Abstract

The aim of this study is analyzing the spillovers of monetary policies from three nations including the US, Japan, and China to the Southeast Asian economies through macroeconomic linkages. By using BVAR model, the research results present distinct responses of economic growth, interest rate and inflation index in Southeast Asia to external shocks of interest rate according to specific characteristics. In particular, nations adopting pegged regime have stronger responses to the changing of the Fed rate and Japanese monetary policy while the opposite trend is found in volatility of Chinese interest rate. However, nations with higher trade openness might have more sensitive reaction to monetary policy of all three countries. On the other hand, the impact of international monetary policies on Southeast Asian countries is explained quite different between the group having higher capital openness and the other one. In general, the results are consistent with many previous studies as well as Mundell-Fleming’s impossibility triple theory.

Plain language summary

Purpose: This study analyzes the spillover effects of monetary policies from three nations including the US, Japan, and China to the Southeast Asian economies through macroeconomic linkages. Methods: By using the BVAR approach proposed by Doan et al. and Litterman, the study analyzes the spillovers effects of monetary policy from three nations to Southeast Asian countries. Conclusions: The nations in Southeast Asia adopting pegged regime have stronger responses to the changing of the Fed rate and Japanese monetary policy while the opposite trend is found in volatility of Chinese interest rate. However, nations with higher trade openness might have more sensitive reaction to monetary policy of all three countries. The results are consistent with many previous studies as well as Mundell-Fleming’s impossibility triple theory. Implications: The size of spillovers varies in every country, depending on factors such as the exchange rate system and the degree of financial integration. Limitations: The number of Southeast Asian countries analyzed is only 6 and the study period was limited to the period from 2009 to 2019 so that the suggested policy implications are only appropriate for this scope.

Introduction

In the context of global integration and technical progress, the role of macroeconomic linkage of nations is becoming increasingly important. Over the past decades, economic integration in Southeast Asia has been advanced creating conditions for goods, services, labor, and capital to be more freely circulated. However, the process of moving capital flows and trade creates spillover effects of monetary policy among countries (Pham & Nguyen, 2019). The spillover effects of monetary policy of some developed countries dealing with huge volumes of foreign transactions such as the US, Japan and China, have impacts on the macroeconomic management of the others (Claus et al., 2016; Pham & Nguyen, 2019).

On the other hand, the Asian crisis in the period 1997 to 1998 showed the role of contagion effects in the region when the financial crisis occurred. The instability of Southeast Asian countries during this period is explained by the high degree of openness (Corsetti et al., 1999) as well as the degree of interdependence in the region (Kaminsky et al., 2003). This crisis also prompted Southeast Asian countries to strengthen cooperation to increase the independence in monetary policy. These cooperative efforts were concretized through the ASEAN Surveillance Process in October 1998 and the Chiang Mai Initiative in May 2000, which provided for multilateral exchanges among ASEAN and China. China, Japan, and Korea. The 2008 financial crisis that began with the collapse of Lehman Brothers once again raised concerns about the volatility of Southeast Asian countries to external shocks.

For many years, researchers have been fascinated by the study of transmission effects from one country’s monetary policy to another. Analyzing the responses of countries based on their features allows them to make the necessary modifications to limit international consequences. In this study, the authors focus on analyzing the spillover of monetary policy from three major economies in the world including the US, China, and Japan to Southeast Asian economies based on the countries’ characteristics of the exchange rate regime, the level of trade openness as well as capital openness. The responses of Southeast Asian nations have been reflected by three main indicators representing the macroeconomic characteristic of one country including GDP’s growth rate, inflation rate, and interest rate. Moreover, the BVAR model has been used to estimate the transmission effects in global macroeconomic environment, which is one of the new empirical techniques and has not been analyzed clearly in previous researches before.

Literature Review

The International Transmission Mechanism of Monetary Policy

The transmission of external shocks to the growth as well as macroeconomic variables has been explained in Ajluni (2005). According to Ajluni (2005), it is argued that for a small open economy, the exchange rate is affected by the movement of capital flows and is the result of the appreciation of the local currency. In other words, changing interest rates will affect the demand for domestic currency, thereby affecting the exchange rate. In addition, market interest rates also affect the company’s decisions as well as ways of consumption and investment. Meanwhile, consumption and investment are two of the main components of aggregate demand and ultimately affect domestic output and inflation. It can be seen that fluctuations in the global economy play an important role in the analysis of small open economies, and changes in a country’s monetary policy will affect interest rates and other macroeconomic variables of other countries.

According to Ammer et al. (2016), the exchange rate channel, aggregate demand channel, and financial channel are the three main channels via which spillover effects from one country’s monetary policy have been transferred to another. First, the renowned IS-LM-BP model created by Mundell (1963) and Fleming (1962) explains the transmission effect of monetary policy through the exchange rate channel. When a country implements an expansionary monetary policy, the money supply of the economy increases and thus the country’s interest rate level decreases and becomes relatively lower than that of other countries. Decreasing interest rates leads to a depreciation of the local currency, encouraging spending and investment, increasing the economy’s net exports, and boosting a country’s trade balance and GDP. However, a pure expenditure-switching impact occurs when a country’s growth in net exports damages the foreign trade balance and foreign GDP (Ammer et al., 2016). The aggregate demand channel is the second channel. When a country’s monetary policy is implemented through raising interest rates, domestic investment and consumption will fall, resulting in an increase in both imports in the host country and exports in the partners. Therefore, the aggregate demand channel has a stimulating effect on spending that has been transmitted to partner countries, helping to increase their GDP. In other words, the aggregate demand channel contributes to the partner countries’ GDP growth. The financial channel is the final one. When a government adopts an expansionary monetary policy, long-term interest rates will fall, and asset prices rise in the home country will rise. This makes investors reassess their portfolios and tend to shift their capital flows to countries with higher yields. These countries will receive foreign investment flows, thereby improving science and technology, improving quality as well as diversifying products and services. In conclusion, depending on the degree of the impacts, transmission effects from one country’s monetary policy to another would be either positive or negative (Ammer et al., 2016). Therefore, Mundell–Fleming model is one of economic models, reflecting the nexus between exchange rate, interest rate, and output of the economy. In this way, a country cannot pursue a pegged exchange rate, an interest rate liberal policy and an independent monetary policy at the same time. An economy can only maintain two of the three above strategies, which was called “impossible trinity.” Consequently, the result of this study will contribute to additional empirical evidence for explaining this theory background.

Previous Empirical Studies

Miniane and Rogers (2007) examined whether capital controls fully protect nations from U.S. monetary shocks, using a unified estimate methodology to look at a wide range of national experiences. The paper utilized a VAR model to analyze macroeconomic data from 26 countries from 1975 to 1988 and discovered that countries with tighter capital controls do not experience lower interest rate increases in response to contractionary US monetary shocks. One issue is that controls are difficult to enforce and can easily be circumvented. Maćkowiak (2007) studied the impact of external shocks and US monetary policy shocks on macro variables in emerging markets (including Hong Kong, Korea, Malaysia, Philippines, Singapore, Thailand, and Latin America) in the period 1986 to 2000. External shocks are a major source of macroeconomic fluctuations in emerging markets, according to structural VARs Furthermore, interest rates and the exchange rate in a typical emerging economy are affected rapidly and substantially by US monetary policy shocks. By constructing structural vector autoregressive (SVAR) models for six economies in the region, Koźluk and Mehrotra (2009) investigated the effects of Chinese monetary policy shocks on China’s major trading partners in East Asia. They discovered that monetary expansion in Mainland China led to temporary and persistent increases in real GDP and price levels in several economies in their sample, most prominently in Hong Kong and the Philippines. The impacts of US monetary policy shocks on the bilateral exchange rate between the US and each of the G7 countries were researched by Bouakez and Normandin (2010). The paper employed the SVAR model for macroeconomic variables in the period 1982 to 2004. The findings show that the nominal exchange rate responds to monetary expansion with delayed overshooting, falling for about 10 months before beginning to appreciate. The shock also causes considerable and long-lasting deviations from uncovered interest rate parity, as well as a period of partial pass-through. Johansson (2012) examined the possible transmission of China’s monetary policy shocks to Southeast Asian equities markets using structural VAR models with short-run constraints. The findings suggest that China’s monetary policy has a small but significant impact on numerous economies in the region. Osorio and Unsal (2013) used a Global VAR (GVAR) model to analyze inflation dynamics in Asia. This model explicitly considers trade and financial linkages between nations, as well as the effect of regional and global inflationary spillovers. The results imply that monetary and supply shocks have been the main drivers of inflation in Asia, but that their contribution to the region’s inflation has decreased in recent years. The empirical study of Yang and Hamori (2014) indicated the transmission influence of US monetary on the ASEAN stock markets through Markov-switching models. Georgiadis (2016) looked at the global effects of US monetary policy on 61 economies between 1999Q1 and 2009Q4. The paper found that US monetary policy causes huge output spillovers to the rest of the globe, which are larger than the domestic impacts in the US for many economies, using the Global VAR (GVAR) model. From 1979Q2 to 2011Q2, Bi and Anwar (2017) looked studied the influence of US monetary policy shocks on China’s primary macroeconomic indicators. According to their findings, a positive shock to the US money supply growth rate initially raises China’s inflation rate, but this effect fades with time. China’s short-term interest rate rises as a result of the shock, and the Chinese currency appreciates versus the US dollar. Hassan et al. (2017) studied the influence of macroeconomic connections on international shock transmission in East Asia using the Global Vector Autoregressive Model (GVAR) on quarterly data of real production, inflation, equity prices, currency rates, and short-term interest rate from 1979Q2 to 2013Q1. In general, the results reveal that China contributes the most shock transmission in the real sector, whereas the United States contributes the most in the equity market. Huynh and Nguyen (2018) used a global vector autoregressive (GVAR) model to examine how macroeconomic shocks from ASEAN-6’s major trading partners (such as China, the United States, and Japan) affect the trade balance in the region. The empirical findings of the research confirm the importance of the US real GDP shock in determining the ASEAN-6 trade balance. In the long run, the authors find that the CNY devaluation will result in a big trade surplus in China and Vietnam, while the US trade balance would deteriorate. Using VAR-X model for 10 developing nations, the transmission effect of US monetary policy on the other economies has been proved by Tillmann et al. (2019). Pham and Nguyen (2019) examined the spillovers from US monetary policy shocks to Asian nations while accounting for country-specific variables in explaining disparities in reaction timing and amplitude. The findings, based on BVAR models, show that policy interest rates in Asian countries generally respond in the same direction as the Fed rate, but with a one-quarter lag. In another study of Bhattarai et al. (2020), spillover effects of US monetary policy on 15 emerging market economies were indicated by a PVAR model. Lakdawala et al. (2021) estimated the transmission effect of US monetary policy on some emerging nations. Elsayed and Sousa (2022) used daily data from August 5, 2013, to September 27, 2019, to analyze the spillover effects of international monetary policies among four major countries including Japan, US, UK, and Europe. By the regression model of TVP-VAR, the result indicated that the higher interest rate was, the stronger spillover effects of monetary policy got. On the other hand, by using VAR model, Zhang et al. (2022) identified the transmission effect of US monetary policy on Chinese output and inflation.

Briefly, analyzing the impact of a country’s monetary policy on economies of other nations has been becoming an interest of researchers in the world. However, results of reviewing previous studies show the impact of international monetary policy on other economies is not only based on the strength of spending transmission effects but also depends on the level of macroeconomic linkages in terms of trade openness and capital openness as well as exchange rate regime that countries are pursing. In Asia, the US, China, and Japan are considered several large countries having a great influence on the Southeast Asian economies. In the trend of global economic integration, spillover effects from one country’s monetary policy on other countries are inevitable and each country has its own goals and economic conditions. Moreover, evaluating the reactions of Asian countries based on the characteristics of each country, helps them make appropriate adjustments to limit international influences as well as the impact of monetary policy of the US, China, and Japan. In addition, the number of studies on the impact of external monetary policy shocks on Southeast Asian countries is still limited. Therefore, this paper studies the spillovers of monetary policy from three nations including the US, Japan, and China to the Southeast Asian economies by using BVAR models. According to this, the Southeast Asian countries have been categorized based on exchange rate regime, the level of trade openness and capital openness to analyze the responses to international monetary policy volatility.

Methodology and Data

Using the BVAR approach proposed by Doan et al. (1984) and Litterman (1980), this study analyzes the spillovers effects of monetary policy of three nations to Southeast Asian countries.

Let Yt be an n × 1 random vector that takes values in Rn. The evolution of Yt, the endogenous variables, is described by a system of p-th order difference equations—the VAR(p):

Where Yt is a (n × 1) vector of stationary endogenous variables, Xt refers to a (n × 1) vector of exogenous variables, μ represents a (n × 1) vector of constant coefficients, ε t expresses a (n × 1) vector of identically and independently distributed error terms meeting the required E(ε t ) = 0, and E(ε t ,−ε′ t ) = Σ, Ai (i = 1, 2, …, p) signifies a coefficient matrix (n × n) of endogenous variables and B is a coefficient vector of exogenous variables.

Vector Yt is constructed to capture the interdependency between three large economies including the US, Japan, China, and Southeast Asian countries with regard to monetary policy and country characteristics. The research model in this study analyzing the impact of monetary policy management in the US, Japan and China on the economies of Southeast Asia is inherited from the previous studies such as Maćkowiak (2007), Georgiadis (2016), and Pham and Nguyen (2019). Therefore, Southeast Asian countries has been classified into two groups according to the characteristics of exchange rate regime (pegged and floating regime), the degree of trade openness (low and high level) and the degree of capital openness (low and high level). Each country group contains variables: real economic growth (y), inflation rate (dp) and interest rate (r) represent the macroeconomic view of nations.

Vector Yt includes: Yt = [ya1 t , dpa1 t , ra1 t , ya2 t , dpa2 t , ra2 t , ya3 t , dpa3 t , ra3 t ]. This article analyzes the impact of monetary policy of the US, China, and Japan, represented by interest rates (ra1) of the US, China and Japan on economic growth (ya2 and ya3), interest rates (ra2 and ra3). And inflation rates (dpa2 and dpa3) of two groups in Southeast Asia which have been classified according to three national characteristics including exchange rate regime, the level of trade openness and capital openness. Therefore, three BVAR models are needed to measure in this study.

Furthermore, The International Monetary Fund (IMF) categorizes nations’ exchange rate regimes in its Annual Report on Exchange Arrangements and Exchange. Additionally, based on the result of a comparison between the ratio of total trade to GDP and the sample mean value, Southeast Asian countries are divided into two groups: high and low trade openness. The criteria for classifying countries according to their capital openness are based on Chinn–Ito index (KAOPEN) (Chinn & Ito, 2019). Countries with a KAOPEN equal to 1 are identified as high capital openness, and countries with a KAOPEN of 0 are classified as low capital openness.

The data are quarterly observations derived from various sources. In order to ensure sufficient data during the research period from 2009Q1 to 2019Q4, six countries in Southeast Asian have been chosen to analyze including Indonesia, Malaysia, Philippines, Singapore, Thailand and Vietnam. These countries are selected based on countries with the highest GDP in Southeast Asia according to the IMF rankings 2020. In order to avoid the structural break caused by the Asia financial crisis in 1997, the research period is selected after 2000. Table 1 shows how to measure variables.

Variable Description.

Source. Authors’ calculation.

According to Table 1, the economic growth is calculated by the annual change in GDP while the inflation rate is defined by consumer price index (CPI). The IMF’s database is used to calculate the actual economic growth rate. The difference of the natural logarithm of the consumer price index is used to calculate inflation. The weighted average is used to compute the variables for each nation group. The weights are based on each country’s average trade share for the same time.

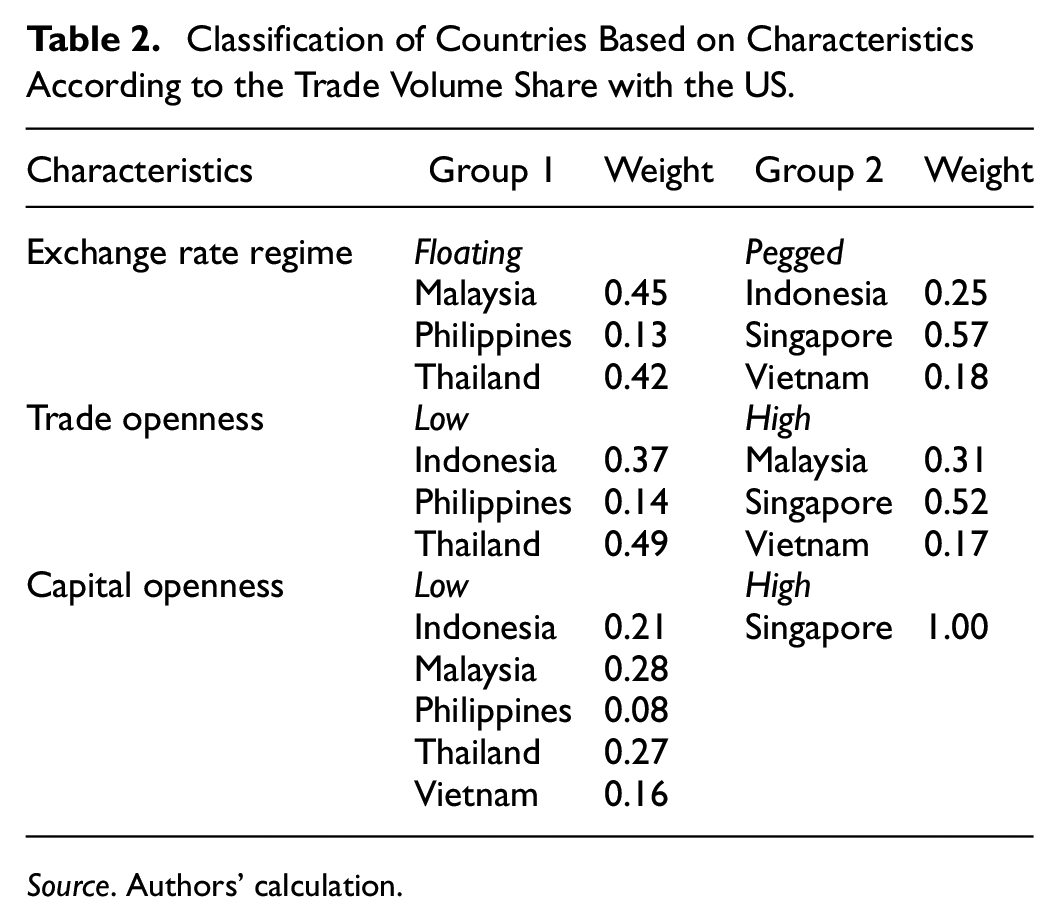

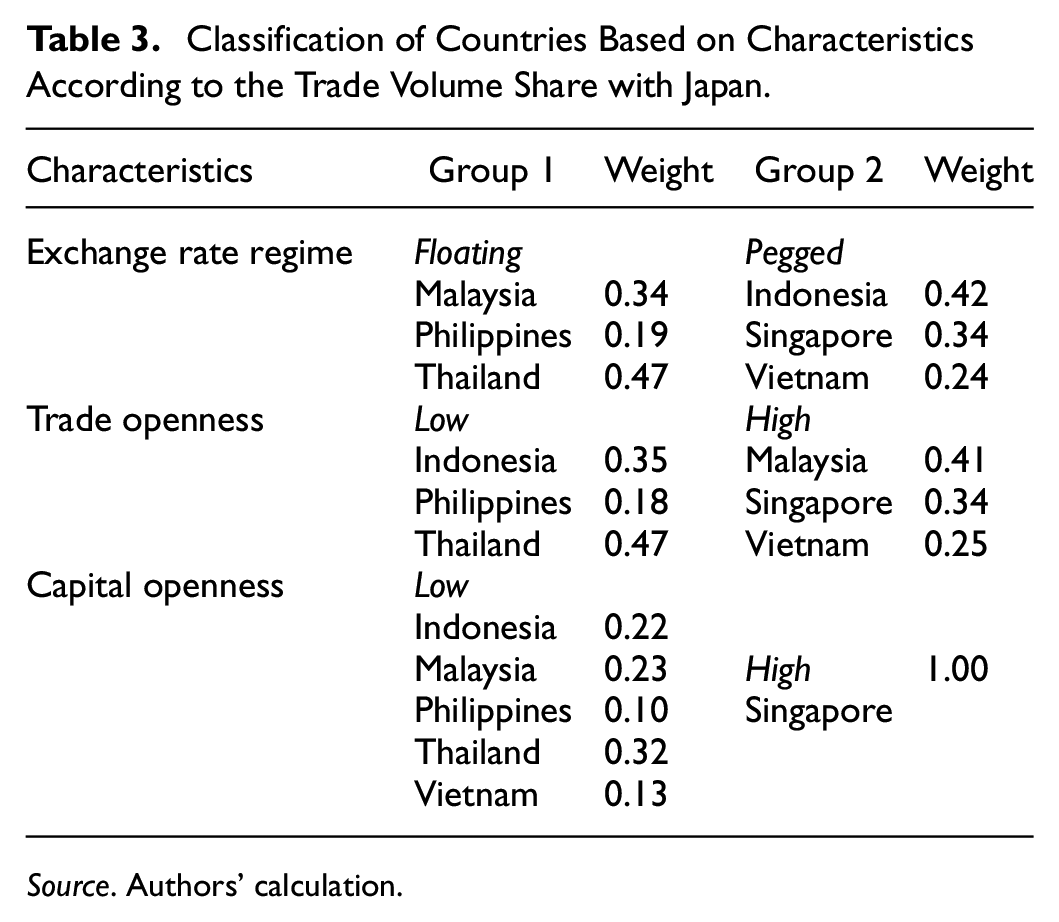

Tables 2 to 4 show how countries are classified based on their characteristics. In each group, weight is determined as the fraction of each country’s trade volume share with the United States, Japan, and China. As a result, weights are used to calculate variables like growth rate, inflation rate, and policy interest rate in each recognized category.

Classification of Countries Based on Characteristics According to the Trade Volume Share with the US.

Source. Authors’ calculation.

Classification of Countries Based on Characteristics According to the Trade Volume Share with Japan.

Source. Authors’ calculation.

Classification of Countries Based on Characteristics According to the Trade Volume Share with China.

Source. Authors’ calculation.

The hypotheses of this study are proposed based on the theory of Mundell–Fleming model and some previous empirical studies such as Georgiadis (2016), Bi and Anwar (2017), and Pham and Nguyen (2019). Firstly, to evaluate the spillover effects of US monetary policy, three hypotheses including H1a, H1b and H1c are suggested as follows:

H1a: US monetary policy affects the economic growth rate of Southeast Asian countries.

H1b: US monetary policy affects the inflation rate of Southeast Asian countries.

H1c: US monetary policy affects the interest rate of Southeast Asian countries.

Secondly, the hypotheses consisting of H2a, H2b and H2c are proposed relating to the transmission effects of Japan as following:

H2a: Japanese monetary policy affects the economic growth rate of Southeast Asian countries.

H2b: Japanese monetary policy affects the inflation rate of Southeast Asian countries.

H2c: Japanese monetary policy affects the interest rate of Southeast Asian countries.

Similarly, three following other hypotheses (H3a, H3b and H3c) about the spillover effects of Chinese monetary policy on Southeast Asian countries are proposed. Specifically, they are:

H3a: Chinese monetary policy affects the economic growth rate of Southeast Asian countries.

H3b: Chinese monetary policy affects the inflation rate of Southeast Asian countries.

H3c: Chinese monetary policy affects the interest rate of Southeast Asian countries.

Before applying the BVAR method, the variables have been examined for stationarity by the Augmented Dickey-Fuller (ADF) test method at all levels. The results show that the variables all stop at the original data series, and they are continued to be analyzed by BVAR approach.

Results and Discussions

The International Monetary Policy Spillovers Effects on Southeast Asian Countries Classified According to Exchange Rate Regime

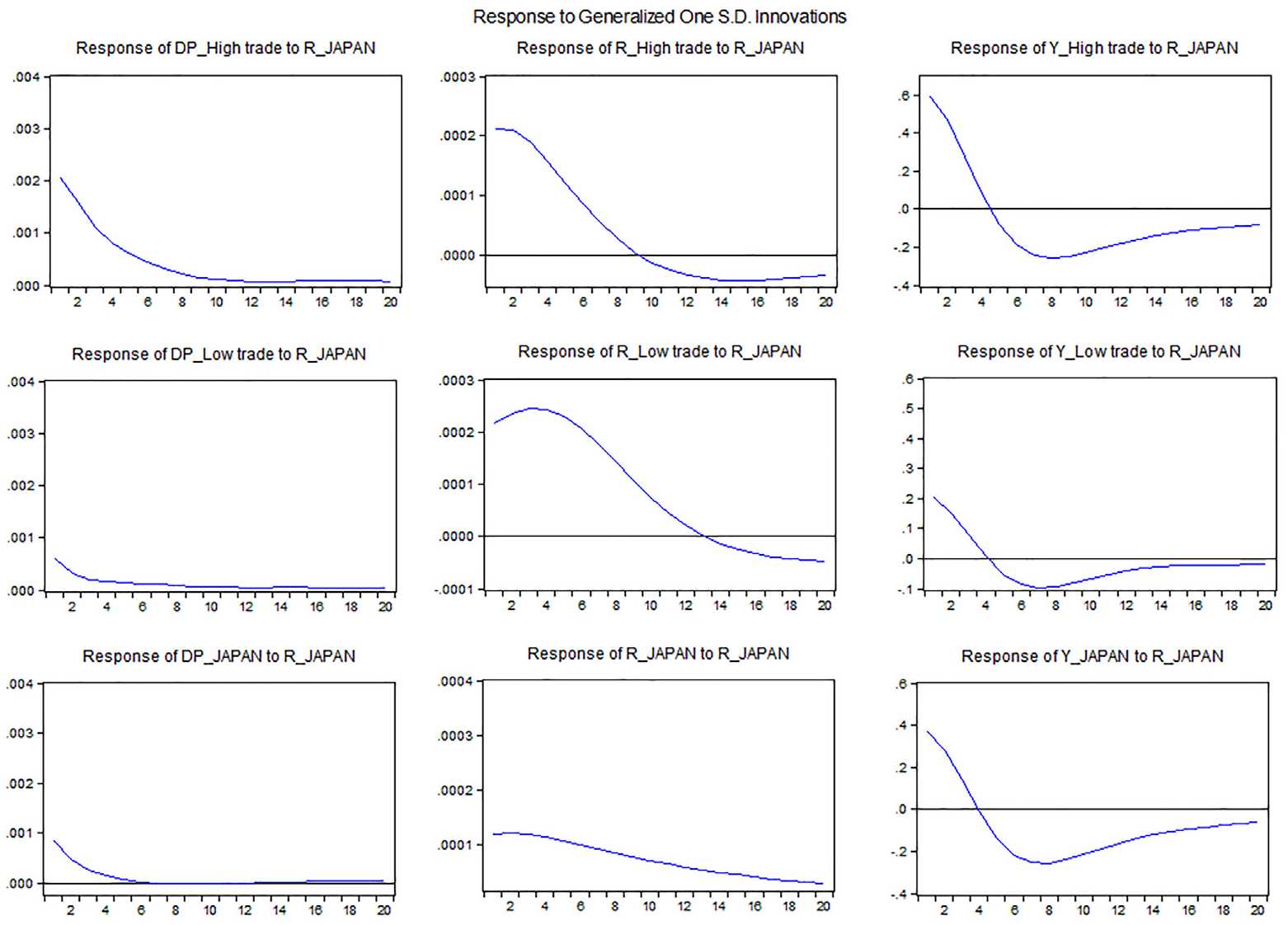

Figures 1 and 2 show that both the US monetary policy and the Japanese interest rate have a favorable impact on the economic growth of both groupings of Southeast Asian countries. This finding is supported by multiple investigations, including Koźluk and Mehrotra (2009), Bi and Anwar (2017), and Pham and Nguyen (2019). The influence of US monetary policy on nations with pegged exchange rates, on the other hand, is stronger than on countries with floating exchange rates.

Spillovers effects of the US monetary policy on Southeast Asian countries classified according to exchange rate regime.

Spillovers effects of Japanese monetary policy on Southeast Asian countries classified according to exchange rate regime.

Furthermore, both the US monetary policy shock and the Japanese monetary policy shock have a positive influence on Southeast Asian interest rates. Nations with pegged exchange rates, on the other hand, are more intensive than countries with fluctuating exchange rates. This study’s findings are similar to those of Johansson (2012) and Bi and Anwar (2017).

However, the impacts of monetary policy shock in the US and Japan on the inflation in two groups of Southeast Asian countries showed in Figures 1 and 2 are different. Firstly, when there is a shock to the US monetary policy increasing interest rates by one standard deviation, the inflation of groups with floating exchange rate regimes in Southeast Asia increases by about 0.0016% in the first quarter and remains after 12 periods. In the US, it grows by 0.0019% and gradually declines after 4 periods. This result is consistent with the study of Bi and Anwar (2017). In contrast, for Southeast Asian countries with fixed exchange rate regimes, inflation is negatively affected by the US currency shock and this reaction is quite short in one period. Second, two groups of Southeast Asian countries benefit from Japanese monetary policy. When the Japanese interest rate is shocked by one standard deviation, the inflation rate in fixed exchange rate countries responds more severely than in floating exchange rate countries. This result is consistent with Johansson (2012) and Bi and Anwar (2017). Furthermore, the findings of this study are explained using the Mundell-Fleming impossible trinity model, which states that adopting a set of three policies, including a pegged exchange rate regime, an independent monetary policy, and free capital flow reflecting macroeconomic linkages, is impossible.

Figure 3 shows that a change in Chinese monetary policy has a favorable influence on both inflation and economic growth in Southeast Asian countries. Nations that use a floating exchange rate regime, however, are more intense than countries that use a pegged exchange rate regime. This result contrasts with the response of Southeast Asian economies to American and Japanese monetary policy as shown above. Moreover, the results of Chinese monetary policy impact are consistent with Koźluk and Mehrotra (2009), Bi and Anwar (2017), and Pham and Nguyen (2019).

Spillovers effects of Chinese monetary policy on Southeast Asian countries classified according to exchange rate regime.

The impact of Chinese monetary policy on Southeast Asian economic growth is often smaller than that of American and Japanese monetary policy. As a result, it is difficult to deny that the United States and Japan play a significant dominant role in Southeast Asia. On the other hand, China’s monetary policy shock has a positive impact on interest rates in Southeast Asian nations that have adopted a fixed exchange rate system, whereas the reverse tendency is observed in the group of countries that have adopted a floating exchange rate regime. Specifically, if China’s interest rate increases by one standard deviation, the interest rate in Southeast Asian countries having pegged exchange rates will increase by about 0.0003 % in the first quarter and last for 1 year before ending absolutely. For the other group, the interest rate in Southeast Asian countries adopting a floating exchange rate regime will decrease about 0.0001% if there is an increase by one standard deviation in external interest rate shock from China. Nevertheless, this spillover effect only lasts for a short time and is quite similar to the result of previous studies such as Johansson (2012) and Bi and Anwar (2017).

The International Monetary Policy Spillovers Effects on Southeast Asian Countries Classified According to Trade Openness

The line graphs in Figures 4 to 6 illustrate that the responses of macroeconomic variables in two groups of Southeast Asian countries to the shocks in monetary policy of the US, Japan and China are quite similar. Most of the impacts are positive which means that there is an upward trend in economic growth, interest rate and inflation index of Southeast Asian countries if Fed or the government of Japan or China raise the level of interest rate. However, only the group of countries having a low level of trade openness has a negative response to external shocks from China. Specifically, if there is a rise in Chinese interest rate by one standard deviation, a fall of about 0.0001% is found in the interest rate of Southeast Asian countries with low trade level. This effect lasts only for a short time.

Spillovers effects of the US monetary policy on Southeast Asian countries classified according to trade openness.

Spillovers effects of Japanese monetary policy on Southeast Asian countries classified according to trade openness.

Spillovers effects of Chinese monetary policy on Southeast Asian countries classified according to trade openness.

Nevertheless, the impacts of monetary policy from the US, Japan and China on Southeast Asian economies having high level of trade openness are stronger than the other countries with low trade level. These results are consistent of Koźluk and Mehrotra (2009) and Bi and Anwar (2017).

The international Monetary Policy Spillovers Effects on Southeast Asian Countries Classified According to Capital Openness

The results from BVAR model show responses of countries in Southeast Asia classified based on the level of capital openness to external monetary policies from the US, Japan and China are quite different.

According to Figure 7, the interest rate of Southeast Asian countries with high capital openness response more quickly and stronger to the impact of Fed interest rates than that of nations with low capital openness level. However, the inflation index of countries with low capital openness has a positive reaction with the US’s interest rate while the insignificant response to the US’s monetary policy shock is found in inflation of countries with high capital openness level. Moreover, the economic growth of both two groups has a positive reaction to the impact of the US’s interest rate. Specifically, countries with high capital openness have stronger response than the others with low capital openness. This result is consistent with Koźluk and Mehrotra (2009) and Bi and Anwar (2017)

Spillovers effects of the USA’s monetary policy on Southeast Asian countries classified according to capital openness.

Figure 8 shows Southeast Asian countries’ reactions to Japanese monetary spillovers depending on capital openness. Those with a low level of capital openness respond strongly and positively to policy interest rates, whereas countries with a high level of capital openness respond more negatively and weakly. In nations with high capital openness, the reaction of the inflation rate is stronger than in those with low capital openness. And in nations with low capital openness, the response of the growth rate is less intense than in countries with strong capital openness. These findings are in line with those of Koźluk and Mehrotra (2009) and Bi and Anwar (2017).

Spillovers effects of the Japanese monetary policy on Southeast Asian countries classified according to capital openness.

Figure 9 clearly shows the influence of China’s monetary policy. It is clear that Chinese interest rate volatility has a favorable impact on inflation in Southeast Asian countries, but the magnitude and duration of the impact varied across two groups, which is consistent with Bi and Anwar’s findings in 2017. In particular, nations with poor capital openness have a stronger reaction to China’s monetary policy shock. In contrast, countries with strong capital openness have a lesser inflation response. In terms of interest rates, Southeast Asian nations with high capital openness have a negative reaction to Chinese monetary policy, whilst the other group has a favorable reaction. Furthermore, according to Koźluk and Mehrotra (2009) and Bi and Anwar (2017), China’s monetary policy has a favorable impact on the economic growth rates of both groups in Southeast Asia. However, the growth rate’s response of countries with high capital openness is more intense to China’s monetary policy than that of nations having lower level of capital openness.

Spillovers effects of the Chinese monetary policy on Southeast Asian countries classified according to capital openness.

Briefly, all findings above in this study are consistent to the proposed hypotheses, which proved that the spillover effects of monetary policy from three nations including the US, Japan and China are transmitted to Southeast Asian countries through three main channels consisting of exchange rate channel, aggregate demand channel and financial channel. In this way, Southeast Asian nations are divided into groups of countries based on exchange rate regime as well as the level of trade openness and capital openness. Specifically, the exchange rate will have the effect of shifting spending, meaning that when the source countries (the US, Japan, and China) cut interest rates, it will stimulate domestic demand since the countries’ goods become more attractive. Therefore, the GDP of other countries will decrease. The aggregate demand channel and the financial channel have an effect to encourage national spending. Through the aggregate demand channel, the reduction of interest rates in the three countries above might lead to an increase in the exports of partner countries and rising GDP. Regarding financial channels, the reduction of interest rates in the source countries might shift capital flows to higher yielding markets by investing in those countries and leads to increasing GDP. It can be seen that a country’s monetary policy might have positive or negative influences depending on the strength of the transmission channels. The results of these analysis of the variable impulse response of the groups of Southeast Asian countries to the impact of the monetary policy of the US, China and Japan show that the countries with a fixed exchange rate regime, trade openness and high capital flows will have a stronger response to the policies of the source countries. This study’s results is consistent with many previous studies such as Koźluk and Mehrotra (2009) and Bi and Anwar (2017) as well as contribute to additional evidence for Mundell-Fleming’s impossibility triple theory.

Conclusions and Further Research Directions

The implications of monetary policy of the United States, Japan, and China on Southeast Asian countries are investigated in this study. The size of spillovers varies in every country, depending on factors such as the exchange rate system and the degree of financial integration. The implications of monetary policy of the United States, Japan, and China on Southeast Asian countries are investigated in this study. The size of spillovers varies in every country, depending on factors such as the exchange rate system and the degree of financial integration.

We propose a variety of policy implications for Southeast Asian countries in the face of spillovers from external monetary policy shocks based on the above findings. External monetary policy from the United States, Japan, or China has a positive or negative impact on macroeconomic indicators in Southeast Asian countries such as inflation, interest rate, and growth rate, depending on the characteristics of each group of countries. Therefore, Southeast Asian countries should adopt a flexible exchange rate policy, in line with supply and demand in market developments in the country and the world. In addition, Southeast Asian countries should promote the active role of trade openness and capital openness, strengthen economic integration, develop financial markets and mobilize international capital sources, but also do not forget to implement the goal of stabilizing inflation, synchronously operating monetary policy tools, coordinating with fiscal policy and other macroeconomic policies to stabilize the macro environment, promote import and export activities are the key to economic growth of countries. Moreover, Southeast Asian countries also need to monitor and update information on the international market to have timely and synchronous policy responses to achieve the highest policy effectiveness, take advantage of opportunities in the world interest rate environment tends to decrease deeply.

However, there are some limitations in this study which imply further research directions in this field. Firstly, due to limited access to data collection, the number of Southeast Asian countries analyzed is only 6. Secondly, the study period was limited to the period from 2009 to 2019 and has not been further updated. Therefore, future research directions need to be expanded to include the number of Southeast Asian countries to make more detailed recommendations for each country. In addition, because at the end of 2019 there was a Covid-19 pandemic that affected the macro policies of most countries, so the study on the spillover effects of monetary policies in the US and Japan, China to other countries should also be considered at this stage and compared with the period when no epidemic occurred.

Footnotes

Acknowledgements

We are deeply grateful to all those who contributed to the success of this research. Firstly, we would like to thank our primary contributor, Thuy Tien Ho, for her support, and contribution of ideas. Secondly, the authors of this paper are supported by University of Finance-Marketing, Viet Nam.

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: The authors are supported by University of Finance-Marketing, Viet Nam

Data Availability Statement

Data sharing not applicable to this article as no datasets were generated or analyzed during the current study.