Abstract

In recent years, the global business landscpae has witnessed a paradigm shift toward sustainable and responsible corporate practices. This transition has been particulalrly pronounced in the energy sector where companies are increasingly recongzing the importance of Non-Financial Reporting Initiatives (NFRI) in shaping their operational strategies. The current study endeavors to delive into the intricate relationship between NFRI and the Weighted Average Cost of Capital (WACC) for energy companies in Pakistan. The current study relied on Partial Least Square Structural Equation Modeling (PLS-SEM) technique to extract useful information about the study topic. The data collected for the period 1999 to 2020 from World Development Indicators. The findings of the study revealed that energy consuption factors are responsiblee for around 31.32% variations in WACC, while economic factors contribute 43.98% variations. The financial factors showed to have 35.72% variations in the WACC. The findings of current study revealed to implement policies fostering sustainable energy practices, robust economic growth, and prudent financial management to positively influence the Weighted Average Cost of Capital (WACC) for enhanced business competitiveness and investment attractiveness.

Plain Language Summary

In recent years, the global business landscpae has witnessed a paradigm shift toward sustainable and responsible corporate practices. This transition has been particulalrly pronounced in the energy sector where companies are increasingly recongzing the importance of Non-Financial Reporting Initiatives (NFRI) in shaping their operational strategies. The current study endeavors to delve into the intricate relationship between NFRI and the Weighted Average Cost of Capital (WACC) for energy companies in Pakistan. The current study relied on Partial Least Square Structural Equation Modeling (PLS-SEM) technique to extract useful information about the study topic.

Keywords

Introduction

In the contemporary business landscape, it is imperative to innovate methodologies for evaluating company financial performance, with a burgeoning focus on the impact of non-financial factors. Addressing the influence of environmental, energy, and social factors on a company’s costs raises critical questions for societal consideration. The Weighted Average Cost of Capital (WACC), a pivotal metric in valuation, represents the rate at which free cash flows are discounted to achieve equivalent outcomes as equity cash flows discounted at the required return on equity (Fernández, 2010).

WACC, inherently neither a cost nor a required return, is contingent upon the cost of equity (ke) and the cost of debt (kd), necessitating their weighted consideration to mirror the company’s capital structure, coupled with tax implications factored in through the relevant tax rate (t) (Farber et al., 2006). Concurrently, a noteworthy surge in CO2 emissions in Pakistan since 2014 stands in contrast to declining trends in other global regions (Lin & Raza, 2019).

The energy sector emerges as a linchpin in the economic development of nations worldwide, with its symbiotic relationship with both households and businesses. Undeniably, the energy industry’s significance is even more pronounced in China, where it intricately intertwines with the overall economy. The holistic Total Factor Energy Efficiency (TFEE) concept, encompassing energy power, efficiency, and heat consumption rate, has been integral to prior energy efficiency assessments (Ruzzenenti & Basosi, 2009).

Against this backdrop, Pakistan’s strategic importance within China’s Belt and Road Initiative (BRI) since 2013 underscores its critical role in receiving substantial infrastructure investments from China. However, Pakistan grapples with mounting financial challenges stemming from environmental shifts while concurrently confronting energy security issues, necessitating a secure, reliable, and affordable energy supply (Asif et al., 2017).

The current study holds exceptional significance, being the first of its kind in Pakistan. Notably, within the energy sector, few studies have delved into the intersection of WACC and non-financial factors. This research uniquely contributes to the field of innovation by focusing on non-financial companies, unraveling intricate relationships between WACC and independent variables such as energy, environmental, and financial factors (Damodaran, 2001).

Literature Review

Non-financial Reporting Initiatives in the World

Establishing an optimal capital structure assumes paramount significance in contemporaneous business dynamics, as it intricately contributes to augmenting a company’s intrinsic value. The composition of a corporation’s working capital, a blend of debt and equity, serves as the financial bedrock supporting its operational endeavors. A judiciously organized structure not only streamlines operational efficiency but also mitigates the overall cost of capital, thereby enriching the company’s valuation (Damodaran, 2001).

Recognized as a pivotal managerial decision, the management of working capital holds pivotal sway over shareholder risk and returns, thereby underscoring its pivotal role in corporate strategy (Zhang et al., 2023). Scholarly inquiry into the correlation between debt and gross domestic output reveals a nuanced interplay. Debt, it has been found, exerts a discernible negative impact on growth dynamics. In instances of low gearing, shareholders anticipate a modest return due to lower associated risks, whereas an increase in debt elevates the Weighted Average Cost of Capital (WACC). Consequently, astute stock investors demand higher yields to offset heightened risks, leading to an amplified cost of equity that surpasses the benefits derived from debt reduction, thereby causing an upward trajectory in the WACC.

A seminal revelation by Modigliani and Miller (1958) posited that, excluding tax considerations, a corporation’s financial structure bears no influence on its cost of capital or overall valuation. The regulatory landscape has evolved since then, with firms listed on the Johannesburg Stock Exchange (JSE) mandated to prepare integrated reports since 2010, aligning with the provisions of the King III report (Onaolapo & Kajola, 2010), as stipulated by the South African government.

In this dynamic commercial environment characterized by cutthroat competition, stakeholders evince a keen interest in the trajectory of organizational progress. Management and shareholders deploy an array of financial ratios, computed from the balance sheet and income statement, to comprehensively assess and evaluate financial performance (Degryse et al., 2012).

This multifaceted exploration underscores the intricate relationship between capital structure decisions, cost of capital dynamics, and the overall financial health of a company. As businesses navigate this complex terrain, the ability to strategically manage working capital emerges as a linchpin for sustained success and enhanced shareholder value.

Non-financial Reporting Initiatives in Pakistan

Onaolapo & Kajola’s (2010) investigation reveals a discernible adverse impact of long-term debt, particularly in emerging nations, on organizational performance (Onaolapo & Kajola, 2010). Previous scholarly inquiries, as evidenced by research spanning (Akbarpour & Aghabeygzadeh, 2011; Črnigoj & Mramor, 2009; El-Sayed Ebaid, 2009), have consistently reported a negative correlation between performance metrics, notably return on assets (ROA), and levels of indebtedness. However, a comprehensive examination by (Fosu et al., 2016), utilizing a substantial dataset from U.K. enterprises, identified a nuanced influence of leverage on organizational value.

Moreover, the assertion by (Islam & Khandaker, 2015; Salim & Yadav, 2012) regarding the industry-specific and operational nuances of businesses underscores the intrinsic variability in capital structure decisions and their consequential impact on financial performance. Notably Saeed and Badar (2013), uncovered a significant correlation between elevated levels of indebtedness and suboptimal business performance within the Pakistani food and sugar industries.

Exceptionally, domestic photovoltaic (P.V.) prosumers exhibit a distinctive real Weighted Average Cost of Capital (WACC) of 4%, attributed to diminished financial resources and a return to fundamental necessities. In contrast, Pakistan’s standardized WACC stands at 7% across all industries, irrespective of whether the anticipated WACC deviates from this benchmark. Intriguingly, an escalation in WACC, while potentially concerning in the broader economic context, does not manifest any discernible impact on the cost dynamics of the energy system, as asserted by Breyer et al. (2017) and Saeed and Badar (2013).

Projections into the future, as envisioned by the authors, anticipate a persistent 7% real WACC for Pakistan by the year 2050. This prognostication underscores the enduring financial dynamics and stability projected for the country within the considered timeframe

Multi Capital Approach in Pakistan

The energy sector plays a pivotal role in shaping the economic trajectory of any nation, influencing both households and businesses. Regardless of demographic specifics, geographical location, or industrial pursuits, the indispensability of energy in sustaining daily operations is irrefutable. The imperative lies in meeting a nation’s energy needs cost-effectively while concurrently upholding environmental sustainability (Kalicki & Goldwyn, 2013). In Pakistan’s Vision 2025, energy security is articulated as ensuring “access to affordable, reliable, sustainable, and modern energy for everyone” (Mirjat et al., 2017). The country, however, grapples with a growing reliance on imported energy, detrimentally impacting its competitiveness and environmental resilience, while other regions globally transition to natural fuels, deemed more cost-effective and environmentally sustainable (Naeem Nawaz & Alvi, 2018).

Pakistan’s recent substantial investments in coal and liquefied natural gas (LNG) power projects have been marred by challenges. Numerous completed projects fail to attain their maximum load capacity due to design flaws and mismanagement, with some even abandoned (Rafique & Rehman, 2017). The formulation of energy policies in Pakistan, encompassing production, consumption, distribution, and transmission, involves the collaborative efforts of governmental, provincial, and local entities (Akhtar & Sarmah, 2018). On the global scale of energy security challenges, Pakistan’s highest score was 1,114 in 1992, contrasting sharply with its lowest score of 1,516 in 2011, attributed to a neighborhood power outage. The current precarious score, at 1,290, remains significantly high compared to 1992 (Mirjat et al., 2017).

Within the power sector, Pakistan has grappled with petroleum and energy shortages, major transmission and distribution failures, aging infrastructure, and significant payment issues (Hassan et al., 2019). The demand for power exceeded 21,500 MW during a 2016 heatwave, necessitating mandatory load shedding to address a 6,500 MW deficit. In rural areas, load shedding and power outages extended up to 20 hr, while major urban centers experienced consistent outages lasting up to 14 hr.

Pakistan’s distribution utilities faced dire financial straits, contributing to extensive load shedding from 2013 to 2016. Moreover, the National Transmission and Distribution Company (NTDC) faced challenges in cleaning 95% of transmission lines in a timely manner in 2017, leading to severe load shedding. Policymakers and scholars have directed their focus toward the intricate relationship between fossil fuel emissions and economic growth, aiming to mitigate emissions without compromising economic development. Pakistan is a focal point of this investigation due to its central role in the issue. While Pakistan’s GDP surged by 375% between 1980 and 2014, fossil fuel emissions only increased by 118% (World Bank, 2016). Despite contributing just 1% to global fossil fuel emissions, Pakistan ranks among the top five countries most affected by climate change, according to the 2018 Global Climate Risk Index (Salam, 2018).

Several prior studies have established connections between energy consumption, financial growth, and CO2 emissions, emphasizing the interdependence of these factors (Zmami & Ben-Salha, 2020). Energy, whether as a composite component or a source, exerts a tangible impact on economic dynamics, as evidenced by extensive research on the relationship between CO2 emissions and financial growth (Teng et al., 2021). Other studies explore the intricate links between globalization, economic considerations, and energy use in the realms of CO2 emissions, renewable energy, foreign direct investment, electricity consumption, capital structure, and economic expansion. Pakistan confronts a myriad of challenges, including escalating energy demand, environmental pollution, and sluggish economic development, with a projected GDP growth of 2.4% in 2020, the slowest among South Asian countries (Asafu-Adjaye, 2000).

As posited by (Asafu-Adjaye, 2000), the utilization of natural gas significantly influences Pakistan’s economic growth. Further investigations delve into the correlation between CO2 emissions and foreign direct investment, electricity consumption, capital structure, and economic expansion. The pivotal role of energy consumption in economic growth is undeniable, highlighting the intrinsic connection between the two. A nation’s energy mix emerges as a critical factor; fossil fuel emissions exhibit a negative correlation with countries that incorporate a higher percentage of renewable energy in their mix (Hanif, 2018; Nicolli & Vona, 2019), while a positive correlation is observed in countries with a lower share of green energy (Nicolli & Vona, 2019). In 2014, renewable energy constituted 47% of total energy consumption in Pakistan, showcasing a positive association between energy consumption and fossil fuel emissions (Shahbaz et al., 2012; Ur Rehman et al., 2019).

To address these challenges and chart a sustainable energy future, Pakistan is prioritizing energy infrastructure improvements as part of the China-Pakistan Economic Corridor (CPEC), with the primary goal of diversifying the overall fuel mix by 2030. This strategic initiative aims to bolster the country’s energy resilience and foster long-term environmental sustainability.

Multi Capital Approach in the World

Globally, the intricate relationship between development and energy is undeniable, forming an inseparable nexus. Human resources, financial capital, energy, and technological advancements transcend economic boundaries, flowing predominantly from the West to the East in the prevailing globalized paradigm. Even before the dismantling of the ideal competitive structure, human resources emerged as one of the essential capital components, manifesting recurrent returns to scale. The AK model, pioneered by Evenson and Westphal (1995), exemplifies the integral role of capital, including financial, in catalyzing growth, influencing the capacity of products to generate enhanced yields.

In the context of India, transport infrastructure emerges not only as a catalyst for economic growth but also as a significant contributor to gross capital formation. Therefore, it is proposed that augmenting transport facilities, encompassing both road and railway networks, in conjunction with promoting gross capital formation, will foster a more pervasive economic growth trajectory in India. The attainment of higher economic growth through enhanced transport infrastructure is underlined by the manifold direct and indirect benefits it imparts to the economy. However, the current state of transport infrastructure in India, both in terms of quantity and quality, falls short in comparison to developed countries. The positive outcomes postulated in this study could be significantly enhanced with substantial improvements in transport infrastructure. Recognizing the pivotal role of transport infrastructure in economic growth, a prudent transport policy is advocated to sustain and augment India’s economic prosperity (Pradhan & Bagchi, 2013). Given the expansive distribution of population and industries in India, a judicious modal transport mix is deemed imperative for fostering economic development. However, a fragmented approach to this critical issue, characterized by seemingly unclear policies, may lead to adverse consequences such as resource wastage and a potential slowdown in long-term economic growth (Pradhan & Bagchi, 2013). To avert such outcomes and maintain economic momentum, concerted efforts are essential to incentivize government investment in transport infrastructure, overcoming constraints like land acquisition. In essence, based on macroeconomic data, this study advocates that the Indian government prioritize upgrading and expanding the country’s transport infrastructure to sustain and amplify the positive economic momentum it has achieved.

Recognizing energy as a fundamental factor of production (Zeeshan et al., 2020), underscores the importance of energy efficiency coupled with price reductions in driving growth. The causal relationship between energy and output has been a focal point since the oil shocks of the 1970s (Paul & Uddin, 2011). Steblyanskaya et al. (2019) delved into the linkages between energy, social, environmental, and financial indicators in Russian oil and gas firms. Various studies, including those by Ghali and El-Sakka (2004) for Japan and Canada and Giannetti et al. (2020) for Pakistan, have identified bidirectional causality between energy and economic development, employing diverse determinants. The surge in global energy demand, driven by rapid population expansion and industrialization, poses a substantial threat to economies, energy security, and sustainable development (Giannetti et al., 2020).

In the case of China, the government’s transformative economic development patterns and significant green investments have led to remarkable improvements in its Industrial Carbon Productivity (ICP) (Long et al., 2020). However, China’s carbon efficiency lags behind other nations due to its heavy industry and reliance on coal-fired power (Bai et al., 2019). Researchers have explored the relationship between ICP and CO2 emissions (Gazheli & van Den Bergh, 2018), with Chinese scholars investigating the carbon efficiency of sub-modern sectors such as materials, power, pulp, paper, and various industries (Lin & Raza, 2019). This nuanced exploration of the interplay between energy, social, environmental, and economic dimensions underscores the imperative for comprehensive policies that prioritize sustainability and efficiency on the global stage.

Methodology

Methodological Base

The research employs a mixed-methods approach, encompassing both observational and quantitative methodologies, to comprehensively investigate the impact of energy, environmental, and financial factors on a company’s Weighted Average Cost of Capital (WACC). The analytical tool chosen for hypothesis testing is the Stata_14 software, specifically utilizing partial least squares structural equation modeling (PLS-SEM) as recommended by Hair et al. (2014). This methodological choice aligns with the exploratory nature of the current research and enhances the suitability of the analysis for the complex relationships being examined.

The research focuses on assessing the impact of energy, environmental, and financial perspectives on a company’s WACC. To facilitate this investigation, quantitative data is derived from the World Development Indicators (WDI), a reputable and authoritative database provided by the World Bank. The data spans the period from 1990 to 2020, constituting the temporal scope of the study. This extensive timeframe allows for a comprehensive exploration of trends and patterns in the variables of interest over the past three decades.

The dependent variable in this study is the Weighted Average Cost of Capital (WACC), while the independent variables include Energy, Environmental, and Financial factors. The utilization of the PLS-SEM technique offers a robust framework for modeling and analyzing the complex relationships between these variables. This method is particularly well-suited for the exploratory nature of the research, providing flexibility in accommodating a variety of data types and ensuring a thorough examination of the intricate interplay among the variables.

To conduct the analysis, the study employs the standard least square (OLS) method. This statistical technique is employed to assess the impact of the selected independent variables (Energy, Environmental, and Financial factors) on the dependent variable, WACC. The OLS method allows for the estimation of the coefficients that represent the relationship between the variables, enabling the identification of significant factors contributing to variations in the WACC.

In summary, the research adopts a comprehensive methodological foundation, combining observational and quantitative approaches. The use of Stata_14 software, along with the PLS-SEM technique, ensures a rigorous analysis of the relationships between energy, environmental, and financial factors and a company’s Weighted Average Cost of Capital. The reliance on the World Development Indicators database and the extended timeframe from 1990 to 2020 further enriches the study’s empirical foundation, providing a nuanced understanding of the dynamics influencing WACC over time. A brief description of each factor is as below in Table 1

Variable Description.

Econometric Modeling

The study investigated the relationship between independent and dependent variables by performing linear regression on each instance and factor inclusion. Figure 1 shows theoretical framework which clearly explain our independent variables and dependent variables.

The Weighted Average Cost of Capital (WACC) is a financial metric that represents the average rate of return a company is expected to pay to its investors, taking into account the proportional weight of each component in the company’s capital structure (Randall & Theodore Farris, 2009). Fernández (2010) argue that WACC is a crucial factor in financial decision-making, such as project valuation and investment analysis. The formula to calculate WACC is as follows:

where:

E is the market value of the company’s equity,

D is the market value of the company’s debt,

V is the total market value of the company’s equity and debt (i.e., E + D),

Re is the cost of equity,

Rd is the cost of debt,

Tc is the corporate tax rate.

Where E.C is energy consumption, E.F is environmental factor, and EE.F represents financial factors. The above mathematical relationship can be explained in an econometric term as:

Weighted average cost of companies (WACC) =

Where β0, β1, β2, and β3 are the coefficient values of independent variables, ∈ represents residuals, and “it” denotes the panel features.

Linear regression calculates the predicted weights, indicated with 0, 1, …, r, which defines the estimated regression function

Research scheme.

Empirical Results

Descriptive Statistics

During the review time frame 1990 to 2020, distinct measurements demonstrate test properties like mean, standard deviation, most extreme, and least upsides of the factors. For example, the descriptive statistics features of variables by Pakistan are given in Table 2.

Descriptive Statistics of Pakistan.

The mean value of Weighted average cost of companies (WACC) for Pakistan during 1990 to 2020 recorded 0.09 with an average standard deviation of 0.01, representing that the possible deviation from the mean value is less than the actual mean value. The base incentive for Weighted normal expense of organizations (WACC) was 0.07, showing that Weighted typical expense of organizations (WACC) during the specific age was belt-molded—the most extreme worth of WACC in Pakistan is at 0.12.

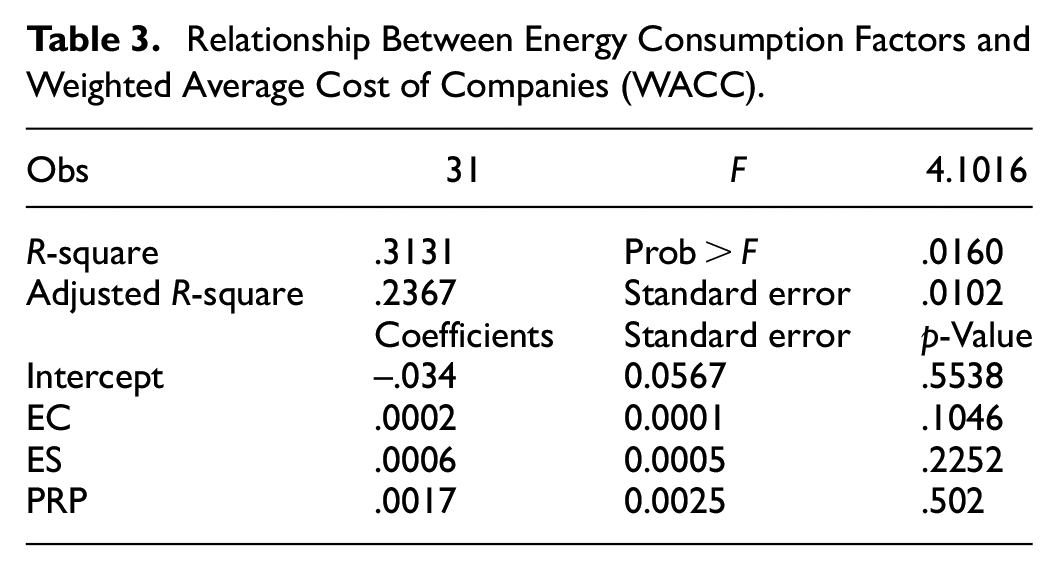

Regression Analysis Between Energy Consumption Factors and Weighted Average Cost of Companies (WACC)

The coefficient of long total energy use has a strong positive impact on WACC in a simple regression model, indicating that for every 1% rise in energy consumed, the WACC increases by 0.0002 units, as seen in the above regression results table 3. According to the findings, the total log amount energy use is responsible for roughly 31% of WACC fluctuations. Energy saving and WACC have positive coefficient values, indicating that the variables under consideration positively impact WACC. The total consumption of renewable savings positively impacts WACC, according to the final model. As a result, total consumption and energy savings are important positive drivers of WACC among energy consumption parameters.

Relationship Between Energy Consumption Factors and Weighted Average Cost of Companies (WACC).

Regression Analysis Between Environment Factors and WACC

In the above analysis results table 4, the coefficient of ROL demonstrates a significant positive effect on WACC in a simple regression model indicating that the WACC increases by −0.0006 units for every 1% increase in overall energy consumption. According to the findings, the log amount of total energy use is responsible for roughly 31% of WACC fluctuations. Both Saving energy and WACC have positive coefficient values, indicating that the variables under consideration positively impact WACC. According to the final model, total energy savings have a large positive impact on WACC. As a result, total measuring energy savings are important positive drivers of WACC among energy consumption parameters.

Relationship Between Economic Factors and CO2 Emission.

Regression Analysis Between Financial Factors and Weighted Average Cost of Companies (WACC)

The autonomous elements are all considerably connected with the reliant factors, as in Table 5. The coefficient of all financial factors has a strong negative impact on WACC in a simple regression model, indicating that for every 1% rise in current ratios (C.R.), the WACC decrease by −0.0060 units, as seen in the above regression results table 5. As a result, total financial factors are important positive drivers of Weighted average cost of companies (WACC) among consumption parameters.

Relationship Between Financial Factors and Weighted Average Cost of Companies (WACC).

Result Discussion

The analysis of Weighted Average Cost of Companies (WACC) for Pakistan spanning the period 1990 to 2020 reveals valuable insights into the financial dynamics of the country. The mean value of WACC during this timeframe is calculated at 0.09, accompanied by a modest standard deviation of 0.01. Bancel et al. (2013) argue that the narrow standard deviation suggests that the possible deviation from the mean is less than the actual mean value, indicating a relative stability in the WACC over the specified period. The base incentive for WACC is identified as 0.07, emphasizing a belt-molded trend, with the maximum recorded WACC reaching 0.12.

Upon examining the regression results, the coefficient of long total energy use exhibits a robust positive impact on WACC in a simple regression model (Bekun, 2022). This finding indicates that for every 1% increase in energy consumed, the WACC experiences a corresponding increase of 0.0002 units. Notably, the total log amount of energy use is attributed to approximately 31% of WACC fluctuations. The positive coefficient values for both energy saving and WACC further underscore their impactful contributions, highlighting them as significant positive drivers of WACC among energy consumption parameters (Akbarpour & Aghabeygzadeh, 2011; Asif et al., 2017; Randall & Theodore Farris, 2009). The positive influence of total consumption and energy savings is particularly emphasized in the final model, consolidating their importance in shaping WACC (Fernández, 2010).

In a parallel analysis, the coefficient of the rate of long-term energy use (ROL) demonstrates a notable positive effect on WACC in a simple regression model. The WACC is shown to increase by −0.0006 units for every 1% increase in overall energy consumption, with the log amount of total energy use accounting for approximately 31% of WACC fluctuations. The positive coefficient values for both energy saving and WACC persist in this context, reiterating their positive impact (Črnigoj & Mramor, 2009; Evenson & Westphal, 1995). Moreover, the final model underscores the substantial positive influence of total energy savings on WACC, positioning them as crucial positive drivers among energy consumption parameters (Damodaran, 2001).

Delving into the financial factors, the autonomous elements exhibit a significant negative impact on WACC in a simple regression model. Specifically, for every 1% rise in current ratios (C.R.), the WACC is observed to decrease by −0.0060 units. This finding highlights the pivotal role of financial factors in shaping the WACC, as total financial elements emerge as substantial positive drivers of WACC among consumption parameters.

Conclusion

Conclusion

Examining the financial landscape of Pakistan from 1990 to 2020, our analysis of the Weighted Average Cost of Companies (WACC) suggests a stable environment with a mean value of 0.09 and a narrow standard deviation of 0.01. This indicates a consistent financial backdrop over the years. Notably, the interplay of energy, environmental, and financial factors plays a pivotal role in shaping WACC (Degryse et al., 2012). The positive relationship between long total energy use and WACC underscores the impact of energy consumption on capital costs (Shahbaz et al., 2012). Financial stability, particularly reflected in current ratios, emerges as a significant factor in reducing WACC (Fernández, 2010). This highlights the importance of integrated strategies that consider both energy management and financial stability to optimize capital costs for businesses in Pakistan (Gazheli & van Den Bergh, 2018).

Policy Recommendations

To enhance energy efficiency, it is recommended that Pakistan encourages businesses to adopt energy-saving technologies. Providing incentives for investments in renewable energy sources will not only contribute to environmental sustainability but also positively impact WACC (Bekun, 2022). Additionally, Afjal et al. (2023) probe that promoting financial stability through supportive policies and facilitating access to affordable financing options for businesses is crucial. The government should focus on sustainable energy practices and the reduction of carbon emissions, aligning policies with global environmental goals.

Public-private partnerships can drive collaborative efforts to implement energy-saving initiatives and share best practices (Wibowo et al., 2019). Encouraging businesses to incorporate long-term energy and financial planning into their strategies, along with continuous monitoring and assessment of policies, will contribute to sustainable economic development (Paul & Uddin, 2011). Overall, a balanced approach considering both energy and financial factors is key to fostering resilience and competitiveness in Pakistan’s evolving economic landscape. By implementing these targeted measures, Pakistan can enhance its economic resilience and contribute to global sustainability goals

Footnotes

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: Funds for this research paper are provided by Harbin Engineering University International Office.

Data Availability Statement

The data that support the findings of this study are available from the corresponding author upon reasonable request