Abstract

The attributes of the business model have become an essential factor affecting enterprise performance and competitive advantage. However, there still needs to be systematic identification of key attributes and empirical tests between key attributes and firm performance. To fill the research gap, we conducted a questionnaire and open-ended coding to identify five key attributes of successful business models, and then a measurement scale was developed. The empirical analysis based on 445 samples shows that the measurement scale of multi-dimensional business model attributes composed of novelty, sustainability, efficiency, expandability, and value co-creation has good reliability and validity. Our findings contribute to identifying key attributes of successful business models from different industries and examining the impact of key attributes on firm performance. Furthermore, the conclusion of this study will be an excellent enlightenment to understand better the key attributes of business models and the firm performance advantages brought by them for both research and practice.

Plain Language Summary

Business models can help enterprises build strong competitiveness and achieve excellent corporate performance. Although the forms of business models vary greatly, the key attributes of excellent business models are similar. Therefore, this article explored and identified the key attributes of excellent business models through open questionnaires and open coding and developed and validated a measurement scale containing five key attributes of business models. Data analysis of 445 sample data verified that the scale developed in this article has good reliability and validity. The main contributions of this paper include: 1. Identifying five key business model attributes managers believe are the most important and can bring competitive advantage and excellent performance to enterprises. 2. Enriching the relevant research results of business model attribute measurement. 3. Providing a new basis for the research on the relationship between business models and competitive advantage and enterprise performance. However, there are still some limitations in this article, such as using cross-sectional data and without considering the life cycle of business models and macro environment, and these research deficiencies are also prospects for future research.

Introduction

In the rapidly changing and competitive market, enterprises must build a successful business model to maintain strong competitiveness and obtain excellent enterprise performance (Massa et al., 2017; McDonald & Eisenhardt, 2020; Snihur & Zott, 2020; Zott et al., 2011). Although the business model appears unpredictable and changeable, the key attributes of a successful business model that can bring competitive advantage and excellent performance to enterprises are highly consistent (Cucculelli & Peruzzi, 2020; Tidhar & Eisenhardt, 2020). Business model attributes could explain why some business models succeed and others fail. Therefore, further research on business models should focus on their core characteristics, starting by exploring the key attributes that can provide a source of value creation (Desyllas et al., 2022; George & Bock, 2011).

Scholars have begun to pay attention to the attributes of business models. Some scholars put forward the common features of business models that can create value for enterprises and call these common features the source of value creation (Amit & Zott, 2001; Wang & Peng, 2002). Subsequently, scholars pointed out that the common characteristics of business models are an essential source of sustainable competitive advantage, which can help enterprises grow and improve performance (Casadesus-Masanell & Ricart, 2010; Dunford et al., 2010; Teece, 2010). As scholars systematically sort out and summarize the attributes of business models, a stream of literature about the infrastructure attributes of business model value creation and the value attributes of improving competitive advantage and enterprise performance begins to appear (Gronum et al., 2015; C. Li & Qi, 2020; Snihur & Eisenhardt, 2022; Yang et al., 2018). However, to a large extent, the key attributes of business models are challenging to explain why some disruptive business models can succeed while others fail in the competition (Leppänen et al., 2023; Yang et al., 2018). Due to the inconsistent conclusions and lack of consensus in the existing literature, we were prompted to examine business models from a practitioner’s perspective to explore their attributes.

Further, although more and more literature has begun to pay attention to business model attributes, empirical results directly related to whether business model attributes can effectively improve corporate performance or have competitive advantages are scarce (Foss & Saebi, 2017; Ndayako, 2021; Snihur & Zott, 2020). One of the main reasons is the lack of a measurement scale (Zhang et al., 2015), which is suitable for business models in different industries. In conclusion, this study aims to answer the question of the shared key attributes of successful business models and develop corresponding measurement scales to promote the research on the key attributes of business models.

The rest of this paper is as follows. In the second part, through the literature review, the definition of business model attributes, the content, and measurement scales of key attributes are systematically sorted out and reviewed. In the third part, questionnaires and open coding identify the business model’s key attributes from practitioners’ practice. In the fourth part, a multi-dimension scale is developed, and exploratory factor analysis and confirmatory factor analysis are used to test the reliability and validity of the scale. The fifth part summarizes and discusses the research according to the critical findings.

Literature Review

Attributes of Business Model

Attributes generally refer to the characteristics of the essence of an entity. The business model aims to improve enterprise performance or gain a competitive advantage (Balboni et al., 2019; Zott & Amit, 2007). All of its operations are carried out around creating value for the enterprise better (Desyllas et al., 2022). However, only a business model with specific attributes can improve an enterprise’s performance and competitive advantage (Yang et al., 2018; Zott & Amit, 2010). Therefore, the business model’s attributes refer to the characteristics that can improve the total value created by the business model and thus enhance the competitive advantage and performance of the enterprise. In addition, some studies have shown that business models that make high profits have higher cognitive complexity and more substantial consensus. In contrast, business models that create low yields have more differences (Malmström et al., 2015), showing that business models with more substantial competitiveness and higher enterprise performance may have some common characteristics (Jiang, 2014; Luo et al., 2019; Snihur & Eisenhardt, 2022; Teece, 2010; Zott & Amit, 2007). Therefore, key attributes are the typical characteristics of business models with consensus and can create high-level enterprise performance.

Content of Key Attributes of the Business Model

After nearly two decades of development, understanding the key attributes of business models has gradually evolved from the early scattered and multi-angle research to more centralized and systematic research. In the early stage of the study, Wang and Peng (2002) pointed out that successful business models that create value have three features in common, namely uniqueness, difficulty to imitate, and down-to-earth. Morris et al. (2005) proposed that the three characteristics of a good business model are sustainability, consistency, and adaptability. Amit and Zott (2001) take startups as the research object and identify novelty, lock-in, complementarity, and efficiency as the source of value creation of startups through information obtained through public channels such as initial public offering (IPO) prospectus, annual report, investment analysis report and company website of sample companies, as well as through structured questionnaires. Subsequently, Teece (2010) pointed out that the key characteristics of a successful business model are as follows: the differentiation of business models, the difficulty of imitation by competitors, and high efficiency, which are essential sources of sustainable competitive advantages for enterprises. In the subsequent research, Teece also pointed out that successful business models can be expanded across multiple market segments (Teece, 2018). Based on the case study, Wen (2010) concluded that sustainable and profitable income is the criterion for judging whether the business model is successful. Dunford et al. (2010) proposed that business model replicability can help new enterprises’ growth and performance improvement. Giesen et al. (2010) pointed out that the business model is consistent, analytical, and adaptable. Casadesus-Masanell and Ricart (2010) considered the business model consistent, self-reinforcing, and robust. Later, scholars began to systemize and summarize the attributes of business models. Jiang (2014) outlined business model value creation attributes into consistency, novelty, efficiency, and sustainability. Zhang et al. (2015) summarized four key attributes based on the theory of resources, the theory of activity system, dynamic capability, and the core connotation of reference business models: value co-creation, difficulty to imitate, expandability, and sustainability. Y. Li (2015) sorted out seven key attributes of business models that can cause enterprises to obtain higher market performance from the overall quality and internal components of business models, which are input factor resource conditions, the difference of production process, certainty, expansibility, the win-win nature of profit models, the uniqueness and complementarity of output products. Gronum et al. (2015) summarized the business model as three attributes: novelty, transaction efficiency, and user simplicity. Yang et al. (2018) further concluded that the attributes of the business model are infrastructure attributes of how to create value and value attributes of how to shape competitive advantage and improve performance through theoretical deduction and literature induction. Similarly, Luo et al. (2019) concluded that the business model attributes are transaction attributes represented by NICE (novelty, lock-in, complementarity, efficiency) and institutional attributes defined by CS (consistency and sustainability) through literature induction. C. Li and Qi (2020), based on the modern value chain theory, put forward that the key attributes of a successful business model enable enterprises to achieve multi-dimensional value appreciation and sustainable profit. However, not all scholars have empirically tested the relationship between key attributes, firm performance, or competitive advantage, and some only put forward a conceptual framework.

Measurement of Business Model Attributes

Scholars first refine the overall attributes of the business model and then develop and measure the scale of the business model. For example, based on grounded theory, Amit and Zott (2001) explored the driving force of value creation of e-commerce startup business models. They extracted the four characteristics of the business models of startups: novelty, lock-in, complementarity, and efficiency. They developed corresponding scales for novelty and efficiency attributes and empirically tested the impact mechanism of novelty and efficiency on enterprise performance. The conclusion points out that a startup’s business model can be designed based on novelty and efficiency (Zott & Amit, 2007). Other scholars have widely recognized and used the business model measurement scale developed by Amit and Zott. Chinese scholars Jiang and Cai (2016) developed a business model measurement scale with four attributes of NICE (novelty, lock-in, complementarity, and efficiency) in combination with China’s situation. Based on the literature review, Zhang et al. (2015) identified and developed a business model measurement scale with four attributes: value co-creation, scalability, difficulty to imitate, and sustainability. Y. Li (2015) proposed and measured the seven key attributes of business models. Most of the existing measurement scales are based on startup and e-commerce enterprises, and there are certain restrictions on measuring business models in other industries.

Reviewing the previous literature makes an essential contribution to studying business model attributes. However, there is still little research on how to improve firm performance and competitive advantage through value creation by key attributes (Foss & Saebi, 2017; Leppänen et al., 2023), predominantly empirical tests on the relationship between key attributes and firm performance (Y. Li, 2015; Zhang et al., 2015). This study tries to fill this gap by identifying key attributes and scale development. This study starts by identifying the key attributes of business models; it will explore the key attributes of business models and their contents by combining qualitative and quantitative methods. Then, it will develop the measurement scales of business model key attributes and conduct empirical tests on large samples.

The Identification of Key Attributes

Method

This study uses statistical investigation to identify key attributes of the business model. The questionnaire survey method is commonly used for statistical investigation and research. Through a questionnaire survey, this study can accurately collect the respondent’s opinions and set open questions in the exploratory questionnaire, requiring them to express their views, attitudes, and characteristics. This study can reveal the essence of the question through information collation, induction, scientific analysis, and other procedures. Therefore, we use an open questionnaire to reveal the nature of the problem through information sorting, induction, scientific analysis, and other procedures.

Identification Process

The first part of the questionnaire introduces the definition of a business model to make the respondents understand its meaning. The second part raises open-ended questions to managers, aiming to understand the characteristics of a successful business model, that is, which can enable enterprises to achieve higher enterprise performance. This question is broader than the number of answers but needs to be listed in order of importance. Both the definition of the business model and the open-ended questions are purposely kept simple and easy to understand. Through these two steps, the respondents can answer the questions based on clear investigation purpose and question definition.

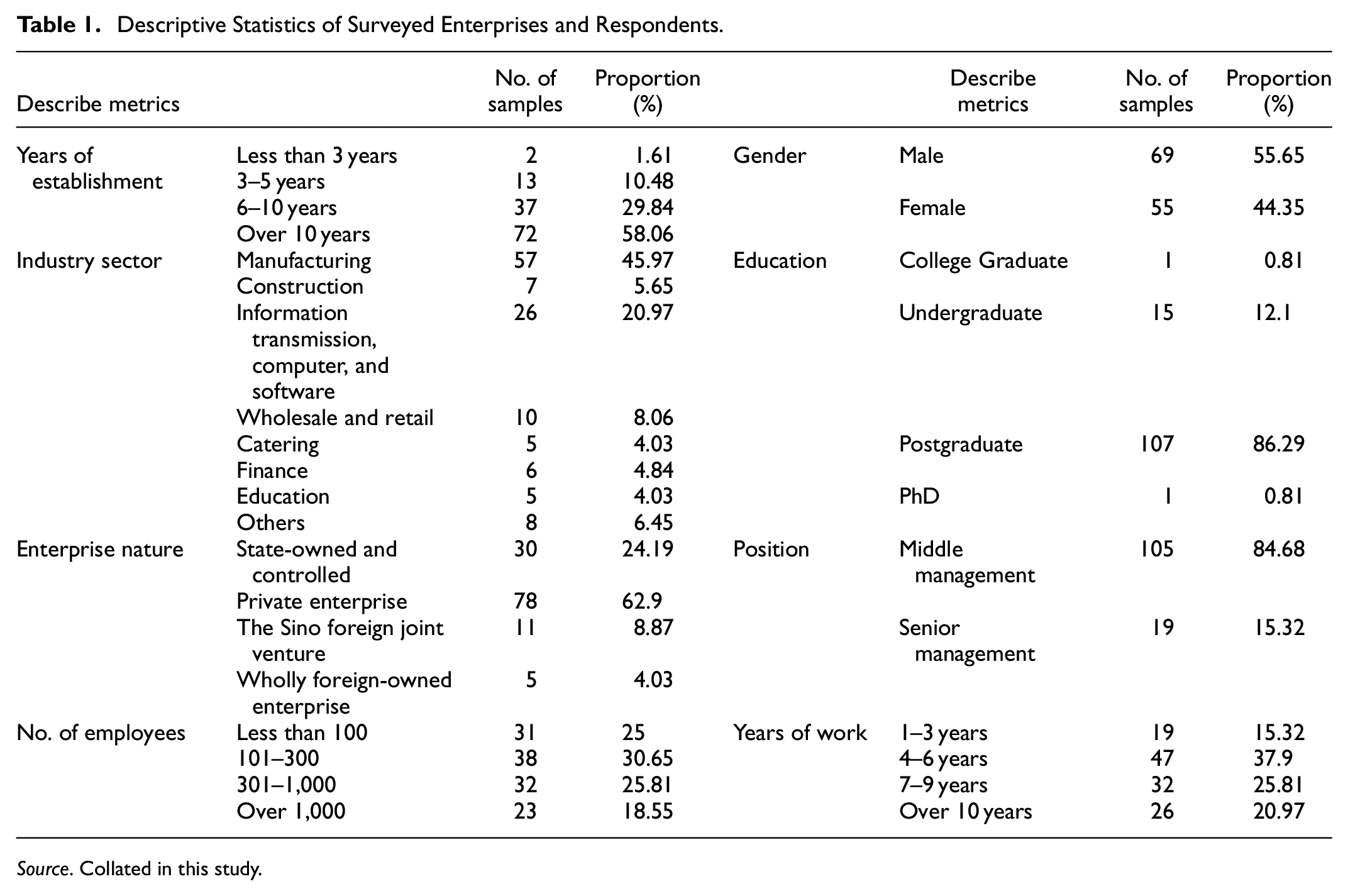

In the survey, 200 questionnaires were distributed, and the respondents included the middle and senior managers. 158 questionnaires were collected, and 124 were valid, with an effective recovery rate of 78.5%. The descriptive statistics of the surveyed enterprises and subjects are shown in Table 1. Through the collation and analysis of the questionnaire, a total of 369 entries were collected. High-frequency lexical chunks in the entries were open-coded through classifying and collating information.

Descriptive Statistics of Surveyed Enterprises and Respondents.

Source. Collated in this study.

1 to 5 items about the characteristics of successful business models were obtained from each respondent.

Invite two coders to code and discuss the content independently at each stage. One coder is very familiar with this study’s context, relevant terms, and documents. In contrast, the other coder is a graduate student majoring in accounting, unfazed to become more familiar with the context, terms, or documents. After each independent coding stage, the two coders will compare the coding results and discuss the differences. Finally, 76 lexical chunks unrelated to the research topic are classified as “meaningless.” The remaining 293 lexical chunks are classified and summarized according to keywords. The coding process is shown in Figure 1. Among them, the frequency of the thesaurus belonging to the novelty category is 96, the frequency of the thesaurus belonging to the sustainability category is 74, the frequency of the thesaurus belonging to the efficiency category is 48, the frequency of the thesaurus belonging to the expandability category is 33, the frequency of the thesaurus belonging to the value co-creation category is 27, and the frequency of the thesaurus belonging to the other categories is less than 5 (for example, difficult to imitate; risk control ability; humanization). Therefore, they are not included in key attributes. Regarding Liu’s (2013) research methods, select attributes with a statistical frequency of more than half the total are regarded as key attributes. Therefore, from the perspective of statistical results, the identified key attribute categories account for 75.3% of the survey results, representing the main types of key attributes of the business model.

Coding process.

Connotation of Attributes

Based on the questionnaire and in combination with the existing literature, the connotation of each business model attribute is defined.

Novelty

Zott and Amit, who first proposed novelty as the main feature of the business model, explained that the essence of the novel business model is to adopt new economic transaction methods, such as contacting stakeholders who have not been contacted before, contacting transaction participants in new ways or designing new transaction mechanisms. The level of value creation of the business model will depend on the subjective evaluation of the target customers on the novelty and appropriateness of the new tasks, products, or services under consideration (Lepak et al., 2007; Cozzolino et al., 2018; Bocken & Snihur, 2020; Ndayako, 2021 ). The greater the novelty and appropriateness of the products or services provided by the enterprise, the greater the potential use value and exchange value for users. The essence of business model design centered on novelty is adopting new activities, transaction structures, or transaction management methods. Therefore, the novelty attribute of the business model can make the business model more unique and reduce the number of alternatives, thus increasing the conversion costs of stakeholders of other business models. Because the improvement of the transaction mode can make the transaction more convenient and faster, it can bring direct utility appreciation to the users (not only consumers). Thus, the novelty of the business model refers to adopting new value creation methods, transaction methods, or value transmission methods.

Efficiency

According to the theory of transaction cost, when the cost of each transaction decreases, the transaction efficiency will increase. Therefore, the lower the cost of the enterprise due to the transaction efficiency, the greater the income and the greater the value created. According to Williamson (1989), improving efficiency can achieve transactions determined by exchange attributes, including information asymmetry and complexity, in a way that minimizes transaction costs and maximizes performance. By increasing the reliability of transactions, reducing the complexity of transactions, reducing the degree of information asymmetry, accelerating the frequency of transactions, improving the flexibility of transactions, and reducing transaction costs and risks, these methods can improve the efficiency of business models, thereby improving enterprise performance. Because the transaction cost is reduced and the responsiveness to customer requirements is greatly improved, these improvements usually lead to a price reduction and an increase in profit and sales turnover. Therefore, the efficiency attribute of the business model refers to the value increase brought to various stakeholders of the business model by improving the transaction efficiency and reducing the average transaction cost.

Value Co-Creation

From the perspective of value network theory, there is a link between enterprise network configuration and value creation. The center of value creation may be a value network rather than an enterprise. Potential alliance partners, suppliers, and customers are value creators. Prahalad named this view “value co-creation” (Prahalad & Hamel, 1990). The value co-creation of the business model mainly means that the future competition of enterprises depends on a new method of value creation, that is, taking the individual as the center, and other stakeholders such as consumers, suppliers, alliance partners, and enterprises jointly create value (Coombes & Nicholson, 2021; Wei & Liu, 2020). For example, in the booming sharing economy and digital economy, consumers participate highly in the value-creation process (Qiao et al., 2020), and the forms are also relatively diverse. As Amit and Zott (2012) said, the boundary of enterprise value creation has gone beyond the boundaries of enterprises and industries. The business model expands the resources of enterprises, and enterprises and all stakeholders jointly create value in the transaction process (Popov et al., 2022). It is worth noting that the value co-creation attribute differs from the traditional value creation theory based on the logic of business exchange. The concept of value co-creation includes the fact that consumers are the participants in the various processes of enterprise value creation rather than the consumers of value and that enterprises will use the resources of partner enterprises in the value network in the value creation process. Value co-creation can be the business model’s basic or key attribute. For example, the business model of many platform enterprises includes the participation of consumers in value creation. Therefore, the value co-creation of the business model refers to the close transaction relationship between the enterprise and other transaction participants that can share resources and capabilities so that the enterprise can create more excellent value without being bound by its resources and capabilities.

Expandability

There are two main views on expandability in the literature. One is that the expansibility of business models means that business models can be replicated. For example, Dunford et al. (2010) believe that enterprises repeatedly apply the business model and improve the business model in the process of repeated application. Zhang et al. (2015) thought that the expandability of business models refers to the difficulty of core enterprises reusing business models. The other point of view is that expandability refers to the ability of enterprises to increase output according to demand after increasing resources (Nielsen & Lund, 2014). The specific ways of expansion can include adding new distribution channels, breaking transmission capacity constraints, and using partners to work. These ways can bring multiple accelerated returns to enterprises rather than linear returns brought by traditional methods. These two views are not contradictory, and they are both manifestations of the expansibility of business models. One is based on customers’ repeated consumption or business repeated use, while the other is based on the expansion of new users or new business models. In practice, many enterprises also use both methods to expand. In conclusion, establishing a highly replicable and scalable business model and establishing and maintaining long-term cooperation with partners are all factors that have an essential impact on the effectiveness of the business model (Cao, 2020). Therefore, the expandability attribute of the business model refers to improving enterprise profits through the repeated application of the business model or the expansion of new markets and products.

Sustainability

Scholars perceive the sustainability of business models mainly from the economic level, focusing on sustainable profits and sustainable competitive advantages, and think that a successful business model should enable an enterprise to make money and maintain its profit flow for a while. Lüdeke-Freund (2010) describes the sustainability of business models as obtaining competitive advantages through excellent customer value creation and helping enterprises achieve sustainable development of business results. In recent years, with the increasing competitive pressure of enterprises and the changing external environment, scholars’ research on the sustainability of business models has expanded to the three dimensions of economy, ecology, and society (Kraus et al., 2020; Pinkse et al., 2023; Xiao & Yang, 2020). Enterprises’ ecological and social responsibilities can help enterprises obtain sustainable competitive advantages. It is not excluded that some enterprises have economic motives behind their undertaking ecological and social responsibilities (Hope, 2018). Ritala et al. (2018) believe that building a successful and sustainable business model also requires the active participation of various stakeholders. Through the questionnaire survey of middle and senior managers of enterprises, this study finds that practitioners’ understanding of the value creation and performance improvement of business models is still focused on the economic impact brought by the sustainability of business models. Under the guidance of the market economy, business model sustainability enables enterprises to gain market competitive advantage and maximize economic value. Therefore, we believe that the sustainability attribute of the business model refers to the extent to which the allocation and adjustment of the business model’s components, resources, and capabilities can bring long-term stable economic performance to enterprises.

Relationship Between Attributes

The attributes of business models have synergy and can influence and promote each other. (1) Efficiency and expandability interact with each other. For example, a second-hand car trading platform reduces the information asymmetry between buyers and sellers by providing customers with the latest and most comprehensive information and removing the intermediaries, thus improving the transaction efficiency; at the same time, the marketing and sales costs, transaction processing costs and communication costs generated in the transaction process can be reduced through scalability (that is increasing the number of transactions on the transaction platform, expanding the number of registered potential transaction users), and ultimately improving the ability to create value. (2) Value co-creation and novelty are interdependent. By connecting the past value creators (enterprises), revenue sources (customers), and cost and cost coordinators (suppliers and competitors) in a novel way, they can create value together. For example, some products or services (free anti-virus software and short video apps) are free to customers. Customers are no longer the source of income in the transaction, but new products or services are generated through customers’ needs. Other related parties of the transaction pay for this and provide the source of income. (3) Sustainability and expandability can develop together. When the business model of an enterprise becomes increasingly mature, and the relationship between the enterprise and the parties in the transaction is gradually stable, industries or enterprises that pursue economies of scale and coordination effects will consider “fission” through business model replication, such as Wal-Mart, Carrefour and other large chain retail enterprises. (4) There is an essential link between novelty and efficiency. Take Uber and Didi’s Premier service as an example; the “reverse thinking” of using idle and non-core resources has innovated the transaction mode. Coordinate with the mobile app, and the status and location of people who want to use the car and those who can provide services can be dynamically updated and matched accordingly, increasing information transparency and improving efficiency.

Scale Development and Verification

According to each key attribute’s connotation and critical characteristics, summarized above, this section will develop and design the business model attribute measurement scale. Referring to the scale development process proposed by Churchill (1979), this study first generates an initial measurement item base based on the literature review and in-depth interviews with the senior management of the enterprise. Then, the items are purified through expert evaluation and prediction tests. Finally, based on large-scale research, factor analysis was used to test the reliability and validity of the scale.

Generate Initial Measurement Items

First of all, according to the description of a business model and business model attributes in the part of the literature review, the research scope of the business model’s attributes is determined. Then, this study conducted several semi-structured interviews with two experts to understand their views on the “business model” and “business model’s attributes.” With the help of experts, it clarified the meaning of the term “business model” and what characteristics managers think of excellent business models from the perspective of practice. On this basis, determine the measurement items of each dimension of the business model. A total of 26 initial measurement items were generated, including (1) Referring to the more mature scale used in the existing literature. According to the research objectives, after making appropriate modifications and getting 13 items. (2) Combined with the expert interview content, the measurement content was refined and compiled, and five items were obtained. (3) Eight items were designed based on the key characteristics of the sorted measurement dimensions.

Expert Review

Five experts from universities and scientific research institutes were invited to review the items to improve the scale’s content validity for the initial scale formed. First, we explained the object’s definition for this review to the experts and asked them to confirm or deny the definition of the business model to be tested. After the affirmative response, experts are asked to evaluate the relevance between each item and the corresponding dimension. In the third step, experts assessed the conciseness and clarity of the items in the initial scale. According to the experts’ evaluation opinions, the following modifications were made: (1) the words that are relatively broad in expression in the item were modified to have a clear meaning. For example, the item “enterprises constantly introduce innovation into business models” in the novelty attribute was changed to “enterprises’ business models provide a combination of products, services, and information in new ways.” (2) Delete the items not closely related to the measurement content and purpose. (3) Revise professional expressions or terms into words that are easy to understand by words or give examples. (4) Delete the items with repeated measurement content and unreadable expression and the specific meaning is unclear, such as “the expansion of the existing business scale.” (5) Delete the items with repeated measurement content and unreadable expression, such as “the business transactions and ways of creating value with other partners of the enterprise are relatively new,” and “the business model of the enterprise can provide corresponding returns for different transaction participants (such as demand satisfaction, profit income, increasing popularity).”

Before sending the questionnaire to potential investigators, this study invited 12 experienced managers to pre-test the questionnaire. These participants answered the questionnaire and follow-up interviews were conducted with them, asking whether there were ambiguous expressions in the questionnaire, checking the wording and understanding of the items, obtaining some feedback on potential problems, and making modifications. The items were screened and modified after the expert review and tracking pre-test, and 20 items were retained. On this basis, the initial questionnaire was prepared using the Likert 7-point scale.

Determine the Formal Questionnaire

Before conducting a large-scale survey, we distributed 215 questionnaires to the middle and senior managers working in the enterprise, and 177 of them were recovered, 143 of them were valid (the effective questionnaire recovery rate was 66.51%), which were used for the pre-test of the survey questionnaire. Churchill (1979) believed the initial items should be simplified by exploratory factor analysis (EFA) and confirmatory factor analysis (CFA) before reliability and validity analysis. Therefore, according to the pre-test results, delete the items with factor load less than 0.4 or serious cross load after rotation, delete the items with CITC value less than 0.4, and delete the items with Cronbach’s α Items whose value will increase. Finally, a scale with five dimensions and 17 items was obtained for a formal large-scale survey and data analysis (see Table 2). Among them, there are four items to measure the novelty of the business model, three items to measure the efficiency of the business model, four items to measure the co-creation of business model value, three items to measure the expansibility of the business model, and three items to measure the sustainability of the business model.

Data Collection

We entrust a well-known research company to distribute questionnaires to enterprises all over China. The distribution objects are managers above the middle level of enterprises (a few of them are the founders of enterprises). A total of 750 questionnaires were distributed, and 525 were retrieved, of which 445 were valid, with an effective recovery rate of 84.8%. The judgment basis of the invalid questionnaire is: (1) If the respondent has worked in the current enterprise for less than 1 year and believes that they have not fully understood the operation of the enterprise’s business model and the actual operation of the enterprise, so their response should be eliminated; (2) If there is a large area of the same assigned value in the questionnaire, it will be eliminated. (3) If the respondents come from government enterprises or monopolistic industry enterprises, the responses will be eliminated if they believe they do not conform to the characteristics of the business model in the market environment.

Results

Exploratory Factor Analysis

The KMO and Bartlett test results on the samples showed that the KMO value was 0.845, higher than the standard level of 0.7. The approximate χ2 value of the Bartlett test is 2,918.216, and the significance p-value is .000 (<.001), indicating that the sample data is suitable for factor analysis. Five common factors with characteristic root values greater than 1 can be extracted (as shown in Table 2), and the cumulative variance interpretation rate is 69.175%.

Results of Exploratory Factor Analysis and Confirmatory Factor Analysis.

Note. Figures in brackets indicate the results of the confirmatory factor analysis.

Confirmatory Factor Analysis

The structural equation model tests the retained variables and their structures. The indicators of the structural model are χ2/df is 1.222 < 3; GFI, CFI, and NFI were 0.967, 0.991, and 0.955, respectively. They are all greater than 0.9. RMSEA is 0.038, less than 0.05. Other indicators are within the acceptable range, indicating that the structural model has an excellent fitting effect. As shown in the factor load factors in brackets in Table 2 and Figure 2, the standard load factors of 17 items in the five dimensions of the business model are mostly greater than 0.70 (those less than 0.7 are also 0.68 or 0.69, close to 0.7), indicating that there is a strong relationship between the factors and the analysis items.

Structural model of business model attributes.

Referring to the method provided by Anderson and Gerbing (1988), this study verifies that the developed five-dimensional model structure is the best measurement model of relationship strength by comparing the fitting indicators of a series of possible alternative models. As shown in Table 3, the relevant index of the five-factor model proposed is good. In contrast, the fitting index of other alternative models needs to reach the ideal level. Thus, the five-factor model is the best model to measure the attributes of business models.

Comparison of Fitting Indicators of Alternative Models.

Note. The four-factor model combines scalability and sustainability. The three-factor model combines value co-creation, expandability, and sustainability. The two-factor model combines novelty and efficiency, value co-creation, expandability, and sustainability. The single-factor model combines all attributes into one factor.

Reliability Test

To verify the reliability of the developed scale, the reliability coefficients of novelty, efficiency, value co-creation, expandability, and sustainability and the reliability coefficients of the scale as a whole were calculated. The coefficients of Cronbach’s α (see the last column of Table 2) are .805, .820, .819, .784, and .839, respectively. The overall reliability of the scale is .859, indicating that the reliability of the questionnaire is good.

Validity Test

First of all, test the convergence validity. Convergent validity refers to the degree of correlation between different measurement items in the same dimension. It can be seen from Table 4 that the AVE of the five dimensions in the business model scale is between 0.535 and 0.634, all of which are greater than 0.5. Moreover, the CR value is between 0.785 and 0.839, greater than 0.7, indicating good convergence validity.

AVE and CR Index Results of Each Factor.

Secondly, the discriminant validity was tested. Discriminant validity refers to the degree of difference between different dimensions or concepts. It can be seen from Table 5 that the square root of the AVE of each dimension is more than 0.7 and is greater than the correlation coefficient with the other four dimensions, indicating that the scale has good discriminative validity.

AVE Square Root Value of Each Factor.

Note. The number on the diagonal is the AVE square root of the dimension, and the other is the correlation coefficient between the dimensions.

*p < .05. **p < .01. ***p < .001.

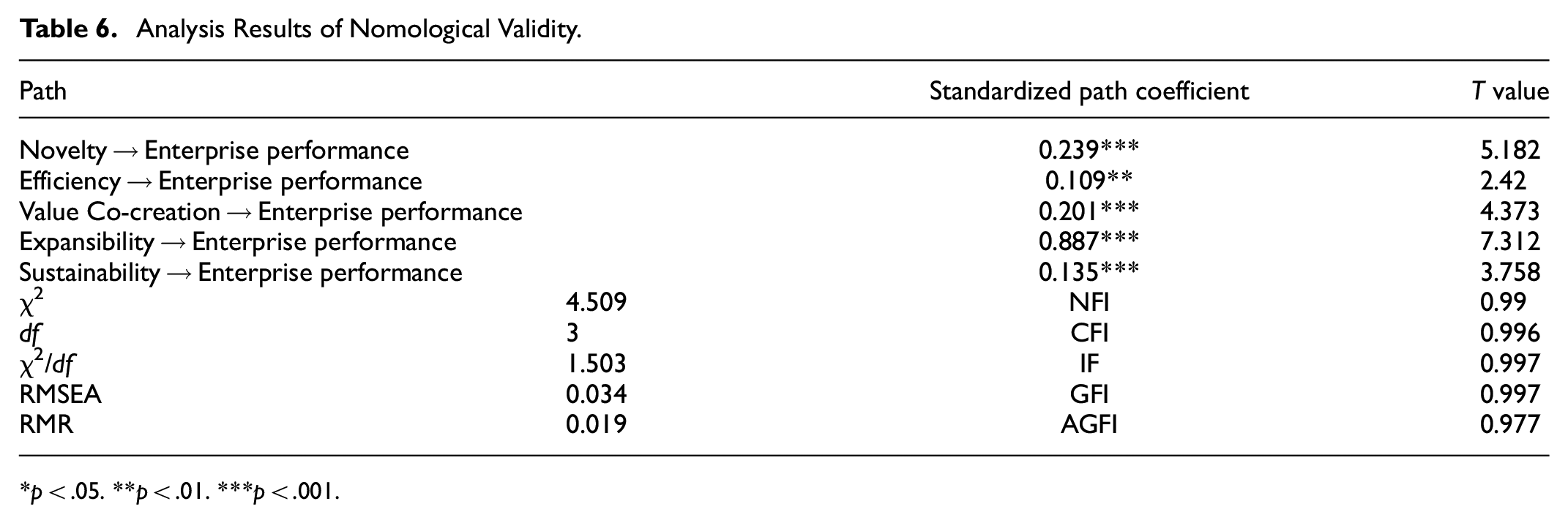

Finally, test nomological validity. Nomological validity is to test the relationship or causal relationship between the measured variables and other variables. As mentioned before, the attributes of the business model will bring excellent enterprise performance to enterprises, so the attributes of the business model will significantly positively impact enterprise performance. Six items were added to the questionnaire to measure the performance of enterprises, namely “the sales growth rate of enterprises in the past three years is high,”“the profit of enterprises has increased rapidly in the past three years,”“the return on investment of enterprises in recent three years is high,”“the total income of enterprises in recent three years is relatively high,”“enterprises have a high market share in the past three years,”“enterprises have achieved good results in market expansion in the past three years.” The Cronbach’s α coefficient of the six items is .850. Use the structural equation model to test the causal relationship between five attributes and enterprise performance (see Table 6). From Table 6, it can be seen that each dimension has a significant impact on the dependent variable enterprise performance. The T value is greater than the standard value of 1.96. All the fitting indicators of the model meet the standard and have good nomological validity.

Analysis Results of Nomological Validity.

*p < .05. **p < .01. ***p < .001.

Discussion and Conclusion

Research Conclusions

Through an open questionnaire and coding for management practitioners, it identifies and concludes that novelty, efficiency, value co-creation, scalability, and sustainability are the crucial attributes of business models that can bring competitive advantages and excellent performance to enterprises. The results of this study support the conclusion about the relationship between business model attributes and firm performance. More precisely, novelty business models emphasize differentiation and efficiency business models enhance firm performance through cost leadership (Aversa et al., 2015; Leppänen et al., 2023; Tidhar & Eisenhardt, 2020; Zott & Amit, 2007). The sustainability of a business model can create a sustainable competitive advantage and generate profitable and sustainable revenue streams in identified markets (Peric et al., 2017; Snihur & Zott, 2020). Value co-creation and expandability can enhance business performance by collaborating to introduce complementary services and replicate profit models (Desyllas & Sako, 2013; McDonald & Eisenhardt, 2020). The empirical results show that a multi-dimensional business model scale of novelty, efficiency, value co-creation, scalability, and sustainability has good reliability and validity. Taking enterprise performance as the dependent variable, each dimension of the business model significantly impacts the dependent variable.

Implications for Theory

This study contributes to the research of business models in three aspects. First, scientific and systematic statistical investigation and research methods further identified the key attributes of business models of enterprises in different industries and the relationship between key attributes and corporate performance and competitive advantage (Eisenhardt & Bingham, 2017; Ahlgren Ode & Louche, 2022). Our findings reaffirm that business model key attributes are essential for improving firm performance and competitive advantage (Desyllas et al., 2022). We also stress that, in addition to the existing research that has verified the business model attributes represented by e-commerce companies and startups (Aversa et al., 2015; Zott & Amit, 2007), the business model attributes of other industries are also worth studying. The key attributes of these business models can enable customers, enterprises, and partner enterprises to participate in value creation and obtain value from it (Snihur & Eisenhardt, 2022). This study organically integrates the theoretical meaning and practical views and gives each attribute a reasonable explanation and connotation definition.

Secondly, we developed a measurement scale containing five key attributes of the business model, which has been verified to have good reliability and validity. Based on a literature review and semi-structured interviews with experts, we identified measurement scales and also verified whether these attributes and measurement scales can be extended to other industries. The survey scope of the development questionnaire used in the identification stage is relatively broad, and it can extract representative business model attributes from different industries and different types of enterprises (Bocken & Snihur, 2020; Pati et al., 2018). On this basis, the attribute measurement scale was developed and tested by a large sample, which confirmed the reliability and validity of the scale and enriched the relevant research results of business model measurement.

Thirdly, this paper contributes to the empirical research of business models and firm performance. Specifically, a new measurement scale is developed in response to the call to study the relationship between business model attributes and firm performance (Leppänen et al., 2023). The scale can lay the foundation for empirically studying the relationship between business models and enterprise performance. The connotation and measurement content of the business model attributes proposed provides a basis for the study of the relationship between business models and enterprise performance (Aversa et al., 2015; Desyllas et al., 2022; Tidhar & Eisenhardt, 2020).

Implications for Practice

The practical implications of our research are reflected in three aspects. First of all, accurately position the enterprise’s strategic direction and purposefully design the attributes of the business model. An enterprise should first have a clear strategic direction or expected goal, and design or plan its business model according to the strategic goal (Bouwman et al., 2019; Casadesus-Masanell & Ricart, 2010), then use the attributes of the business model to help the enterprise achieve its goal (Pang et al., 2019). Nowadays, the elimination rate of enterprises is very high. Even if many enterprises succeed in entrepreneurship, they will still need help or close down in a few years. Therefore, enterprises should clearly understand the value creation mechanism of key attributes and use these attributes to achieve enterprise goals.

Secondly, build appropriate key attributes according to the enterprise’s resource capacity. Enterprises can improve their competitiveness and help them survive in the dynamic environment by building several interrelated and coordinated business model attributes (Ferreira et al., 2020; Teece, 2018). Simply constructing or adjusting a particular attribute may achieve temporary success, but it is not easy to achieve the organic unity and sustainable development of all elements of enterprise operation.

Thirdly, carry out business model innovation with the concept of “win-win.” The business model is a transaction structure that crosses organizational boundaries. Many enterprise managers have begun to realize the importance of “win-win” the construction of each key attribute of the business model is inseparable from the contributions of suppliers, partners, customers, and other stakeholders (Ehret et al., 2013; Foss & Saebi, 2017; Zott et al., 2011). New trading methods or products built to meet customers’ changing needs can bring enterprises expandable markets and sustainable benefits. Reaching a particular scale of economy will reduce transaction costs and improve efficiency to realize the ordinary profits of enterprises and other partners.

Limitations and Suggestions for Future Research

Although this study strictly follows the scientific scale development process and has good reliability and validity, there are still areas for improvement. First, to avoid possible common method deviation, other measurement methods, such as obtaining secondary data for verification, will be considered in future research. Secondly, although the developed scale has good reliability and validity because the business model is a complex construct, it still needs to be continuously tested and revised in future research. Future research can dynamically track the key attributes of the enterprise’s business model, considering whether the key attributes of the business model will change at different stages of life cycles (Bouwman et al., 2019). In addition, the analysis mainly focuses on Chinese companies, which may limit the universality of key attributes of business models. Whether the macro-background of enterprises affects the effect of key attributes of business models (White et al., 2022) is also worth studying in the future.

Footnotes

Acknowledgements

The author gratefully acknowledges comments on earlier versions of the paper by seminar participants at the Business School of Liaoning University in China.

Declaration of Conflicting Interests

The author declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author received no financial support for the research, authorship, and/or publication of this article.

Data Availability Statement

Data sharing not applicable to this article as no datasets were generated or analyzed during the current study.