Abstract

The promotion of low-carbon production is a crucial aspect of sustainable development, and carbon trading has proven to be an effective means of achieving this goal. However, the limited capital hinders small and medium-sized enterprises (SMEs) from achieving low-carbon production. Thus, this paper examines a low-carbon supply chain comprising a financially constrained manufacturer and a well-funded retailer. We propose a game-theoretical model that addresses the financial constraints of the manufacturer through buyer-backed purchase order financing (BPOF) or advance payment discount (APD) with carbon trading revenue-sharing contracts. We investigate the determination of pricing and carbon emission reduction strategies by firms utilizing diverse financing models. We find that the total amount of carbon emission reduction increases with the manufacturer’s carbon trade revenue-sharing ratio. The financing rate of BPOF has a negative impact on the amount of carbon emission reduction, while the discount rate of APD will not affect either the carbon emission reduction or the revenue of the supply chain. Among the two financing strategies, APD is optimal for maximizing profit and promoting low-carbon development throughout the supply chain.

Keywords

Introduction

Climate change and global warming represent paramount challenges of our era, with carbon emissions serving as a primary driver of these issues. Consequently, countries around the world are actively seeking solutions to reduce their carbon footprint. China has taken the leading role in the effort by committing to peak CO2 emissions by 2030 and achieve carbon neutrality by 2060 at the United Nations General Assembly in 2020. To attain this objective, China established a nationwide carbon emission trading market in 2017 (Hu et al., 2017), enabling companies to generate revenue from carbon trading and further promote low-carbon production. Additionally, consumer demand for low-carbon products is also on the rise. According to JD’s statistics from 2019, the year-on-year growth rate of green consumption-related goods is 18% higher than the total sales growth rate of the platform (H. Yang & Chen, 2018). This provides additional incentives for companies to prioritize low-carbon production.

Driven by the carbon trading mechanism and the increasing consumer demand for low-carbon products, enterprises that prioritize low-carbon production are compelled to bear the costs associated with carbon management. However, a research report on energy conservation and emission reduction in Chinese enterprises during the 13th Five-Year Plan period reveals that tight capital constraints have hindered investment in these areas. Additionally, SMEs are a significant part of the economy and account for 70% of global pollution (Revell et al., 2010). However, the limited availability of capital often poses a challenge to the progress of SMEs in attaining low-carbon production (Karpoff et al., 2005). Financing options for low-carbon initiatives include international climate financing, government subsidies (Z. Li et al., 2021), and financial institution loans. Yet credit barriers make it challenging for SMEs to secure investment from international or governmental sources. Financial institutions face equal challenges in providing low-carbon investment opportunities for SMEs due to their prioritization of economic interests (Meng et al., 2020). The presence of information asymmetry exacerbates the difficulties encountered by SMEs in accessing financing (Berger & Udell, 2006). However, prevailing research on low-carbon supply chains predominantly concentrates on strategies for mitigating emissions (Sun & Xiao, 2018; Xia et al., 2023), overlooking the financial constraints. This paper aims to provide financing suggestions for low-carbon supply chain SMEs under carbon trading, promoting low-carbon development.

Supply chain financing, as a prominent funding alternative (Caniato et al., 2016), offers an effective solution to the financial challenges encountered by SMEs (C. Wang et al., 2019). Capital-constrained enterprises can secure production funds through supply chain financing, which relies on the actual trading history of the supply chain. Supply chain financing also plays a crucial role in low-carbon supply chains. Apple has pledged to offer financial and technical assistance to suppliers facing challenges with green production financing, as stated in its Supplier Responsibility Progress Report. The Qing Liu program, led by Jing Dong, has unveiled its strategic plan to launch a collaborative initiative with nine prominent brands aimed at fostering sustainable development across diverse facets of the supply chain, including packaging reduction, innovation and application of green logistics technology, energy conservation, and emissions reduction (J. Cao et al., 2016). Revisiting the aforementioned theoretical framework and drawing upon extensive practical experience, our study aims to explore the role of supply chain financing in mitigating financial challenges encountered by low-carbon SMEs.

Ensuring a harmonious alignment of stakeholders’ interests constitutes a pivotal facet in low-carbon supply chain management. Scholars have proposed revenue-sharing (J. Cao et al., 2016; Zhen & Han, 2022) and cost-sharing contracts (Ghosh & Shah, 2015; Z. Zhang & Yu, 2022) as efficacious measures. Both can facilitate Pareto improvement. Our research is motivated by the work of Wu et al. (2022), who integrated supply chain financing with low-carbon cost-sharing contracts to yield novel insights. Although carbon emission cooperation among enterprises can effectively improve the environment and balance benefits within the low-carbon supply chain, the impact of revenue-sharing contracts on financing and emission reduction strategies remains an open question.

This study aims to address the following questions: (1) What is the correlation between the carbon revenue-sharing ratio and carbon emission reduction? (2) What are the optimal operations of low-carbon supply chain companies under diverse financing strategies? (3) How do financing costs affect their strategies?

We investigate a low-carbon supply chain involving a capital-constrained manufacturer and a well-funded retailer operating under a carbon emission trading mechanism. The manufacturer can raise funds through buyer-backed purchase order financing (BPOF) and advance payment discount (APD). Additionally, we implement a carbon revenue-sharing mechanism to redistribute the benefits of carbon trading between the two parties. Utilizing the Stackelberg model, we determine the optimal solutions for wholesale pricing, retail pricing, low carbon emission levels, and demand for low-carbon products based on each supply chain member’s profit maximization strategies.

The contributions of this paper are as follows: It introduces a novel revenue-sharing mechanism for carbon trading to promote low-carbon development. It enriches the research on low-carbon supply chain financing by introducing buyer-backed purchase order financing and advance payment discounts. The limited literature considering low-carbon supply chain financing has not addressed the topic of buyer-backed purchase order financing and advance payment discounts. It integrates multiple focal issues within the low-carbon supply chain, comprehensively addressing low-carbon supply chain financing, carbon trading, and consumers’ low-carbon preferences. Previous studies have only examined one or two of these factors.

The remainder of this paper is organized as follows. We review the relevant literature comprehensively in Section “Literature Review.” In Section “Models,” we present the fundamental notations and assumptions, along with the model framework and corresponding results. In Section “Analyses and Discussions,” we present a detailed numerical analysis. We conclude with a summary and discuss future research directions in Section “Numerical Analysis.” All proofs can be found in Appendix A.

Literature Review

Supply Chain Financing

Supply chain financing is a financial management method that facilitates the flow of funds throughout the supply chain, thereby enhancing the overall value of the supply chain (Hofmann & Kotzab, 2010). Supply chain financing has emerged as a prevalent means for SMEs to secure funding, and it has become the focus of scholars. Yan et al. (2021) studied the receivables financing mode in supply chain financing with the participation of core enterprises. Cai et al. (2014) studied bank financing and trade credit financing modes under capital constraints. Zhi et al. (2022) compared in-transit inventory financing with traditional financing modes. L. Yang et al. (2018) studied the pricing and emission reduction decisions of enterprises under bank loan and delay-in-payment. In addition to the above financing modes, the 2008 International Monetary Fund estimated that advance payment discounts accounted for a market share of 19% to 22% in trade finance instruments and suggested that advance payment discounts could effectively alleviate financial distress (Zhao & Huchzermeier, 2019). Purchase order financing is also a viable financing approach that entails the buyer guaranteeing funds to the supplier until delivery of the order. The Banco Financiero Nacional, Mexico’s state-owned development bank, initiated this program to foster business growth in the United States, the United Kingdom, Canada, and China (Zhao & Huchzermeier, 2019). Despite the prevalence of both financing modes in practical scenarios, there remains a dearth of research investigating them. Specifically, most low-carbon supply chain financing studies primarily concentrate on direct bank financing (E. Cao et al., 2019). Therefore, this paper selects the BPOF and APD modes as viable options for low-carbon supply chain financing to address the existing research gap in this area.

Low-Carbon Supply Chain

First, the literature on the low-carbon supply chain has gained much attention in carbon emission trading and low-carbon preferences. Xie and Zhao (2014) constructed a new game-theoretic model for an emission-dependent supply chain in a cap-and-trade system. Pu et al. (2018) revealed the impact of consumers’ low-carbon preference on demand and price. Su et al. (2020) investigated the pricing decisions in supply chains influenced by consumers’ green preferences under varying power structures and the optimal strategy of the green supply chain. Based on consumers’ low-carbon preferences, Sun and Xiao (2018) identified consumers’ channel preferences and determined the optimal emission reduction boundary for low-carbon supply chains. By reviewing previous studies, it is evident that the low-carbon preference of consumers has become a widely discussed factor among scholars studying emission reduction strategies in low-carbon supply chains. Therefore, this paper also regards consumers’ low-carbon preference as an essential parameter. The lack of research on carbon trading policies and consumers’ low-carbon preferences with emissions reduction of low-carbon supply chains is still notable. X. Wang et al. (2018) have explored the impact of these two factors on carbon emission reduction. This study further investigates the financing of the low-carbon supply chain, considering consumers’ preferences for low-carbon products and carbon trading.

Furthermore, most studies on low-carbon supply chains focus on the interplay between suppliers and manufacturers. Deng et al. (2021) constructed a game-theoretic model comprising a manufacturer, a bank, a green supplier, and a non-green supplier to derive optimal strategies for the manufacturer and suppliers. B. Li et al. (2021) established a low-carbon supply chain model to investigate the financing strategies of manufacturers influenced by low-carbon initiatives. E. Cao et al. (2019) examined the financing strategies of manufacturers in response to low-carbon preferences among consumers, while Qin et al. (2021) explored the external financing approach of e-commerce platforms and analyzed the manufacturer’s financing strategy base on the above supply chain model. Numerous low-carbon supply chain financing models are constructed based on the relationship between suppliers and manufacturers, but retailers also support upstream enterprises financially for low-carbon development in practice. Therefore, this paper considers the low-carbon supply chain comprising a small and medium-sized manufacturer and an established retailer in the model and investigates the low-carbon supply chain financing and emission reduction strategies accordingly.

Revenue-Sharing Contract in Low Carbon Supply Chains

In addition to the above works, this paper contributes to the growing literature on revenue-sharing contracts in low-carbon supply chains. H. Yang and Chen (2018) found that the implementation of revenue-sharing and cost-sharing contracts can effectively incentivize suppliers to invest in low-carbon technologies. Z. Liu et al. (2022) investigated the revenue-sharing contracts under the carbon trading mechanism and the existence of consumers’ low-carbon preferences. Other studies have demonstrated that cost-sharing and revenue-sharing contracts for carbon emission reduction can effectively coordinate supply chains in the context of carbon tax policies (L. Liu & Li, 2020; L. Zhang et al., 2018). S. Yang and Wang (2016) discovered that revenue-sharing contracts can effectively coordinate both centralized and decentralized supply chains while simultaneously increasing the profits of all participants and improving carbon emission reduction. B. Wang et al. (2021) developed a revenue-sharing contract game mechanism for coal-fired power supply chain enterprises, analyzing centralized decision-making and their respective carbon emission reduction and profit situations without contracts. However, previous studies have mainly focused on revenue sharing without considering supply chain financing or the sharing of carbon trading revenues.

In summary, this paper distinguishes itself from the existing literature by integrating the revenue-sharing mechanism of carbon trading into the financing model of the low-carbon supply chains and addressing overlooked factors such as BPOF and APD. Additionally, it incorporates two crucial elements: the carbon emission trading mechanism and consumers’ low-carbon preferences. Finally, we analyze the impact of revenue-sharing ratio, loan interest rate, and discount rate on carbon emission reduction and financing strategies. This study contributes to the research on financing low-carbon supply chains, offering valuable insights for promoting the low-carbon development of supply chains.

Models

Basic Notations and Assumptions

Under the carbon cap-and-trade scheme, manufacturers can generate revenue by selling credits for reducing carbon emissions. Concurrently, the increasing consciousness of consumers toward low-carbon consumption is propelling the demand for eco-friendly products. Due to these two factors, the manufacturer is more willing to engage in low-carbon production. However, the low-carbon inputs will result in escalated production costs, further constraining the manufacturer’s capital.

Accordingly, we establish a low-carbon supply chain linking a capital-constrained manufacturer to a well-established retailer. The manufacturer sets its wholesale price and determines the total carbon emission reduction before the retailer determines its retail price. The revenue from carbon trading is allocated between the manufacturer and the retailer. We establish the low-carbon supply chain without financial constraints (NF) as the benchmark model, upon which we compare two financing strategies: the manufacturer obtains loans from banks via buyer-backed purchase order (BPOF) and from retailers through advance payment discount (APD). A summary of the model notation is presented in Table 1.

Notations for Parameters and Variables.

The subscripts

The assumptions of this paper are as follows:

The retailer possesses adequate financial resources to support the manufacturer’s investment in their low-carbon production.

The carbon emissions of the manufacturer are within the prescribed limit.

The manufacturer and the retailer are informationally symmetric and risk-neutral.

Market demand is influenced by the combination of retail pricing, total carbon emission reduction, and consumers’ low carbon preferences. According to Wu et al. (2022), as the price of a product increases, its demand decreases; however, if the manufacturer reduces their total carbon emissions, consumer demand for the product will increase due to their preference for low-carbon products.

5. The manufacturer uses a quadratic function of low carbon emission levels

6. All firms in the supply chain are assumed to be going concerns.

Non-Capital Constraint Financing (NF)

In the benchmark model, the manufacturer is not capital-constrained and can achieve low-carbon production by utilizing their funds to cover the production costs and carbon emission reduction expenses. In this low-carbon supply chain, the wholesale price

The first term in Equation 2 represents the total price paid by the retailer for selling the product, while the second term denotes production cost. The third term signifies carbon trading revenue earned by the manufacturer through selling carbon allowances with a sharing ratio

Proposition 1. If the manufacturer possesses sufficient funds, the optimal wholesale price, total carbon reduction, sales price, and market demand in a low-carbon supply chain will satisfy the following conditions:

According to the optimal operational decisions proposed in Proposition 1, we conduct a sensitivity analysis of the manufacturer’s optimal production decision concerning the carbon revenue-sharing ratio

Corollary 1.

Corollary 1 suggests that in a low-carbon supply chain with no financial constraints, the optimal wholesale price, total carbon emission reduction by the manufacturer, optimal sales price, and market demand exhibit a monotonic increase concerning the carbon revenue share of the manufacturer. The reason is that the carbon revenue-sharing ratio increase enables manufacturers to maximize their benefits from low-carbon production through carbon trading. Therefore, the manufacturer will increase its low-carbon input to achieve the desired reduction in total carbon emissions

Non-capital constrained business process.

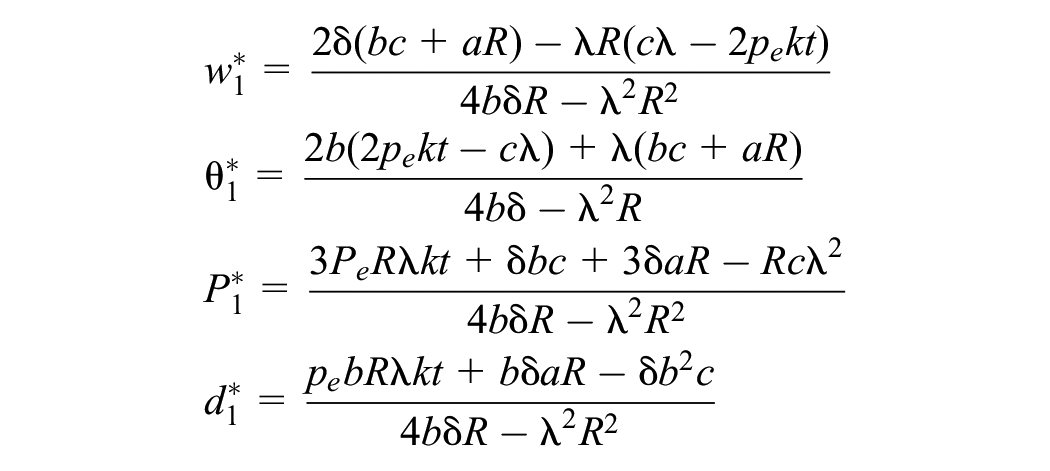

Buyer-Backed Purchase Order Financing (BPOF)

In this financing model, the manufacturer first sets its wholesale price

We can obtain Equation 4 by deducting the financing cost

Proposition 2. Under buyer-backed purchase order financing, the optimal decision of a capital-constrained manufacturer in a low-carbon supply chain encompasses:

Considering the sensitivity of the equilibrium solutions to both the revenue-sharing ratio of carbon trading and the interest rate under BPOF financing, we can derive Corollary 2.

Corollary 2. Under the buyer-backed purchase order financing,

Corollary 2(a) indicates that the total reduction in carbon emission, wholesale price, sales price, and market demand increases with the proportion of carbon trading revenue in BPOF financing.

Business process under buyer-backed purchase order financing.

Corollary 2(b) shows that the optimal total carbon emission reduction of the manufacturer, optimal wholesale price, product sales price, and demand monotonically decreases with the financing interest rate in BPOF financing. The reason is that insufficient capital for low-carbon production forces manufacturers to seek funds from financial institutions, and higher financing rates result in increased financing costs

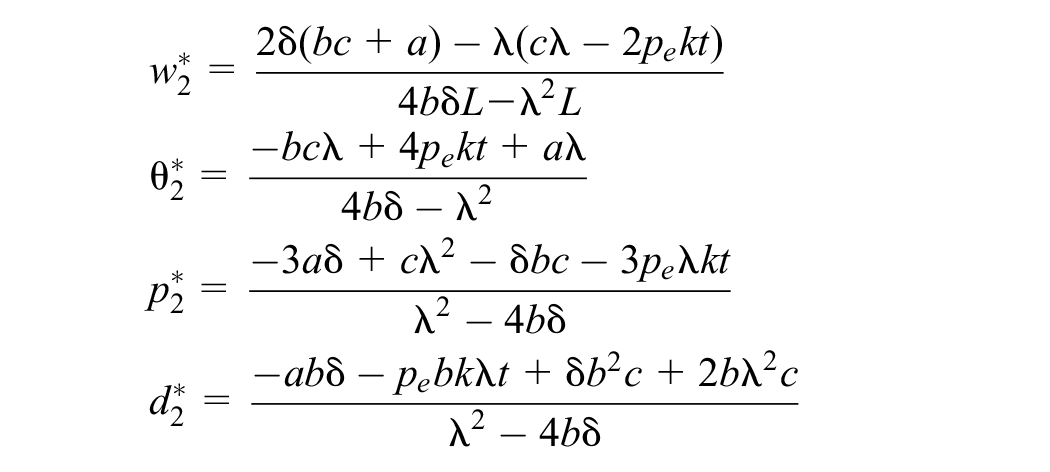

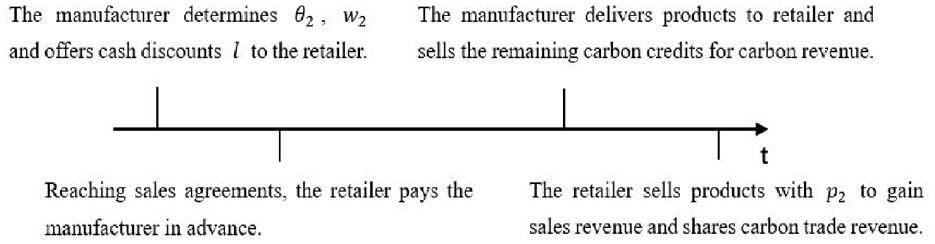

Advance Payment Discount (APD)

We can describe the decision-making process for Advance Payment Discount financing as follows. The manufacturer sets its wholesale price

The manufacturer’s profit function in Equation 6 consists of the net advance payment received by the manufacturer after cash discount, production cost of the product, carbon trading revenue earned by the manufacturer, and carbon reduction costs incurred by the manufacturer. The retailer’s profit function in Equation 7 consists of sales revenue, advance payment to the manufacturer, and carbon trading benefits. By solving the maximization problem for both the manufacturer and retailer, Proposition 3 can be derived.

Proposition 3. When the financially constrained manufacturer in the low-carbon supply chain is financed through APD, the optimal decision in the supply chain satisfies the following conditions:

By conducting a sensitivity analysis on the key parameters, namely the revenue sharing ratio

Corollary 3. Under advance payment discount,

Corollary 3(a) demonstrates that the total reduction in carbon emissions, wholesale product pricing, sales pricing, and product sales of a capital-constrained manufacturer utilizing APD financing will continue to increase monotonically with an increase in the retailer’s carbon revenue-sharing ratio. By comparing Corollary 1 with Corollary 2 (a), we observe that the optimal total carbon emission reduction, wholesale price, retail price, and product sales in a low-carbon supply chain increase proportionally to the manufacturer’s carbon revenue-sharing ratio. It holds regardless of whether the low-carbon supply chain is capital-constrained or financed through alternative means. The consistent influence of the carbon revenue-sharing ratio on carbon emission reduction and product sales within the low-carbon supply chain remains evident, irrespective of specific circumstances.

Business process under advance payment discount.

Corollary 3(b) indicates that the wholesale price in APD mode increases monotonically with the prepayment discount. The total amount of carbon emission reduction, product sales price, and demand remain independent of such discount. In contrast to the BPOF model, financing through APD ensures that the manufacturer’s financing cost equals a cash discount. The manufacturer offsets the cash discount by raising the wholesale price without affecting its low-carbon input. Consequently, the magnitude of the cash discount does not affect the total carbon emission reduction. The retailer receives advance payment discounts to cover the loss from higher wholesale prices. Therefore, the alteration in sales discount does not impact the retailer’s sales price as its revenue remains unchanged in essence. According to assumption 4,

Analyses and Discussions

In this section, we compare the low-carbon input, product demand, income of the manufacturer and the retailer, and supply chain’s overall income between APD and NF as well as APD and BPOF. To facilitate comparison, we set the discount rate in APD equal to the order financing rate in BPOF (i.e.,

Theorem 1.

(a) The total amount of carbon emission reduction and product sales within the supply chain are presented as:

(b) The benefits of the manufacturer, the retailer, and the supply chain are demonstrated as:

Theorem 1(a) demonstrates that the total carbon reduction and product quantity remain constant between APD and NF. In APD mode, the retailer’s discount represents the manufacturer’s financing cost. The difference between APD and NF modes is that manufacturers must bear financing costs to address funding issues. As the supply chain leader, the manufacturer sets wholesale prices and transfers financing costs. Retailers tend to accept these prices more readily due to the sales discounts they receive. The emission reduction and production strategy will no longer change after fully compensating for the manufacturer’s financing costs. Therefore, the total amount of carbon emission reduction and product quantity remains consistent under APD and NF. Theorem 1(b) demonstrates that the manufacturer, retailer, and supply chain achieve equivalent revenue outcomes under APD and NF. We can see that the manufacturer can achieve the same low-carbon production benefits in both APD and NF modes, as they have identical optimal solutions from Theorem 1(a). As a result, carbon trading revenue and low carbon production cost are also equivalent due to the equal amount of carbon emission reduction in both modes. Therefore, the manufacturer’s total benefits remain unchanged between both models. The retailer assumes financing costs transferred from the manufacturer through wholesale prices while simultaneously enjoying financing benefits from discounts. As a result, the retailer’s profit in APD mode is equivalent to that of NF mode. In the APD mode, financing activities within the supply chain result in revenue gains or expense burdens for internal members. These impacts remain confined to the supply chain and do not alter overall supply chain benefits.

Theorem 2. The manufacturer can achieve enhanced reductions in carbon emissions and meet higher product demand through buyer-backed purchase order financing compared to advance payment discounts, that is,

Theorem 2 demonstrates the adoption of advance payment discount (APD) results in higher total carbon reduction and product demand when the financing rate for buyer-backed purchase order financing (BPOF) is equivalent to APD. In both modes, the manufacturer bears the financing costs; however, retailers are more tolerant of wholesale prices under APD due to their cash discount benefit. The financing cost of the manufacturer is shifted entirely in the APD mode, which is impossible in the BPOF mode. Therefore, the manufacturer should reduce capital requirements for low-carbon production in BPOF mode by decreasing carbon emission reduction. However, this may lead to decreased product sales due to low carbon consumption preference. Compared to BPOF mode, APD mode results in higher total carbon emission reduction and product demand.

It’s hard to draw a definitive conclusion in this section regarding the comparison of returns between the manufacturer and retailer under BPOF and APD due to the complexity of the model. Therefore, numerical experiments will be conducted in Section “Comparative Analysis of Profits” to supplement our findings.

Numerical Analysis

In this section, we further analyze the effects of pivot parameters such as carbon revenue-sharing ratio

Comparing the Optimal Decision and Market Demand

Firstly, we examine the impact of the revenue-sharing ratio

The sensitivity analysis of

Figure 4 illustrates the variation of the wholesale price

In Figure 4 panel (b), when the carbon revenue-sharing ratio is constant, both NF and APD modes yield higher total carbon emission reductions than those achieved in BPOF mode. Finally, it can be observed that product demand in NF and APD modes is equal at a given carbon revenue-sharing ratio and significantly greater than that of BPOF mode, thereby validating Theorem 1(a) and Theorem 2. APD is more conducive to enhancing the carbon emission reduction level and facilitating the sales of low-carbon products.

Subsequently, we will examine the influence of financing rates and discounts on optimal decision-making.

As depicted in Figure 5, under the BPOF mode, the manufacturer’s total carbon emission reduction

The sensitivity analysis of

Comparative Analysis of Profits

This section presents a comparative analysis of the profits generated by the manufacturer, retailer, and entire supply chain under different financing modes, revenue-sharing ratios, financing costs, and discount rates. Additionally, it supplements the existing comparison between manufacturer and retailer profits in various supply chain financing scenarios.

By varying the revenue-sharing ratio between 0 and 1 while keeping other parameters constant, we can generate Figure 6.

The profit of the manufacturer and the retailer with

Combining panels (a) and (b) in Figure 6, we observe that

Furthermore, by equating the financing rate to the advance payment discount and varying it between 0 and 0.1 while keeping other parameters constant, we can derive the manufacturer’s and retailer’s profit under different financing strategies in Figure 7.

The profit of the manufacturer and the retailer with

Figure 7 illustrates the profits generated by the manufacturer and retailer based on two financing strategies. Panel (a) shows that an increase in the financing rate will reduce the manufacturer’s profit. However, under the APD mode, the financing cost borne by the manufacturer does not affect their profit. Furthermore, the manufacturer’s revenue is consistently higher under APD than BPOF when there is a financing cost. Panel (b) demonstrates that the retailer’s revenue is consistently higher under APD mode than buyer-backed purchase order financing. The equilibrium profit of the retailer remains unaffected by advance payment discounts. Therefore, when the manufacturer faces capital constraints, APD is the optimal choice for both the retailer and the manufacturer. The advance payment discount does not affect the equilibrium profit of either party. However, under BPOF, an increase in financing rates will result in revenue loss for both parties.

Figures 8 and 9 demonstrate that the overall profit in NF and APD consistently surpasses that of BPOF. In the APD mode, the total supply chain profit remains equivalent to NF, regardless of variations in carbon revenue-sharing ratios or advance payment discounts. However, for BPOF, the low-carbon supply chain’s overall profit declines with increasing financing rates. The APD financing, as an internal financing method within the supply chain, does not result in losses throughout the entire supply chain. Conversely, BPOF is external financing that transfers benefits of the supply chain to financial institutions outside of it. From a holistic perspective on low-carbon supply chains, manufacturers facing capital constraints should opt for APD financing to maximize overall profits.

The supply chain’s revenue with

The supply chain’s revenue with

Although the above analyses assume that the financing interest rate is equal to the advance payment discount rate, we can observe that only a zero financing interest rate can make BPOF as beneficial as APD from Figures 7 and 9. However, this is impractical in reality. Therefore, APD financing remains optimal.

Conclusions

This paper presents a low-carbon supply chain model that involves a large retailer and a capital-constrained manufacturer. We introduce a carbon revenue-sharing mechanism to distribute the benefits of carbon cap-and-trade in the supply chain based on a predetermined ratio. We obtain the optimal decisions under different financing modes and conduct the sensitivity analysis of pivot parameters. We also perform a numerical experiment on the profits of the manufacturer, retailer, and the whole supply chain. Our findings suggest that a carbon revenue-sharing contract can effectively enhance the retailer’s revenue and enable them to fund the manufacturers. However, as the manufacturer’s proportion of revenue increases, so does the total amount of carbon emission reduction. APD financing mode is more advantageous for the supply chain to achieve low-carbon production than the BPOF mode. We find that APD results in higher reductions in carbon emissions and greater demand for low-carbon products than BPOF through a comparison of optimal decisions for low-carbon production under different financing modes. Under the two financing strategies, the carbon revenue-sharing ratio and financing interest rate affect the total reduction of carbon emissions. Interestingly, the manufacturer’s prepayment discount does not affect their overall carbon emissions reduction.

Because APD financing offers maximum benefits for low-carbon production and supply chain participants, financially constrained manufacturers opt for APD financing when both BPOF and APD are available. Additionally, retailers who pay manufacturers in advance can promote low-carbon development within the supply chain while maximizing profits. Therefore, it is imperative for large retailers to proactively provide financial support to reputable manufacturers and promote the development of low-carbon supply chains. Capital-constrained manufacturers should establish an appropriate carbon revenue-sharing ratio under the carbon cap-and-trade policy, which not only serves as an incentive for them to produce low-carbon products but also encourages retailers to provide funds for them. By involving retailers in low-carbon production, the manufacturers can have sufficient capital, and the overall low-carbon supply chain can develop better. However, we should pay attention to the carbon revenue-sharing ratio between the manufacturer and the retailer. Lower financing interest rates can encourage small and medium-sized manufacturers to engage in low-carbon production. This research can facilitate more favorable financing decisions for manufacturers with limited funds, thereby promoting the development of a low-carbon economy and achieving sustainable growth. The carbon revenue-sharing contract presents a novel approach to studying low-carbon supply chain contracts.

We can extend the research in several directions. Firstly, our investigation solely focuses on the impact of carbon revenue-sharing ratios on relevant decision variables without providing a definitive ratio for low-carbon supply chains. Future studies can explore methods to establish an exact revenue-sharing ratio for low-carbon supply chains. In addition, we assume a good reputation manufacturer without considering the default risk, which is a future research direction. We further hypothesize that the retailer possesses sufficient financial resources to support the manufacturer in achieving low-carbon production. Future research should also consider the financial-constrained retailer, who may incur additional financing costs for the advanced payments.

Footnotes

Appendix A

Acknowledgements

We thank the reviewers and editors for their helpful comments on the revision of manuscript.

Author Contributions

Author 1: Conceptualization, Supervision, Writing, Review & Editing. Author 2 (Corresponding Author): Methodology, Software, Formal Analysis, Visualization, and Writing. All authors read and approved the final manuscript.

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: This research was funded by the Program for the Philosophy and Social Sciences Research of Higher Learning Institutions of Shanxi, grant number 2021W014.

Ethical Approval

This article does not contain any studies with human participants performed by any of the authors. The authors consent to participate and publication.

Data Availability Statement

Data sharing not applicable to this article as no datasets were generated or analyzed during the current study.