Abstract

This article investigates the livelihood condition and income security concerns of Fijian seniors, retirees, and older persons, with a particular emphasis on the services provided by the Fiji National Provident Fund (FNPF). The report focuses on essential components of Fiji’s society and economy, such as population aging, retirement provisions, and the FNPF’s role. It also investigates the potential and conditions of poverty in the country, notably the poverty and health crisis among the elderly. The data for the study is gathered using a combination of quantitative and qualitative methodologies. A questionnaire survey is administered to 439 retirees, 45% of whom are female and 55% of whom are male. In-depth interviews and focus group sessions are also done to acquire a better understanding of the challenges and requirements of the elderly. Desk research is used to analyses numerous records received from the FNPF, publicly accessible yearly reports, and Department of Social Welfare pertinent resources on social services. The study highlights the FNPF’s general services to assure efficiency in financial obligation to pensioners, as well as the crucial relevance of economic stability for pensioners based on their monthly pension receipts. The data analysis and conversations shed light on the issues that Fijian retirees confront and potential areas for improvement in the FNPF’s services. Finally, the article emphasizes the importance of increased support and targeted measures to address the livelihood challenges of Fijian pensioners. The study’s findings can help policymakers and stakeholders devise effective methods to ensure the well-being and financial security of the country’s aging population.

Plain Language Summary

This article investigates the livelihood condition and income security concerns of Fijian seniors, retirees, and older persons, with a particular emphasis on the services provided by the Fiji National Provident Fund (FNPF). The report focuses on essential components of Fiji’s society and economy such as population aging, retirement provisions, and the FNPF’s role. It also investigates the potential and conditions of poverty in the country, notably the poverty and health crisis among the elderly

Introduction

The transition to modernity brought significant changes in social, economic, and cultural aspects of life as well as advances in science and technology. Health and wellbeing, particularly, have been improved through research in medical and health sciences. The social benefits of these are the epidemiological and demographic transitions in almost all societies underscored by the eradication of many communicable diseases and consequent improvements in life expectancy. This has meant increases in population ageing and older people in all societies; a demographic situation which will continue for some time. Increasingly, the chronological age 60 years has become the defining age for demographic and economic studies of the elderly. Recent analytical work on ageing has noted that “one in nine persons in the world (is) aged 60 years or over” (United Nations Fund for Population Activities, 2012). In the last 30 years, the World Health Organisation has issued reports that have brought focus to the health-related dimensions, requirements, and socioeconomic challenges associated with the process of ageing (WHO, 1984, 1986, 2012). The Madrid Plan of Action on Ageing (United Nations, 2003) emphasized the worldwide concerns and challenges associated with the increasing ageing of the global population (Sidorenko & Walker, 2004). Additional research has contributed to the comprehension of gender disparities in the ageing process. For instance, studies have highlighted the greater life expectancy of women (ILO, 2006) as well as their increased susceptibility to economic vulnerability (ILO, 2006) and the higher likelihood of experiencing poverty in old age (WHO, 2006).

Along with these changes is industrialization and its corresponding, and most significant, impact on the nature and structure of work and living arrangements (Pohlanyi, 1944). It brought wage and salary work, through formal employment, as primary means of livelihood and contributed to the weakening of traditional family structures through urbanization and migration. These together undermined the extended family and its responsibility for collective care for the elderly, the sick and the infirm. It also threatened the security of livelihood with the risk of unemployment and un-employability due to illness and age and brought the issue of age, ageing, and work from the confines of informal subsistence structures to the formality of the workplace, work contracts, and wages. With these, it introduced the concept and practice of pension and retirement, at a certain age, as the time of withdrawal from formal employment. The thinking that informs this was that during one’s working time, preparations for retirement through savings and accumulation of other relevant resources are undertaken to prevent the search for work at old age. The age of retirement has exhibited variation since the Bismarckian era and seems to be increasingly disconnected from an individual’s work capacity. However, the potential for insufficient resource accumulation and the ongoing increase in the cost of living remained a concern. The scholarly examination of this particular risk, as well as various strategies following the involvement of Bismarck, highlights the recent assertion made by Myles that the association between old age and poverty has diminished (Myles et al., 2002). However, Erol and Unal (2022) find evidence of a significant negative impact of recent immigrants on overall employment rates. Interestingly, this negative effect is more severe than reported in previous research using German data from the 1980s to the early 2000s. The negative impact that new immigrants are having on the employment rate of current workers may be due in part to their relatively lower degree of integration into the local labor markets and displacement impacts.

Notwithstanding the observation of Myles et al. (2002) the enduring concern with ageing in the midst of rapid economic change, is the threat of poverty and sustaining livelihood at retirement. We apply the term livelihood to refer to the totality of life and living conditions, including, especially, access to basic needs through adequate economic resources. We posit that livelihood can be at risk in old age and retirement when economic resources are meager and constrain access to basic needs and services. In doing so, we also underscore the circularity of the relationship between lack of access to services, including health, and poverty, as noted by the World Health Organization study (WHO, 2007), and recognize the threat of poverty and health, especially for women ageing. This paper examines the critical challenges to the livelihood of retirees or pensioners in Fiji who benefit from an established unfunded pay-as-you-go facility called the Fiji National Provident Fund (henceforth the Fund). This category of the aging population is less than 10% of the total elderly population, many of whom do not belong to this fund. Furthermore, though retirement remains at age 55, the percentage of older people, that is, those 60 years and over, of the retiree population is increasing. From about 24% in 1996, it increased to 32% in 2007, with a higher percentage living in urban areas and towns (Ministry of Women, 2011). The issues relating to the livelihood of those without benefits from the Fund are examined elsewhere (WHO, 2006). Suffice it to say that their livelihood is provided through multiple sources. These include family/kin relations, an unfunded but targeted social pension, and other subsidized social services of the government as part of a broad poverty alleviation program.

We have adopted the word

The World Bank rightfully underscored the issue of risks to livelihood in old age through poverty with its seminal work on “Averting the Old Age Crisis” (World Bank, 1994 ) and provided recommendations for countries to avert the crisis with policies that can contribute to economic growth. These policies are usually part of the poverty alleviation strategies of a broad neo-liberal development framework. The report surveyed prevailing systems for the provision of means of livelihood at retirement across many different economies. These schemes grew and became widespread post World War II and were introduced, at various times, into developing countries or former colonies. In a recent overview of pension schemes, Hujo (2014, p. 7) rightly observed, “Pensions reflect the protective role of social policy by guaranteeing income security and preventing poverty during retirement or old age.” He also recognized pensions as playing productive, redistributive, and reproductive roles in society’s larger scheme of things. However, perhaps the enduring question is the extent to which pensions are available in developing countries and to whom. The existing body of literature has put forth several plausible reasons for the observed phenomenon of reform reversal. According to several researchers, the main driving force behind reversals is the global financial crisis (Kay, 2014; Price & Rudolph, 2013; Schwartz & Arias, 2014). Nevertheless, this perspective is insufficient in explaining the latest reform reversals observed in Lithuania, Romania, Croatia, and North Macedonia. It is worth noting that these instances transpired a complete decade following the global crisis. Pension privatization plans have been quickly shot down in Western European countries with well-established Pay-As-You-Go (PAYG) systems. On the other hand, most Eastern European countries with similar PAYG histories have opted for the World Bank’s multi-pillar reforms from 1994, even though this approach has been heavily criticized (N. Barr, 2000; Beattie & McGillivray, 1995; Orszag & Stiglitz, 2001). The most controversial part was the “second pension pillar,” which required private pension funds to be set up separately from current pay-as-you-go systems. This caused the public pension system to have to pay huge transfer costs for decades (Altiparmakov & Nedeljkovic, 2022).

To date, pension schemes vary among developing countries of either Lower or Middle-income categorization as much as they do in the developed countries (Esping-Andersen, 2015). So also is the age of retirement itself and receipt of pension payments. The existing schemes are either self-funded through a Pay-As-You-Go (PAYG) facility, unfunded as government social pensions (either universal or targeted) derived from taxes, and government subsidy, insurance schemes, or both (ILO, 2006; WHO, 1994). Notably, funded pension schemes based on formal employment have not usually covered most workers in developing countries (Palacios & Pallares-Millres, 2000). This remains a concern for developing countries in the midst of population ageing as they implement strategies for development, informed mostly by policies of growth and their restraint on social spending.

The paper first outlines key aspects of Fiji’s society and economy, including an overview of population ageing, provision for livelihood at retirement, and the role of the Fiji National Provident Fund. It also outlines the conditions and potential of poverty in the country and the crisis of poverty and health in old age. The livelihood situation of pensioners is captured and analyzed at two levels. First, the general services offered by the National Provident Fund to ensure efficiency in its “financial” responsibility to pensioners and second, and most importantly, income security and pensioners’ concerns with livelihood needs based on the monthly pension receipts. In the paper, pensioners, retirees, and older people are used interchangeably. This is due to the overwhelming representation of people 60 years and over in the retiree population serviced by the National Provident Fund (Table 1) . The study’s methodology is then presented, followed by the data analysis, discussions, and conclusions.

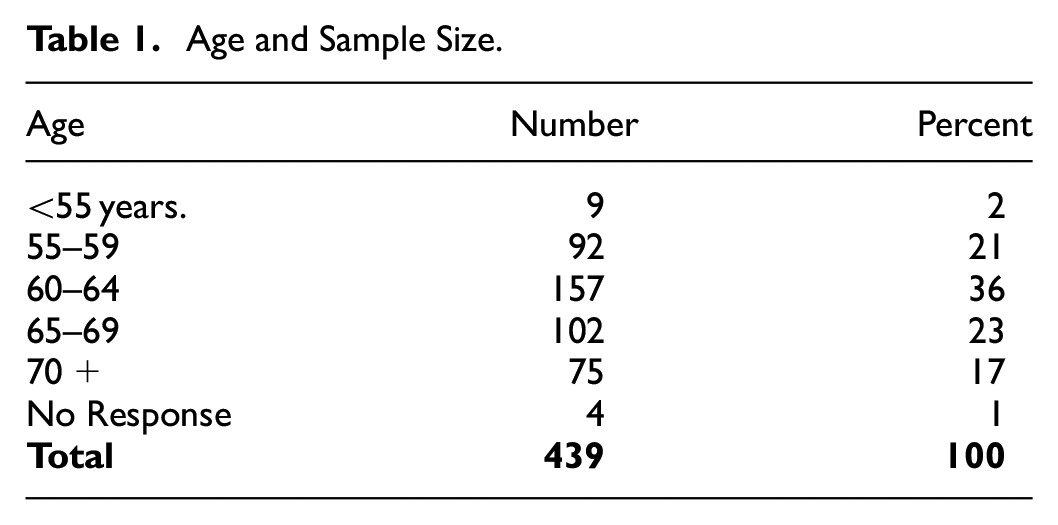

Age and Sample Size.

Fiji: Aspects of Society and Economy

Fiji, located in the South Pacific, is an archipelago characterized by a diverse population consisting primarily of indigenous individuals, known as I’taukei, and Indo-Fijians. The I’taukei population comprises approximately 57% of the total national population, while Indo-Fijians account for approximately 37% (Ministry of Planning and Statistics, 2010). Other ethnic groups include Chinese, Pacific Islanders and Europeans. The country covers a total area of about 18,272 km and spreads over 300 islands of which about a 100 are inhabited. Total population as of 2021 was 893,468 (Fiji Bureau of Statistics [FBS], 2021; Ministry of Planning and Statistics, 2011 ). Fiji gained independence in 1970 as a British colony and embarked on a development agenda influenced by the import substitution strategy of the 1970s. Since the mid-1980s, the development strategies have been influenced by a neo-liberal framework provided by the International Monetary Fund (IMF) and World Bank. This framework places a strong emphasis on economic growth. During the latter part of the 1990s, the government, in response to a growing poverty rate, adopted and executed the Poverty Alleviation Programme driven by the World Bank (World Health Organization [WHO], 2007). Subsequently, the situation has persisted, accompanied by government intervention through the implementation of equalization initiatives, including the provision of free education spanning from primary to secondary levels, as well as a subsidy for tertiary education coupled with a loan program. The aim is to harness a well-educated population as a powerful human resource for fostering economic development. Furthermore, a specific subsidy has been implemented for public utilities such as housing, water, and power. The economy is primarily propelled by various sectors, including tourism, commercial agriculture, fisheries, hardwood, and gold mining, as well as remittances. The latter nets an annual average exceeding $300 million dollars. (Ministry of Planning and Statistics, 2011). The Report noted that any decline of remittances would have a negative impact on the wellbeing of dependent households to cover primary needs such as food, education, and health care as well as improvements in housing. The portion of remittances that contribute to the livelihood of elderly people remains under research. Additionally, small-scale manufacturing is also prevalent in the production of consumer items, garments, and textiles. (ILO, 2016). Between 2004 and 2010, the economy experienced a period of sluggish growth primarily due to a decline in investments. However, it subsequently underwent a satisfactory recovery, driven by growth in construction, manufacturing, and tourism receipts. This recovery resulted in an average growth rate of approximately 4% between 2011 and 2015, as reported by the Ministry of Economy (2017, p. 120). According to the World Bank’s data for the year 2020, the Gross Domestic Product (GDP) per capita stood at U$4,376, while the Gross National Income (GNI) per capita was recorded at U$4,720.

The sugar industry, which has historically been a significant contributor to the country’s economy, has experienced a decline in prominence since the late 1990s. This decline can be attributed to the cessation of European Union subsidies and a concurrent crisis concerning land leases. This phenomenon instigated a movement of rural laborers to urban areas, as young agricultural workers sought employment opportunities that were not accessible in their hometowns, consequently leading to a significant increase in the number of individuals who were unemployed. According to the International Labour Organisation (ILO), in 2016, the prevailing unemployment rate stood at 6.2%, with a notably higher rate of 18.2% observed among individuals aged 15 to 24. The prevalence of informal employment is substantial, reaching 60%, with notable disparities observed between males and females, at 57% and 65% respectively (Government of Fiji, 2011). In the demographic subset of individuals aged 60 to 64, it has been observed that the rates of labor force participation can be as low as 30%. Fiji has been classified as a middle-income country, with a Human Development Index (HDI) of 0.724. However, it is evident that there is a prevalent state of poverty within the nation, as indicated by the national poverty rate that consistently hovers around 29% to 30%, considering the disparities between urban and rural areas (FBS, 2017). The situation is further aggravated by the presence of low and progressively unchanging wages from 2009 to 2016, a 20% devaluation of the Fiji dollar in 2009, resulting in a subsequent 38% increase in essential food items, and a fluctuating value added tax ranging between 17% and 12% (K. Barr, 2017).

According to the 2013 data, the life expectancy for males and females is reported to be 67.6 and 69.9 years, respectively. According to the Asian Development Bank (ADB, 2014), there have been advancements in the fields of health and sanitation, resulting in a growing proportion of the population gaining access to safe water and sanitation facilities. According to data from 2013, the proportion of the population with access to sanitation was 87.2%, while the proportion with access to water was 96.3%. The nation is currently experiencing a significant increase in urbanization, as evidenced by the fact that 60% of the country’s population now resides in urban areas. This trend is accompanied by the emergence of extensive informal settlements located both within the city limits and on the outskirts of major towns. The country’s susceptibility to hurricanes due to its geographical location can have detrimental effects on the economy, particularly in relation to housing. The enduring impact of Hurricane Winston on agriculture, housing, and the economy remains evident, as scholarly research has also highlighted the profound and wide-ranging consequences of climate change (WHO, 2013).

Population Ageing and Retirees in Fiji

The phenomenon of population aging remains a prominent aspect of the ongoing demographic shifts occurring in Fiji. According to Plange (1994), the elderly population in Fiji has experienced a gradual increase from approximately 5% in the early 1980s. As reported by the Government of Fiji (2011), the current elderly population stands at approximately 7.5%, which translates to approximately 73,900 individuals in relation to the total population. Projections indicate that this proportion is expected to rise to 17% by 2050. Just over 53% of the elderly population is found to be residing in rural areas. The aging of the population has a significant influence on labor force participation. In the year 1996, the proportion of individuals aged 60 years and above constituted 7.9% of the total population while comprising 5.7% of the employed workforce. According to the Fiji Bureau of Statistics ((2016, p. 16) , the proportion of the population affected by this phenomenon rose to 10% by 2007, while it accounted for 6.2% of the labor force. However, it is worth noting that the labor force participation rate was relatively low at 30%. The population of retirees has also experienced a consistent increase. According to the Government of Fiji (2011), the proportion of individuals aged 60 years and above who were retired was 31% in 2007. Given the upward trend in life expectancy, it is inevitable that this percentage will experience a corresponding increase. Fiji is experiencing a discernible trend of feminization in its aging population, as evidenced by a decreasing sex ratio. Specifically, the sex ratio has declined from 90.9 in 2000 and is projected to further decrease to 81.6 by 2025. According to the available data, the proportion of females aged 60 years and older in the population was 52.4% in the year 2000. It is projected to rise to 55.1% by the year 2025. According to Plange (1987) and the Ministry of Social Welfare, Government of Fiji (2011), the aging population is experiencing a greater number of widows compared to widowers, which can be attributed to the higher life expectancy of women.

The primary challenge faced by the younger elderly population in terms of their pension is the official retirement age, which is typically set at 55 years old. This age requirement is primarily applicable to public sector workers, although it is gradually being implemented in other sectors as well. Additionally, post-retirement employment opportunities, particularly in urban areas, present significant difficulties for this demographic. These challenges, as highlighted by Plange (1999), pose a considerable risk to the livelihood of individuals in their old age. According to WHO (2006) report approximately 70% of individuals aged 60 and above lack coverage from any established pension program. The current absence of a comprehensive policy to address an impending crisis is particularly concerning, particularly when considering the research findings that indicate a correlation between aging and poverty in developing nations (Barrientos, 2006). The various methods employed to maintain a sustainable livelihood during old age in Fiji can be classified into five distinct categories. The factors contributing to the financial security of older individuals can be categorized into five main areas. Firstly, the efforts of older individuals, particularly those living in rural areas and relying on semi-subsistence lifestyles, play a significant role ( Plange, 1999; K. Seniloli & Tawake, 2015). Secondly, the continuation of both formal employment and informal self-employment contributes to their financial well-being. Thirdly, access to a state social pension specifically designed for older individuals provides a targeted form of financial support. Fourthly, the National Provident Fund, although lacking sufficient funding, also contributes to their financial security. Lastly, a combination of these factors, including remittances in both monetary and non-monetary forms, further enhances their financial stability. According to Plange , there is a notable underrepresentation of women in the category of recipients of FNPF provident payments, particularly in relation to formal employment, with a focus on public sector workers.

The Fiji National Provident Fund

The establishment of the Fiji National Provident Fund (FNPF) took place in 1966 through the enactment of the FNPF Act. This retirement fund was specifically designed to cater to the needs of public sector employees, and its inception occurred toward the end of the Pax Britannica era. Subsequently, this policy has been expanded to encompass all employees. Currently, it stands as the sole superannuation fund in the nation that is legally obligated to gather mandatory contributions for the purpose of securing retirement savings for all employed individuals within the country. The contribution has experienced an increase from an initial rate of 10 pence per dollar in 1966 to the current rate of 16%, which was implemented in 2000. The FNPF Act has been subject to periodic amendments to address the nation’s evolving social and economic conditions. The modifications encompassed provisions that permitted the partial withdrawal of accumulated contributions for housing, education, and other social and cultural needs. These factors were deemed essential to contribute to future welfare by means of constructing or acquiring a house and providing education for oneself or one1’s children. One of the primary motivations for individuals to withdraw from higher education programs is to enhance their skills, which in turn leads to improved marketability and the potential for higher earnings. Additionally, such skill development can contribute positively to the overall growth and sustainability of the Fund. Additional structural changes were implemented in 2011 following assessments of the Fund’s procedures, which encompassed evaluations of investments, pension calculations, and payments (ILO, 2006; World Bank, 2006). These factors collectively influenced the decision to implement a “new pension business model characterized by actuarially fair and sustainable rates.” According to the Fiji National Provident Fund (FNPF, 2012), Presently, the Fund offers a variety of discretionary products to retirees upon reaching the age of retirement. The various types of pensions offered are as follows: Life pension, Joint pensions, Part Lump sum/Part Life pension, Part Lump sum/Part Joint Pension, Part Lump sum/Part Life/Part Joint, and Full Lump sum (FNPF, 2012). The main aim of the reform is to guarantee the long-term viability of the Fund.

The Fund makes considerable efforts to respond to the needs of pensioners. Essentially, these are all geared to achieving a responsive and effective delivery of Pension related services to the over 7,000 pensioners with the Fund. The range of these services includes the following:

Pensioner Confirmation and Queries services

Collection of Pension orders

Pensioner Renewal Certificate (every 4 months)

Retirement & Pension Advise (counseling services)

Change of payment mode (new bank account or order)

Home inspection (for pensioners who cannot visit our offices)

Update of pension details (address or phone contact).

Pension payments

Aging Fiji: Poverty, Health, and Livelihood

The primary factor in guaranteeing a sustainable quality of life during one’s later years is the ability to access and fulfill basic needs, with a particular emphasis on health and well-being. The existing body of research on the topic of livelihood in old age has emphasized the challenges experienced by elderly individuals as well as the obstacles that certain families encounter in terms of offering care and assistance to older individuals (Help Age International, 2000, p. 34). In a previous publication, I have characterized the absence of resources necessary for sustaining a basic standard of living during one’s later years as a form of “social disability” (Plange, 1991). The research conducted on aging and the elderly in Fiji spanned from 1984 to 1993, as documented by Plange (1987, 1990, 1994) . S. Panapasa and Maharaj (2002) as well as K. Seniloli and Tawake (2015) have both emphasized the healthcare requirements of older individuals due to disabilities or chronic illnesses. These studies corroborate the conclusions reached by previous researchers (Knodel & Chayovan, 1997). In Fiji, the burden of disease at the national level is predominantly influenced by non-communicable diseases, which are further exacerbated by the high prevalence of risk factors including smoking, alcohol consumption, and over-nutrition. According to a report by the World Health Organisation in 2003, it was observed that these practices have adverse effects on the mortality and morbidity of older individuals. Common health conditions among elderly individuals in Fiji encompass diabetes, hypertension, heart disease, and cerebrovascular diseases. According to the Ministry of Health (2014), as well as K. Seniloli and Tawake (2015), it is evident that the prevalence of Type 2 Diabetes (T2DM) in the population aged 60 to 64 has exhibited a consistent upward trend over the course of the last two decades, with figures rising from 17% in 1980 to 36.8% in 2011. Morrell et al. (2016) observed parallel rises in both obesity and cardiovascular diseases. According to a recent study conducted in Fiji by K. L. Seniloli and Tawake (2016), it has been observed that the older demographic tends to experience a higher likelihood of illness, physical weakness, or disability compared to individuals in middle age. The typical elderly individual, as described by K. Seniloli and Tawake (2015), is characterized by limited mobility and the presence of a disability or other significant medical conditions that necessitate ongoing medical attention and healthcare. S. Panapasa and Maharaj (2002) discovered that gender differences are an inevitable occurrence. The study conducted in Fiji observed a notable inclination for older widows to experience disabilities because of impoverished conditions and unaddressed healthcare requirements.

Although K. Seniloli and Tawake (2015) have highlighted the availability of care within family and kin networks, empirical evidence suggests that the resources allocated for caregiving often do not align with the desire to provide care. The gradual reduction in family size also contributes to a decline in available family resources for caregiving. As an illustration, WHO (2006) reported that approximately 60% of elderly individuals in Fiji resided in shared households, which often included their children. According to the Fiji Poverty Report (2006), there was a reduction of approximately 30% in the indicator by 2017. Previous studies have emphasized the significance of social networks in promoting health and well-being among older individuals (Seeman and Crimmins, 2001).

The issue of poverty in Fiji exacerbates concerns regarding livelihood and aging. According to the Asian Development Bank (ADB) report spanning from 2014 to 2018, the National Poverty Survey conducted in 2009 revealed a poverty incidence of 35% in 2003, which decreased to 31% in 2008 (ADB, 2014-2018). The prevalence of poverty among the elderly is highlighted by the statistic that approximately 70% of individuals aged 60 and above lack coverage from any form of pension system (ADB, 2014). According to the Ministry of Social Welfare, Government of Fiji (2011), individuals who receive a formal retirement pension from the Fund have an average monthly payment of approximately FJD 350 or FJD 81 per week. According to the National Policy on Aging, the income level discussed is approximately 1.7 times the poverty line for urban residents and approximately 2.0 times the poverty line for rural residents (Ministry of Social Welfare, Government of Fiji, 2011). The National Policy document acknowledges that the average pensioner who benefits from the Provident Fund may not be considered impoverished. However, the distribution of pension amounts is likely skewed toward the lower end, with a small number of individuals receiving pensions well above the average while the majority receive pensions below the average (Ministry of Social Welfare, Government of Fiji, 2011). The latter phenomenon is a result of a multitude of factors. These factors encompass inadequate salary and wage levels, resulting in constrained contributions to the Fund. According to K. Barr (2017), the segment of the population situated at the lower end of the wage/salary distribution poses a significant risk to their own sustenance due to the rise in poverty and inequality, which has severe repercussions for workers’ families.

The purchasing power within the economy is subject to constant influence from rising inflation and the imposition of value added tax on essential food items, resulting in significant negative consequences for household income (WHO, 2006). However, it is important to acknowledge that an additional element contributes to poverty and old age among retirees in Fiji. The phenomenon being referred to is the act of retired individuals withdrawing their accumulated contributions in a single lump-sum payment, which is subsequently spent within a relatively brief period. This behavior carries certain unavoidable repercussions, such as financial need, as highlighted by K. Seniloli and Tawake (2015). Traditional living arrangements with children and others fail to fulfill a specific requirement. Traditional living arrangements, characterized by extended family structures that effectively pool resources (S. V. Panapasa, 2002; Plange, 1994), no longer offer a reliable means of escaping poverty or ensuring a satisfactory standard of living during old age. According to a study conducted by the World Bank in 2011, it was discovered that households in Fiji that consist of children and elderly individuals are significantly more susceptible to experiencing poverty. Households that consist of both elderly individuals and children exhibit the highest levels of poverty, as indicated by a poverty headcount rate of 52%.

This study focuses on the provision of government assistance exclusively to individuals who are recipients of the Fund and belong to the retiree and elderly population. The scope of this aid is restricted to reduced rates for public transportation for individuals who are 62 years old or older, in addition to the provision of free prescription medications at designated pharmacies.

Methodology

The study employed a combination of quantitative and qualitative research methods. The data collection methods employed in this study included a survey utilizing a questionnaire, as well as key informant interviews and focus group sessions. The themes for the focus group and key-informant interviews were derived from selected components of the survey questionnaire. The primary method employed for this study was desk research, which involved the examination and analysis of various documents. These documents were obtained from the National Provident Fund, as well as publicly accessible annual reports such as the National Policy on Aging, 2011 to 2015 published by the government Ministry of Women, Children and Poverty Alleviation. Additionally, relevant materials on social services were sourced from the Department of Social Welfare. The key informants comprise the Director of the Fiji Council of Social Services and the Director of the Social Welfare department.

The collection of quantitative data was conducted by sampling a representative portion of the retiree population. From this sample, specific respondents were chosen to participate in both in-depth interviews and focus group discussions. The Provident Fund provided access to the pensioner master list, which was utilized to employ a multi-stage stratified random sampling approach for the selection of respondents from various regional branch offices of the Provident Fund. A sample size of 439 participants was chosen, with 45% being female and 55% being male. A sample size equivalent to 12% of the master pensioner list provided by the Fund was taken. The data, consisting of 76% of individuals aged 60 and above, encompasses both retired individuals and elderly members of the Fijian population who receive monthly Provident fund payments.

The questionnaire underwent a pilot phase and was subsequently modified to address concerns raised by respondents regarding certain questions. The interviewers underwent a two-week training period, followed by a six-week duration for the actual data collection process. The challenge arose because of the remote geographical locations and the inherent complexities associated with locating and surveying the selected participants. The data underwent subsequent cleaning and processing using the SPSS software to generate basic frequency and cross-tabulation tables. The data obtained from the in-depth interviews and focus groups were thoroughly analyzed. Specifically, relevant information pertaining to livelihood needs and care were extracted and compared with the tabulated responses obtained from the survey data using SPSS. The researchers sought ethical approval from his Institution’s Human and Ethical Research Committee.

Analysis: Providence, Provident Fund, and Retiree Livelihood

The analysis is divided into two categories. First what I describe as structural/operational issues. These refer to the design of the organization and its service delivery functions to address pensioners primary need, that is ensuring the accurate and regular payment of pensions. These include interactions with pensioners for the miscellany of services that the Fund offers. The second is the livelihood issue and refers to the income that the pension offers and the limitations of this income in securing livelihood needs as experienced by pensioners. The Fund arrangements and monthly payments are based on actuarial calculations on pensioner contributions during working life. Given the low contributions of many retirees the Fund, through its restructuring in 2006, by decree, provides a minimum payment where the actual monthly return would be below the calculated contributions. The question for the analysis, in relation to the World Bank legitimate concern, with the challenges of averting old age crisis with livelihood in Fiji, is whether the Provident Fund payment, as an employer’s contribution for later life, is enough to contribute to averting the old age crisis in Fiji and potential poverty in old age.

Retiree Profile

By 2014 over 7,000 persons were recipients of monthly payments from their contributions with the Provident Fund (Others would have taken their total contributions in full and literally closed accounts with the Fund). This means, as noted by the Ministry of Social Welfare, just about 10% of the elderly population were recipients (Ministry of Social Welfare, Government of Fiji, 2011). From our survey, a profile of the average Provident Fund recipient emerges; the retiree had up to high school education (Figure 1), over 60 years old, married, male, unemployed, and living with at least two people in any of the towns in Fiji. As per the survey data, 76% of respondents are 60 years and over.

Retirees level of education.

The Provident Fund: Structure of Service Delivery for Pensioners

The primary service delivery function for retirees is first ascertaining their identity and second regular and efficient disbursement of monthly payments to those who have opted for such. In the different ways through which these functions are performed retirees appear to be very satisfied and welcomed the services. Over 80% of respondents registered satisfaction with the services provided either online, phone contacts, or personal visits to the respective offices of the Fund. Of these the assurance of uninterrupted monthly and timely payments rated high in satisfaction at 80%. This was followed by renewal of pension certificates at 68%. There was also high satisfaction by pensioners of the extent to which confidentiality is given to matters relating to their pensions and payments. Additionally, over 70% of respondents found the National Provident Fund to be relevant in their lives as retirees. A retired schoolteacher remarked that “without the Fund I would not know what to do after retirement.” Another noted that “the monthly checks are very important to me... I have some money every month, little but very regularly and I like that.” Another was philosophical that “life is nothing without money these days everything is for sale.” Fund personnel were also reported to be helpful and willing to assist when and where necessary. Increasingly, in both the focus groups and in-depth interviews, the efficiency of the Fund in general services for retirees and older people were applauded with an emphasis on the speed with which payments commenced at retirement.

These plaudits for the general services offered by the Fund are a far cry from the livelihood related concerns expressed by respondents to both the survey questions and at Focus group and key informant discussions. Three categories of issues dominated these responses and discussions. These are health and health needs, low income expressed as the monthly payments by the Fund, and issues with food expressed, variously, as cost and cost of living in relation to the purchasing power of retirees in the market. Together, they capture the core of what we have referred to above as livelihood and the challenges faced by older people. They also underscore the prevailing crisis of old age in Fiji. We present an analysis below taking each by turns and exploring their wider implications for livelihood.

“Providence” and Livelihood: Pensioner Concerns and Crisis of Livelihood

Chronic ailments, diseases, and disabilities have been identified as inherent features of the ageing process. Previous studies conducted on Fiji, commissioned by the World Health Organisation (WHO) in 1984, have established the findings. Subsequent analytical investigations focusing on the elderly population in Fiji, conducted by Plange (2022), have also observed a gradual deterioration in physical health as individuals age. Furthermore, K. Seniloli and Tawake (2015) have more recently corroborated these findings. Seniloli and Tawake (year) observed a notable disparity in the health status of elderly individuals residing in rural and urban areas. They found that a considerable proportion, specifically 35%, of elderly individuals in rural areas exhibited signs of poor health. Moreover, the researchers observed that prevalent health concerns among the elderly population in Fiji include visual impairment, mobility limitations, the presence of multiple chronic diseases, and reduced energy levels when engaging in activities of daily living. Furthermore, a recent study conducted by student nurses from the College of Medicine, Nursing, and Health Sciences at Fiji National University has also observed the high occurrence of non-communicable diseases (NCDs) among older individuals within a specific province. The matter pertaining to health and healthcare invariably leads to expenses associated with either preventive measures, treatment, or both. According to the Ministry of Women’s policy document in 2011, it was explicitly stated that the significant expenses incurred in providing healthcare for elderly individuals primarily stem from their increased susceptibility to chronic non-communicable diseases, which are known to be costly in terms of treatment (Ministry of Women, 2011, p. 12).

The survey results indicate that cost was the primary factor influencing respondents’ responses, and this concern was also frequently expressed in the discussions. The respondents’ remarks increasingly focused on health requirements, with a recurring emphasis on whether the Provident Fund could facilitate discounted medication purchases for elderly individuals. More than 70% of participants provided feedback regarding the financial aspect of healthcare, expressing concerns about the high cost of medical services. They emphasized the necessity of reducing healthcare expenses and suggested that the government establish agreements with pharmacies to offer discounted prices on prescribed medications or even provide free healthcare services. According to one respondent, it is imperative to establish a medical scheme that caters to the needs of elderly individuals, offering support in cases where pensioners become incapacitated and confined to bed. The following is an enumeration of the various concerns and challenges faced by retirees, which collectively encompass the risks and difficulties associated with their livelihoods.

The Fund should adopt a range of strategies to improve retirees’ welfare. One potential solution to reduce financial difficulties for the elderly is using discount cards for medications and necessities. Furthermore, the use of food coupons targeted toward retirees has the potential to enhance their economic alleviation. Additionally, it is recommended that the Fund consider distributing earnings generated from investments to pensioners, promoting a fairer allocation of payments. One crucial measure entail developing a health and medical program mainly designed for retirees to address their distinct healthcare requirements. To safeguard the financial well-being of retirees, it is advisable to regularly implement modifications to pensions that include a Cost of Living Allowance (COLA). Moreover, it is vital to engage in a thorough study of the tangible living circumstances of retirees to facilitate well-informed decision-making. In light of evolving economic environments, it is recommended that the Fund consider avenues for augmenting the minimum pension to ensure the financial well-being of retired individuals.

These comments serve as an indicator of the various difficulties faced by the majority of retirees in Fiji, encompassing health issues and other aspects related to their well-being. Nevertheless, the government has not been unaware of these concerns. The current governmental policy entails the provision of income-based targeted assistance for subsidized drugs at local pharmacies, contingent upon their availability. According to a respondent, the act of seeking drugs without relying on subsidies results in a reduction of available funds for other necessities. This poses a particular challenge for elderly individuals, who often receive small payments from the Fiji National Provident Fund (FNPF). The Figure below demonstrates that as the population ages, a larger proportion of Fund recipients consists of older retirees.

Other areas of livelihood concern expressed by the pensioners include purchasing power for food and other daily or periodic necessities. Again, over 70% of respondents repeatedly referred to the need for pension payments to be adjusted periodically to the cost of living. This is significant as the Fund pensions payment is fixed without any adjusted overtime. This means increasing pressure on purchasing power of many retirees as costs and prices escalate with time. Small wonder then that over 80% of respondents requested assistance with food and basic needs, while almost all respondents expressed concern with the cost of living and value-added tax on basic food items. It is in the light of this that almost all respondents were unanimous in their call on the Fund to share investment profits with pensioners, to reveal the nature of investments, and to revert to the higher percentage (until 1990 about 25%) of accrued contributions that was previously paid to retirees.

Embedded in the call to profit-sharing and cost of living adjustment to payments is the average low monthly receipts per retiree which, as the National Policy on Aging noted, is just at or below the formal (objective) poverty line. This means, for most retirees, the existential chances of falling into “formal” (as defined by government) poverty are real with the changes in the economy. Secondly, we take the suggestion for cost of living adjustments as an expression of subjective poverty emerging from the crisis of making ends meet. Current average monthly pension payment is at 273.43 Fijian dollars a month (FNPF, 2018). This is about FJD 68.36 per week. Compared to the recently increased national minimum hourly wage to 2.68 dollars (or average weekly earnings of 99.16) the average retirees’ monthly pension payment is 65.40% of the minimum wage. The repeated calls and protests by labor unions on the economic challenges faced by workers at this wage level are certainly equally applicable to many of Fiji’s retirees (K. Barr, 2017).

Studies in “Old Age Poverty and Health” (Adena & Myck, 2014) argued for a measure of subjective poverty as, “declarations by respondents on how easily they can make ends meet.” They concluded that if the answer is “with some” or “with great” difficulty, individuals can be classified as poor.’ On this note it is logical to conclude that majority of retirees/older people, on monthly pensions in Fiji, are poor both formally in relation to the objective definition of poverty and the subjective self-reported ability to make ends meet. The former due to average pension receipts per month, which is below the national minimum wage and the latter due to their complaints on difficulties with cost of basic needs.

Evidence from the survey data also provides two issues of relevance to potential livelihood crisis for retirees. These are the level of education and employment. The latter remains and enduring challenge for the current older people and retirees in Fiji as they have limited prospects of employment (Plange, 1994 ). Figure 2 above shows that only about 7% of retirees were formally employed at the time of the survey. Two factors account for this. The nature of the economy and level of education. The economy has undergone fluctuations but generally growing albeit slowly with employment mostly in the service and retail sectors. Secondly, the level of education of current retirees remains largely at high school level and with skills not complementary to current skill and increasingly digital demands of work and industry. The relevance of higher education and employment and income status of the elderly has been demonstrated in research undertaken by Gaiha and Imai (2004). The study concluded that “PMCE (per capita monthly consumption expenditure) is determined by the higher education status of the elderly... in all samples.” With traditional safety nets to cushion the potential effects on the wane, it is arguable that older people in Fiji on retirement payments do face an existential crisis of livelihood and poverty. The age range that receives the most FNPF benefits is 60–64 (Figure 3). In the face of this crisis increasing numbers of retirees are making requests to the government for social assistance, while others make applications for consideration of social pension inspire of their ineligibility (Conversations with Director of Social Welfare, Ministry of Women, Children and Poverty alleviation, March 7, 2018).

Employment status of retirees by level of education.

Aging of fund recipients.

Conclusion

It is apparent that retired individuals in Fiji encounter challenges pertaining to their means of subsistence, despite the financial benefits derived from the Provident Fund. Research conducted by Phipps (2003) has demonstrated that poverty has a significant influence on both health and well-being. This implies that the rising life expectancy, facilitated by advancements in medical interventions, coupled with the growing prevalence of chronic illnesses and disabilities, can result in exorbitant expenses for a significant portion of the elderly and retired population in Fiji. Consequently, this situation may present a severe threat to their overall well-being and financial stability. According to Pandey’s (2009) study conducted in India, it was observed that there is a decline in the proportion of elderly individuals living below the poverty line as their health level improves from poor to excellent. Additionally, the study found that a lower income level is a significant factor contributing to poor health among the elderly. There is currently a lack of specific research examining the impact of poverty on the health issues of the elderly population in Fiji, despite the presence of suggestive evidence in certain studies.

The endeavors undertaken in Fiji to mitigate the challenges associated with old age through livelihood initiatives are commendable, albeit with certain limitations. The introduction of government social pension in 2013 aimed to exclude individuals who already receive superannuation or other benefits, as stated by the Department of Social Welfare (2016). The monthly revenue generated by this program is relatively low, significantly lower than both the revenue from the Fund and the national minimum wage. In response to the perceived crisis, the government implemented subsidized and restricted services in the domains of healthcare and transportation.

One potential strategy for mitigating the economic ramifications of retirement and mitigating the potential crisis of poverty and financial insecurity in old age could involve implementing a policy adjustment to increase the retirement age and encourage the employment of individuals who possess the physical and mental capacity to continue working. The employment prospects for older workers in Fiji have remained unfavorable, as noted by Plange (1999), and this situation has persisted. Despite concerted efforts to secure employment opportunities, a significant proportion of individuals across various educational levels (including primary, secondary, and tertiary) continue to experience unemployment, with the figure surpassing 70%. Moreover, due to the fact that a significant proportion of the beneficiaries are located in urban regions, the customary practice of engaging in agricultural activities in rural areas to augment one’s earnings is not accessible.

The government’s efforts to ensure a satisfactory standard of living in retirement, as facilitated by the National Provident Fund, seem to be insufficient in meeting the needs of the majority of retirees. Currently, numerous individuals are experiencing significant challenges in sustaining their livelihoods due to the inflexibility of their pension payments in light of evolving family dynamics, economic fluctuations, rising expenses, and limited opportunities for employment that can supplement their subsidized pension income.

Footnotes

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.

Data Availability Statement

Data available on request from the authors.