Abstract

This study empirically investigates the impact of external debt on economic growth, and assesses whether institutional quality matters for this influence, using data from 18 emerging countries during 1996 to 2020. The findings indicate that although an upsurge in external debt negatively affects economic growth, this impact is mitigated when there is an improvement in institutional quality, as reflected by three governance indicators: anti-corruption perception, voice and accountability, and perceptions of the rule of law. However, other three governance indicators (political stability, government effectiveness, and regulatory quality) failed to affect the economic growth favorably. These results have important implications for policymakers in emerging countries who are currently facing major fiscal and external imbalances due to high expenditure on military goods/thigh cost of war, decrease in trade, and financial loss due to the COVID-19 pandemic.

The study attempts to examine the relationship between external debt and economic growth by considering the importance of institutional quality in 18 emerging countries. It uses panel cointegration, panel ARDL, and Dumitrescu & Hurlin panel causality test causality test methods in the analysis. Results indicate that external debt negatively affect economic growth. But external debt combined with improvement in anti-corruption perception, voice and accountability, and the perceptions on the rule of law exert positive influence on economic growth. Therefore, emerging countries should focus on curbing corruption, giving freedom to citizens, and agents executing the standard roles of society.

Introduction

Decades ago, the world was dealing with several economic crises, including the first and second oil price crises resulting in a worldwide slowdown in productivity and an international crisis (the slowdown may vary at country level). At the beginning of the 21st century, countries worldwide experienced a global financial crisis (between 2007 and 2009). Moreover, many countries have experienced country-level economic slowdown from 2012 to 2017 due to changes in economic policy at domestic-level. According to Kemoe and Lartey (2022), the impact of government public debt on the economy has come to the fore in policy debates after the global financial crisis. Recently, COVID-19 harmed economies around the world in multiple ways like slowing down: growth rate, productivity, health infrastructure, trade activities, etc. (Hanushek & Woessmann, 2020; McKibbin & Fernando, 2020; Nicola et al., 2020; Sawada & Sumulong, 2021). The significant negative impact of the global crisis/recession is visible in all countries of the world. It is affecting the worldwide development process and economic growth. In the aftershock of the COVID-19 pandemic, public debt has significantly increased to sustain economic growth, financial status, public welfare, and straighten the country’s economic condition.

Most of the emerging and least developed countries that are facing the problem of low level of household savings, and limited sources of tax revenue are unwilling to jeopardize macroeconomic stability by resorting to increased printing of money (Ogunmuyiwa, 2011). In addition, these countries generally have low-income sources, but need a large amount of effective government expenditure. Therefore, they depend on borrowing in the form of remittances, financial relief and external borrowing (Mazorodze, 2020; Senadza et al., 2018). External debt in the form of foreign investment has been an essential source of domestic recovery to improve economic health. It is an attractive option to finance infrastructure for development prospects (Ogunmuyiwa, 2011). Public borrowing takes place in both domestic and foreign markets. Over the past few decades, many countries have used foreign borrowings mostly for capital and development projects. The rising trend of foreign debt has become a worrying situation for many indebted countries (Abbas et al., 2020). Economic theories such as debt overhanging theory and crowed liquidity constraint theory argue that the prudent use of externally borrowed funds aids both emerging and developed nations in achieving their growth targets (Krugman, 1988; Roubini & Sachs, 1989). However, superfluous external debt has crowding-out effects in terms of increased borrowing costs and fixed predetermined charges on savings, income, and foreign reserves. Furthermore, poor management/utilization and inefficient allocation of external funding to the domestic market negatively impact the host nation’s economic growth and monetary stability (Al Kharusi & Ada, 2018). In addition, Awan and Qasim (2020) noted that foreign loans help to accelerate the development process and also create multi-pronged problems if the borrowed money funds are not used properly, including political and economic sanctions with high-interest rates. Krugman (1988) states that the obligation to pay borrowed money discourages investment decisions in developing nations and thus slows down the nation’s growth. Thus, it is necessary to use the foreign loans for the productive purposes, and these should be borrowed with minimum conditional ties (Senadza et al., 2018).

In recent decades, there has been a considerable surge in public debt. Many scholars have tried to pin down and explain the relationships between public debt and economic growth. Their key findings suggest that the impact of external debt on economic growth is nonlinear, with adverse effects visible only after a particular threshold level of debt-to-GDP ratio (Checherita & Rother, 2010; Ferrarini, 2008; Panizza & Presbitero, 2014; Reinhart & Rogoff, 2010; Woo & Kumar, 2015). Moreover, many studies share the positive link between public debt and economic growth in developing countries (Didia & Ayokunle, 2020; Sheikh & Wang, 2013). In addition, numerous studies in developing nations demonstrate that the relationship between public debt and economic growth depends not just on the amount of debt but also rest on the effectiveness of institutional quality, governance, and policies (Tarek & Ahmed, 2017). Cordella et al. (2010) and Presbitero (2008) provides the evidence that countries with lower debt to GDP ratio than the threshold level may experience lower economic growth due to poor institutional quality/governance. A certain level of institutional quality/governance is needed to encourage a threshold level of investment to stimulate growth and benefit from debt relief (Asiedu, 2003; Dessy & Vencatachellum, 2007). Tarek and Ahmed (2017) demonstrate the indirect impact of lousy governance operating via decreased GDP, and the inclusive effect of good governance on debt accumulation. Nguyen and Luong (2021) conclude that weak governance leads to a higher accumulation of public debt, while debt improves the institutional quality concerning government effectiveness, regulatory quality, and the rule of law. Further, a strong consensus has emerged over the analogy that good governance allows nations to successfully manage their public debt by reducing borrowing costs, limiting risk, and developing their domestic debt markets (Tarek & Ahmed, 2017). Some studies show positive impact of governance on economic growth and the damaging effect of poor governance on economic growth (Manasseh et al., 2022; Mauro, 1996; Tanzi & Davoodi, 2002).

It could be observed from the literature that few studies examined the interaction between external debt, institutional quality, and economic growth with reference to emerging countries. It is a well-known fact that emerging countries are major recipients of external debt. In this context, the present study attempts to examine the relationship between external debt and economic growth by considering institutional quality in 18 emerging countries. This study makes four main contributions to the literature as follows.

(i) This study examines the nexus between eternal debt and economic growth in 18 emerging countries who have been ignored in previous works.

(ii) The interactions of governance (with six indicators), external debt, and economic growth are further explored with special emphasis on the interactive impact of governance as proxied by Kaufmann et al. (2010).

(iii) The dynamic Panel ARDL model with three Pooled Mean Group (PMG), Mean Group (MG), and Dynamic Fixed Effects (DFE) estimators are used for empirical investigation.

(iv) It further uses the Dumitrescu and Hurlin panel causality test to check the robustness of empirical findings.

The result of this study exhibits significant long and short-run relationship among economic growth, external debt, investment, human capital and inflation. The study also reveals negative influence of external debt on economic growth in emerging countries. Considering the relevance of governance indicators with the external debt, the study finds positive influence of three governance indicators (Control of corruption, Voice and Accountability, and Rule of Law) on economic growth, and negative influence of the rest three indicators (Political Stability, Government Effectiveness, and Regulatory Quality) on economic growth. The overall findings suggest that the impact of governance on economic growth is sensitive to the choice of indicators of good governance.

The balance of this paper is organized as follows. A review of the literature is presented in Section “Survey of Literature Review.” Data set and descriptive analysis are presented in Section “Data Set.” The research methodology is described in Section “Research Methodology.” Discussion of results is provided in Section “Empirical Findings.” Finally, Section “Conclusion, Policy Implication, and Recommendation” highlights the concluding remarks and policy recommendations.

Survey of Literature Review

Empirical results regarding the relationship between debt and economic growth could be intensely affected by the choice of variables, methodology, sample period, and selection of countries. In general, there is mixed evidence of a positive/negative relationship between public debt and economic growth. The present study divides the literature survey into two sub-sections based on convenience. The first sub-section highlights the review on the connection between public debt and economic growth. The second sub-section describes the nature of studies that are based on external debt, economic growth, with consideration of institutional quality.

Public Debt and Economic Growth

The popular and most cited study by Reinhart and Rogoff (2010) examined the association between inflation, high central sovereign debt, and economic growth using two decades of historical data set for 44 developing and developed countries. Their findings suggest a tenuous relationship between the two variables, yet they contend that if the debt-to-GDP ratio surpasses 90%, it could prove detrimental to economic growth. However, the identified threshold level of debt-GDP ratio has become contentious due to several analytical flaws in their calculation as noticed by those who find no discontinuity in Debt-Growth relation above the 90% threshold level. Minea and Parent (2012) exhibits that the threshold level stays at around 115% of the Debt-GDP ratio. Above this threshold, public debt is found to have a negative association with economic growth.

Several other studies uphold the findings of Reinhart and Rogoff (2010). Woo and Kumar (2015) find the inverse U-shaped association between government debt and economic growth. Their results indicate that threshold level of debt-GDP ratio as 90% which will be harmful to economic growth by taking data from 38 developed and emerging countries spanning four decades. Checherita-Westphal and Rother (2012) provide similar evidence for the Euro area’s countries. Utilizing five-year overlapping data on government debt and its squared term, they identified an inverse relationship between public debt and economic growth when the debt-GDP ratio surpasses 90%. The result of Reinhart and Rogoff (2010) was also evident in developing countries (Presbitero, 2012), and advanced countries (Panizza & Presbitero, 2014).

External Debt, Economic Growth, and Institutional Quality/Governance

According to the neoclassical theory there exist a positive link between external debt, and economic growth. In contrast, the debt overhang theory posits that external debt beyond a threshold level (excessive external debt) negatively affects economic growth. Therefore, this theory aligns with the recommendation of the neoclassical growth theory which advocates for external financing as a crucial policy option to stimulate economic expansion, particularly in cases where domestic sources are inadequate. However, caution should be taken to evaluate the marginal consequence of the debt on economic growth (Manasseh et al., 2022). If the external debt is not used efficiently, it does more harm than good. It is because of the fact that external debt aided the financing of nonprofitable and unproductive initiatives that contributed to a slowdown in economic growth (Zouhaier & Fatma, 2014).

Some studies have negated the postulates of the neo-classical theory on external debt-GDP relationship, by finding a negative relationship between the two (Audu, 2004; Elbadawi et al., 2003; M. Hameed et al., 2021; Karagol, 2002; Kaufmann et al., 2010; Onyekwelu & Ugwuanyi, 2014; Pattillo et al., 2004).

Using multivariate cointegration techniques, Karagol (2002) conducted a study on turkey, and identified a negative association between external debt and economic growth, in the long-run. This result is also in line with the findings of A. Hameed et al. (2008) for Pakistan and Qayyum and Haider (2012) for low income countries

Recently, a study by Fagbemi (2020) provides no linkage between external debt and economic growth for West Africa for the period 1986 to 2018. Some studies also found this relationship such as Al Kharusi & Ada (2018) for emerging countries, Casares (2015) for developed and developing countries, and Mohsin et al. (2021) for South Asian countries. In contrast, Edo et al. (2020) found a positive connection between debt and economic growth for the sub-Saharan African countries.

Few studies find positive or inconclusive results while examining the relation between external debt and economic growth, by considering other economic variables in their model. Kim et al. (2017) extend the work of Cooray et al. (2017), Kim et al. (2017), and Lee et al. (2017) and investigate the relationship between corruption, shadow economy, and external debt from 1996 to 2012. The study finds a positive and significant impact of corruption on external debt and growth. This study also suggests a positive relationship between the shadow economy and corruption on public debt by decreasing the tax revenue rate. Lee et al. (2017) did not find conclusive results regarding the relationship between external debt and economic growth.

There is increasing consensus amongst researchers, economists and policymaker on the fact that institutional quality is essential in defining the growth distinctions amidst nations. How does governance influence public debt? Several existing empirical literatures are available that provide the impact of governance/institution quality on the public debt and economic growth. Savoia and Sen (2015) also mention the importance of State capacity as a factor in determining economic growth which delves into the convergence debate across countries in the world. Kilishi et al. (2013) conducted a study on Sub-Saharan Africa using GMM methodology to determine whether institutional quality affects economic performance. Their findings indicate that the role of governance and regulatory quality seemed to display the most solid impact on SSA’s economic performance. Moshammer et al. (2016) investigated how the link between debt and the initial level of institution quality can explain variations in economic information in European countries. It deals with two aspects. First, it describes how institutional quality impacts economic growth, and second, it explains the connection between public debt and economic growth. This research used four institutional quality indicators derived from the results of Acemoglu et al. (2004). It finds a low institutional quality level, and poor economic growth in the European Union (EU), when the initial level of government debt is above a threshold level. Vianna and Mollick (2017) studied Latin America and deliberated on the impact of institutional quality on economic development by using data for the period 1996 to 2015. The result of this study shows that 0.1% improvement in institutions leads to a 3.9% rise in per capita output and has a 2.6% impact on global development. Tarek and Ahmed (2017) investigates the connection between governance and public debt accumulation for the 17 MENA Countries using data from 1996 to 2015. Results from the GMM suggest that three governance indicators (political stability, regulatory quality, and rule of law) support the governance and debt relationship hypothesis, that is, poor governance is associated with greater accumulation of public debt. This study also explains bad governance in MENA countries operating via decreased GDP growth. Sani et al. (2019) studied the relationship among public debt, institutional quality, and economic growth in 46 Sub-Saharan African countries by using GMM methodology for the period 2000 to 2014. They found that institutional quality affect economic growth, directly and indirectly. The relationship between institutional quality and public debt is found to be statistically influenced by the interaction term of public debt and governance indicators. Government effectiveness, control of corruption, and regulatory quality are the most crucial factors in promulgating negative effect of public debt on economic growth. The similar relationship is also examined by Kemoe and Lartey (2022) for 44 Sab-Saharan African countries using data from 1996 to 2014. Using the GMM method, the study finds that when public debt rises, it negatively affects economic growth. At the same time, this effect is diminished after an upsurge in the institutions’ quality. Nguyen and Luong (2021) study the relationship among fiscal policy, institutional quality, and public debt for 27 transition countries from 2000 to 2018. They found that curtailing public expenditure and enhancing government revenue may lower government debt. Further, this study demonstrates that weak governance contributes to higher levels accumulation of public debt

Few studies have also examined the relation among institutional quality, external debt, and economic growth in Emerging Countries. For the 53 emerging countries, Daud (2020) examined the relationship between external debt, institutional quality, and economic growth. Their findings suggest adverse effects of external debt on a country’s growth using the GMM method.In contrast, institutional quality expands the country s growth, indicating that external debt on economic growth is contingent on the level of institutional quality.

Considering the above works which take diverse countries, methodology, and choice of variables, this is the first study that contemplates external debt, governance, and economic growth indicators for 18 emerging countries.

Data Set

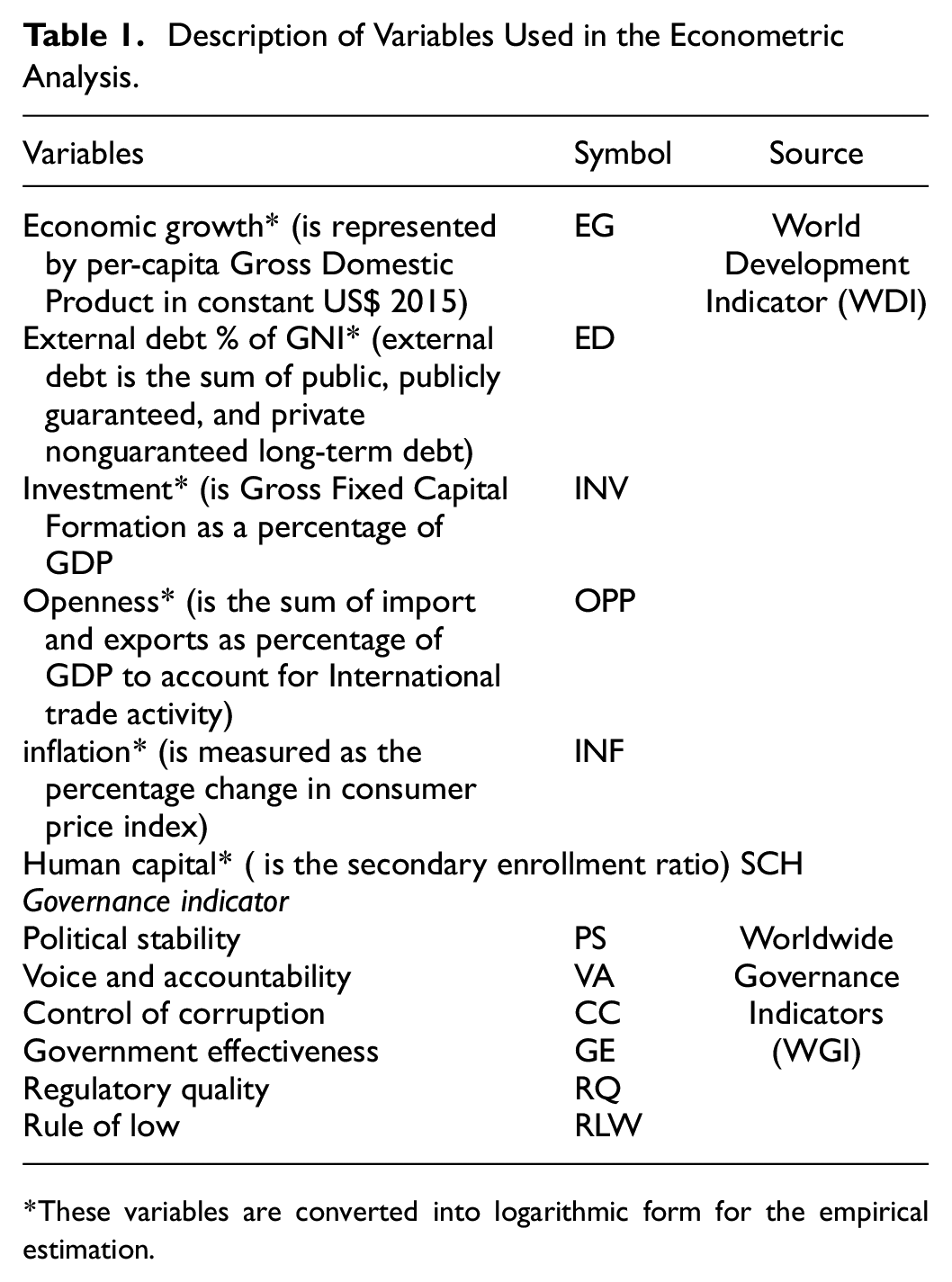

This study uses the World Development Indicator (WDI), and World Governance Indicators (WGI) panel data set from 1996 to 2020 for 18 emerging countries (i.e., Bangladesh, Brazil, Bulgaria, China, Colombia, India, Indonesia, Mexico, Morocco, Pakistan, Peru, Philippine, Romania, Russia, South Africa, Thailand, Turkey, and Ukraine). Choice of countries is based on IMF country classification, and subject to availability of data. Moreover, there are very few studies which empirically examine the connection among institutional quality, external debt, and economic growth in these countries. Descriptions about the main variables of interest are provided in Table 1. The dependent variable in this study is the per capita gross domestic product (EG). External debt (ED) consists of public, publicly guaranteed, and private nonguaranteed long-term debt, use of IMF credit, and short-term debt. To know the impact of institutional quality/governance on external debt, and on economic growth, six sets of governance indicators are used, namely Control of Corruption, Government Effectiveness, Political Stability, Regulatory Quality, Voice and Accountability, and Rule of Law based on Kaufmann et al. (2010). Though these indicators are criticized on the bases of its recent construct, and probability of measurement errors, it is acknowledged that these indicators cover a broader definition of institutions and governance which are helpful in making policy decisions (Williams and Siddique, 2008). These six indicators are interacted with the external debt to explore their effect on economic growth considering the significance of legal systems, institutions, and political environment in selected emerging countries. The governance indicators are measured on a scale of

Description of Variables Used in the Econometric Analysis.

These variables are converted into logarithmic form for the empirical estimation.

Descriptive Analysis

Firstly, the trends in external debt to GNI ratio (in %) for 18 emerging countries considered in our analysis is provided in Figure 1. It can be observed from the graph that, the trends in external debt ratio varies between countries. But one thing could be ascertained that after the COVID-19 pandemic (2019), there is an increasing trend in external debt ratio. Secondly, descriptive statistics of all the variables are computed to know the normality and adequacy of the data set. The findings of descriptive statistics are presented in Table 2. The mean value of economic growth in emerging countries is 8.22, with a standard deviation of 0.76. Economic growth values also range from 6.37 (minimum) to 9.40 (maximum). The mean value of the external debt is 3.55 with a standard deviation of 0.51, ranging from 2.12 (minimum) to 5.13 (maximum). It signifies that economic growth and external debt are dissimilar across emerging countries. Moreover, all six governance indicators report a negative mean value with a maximum Standard deviation of 2.61, and it ranges from a negative value (minimum) to a positive value (maximum).

Evolution of external debt ratio (% of GNI).

Descriptive Statistics.

Source. Calculated by own.

Research Methodology

The present study tries to analyse both the long-run and short-run relationships among governance indicators, external debt, and economic growth utilizing the panel ARDL model initiated by Pesaran et al. (1999).

Preliminary Tests

This study first checks the stationarity properties of the underlying variables using two panel unit root tests namely, Im et al. (2003) test (IPS) and Levin et al. (2002) test (LLC). Both LLC and IPS tests are built upon the widely recognized Dickey-Fuller (ADF) method (Im et al., 2003). IPS method is most suitable for exploring unit roots in panel data. Lag length is chosen by considering the Akaike Information criterion (AIC).

Panel Cointegration Tests

In the next step before applying panel cointegration test, it is essential to determine whether a long-run relationship exists between external debt and economic growth by using two-panel cointegration tests: Pedroni (1996) and Westerlund (2007). Pedroni (1996) test suggests seven different panel cointegration tests that check for the absence of cointegration. Out of seven tests, three tests are based on between-dimension, and rest four tests are based on the within-dimension. Additionally, the generalized least square correction model is used to correct the independent idiosyncratic error terms across the individual variables. Moreover, Westerlund (2007) cointegration test provides four panel cointegration estimation. This test follows the “null of no cointegration” and rejection of null hypothesis signifies the existence of cointegration in at least one individual unit.

Panel Autoregressive Distributed Lags Model

In order to assess the dynamic (interaction) impact of institutional quality and external debt on economic growth, this study applies panel autoregressive distributed lag (panel ARDL) approach under the maximum likelihood estimation (MLE) framework advanced by Pesaran et al. (1999). Panel ARDL method has several advantages. (i) It is capable in confirming the long-term cointegration relationship exists between the variables, even if they are in a different order of integration, that is,

Panel ARDL model follows a two-step procedure where the first step observes the incidence of co-integration between the variables. If the co-integration nexus is established in the first step, the subsequent step includes the estimation of long-run and short-run coefficients. The short-run restrictions could be imposed by approximating an error correction model related to the long-run estimations.

The main model of the Panel ARDL method aims to establish the relationship between external debt and economic growth. The model is as follows:

In Equation 1

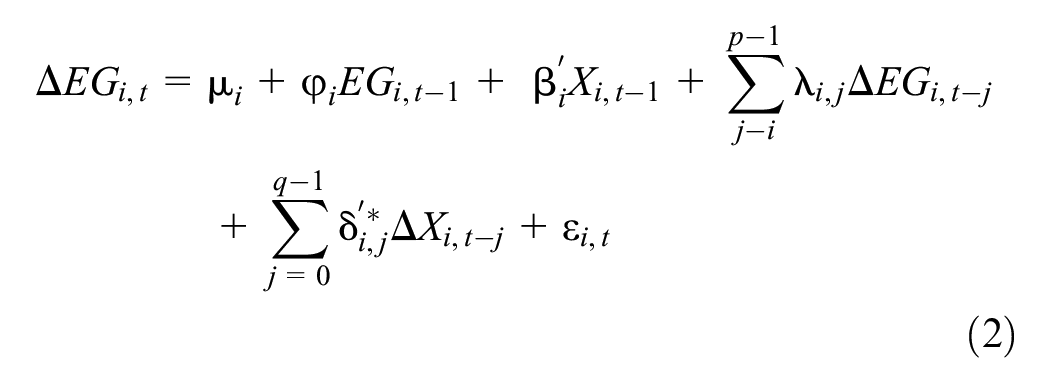

Equation 2 signifies the parameterization of the PMG ARDL model into the error correction model (ECM) based on Pesaran et al. (1999) as follows:

Here

Equation 2 is expressed as an error correction equation by further grouping the variables in levels:

Here

Where

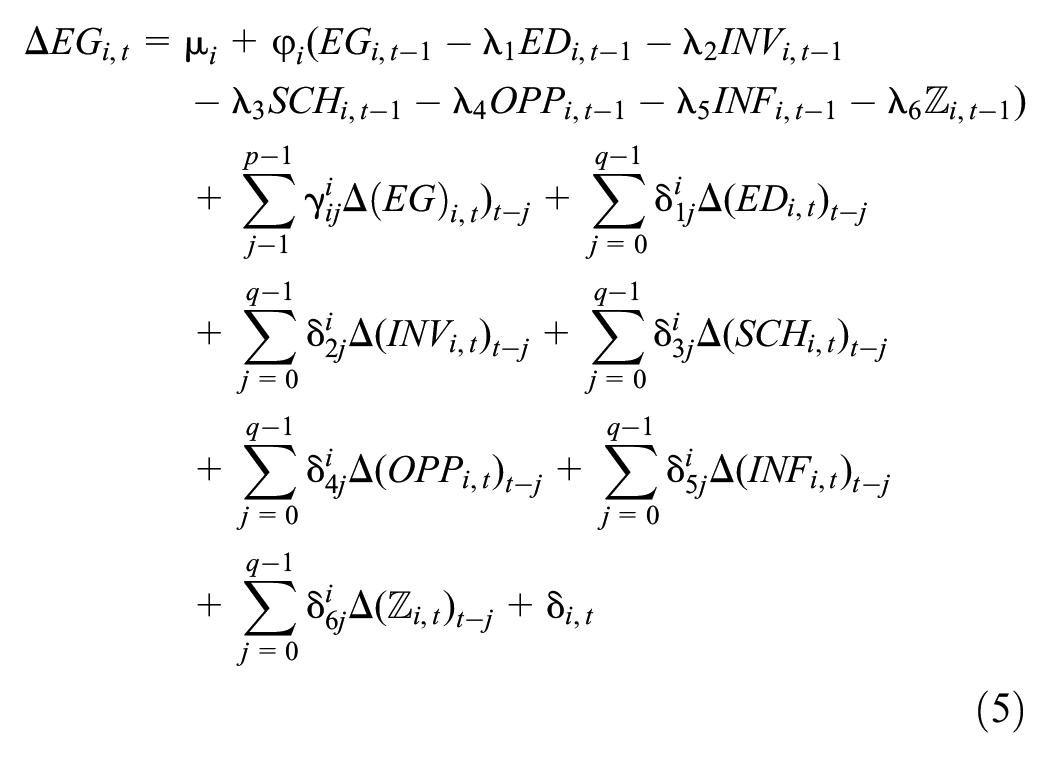

Based on the methodology presented in Equation 3, the following model is formed:

In Equation 5, to remove the serial correlation, the dependent variable

The MG variant of panel ARDL method is based on country-specific regressor. It permits heterogeneity of sample countries in both long- and short-run, and its legitimacy is dependent on the dimension of time series data. The DFE estimator is the final estimator of the Panel ARDL model. This imposes uniformity restrictions both in the short run and long run. But the intercept can be changed across the cross sections with DFE estimators. Lastly, the consistency and efficiency of each estimator is determined by the Hausman test.

Panel Causality Test

The important conclusions can be derived from the coefficients gathered from panel ARDL. However, these consequences are incapable of showing a causal relationship among the variables. Causal relationship among the variables should be inferred to make suitable policies. Therefore, this study uses the Granger causality test of Dumitrescu & Hurlin (2012) to investigate causal links among variables. The feature of this method is its applicability to both heterogeneous and unbalanced panels as well as in situations where

Where the constant term is

Empirical Findings

Table 3 summarizes the findings of the unit root test of the variables in interest. The findings of the IPS unit root test indicates stationarity of six variables at levels (i.e., economic growth, external debt, inflation, regulatory quality, government effectiveness, and control of corruption), while the outcome of

Panel Unit Root Test.

Note. * indicates critical values which are: without trend:

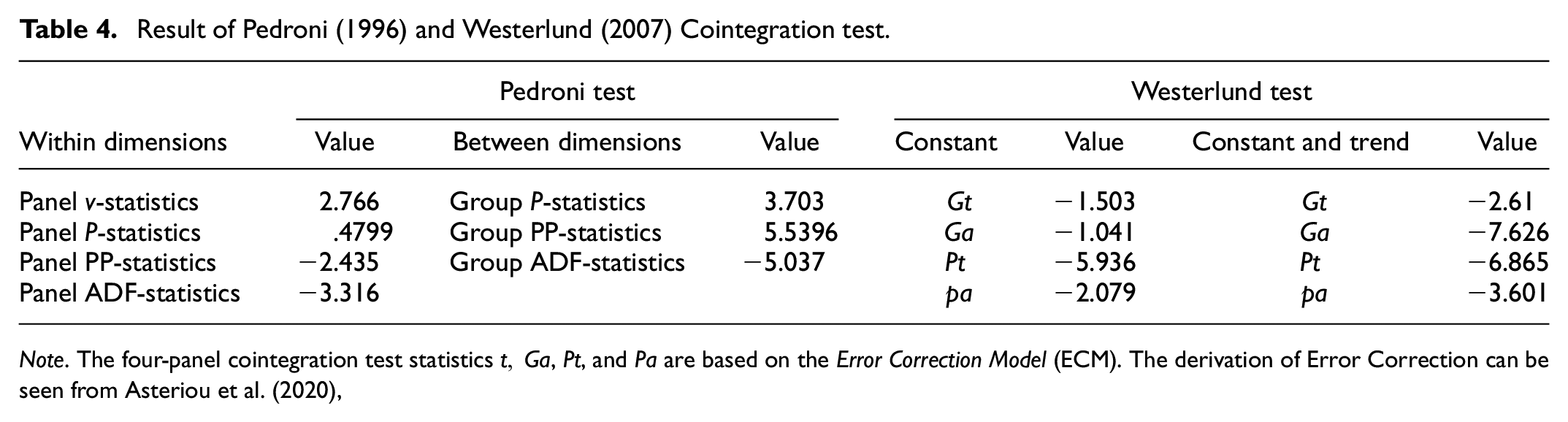

Before estimating the panel ARDL model, two panel cointegration tests (Pedroni, 1996; Westerlund, 2007) are conducted to understand the long-run relationship between economic growth and external debt. Both Pedroni and Westerlund method findings are reported in Table 4. Pedroni test result rejects the null hypothesis

Result of Pedroni (1996) and Westerlund (2007) Cointegration test.

Note. The four-panel cointegration test statistics

Panel ARDL Model Result

In the next step, the long-run and short-run behaviors of the variable of interest are examined using DFE, MG, and PMG estimators. As per the Hausman test, the PMG estimator yields the most accurate, trustworthy, and statistically significant outcomes in determining the long-run and short-run coefficients (result of Hausman test is available on demand). Therefore, this study considers the PMG estimator in identifying the long-run and short-run coefficients. The optimal lag length for all the models is determined using the

First, the Panel ARDL model presents the relationship between external debt and economic growth without taking the governance indicators. The findings of Model-1 are illustrated in Table 5. In the long run, a significant negative relationship between external debt and economic growth is found in 18 Emerging countries. The findings indicate that a 1% rise in external debt leads to a 0.10 percentage point decrease in economic growth. The same result is found for the inflation wherein 1% rise in inflation leads to a −0.23 percentage point decrease in economic growth. A significant positive relationship is drawn in relation to investment and human capital, meaning that a percent rise in both the variables leads to a 0.68 and 0.17 percentage point rise in the economic growth, respectively. The coefficient of error correction model (ECM) has a negative sign, that is, −0.110, suggesting adjustment of 11% in the long-run equilibrium path. In the short run, there is also an inverse relationship between external debt and economic growth..

Result of Panel ARDL Model-1 (Dependent Variable: Economic Growth).

Note. The significance levels of the coefficients are represented * for the 5%. ARDL lag structure

In order to consider the impact of institutional quality on external debt and thereby on economic growth, interaction term of institutional quality and external debt is taken as an independent variable. The overall findings are reported in Table 6 (Model-2 to Model-7) Section A reports the findings of PMG, Section B reports the findings of MG, and Section C reports the findings of DFE respectively. The long-run result in Model-2 shows that the interaction of external debt with control of corruption (CC) has a significant favorable impact on

Result of Panel ARDL Model-2 to Model-7 (Dependent Variable: Economic Growth).

Signify the statistical significance at the 1% level.

The interaction of external debt with government effectiveness (GE) has been used in Model-4. The result evinces significant negative impact of the interaction term of GE and external debt on economic growth. The coefficient of the interaction term [GE × ED] reveals that a percent rise in the GE leads to a −0.045% reduction in the country’s economic growth in the long run. It signifies that effective government may increase the country’s external dependence, and reduce economic growth. This result is contrary to our expectation and as found by earlier studies (Manasseh et al., 2022; Nguyen & Luong, 2021; Tarek & Ahmed, 2017). It could be because of differences in specification of the model, and choice of sample of countries. Model-5 includes the interaction of external debt with the Rule of Law (RLW) in explaining economic growth. The long-run results show a significant and positive coefficient for the interaction term [RLW × ED] in determining

Model-6 considers the interaction of external debt with Voice and Accountability (VC) to explain economic growth. The long run result indicates negative and significant impact of the interaction term [VA × ED] on economic growth with a coefficient value of −.015. It implies that with the improvement in voice and accountability, borrowings on account of external debt might increase, and the growth may slow down. The model-7 includes the interaction of external debt with the Regulatory Quality (RQ) so as to measure its impact on economic growth. The long run finding suggests that interaction of RQ with external debt has a significant negative impact on economic growth. Its coefficient reveals that 1% surge in [RQ × ED] results in weakening of the country’s economic growth by −.067%. This result is in conformity with the outcome of Nguyen and Luong (2021) and Tarek and Ahmed (2017). Notwithstanding the long-run results, in the short run the interaction of external debt with all the governance indicators exert positive and significant impact on economic growth except the VA indicator. It signifies that in the short-run external borrowings may lead to higher economic growth with improvement in institutional quality. Moreover, the error correction terms in all models turn out to be negative and significant, suggesting convergence in the long-run equilibrium path.

The crux of the above findings is that three out of the six governance indicators (control of corruption, voice and accountability, and rule of law) exert positive influence on economic growth, while rest three indicators (political stability, government effectiveness, and regulatory quality) posit negative influence on economic growth in selected emerging countries.

Panel Causality Tests: Robustness Check

After understanding the relation among external debt, institutional quality, and economic growth, the Dumitrescu-Hurlin Granger Causality test is conducted to check the robustness of the panel ARDL results. Results are reported in Table 7. The null hypothesis of Dumitrescue-Hurlin Granger causality test is that each individual determinant (such as external debt, investment, inflation, human capital, control of corruption, government effectiveness, political stability. rule of law, regulatory quality, and voice and accountability) does not Granger cause economic growth. The tests statistics (W-stat and Z-stat) for all variables are found be significant except for openness, government effectiveness, political stability, and regulatory quality indicating rejection of the null hypothesis. It advocates that all the variables, including governance indicators, do Granger cause economic growth. This study does not find bidirectional causality between any two combinations of variables, which endorses robustness in endogeneity bias. Thus, these findings confirm the conclusions drawn from the panel ARDL test (Dumitrescu and Hurlin, 2012).

Dumitrescue-Hurlin Panel Causality Tests.

, **, and ** Signify statistical significance at

Conclusion, Policy Implication, and Recommendation

External debt is often considered a significant source of revenue for various emerging countries serving as a crucial means to finance domestic initiatives aimed at fostering economic growth and development. However, many developing countries have failed to effectively utilize this external source of revenue to progress their countries. Some countries are also experiencing precarious debt situations with the advent of the recent COVID-19 pandemic. This study examines the relationship between external debt, economic growth, and governance across 18 emerging countries using annual data from 1996 to 2020.

The fundamental conclusion of this paper is that external debt has long-run associationship with economic growth. The study reveals negative association between external debt and economic growth both in the short-run and long-run. It suggests that the higher the external debt, the lower would be the economic growth. It implies that enormous amount of borrowing and future debts and negligence in using the funds efficiently would hamper economic growth in these countries. However, external debt can also exert positive impact on economic growth when there is an improvement in the institutional quality. This study reveals that the interaction of external debt with three governance indicators namely control of corruption, voice and accountability, and rule of law influences economic growth favorably. It suggests that quality of governance especially in controlling corruption, freedom of citizens in choosing a worthy government, and improved law enforcement institutions matter in promoting efficient use of external debt in emerging countries considered in our analysis. The interactions of external debt with other three governance indicators (political stability, government efficacy, and rule quality) affects economic growth unfavorably. The relationship between governance indicators and economic growth is also validated from the causality analysis. Though this result is contrary to the expectations, it is understandable that these three indicators are highly correlated with each other. An unstable government with rise in violence/terrorism will have less incentive to formulate and implement sound policies, and its regulatory quality would be poor. The poor regulation would hinder the development of the private sector. However, despite having a stable government, with improved public services, and reduction in crime rate, the pressure from the opposition parties may lead to inefficient use of external debt resulting in a reduction in economic growth.

All the governance indicators may not affect the external debt and economic growth favorably as as demonstrated by the findings of Tarek and Ahmed (2017). They found that poor governance (low score in political stability, absence of violence, regulatory quality, and rule of law) lead to higher accumulation of public debt in MENA countries. But good governance (high score in control of corruption, and voice and government effectiveness) can also lessen the accumulation of public debt which supports the romantic view of corruption. Moreover, using data from 44 Sub-Saharan African countries, Kemoe and Lartey (2022) discovered a negative association between public debt, and economic growth, it’s impact get reduced with improvement in the institutional quality captured by anti-corruption perception and government effectiveness indicators.

This work provides some concrete suggestions/implications for policymakers as follows. First, the enormous amount of external debt with the advent of economic crises, needs to be addressed with a sound debt management policy. Second, recently it has been noticed that many emerging countries are misusing debt by offering freebies which results in a high debt burden to the government exchequer. Therefore, authorities need to make extensive policies to use the debt effectively. Third, governments of emerging countries should improve the quality of governance by ensuring better voice and accountability, control of corruption, and enforcing the rule of law. Fourth, most of the emerging countries spend more than required amount debt in preventing war, improving the trade balance, and reducing financial loss with the advent of COVID-19 pandemic. Therefore, it needs urgent attention of government authority to use the debt adequately.

Footnotes

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with or publication/or publication of this article.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.

Data Availability Statement

The datasets generated and/or analyzed in the current study are available in the World Bank database (https://data.worldbank.org/) and Worldwide Governance Indicators (![]() ) repository.

) repository.