Abstract

This paper examines the complex nexus between regulation and inequality in Zimbabwe’s microfinance and tourism sectors. Rural Small to Medium Enterprises in Tourism (SMETs) is typical in the informal sector. However, SMETs in rural areas face financial, regulatory, and exclusionary constraints. This paper follows a qualitative literature review methodology guided by an exploratory design. In addition, one secondary case study was included to highlight the lived realities of SMETs. Findings indicate a complex connection between regulation and inequality in the economy. Overregulation leads to corruption, marginalization, and exclusion of small business activities. SMETs are constrained because they need access to finance for business growth. Thus, the nexus between the two variables profoundly impacts policy. The government must entangle the relationship for policy directions in the microfinance and tourism sectors. The paper concludes that the nexus between regulation and inequality needs urgent attention. The paper’s originality is based on using a systematic literature review to assess how regulations affect microfinance’s ability to fund rural SMETs so that these areas could have economic opportunities that would improve the livelihoods of people residing in these areas, thereby addressing inequalities. Furthermore, it contributes to the debates on the complex relationship between regulation and inequality of two sectors (microfinance and tourism) in Zimbabwe. It also informs future lines of research on the subject. Due to noted limitations on the research design used, more comprehensive empirical studies are required to understand the complexity of the nexus.

Plain Language Summary

This paper explores the link between regulation and inequality in Zimbabwe’s microfinance and tourism sectors, with a focus on rural Small to Medium Enterprises in Tourism (SMETs). It employs a qualitative literature review methodology. One secondary case study is included to understand the constraints faced by SMETs in rural areas. The results indicate that overregulation leads to corruption, marginalization, and exclusion of small business activities, hindering SMETs’ access to finance and business growth. The paper highlights the urgent need for policymakers to address the complex nexus between regulation and inequality and calls for further empirical research to understand the intricacies of the relationship. It contributes to debates on the regulation-inequality connection and offers insights into the future lines of research. However, it has limitations due to the research design, highlighting the need for more comprehensive empirical studies.

Introduction

Zimbabwe underwent a trying period between 2000 and 2009, which most authors have dubbed “the lost decade” (see, e.g., Kaminski & Francis, 2011; Mkandawire, 2020). In these years, Zimbabwe experienced deep-seated problems of poverty and unemployment. The economy was characterized by hyperinflation, acute unemployment, and severe shortages of essential commodities (Chikoko & Kwenda, 2013; Miller & Ndhlela, 2020). These challenges trickled to the microfinance and Small to Medium Enterprises (SMEs) sectors. The microfinance sector is meant to close the financial gap, especially for those who cannot access formal institutions’ finance. Therefore, SMEs, especially the informal ones, are serviced by the microfinance sector because of their financial profiling (Mago & Hofisi, 2016). The economic crisis threatened many SMEs who had to close their establishments, thereby affecting microfinanciers (Chikoko & Kwenda, 2013). During the crisis, the Central Statistical Office (CSO) in 2007 reported an unemployment rate of 80% (Luebker, 2008). Reports by DFID (2009) and Lemelle and Stulman (2009) in Africa Outlook pitched the Zimbabwean unemployment rate to 90%. The prevailing conditions thus allowed for an exceedingly high level of unemployment, and most macro-economic fundamentals faced a near-collapse. Poverty levels were estimated at around 80% (Kabonga et al., 2021; UNDP Zimbabwe, 2012). The country’s socioeconomic status has mostly stayed the same, as Zimbabweans are still experiencing increased levels of poverty and inequality (World Bank, 2022). For example, Zimbabwe’s multidimensional poverty index was 42.2% in 2019, while in 2017, a poverty rate of 33.9% was recorded (World Bank, 2020, 2022). The Central Intelligence Agency’s (CIA, 2022) World Fact report estimated that 38.3% of the population lived under the poverty line in 2019. Spatial inequalities further extenuate the poverty levels as people in rural areas are highly affected. In 2011, 76% of rural households living in poverty compared to 24% of those residing in urban areas (UNDP Zimbabwe, 2012, p. 8). The rural populace is therefore subjected to inequalities caused by a lack of opportunities (Kabonga et al., 2021; Swinkels et al., 2019). As a result, some migrate to urban areas for opportunities that are also inadequate due to the economic climate (CIA, 2022).

Community-based small business ventures could benefit the poor in rural areas. Pranita et al. (2022) argued that tourism could help rural communities fend for themselves without depending on external stakeholders. Rogerson and Rogerson’s (2021) work talks about alternative tourism development where activities in rural areas include gastronomy, agritourism, camping sports, events, and arts and crafts that could help invigorate economic activities for the rural poor. The sector is also crucial in exposing rural people to sustainable economic activities to help alleviate poverty and inequalities (Dube & Nhamo, 2020). However, the Zimbabwean tourism sector has encountered various challenges, like the economic crisis of 2000. As a result, the tourism sector was deeply affected, especially SMETs (Baipai et al., 2022). Dube and Nhamo (2020) also add that the tourism sector has been affected by the drought resulting from climate change, especially in areas like Kariba and Victoria Falls. Recently the COVID-19 pandemic-induced lockdowns made many SMETs shut down their businesses while others had to diversify their businesses to earn a living (K. M. Adams et al., 2021; Makoni & Tichaawa, 2021).

The importance of tourism-related activities in addressing issues of poverty can be seen in efforts such as the anti-poverty tourism interventions (ATI) observed in the 21st century (Aramberri, 2020; Oskam et al., 2022; Phi et al., 2018). These initiatives ensure that the poor reap the benefits of tourism proceeds. Hence, financing models like microfinance tourism (MFT) have been introduced to support tourism economic activities and the poor. Microfinance is believed to be one viable alternative to fighting poverty (Gakpo et al., 2021; IFAD, 2007). Therefore, MFT is an ATI that uses microfinance and tourism to address poverty issues in areas where tourism occurs (Aramberri, 2020; Oskam et al., 2022; Phi et al., 2018). In developing countries like Zimbabwe, regulatory processes should create a conducive environment to support such initiatives.

The socioeconomic, environmental, and pandemic-related issues and regulation factors have added to the problems affecting SMETs. A poor regulatory environment has led to tourism leakages where the excess money from tourism activities was leaving the country (Chirenje et al., 2013). In contrast, local tourism beneficiaries only receive the crumbs of those funds (Chirenje et al., 2013). However, if the tourism sector were well regulated, there would be no significant disparities between the money made by businesses at the grassroots level and the intermediary service providers working with these businesses. Brandl et al. (2019) opine that those stringent regulations benefit businesses, although it might not seem so when some regulations are introduced.

Nevertheless, limited studies explore regulatory matters about SMETs and microfinance in Zimbabwean. The nexus is brought forth because tourism can potentially increase Zimbabwe’s economic activities, thus lessening unemployment and poverty, especially in rural communities with few opportunities (Musavengane et al., 2020). However, when funding is, inaccessible SMETs are at risk as their survival is under threat when businesses lack resources to remain afloat (Musavengane et al., 2020). Furthermore, commercial banks are aloof to funding small businesses due to their inability to meet loan requirements such as collateral (Dube & Dube, 2016; Fanta, 2015; Mutsindikwa & Gelderblom, 2023). In these instances, microfinance and informal finance are the only options for securing loans (Mago & Modiba, 2022). However, given the challenges of the microfinance sector in Zimbabwe, more research is required to understand how SMETs financing challenges can be addressed.

This paper aims to explain the complex debate on the nexus between regulation and inequality in Zimbabwe’s microfinance and tourism sectors. Less developed countries (LDCs) have high inequality levels yet are highly regulated (Chambers et al., 2019). Their effects on tourism are also assessed on small to medium enterprises (SMETs). Therefore, the objective of this study is to investigate the complex link between regulation and inequality in the two sectors.

This paper aims to contribute to the existing body of knowledge by exploring the relationship between regulation and inequality in the microfinance and tourism sectors. While previous studies have examined the impact of regulations on these sectors (see, e.g., Makina et al., 2014; Price, 2020; Spiegel, 2009; Zibanai, 2013, 2016), the nexus has yet to be investigated. Proposed policy recommendations will help policymakers improve access to these sectors and reduce inequality while promoting inclusive economic growth.

Following this introduction is section 2, which discusses the literature on the regulatory environment, microfinance, and its related issues on poverty and business support, survival strategies for micro financiers and SMET challenges in Zimbabwe. Section 3 provides the study’s theoretical framework, and section 4 focuses on the methodological process. Results are discussed in section 5, and section 6 concludes the study.

Literature Review

Access to finance plays a critical role in the business sector and can determine the sector’s success and failures. For example, lack of finance has led to businesses in Zimbabwe failing due to not receiving the required finance from the formal financial sector (Kwenda & Matanda, 2015). In addition, when the financial sector is underdeveloped to service all businesses, especially SMEs, they turn to short-term financing options like microfinance (Kwenda & Matanda, 2015). The microfinance sector is therefore researched in this paper to assess how it can close the gaps of funding for SMETs when properly regulated and how such changes can influence the inequalities experienced in Zimbabwe in the following subsections.

Regulatory Environment

The regulatory environment can impact countries’ socioeconomic conditions, particularly the business environment. Regulations are deemed necessary, especially in maintaining a balance between the financial providers and consumers of their services by managing risks (Muganyi et al., 2022). However, it is argued that stringent regulations affect the creation of businesses, thereby necessitating inequalities as not all aspiring entrepreneurs can participate in business ventures (Chambers et al., 2019). Chambers et al. (2019) established that countries with stringent regulations have high-income inequalities. The Gini coefficient is one of the tools used to measure income inequalities (Chen et al., 2010). The coefficient ranges from 0 to 100, with 0 representing no inequality and 100 representing the highest inequality (World Bank, 2022). Marginalized populations attribute income inequalities to limited access to resources, opportunities, and employment.

For example, a developing country like South Africa had a Gini coefficient of 69.3 in 2008 and 63 in 2014 (World Bank, 2022). The Gini coefficient of Zimbabwe was ranked at 50.3 in 2019, indicating low inequalities compared to South Africa. Neighboring countries also show a high Gini index; for example, Botswana was at 53.3, Mozambique at 54, Zambia at 57.10, Namibia at 59.10, and lower indices for Algeria at 27.6 and Mauritius at 36.8 in 2017 (World Bank, 2022). The latter has been cited for having relaxed regulations making it one of the better countries for business in Africa. The World Bank’s report on the Ease of Doing Business (DB) (2020) ranked Mauritius number at 13, South Africa at 78, Zambia at 84, Botswana at 87, Namibia at 104, Mozambique at 138, Zimbabwe at 140, Algeria at 157. The DB ranking of Algeria versus its Gini index contradicts the results by Chambers et al. (2019). However, comparing the DB ranking of Zimbabwe’s neighboring countries with their Gini index supports Chambers et al.’s (2019) argument about inequality.

Microfinance and Poverty Alleviation

Microfinance was introduced as a tool that could be used to fight poverty by extending credit to the poor underserved by the formal financial sector. Availing credit to the poor was viewed as helping individuals finance projects that could alleviate poverty (Modisagae & Ackermann, 2018). There are reports on how microfinance has facilitated access to finance, thereby closing financial access inequalities and alleviating poverty (Khandker & Koolwal, 2016; Wang & Ran, 2019). However, some areas are not serviced by this sector, thus creating inequalities. For example, some people in rural communities do not have access to microfinance (Hasan et al., 2020). Alternative modes of ensuring that microfinance reaches everyone include digitization of the sector, which is a sound alternative, as seen in some developing countries like China (Cao et al., 2021). This alternative might be efficient in well-networked areas; for countries like Zimbabwe, where poor infrastructure affects connectivity, this might not readily resolve experienced challenges of accessing microfinance.

Furthermore, Microfinance is inundated with challenges that cloud its relevance in reducing poverty because of commercialization, which has led to microfinanciers charging high-interest rates, thereby impoverishing their clients (Wang & Ran, 2019). Additionally, some challenges experienced by the sector, such as debt defaulting, are partially motivated by regulations not considered by lenders and creditors (Modisagae & Ackermann, 2018). Therefore, the sector needs to be regulated to ensure that all stakeholders are protected.

Although a well-regulated microfinance sector can optimize its service provision and reach rural areas, some scholars question its impact. A study conducted in Nigeria and Zambia revealed a growth in the sector because of regulations (Siwale & Okoye, 2017). These authors further state that the existing regulations have not effectively serviced the previously excluded, thus perpetuating inequalities. This disconnection was due to the regulations not being innovative to address the needs of the sector and its intended beneficiaries (Milana & Ashta, 2020). Siwale and Okoye (2017) stated that these non-inclusive regulations were adopted from the banking sector. A sector already excluding most rural communities and small businesses. Governance issues also contribute to the satisfactory performance of MFIs and their social impact (Imran & Shafique, 2022). Thus, external regulations (government-induced) are insufficient to regulate the sector appropriately. They must be reformulated and closely monitored to ensure the sector’s commitment to its social pact.

The microfinance sector is criticized for not reaching the marginalized groups. It is not reducing gender inequities unless regulators can enforce this aspect (Johnson, 1998). Most of them do not reach rural areas but are concentrated in cities (Gakpo et al., 2021). Also, microfinance does not always create jobs (Gakpo et al., 2021). Arguments could be that microfinance is not always used for economic activities. Gakpo et al. (2021) further reported that Ghanaian SMEs did not source funds from microfinance institutions in their study. In this context, it makes sense for microfinance not to positively impact job creation.

Microfinance in Zimbabwe

Poverty and unemployment issues were already rife in Zimbabwe prior to 2000. The economic crisis just intensified what the country was experiencing. Therefore, the economy still needs pro-poor interventions to help the poor escape poverty. The current macroeconomic environment has not helped the situation but forced many into poverty. The economy faced daily stresses, especially in 2008, as was manifested by cash shortages, rampant price increases, and acute shortages of non-compressible products such as fuel and foreign currency (Chikoko & Kwenda, 2013). During this period, the economy survived by importing essential commodities from individuals from neighboring countries. Sithole and Muguti (2018) described the period as three lost decades since several opportunities were lost due to economic and political challenges. These political and economic challenges deepened poverty hence the need for mitigation strategies. The aftermath of the crisis is evident from the high emigration rate as Zimbabweans seek better opportunities (Swinkels et al., 2019).

Microfinance is relevant because financial access for business purposes is a challenge for entrepreneurs needing to start or diversify businesses, especially in countries like Zimbabwe (Baipai et al., 2022; Basera et al., 2022). However, since tourism activities in rural spaces are linked to natural resources, some entrepreneurs may need funds to create tourism-related activities for business purposes. For instance, Baipai et al. (2022) suggest that farms with access to dams can participate in agritourism by starting watersport activities. Such activities can contribute to the tourism value chain (e.g., catering and cultural activities). The authors further found that lack of financial support affects businesses’ sustainability in some rural areas in Zimbabwe. Therefore, microfinance may play a catalytic role in creating tourism-related businesses because subsectors like agritourism will require funds. For example, the study by Basera et al. (2022), which investigated traders servicing the tourism sector in the Vumba mountains area, discovered that these business owners did not have access to funds to support their businesses. However, opportunities for the microfinance sector presented above are unfortunately linked with government administrative issues such as regulatory policies.

Regulation of Zimbabwe’s Microfinance Sector and Its Impact on Tourism

Macroeconomic stability, political stability, prudent banking and supervisory practices, and liberalized interest rates are important policies requiring the government’s attention (J. Adams & Raymond, 2008). Liberalized interest rates contribute to the financial development needed in developing countries (Muganyi et al., 2022). Despite the socioeconomic and political challenges faced by SMETs, they demonstrated resilience. The difficult socioeconomic and political conditions led to the growth of the informal sector as the formal sector collapsed (Sithole & Muguti, 2018). It played a vital role in the economy during the crisis. SMEs became economic drivers that sustained people’s livelihoods (Makoni & Tichaawa, 2021; Mxunyelwa & Henama, 2019). This realization prompted the government to find ways of promoting the microfinance sector.

In Zimbabwe, the microfinance sector operated without a national policy for decades. It was guided by the outdated and non-supportive Moneylending and Rates of Interest Act [Chapter 14:14] of 1930 (Makina, 2009). The Act did not support the sector’s growth (UNDP Zimbabwe, 2008; ZAMFI, 2007). It could have served the microfinance sector more adequately. This failure led to the commercial banks’ Act regulating the sector, which was a misfit (Makina, 2009). The lack of pertinent regulations and the economic crises contributed to a collapse of the sector with attrition of over 1,600 businesses between 2003 and 2009 (Makina, 2009).

In 2005, a Consultative National Microfinance Task Force was formed by the Reserve bank of Zimbabwe (RBZ) to investigate the possibility of developing a National Microfinance Policy. Members of the task force were government ministries, apex organizations of microfinance, such as the Zimbabwe Association of Microfinance Institutions (ZAMFI) and moneylenders, microfinance institutions, development partners, and the RBZ (National Task Force on Microfinance, 2008). Their mandate was to develop guidelines to promote sustainability in the microfinance sector. ZAMFI was the main stakeholder who advocated for the policy. The policy development process started with the establishment of a task force in 2005 whose mandate was to develop guiding principles for a sustainable microfinance industry.

Ernst and Young was commissioned to conduct a survey between December 2005 and March 2006. The survey found a 30/70% split between the economically active population served by formal and informal financial services, respectively (RBZ, 2006). The findings demonstrated the dire need for a policy to support the microfinance sector, leading to the National Microfinance Policy in 2008. The policy’s main objective was to promote a sustainable microfinance sector. This policy would promote financial inclusion, promote synergy between the formal and informal financial sectors, enhance financial services delivery to the poor and SMEs, and enhance rural transformation. Additionally, the policy would support linkages between the formal and informal financial systems.

In 2008, the Southern Africa Microfinance and Enterprise Capacity Enhancement Facility (SAMCAF), a non-governmental organization (NGO) supporting the microfinance sector, conducted a study in the SADC region. SAMCAF (2008) synthesized the salient features of the National Microfinance policy. They recommended the creation of an enabling regulatory environment to enhance sustainable microfinance. This environment could be achieved by establishing deposit-taking microfinance banks like the famous Kenyan Rural Enterprise Program (K-REP) bank. Another recommendation was to integrate microfinance into the formal financial system. This integration would ensure access to financial services on a sustainable basis.

Furthermore, capacity-building programs were suggested to stabilize the microfinance sector. This capacity-building would close the technical skills gap between microfinance institutions (MFIs), regulators, and apex organizations. In addition, a need to establish a credit reference bureau was identified (SAMCAF, 2008) to improve information and credit risk management.

Despite these efforts, the growth of the microfinance sector is still a concern, especially given that in 1997 the sector used to service small and micro-enterprises with close to $2.6 million (Makina, 2009). This growth meant the demand for such services was high across the small business sector. Makina (2009) further states that the demand during that period was $ 31 million. The client demand has increased steadily since 2011 when 58,325 were recorded (Chamboko & Guvuriro, 2022). Additionally, the demand increased to 454,428 in 2019 and declined to 303,323 in 2020, with the COVID-19 contributing to the downward trend. In 2021, demand increased to 307,655, a decline of 285,634 in the third quarter of 2022 (RBZ, 2022). The downward trend reached a low of 280,172 in June, indicating challenges in the microfinance sector (RBZ, 2022). Moreover, of the recent 285,634 loans, only 124,216 were disbursed to women.

To strengthen the National Microfinance Policy, the government amended the 1930 Act to the Microfinance Act [Chapter 24:29] in 2013. It was then amended to the Microfinance Act [Chapter 24:30] No. 6 of 2019 to close identified gaps and improve the microfinance support mechanism, which needed to be improved. Current guidelines originated from the improved 2019 document. The Microfinance Act (2019) provisions how microfinance businesses should operate. It details the interest to be charged, licensing and registration requirements, and how to conduct business lawfully. It further offers protection to the consumers of this product. Consumer protection is crucial, given that some MFIs charge exorbitant interest rates to grow their businesses quickly. Not rendering a fair service that empowers borrowers leads to customer dissatisfaction that may affect future businesses. Dzingirai et al. (2021) affirm that there was some level of disloyalty from MFIs clients due to not being satisfied with the service rendered by these institutions. However, one of the criticisms of the Act is that it is outdated and thus fails to serve the microfinance sector (Makina, 2009). This failure was a misfortune that affected the poor and SMETs dependent on the sector. Even after the rise of some micro financiers in the last decade (Dzingirai et al., 2022), it is reported that Masvingo experienced an attrition of 180 micro financiers from 200 between 2008 and 2018 (Matanda & Matanda, 2019). Moreover, the microfinance attrition rate in Masvingo was due to de-registrations caused by regulatory burdens.

Survival Strategies of Micro Financiers

During the fiscal crisis, the guiding regulatory statutes posed challenges for microfinanciers, as the lenders could not increase their interest to offset the inflation cost (Chikoko & Kwenda, 2013). In such conditions, there is a threat to the survival of microfinanciers. Chikoko and Kwenda (2013) suggest that microfinanciers should diversify their service portfolios to have comprehensive coverage of customers to survive market-related challenges. They further suggest that stakeholders in this sector must pressure governments to implement regulatory measures to support the sector. The call for better policies to regulate the microfinance sector was also noted in a Kenyan study where Domeher et al. (2017) stated that the country’s deteriorating microfinance sector could perform better and be sustainable if there were supportive policies. Other strategies include microfinance tourism (MFT), where microlending is sustained by raising funds while low-interest rates are charged to small businesses (Phi et al., 2018). According to Phi et al. (2018), the stakeholders involved in this fundraising model are the local entrepreneurs needing a low-interest loan, a micro financier, and tourists. The tourists use the services of a local entrepreneur while experiencing the culture and challenges of the village; in return, tourists contribute to the success of the micro financier. The microfinancier’s role is to provide microcredit and other financial services necessary to support these poor communities. Partnerships with private businesses are other cited strategies for the microfinance sector to raise capital to service a wider market and to grow the business (Matanda & Matanda, 2019). Recently, the Microfinance Act included the concept of a “perpetual license” to support the sector (Bhebhe, 2020). As a result, MFIs are no longer required to renew operating licenses annually. Bhebhe (2020) further reported that authorities anticipate that perpetual licenses will stimulate an increase in the number of investors to boost the sector’s growth, which drives the growth of SMEs.

Studies have researched the contribution of tourism to the economic environment of Zimbabwe as well as how it supports poverty alleviation efforts (Baipai et al., 2022; Basera et al., 2022). However, there is limited research into how the struggling SMET sector is affected by the lack of a regulatory environment to support micro financiers so that the poor can access affordable loans; this paper aims to fill that gap. The national microfinance policy should set a clear direction. The government should enhance vibrancy in the sector by speeding up the development and adopting an appropriate regulatory and supervisory framework. The 2005 policy framework still needs to be finalized in line with ZAMFI’s analysis. Below is a case of an SMET in the Zaka district of Masvingo province, Zimbabwe.

Case of Madanhire Village Tourism in Zaka Valley

Madanhire village tourism is an initiative started by a self-funded entrepreneur. This case is used to highlight the issues related to funding, as the researchers could only find one source that has been published in this area. Activities involve providing rural tourism opportunities to travellers (Axelrod, 2021). The establishment arranges transport for tourists from Masvingo town, about ninety kilometres away, in the Zaka district in Masvingo province. Located in the Zaka valley near Gunguvu School, a traditional African homestead was transformed into a rural tourist hub. Tourists live with the Madanhire family in a rural home for a prolonged period.

Additionally, they eat traditional foods cooked by family members (Axelrod, 2021), and guests help with the daily farm harvesting and cooking. Tourists are also exposed to rural-style African animal care. Furthermore, hiking activities in the hilly environment of the village are available. Tourists join local traditional parties with African dancing and drumming. In addition, they socialize with members of the other extended family members, friends, and community members (Axelrod, 2021). Payment depends on the time tourists spend at the homestead and the activities they want to enjoy. The charges help the owner of the establishment generate income. Figure 1 shows mountains with hiking trails.

Hiking trails in Zaka Valley.

The challenge for the establishment is to generate enough capital to improve the facility to display the Africanness and Karanga culture expected by tourists. Microfinance could support tourist provisions and enable similar businesses to market their services. According to Axelrod (2021), the owner does not have bank finance access. The SMET owner has benefited from tourist donors who funded him to drill a borehole for water supply. He uses the same borehole and pump to draw water for irrigation. He grows vegetables on a small plot. Wild vegetables are gathered from the fields and mountains to supplement kitchen supplies. Mushrooms, for example, are picked from the nearby mountains. They also pick harugwa(in Karanga dialect) or harurwa (in Zezuru dialect), edible stink bugs (biological name Encosternum delegorguei Spinola). Harugwa is picked from trees in the nearby mountains and is dried and fried to make a delicacy that has become a favorite for many tourists. Tourists also join in the bug-picking exercise. In addition, they pick wild fruits for fresh eats during picking, after which extras are taken to the homestead for kitchen supplies. Finally, the tourist village buys some bugs for a snack or relish that can be eaten with the local thick porridge or pap called sadza in the Shona language. Figures 2 to 4 show the stink bug(harugwa) eaten at the homestead. The tourists’ indulgence in local food highlights Madanhire as a potential future gastronomic destination (Rogerson & Rogerson, 2021). However, the lack of funding has constrained the tourism business in the area. Strengthening microfinance could improve access to finance for the business. The authors argue that such areas with a rich culture to be explored qualify as micro niches that offer tourists an experience that could advance tourism activities in rural areas (Rogerson & Rogerson, 2021).

Harugwa eating leaves.

Picked live harugwa.

Fried harugwa (as relish) in a plate of sadza.

A webpage or blog could improve the global visibility of the business. Unfortunately, the owner has failed to keep his webpage active because of a lack of finance. However, microfinance could help in this regard. Most tourists come from abroad, so the maintenance and sustainability of the website are a perpetual benefit for the business. Nevertheless, due to non-payment of bills, his telephone numbers are no longer working because the landlines are now dysfunctional.

Theoretical Framework

This paper is premised on financial inclusion and institutional theories. The former is relevant because the inequalities in Zimbabwe’s rural communities are based on limited access to finance. These areas are underserved by the formal sector due to a lack of requirements for servicing loans such as collateral (Hasan et al., 2020). Thus, the business sector in rural areas is subjected to similar challenges since institutional constraints posed by banks exclude disadvantaged areas (Mahdi, 2018). One of the financial inclusion practices is microfinance, which is supposed to enable individuals and businesses to use the expended micro funds for income-earning activities (Mader, 2018; Ozili, 2020). Hence the need to establish how the regulatory framework in Zimbabwe affects this microfinance sector and its overarching imperative of alleviating poverty and thereby reducing inequalities. Institutional theories explain how organizational systems are influenced by sociocultural (including social rules and norms), economic, legal, political, technological, and environmental contexts (North, 2018; Scott, 2013). They include Institutional Logics Theory (which focuses on how logic shapes behavior), Institutional economics theory (which argues that institutions play a role in shaping economic outcomes), and Resources Dependency Theory (which argues that all organizations depend on resources such as finance).

While reviewed papers for this study used theories such as financial inclusion and classical research method, the latter could not be adopted because it was deemed unsuitable for this paper, as it is development orientated.

Methods

This paper aimed to investigate the nexus between regulation and inequality in the microfinance and tourism sectors. This qualitative study used an explorative literature review design to understand what scholars have discovered about the effect of microfinance regulations on funding rural SMETs. In the context of this paper and the outlined objectives, we identified qualitative literature review as a suitable methodology to provide relevant answers. It is a relevant methodology for the identification and synthesis of existing research on regulation and inequality in the microfinance and tourism sectors. The methodology involves a systematic, logical, and rigorous search of relevant extant literature (Stratton, 2019).

The following research questions were posed to guide the search string for literature:

RQ1: How do regulations influence the microfinance sector in servicing SMETs in rural Zimbabwe?

RQ2: How does microfinance affect inequality?

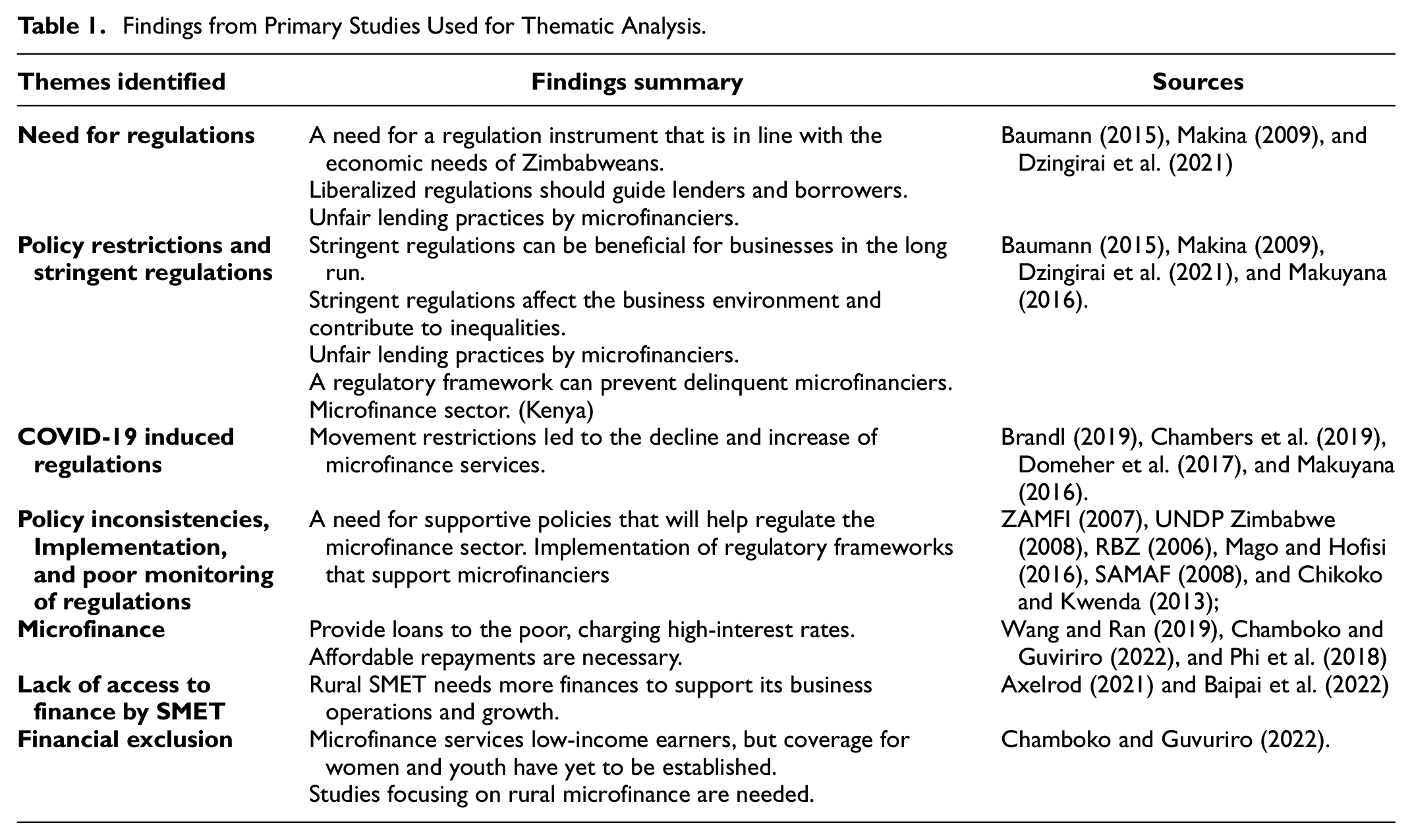

The above questions helped create keywords to guide the search for primary papers in Table 1. In addition, the search strategy is cited to help improve the methodical rigour (Bandara, 2015). Databases such as SCOPUS and Google scholar were used to search for articles. Given the limited availability of secondary sources on microfinance regulations in Zimbabwe, the literature search was broadened to include sources published from 2000, thus including papers published between 2000 and 2022. Search terms were used to identify journal articles from databases. The search terms included “regulation,”“inequality,”“informal sector,”“microfinance,”“microfinance regulation,” and “small to medium enterprises in Tourism.” The search resulted in 32 articles published in reputable journals, and reports from prominent organizations like the World Bank, UNDP, and ZAMFI were consulted to ensure quality literature sourcing. In addition, a small business case in a rural village in Zimbabwe was included to validate the literature findings and gaps. Data were analyzed using content and thematic analysis.

Findings from Primary Studies Used for Thematic Analysis.

Discussion

Zimbabwe is one of Africa’s most highly unequal countries, and the findings further indicate the vulnerability to poverty that rural Zimbabweans face. However, small businesses have the potential to spur economic activities in these rural communities and help reduce inequalities that exist. However, this is a challenge as these communities need more financial services as formal financial providers mostly exclude them (Hasan et al., 2020). While microfinance is key to addressing financial access for such communities to help alleviate poverty (Wang & Ran, 2019), the financing gap still exist due to problems related to services offered by microfinanciers (Baipai et al., 2022; Basera et al., 2022). In addition, findings reveal limited records of disadvantaged groups receiving microfinance (Chamboko & Guvuriro, 2022). Therefore, a well-regulated microfinance sector has the potential to close the gap in access to finance. However, a poor regulation environment dampens the environment, especially when people cannot afford to repay loans or do not have the collateral to borrow money (Chambers et al., 2019; Modisagae & Ackermann, 2018; Muganyi et al., 2022). It can also lead to attrition if the microfinance sector is not supported to thrive (Chikoko & Kwenda, 2013; Matanda & Matanda, 2019).

Regulation is relevant in business sectors as it enables businesses’ smooth functioning and management. Regulation can be conceptualized as ensuring sanity and soundness in a sector using the legal framework. However, liberalization is a state with little government control, where the market forces become the pacesetters. Liberalization sounds ideal but can result in lawlessness and stifle the business environment due to a lack of regulations. Makina (2009) argues that a liberalized financial sector should effectively manage lenders and borrowers. For example, the Zimbabwean microfinance sector once enjoyed a liberalized environment because of the absence of a clear microfinance policy. Microfinance institutions could accept deposits, give out loans, charge high-interest rates and hold borrowers’ assets as collateral security. However, practices such as high-interest rates defeat the purpose of microfinance as lenders end up not affording repayments and losing their assets used for collateral (Chamboko & Guvuriro, 2022). Thus, microfinance perpetuates inequalities in access to finance and impoverishes those accessing the product. This finding aligns with what critics of microfinance regulations have expressed (Johnson, 1998; Siwale & Okoye, 2017).

Additionally, the liberalized environment gave people a “borrowing bonanza,” which created a “debt spiral.” One borrower would borrow from institution A and then go to institution B to repay institution A. They borrow again from institution C to repay institution B. The lack of monitoring and follow-up created a serious localized bubble that saw many MFIs closing shop because of poor repayments (SAMAF, 2008). Some were put under judicial management (e.g., McDowell’s International; Mago et al., 2013). Because of a lack of follow-ups, many would borrow and buy tickets to the United Kingdom (UK) without repaying their loans. Many people migrated to the UK during the crisis for greener pastures (Bloch, 2006). They would then raise money by borrowing from various moneylenders. They exploited a loophole because the institutions did not seek references. The authorities, leading to the near collapse of the microfinance sector, never investigated such corrupt activities. The environment did not help local rural tourist businesses because they had no collateral.

The above examples indicate the shortfalls of an unregulated sector where the ecosystem becomes unconducive to all stakeholders, supporting Brandl’s (2019) assertions on stringent regulations. A poorly regulated microfinance has the potential to create inequalities in terms of accessing funds, especially for businesses aiming at creating employment opportunities for the poor. SMETs are expected to benefit from microfinance to enhance poverty alleviation in rural areas through rural tourism (Mxunyelwa & Henama, 2019; Ngoasong & Kimbu, 2016). However, policy restrictions in the microfinance sector have not improved access to finance; hence business activities remain subdued. SMETs can be empowered through policies that support rural tourism businesses for livelihood enhancement (Makoni & Tichaawa, 2021; Ngoasong & Kimbu, 2016). In addition, institutional changes have retarded growth in the tourism sector, with SMETs being the most brutally hit (Nyaruwata, 2017).

The Zimbabwean economy has undergone stringent regulations in the microfinance sector. For example, high capital requirements promulgated by the RBZ made many microfinance institutions leave the sector (Olubukola et al., 2021). Regulation, in this case, was detrimental to the sector’s development. However, Baumann (2015) argues that regulation could be the right way for Zimbabwe and other developing countries. Therefore, regulations should be developed and implemented to make them manageable to the SMET and microfinance sectors. The context worsened the inequality of the poor, who could hardly access financial resources from the formal finance sector. The death of MFIs worsened the poor’s lack of access to finance, especially those in rural areas. As a result, inequality is perpetuated as rural tourism ventures collapse (Nyaruwata, 2017) in the face of the complexity of the triad nexus. Furthermore, recent regulations invoked by the COVID-19 pandemic worsened the situation of SMETs (Makoni & Tichaawa, 2021). These regulations show how government institutions also contribute to challenges faced by businesses as noted by institutional theories (Mader, 2018).

Therefore, there is a need to revitalize microfinancing in Zimbabwe to enable more businesses to be established and those in operation to be sustainable. As was noted by Phi and Dredge (2019), MFT approaches can be adopted to help MFIs be self-reliant. MFT opens an opportunity for tourists to participate in helping the poor address their poverty-related issues, thus enabling tourism activities to directly benefit the poor, unlike the case noted by Chirenje et al. (2013). The MFT approach can be applied by Madanhire village so that tourists can enjoy both tourism-related activities, learn about the poverty-related challenges that the villagers face, and help raise funds. The funds raised can encourage other villagers to start businesses supporting Madanhire with other tourism-related activities, such as crafts. Increased activities will help secure livelihoods for the villager, thereby reducing poverty. With available funds (through microfinance), Baipai et al.’s (2022) view of turning farms into agritourism can easily be explored to increase livelihood-earning options for the rural poor.

A regulated microfinance sector is necessary for COVID-19’s impact recovery measures to help rebuild the Zimbabwean economy. Supportive policies are critical to ensure that access to finance will not deter the needed growth of SMETs. As was already noted by Baipai et al. (2022), a lack of funding affects rural-based tourism; more financial streams are required to support SMETs. Moreover, the sources of funds should have affordable repayments (Phi et al., 2018) for rural businesses to support business growth and sustainability.

It is important to note that there are divergent and conflicting perspectives on the regulation and inequality nexus in the Zimbabwean microfinance and tourism sectors. For example, regulation increases compliance costs (Kanyenze, 2011) but enhances consumer protection and promotes responsible lending practices (Makina et al., 2014; RBZ, 2006). Regarding the sectoral arguments, the Zimbabwe Tourism Authority (2019) argues that regulation discourages investments as SMETs face operational difficulties that reduce profitability. Furthermore, policy inconsistencies and unpredictability cause challenges in the Zimbabwean economy (Abel et al., 2013). However, properly managed regulations can promote progress in the microfinance and tourism sectors (Abel et al., 2013).

Conclusion

The nexus between regulation and inequality is a social reality in Zimbabwe. Urgent attention is needed to ensure a balance between the variables. The paper suggests that a sound policy on inequality will create a balance between the variables. The policy is the best conduit that can be used to harmonize the link between regulation of the microfinance sector to support rural SMETs to deal with the problem of inequality. Harmonization of regulation and inequality will balance economic progress and development. Policymakers should consider giving SMETs access to finance to invigorate their businesses. The Madanhire rural tourism business case demonstrates the great need for financial resources to promote the growth of SMETs in rural areas. Rural livelihoods can be promoted if rural SMETs can have access to finance. It is recommended that the government fast-track the microfinance sector’s regulation to function effectively and efficiently. The regulations should also be flexible enough to allow microfinanciers to diversify their offerings to manage economic shocks.

This paper sheds light on the issues created by the complex relationship between regulation and inequality in Zimbabwe’s microfinance and tourism sectors. Some of the practical implications proposed by this study include aligning the regulatory framework to help policymakers and role players in microfinance to support SMETs, given that microfinance can stimulate economic activities and solve social challenges. Innovative policy regulations that are lender and borrower sensitive can ensure increased participation of lenders and investors in this sector. Therefore, a well-regulated microfinance sector has the potential to support SMETs in growing their businesses and to enable the rural poor to start economic activities that could contribute to the tourism value chain. The result can be rural communities welcoming more tourists, thus creating financial stability to avert poverty and inequality. Women should also be encouraged to participate in these economic activities so that inequalities at the household level can be managed. This paper can prompt debates among academics and policymakers on how regulations should be approached, cognisant of the importance of supporting the microfinance sector because of its need to service rural areas and SMETs. The paper explored the complex nexus between regulation and inequality in Zimbabwe’s microfinance and tourism sectors related to SMETs using a qualitative review methodology guided by an exploratory research design. Microfinance (which incorporates financial inclusion) and institutional theories as its conceptual lens.

This paper foregrounded policy issues that affect the SMETs sector by focusing on how regulation and deregulation of the Zimbabwean microfinance sector contribute to poverty and inequality. However, this paper has limitations. The limitations include the use of qualitative literature review and the use of gray literature, which have limitations because they are not peer-reviewed. Google Scholar is also criticized for containing gray literature. In addition, we did not use quantitative methods, which could be employed in future to answer questions from a positivist perspective. Future studies could use comprehensive data collection strategies like mixed methods to gather more data on the impact of the lack of microfinance for rural SMETs. Furthermore, such studies can be gender aggregated to understand the extent of inequalities and participation of both genders in SMETs.

Footnotes

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: The funding refers to the page fees for this article that will be paid by Nelson Mandela University through the SANLiC agreement.

Data Availability Statement

Data sharing not applicable to this article as no datasets were generated or analyzed during the current study.