Abstract

This study examined the causal relations among per capita CO2 emissions, per capita income, non-fossil fuels electricity production, and energy productivity for the Spanish economy (1970–2017) using structural equation modeling with quadratic effects and introducing the fundamentals of the derived demand to formulate a novel approach. The relationships revealed statistical significance with a scale effect between income per capita and the level of per capita CO2 emissions. There is also a structural effect, dominated by a higher share of non-fossil fuel electricity production, and a technical effect associated with a reduction in energy intensity due to a sustained increase in capital formation and a policy of higher energy prices in the long term. Thus, climate change policies must be based on a sustained effort to modify the energy supply, in addition to an accumulation of capital stock and a sustained policy of keeping relative energy prices, at least in the transition phase to more environment-friendly energy production.

Plain Language Summary

Purpose: To study the causal relations among per capita CO2 emissions, per capita income, non-fossil fuels electricity production, and energy productivity for the Spanish economy (1970–2017). Methods: using structural equation modeling with quadratic effects and introducing the fundamentals of the derived demand to formulate a novel approach. Conclusions: From the point of view of climate change policies, the results for the Spanish economy show that there are two opposing forces that public authorities need to consider. On the one hand, the growth of material welfare, expressed in our model by the level of per capita income, favors an increase in per capita emissions. On the other hand, it is needed an approach to promote electricity production as a primary energy source, and policies that ensure a sustained investment effort to move toward a growing and less polluting capital stock Implications: policies to combat climate change should be based on that pillars, which requires substantial funding. In this respect, a financing policy along the lines of the EU’s Next Generation Funds looks appropriate, and an effective policy to combat climate change requires, at least in the transition phase, a reduction in energy intensity, which would have its touchstone in relative prices Limitations: It is not clear the role of relative energy prices using this methodology in the short run.

Introduction

The need to combat climate change has led to an expanding integration of climate and energy policies in recent years, giving rise to energy transition or ecological transition policies. In many countries, medium- and long-term plans have been designed and implemented to simultaneously achieve objectives in both areas. Within the European Union (EU), Integrated National Energy and Climate Plans have been developed for 2021 to 2030 based on the so-called European Green Pact of 2019, which has a public action horizon until 2050.

In the case of Spain, for example, one of the largest four EU economies, some results in recent years suggest that, as a result of the implementation of these plans, there has been a certain decoupling between GDP evolution and CO2 emissions (https://energia.gob.es/balances/Balances/LibrosEnergia/libro-energia-espana-2019.pdf), even allowing for GDP growth of 2% in 2019 and a fall in CO2 emissions of 5.6% year-on-year.

However, the nature of this decoupling is debatable since final energy consumption in Spain declined in 2019 by about 2% year-on-year. In this sense, the decoupling could be considered an increasingly less energy-intensive economic growth, indirectly affecting the volume of CO2 emissions.

In this sense, a sustained policy of high energy prices that reduces energy consumption, in the long run, would not be the same as a policy of substituting subsidized production technologies that essentially eliminate the effect on energy prices. Both produce an emission reduction effect, but the latter will likely not affect energy demand. At the same time, the former reduces the amount of energy demanded with a technology mix that does not vary in terms of pollution intensity.

Observation of these results raises questions about the relationships between essential variables such as income, energy demand, technology, prices, and GHG emissions. The present research aims to test the nature of these relationships, in the conviction that there is no study of this nature for the case of Spain and that its results could serve as a guide for examination in other countries. In any case, it is difficult to assume the consistency of an energy transition policy that ignores the nature of these relationships or the role of some of the most critical variables.

This research proposes a well-founded structural relationship that can facilitate the correct articulation between instruments and objectives of energy transition policies and, primarily, determine the appropriate policy instruments for this purpose. Based on the 2015 Paris Agreement, the design proposed by the UNFCCC (2015) about each country’s contribution to an effective fight against climate change is based on the different emission drivers proposed by the Kaya identity (see https://unfccc.int/sites/default/files/2.4_cicero_peters.pdf). More specifically, Kaya’s identity (Kaya, 1989) taught us that CO2 emissions could be expressed as a combination of emission drivers, population, per capita income, energy intensity, and pollution intensity (or technology).

It is true that the Kaya identity, as an accounting equation, does not allow us to see the underlying causalities between factors and ignores non-proportional effects between individual factors (AguirBargaoui et al., 2014). However, as Wang et al. (2011) have shown, a decomposition of these factors as functions of independent variables would serve as explanatory variables leaving CO2 emissions as the dependent variable.

To this end, this research proposes, through a system of structural equations, a novel approach to the energy intensity concept based on the knowledge provided by economic theory, employing the concept of the derived energy demand function. The derived energy demand function allows it to incorporate energy prices and capital stock as explanatory variables for energy transition policies. Furthermore, decomposing the identity factors, we find that non-fossil fuels electricity production (not total electricity production) is an interesting proxy variable for the economy’s pollution intensity, insofar as electricity as primary energy can only be produced with non-fossil energy sources (renewable or not). Furthermore, quadratic formulae are introduced in the developed model, which helps better explain the non-monotonic or non-linear variations in the established relationships, thus overcoming another primary problem while using Kaya’s identity directly.

Finally, an analysis approached this way forces research focused on a national economic reality since the model based on Kaya’s identity is a national model. This is a limitation, as it omits international energy flows and cross-border effects from the analysis. However, it allows for a more detailed analysis of national realities and for targeting more effective energy transition policies.

The system of structural equations is applied to the Spanish economy for the period 1970 to 2017, and the results are precise. It is possible to maintain the Environmental Kuznets Curve (EKC) hypothesis that per capita CO2 emissions do not start to reduce per se from a given level of per capita income.

This brake is applied on per capita CO2 emissions because the economy has been subjected, through energy policy, to a process of substitution in the energy mix, accompanied by policies of capital accumulation and of long-term energy prices favoring continuous gains in energy productivity and, in the case of Spain, having a more substantial impact on the reduction of per capita GHG emissions than the increase in emissions caused by the growth of per capita income.

Literature Review

There is a long tradition in the development economics literature relating energy demand to economic growth. This literature has been evolving since the seminal work by Kraft and Kraft (1978), which claimed the one-way causality of economic growth to energy consumption, spurring a long list of studies on these characteristics (Ghali & El-Sakka, 2004) until one of the last works (Liddle & Huntington, 2020), where they assemble a comprehensive panel dataset with 37 OECD countries and 41 non-OECD countries and conclude that “the GDP elasticity of energy varied substantially from country to country” and they did not find “evidence that the elasticity varied systematically according to GDP per capita/level of development.”

Nevertheless, with the obvious global problems of climate change and a different definition of economic development, now sustainable development (WCED, 1987), concern is more on the relationships between income and the level of pollutant emissions, with a particular interest in many cases in contrast to the so-called EKC hypothesis, which proposes an economic growth that is initially very intensive in terms of polluting emissions, but which is tempered as countries’ per capita income increases.

In this respect, the seminal proposal by Grossman and Krueger (1995) confirmed this hypothesis, using a flexible function in a reduced form for their assessment, and identified a “peak” in pollution (for different pollutants) relative to per capita income. Discussing the possibility of monotonic increases in variables, such as atmospheric pollution, they claimed that “ nothing [is] inevitable” in the long term. Other scholars (e.g., Narayan & Smyth, 2005) advocated the same causal direction in the long term, albeit at much weaker levels in the short term. Waslekar (2014) considered that the EKC hypothesis has been fulfilled and that a global EKC will exceed the maximum of the inverted U before 2050. However, the result has not always been so straightforward. For example, an alternative line of research found that causality between pollution and per capita income does not exist in some countries and areas (e.g., Dinda & Coondoo, 2006). Based on a model similar to that of Grossman and Krueger, using emissions by carbon footprint for a sample of 40 countries, Pablo-Romero and Sánchez-Braza (2017) pointed out that the EKC hypothesis is not fulfilled, finding notable differences in the elasticities calculated for each country.

Therefore, even if the EKC hypothesis can be accepted, it is unclear whether per capita income growth can reduce pollutant emissions as the only explanatory variable. What is striking in this case is that no transition policy would have to be implemented since per capita income growth would generate the ecological transition by itself. In any case, these studies use very reductionist models that are far removed from an excellent theoretical basis, and the possible conclusions contradict the worsening of the problem.

The research shows this critical point by Itkonen (2012), where using a transformation of a regressor as a regressor in a VAR model concludes that when energy demand depends on output, the result gives us an “overly optimistic view of the possibility of achieving climate policy goals simply through economic growth […] before turning, output increases emissions faster.”

Other studies have questioned the direction of the causal relationships between GHG emissions and growth, even observing different short- and long-term results. Thus, Pao and Tsai (2010), using data on BRIC countries between 1971 and 2005, found a one-way causality from emissions to output in the long term. Wang et al. (2011), using panel data for 28 Chinese provinces, further pointed out that emission reduction policies affect Chinese economic growth, and the relation between economic growth and emissions has the form of a U and exhibits bidirectional causal in the short term. Barassi and Spagnolo (2012) modeled a VAR-GARCH from 1870 to 2005 and observed causal bidirectionality and an effect of economic growth per capita on emissions per capita. Although these results may be very consistent from a statistical point of view, the truth is that they suffer from the same problem as those that follow reductionist approaches, far removed from more consistent theoretical foundations. In any case, it does not seem reasonable to assume a bidirectional or inverse causality with the byproduct or waste that is always the result of economic activity.

Other research has preferred directly studying the causal relationships between economic growth and energy consumption since GHG pollutant emissions are still a byproduct of energy use. In this sense evidence has been mounting regarding bilateral causality and interdependence between growth and energy consumption, as provided by Pedroni (2000), Paul and Bhattacharya (2004) for India, and Apergis and Payne (2012). Acaravci and Ozturk (2010), using a sample of 19 European countries, failed to generalize causal relations and their directions in the short- and long-term.

In short, a general concern on the causal direction of the relations between output, energy, and pollution can be inferred. However, the use of autoregressive models or the lack of a common theoretical foundation somewhat weakens it. Meanwhile, econometric complexity and multiple attempts to cover large samples of countries and variables have been added, with techniques such as panel data, to determine patterns. Somehow, and with better theoretical foundations in general, it only sows doubts, due to the bicausality or absence of causality, as to which variables (instruments) should favor an energy transition policy.

Most of these works have been criticized for econometric reasons based on the stationarity or biases of omitted variables. In this respect, other studies overcome these issues in a more satisfactory manner. One way is the use of a multivariate approach, in which long-term causality à la Granger is sought, using techniques such as that of Toda and Yamamoto from 1995 and generalized forecast error variance decompositions, either for a country (Soytas et al., 2007) or a group of countries (Sari & Soytas, 2009). One finding of these methods is that energy consumption causes CO2 emissions and not vice versa, at least in the case of the USA (Soytas et al., 2007).

Therefore, energy or ecological transition policy, which aims to minimize GHG emissions, must be based on a coherent energy policy. However, assuming this causality and its meaning, to implement it, these studies do not attempt to seek what the essential components of the energy policy would be. In other words, the models lack a more significant decomposition that would make it possible to determine the most effective instrumental variables of the potentially influencing policy. In this regard, one interesting contribution by Liddle and Sadorsky (2017) is that they propose a model to explain how non-fossil fuels replace fossil fuels in the OECD environment.

Another empirically relevant issue is the geographical or political dimension that must be factored in. More specifically, energy transition policies may depend on economic variables that evolve differently in each country, where different effects of scale, structural or technological change appear. As summarized by Bo (2011) there is a general acceptance that the income elasticity of the demand for environmental quality can help correct environmental excesses while highlighting the existence of scale, structural, and technical effects.

From this perspective and emphasizing a national approach to the problem, Ang (2007) studied the case of France from 1960 to 2000 with a model relating per capita GHG emissions to energy demand and output growth in its linear and quadratic forms, following Antweiler et al. (2001) and Coxhead (2003), with a VAR model and Johansen (1988) tests or Auto Regressive Distributed Lags by Pesaran et al. (2001). One conclusion is that the scale effect dominates initially, at least in France. However, later, composition (from structural change) and technology effects end up dominating the scale effect, confirming the EKC hypothesis and a one-way causality of economic growth: growth in energy consumption and CO2 emissions in the long term, and reverse causality in the short term.

With the same sort of results, using the Greek economy for the period 1977 to 2007 as a case, Hatzigeorgiou et al. (2011) highlighted a long-term causality that goes from GDP to energy intensity, as well as another that goes from GDP to CO2 emissions, in addition to a two-way causality between the energy intensity and CO2 emissions.

These exciting findings provide a glimpse of the importance of the short-term rigidity of the production structure and energy markets and, to that extent, the limited possibilities for manipulating GHG levels, if not at the cost of reducing economic activity. They also highlight the importance of capital stock as a variable mediating between economic activity and energy uses and its polluting byproducts, which is considered fixed (rigid) in the short term. So, variations in polluting emissions may affect energy consumption and economic activity.

Although the analyses cited by Ang (2007) and Hatzigeorgiou et al. (2011) are conclusive and start from a table of relationships in the EKC tradition and are in line with Kaya’s identity at the national level, they do not go into the variables that make it possible to modify the relationships between energy consumption or output and GHG emissions. Therefore, the present research assumed that the relations between pollution emissions, energy, and economic growth would require a more significant theoretical foundation. The flexible and reduced functional form, used since Grossman and Krueger (1995), and which relies on the value of income raised to the nth power, must be formulated differently.

We considered the necessity of addressing an empiricist approach, such as the EKC, but aimed more to posit, using a system of structural equations (Sarstedt et al., 2017; Wold and Andreas, 1975), variables that have not always been satisfactorily taken into account—especially those referring to the composition of energy demand by source and its relation to pollution.

We also considered energy intensity as a version of energy productivity (and vice versa). Notably, we took as a promising starting point, the Marshallian idea of energy demand as a derived demand (Berndt & Wood, 1975). This point of view revealed the effect on the energy demand of the capital stock with which it is consumed. We further recognized that real income and relative prices would influence the aggregate energy demand in the short and long term. Therefore, we sought a consistent explanation for the scale, structural, and technical effects by proposing a non-linear structural equations system that could better describe actual behavior. Following the country analysis by Ang (2007), we focused on Spain from 1970 to 2017, given that the national stamp has prevailed in economic growth strategies, productive specialization, and energy policies.

Materials and Methods

From an aggregate point of view, our proposal will look for a relationship between economic activity and pollution. Our starting point is to assume that the level of CO2 emissions per capita is a function of the level of income per capita, energy intensity (energy demand/GDP), and polluting intensity (emissions of CO2/energy demand) of the economy, supported for instance by the practical and well-known Kaya’s Identity (Kaya, 1989).

Thus, energy and pollution intensity have energy demand as a common element. The demand function, according to Deaton and Muellbauer (1980) and following Stone and Richard’s (1954) initial approaches, in Hicksian or compensated terms, is one that relates a dependent variable, which is the quantity demanded of a good, to actual spending and the relative price of the good (or deflated price, if compared with the rest of the goods in the economy). However, these demand models are intended for final goods, not intermediate goods like energy. Energy demand must be expressed as a function of derived demand (Marshall, 1938 [1890], p. 381). In other words, in the provision of a service, energy is jointly demanded with capital or a durable consumer good. Thus, the demand for energy in the economy must also be stated in terms of capital stock.

Meanwhile, the level of a byproduct generated by economic activity, such as pollution, depends partly on the types of energy used. Thus, if non-fossil fuels electricity production is considered a non-polluting primary energy source (only renewable sources of energy and nuclear power are regarded as non-fossil fuels electricity production) in terms of GHG (although only in contrast to CO2), its weight in the mix of the primary energy demand would indicate the resulting level of emissions and be among the explanatory variables, as a proxy variable, of the level of CO2 emissions per capita.

Thus, regarding the energy demand function in the economy, we formulated a system of non-linear structural equations in which the level of CO2 emissions per capita is a function of per capita income (first hypothesis), energy intensity (second hypothesis), and pollution intensity (third hypothesis).

As it has been formulated above, to the extent that energy intensity is an expression of energy demand, we formulated a supplementary equation in which energy intensity depends on the income, the capital stock of the economy (fourth hypothesis), and relative energy prices (fifth hypothesis). Moreover, the pollution intensity is a function of the weight of non-fossil fuels electricity production has in the energy demand mix. In this sense, it also had to be considered (reiteration of the third hypothesis). Therefore, we posited the following model (Structural Equation Model 1 and Figure 1):

Energy intensity, energy prices, per capita CO2, per capita income, and capital stock (Base 1970 Index = 100).

Subsequently, we used the data pertaining to the Spanish economy. We obtained a series of data on the GDP and population from the official statistics of the Instituto Nacional de Estadística for the period 1970 to 2017 (www.ine.es). 1 The data referring to energy consumption, energy prices, and CO2 emissions for the same period were obtained from the official annual publication of the old Ministry of Industry and Energy of Spain and the Libro de la Energía en España (https://energia.gob.es/balances/Balances/LibrosEnergia/). We elaborated the relative energy price index by considering the price of each primary energy source (annual average price), weighted by the weight of each of the energies in primary consumption, according to official statistics. This energy price index was deflated by ‘Spain’s official consumer price index. For the series data on capital stock, we used the data published by the Instituto Valenciano de Investigaciones Económicas (https://www.fbbva.es/microsites/stock09/fbbva_stock08_i32.html).

Figure 1 provides a descriptive representation in the form of an index base of 100 in 1970. The value of energy intensity was relatively stable until 2003 when it began to fall amid increases in the relative prices of energy. Spain’s maximum per capita CO2 emissions were in 2005, or before the global financial crisis of 2007 to 2008. The capital stock curve followed an increasing path until it flattened in 2008 and began to recover in 2013. The data could be interpreted to reflect some relation between the level of emissions per capita in Spain and energy intensity, which the evolution of GDP per capita would partially annul. Moreover, energy intensity may be conditioned by the capital stock and relative energy prices, which would affect the levels of per capita CO2 emissions.

Grounded on the previous theory and based on the proposed structural model, we posited the following hypotheses:

H1: Per capita income positively influences per capita CO2 emissions.

H2: Non-fossil fuels electricity consumption negatively influences per capita CO2 emissions.

consumption (inverse pollution intensity proxy variable) negatively influences per capita CO2 emissions.

H3: Energy intensity (inverse of energy productivity) positively influences per capita CO2 emissions.

H4: Energy intensity is negatively influenced by capital stock.

H5: Energy intensity is positively influenced by income level.

H6: Energy prices negatively impact energy intensity.

Empirical Results

To test these hypotheses, we estimated the model using the partial least squares (PLS) method, a causal-predictive approach (Sarstedt et al., 2017; Wold and Andreas, 1975). We used the estimation software SmartPLS 3 (Ringle et al., 2015).

Our model consisted of two sub-models: a formative measurement model, whose variables, in this case, are measured by a single item (Hair et al., 2014), and a structural one. We estimated the structural model parameters utilizing 5,000 subsamples of bias-corrected bootstrapping (Chin, 1998; Hair et al., 2017). The sample size was 48, corresponding to the 1970 to 2017 period. Next, we analyzed the measurement and then the structural models. As the variables were not latent and non-composed but measured by a single item, the traditional quality indexes (convergent validity, indicator collinearity, statistical significance, and relevance of indicator weights) for latent variables did not apply. Figure 2 presents the structural model schematically.

Structural model schematic diagram. Beta values and (p-values) on arrows.

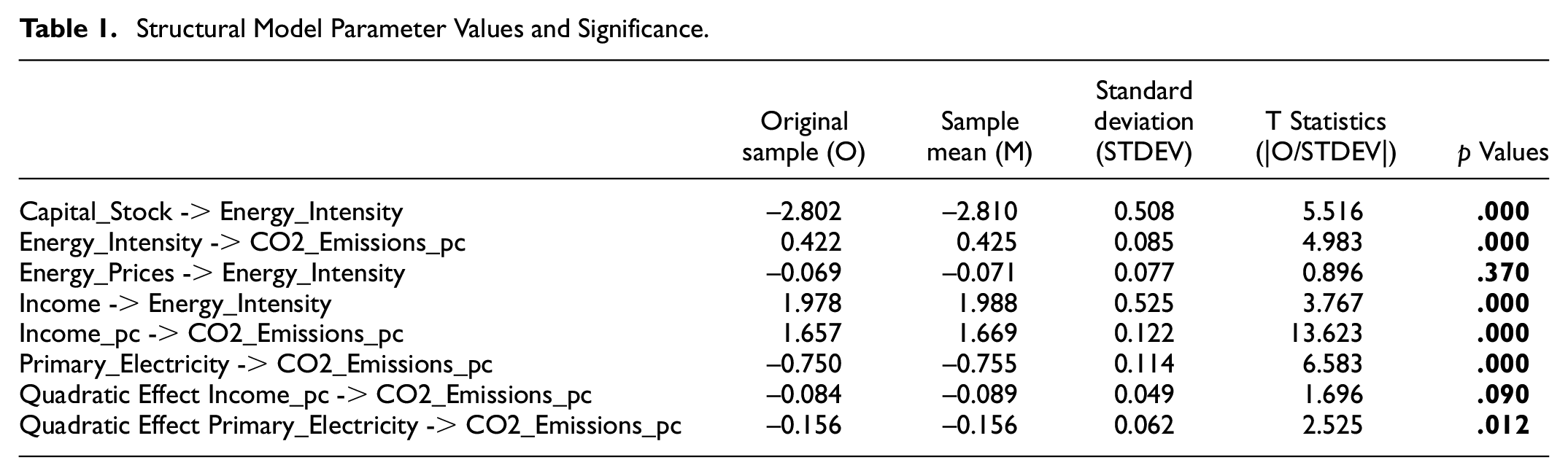

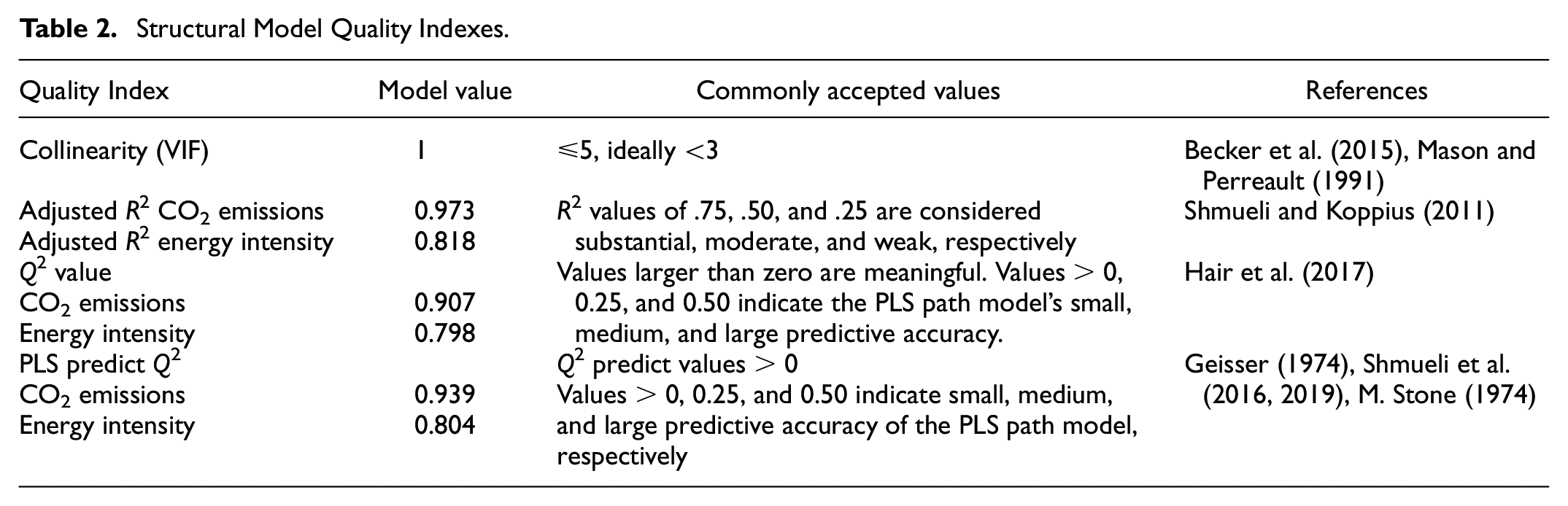

Next, we assessed the structural model following the standard assessment criteria: coefficient of determination (R2), blindfolding predictive accuracy Q2, statistical significance and relevance collinearity of path coefficients, and model predictive power (Shmueli et al., 2016). The results, summarized in Tables 1 and 2, showed that the proposed model fulfilled all the commonly required quality indexes.

Structural Model Parameter Values and Significance.

Structural Model Quality Indexes.

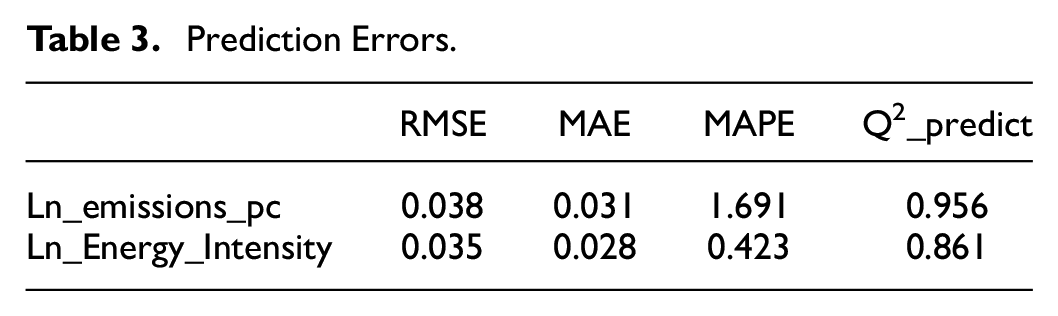

We then prepared classical quality indexes for the structural model: the adjusted coefficient of determination (R2), blindfolding-based cross-validated redundancy measure Q2, and statistical significance and relevance of the path coefficients. We also assessed the ’model’s out-of-sample predictive power using the “PLS predict” method (Shmueli et al., 2016, 2019). Given the macroeconomic policy implications of our conclusions, we presented the prediction errors in Table 3. All of the index values complied with the requirements in the literature.

Prediction Errors.

Discussion

This study has aimed to verify if the hypotheses derived from introducing a derived demand function in an explanatory model of per capita CO2 emissions level would be compatible with the causality implied by the function itself. In this sense, the results could not have been more evident.

In a radical difference from previous research (e.g., Dinda & Coondoo, 2006), our results (Table 1) showed that the level of per capita CO2 emissions depended strongly and positively on the level of per capita income (H1). Thus, the higher the per capita income, the higher the level of per capita emissions. Introducing a quadratic relation between these variables was significant at a low level (more than 90% but less than 95%), compared to the linear one. To an extent, the scale effect entailed by this relation, although measured in per capita terms, would show that a higher basket of goods and services produced per person relates to a higher level of pollution per capita, all other things being equal. In this way, our results confirmed previous findings, such as those of Soytas et al. (2007). In terms of policy, we expect countries with a higher per capita GDP to show a more complex way to control emissions or a comparatively more substantial effort to do it. These results are in line with Hatzigeorgiou et al. (2011). However, with results similar to those of Grossman and Krueger (1995) in their seminal work, the negative sign in the quadratic relationship between per capita income and per capita CO2 emissions guides national policymakers on controlling emissions when the country reaches a certain per capita income. Even though, as Itkonen (2012) showed, the turning point occurs later than expected, and before turning, output increases emissions faster, giving an “overly optimistic view.”

To avoid this bias, our results highlight three different aspects of the scale effect, which will be essential to address the CO2 policy in Spain, in line with Ang’s (2007) results. In our case, using elasticities of energy intensity is essential with a derived demand for energy. The first of these effects is the composition of primary energy sources. From this perspective, and according to Díaz et al. (2019), the proposed model showed that pollutant intensity is a growth factor in per capita emissions that can be contained by an energy production process capable of replacing fossil-based energy sources. In our case study, there is a linear and significant negative relationship between the weight of non-fossil fuels electricity production in the energy consumption mix and the level de per capita CO2 (H2). These results are fundamentally in line with the strong results by Liddle and Sadorsky (2017), who noted in their model the high value of long-run displacement elasticities between electricity produced from non-fossil sources and the level of emissions per capita. Then, policymakers must introduce incentives for an energy supply with more non-fossil fuel electricity production. Thus, the increasing weight of non-fossil fuels electricity production in the primary energy mix, as a non-polluting source of GHGs, is a factor that can reduce the scale effect. Besides, the results clearly show a negative and significant quadratic relationship between non-fossil fuels electricity production and per capita CO2, indicating that policies addressed to this goal will give the best results in the long run.

Moreover, according to our results, there are two distinct effects in addition to the initial scale effect, both coming from a reduction in per capita CO2 emissions based on a reduction in energy intensity (H3), equivalent to an increase in energy productivity, showing a negative sign in this result and the unchallenged statistical significance. One of the most critical findings of our study is the usage of the concept of derived demand for energy which is an infallible response about the main variables (income, energy prices, and capital stock) and the statistical significance of the relations among these variables to any policymaker’s question on how to reduce energy intensity. Related to income, the result is clear: the higher the income of the country, the higher the energy intensity (H5). In this sense, this result reinforces the idea that per capita income favors an increase in per capita emissions since income now favors energy intensity, and an increase in energy intensity favors an increase in per capita emissions.

Our results show that the relationship between capital stock and energy intensity is negative and statistically significant (H4). In this sense, we found a second effect showing that the growth of capital stock could incorporate dynamic improvements in energy productivity in the case of the Spanish economy, evincing not only the relevance of studying one country with its particularities but also the importance of a policy based on maintenance or increase of investment involving a process of capitalization and substitution of productive capital stock related to the most polluting production.

Finally, even though the results show a low statistical significance, there is unambiguously a third effect derived from our approach to the problem showing that relative energy prices could be an efficient signal of the shift toward a reduction in energy intensity and, through it, a reduction in per capita CO2 emissions (H6). This result is consistent, although less robust, with the empirical evidence of Parker and Liddle (2016) and Azhgaliyeva et al. (2020) on the price effect and its instrument in energy efficiency and pollutant emissions reduction policies. This last finding means that it is necessary to formulate a high relative energy prices policy to decrease the level of energy intensity and the resulting reduction in per capita emissions.

Conclusions

The Spanish economy of the past five decades demonstrated the precise incidence of the level of per capita pollution from the accumulation of capital stock and a policy of substitution of polluting primary energy sources, reinforced by the incentive of a policy of relative energy prices. The level of per capita income dictates, above all, the level of per capita emissions.

From the point of view of climate change policies, the results for the Spanish economy show that there are two opposing forces that public authorities need to consider. On the one hand, the growth of material welfare, expressed in our model by the level of per capita income, favors an increase in per capita emissions. However, this is a limitation for policymakers because policies based on economic stagnation do not seem reasonable, as the United Nations was able to realize in its 1987 proposal Our Common Future and its definition of sustainable development.

On the other hand, our results show that policies to combat climate change should be based on three pillars: an approach to promote electricity production as a primary energy source. Non-fossil fuels electricity production means production from sources such as wind, water, or the sun, but also nuclear energy. In this respect, strategies such as the one implemented by the EU through the European Green Pact, in which the concept of electrification of the economy based on green primary production (renewable and nuclear) plays a central role, seem very timely.

A second axis points to policies that ensure a sustained investment effort to move toward a growing and less polluting capital stock, which requires substantial funding. In this respect, a financing policy along the lines of the EU’s Next Generation Funds looks appropriate.

Finally, the sign of relative scarcity prices and, more specifically, relative prices is relevant in market economies. In this sense, research has remained relatively limited. However, it suggests that an effective policy to combat climate change requires, at least in the transition phase, a reduction in energy intensity, which would have its touchstone in relative prices that do not show signs of falling, either through taxes or through administrative penalties for production employing polluting energies.

Footnotes

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.

Data Availability Statement

Data sharing not applicable to this article as no datasets were generated during the current study