Abstract

Corporate strategic deviance plays an essential role in the survival and development of enterprises; however, does it have the same impact on all types of goals (corporate growth and corporate profit)? Using Chinese listed companies from 2010 to 2018, we address this question by examining the influence of corporate strategic deviance on corporate growth and corporate profit. The results show that corporate strategic deviance has a positive effect on corporate growth; the institutional environment strengthens the positive relationship between corporate strategic deviance and corporate growth; the relationship between corporate strategic deviance and corporate profit is a U-shaped function; and the U-shaped relationship between corporate strategic deviance and corporate profit becomes weaker when companies in developed institutional environments. Our research moves beyond the debate about whether corporate strategic deviance increases or decreases corporate performance by analyzing the effect of corporate strategic deviance on different corporate goals in China, the results are helpful to understand the inconsistent conclusions of existing research. In addition, our study enriches the situational theory of corporate strategic deviance that affects corporate growth and profit by introducing the institutional environment as a moderating variable.

Plain Language Summary

Using Chinese listed firms between 2010 and 2018 as research sample, this study examines the relationship between corporate strategic deviance and corporate performance (corporate growth and corporate profit) and analyzes the moderating effects of the institutional environment on those relationships. The results are as follows: first, corporate strategic deviance has a positive effect on corporate growth; second, there is a U-shaped relationship between corporate strategic deviance and corporate profit; third, the institutional environment has a positive moderating effect on the relationship between corporate strategic deviance and corporate growth; finally, the institutional environment has a negative moderating effect on the relationship between corporate strategic deviance and corporate profit, that is, the U-shaped relationship between corporate strategic deviance and corporate profit in developed institutional environments will become gentle. Our research moves beyond the debate about whether corporate strategic deviance increases or decreases corporate performance by analyzing the effect of corporate strategic deviance on different corporate goals in China, the results are helpful to understand the inconsistent conclusions of existing research. In addition, our study enriches the situational theory of corporate strategic deviance that affects corporate growth and profit by introducing the institutional environment as a moderating variable.

Introduction

Although corporate growth and corporate profit are relevant to companies in any economy, balancing these goals is especially important for companies in emerging markets (Chandra et al., 2022; S. H. Park et al., 2013). Growth is beneficial for corporates to attract external resources and gain competitive advantages (Chen et al., 2009; Haveman, 1993); profit is crucial to business operation (Purbawangsa et al., 2019), just as existing research found that the only task of enterprises (especially enterprises in emerging markets) is to obtain profits. Companies in emerging markets need to grow rapidly (Chen et al., 2009); at the same time, they need to generate sufficient financial returns to maintain and enhance their competitiveness because the capital market is underdeveloped (Levinthal & Wu, 2010). Therefore, both growth and profit are critical for companies in emerging markets. However, corporate growth and corporate profit are two different goals; corporate growth is not always consistent with profit maximization (Bardolet et al., 2017; Cho & Pucik, 2005; Dow & Baumol, 1960). In fact, there is an inherent tension between pursuing growth and profit, especially when resources are scarce (K. Park, 2011). Corporate growth requires scale expansion or revenue increase; but profit maximization requires enterprise sales growth at the best level, that is, the marginal revenue obtained by sales units equals marginal cost. Companies generally follow a sequential approach: pursuing growth or profit. However, limited resources and a rapidly changing environment need companies in emerging markets to strive for both.

Strategy plays a guiding role in enterprise development. Corporate strategic deviance reflects the degree of deviation between a corporate’s strategy and the industry mainstream strategy (Carpenter, 2000; Tang et al., 2011). Existing studies have discussed the effects of corporate strategic deviance on various aspects of firms, such as earnings management (J. Sun et al., 2016), stock price crash risk (Habib & Hasan, 2017), annua report readability (Lim et al., 2018), information environment (Bentley-Goode et al., 2019), cash holdings (Dong, Chan, Cui, & Guan, 2021) and auditor selection (Dong, Cui, & Gao, 2021). These researches mainly focus on the role of corporate strategic deviance in the accounting field, and there is still a lack of discussion on the influence of corporate strategic deviance on corporate performance; more importantly, the conclusions of existing studies on corporate strategic deviance and corporate performance are inconsistent (the findings are both positive and negative) (Bao et al., 2014; Goll et al., 2007; Shrader & Simon, 1997; Z. Wang et al., 2021), this provides research opportunities for us. Corporate performance can be subdivided into corporate growth and profit, which are two completely different goals; the diversity of corporate goals determines strategic deviance can affect more than one corporate goal simultaneously. Our study highlights the difference between corporate growth and corporate profit and proposes that corporate strategic deviance has different effects on them.

In addition, this study addresses the moderating effect of the institutional environment between corporate strategic deviance and corporate goals (corporate growth and corporate profit). Strategic research has increasingly focused on the impact of institutions and proposes that strategies have different effects on corporate goals in different institutional environments (Ahuja & Yayavaram, 2011; Gao et al., 2017; R. Li & Ramanathan, 2020; Marquis & Raynard, 2015). The institution-based view suggests that corporate strategy could be affected not only by industry and enterprise factors but also by institutional factors (Peng, 2002).Institutional environment refers to the quality of local institutions, it is not consistent among provinces in China (S. Han et al., 2021; Xie, 2017). The local governments have an essential influence on economic activities and business decisions in less institutionally developed provinces; however, in more institutionally developed provinces, the local governments refrain from interfering in economic activities to keep the market-determining business activities. Considering the important impact of institutions (S. Han et al., 2021; Peng, 2002; X. Wang et al., 2017; Xie, 2017), our research believes that the institutional environment may affect the relationship between corporate strategic deviance and corporate goals (corporate growth and corporate profit).

This study intends to contribute to the strategy research in two aspects. First, our study contributes to corporate strategic deviance by empirically examining its influence on different goals (corporate growth and corporate profit). Although existing studies have documented the effects of corporate strategic deviance on corporate performance (Bao et al., 2014; Goll et al., 2007; Shrader & Simon, 1997; Z. Wang et al., 2021), the results are mixed, and they cannot provide adequate explanations for these inconsistent findings. Our study highlights the difference between corporate growth and corporate profit and finds that corporate strategic deviance could promote corporate growth and there is a non-linear relationship between corporate strategic deviance and corporate profit, this resolves the conflicts among existing studies. Second, we emphasize the moderating effect of the institutional environment on the relationship between corporate strategic deviance and corporate goals in emerging markets. The institution-based view has attracted increasing attention in recent years (Gedajlovic et al., 2012; Hornstein & Zhao, 2018; Y. Li et al., 2023; Peng et al., 2008; Yang et al., 2020), scholars are interested in how firms (particularly in emerging markets) respond to the changing institutional environment (Banalieva et al., 2015; Durand et al., 2019; H. Kim et al., 2010; Uchida, 2023). The interaction of corporate strategy with institutions is a complex process that can influence corporate goals; this could help us further understand the contingency of strategic deviance and corporate goals (corporate growth and corporate profit).

The remainder of our article proceeds as follows: section 2 develops four hypotheses on the effects of strategic deviance and corporate goals (corporate growth and corporate profit) and the moderating effects of the institutional environment; section 3 describes the data, variables, and model definition; section 4 reports the empirical results; section 5 discusses the conclusions, implications, and directions for future research.

Hypothesis Development

Corporate Strategic Deviance and Corporate Growth

Strategy plays an essential role in the survival and development of enterprises (Sirmon & Hitt, 2009), a main difference between high-growth firms and non-growth firms is strategy (W. C. Kim & Mauborgne, 1997), it may lead to slow growth or even recession when strategy is not ideal. There is an industry mainstream strategy due to industry regulations, planning opinions, and imitations (DiMaggio & Powell, 1983; Meyer & Rowan, 1977). If enterprises’ strategies are inconsistent with industry mainstream strategies, they face high risks (such as the impairment of legitimacy) but little competitive pressure; they could obtain leading positions (Navis & Glynn, 2011; Powell & DiMaggio, 2012).

We believe that corporate strategic deviance can promote corporate growth due to two reasons. One, enterprises could attract more investors’ attention and support with strategic deviance increases (Cuellar & Gertler, 2006). Mainstream strategies usually constrain performance; corporates consistent with industry mainstream strategies cannot attract investors’ attention, resulting in financing difficulties. However, corporations present uniqueness with strategic deviance increases; investors may give more attention and support, just as the resource-based view pointed out that uniqueness rather than imitation provides competitive advantages for enterprises to obtain resources (Litov et al., 2012). Although enterprises with high strategic deviance face high management costs, transaction costs, and institutional costs, which may increase the uncertainty of cash flow, existing studies found that the uncertainty of cash flow caused by strategic deviance can promote R&D investment and corporate value (Cui et al., 2019).

Two, competitive pressures decrease with strategic deviance increases, and corporates have more opportunities to obtain leading positions. Competition is the comprehensive result of the average distance between a firm and its competitors and the number of competitors in the resource space (Baum & Mezias, 1992). Enterprises in the same industry have similar strategies due to constraint and cluster; enterprises cluster around industry mainstream strategies have prominent characteristics in organizational structures and behaviors (Navis & Glynn, 2011; Zuckerman, 1999), and these companies are highly similar. While a corporation whose strategy is consistent with the industry mainstream strategy has legitimacy, it faces competition in resource, market, and customer (McNamara et al., 2003), as the five forces model pointed out that the bargaining power of suppliers, the bargaining power of buyers, the threats of new entrants, the substitutes and the rivalry determine competition intensity and attraction intensity. A corporation’s strategy that is inconsistent with the industry mainstream strategy can increase the distance between it and other competitors and put itself in a place where competition is insufficient (Porter, 1991); it could be away from the central trend and competition (Porac et al., 1995). Corporates’ competitive pressures decrease with strategic deviance increases, and corporates could grow fast and obtain leading positions. Therefore, corporate strategic deviance can promote corporate growth from a competitive perspective.

Based on these two reasons, we predict that corporate strategic deviance has a positive effect on corporate growth. Specifically, strategic deviance is beneficial for enterprises to obtain stakeholders’ attention and support and reduce competitive pressures. Therefore, we propose that:

Corporate Strategic Deviance and Corporate Profit

Corporate strategic deviance influences corporate profit through two mechanisms: On the one hand, enterprises face high costs with strategic deviance increases which may hurt profit; on the other hand, enterprises’ competitive pressures decrease with strategic deviance increases, which increases market share and customer loyalty, ultimately, promotes corporate profit. Hence, we propose a new theoretical framework based on these two perspectives and expect that there is a curvilinear U-shaped relationship between corporate strategic deviance and corporate profit.

We argue that the disadvantages outweigh the competitive advantages when strategic deviance is low to moderate, leading to negative influences on corporate profit. First, enterprises with high strategic deviance cannot directly use experience and channels from other corporations in the same industry, so they have high management costs. This is because of efficiency decline (productivity decline and learning efficiency decline) due to resource use differences and exploration cost increase (Hou et al., 2020). Second, companies with high strategic deviance are not conducive to cooperating with partners, which increases transaction costs. Enterprises with prominent characteristics in a rapidly changing environment are more accessible to be recognized, individuals are bounded rational due to limited information and knowledge, existing studies showed that partners do not have a comprehensive understanding of enterprises, and they tend to choose enterprises that are typical in strategy (Duan & Jin, 2014). Enterprises with high strategic deviance need more explanations to gain cooperation; this increases enterprises’ transaction costs, just as the existing research found that enterprises’ cost equity capital increases with strategic deviance increases (H. Wang et al., 2017). Third, corporates with high strategic deviance need more explanations and coordination to prove they are legitimate, which increases institutional costs (DiMaggio & Powell, 1983). Institutional theory holds that legitimacy is essential to business operations (S. L. Sun et al., 2017); a firm with high strategic deviance could face serious legitimacy threatened or impaired (Dong, Gao, Sun, & Ye, 2021). There is an acceptable range around the mainstream strategy, and differences within the acceptable range will not make an enterprise lose its legitimacy (Deephouse, 1999); however, once it is beyond the acceptable range, enterprise behaviors may be questioned. Enterprise legitimacy may face a precipitous decline with strategic deviance increases (Haans, 2019). Compared with the rapid increase of management costs, transaction costs, and institutional costs, the low deviation from the acceptable range cannot make enterprises get rid of fierce competition. Specifically, there is no significant difference in competition between corporates with strategic deviance (from low to moderate) and the industry mainstream strategy. They still in a fiercely competitive environment and need more differences to escape the fierce competitive pressure. Therefore, corporate profit decreases when strategic deviance increases from low to moderate.

However, there is a point of corporate strategic deviance that the competitive advantages exceed the disadvantages (management costs, transaction costs and institutional costs). In other words, there is a positive relationship between corporate strategic deviance and corporate profit when over a certain point. The reasons are as follows: One is that enterprises could attract more consumers’ attention and support with strategic deviance increases (Cuellar & Gertler, 2006). Existing studies even found that the uncertainty of cash flow caused by strategic deviance could promote R&D investment and corporate value (Cui et al., 2019). The other reason is that corporations’ competitive pressures rapidly decrease when their strategic deviance is high; they can obtain excess profits, and their revenue is far more than management, transaction, and institutional costs. Specifically, although both management costs and transaction costs increase with strategic deviance increases, the impact is small compared with the benefits. In addition, when an enterprise’s strategy changes from edge just beyond the acceptable range to position far from the acceptable range, legitimacy will not precipitously reduce because stakeholders no longer consider it in the industry (Haans, 2019; Zuckerman, 1999). In other words, firms positioned far from the acceptable range have almost the same legitimacy as those just outside the acceptable range. That is, differences seriously damage legitimacy initially, but the damage slows down after a certain threshold; there is no difference in legitimacy between enterprises with high strategic deviance and enterprises with moderate strategic deviance. Figure 1 illustrates the negative effect of corporate strategic deviance on legitimacy (with the solid line) and the positive effect of corporate strategic deviance on competitive advantage (with the dotted line). Therefore, we propose that corporate profit increases when strategic deviance increases from moderate to high.

Theorized effects of corporate strategic deviance.

In summary, we posit that when companies have low and high strategic deviance, the promotion effect of strategic deviance on corporate profit is more obvious; companies face the lowest profit when they have medium-level strategic deviance, because of high costs and competitive pressures. In other words, we hypothesize that there is a curvilinear relationship between corporate strategic deviance and profit.

Based on the above analysis, we hypothesize:

The Moderating Effect of Institutional Environment Between Corporate Strategic Deviance and Corporate Growth

Institutional theory holds that a country’s economic, political and institution jointly determine production costs, transaction costs and corporate strategies (D. North, 2005; Peng, 2003). A strategy have different effects on corporate goals in different institutional environments (Ahuja & Yayavaram, 2011; Gao et al., 2017; R. Li & Ramanathan, 2020; Marquis & Raynard, 2015). Institutional environment refers to the quality of local institutions, it has two characteristics in China: first, there are institutional voids while institutional quality is gradually improving (Khanna & Palepu, 1997); second, there are variances in institutional quality among different provinces (S. Han et al., 2021; Q. Wang et al., 2008; Xie, 2017; Xu, 2011). We argue that the institutional environment may affect the relationship between corporate strategic deviance and corporate growth.

We believe that the positive relationship between strategic deviance and corporate growth will be stronger when firms are in provinces with developed institutional environments. The reasons are as follows: first, market competition in regions with developed institutional environments is fairer and fiercer, which provides opportunities for companies to achieve industry-leading positions through deviant strategies. In this environment, consumers are rational and picky because they have more choices, and they pay more attention to the intrinsic value of differences (Zeng et al., 2020); the partners pay more attention to opportunities that corporate strategic deviance may bring, they have high requirements for cooperative enterprises, the support of partners and consumers provide opportunities for companies to achieve leading positions through strategic deviance. Second, enterprises in regions with developed institutional environments can obtain accurate market information and developed capital market (Hoskisson et al., 2000; J. Li & Qian, 2013). Developed institutional environments can effectively avoid information asymmetry, which is conducive to enterprises choosing and adjusting their strategies. At the same time, developed institutional environments provide sufficient resources for enterprise, which effectively promote the positive impact of strategic deviance on corporate growth. Therefore, we hypothesize:

The Moderating Effect of Institutional Environment Between Corporate Strategic Deviance and Corporate Profit

Institutional environment also affects the relationship between corporate strategic deviance and corporate profit. We argue that developed institutional environments weaken the negative relationship between corporate strategic deviance and corporate profit when strategic deviance is low to moderate. This is because that developed institutional environments reduce resource constraints and information asymmetry, allowing corporates to utilize competitive advantages more efficiently from strategic deviance. First, companies in developed institutional environments could obtain scarce resources in market (Peng, 2003), which can reduce enterprises’ transaction costs. For example, companies can find alternative credit funding as China’s capital market develops (Nee & Opper, 2012), this provides resources for the deviant strategy. Second, developed institutional environments help companies overcome information asymmetry (Peng & Heath, 1996). Enterprises in developed institutional environments can understand consumers’ needs and reduce the trial-and-error costs. Third, consumers in developed institutional environments are rational to differentiation, which provides a good market environment for the deviant strategy (Zeng et al., 2020). So, developed institutional environments can reduce enterprises’ transaction costs and the trial-and-error costs, and provide a good market environment for corporate strategic deviance. On this basis, we expect that developed institutional environments weaken the negative relationship between corporate strategic deviance and corporate profit (when strategic deviance increases from low to moderate).

However, developed institutional environments combined with high corporate strategic deviance are more likely to erode profit. This is because firms located in regions with developed institutional environments may face more significant institutional pressures, highlighting the negative effect of corporate strategic deviance on corporate profit (R. Li & Ramanathan, 2020). The most significant characteristic of emerging markets is institutional voids (Khanna & Palepu, 1997), which may be more evident in less-developed regions. Although institutional voids may bring obstacles for enterprises to analyze market information and provide trading reputation signals (Khanna & Rivkin, 2001), it provides profitable opportunities to firms with resource priority and market advantages. Specifically, corporates in less-developed regions are subject to fewer institutional constraints and are more likely to exploit deviant strategies to create value; in contrast, governments and industry associations in developed institutional environments make corporations’ behaviors within an acceptable range; they are more likely be punished once they are beyond the acceptable range, which makes it virtually impossible for them to obtain profits through strategic deviance. Just as Denrell et al. (2003) pointed out that enterprises with resource priority and market advantages can obtain profit when the strategic factor market is incomplete. Therefore, we posit that developed institutional environments weaken the positive relationship between corporate strategic deviance and corporate profit (when corporate strategic deviance increases from moderate to high).

On this basis, we hypothesize:

Methodology

Data

The data in this study is from China Stock Market and Accounting Research Database (CSMAR). The dataset contains detailed information on indicators at both firm and industry levels, and it has been widely used in management research. The data of the institutional environment from China’s Marketization Index Report (2016). We focus on the 2010 to 2018 period in particular due to global financial crisis in 2008 (Haveman et al., 2017), we argue that this reduces the undesirable noise to our data. We remove firms with missing information, the final sample includes 20,798 observations.

Variables

Dependent Variable

We use sales growth and ROA to measure corporate growth and corporate profit, as applied in previous studies. Corporate growth is measured by the percentage of sales change between the next year and the current year (Jones & Miskell, 2007; Zhou & Park, 2020) and corporate profit is measured by ROA (Guo, 2017; McGahan & Porter, 1997).

Independent Variables

Strategic deviance reflects the degree of deviation between a corporate’s strategy and the industry mainstream strategy. We measure strategic deviance from six dimensions (Finkelstein & Hambrick, 1990; Tang et al., 2011; Ye et al., 2014): advertising intensity (the sales expenses/the operating income); R&D intensity (the net value of intangible assets/the operating income); capital intensity (the net value of fixed assets/employees); the renewal of fixed assets (the net value of fixed assets/the original value of fixed assets); the indirect cost efficiency (the management expenses/the operating income); financial leverage (the sum of short-term loans, long-term loans and bonds payable/the book value of equity). First, we calculate each enterprise’s advertising intensity, R&D intensity, capital intensity, the renewal of fixed assets, the indirect cost efficiency, and financial leverage; second, we calculate the difference between each index and the industry average, then divide the difference by standard deviation to standardize and take the absolute value; third, we calculate the arithmetic mean of six standardized indicators, this is corporate strategic deviance.

Institutional Environment

We use the market index (includes the relationship between government and the market, the development of non-state enterprise, the development of commodity markets, the development of credit market, and the development of the legal environment) from China’s Marketization Index Report (2016) to measure institutional environments. We predict the market index in 2017 and 2018 based on average growth range (Ma et al., 2015; Yu et al., 2010).

Control Variables

We control for equity restriction, asset liability, firm size and firm age that may influence corporate growth and corporate profit. First, equity restriction is measured by the number of shares held by the largest shareholder/the total number of shares held by the second to tenth shareholder. Second, we measure asset liability by the total loads/the total assets. Third, firm size is the number of employees (logged).

Model Definition

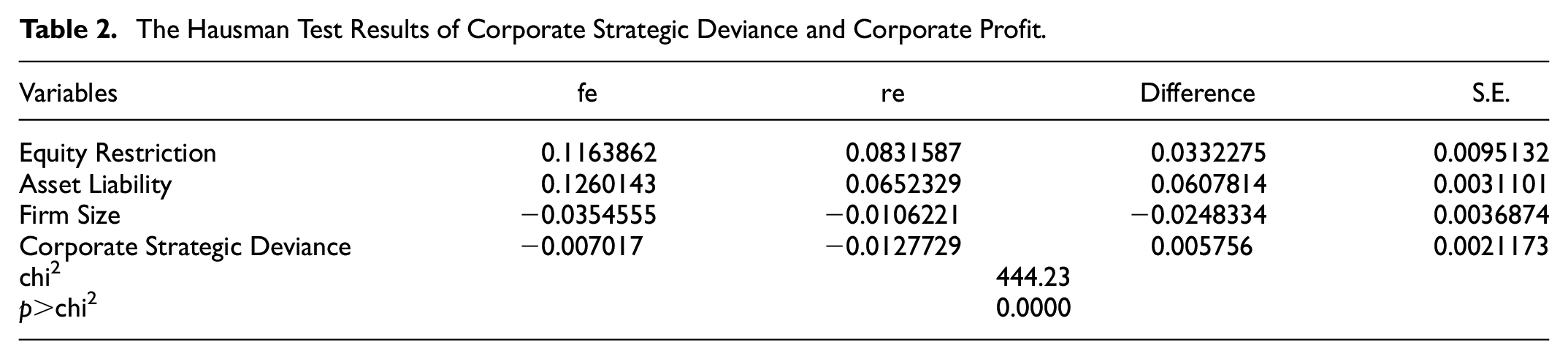

The Hausman test results of corporate strategic deviance and corporate growth show that

The Hausman Test Results of Corporate Strategic Deviance and Corporate Growth.

According to the Hausman test results of corporate strategic deviance and corporate profit (

The Hausman Test Results of Corporate Strategic Deviance and Corporate Profit.

We construct the regression models (as shown in Equation 1, Equation 2, Equation 3, and Equation 4): first, we use model (1) to test whether corporate strategic deviance has a positive effect on corporate growth; second, we use model (2) to test whether corporate strategic deviance has a curvilinear (U-shaped) relationship with corporate profit; third, we establish model (3) to test the moderating effect of the institutional environment on the relationship between corporate strategic deviance and corporate growth; finally, we establish model (4) to test the moderating effect of the institutional environment on the relationship between corporate strategic deviance and corporate profit.

where

Results

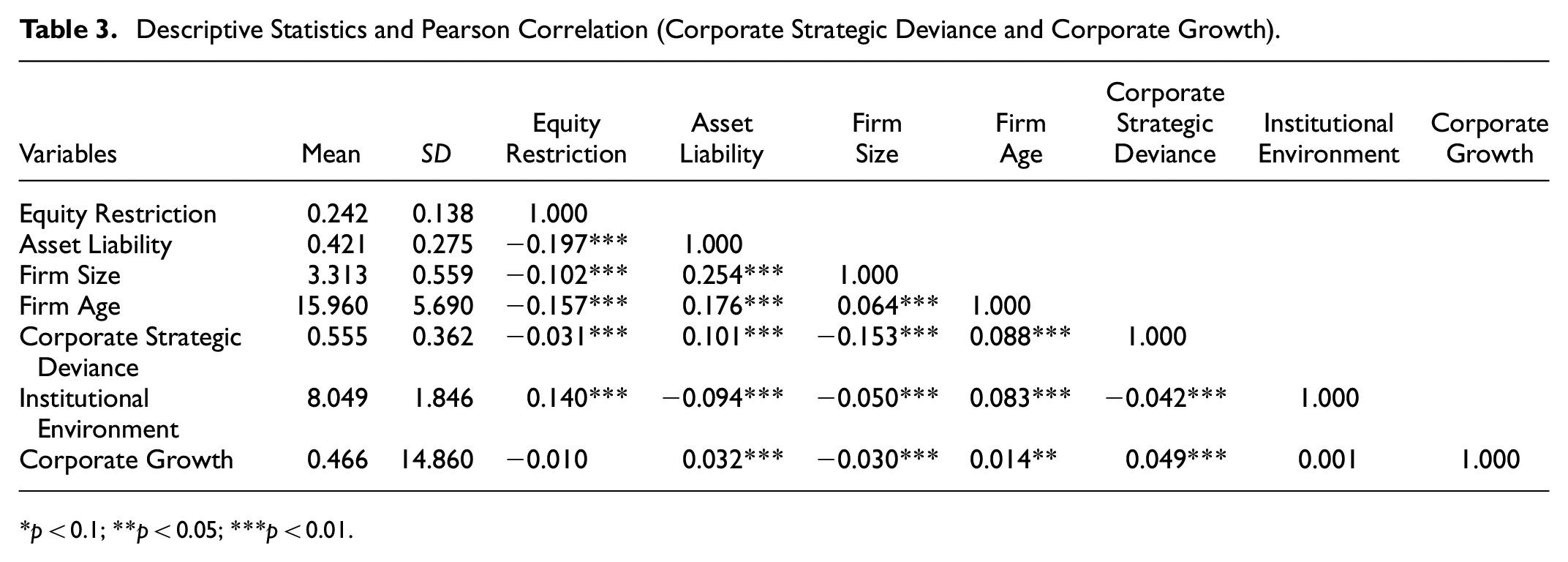

Descriptive Statistics and Pearson Correlation

Table 3 reports descriptive statistics of variables and the correlation coefficients between corporate growth and other variables. There is a significant positive correlation between corporate growth and corporate strategic deviance.

Descriptive Statistics and Pearson Correlation (Corporate Strategic Deviance and Corporate Growth).

p < 0.1; **p < 0.05; ***p < 0.01.

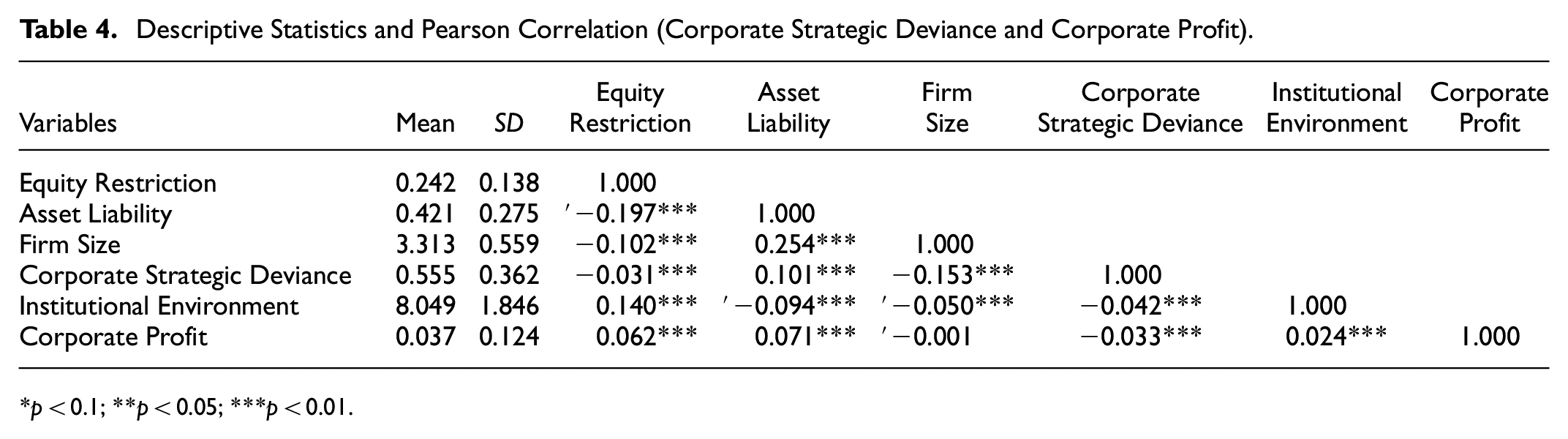

Table 4 contains descriptive statistics and the correlation matrix of corporate profit and other variables. There is a significant correlation between corporate profit and corporate strategic deviance.

Descriptive Statistics and Pearson Correlation (Corporate Strategic Deviance and Corporate Profit).

p < 0.1; **p < 0.05; ***p < 0.01.

Regression Results

From Table 5, we can conclude that Hypothesis 1 and Hypothesis 3 are supported. Models 1 and 2 yield support for Hypothesis 1, with corporate strategic deviance being significant. In Model 2, the coefficient estimate of corporate strategic deviance on corporate growth is positive and significant (

Regression Results (Corporate Strategic Deviance and Corporate Growth).

p < 0.1; **p < 0.05; ***p < 0.01.

We draw the moderating effect diagram to intuitively display the moderating effect of the institutional environment on the relationship between corporate strategic deviance and corporate growth, as shown in Figure 2. Figure 2 shows that the positive relationship is stronger when firms are in more institutionally developed provinces.

Corporate strategic deviance and corporate growth: The moderating effect of institutional environment.

From Table 6, Hypothesis 2 and Hypothesis 4 are supported. In Model 6, corporate profit is negatively and significantly related to the linear term of corporate strategic deviance (

Regression Results (Corporate Strategic Deviance and Corporate Profit).

p < 0.1; **p < 0.05; ***p < 0.01

Figure 3 display the U-shaped relationship between corporate strategic deviance and corporate profit.

Corporate strategic deviance and corporate profit.

Robust Test

We conduct additional analyze to test the robustness of Hypothesis 1 and Hypothesis 3. We measure corporate strategic deviance from four dimensions: capital intensity, the renewal of fixed assets, the indirect cost efficiency, and financial leverage (Y. Han, 2021; He & Yin, 2018), the results remain the same (Table 7).

The Robustness Test of Corporate Strategic Deviance and Corporate Growth.

p < 0.1; **p < 0.05; ***p < 0.01.

We conduct the Utest to further determine the U-shaped relationship between corporate strategic deviance and corporate profit. The results show that the extreme value (1.450) falls within the value range of corporate strategic deviance [0, 8.975]; and the research results reject the null hypothesis at the statistical level of 1% (as shown in Table 8). Therefore, the results indicate that corporate strategic deviance has a U-shaped relationship with corporate profit, which support for Hypothesis 2.

The Utest Result of Corporate Strategic Deviance and Corporate Profit.

Discussion and Conclusion

Using Chinese listed firms between 2010 and 2018 as research sample, this study examines the relationship between corporate strategic deviance and corporate performance (corporate growth and corporate profit) and analyzes the moderating effects of the institutional environment on those relationships. The results are as follows: first, corporate strategic deviance has a positive effect on corporate growth; second, there is a U-shaped relationship between corporate strategic deviance and corporate profit, that is, when corporate strategic deviance is low or high, it has a greater impact on corporate profit, by contrast, the medium level of corporate strategic deviance has less impact on corporate profit; third, the institutional environment has a positive moderating effect on the relationship between corporate strategic deviance and corporate growth; finally, the institutional environment has a negative moderating effect on the relationship between corporate strategic deviance and corporate profit, that is, the U-shaped relationship between corporate strategic deviance and corporate profit in developed institutional environments will become gentle.

Theoretical Implications

Our paper contributes to the literature in two ways. First, this study jumps out of previous research on the promotion or suppression of corporate strategic deviance on corporate performance and subdivides corporate performance into corporate growth and corporate profit, which explains the inconsistent conclusions on the relationship between corporate strategic deviance and corporate performance. Both corporate growth and corporate profit are important in emerging markets, this study finds that high corporate strategic deviance can bring growth and profit. This solves the inconsistency of current research on the relationship between corporate strategic deviance and corporate performance (Bao et al., 2014; Goll et al., 2007; E. Kim & McIntosh, 1996; Shrader & Simon, 1997; Singh et al., 1986; Z. Wang et al., 2021), deepening the understanding of corporate strategic deviance how to affect corporate goals.

Second, our research adds to the understanding of corporate strategy in different institutional environments. Existing studies have emphasized the adverse impact of institutional voids on enterprises, but our study points out that developed institutional environments may be a constraint for corporates whose strategic deviance is high to obtain profit. The result that developed institutional environments are conducive to enterprises to obtain resources and customers, which reconfirms Scott’s (1995) view that institutions provide stability and meaning to social activities. However, institutional pressures make corporates with high strategic deviance are more likely to be punished, this is consistent with the view of D. C. North (1990) and DiMaggio and Powell (1983) that enterprises must follow the “game rules”, conform to institutional expectations and requirements. Overall, developed institutional environments can strengthen the effect of corporate strategic deviance on corporate growth; however, developed institutional environments highlight the legitimacy disadvantage of strategic deviance. These findings reveal the complex interplay between the institutional environment, corporate strategic deviance, and corporate goals, which provide new insights into the evolution of institutional perspectives.

Managerial Implications

Our results also generate some managerial implications. The results are consistent with the reality of Chinese enterprises and have some similarities with Porter’s view of corporate competitive strategy. Although corporate strategic deviance and Porter’s differentiation strategy are not the same concept, if an enterprise implements Porter’s differentiation strategy, its strategic deviance is high. In China, the industry mainstream strategy is usually consistent with the low-cost strategy, so enterprises that are consistent with the industry mainstream strategy choose the low-cost strategy. Although the products’ unit price of such enterprises is low, they can obtain high profits due to the low costs and the large market (they have enough customers). However, the costs of corporates are high when their strategic deviance is high, but the uniqueness can bring high operating income, and corporates also have high profits. It is worth noting that the relationship between corporate strategic deviance and corporate profit may differ in developed markets because the industry mainstream strategy and the low-cost strategy in developed markets may not be consistent.

In addition, enterprises should consider the impact of the institutional environment when formulating their strategies. China is in the stage of market transition, with uneven development among provinces. It is easier for enterprises in institutionally developed provinces to obtain market information and resources, and market competition is fairer and fiercer. Corporations with high strategic deviance in institutionally developed provinces can increase their market share, which is conducive to growth. However, developed institutional environments highlight the legal disadvantages of enterprises whose strategy deviates from the industry mainstream strategy, and enterprises are more likely to be restricted and punished.

Limitations and Directions for Future Research

Although the results provide some references for the influence of corporate strategic deviance on corporate goals, there are some limitations of our study. First, the effectiveness of corporate strategic deviance in developed countries may differ. There are some differences between China and developed countries regarding resources and market environments (Thanh et al., 2022). In future, we can compare the effect of corporate strategic deviance on corporate goals in developed markets and emerging markets, to provide a more comprehensive reference for the role of strategic deviance. Second, this study examines the moderating role of the institutional environment on the relationship between corporate strategic deviance and corporate goals, however, these relationships may be affected by other factors, such as market competition; future research should explore the moderating effects of other potential variables.

Footnotes

Acknowledgements

The authors would like to thank anonymous reviewers and the editorial team for their insightful suggestions and warm works.

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: This study is supported by MOE (Ministry of Education in China) Project of Humanities and Social Sciences (Project No. 20YJA630039).

Data Availability Statement

The data used in this study are available from the corresponding author on reasonable request.