Abstract

In this study, we explore the interaction between fiscal and monetary policies in Japan over a period including the Global Financial Crisis (GFC) and a phase of the Covid-19 pandemic under the presupposition that policy regimes are fixed and there are random switches between the two regimes. Using the Regime switching model, the results show that fiscal policy is more active in Japan than monetary policy, especially during the GFC and the Covid-19 pandemic. By using the Bayesian VAR model, we continue to further analyze the response of macroeconomic factors to an expansionary fiscal policy to verify the above findings once again. The results indicate that government expenditure helps boost the economy in the short-run. The positive impact of a government expenditure shock on GDP, PPI, and Investment lasts about three to four quarters, while private consumption only increases in one next quarter. These positive responses can increase the inflation rate and make the local currency overvalued, reflected in the increase in the effective exchange rate. A fiscal policy shock does not have much impact on the monetary policy, specifically, the money supply and interest rates of long-term government bonds still tended to decrease as expected by Japan. This is the basis for studying policy implications for some countries pursuing similar policies to Japan.

Introduction

While most of the world’s economies experienced explosive growth in the 1990s and 2000s, Japan’s problems seem unique compared to other countries when they experienced economic stagnation—so-called “Japan’s lost decades” (Yoshino & Taghizadeh Hesary, 2015). The per capita GDP of Japan in the 1990s grew by only 0.6%, which is quite low compared to that of the US (2.6%), and Japan has lagged behind the leading industrial countries. Researchers have criticized the Bank of Japan for not implementing sound monetary policy, which is one of the causes of the country’s lost decade (Ahearne et al., 2002; Bernanke, 2000; Jinushi et al., 2000). The Bank of Japan was blamed for being late in easing monetary policy (reducing interest rates). Until the decision to cut down interest rates was made, the reduction was not enough, even rushed to up interest rates as soon as the economy showed evidence of recovery at the end of 1993. In 1995, short-term interest rates dropped from above 2% to 0.4 to 0.5% in the summer and fall. When the Japanese economy slumped again in early 1997, the Bank of Japan was unable to lower interest rates. The economy has been in a state of deflation since 1998. But during the GFC, interest rates in Europe and the US fell to 0%, and during the economic recovery, the inflation rate did not rise again—a strange coincidence with what happened in Japan in the 1990s. No longer a special case, Japan is now a case study of what happens in an environment where the interest rate and inflation rate remain low for a long period—the situation that many developed economies, including the UK, Germany, France, Switzerland, Italy, and Singapore, are facing during the Covid-19 pandemic. According to Ubide (2019), at ZLB, monetary policy must clearly collaborate by maintaining low-interest rates for the required period of time while fiscal policy must take the lead by adopting an expansionary view. This has been the situation in Japan for the past few years, where the government has taken a fiscal expansionary policy and the Bank of Japan is collaborating with its framework for yield curve control. When interest rates are extremely low, an expansionary fiscal policy will be advantageous and have a significant multiplier effect.

The coordination of Japan’s monetary and fiscal policies has been a critical concern in policy discussions since the Bank of Japan gained more independence in the 1990s (Westelius, 2020). When traditional monetary policy tools are insufficient, combining fiscal and monetary policies can be an excellent method to boost activity and create inflation. However, it was challenging to coordinate policy in Japan due to several reasons. The lack of coordinated policies is the biggest barrier. According to Westelius (2020), the Bank of Japan’s fear of financial monetization is to blame for this failure since it prevents it from implementing large-scale quantitative easing even when economic conditions are assured. In addition, the Bank of Japan has long maintained that a supportive fiscal environment and structural changes are essential for economic recovery. In the meantime, the Japanese government has claimed that a large public debt will restrict financial support and that more aggressive monetary stimulus measures are required to avoid deflation and foster an atmosphere that will allow for the passage of difficult reforms. On the other hand, many recent studies also support the coordination between fiscal and monetary policies (Bartsch et al., 2019; Klein & Linnemann, 2019; Lawal et al., 2018). In this context, the experience of Japan can provide many important lessons in the management of policy in countries. This motivated us to carry out this study.

We first relied on the regime-switching model proposed by Chung et al. (2007) and Davig and Leeper (2007, 2011) to analyze the impact of fiscal and monetary policy regime-switching over the research period from 1998 to 2022, which includes the GFC and the Covid-19 pandemic. Our result suggested that fiscal policy is more active than monetary policy in most studied periods, especially during the GFC and the Covid-19 Pandemic.

Since the fiscal policy is more active than the monetary policy, we continue to apply the Bayesian VAR model to further analyze the impact of expansionary fiscal policy (which is being implemented by the Japanese government) on macroeconomic factors. Specifically, we examine the impulse-response function of a fiscal policy unit shock to variables such as real GDP, domestic producer price index (PPI), private final consumption expenditure, GDP deflator, real narrow effective exchange rate, general government revenue, and M2. The results show that GDP, private consumption, GDP deflator, and PPI only increase in the short term and last for the duration of the policy.

The rest of the study is organized as follows: Section 2 describes literature reviews. Section 3 presents the fiscal and monetary policy regime-switching model’s dataset, model, and empirical results. Section 4 clarifies how Japan’s fiscal policy affects macroeconomic activities during the crisis periods. Finally, the conclusion and some policy implications are presented in Section 5.

Literature Review

Theory of Fiscal and Monetary Policy

The Taylor rule is one of the important monetary policy models proposed by researcher John B. Taylor—a Professor at Stanford University (USA) in 1993. This is considered a technical tool for the central bank to regulate interest rates to stabilize economic activities. When inflation is high or the economy’s output exceeds full employment, the Taylor rule hints that the central bank should raise interest rates (a tight monetary policy) in the short run to lower inflation. On the other hand, the Taylor rule indicates that interest rates should be cut when inflation and employment are low (an expansionary monetary policy). Sometimes, monetary policy targets can be contradictory, as in the case of stagflation, when inflation is over the target while output is below full employment. In such a situation, the Taylor rule needs to determine the relative weights of the decrease in inflation to the increase in output (Taylor, 1993).

The inflation rate affects the direction of interest rates, and conversely, interest rates affect the direction of inflation (Fisher, 1930; Mishkin, 1992). If inflation is high, interest rates will basically be increased to slow down economic growth. If inflation is low, economic growth is generally slow, and a fall in interest rates is done to reduce borrowing costs and promote economic growth. More spending and a stronger economy can lead to higher inflation as borrowing capacity improves. The Central Bank aims is to strike the correct interest rate balance to control growth while keeping unemployment low and earnings high (Blinder, 1999). Excessive growth, which can lead to high inflation, is another concern for central banks.

When interest rates rise to reduce inflation, foreign investment is often attracted because interest rates are higher relative to other countries (Calvo et al., 1996). This makes the exchange rate higher. However, if inflation is higher (which reduces the purchasing power of that currency), the currency’s growth may be limited. At that time, an active monetary policy will be implemented. The Central Bank uses its powers to establish a set of policies in response to the changing economic conditions of the national economy. The opposite of active monetary policy is passive monetary policy, which involves a set of regulations that implement monetary policy. Legislation requiring a 1% drop in short-term interest rates to lower economic production by 1%, as measured by inflation-adjusted GDP, is an example of passive monetary policy. It is based on established principles rather than the policymakers’ own decisions.

When the nominal interest rate falls below zero (the zero lower bound—ZLB), monetary policy loses its power to boost the economy by further lowering nominal interest rates (Bernanke et al., 2004). However, the monetary authority may still stimulate by setting a direction for future interest rates that raises inflation expectations and lowers the present real interest rate. When the monetary authority is ready to give advance guidance for the short-run exchange rate, passive monetary policy is characterized as establishing future and present short-term interest rates while keeping a role at the ZLB.

The monetary policy of the New Keynesian view is described according to the Taylor rule. A target nominal interest rate, including an amalgamation of desired inflation and interest rate, is set to respond aggressively to deviations in inflation and production from their expected objectives (Clarida et al., 1999; L. G. Liu & Zhang, 2010; Galí, 2015).

Fiscal policy includes active fiscal policy and automatic stabilizers. Active fiscal policy is a policy where the government can alter spending levels or change tax rates to keep aggregate demand stable near the potential output (Zagler & Dürnecker, 2003). According to the direction affecting output, active fiscal policy is divided into expansionary and contractionary fiscal policy. The expansionary fiscal policy stimulates output growth, which is implemented when the economy falls into a recession. An economy that is not under inflationary pressure is a favorable condition for implementing expansionary fiscal policy. On the contrary, a contractionary fiscal policy is intended to restrain growth and inflation when the economy grows excessively, resources are overused and the risk of high inflation appears.

The two main tools of an active fiscal policy include government expenditure and tax revenue. Changes in government spending directly affect aggregate demand, while changes in tax revenue have an indirect effect through increasing household disposable income and after-tax profits of businesses. Governments can use either or both of these tools at the same time. The priority use of this tool or another when implementing fiscal policy affects the structure of budget revenue and expenditure.

Automatic stabilizers are a self-regulating mechanism in the economy. It includes self-stabilizing and self-regulating tools to prevent the economy from falling into recession and avoid economic shocks (Brown, 1955; Despres et al., 1950). The modern financial system has strong and fast automatic stabilization elements. Those are automatic tax changes (Auerbach & Feenberg, 2000). The modern tax system includes progressive income taxes on individual income and corporate profits. When national income rises, tax revenue rises, and when national income falls, tax revenue falls (the government has not yet adjusted the tax rate). As a result, the tax system serves as a quick and effective auto-stabilizer. Automatic stabilizers, on the other hand, simply minimize but do not totally eliminate economic volatility. Therefore, the change in the state budget deficit or surplus does not always come from causes related to active fiscal policy but may be caused by the impact of the economy’s self-stabilizing tools.

The monetary and fiscal policies have a close relationship, so the effectiveness of one police will affect the effectiveness of the other and consequently affect the effectiveness of the two policies, which was confirmed by Sargent and Wallace (1981), one of the first studies on the interaction of fiscal and monetary policies. Accordingly, when setting monetary and fiscal polices, policy-makers work together to decide the price level and keep the government in check. When a policy-maker goes after a goal that is not contrary to the goals of other authorities, it is called “active”; otherwise, it is called “passive.”

Ricardian equivalence is one of the neoclassical macro theories that is based on the Rational Expectations hypothesis, market-clearing logic, and other rigorous assumptions (Buchanan, 1976). According to this theory, regardless of how government spending is funded, it has no effect on aggregate demand, GDP, or welfare. They claimed that the tax cuts would result in a rise in government debt to cover spending. As a result, any rise in disposable income as a result of a tax decrease would be deemed a transitory rather than a permanent increase, and hence would not affect aggregate demand. As a result, there is a Ricardian equivalence between taxes and debt in funding an expansionary fiscal policy.

According to the Taylor rule, if the policy regime is fixed, an active monetary policy combined with a passive fiscal policy will produce the effects predicted by monetarists and Ricardians. In contrast, when active fiscal policy links with passive monetary policy, changes in taxes and currency will increase aggregate demand, which is non-monetary and non-Ricardian. Following previous financial crises such as the fall of Lehman Brothers and the European debt crisis, the governments of the main industrialized nations have pursued aggressive fiscal and monetary policies. As part of unconventional monetary policy, the central banks of those nations have adopted quantitative easing (QE) by bringing nominal interest rates to a zero lower bound (ZLB).

Previous Studies on the Regime-Switching of Fiscal and Monetary Policy

Lucas (1976) explored once-and-for-all changes rather than policy changes under the regime. Cooley et al. (1982, 1984), and Sims (1986, 1987) claimed that it is logically inappropriate to implement policies such as once-and-for-all change decisions. After all, if policymakers consider switching the regime, it will not last. If there is historical data for changes in exchange rate regimes, governments will have the distributional patterns of those regimes. Therefore, the expected decision rules of governments will reflect their assumption that policy change cannot be once-and-for-all changes.

Chung et al. (2007) discovered that policy reaction functions in the United States varied considerably over time. This research looked at how the impact of policy shocks changes when monetary and fiscal regimes follow a Markov process. The findings showed that the Taylor rule governs monetary policy in one regime, and taxes grow in lockstep with debt; in another, the Taylor rule is disregarded, and taxes are exogenous. The empirical analysis also revealed that this environment has a unique restricted non-Ricardian equilibrium. Government policy will be based on the likelihood that future fiscal and monetary shocks will have a positive impact.

Davig and Leeper (2006) estimate regime-switching rules for post-war monetary and fiscal policy in the United States and propose an estimated policy process based on a calibrated dynamic stochastic general equilibrium model. The decision rule is unique and creates stationary long-run rational expectations where tax shocks always affect output and inflation. The neutral elements of Tax in the model arise only through the mechanism that follows the price level theory. Empirical evidence in the United States showed that tax shocks have a more significant impact compared with a popular monetary model. Because long-run policy behavior dictates the presence and uniqueness of equilibrium, qualitative inferences drawn from complete sample information are more accurate than policy regimes in a regime-switching setting.

Using a Markov regime-switching model, Cevik et al. (2014) investigated the interaction between fiscal and monetary policy for certain former transition, emerging European economies from 1995Q1 to 2010Q4. The findings revealed a property shift between active and passive regimes in monetary and fiscal policy rules. According to the empirical findings, all countries employ active and passive monetary policies. Estonia, the Czech Republic, Slovenia, and Hungary have alternated active and passive fiscal systems, while the Slovak Republic and Poland appear to have a single fiscal regime.

Xu and Serletis (2016) applied the regime-switching GARCH estimation to expand the available studies on regime change. Research results on quarterly U.S. data for the period 1949Q1 to 2015Q2 suggested that the U.S. fiscal policy was active in the first half of the 1950s. However, the probability of a passive tax policy increased significantly in the mid-1980s. Moreover, fiscal policy was active after the global financial crisis, consistent with the fact that it was in response to the global financial crisis. The results also show that when monetary policy is passive, its volatility responds strongly to currency shocks.

In addition to studies that support the hypothesis of regime-switching of fiscal and monetary policy, many studies have shown that policy management needs a combination of these two policy tools. Lawal et al. (2018) used the ARDL and EGARCH models to analyze the impact of the interactions between fiscal and monetary policy on stock market behavior (ASI) and the impact of the volatility of these interactions on the Nigerian stock market. The study also provided evidence on the long-term relationship between ASI and monetary-fiscal policies and confirmed that ASI volatility is largely sensitive to fluctuations in the interaction between the two policy instruments. Therefore, both policies should be considered in parallel when formulating stock market policy because their interaction significantly affects stock market behavior.

Klein and Linnemann (2019) examined the impact of government expenditure shocks on the US economy using a time-varying parameter vector autoregression. The findings show that the current Great Recession has been characterized by abnormally strong production impulse responses to fiscal shocks. Moreover, various other components’ reactions are out of the ordinary, underscoring the period’s distinctiveness. The pattern of fiscal shock reactions does not quite meet the New Keynesian model’s assumptions for an economy with a zero lower bound on nominal interest rates, nor does it suggest that fiscal policy impacts fluctuate frequently depending on the state of the economic cycle.

Using the Bayesian VAR model, Yong and Dingming (2019) investigated the influence of government spending shocks on interest rates, particularly long-term interest rates, and the role of agents’ expectations in the impact of government spending on interest rates in the United States. According to the study, increasing government expenditure raises both long and short-term interest rates. An increase in long-term interest rates in response to a positive government expenditure shock indicates higher predicted short-term interest rates in the future, highlighting the necessity of a combined fiscal and monetary policy approach.

Guler (2019) attempts to find out the level of fiscal or monetary dominance by assessing the interaction of fiscal and monetary policies in Turkey from 2000 to 2018 using VAR and ARDL models. The results concluded that monetary policy is dominating fiscal policy in the relevant period. Specifically, according to the results obtained from the VAR analysis, monetary variables have a significant influence on fiscal variables. However, there is no evidence of fiscal influence on monetary policy. Evidence obtained from the ARDL bound test supports these findings.

Also studying the interaction between fiscal policy and monetary policy in Turkey, Büyükbaşaran et al. (2020) focused on how the behavior of financial and monetary regulators changes when they are exposed to macroeconomic shocks or policy shocks of their counterparts. Applying the Bayesian Structural Vector Autoregression (SVAR) model for the period 2003Q2 and 2018Q4, the results showed that the nature of the shocks has significant interactions between the two policies: while they are complementary in the case of aggregate demand and aggregate supply shocks (i.e. both the authorities applying contractionary or loose policy), they will move in different directions as shocks arise from policy changes (i.e. while one of the authorities follows a contractionary policy, the other implements a loose policy).

Azad et al. (2021) studied the interaction of fiscal and monetary policies of Canada in the period 1990Q1 to 2020Q4 and applied the SVAR model to assess the impact of fiscal policy during the Covid-19 pandemic. The findings suggested that fiscal policy is more active than monetary policy, and that deficit spending aids short-term economic growth. However, the study also noted that if the fiscal stimulus ends, the favorable benefits on GDP and private spending will disappear. The central bank’s inflation targeting will be hampered by rising long-term interest rates, declining investment, and rising inflation.

Chibi et al. (2021) used the State-space model with Markov-switched on Algeria’s data for the period from 1963 to 2017. The findings suggested that Algeria’s monetary and fiscal policies interact in opposition to one another during the majority of the sample period, in which the fiscal authority makes the policy decision first, while the monetary authority has a passive behavior corresponding to the given fiscal policy.

Applying structural models to Chinese data from 1993 to 2017, D. Liu et al. (2021) revealed that a regime where passive monetary policy is combined with active fiscal policy is significantly preferred. Furthermore, under this regime, fiscal policy shocks significantly affect inflation and output growth variations in both the short and long run.

The interaction between fiscal and monetary policy was the research topic of Kassab (2022). Applying Markov-switching regression on quarterly Egypt data for the period 2001Q1 to 2020Q2, the study showed that fiscal policy in Egypt always responds to government debt, although the extent of this response varies throughout periods. In addition, there has not been any synchronization in the regime change in the rules of monetary and fiscal policy in this country. After that, a sign-restricted vector autoregression (SRVAR) model was applied to analyze the impact of different potential monetary-financial policy combinations on macro variables in Egypt. Findings indicated that the effects of fiscal stimulus on real consumption and GDP in Egypt do not last longer than the stimulus due to the Ricardo Equivalence effect, in which agents expect higher taxes in the future to finance the stimulus deficit. This effect can be mitigated by an appropriate monetary policy but at the expense of the inflationary pressures that an inflation-targeted central bank has to deal with.

Previous Studies on the Fiscal and Monetary Policy in Japan

Since the collapse of its bubble economy in the early 1990s, Japan has fallen into a long stagnation (Sato, 2022). The Bank of Japan has been adjusting its monetary policy strategy over the past two decades in response to a very long period of low inflation, setting the bar for the use of unconventional measures. It has reduced policy interest rates to zero and, more recently, to negative levels, implemented several asset purchase programs, forward guidance, and, most recently, a yield curve control policy. Despite all of these initiatives, inflation in Japan has been consistently low, with rates falling significantly below the central bank’s objective in recent years (Borrallo & Río López, 2021). Okimoto (2019) examined the dynamics of inflation trends in Japan over the past three decades based on a smooth transition Phillips curve model. The results showed that the application of the policy of inflation targeting and quantitative easing in early 2013 helped Japan to get out of deflation successfully, but not enough to achieve the 2% inflation target. According to Westelius (2020), one of the reasons is that the coordination between monetary and fiscal policies is incomplete and sometimes counterproductive. Policy coordination failures and concerns about perceived violations of institutional independence have resulted in insufficient policy support prior to Abenomics and one-way stimulus in Abenomics. In addition, Japan has faced many challenges from other structural features of the economy, such as population aging and falling natural interest rates. And various monetary policy strategies implemented by the Bank of Japan have not yet succeeded in overcoming these difficulties (Akram, 2019; Borrallo & Río López, 2021).

In this study, we analyze the interaction between monetary and fiscal policies in Japan during the period 1998Q1 to 2020Q4. As one of the leading economies in the world, Japan was an exceptional case when it experienced slow economic growth and recession during the 1990s. The Japanese government continuously maintained zero lower bound on nominal interest rates, but inflation has not increased again during the economic recovery. Our result is quite similar to the situation of the US and European countries during the GFC and some developed countries during the Covid-19 pandemic. Therefore, the study of Japan’s fiscal and monetary policy interactions provides important policy implications for countries in which a similar situation occurs. Besides, the application of the Bayesian VAR model helps to clarify the responses of macroeconomic factors to the expansionary fiscal policy, which was applied in Japan during the GFC and the Covid-19 pandemic. The results confirm again that in times of crisis, expansionary fiscal policy should be maintained. Given the findings, the study proposes several policy implications for some countries of a similar nature to Japan.

Monetary and Fiscal Policies Interactions

Dataset and Model

Based on the studies of Davig and Leeper (2006, 2011); Chung et al. (2007), interest rate rules for monetary policy and tax rules for fiscal policy of Japan are considered that randomly switch between two regimes. The study uses data collected quarterly for the period 1998Q1 to 2022Q4, which includes both the GFC and the Covid-19.

Regarding monetary policy, we regard the monetary policy rule to follow Taylor (1993) based on Chung et al. (2007) and Davig and Leeper (2007) through the regime-switching model as follows:

where:

In equation (1),

Tax rules for fiscal policy are represented by the regime-switching model as follows:

where

Appendix describes the variables and data source used for the regime-switching model.

Equation (1) implies that monetary policy in various regimes responds differently to inflation and the output gap because

In addition, equation (2) shows that in different regimes, fiscal policy responds to lagged debt-to-GDP ratio, output gap, and government expenditure-to-GDP ratio differently because

Empirical Result

The log likelihood function is iteratively constructed using Hamilton filter (Hamilton, 1994). After that, it is estimated as part of the maximum likelihood estimation. Panels A of Tables 1 and 2 show the estimated parameters of the regime-switching model for fiscal and monetary policy in equations (1) and (2); panel B shows the estimated transition probabilities.

Regime Switching Model of Monetary Policy.

Note. Sample period, quarterly data, 1998:Q1 to 2022:Q4. Numbers in parentheses are p-values.

Regime Switching Model of Fiscal Policy.

Note. Sample period, quarterly data, 1998:Q1 to 2022:Q4. Numbers in parentheses are p-values.

The results of the switching in monetary policy are presented in Table 1. In both active and passive regimes, the relationship between inflation and monetary policy does not follow the Taylor rule. As shown in Panel A, CPI has a statistically insignificant negative impact on the average interbank interest rate (

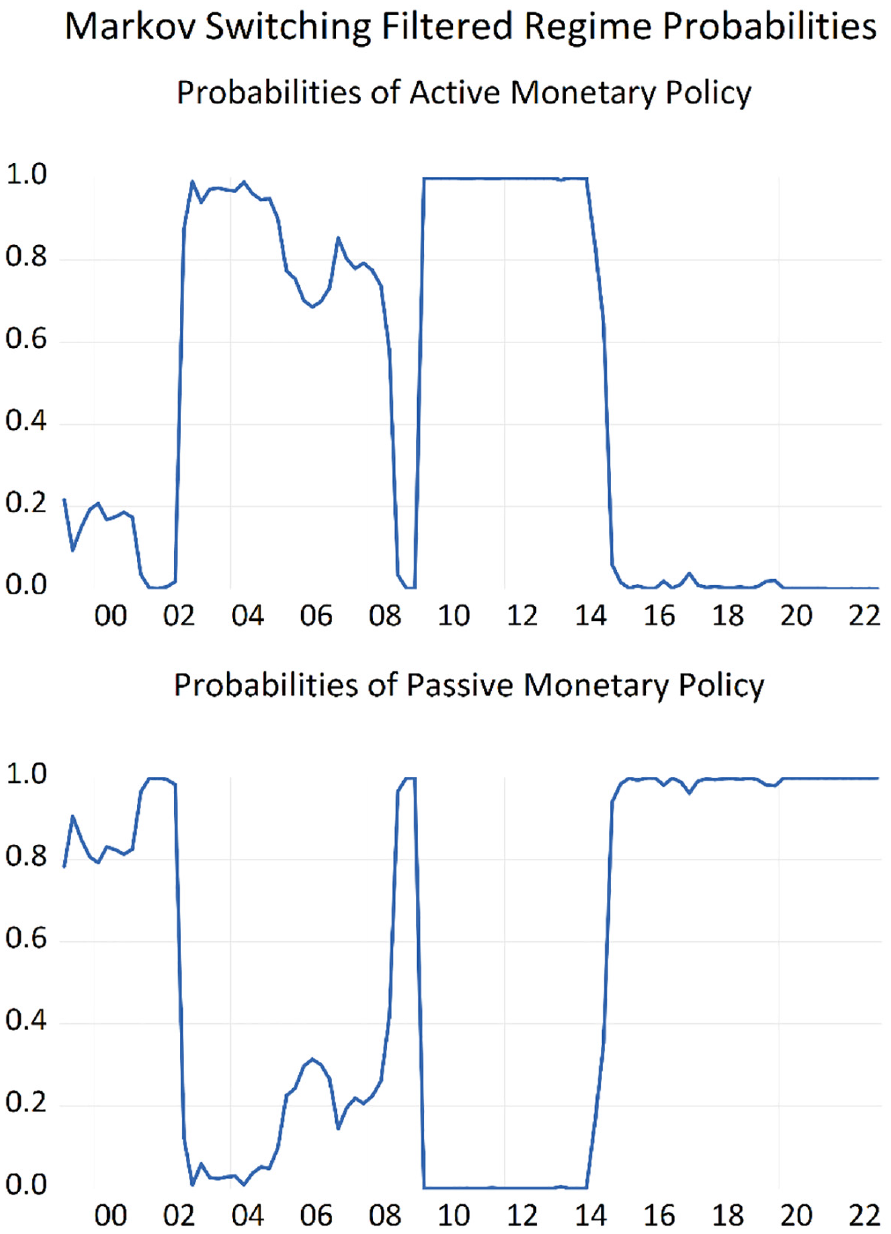

Figure 1 presents the probabilities of a monetary policy switching for active and passive regimes, respectively. These probabilities are presented at time t in accordance with the full sample data. It is shown that the monetary policy moves flexibly and switches continuously between the active and passive regimes. However, during the GFC and the Covid-19 pandemic, the monetary of Japan was passive.

Monetary regime probability.

Table 2 shows the regime-switching in fiscal policy. It switches from active regime, responding negatively to government debt (

The probabilities of a fiscal policy switching for active and passive regimes are presented in Figure 2. It can be found that Japan’s fiscal policy has been active most of the study period, especially during the GFC and the Covid-19 pandemic. Therefore, to further study the impact of expansionary fiscal policy on macroeconomic factors and analyze the influence of expansionary fiscal policy on the economy, we analyze the impulse-response function of a positive government expenditure shock (also known as a deficit spending shock) based on estimates from the Bayesian VAR model.

Fiscal regime probability.

Fiscal Policy Shock During GFC and Covid-19 Pandemic

Data and Model

Following the approach of Uhlig (2005), Mountford and Uhlig (2009), the study applies an impulse-response function from the empirical estimates of the Bayesian VAR model to analyze the response of macroeconomic factors after a fiscal policy shock. The BVAR model are as follows:

where

Consider the following conditional prior distribution of the VAR coefficients

where the vector b is the prior mean of the coefficients of each equation,

where

The Minnesota prior on

The BVARs are also estimated based on a normal-Wishart prior distribution for the parameters. While the Minnesota prior does not take into account any uncertainty in the estimation of the variance-covariance matrix of error terms,

Following the research by Azad et al. (2021), the BVAR model includes the following endogenous variables: real government final consumption expenditure (GE), the real GDP (GDP), private final consumption expenditure (CSP), gross fixed capital formation (INV), domestic producer prices index (PPI), GDP deflator (DEF), real narrow effective exchange rate (ER), money supply (M2), general government revenue (GRE), and yield on long-term government bonds (BY). The data for these variables have been retrieved quarterly from 1998Q1 to 2022Q4 from various available sources such as the Federal Reserve Bank of St. Louis (FRED) database (for GE, GDP, CSP, INV, PPI, DEF, ER, BY), World Economic Outlook (WEO) Database (for M2, GRE). The real narrow effective exchange rate and M2 are calculated monthly, while the general government revenue is annual. Therefore, the arithmetic average was used to convert them to quarterly frequency. The description and data sources for these variables are presented in Table A2 of Appendix.

Empirical Result

Figure 3 shows the responses of macroeconomic factors to a fiscal policy shock. As government expenditure increases in the first quarter, GDP and CSP increase in the following quarter, but then fall again. If the economy is experiencing a negative output gap, a loose fiscal policy can boost the economy and narrow the gap in the short term. However, the positive effect on CSP and GDP only lasts one quarter. This result is concordant with Blanchard and Perotti (2002), Coenen et al. (2012), and Owyang et al. (2013), which provided evidence that a positive shock of government spending will have a positive effect on output. Specifically, Blanchard and Perotti (2002) provided evidence that a positive shock to government spending will positively affect US output after the war period. According to Coenen et al. (2012), the euro area’s discretionary fiscal policy undertaken during the financial crisis increased quarterly real production. Furthermore, according to Owyang et al. (2013), government expenditure has a considerable influence on the Canadian economy during a recession.

The impulse—response function of macroeconomic factors after a government expenditure shock.

In addition, after a government expenditure shock, government investment increases and lasts for four quarters, consistent with the findings of Barsky and Sims (2012). During recessions, Barsky and Sims (2012) discovered that more government investment is related to higher output and consumption growth than during normal periods. Their research found that expenditure shocks during a recession had a longer-lasting impact on government investment rises than during a normal era.

The study shows that long-term bond yields decline after a government expenditure shock for long-term government bonds. This response contrasts Klein and Linnemann (2019), Yong and Dingming (2019). News of increased government spending will significantly increase bond yield in the short and long-term as public expectations about monetary policy change; they question the government’s ability to repay its debt and require higher interest rates. This result is almost impossible in Japan, where monetary policy is managed to achieve inflation targeting. In response to the Covid-19 pandemic, the Bank of Japan decided to maintain negative interest rates and announced some adjustments to monetary policy. Accordingly, the short-term interest rate remained at −0.1% and the long-term interest rate was 0% to make the inflation target 2% and restore the economy.

This result might be attributable to demand-pull inflation, which occurs when government expenditure exceeds income, resulting in increased private consumption and, as a result, higher real GDP. While the central bank strives to reach or surpass potential GDP, increased government expenditure can cause inflationary pressures on the economy.

Furthermore, studies show that the real narrow effective exchange rate increases significantly in the face of deficit expenditure, implying that the local currency is overvalued. This result aligns with the Mundell–Fleming–Dornbusch (MFD) model and the standard dynamic general-equilibrium model in a perfect financial market, which anticipates that an unexpected rise in government expenditure will boost the dynamic price of the local currency in practice (Bouakez & Eyquem, 2015). According to the MFD model, an increase in the local currency due to an increase in aggregate demand is the outcome of an increase in public expenditure. Inflationary pressure is created in the country as aggregate demand rises, leading the price of local goods to rise faster than the price of imported commodities. Bouakez and Eyquem (2015) emphasized that “in dynamic general-equilibrium models with complete markets, the real appreciation ensues from a risk-sharing condition that relates the real exchange rate to the ratio of marginal utilities of consumption across countries. As long as the composition of the consumption basket differs across countries (due, for example, to home bias in preferences), an increase in public spending in the domestic country raises the tax burden of domestic households relative to the rest of the world, which in turn raises the relative shadow value of wealth in the domestic country and appreciates its currency in real terms.”

The money supply decreases in response to a government spending shock. This comes from maintaining low long-term interest rates (0%) and accepting negative short-term interest rates in Japan. In addition, we also find a significant increase in investment in response to a government spending shock. Maintaining low-interest rates will encourage businesses to increase investment and reduce financial burdens, especially in periods of crisis. This finding is in contrast to the US case, where an increase in government expenditure will lead to a considerable decrease in private investment according to Bouakez and Rebei (2007).

Conclusion

Using Japanese data from 1998Q1 to 2022Q4, through a regime-switching model, this study demonstrates that fiscal policy is more active than monetary policy. Further analyzing the response of macroeconomic factors to an expansionary fiscal policy through an impulse response function based on estimates from the Bayesian VAR model, we find that government expenditure helps boost the Japanese economy in the short term. The positive effect of government expenditure shocks on GDP, PPI, and investment lasts about three or four quarters, while this impact on private consumption only lasts for the next one quarter. These positive responses can increase inflation and make the local currency overvalued, which is reflected in the increase in the effective exchange rate. Fiscal shock does not have much impact on monetary policy, in particular, money supply and long-term bond interest rates still tend to decrease, in line with what Japan is aiming for.

From the above research results, we propose some policy implications. To minimize the impact of the crisis and pandemic on the economy, countries should use expansionary fiscal policy rather than using monetary policy to regulate the economy. In particular, government spending plays a very important role when consumer spending sharply declines. The government needs to act as the main spender, the main platform for economic growth in times of crisis. In the short-term, expansionary fiscal policy may not affect monetary policy, specifically, money supply and long-term bond interest rates still tend to decrease to encourage investment and reduce financial pressure in the short term as expectations of Japan and some countries having similar characteristics.

However, expansionary fiscal policy has an effect on the long-term stability of monetary policy. For example, the expectation of a large and prolonged budget deficit due to poor budget expenditure efficiency leading to high government debt demand reduces confidence in the economy and increases financial market volatility. Large budget spending on inefficient public investment also strongly affects inflation, inflation expectations, and balance of payments. In particular, high inflation expectations reduce the effectiveness of the monetary policy.

Besides the obtained results, our study still has some limitations. One of them is the scope of the study as this paper was only conducted on the Japanese dataset. Future research can also extend to more countries instead of just one country like Japan, or compare specific countries/groups of countries, in order to test if the above results are robust at both country and global levels.

Footnotes

Appendix

Variable Description and Data Source of the Bayes VAR Model.

| Signs | Descriptions | Research | Source |

|---|---|---|---|

| GDP | Real gross domestic product, taken the form of logarithm | Azad et al. (2021) and Kassab (2022) | Federal Reserve Bank of St. Louis (FRED) database |

| GE | Real government final consumption expenditure, taken the form of logarithm | Azad et al. (2021) and Kassab (2022) | Federal Reserve Bank of St. Louis (FRED) database |

| CSP | Private final consumption expenditure, taken the form of logarithm | Azad et al. (2021) and Kassab (2022) | Federal Reserve Bank of St. Louis (FRED) database |

| INV | Gross fixed capital formation, taken the form of logarithm | Azad et al. (2021) and Kassab (2022) | Federal Reserve Bank of St. Louis (FRED) database |

| PPI | Domestic producer prices index | Azad et al. (2021) | Federal Reserve Bank of St. Louis (FRED) database |

| DEF | Gross Domestic Product Deflator index, taken the form of logarithm | Azad et al. (2021) and Kassab (2022) | Federal Reserve Bank of St. Louis |

| ER | Real narrow effective exchange rate | Azad et al. (2021) | Federal Reserve Bank of St. Louis (FRED) database |

| M2 | Money supply M2, taken the form of logarithm | Azad et al. (2021) | World Economic Outlook (WEO) Database |

| GRE | General government revenue, taken the form of logarithm | Azad et al. (2021) and Kassab (2022) | World Economic Outlook (WEO) Database |

| BY | Yield on long-term government bonds | Azad et al. (2021) and Kassab (2022) | Federal Reserve Bank of St. Louis (FRED) database |

Acknowledgements

The author acknowledges being supported by the University of Finance-Marketing, Viet Nam.

Declaration of Conflicting Interests

The author declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author received no financial support for the research, authorship, and/or publication of this article.

Data Availability Statement

The data that support the findings of this study are available from the corresponding author upon reasonable request.