Abstract

While it is hypothesised that inflation and external debt stifle human development, empirical findings on this relationship have been equivocal. This study investigated the impact of inflation and external debt on human development (proxied by the Human Development Index) in 14 Southern African Development Community (SADC) countries. Estimations were based on the two-step system Generalised Method of Moments (GMM). The results of pooled Ordinary Least Squares (POLS) and difference GMM were also reported for robustness. It was established that inflation and external debt stifle human development. Based on these results, policies to reduce inflation and external indebtedness are necessary for human development in the SADC region. To control inflation, SADC countries should avoid monetising budget deficits. Regarding external debt, SADC countries should diversify exports, boost foreign currency earnings, and reduce indebtedness. SADC countries should also allocate borrowed funds for infrastructural development, for example, railways, roads, and electricity. This is the first study to investigate the effect of external debt on human development among SADC countries. Moreover, an estimation technique robust to endogeneity bias and heteroscedasticity is adopted.

Introduction

In developing countries, the efficiency and effectiveness of economic systems in improving the welfare of citizens is derailed by regular price and currency instability. Above single digit inflation erodes national budgets, savings and aggregate demand in the SADC region. Real incomes are continuously being eroded by inflation, creating a system that fight noble policies to improve economic well-being of citizens. High inflation also widens the “savings-investment gap,” a key limiting factor to sustainable economic development. Structural development models advocate for closing the savings gap through increased foreign capital to enhance economic growth and development. In this regard, institutions offering development support such as the World Bank usually disburse long-term finance for infrastructure projects such as transport and communication, agriculture, health and education (Maurer, 2017). Other multilateral institutions such as the IMF offer conditional Balance of Payment support to enhance macroeconomic stability (Muhumed & Gaas, 2016).

The widening development gap, coupled with a growing scarcity of both borrowed and available funds, is continuously redefining the development needs of the Global South. Increased globalisation brought new opportunities for foreign currency denominated funding in developing countries (García-Arias, 2008). To finance developmental needs and subsequently address economic challenges such as high inflation, low growth and living standards, government usually borrows from bilateral and multilateral partners (Foster et al., 2023). Most SADC member states had high levels of external debt in the 1990s and specifically in 2001, external debt as a percentage of GDP reached alarming levels by exceeding 100% for Angola, Democratic Republic of Congo, Malawi, Mozambique, Tanzania and Zambia (SADC, 2022). In 2012, most SADC countries’ external debt was within the macroeconomic convergence target of 60% except Seychelles and Zimbabwe (SADC, 2022). There are some SADC countries that benefited from the Heavily Indebted Poor Countries (HIPC) Initiative and hence the average external debt for SADC countries is slightly above the continental average (SADC, 2023).

Below the external debt threshold, the country’ economic fundamentals are usually stable and the risk profile is low while international lines of credit are plenty. Unlike domestic debt, where borrowers benefit during inflationary periods, the cost of external debt increases with the level of inflation. At high levels of inflation, the exchange rate usually depreciates triggering, debt default in over-indebted countries. African Development Bank (AfDB, 2024) stressed that the debt exposure in Southern Africa varies from country to country and the average external debt in Southern Africa remained high, rising to an average of 49.5% of GDP in 2023 from 46.2%. For nonindustrial countries, Kose et al. (2022) suggested 40% debt-to-GDP ratio -as a turning point at which risks of debt exposures start to increase, and is even around 25% for lower-income countries. Notably, debt overhang is unsustainable and retard a country’s growth potential (Khan et al., 2025).

Above certain external debt to GDP threshold, external debt not only drags GDP growth but impedes poverty alleviation strategies and human development. The country’s risk profile deteriorates, and usually, this is marked by episodes of macro-economic instability (International Monetary Fund and World Bank, 2022). Debt financiers, concerned with minimising defaults, become increasingly reluctant to extend further credit. Government’s thrust to improve human development is constrained by repayments of external debt competing for funding with new and other development projects in progress. In some cases, Government might resort to unfavourable policies such as monetised budget deficit. This causes inflation and lowers living standards through reduced economic growth and development. Over-indebtedness also crowds-out the much-needed private sector investment and social expenditure.

Apart from over-indebtedness and increased likelihood of macroeconomic instability, adoption of structural adjustment models in Southern Africa excluded vulnerable groups from access to health and education (Thomson et al., 2017). The anticipated development trajectory failed to take-off in some countries despite increased external financing and support. Notably, poverty levels are increasing in many developing countries and renewed efforts are needed to improve economic well-being of citizens by 2030 (Chikandanga et al., 2025). Greater income inequality is marked by significant levels of malnutrition in some countries despite record breaking levels of economic growth in some SADC countries (Gregory Kambaila, 2019; Louis & Kaberuka, 2008).

According to Olamide et al. (2022), the Southern African Development Community (SADC) seeks to improve the welfare state of its members through regional integration. Some of these countries are characterised by high levels of poverty and income inequality, low economic growth, high public debt, low living standards and episodes of high inflation. Notably, Zambia, Mozambique, Malawi, the Democratic Republic of Congo and Zimbabwe once suffered episodes of hyperinflation. At one point, SADC member states set a macroeconomic convergence benchmark of 3% inflation rate by 2018 (SADC, 2023), a target that was hardly attained by member states. However, according to AfDB (2024), on average, only Southern African countries experienced a decline in inflation in the continent by 2.7% to 9.3% in 2023, but since the COVID-19 pandemic, inflation pressures remain high across the African continent.

Apart from targeting the attainment of the 2030 Sustainable Development Goals (SDGs), Southern African countries had embraced Agenda 2063 spearheaded by the African Union (AU). Agenda 2063 is inward looking, targeting inclusive growth and sustainable development for Africa through industrialisation and value-addition of abundant natural resources (SADC, 2015). The agenda seeks to build on existing development strategies but some strategies like external financing strategies have reached the threshold that drags human development. This study investigated the impact of inflation and external debt on human development in SADC countries using the Generalised Method of Moments (GMM) estimator. While it is hypothesised that inflation and external debt retard the attainment of a better welfare state, empirical findings on this relationship have been equivocal. Although inflation is expected to worsen poverty and reverse gains in the country’s development agenda, Mohammed (2022) obtained contradictory results for Sub-Saharan Africa while Onakoya et al. (2019) and Omodero (2019) found insignificant results. Also, Nwokoye et al. (2024) found that external debt stocks and external debt service positively impacted the Human Development Index (HDI) in Nigeria. In a study of the BRICS nations, Ayoub et al. (2024) found that external debt improved life expectancy, a key component of the HDI.

Given the ambiguous effect of inflation and indebtedness on human development, the study analyses this relationship in the context of SADC countries. To date, there is no similar study for the SADC region on this topic. Moreover, this study used a two-step system GMM, a novel estimator, that is robust to endogeneity bias and heteroscedasticity. The study complements strategies to enhance human development in SADC in line with SDGs.

Literature Review

Theoretical and Conceptual Framework

Endogenous Growth Theory

Endogenous growth theory was developed to explain long-run growth generated from internal forces rather than external forces (Lucas Jr, 1988; Romer, 1990). The model is anchored on human development, technological advancement and knowledge, which are the key drivers of growth (Romer, 1994). To induce growth, a combination of the aforementioned should be utilised to improve growth and HDI. Furthermore, there is a need for knowledge acquisition to achieve human capital development. Romer (1990) suggested that investment in HDI unlocks knowledge acquisition. Such knowledge should be used to channel resources towards productive sectors which improves HDI. The model assumes the government to play a centre role of stimulating the economy through its expenditure. This spending improves HDI through the provision of public goods and services which will be financed by increased taxation. However, this might have a dual effect, as it could stifle private innovation and investment from the private sector (Adedeji et al., 2024). The region is suffering from increased poverty levels and low living standards due to its excessive taxation structure, resulting in low private investemet (Ndulu, 2007). In cases of an unbalanced budget, the government may resort to debt which will be financed through taxation and interest rate hikes, resulting in inflation build up. Given the high population growth in Africa, the government is more likely to run into a deficit and this will trigger tax hikes to fund expenditure, hence driving citizens into poverty at the same time deterring investment (Ndulu, 2007).

However, Mankiw et al. (1992), Barro and Sala-i-Martin (1992), and Evans (1996) criticised the model, stating that its predicted long-run convergence between the less developed and developed economies is not applicable in the real world because of different economic growth policies and institutions. The model is very useful to the current study because the SADC region is focused more on structural transformation, which is achievable through human development and technological innovation. In addition, the regional governments are operating under constrained budgets, unsustainable debts and inflationary economic environments, which is very detrimental to HDI.

Debt Overhang Theory

The debt overhang hypothesis by Krugman (1988) postulated that the accumulation of excessive public debt impedes economic growth and poverty alleviation. Debt overhang occurs when investors or creditors predict that a nation’s debt is surpassing its repayment capacity, the expected increase in debt-serving costs signalling a reduction in domestic and foreign investment, resulting in a decline in economic growth (Krugman 1988; Pattillo et al., 2002). The crowding-out effect happens when the government channels resources towards debt servicing instead of investing in the social service sector, which improves HDI (Pattillo et al., 2002). The accumulation of public debt triggers the government to raise taxation levels and interest rates, which are inflationary in nature, thereby driving people into poverty through the activation of crowding-out policy mechanisms (Pattillo et al., 2002). Building on the established theories of debt overhang and crowding-out effects, the theoretical foundation predicts a negative impact of external debt on HDI (Ampah & Kiss, 2021; Dinga et al., 2025). This theoretical foundation recognises that these relationships are non-linear in nature, confirming that debt is optimal below the minimal threshold, and beyond that level, debt overhang and crowding-out begin to manifest (Dawood et al., 2024).

The accumulation of unsustainable debt lowers growth prospects, further curtailing government social spending, thus exacerbating poverty levels. Elkhalfi et al. (2024) contended that external debt is a future burden which slows capital accumulation and consumption. In addition, this limits resource allocation towards human development. From this analysis, the model is very pertinent to the current study because SSA economies are drowning in unsustainable public debt.

Moreover, the current study draws inspiration from the aforementioned Endogenous growth model and debt overhang theory regarding the influence of indebtedness and inflation on HDI. As suggested by Adedeji et al. (2024), the government seeking to influence growth and HDI engages in unbalanced expenditure, accumulating external debt, which discourages investment because investors will perceive austerity measures which are inflationary (Ampah & Kiss, 2021; Dinga et al., 2025; Pattillo et al., 2002). The government may resort to monetising debt or devaluing its currency, leading to inflationary pressure which erodes the purchasing power of households, especially the low-income earners, pushing them into poverty (Pattillo et al., 2002). Servicing external debt diverts resources from social spending, worsening the deterioration of HDI (Ampah & Kiss, 2021; Dinga et al., 2025; Vaggi & Frigerio, 2024). As a result, the current study investigates the effects of indebtedness and inflation on HDI in the SADC region. Graphically, the concept of this study is illustrated in Figure 1.

Theoretical framework.

Empirical Review

Surprisingly, the bulk of studies took a myopic approach of analysing the impact of inflation and indebtedness on poverty separately, yet a paucity of them used a comprehensive analysis of inflation, indebtedness and HDI. Notably, most of them used linear models, hence giving nonconclusive results. For instance, Onakoya et al. (2019) concluded that inflation promotes human development, while Celik and Kostekci (2025) documented that inflation is detrimental to human development.

Debt and Human Development

Empirical studies on debt and HDI are still scant, while there is a large body of work on its impact on economic growth. Below, a review of this strand is given.

Researching public debt and human capital development in Nigeria, Nwokoye et al. (2024) used a fully modified ordinary least squares approach from 1990 to 2021. The study disaggregated debt into domestic and external debt. The results obtained conclude that disaggregated debt is positively related to HDI. Lastly, no evidence of debt overhang was found. Surprisingly, the conclusion from the study is in contradiction with the debt overhang hypothesis.

Similarly, Vaggi and Frigerio (2024) in SSA concluded that there is a trade-off between debt service and human development expenditures; the region was found to be trapped in unsustainable debt trajectories that predated COVID-19. The study used the Geometry of Debt Sustainability model (GDS) from 2015 to 2024 in Kenya and Ubuntu countries using SSA average indebtedness conditions.

On the other hand, a non-linear Panel Smooth Threshold Regression (PSTR) was employed on 95 developing countries from 2002 to 2015 (Zaghdoudi, 2018). The obtained results documented that there is a positive relationship between human development and external debt below a 41.7775% debt threshold. Above the minimal threshold, external debt becomes detrimental to human development.

A GMM and dynamic correlated estimation approaches were applied to 32 Asian economies from 1995 to 2020 (Dawood et al., 2024). The findings revealed that investment, total factor productivity and national savings have a non-linear effect of external debt on economic growth, while productivity and saving bring linear effects.

On the other side of the Asia-Pacific region Brueckner et al. (2024) used GMM and concluded that external debt mitigates natural disaster adverse impacts on the human development index. Moreover, there is an inverse relationship between natural disasters and the human development index. Lastly, external debt was found to smooth consumption during periods of disasters, hence improving human development.

A dynamic common correlation effects methodology was used on 35 SSA countries from 1995 to 2018 (Dinga et al., 2025). Domestic investment was found to be promoting economic development and human development index measured using the proxy of income, education and life expectancy. However, external debt drag the human development index components of life expectancy, education and income. While the model was robust, a potential endogeniety problem can be noted with reverse causality. Lastly, the study failed to account for the importance of governance, which is crucial for debt.

Using a Driscoll-Kraay, Augmented Mean Group and Panel Corrected Standard Errors from 1991 to 2005, Ampah and Kiss (2021) examined the implications of external debt and capital flight in the SSA region on welfare. HDI was used as a proxy for welfare, and concluded that external debt and capital flight are detrimental to welfare, resulting in debt overhang. However, the study’s chosen estimation procedure is subject to endogeneity bias. Narrowing down to the SADC region, a dynamic common correlated effects and augmented mean group estimation was used on 16 countries from 2000 to 2020 (Okoth & Omar, 2025). Economic growth was found to contribute towards HDI. However, environmental pollution and corruption had a mixed impact across the whole region. Based on these empirical findings, it is not clear how debt influences HDI. Subsequently, the study develops and evaluates the following hypothesis

Inflation and Human Development Index

Onakoya et al. (2019) concluded that inflation and FDI have a positive relationship with human capital development, while exchange rates and trade openness are negatively related to poverty, after using Ordinary Least Squares on 21 African countries from 2005 to 2014.

Following the same approach and multiple linear regression was Omodero (2019) in Nigeria from 2003 to 2017. Government capital expenditure and inflation were found to be negatively insignificant to human development. Similarly, corruption was found to have no impact. On the other hand, government recurrent expenditure was positively related to human development. However, the chosen estimation approach is subject to an endogeneity problem, hence resulting in estimation bias.

A Moment Quantile Regression technique was used in nine countries from Central and Western Asia from 2000 to 2021 (Celik & Kostekci, 2025). The obtained results revealed that corruption reduces human development, while political stability and the rule of law positively contribute to human development. In addition, trade openness and carbon emission reduction promote human development. Inflation, unemployment and population growth negatively affect human development. The study left out the importance of governance and the chosen study frame is out dated making the conclusion less effective to stimulate relevant policy formulation.

Furthermore, Akinlo and Dada (2021) moderated the effects of FDI on environmental degradation and poverty reduction using two-step GMM and 39 SSA countries from 1960 to 2018 The findings concluded that FDI reduces poverty measured using HDI. However, the interaction term of FDI was found to be inducing poverty effects of environmental degradation. Conversely, when measuring poverty using HDI, the interaction term of FDI reduces poverty. The study neglected to empirically test the moderating role of FDI to ascertain how it affects the strength and direction of the relationship between environmental degradation and poverty.

In addition, an ARDL approach was used in the Maghreb region from 1990 to 2022 (Mateko, 2025). The obtained results revealed that in the short run agricultural sector increases poverty. While, in the long run, manufacturing sector reduces poverty. As a result, the study developed and tested H2 to examine the effects of external debt on the Human Development Index.

The weakness in the prior studies on the relationship between external debt, inflation and HDI in the SADC region stems from the outdated time spans, biased econometric models and a myopic approach of treating inflation separately. These studies, predominantly Okoth and Omar (2025), Ampah and Kiss (2021), Akinlo and Dada (2021), Dinga et al. (2025), underscore the critical need for more recent and region-specific research to address these shortcomings. Results from these findings are intriguing, yet the majority of them neglected the impact of inflation on HDI. Additionally, they employed other econometric models, constraining the applicability and reliability of their findings. Future research must rectify these methodological weaknesses by adopting a more advanced econometric model and integrating current data. Therefore, the study seeks to examine the effect of inflation, indebtedness on HDI, which is the study’s novel feature, by using an advanced econometric model and recent data.

Methodology

Empirical Analysis

To investigate the impact of inflation and indebtedness on human development, the HDI was used as the dependent variable. This proxy has been used in previous studies (Asongu et al., 2023; Chipunza & Ntsalaze, 2025). The HDI is computed as the geometric mean of three indicators: health, education, and a decent standard of living (United Nations Development Programme, 2025). Health is proxied with life expectancy, education by the mean number of years of schooling, while per capita income represents living standards. Given the dynamic nature of most economic relationships, the lagged dependent variable was included as one of the explanatory variables. Thus, to assess the impact of inflation and indebtedness on human development in the SADC region, the dynamic model was specified as:

where i denotes country, t is time (in years),

Due to differencing and the dynamic nature of the models, first-order autocorrelation (AR1) is expected in the difference and system GMM. However, second-order autocorrelation (AR2) is not allowed (Atsu & Adams, 2023; Emin & Emin, 2025). Besides the issue of first- and second-order autocorrelation, the reliability of GMM estimates also depends on instrument validity. Instrument validity is confirmed through the Hansen’s J or Sargan’s test of over-identifying restrictions. If the instruments are valid, the null hypothesis of valid instruments is not rejected, that is, the Hansen’s J or Sargan’s test should be insignificant. To control the bias caused by instrument proliferation, the GMM estimations in this study included the “collapse” sub-option (Roodman, 2009). Ideally, the number of instruments should not exceed the number of cross-sections (N), although this does not necessarily safeguard the Hansen’s J test (Roodman, 2009). In this study, the lagged dependent variable was used as an instrument in the gmm-style while all the explanatory variables were the instruments in the iv-style. Next, each of the explanatory variables used in the regressions and their a priori relationships with human development are justified.

According to the debt overhang theory (Krugman, 1988), excessive debt is a tax on future economic prospects, reducing investment and economic growth. Indebtedness may also force the government to reduce crucial spending on health and education (Chipunza & Ntsalaze, 2024), thereby adversely impacting these key components of the human development index. Thus, a negative relationship between debt and the HDI is expected (Ampah & Kiss, 2021).

Regarding inflation, a negative relationship with human development generally exists (de Carvalho et al., 2017; Gonese et al., 2023). Inflation erodes purchasing power and negatively impacts real expenditure on health and education, resulting in a deterioration of the human development index. Inflation also stifles economic growth, causing a decline in per capita income. A fall in per capita income undoubtedly reduces the HDI. Therefore, inflation is expected to negatively impact human development.

Besides per capita income and life expectancy, educational attainment is a key component of the HDI. In most SADC countries, the government accounts for a significant share of total educational expenditure. Therefore, an increase in government education expenditure is expected to improve educational attainment and boost the HDI (Nurvita et al., 2022; Özbal, 2021). Government education spending is predicted to promote human development.

Despite the government’s role in health and education financing, household liquidity constraints inhibit human capital investments. International remittances can play a significant role in bridging this financing gap. Households find it easier to use remittances to pay for health and education, leading to improvements in the human development index (Khan, 2024; Xia et al., 2022). Thus, remittances are hypothesised to have a positive relationship with the HDI.

Without good governance, resources channelled to sectors such as health and education could be a social waste. Government effectiveness entails quality public service delivery and the ability of the government to develop and implement policies. The conversion of available resources into human development outcomes depends on the effectiveness of the government. A high level of government effectiveness accelerates human development (Chipunza & Ntsalaze, 2025; Kunawotor et al., 2024; Okoth & Omar, 2025); hence a positive association is expected.

Data and Sources

Balanced, annual panel data for the period 2010 to 2023 was used. HDI data were obtained from the United Nations Development Programme (UNDP, 2025), while inflation statistics were accessed from the International Monetary Fund (IMF, 2025). The source for the rest of the variables was the World Development Indicators database (World Bank, 2025). Table 1 provides a description of the variables, the data sources, and the expected relationship with human development. The study was based on 14 SADC countries, namely, Angola, Botswana, Comoros, Democratic Republic of Congo, Eswatini, Lesotho, Malawi, Madagascar, Mauritius, Mozambique, South Africa, Tanzania, Zambia, and Zimbabwe. Data on external debt was not available for Namibia and Seychelles; hence, the two countries were excluded from the analysis. The dataset contained a few missing observations that were filled using mean imputation.

Description of Variables.

Source. Authors’ computations.

Results

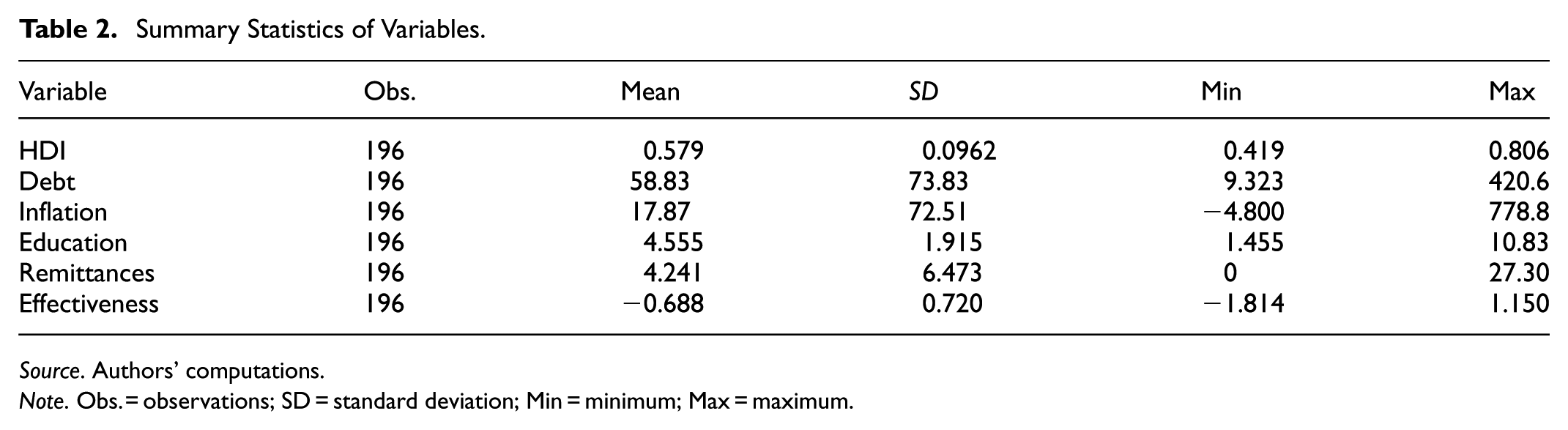

Summary Statistics

The summary statistics of the variables employed in the study are presented in Table 2. High variability was been observed for all variables, except HDI and education. The mean value of the HDI was 0.579, with a minimum of 0.419 and a maximum of 0.806. As a proportion of Gross Domestic Product (GDP), SADC governments spend 4.555%, on average, with some countries allocating less than 2% of GDP, for example, Angola, Comoros and the Democratic Republic of Congo. There have been wide variations across countries regarding price stability (inflation). While the mean annual inflation rate stood at 17.87%, it entered the triple-digit territory in SADC countries such as Zimbabwe. Concerning indebtedness, the status of SADC countries has not been pleasing as external debt stocks (as a proportion of Gross National Income) have been 58.83%, on average, reaching a high of 420.658% in Mozambique. Remittances also reflected wide variability, reaching 27.30% of GDP, with a mean of 4.241 and a standard deviation of 6.473%. In terms of government effectiveness, SADC countries have generally struggled, with the mean index being −0.688.

Summary Statistics of Variables.

Source. Authors’ computations.

Note. Obs. = observations; SD = standard deviation; Min = minimum; Max = maximum.

Results of Multicollinearity Tests

Multicollinearity tests were based on the method of variance inflation factors (VIF). As reported in Table 3, the mean VIF was 1.43, while the highest was 1.91. Moreover, the correlation matrix shows that none of the correlations exceeded 0.80. According to these results, there was no evidence of multicollinearity among the regressors used in this study; all the VIF values were less than 5 and all correlation coefficients were lower than 0.80.

Results of Multicollinearity Tests.

Source. Authors’ computations.

Note. VIF = variance inflation factor.

Regression Results

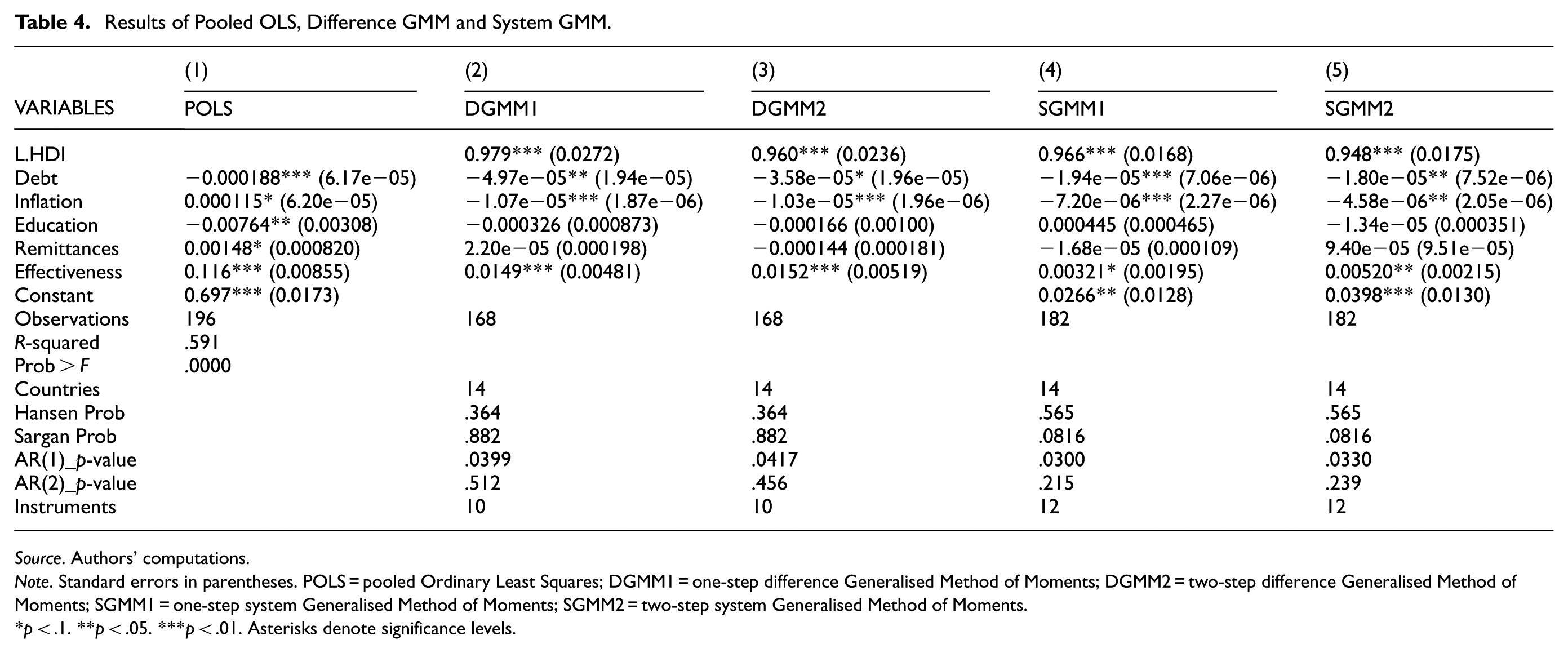

The estimation results on the influence of inflation and indebtedness on human development are presented in Table 4. As shown by the results of the dynamic models, the coefficient of the lagged dependent variable is positive and significant, indicating that human development is a gradual process. Generally, the results of the difference GMM align with those of the system GMM. In both cases, indebtedness and inflation stifle human development, while good governance enhances it. Following Roodman (2009), the results of the pooled OLS technique are also reported to confirm the reliability of the GMM estimates. The pooled OLS results reinforce the notion that the debt burden inhibit human development in the SADC region.

Results of Pooled OLS, Difference GMM and System GMM.

Source. Authors’ computations.

Note. Standard errors in parentheses. POLS = pooled Ordinary Least Squares; DGMM1 = one-step difference Generalised Method of Moments; DGMM2 = two-step difference Generalised Method of Moments; SGMM1 = one-step system Generalised Method of Moments; SGMM2 = two-step system Generalised Method of Moments.

p < .1. **p < .05. ***p < .01. Asterisks denote significance levels.

Given the relative merits of the two-step system GMM discussed in the empirical analysis section, the results interpretation for this study are based on this model. The negative coefficient of debt in Table 4 implies that the HDI deteriorates as SADC countries accumulate more external debt. Specifically, a 100% increase in external indebtedness reduces the HDI by 0.0018 points. Similarly, a 100% rise in inflation is associated with a 0.000458-point decrease in the HDI. Unlike indebtedness and inflation, government effectiveness promotes human development among SADC countries. A 1% improvement in government effectiveness enhances the HDI by 0.0052 points.

Regarding the regression diagnostics, the Hansen and Sargan tests reveal that the instruments are valid. As highlighted in the methodology section, the statistical insignificance of these tests confirms the validity of the instruments. The results show that the tests are insignificant in all cases; hence, the null hypotheses are not rejected. In addition, the serial correlation tests confirm the presence of first-order autocorrelation (the test is significant). On the other hand, there was no autocorrelation of the second order since the probability value of the test exceeded 0.05. These results are consistent with the GMM estimation requirements.

Discussion

The study revealed the impact of external debt and inflation on Human Development Index in SADC. The significant negative results of the impact of inflation on HDI are in line with Celik and Kostekci (2025) who documented that inflation is detrimental to human development. However, the significant negative results indicating that external indebtedness reduces economic well-being of citizens are in contrast to Nwokoye et al. (2024), who found that external debt stocks and external debt service positively impacted the human development index and also, Ayoub et al. (2024), who support that external debt improved life expectancy. They are in line with Zaghdoudi (2018), who found a positive relationship between human development and external debt below a 41.78% debt threshold. External debt positively affects human development usually when the country’s debt to GDP ratio is still below the threshold and if debt conditions are supportive to increased social expenditure.

Given average external debt as a percentage of GNI of 58.63% in SADC, over-indebtedness in some countries worsens human development indicators by crowding out social expenditure as most government revenue is directed towards debt repayment. Such countries will persistently struggle to meet the Abuja declaration for 15% and 20% of the national budget towards health and education sectors respectively. Debt overhang increases country’s risk, exchange rate volatility and uncertainty leading to decrease in local and foreign direct investment. This drags economic growth and job creation, negatively affecting well-being of citizens in the SADC region. Conditional debt limiting government subsidies on health and education further amplify the negative effect of external debt on human development.

Given that Agenda 2063 is built on existing development strategies, SADC countries need to reconsider the use of external debt as a development strategy. The significant negative relationship between HDI and level of external debt in the SADC region requires government to borrow for productive purposes or to fund self-sustaining projects that will generate enough funds to repay the debt. In this regard, policy makers may consider prioritising grants for social expenditure, given that it is usually subsidised and does not generate significant cashflows that can be ring-fenced to repay debt. Borrowing should thus not be a last resort meant to avert a national crisis as this reduces the bargaining power of the borrower and forces the nation to enter into expensive debt contracts. Countries should also regularly honour their international debts obligation to protect the country’s risk profile and open more lines of credit for various sectors of the economy in future. SADC countries should therefore seek to attain at most 40% debt-to-GDP ratio suggested by Kose et al. (2022) and Zaghdoudi (2018), for nonindustrial countries, as this is turning point at which risks of debt exposures such as capital flight start to increase instead of the region’s macroeconomic convergence target of 60%.

Most SADC countries had struggled over the years to maintain inflation level to single digit levels with some having recorded world records for hyper-inflation. The study revealed that high inflation reduces welfare in the SADC region and is in contrast with Onakoya et al. (2019) concluded that inflation promotes human development. Inflation erodes real income, and the plight poor and fixed income earners is worsened by inflation. High inflation extends the poverty net to middle income earners whose family income might fall below the poverty datum line, causing food insecurity and lower living standards. The region’s reliance on food and energy imports exposes it, not only external shocks, but imported inflation that further prompt regional macro-economic instability. AfDB (2024) noted that economic growth in Africa is driven by private consumption and once inflation increases, private consumption declines leading to lower growth rates. Austerity measures are therefore strongly recommended to attain the SADC macroeconomic convergence inflation target of 3%. Member states should spend within their means and minimise budget deficit and avoid monetised debt.

Monetised debt is highly inflationary. Over-indebtedness also leads to depreciation of exchange rate. This exposes SADC countries to inflationary shocks and macroeconomic instability. External debt cost increases as the currency depreciates, further crowding out social expenditure. The government might increase taxes to finance the debt and this builds-up cost push inflation. Attempts to ensure macroeconomic stability by increasing interest rates when there is uncertainty due to unsustainable external debt further fuels inflation. The significance of government effectiveness in enhancing economic well-being in the SADC region requires member states to further strengthen good governance and combat all forms of corruption to ensure that resources are allocated efficiently and effectively. This will ensure that resources targeting human development are not diverted towards white elephant projects and the bureaucrat becomes accountable for every dollar budget allocated. Government effectiveness therefore improves delivery of public services including health and education, and also creates an enabling economic environment and fiscal discipline.

Conclusion

The study, using Generalised Method of Moments (GMM) estimator, revealed that both unsustainable external debt and inflation significantly inhibit human development in SADC while government effectiveness enhances it. Continued external borrowing by SADC member states without accelerating current external debt repayment or rescheduling it delays the attainment of SADC’s macroeconomic convergence target. There is need for SADC member states to carefully manage external debt and inflation in order to ensure macroeconomic stability and better living standards for citizens. To control inflation, SADC countries should avoid monetising budget deficits. Regarding external debt, SADC countries should diversify exports, boost foreign currency earnings, and reduce indebtedness. SADC countries should also allocate borrowed funds towards capital expenditure. The success of these recommendations largely depends on good governance which creates an enabling environment for sustainable economic development. Addressing inflation and over-indebtedness head-on also enhances the attainment of AU’s Agenda 2063. Given that HDI is a broad measure of human development, future studies might consider examining the effect of external debt and inflation on specific indicators of human development and extend the study period while employing other recommended panel data econometric methodologies such ARDL.

While this study provides valuable insights into human development across the SADC region, the analysis could not include all member states due to constraints in data availability. The macroeconomic approach employed does not also capture country-specific determinants of human development at the household level, nor does it account for variations in income distribution. In cases where there is high unequal distribution of income, it might alter the results. Additionally, the estimated Human Development Index (HDI) for developing countries may be subject to inherent biases. A significant and growing informal sector, alongside other unrecorded economic activities that underpin rural livelihoods, is often not fully reflected in national accounting. This may lead to systematic underestimation or overestimation of true development levels, particularly considering that the majority of the population lives in rural areas.

Footnotes

Consent to Participate

There are no human participants in this article and informed consent is not required.

Author Contributions

All authors contributed equally to this work.

Funding

The authors received no financial support for the research, authorship, and/or publication of this article.

Declaration of Conflicting Interests

The authors declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Data Availability Statement

The data used in this study is publicly available and can be accessed from the following websites: (https://databank.worldbank.org/source/world-development-indicators#; https://www.imf.org/external/datamapper/PCPIEPCH@WEO/COD/SSQ/; ![]() ).

).