obtain key resources by connecting with the external environment (Bjørnåli & Gulbrandsen, 2009; Cai & Wang, 2007). The greater the demand for effective external connections, the larger the board size should be (Jeffrey, 1972). Based on the unique nature of USOs, a large-scale board of directors may help USOs obtain higher quality external resources from the entrepreneurial support network composed of stakeholders, such as parent universities, government and industrial partners (W. Li & Xia, 2013), providing a strong resource supply for the development of USOs. We thus hypothesize the following:

Hypothesis 2: USOs’ board size is positively related to enterprise performance.

Organizational Form and Enterprise Performance

China’s Ministry of Education (MOE) proposed that it is necessary to complete the restructuring of USOs with the stock system within a limited time and establish a modern enterprise system in USOs as soon as possible (Du & Song, 2008). Gao & Wang (2006) highlighted that after the reform of the enterprise system, corporate governance is generally better off than those enterprises without reform. After USOs are officially transformed into corporate system enterprises, their original serious problems such as unclear property rights, along with ambiguous rights and responsibilities can be effectively improved (Huang, 2018), as well as accelerating the process of de-administration and autonomy. Accordingly, USOs that have successfully transformed the organizational form into a corporate system will help it to better respond to sudden market changes, increase business flexibility and vitality of USOs, as well as arouse enthusiasm of owners and operators so as to improve the economic benefits from USOs. We thus hypothesize the following:

Hypothesis 3: USOs’ transformation of organizational form is positively related to enterprise performance.

Human Capital, Board Size and Enterprise Performance

Human capital refers to the knowledge, skills, and abilities embodied in the person (Coff, 2016). Resource-based theory believes that the non-homogeneous distribution of precious resources such as human capital among enterprises, explains the divergence of performance and has always been regarded as the key driving force of strategy and performance (Acedo et al., 2006; Hambrick & Mason, 1984; Jay, 1991). Companies retaining valuable resources like human capital that others cannot easily duplicate or purchase will perform better than competitors lacking these resources (Jay, 1991; Margaret, 1993). In order to promote transformation of the business mode from an administrative orientation to a market orientation, USOs will set up a board of directors and expand its size, coordinating the interests of multiple stakeholders. Furthermore, they will formulate strategic planning and combine market operations with diversified professional knowledge. Having high-quality human capital will help USOs to accelerate the process of this transformation through the board of directors and better adapt to the development of a market economy (Ji & Zhang, 2015).

Firstly, enterprises with strong human capital will actively adapt to the regulation of industrial policies within their business domain, adjust production and operation decisions and show a certain “policy compliance behavior” (Boubakri et al., 2008), so as to obtain more scarce resources with lower market prices, which can then lead to improvement of market competitiveness. Secondly, for different employers, there are differences in the intellectual level, psychological state and working ability, which all lead to different enterprise resource utilization abilities (Ren & Wang, 2010). Thomas & Ramaswamy (1996) pointed out that if an enterprise’s manager has a unique ability that matches the strategic orientation of the enterprise, it will greatly improve organizational performance. Moreover, when the cognitive ability of employers is high, their information processing ability and resolution ability in the face of different stimuli are also strong (Ren & Wang, 2010), and this helps to increase their cross-border activities which is generally considered as a strategic activity of an enterprise (Marc, 1984). The result is the connection of the organization and external environment (Dennis, 1971). Therefore, when the human capital of USOs is strong, it will help enterprises to better cope with changes of market demand and national policies so they can seize the opportunity. It is also conductive for USOs to explore and obtain external resources more actively and make efficient use of the existing resources in an organization. This will enhance the core competitiveness of enterprises and improve enterprise performance. We thus hypothesize the following:

Hypothesis 4: Compared with USOs having weak human capital, the board size in USOs with strong human capital has a stronger positive effect on enterprise performance.

Methodology

A general survey was conducted regarding the aspects of assets, ownership nature and operation status of Hubei Province’s USOs from 2015 to 2017. The sample of USOs comprises of 202 firms established by these universities from 1984 to 2017. After removing companies with flawed data, such as missing and abnormal data, and companies in the real estate market, the total number of enterprises analyzed in this study is 150, which derives from 39 universities, including 60 enterprises in 6 subordinate universities and 90 enterprises in 33 local universities. Additionally, subordinate universities refer to universities under the State Council or direct subordinate organizations. In addition, due to some USOs’ deficiency with lack of data in 2015 and 2016, the data selected in this research is the data of USOs in Hubei Province at the end of 2017, thus avoiding the impact of ineffective data on robustness.

The dependent variable is enterprise performance, which describes the efficiency of business operations. ROE (ratio between the net profit and the owners’ equity) is a common financial performance index to measure enterprise performance in empirical research. The independent variables in this study include equity structure, board size and organizational form where the equity structure variable is measured by the proportion of equity held by a parent university in USOs, the board size variable is measured by the number of boards and the organizational form variable is operationalized as a dummy variable equal to 1 if the legal form of USO is a corporation and 0 otherwise. As for the moderating variable human capital, including two indicators, one is employee productivity (natural logarithm of ratio between the business income and the total number of staff), which shows the contribution of each employee to the USOs’ business income and it is the direct representation of human resources’ value (Wang, 2019). The other is the proportion of public institution staff (ratio between the number of public institution staff and the total number of staff). The term public institution staff refers to the type of staffing used by units or institutions whose funds are disbursed from the state public service expense accounts. Their main function is to create or improve production conditions, enhance social welfare and meet the masses’ needs in education, culture, health, etc. Generally, the education background of public institution staff must be at least a bachelor degree level or above, so the proportion of public institution staff can reflect the education level of staff and the quality level of human resources (H. Zhang et al., 2015).

This study also includes several control variables related to spin-offs, parent universities and locations that might impact dependent variables. Company age (a categorical variable equal to 1 if the enterprise’s establishment time is under 5 years, equal to 2 if the enterprise’s establishment time is 5 to 10 years and equal to 3 if the enterprise’s establishment time is over 10 years) is a key element in companies’ development with the longer the development time, the higher the degree of resource accumulation (Rasmussen, 2011; Van Geenhuizen & Soetanto, 2009). Acknowledging the importance of company size, which is measured as the natural logarithm of business income (Acs & Audretsch, 1987), We also control for the asset-liability ratio, measured as ratio between total liabilities and total assets (Selarka, 2014; Wei & Ke, 2015). The attribute of parent universities are controlled, measured as a dummy variable equal to 1 if the parent university is the type of subordinate university and 0 otherwise, the policy advantages of subordinate universities may be higher (Yang et al., 2007). The regions where USOs are located are also controlled, measured as a dummy variable equal to 1 if a USO is in Wuhan and 0 otherwise. Wuhan is the capital city of Hubei Province, its regional economic strength, capital market activity and policy preference may be better than other cities, which is more conducive to the development of USOs (Meoli et al., 2017; Meoli & Vismara, 2016). Details on the variable definitions are reported in Table 1.

Variable Definition.

This study uses Hierarchical Regressions to test the relationship between corporate governance structure (equity structure, board size and organizational form) and enterprise performance, as well as the moderating effect of human capital on the relationship between board size and enterprise performance. The first regression model to the fourth regression model examine the impact of equity structure, board size and organizational form on enterprise performance. The fifth regression model adds the moderating variable human capital, the sixth regression model adds the interaction between human capital and board size based on the fifth one, among which,

Results

Descriptive Analysis

The descriptive statistics of the sample companies are shown in Table 2. The mean of ROE is 0.406, and the D-value between the minimum and the maximum is 22.423. This indicates that there are great differences in the performance of USOs. The mean of the ES is 0.719, showing that on average, parent universities’ equity ratio in USOs is 71.9%, indicating that there is a close relationship between parent universities and USOs. The mean of BS is 2.84, the minimum is 0 while the maximum is 11, implying that there are some USOs left without a board of directors and there is a large gap of USOs’ board size. The mean of OF is 0.753, that is, 75.3% of USOs have followed the policy of China’s Ministry of Education, carried out enterprise restructuring and established a modern enterprise system. With regard to human capital, the mean of IS is 0.235, showing that 23.5% of the staff are public institution staff on average. Moreover, the EP mean is 3.074, the minimum is −1.184 while the max is 7.716 which indicates that there is a huge gap in employee productivity of USOs.

Descriptive Statistics.

Regression Analysis

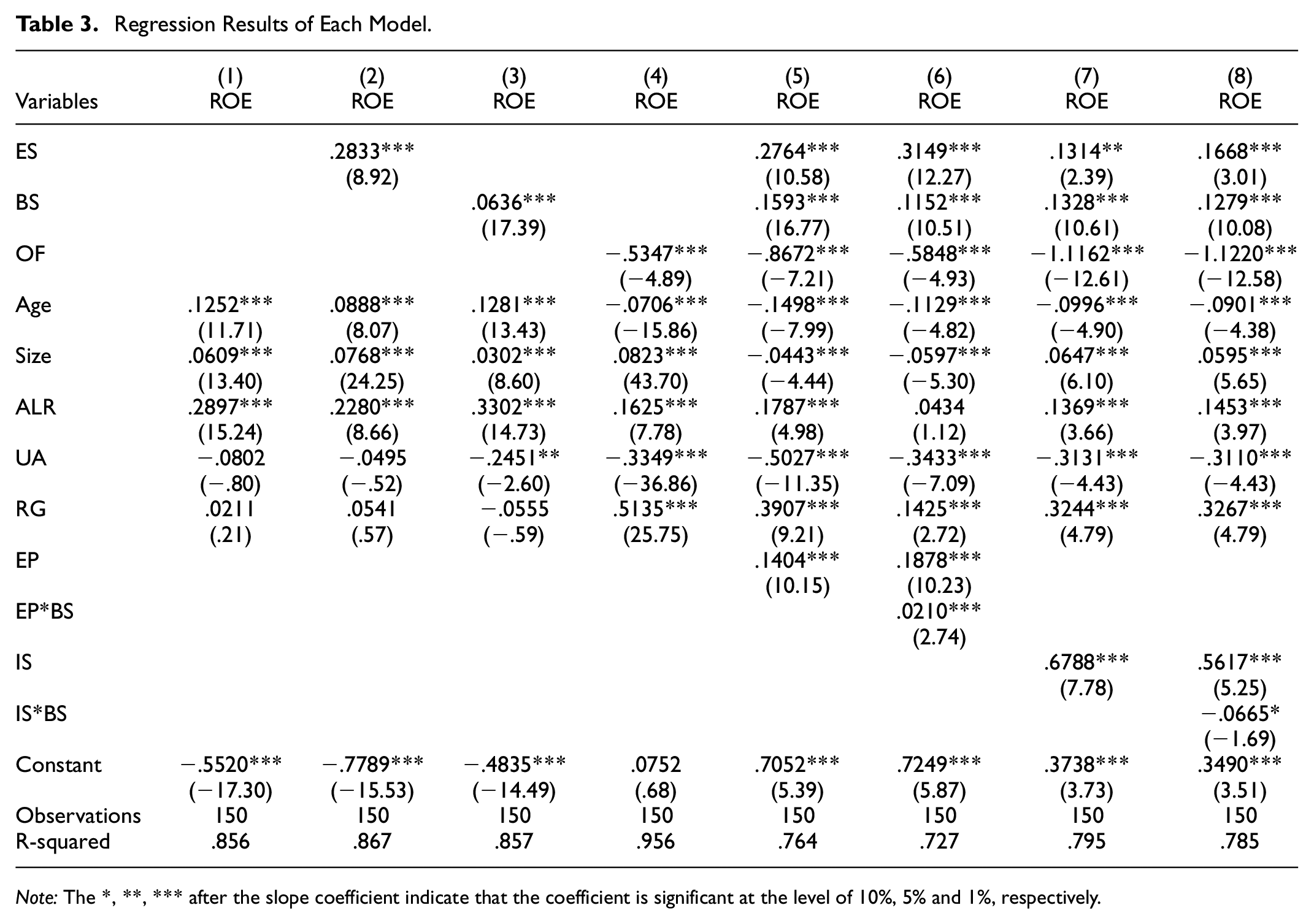

Table 3 reports the regression results. Model 1 is the baseline model showing the effect of the control variables and the influence of these control variables in other models is basically the same. Model 2 tests the relationship between equity structure and enterprise performance. The results show that equity structure has a positive correlation with enterprise performance (=.2833, p < .01). The regression results support hypothesis 1. Model 3 examines the relationship between board size and enterprise performance. The results show that there is a positive correlation between board size and enterprise performance (=.0636, p < .01), supporting hypothesis 2. Model 4 tests the relationship between organizational form and enterprise performance. Although the regression result is significant (=−.5347, p < .01), showing a negative correlation between organizational form and enterprise performance which is inconsistent with our expectation. Analyses in model 4 does not support hypothesis 3.

Regression Results of Each Model.

Note: The *, **, *** after the slope coefficient indicate that the coefficient is significant at the level of 10%, 5% and 1%, respectively.

Model 5 to model 8 test the moderating effects of human capital on the relationship between board size and enterprise performance and the regression results partially support hypothesis 4. Model 5 shows that EP has a significant positive effect on enterprise performance (=.1404, p < .01). As shown in Model 6, the interaction effect of EP with BS is significant (=.0210, p < .01), which supports hypothesis 4. Additionally, model 7 indicates that IS has a significant positive effect on enterprise performance (=.6788, p < .01), and model 8 shows that the interaction effect of IS with BS is negatively significant (=−.0665, p < .1). However, this result does not support hypothesis 4. To illustrate the patterns of interaction effects that supported hypothesis 4, we plotted the interaction effects using one standard deviation above and below the mean to represent high and low levels of the moderating variable (Acs et al., 2009). Figure 2 displays a deeper slope when employee productivity is high: the level of enterprise performance shows an increase from 0.5265 to 1.3688. When employee productivity is low, the level of enterprise performance only increases from 0.2308 to 0.7736. This suggests that employee productivity has a positive moderating effect on the relationship between board size and enterprise performance.

The moderating effect of employee productivity.

Robustness Analysis

We run additional models to further probe the robustness of empirical results as follows. One is to add a new control variable, that is, the university senior manager variable (USM), measured as the number of senior managers in USOs dispatched by their parent universities respectively. If senior managers of USOs come from their parent universities, they are more likely to build a bridge between the university and the enterprise, give full play to the technological advantages of parent universities, so as to improve enterprise performance (Wei & Ke, 2015). The results are basically consistent with the above and are shown in Table 4. The other is selecting enterprises whose primary business is closely related to the construction discipline of parent universities, that in the total sample as a new observation sample, the observations are 74, accounting for 49% of the total sample. The results remain similar to these additional tests with different sample periods.

Robustness Test Results.

Note: The *, **, *** after the slope coefficient indicate that the coefficient is significant at the level of 10%, 5% and 1%, respectively.

Discussion

This study analyzes the impact of corporate governance structure on enterprise performance of USOs and discusses the moderating role of human capital. We use cross-sectional data to test the hypothesis, which includes 150 USOs from Hubei Province, China and the empirical results partially support the hypothesis.

Firstly, the study finds significant positive effects of parent universities’ equity ratio in USOs on enterprise performance. As an important means to improve capital allocation and operational efficiency, optimizing the ownership structure and adjusting the proportion of equity are of great significance to the development of enterprises. The increase of equity ratio not only helps to give full play to the advantages of state-owned capital, it also helps to enhance the enthusiasm of shareholders, increase the leadership and incentive role of enterprise managers, strengthen the internal control system of enterprises, and improves enterprise performance. With formal equity links between parent universities and USOs, universities can better support enterprises with resources such as technology and knowledge, sharing infrastructure such as computers, equipment and laboratories. Therefore, a USO can appropriately increase the equity ratio of the parent company in the enterprise. It can effectively strengthen the connection with universities through the increase of equity ratio. We can obtain the help of talented individuals with their professional knowledge and other resources through the existing resources of colleges and universities. This will help promote the high-quality development of enterprises. Thus, a USO can appropriately increase the parent university’s equity ratio in the enterprise, strengthen the connection with the university and make full use of university resources, such as technology, talent advantages and various professional knowledge, in order to improve the utilization efficiency of resources. However, USOs cannot blindly improve the ratio of university equity ownership in USOs which may be counterproductive because when the ratio exceeds a threshold point, it will have a negative impact on enterprise performance. There are a significant body of scholars who have proved that there is an inverted U-shaped relationship between the proportion of state-owned shares and enterprise performance (Tian & Jiang, 2015; Yang, 2014; R. Zhang & Jiang, 2018).

Secondly, the study demonstrates significant positive effects of board size on enterprise performance. The research shows that by increasing the number of directors enables the board of directors to more efficiently establish external links that attract key resources based on the resource dependence theory. This is because external and independent directors can provide high-quality advice to executives which may be somewhat difficult to obtain from within the company in addition to the expertise and resources from internal directors. Various kinds of directors bring different information and connections to enterprises. Therefore, the establishment of a board of directors can not only protect the interests of all stakeholders, but also ensure the effectiveness of decision-making and improve the company's operating efficiency (Qi, 2004). Due to USOs’ board of directors in China many of whom are often composed of the existing leaders in charge of assets, finance and scientific research in universities, they are usually very unfamiliar with the domain of commercialization and private industry (Q. Gao, 2017). This may lead to internalizing the university’s academic institutional logic that “emphasizes the search for fundamental knowledge, research freedom, rewards in the form of peer recognition, and the open disclosure of research results” (Agarwal et al., 2004), and this does not apply to the business and may engender a negative impact on the enterprise. Successful technology commercialization requires not only the creation but also the application of knowledge. Therefore, the expansion of the board of directors can not only make up for the lack of knowledge structure and experience of internal directors, but also enrich the diversity of knowledge and experience of board members. This can ensure the board’s issues are fully discussed, reduce the company's operating risks and improve the accuracy of decision-making. This can help USOs to provide technical knowledge support for enterprises along with relevant business and industrialization knowledge. This has the effect of reducing the risk of business operations, as well as helping USOs to obtain more resources in realizing technology transformation.

Thirdly, this study also confirms the positive moderating effect of employee productivity on the relationship between board size and enterprise performance. The higher the level of human capital, the higher the capacity of processing various information (Ren & Wang, 2010). This is conducive to amplifying the positive effects of board size expansion, accelerating the process of the board’s high-quality decision-making and utilizing board of directors’ knowledge effectively. As for the negative moderating effect of the proportion of public institution staff, which is not aligned with hypothesis 4, this may be caused by the specialty of public institution staff. In China, it is generally believed that public institution staff have an “iron an rice bowl,” their work and income are relatively stable. Therefore, although their quality and ability may be high, they lack enthusiasm and initiative in their work and have a serious problem of job burnout (Y. Wang et al., 2015), which is not conducive to enterprise performance. Therefore, it is necessary to guide and motivate employees to participate in continuing education, improve their working ability and stimulate their vitality in order to help enterprises better deal with risks and challenges (K. Gao et al., 2020).

Fourthly, this study reveals that the organizational form of USOs has a negative impact on enterprises performance which is not in line with our expectations. The reform of USOs implemented by China's MOE requires USOs to establish a legal entity with clear property rights, definite rights and responsibilities, the separation of government and enterprises, and independent operation (Hong, 2017). In fact, many enterprises that have completed restructuring and have established a company system, do not align with requirements from the MOE. They are still used for universities’ administrative management and their business philosophy has not yet realized the transformation from administrative orientation to market orientation. In addition, USOs’ market operation is restricted by the general rules of universities, their imperfect decision-making system will usually affect the adjustment of enterprise strategy and business policy, which may not keep up with the pace of market changes, fail to seize market opportunities and affect enterprise performance. This indicated USOs that have completed the restructuring need to accelerate the process of “de-administration,” ensure the autonomy and market orientation of enterprise operations in order to realize real independence. Furthermore, USOs need to ensure the improvement of relevant decision-making systems and regulatory systems at the institutional level.

The research findings add to the scant literature on the performance implications of corporate governance structure and thus offer several contributions (Kong et al., 2023). First, much of the previous literature focuses either on the aspect of parent universities’ implications on enterprise performance or the external environment aspect (Kroll & Liefner, 2008; Meoli et al., 2017; Yang et al., 2007). While some studies have analyzed influencing factors at the enterprise level (C. Zhang, 2014; C. Zhang & Xia, 2012), many ignore the corporate governance variable. Our research results show that the corporate governance structure of USOs, including equity structure, board size, and organizational form, will have a significant impact on enterprise performance. In particular, the corporate governance variable in this study includes the organizational form variable, which is not available in much research. USOs are usually part of the administrative structure of universities, so universities directly manage and are responsible for debts, thus they are nominally state-owned enterprises (Yu & Zheng, 2019). Therefore, due to the unique nature of Chinese USOs, whether a company system is established will have a great impact on the operation and management of enterprises.

Second, the main goal of Chinese USOs at present is to improve the development status of enterprises and enhance enterprise value (Xia et al., 2010). The results of this study may provide some reference for the institutional reform and enterprise management of USOs. Parent universities' equity in USOs will be conducive to realize strategic objectives and acquire key resources to maintain good performance of enterprises, and there is therefore room for both enterprise and university managers to reflect on the significance of universities' investments in USOs' equity. Additionally, USOs should also focus on the importance of board of directors to the development of enterprises, which usually has an irreplaceable position for the acquisition and utilization of resources (Jeffrey, 1972). The results show that USOs should also pay attention to improving the level of human capital in order to better play the role of board of directors. In addition, this study underlines the influence of organizational form on enterprise performance. USOs should not merely emphasize the change of organizational form, but also pay attention to transformation of driving ideas and systems to support the necessary institutional reform.

Conclusion

In this study, we examine the effects of USOs’ corporate governance structure which includes equity structure, board size and organizational form, on enterprise performance in a Chinese context, as well as the moderating effect of human capital on the relationship between board size and enterprise performance. This study takes 150 enterprises in 42 universities in Hubei Province as samples in 2017 using the weighted least square (WLS) method. The research finds evidence of positive relationships between equity structure and enterprise performance, as well as between board size and enterprise performance. However, a positive effect is not found between organizational form and enterprise performance, which shows a prominent negative effect. Moreover, human capital which is partially positive, influences the relationship between board size and enterprise performance.

The current research limitations are as follows. Firstly, this paper does not consider the selection of indicators comprehensively due to the difficulty of quantifying some indicators and the difficulty of collecting specific data. Secondly, our considerations in selecting corporate governance variables are not perfect because corporate governance is a complex concept. Finally, in terms of the composition of the board of directors, due to data and other factors, the composition of the board of directors is relatively simple. Therefore, future research can broaden the choice of corporate governance variables and the composition of the board of directors under the premise of data availability. For example, the composition of the board of directors can be considered from the aspects of quantifying the ability of directors and adding entrepreneurial experience in order to study the relationship between relevant variables more clearly.

Footnotes

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: This work was supported by the Center for Reservoir Resettlement, China Three Gorges University [grant number 2019KQ01].

Data Availability Statement

Data sharing not applicable to this article as no datasets were generated or analyzed during the current study.