Abstract

This study uses a modified UTAUT model to examine behavioral factors influencing mobile banking services’ (MBS) adoption in China. Despite the abundance of smart mobile phones, the uptake of mobile banking among the population remains low. To address this issue, this study integrates four variables—perceived financial cost, awareness, technology infrastructure support, and government regulations—into the UTAUT framework to explore their impact on driving the adoption of MBS. Based on convenient sampling techniques, it uses 567 valid responses collected through a self-administered questionnaire and applies multiple regression analysis methods for data analysis using SPSS-26 software. Results indicate that performance expectancy, effort expectancy, perceived financial cost, and awareness are significant drivers of behavioral intention to use MBS in China. Technological infrastructure support positively influences performance expectancy, and individuals’ intent to use and adopt MBS in China. Government support significantly drives the individual’s behavioral intention to use and adopt MBS. Furthermore, behavioral intention to use MBS significantly predicts its adoption in China. The practical and academic ramifications of MBS on the growth and development of sustainable mobile banking systems are presented.

Introduction

Advancements in information and mobile technology systems provide businesses with a new impetus to achieve higher efficiency in service output. The banking industry also leverages modern mobile technological systems to enhance its operations, particularly through mobile banking services (MBS). Banks utilize information and mobile technologies to transform the traditional brick-and-mortar banking service delivery system into advanced operations such as transaction tracking and processing, queue management, account opening and checking, and information provision (Altin Gumussoy et al., 2018; Shankar & Kumari, 2016). Financial organizations provide mobile banking services through portable technological systems (Shankar et al., 2020; Tam & Oliveira, 2017) and these services are accessible through various mobile computing devices such as smartphones, tablet computers, and personal digital assistants (PDAs)(Koksal, 2016; Laukkanen & Kiviniemi, 2010). These mobile technologies empower banks to provide 24-hr banking services to customers worldwide (Z. U. Rehman & Shaikh, 2020; Tam & Oliveira, 2017). The flexibility and mobility of mobile systems also enable banks to create tailor-made services for their consumers (Chawla & Joshi, 2019; Quirici, 2020).

The digital economy has drastically revolutionized the financial industry including the operation of banks (Ashurovich, 2022; Tsindeliani et al., 2022). Particularly, the advanced technological systems have significantly enhanced the efficiency and effectiveness of bank operations, contributing to the improvement of monetary systems that ensure stability and flexibility to outside stimuli that is, sustaining structural transformation and the creation of a competitive environment (Jamalurus, 2022; Mansour & Salem, 2022). Additionally, the extensive digitalization in the banking industry also augments transparency in business operations, diminishes bribery (corruption), and improves regulations and supervision systems in the banking sector (Naimi-Sadigh et al., 2022; Tsindeliani et al., 2022). The digital transformation in the banking sector also expanded the range of services that banks can offer and facilitated new service functions to drive better cooperation between banks and consumers (Ha & Nguyen, 2022; Rushchyshyn et al., 2022). Digitalization of products and services also helps banks to compete based on the quality of their digital services, which could influence customers to either remain or switch to another bank (Gautam & Sharma, 2022; Jaroli et al., 2022).

M-banking has a profound bearing on the banking system due to the widespread use of mobile and smartphone devices (Safeena et al., 2012). Despite the growing availability of mobile phones, the use of smartphones for undertaking m-banking services or accessing financial data is not as prevalent as anticipated (Ramdhony & Munien, 2013; Shih et al., 2010). For instance, smartphone adoption in China has risen from 50% of the population in 2018 (Daniel, 2021) to 75% of the population in 2022 (Statista, 2023c). However, the MBS adoption is still low as 254 million (18% of the population) registered m-banking users as compared to the number of mobile device subscribers 1.7 billion as of July 2023 with an estimated mobile internet penetration rate of 99.8% in China—an indication that the Chinese economy and society have reached a higher degree of digitalization (Statista, 2023b). This less active use of mobile banking is the major research problem identified in this study since it deprives people especially those in deprived regions the chance to enjoy the socio-economic benefits and improvement in their quality of life that comes with the adoption of MBS.

China’s m-banking literature indicates that artificial intelligence and anthropomorphism can enhance individual desires to adopt mobile banking services while at the same time, both intelligence and anthropomorphism demonstrate an insignificant impact on perceived risk (J.-C. Lee & Chen, 2022). Current technological innovations like mobile banking can contribute to mitigating the significant divide in financial accessibility between urban and rural sectors in China (Zhu et al., 2022). Particularly, tackling the challenge of the lack of adequate availability of financial infrastructure and financial products in the rural financial situation in China would bolster the wider adoption of mobile banking services (Zhu et al., 2022). Given the faster pace of technological transformation in the banking sector, there is a need for government intervention to develop comprehensive programs and legal regulations to guide the implementation of a digitized banking sector (including m-banking) to achieve financial sustainability (Chouaibi et al., 2022; Tsindeliani et al., 2022).

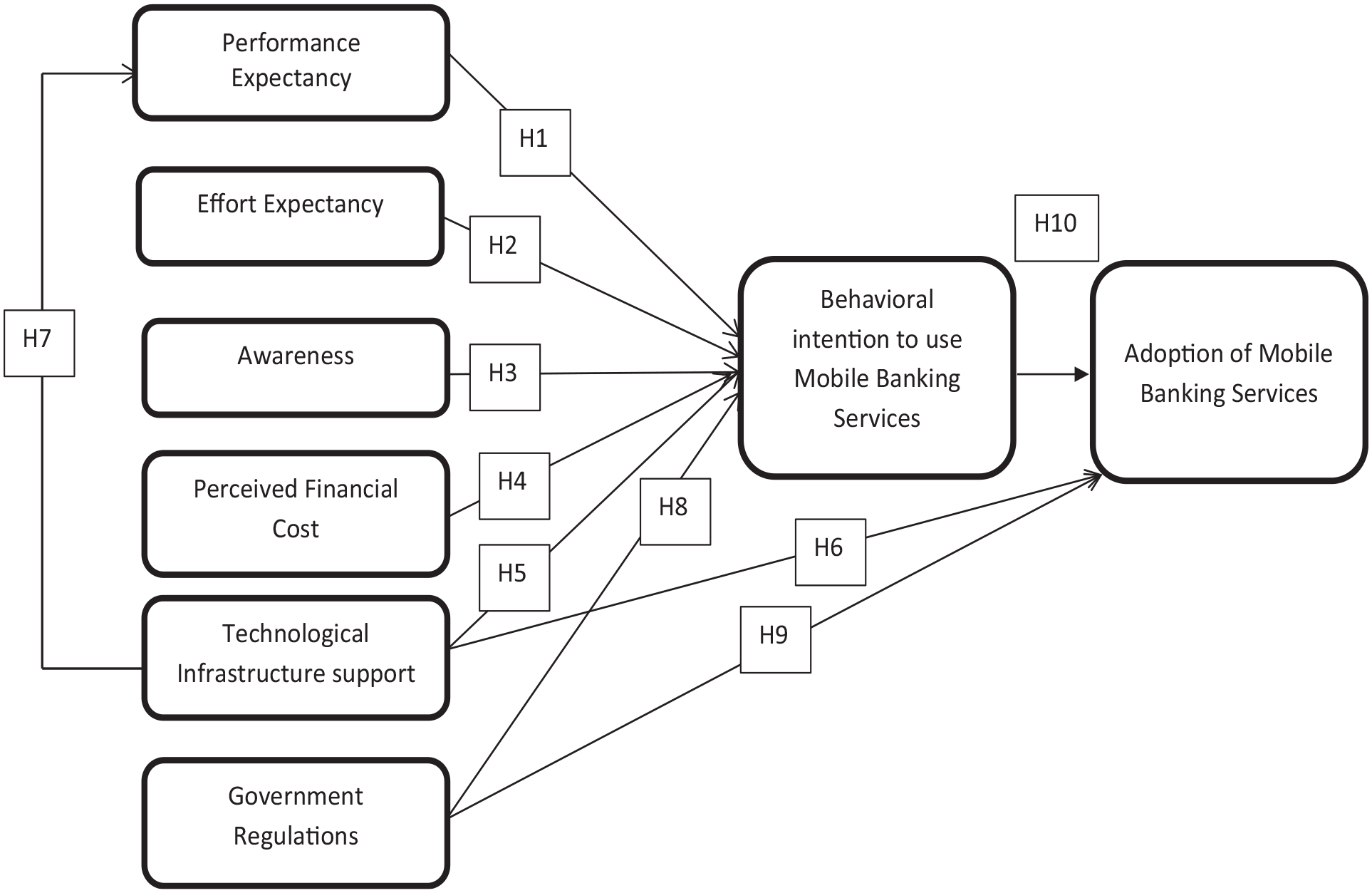

The objective of this research is to understand the factors that encourage mobile banking services adoption among Chinese citizens based on the fundamental framework of the Unified Theory of Acceptance and Use of Technology (UTAUT) model. This study developed a modified UTAUT model to integrate perceived financial cost, awareness, technology infrastructure support, and government regulations into the UTAUT to unearth the factors that can drive the wider adoption of mobile banking services in China. UTAUT is the most utilized, robust, validated, and reliable model to study technological adoption since it was integrated with other well-known models and outperformed individual models like TAM (Venkatesh, 2022; Venkatesh et al., 2003). Thus, it is an appropriate model to measure the drivers of technology acceptance and diffusion like mobile banking services adoption in China. Additionally, UTAUT has been validated in diverse geographical settings to elucidate drivers of technology adoption and consequently solidify its generalizability potential (Venkatesh et al., 2012). The broader research question interrogated in this study is: what factors drive the intention of Chinese citizens to use MBS based on the UTAUT model? The specific and explicit research questions are: (1) to what extent does the perceived financial cost and awareness along with the two core constructs of UTAUT (performance and effort expectancy) influence the intention to use MBS? (2) To what extent do technological infrastructure support and government regulations influence the intention to use and adoption of MBS? (3) To what extent does technological infrastructure support influence the performance expectancy of MBS? (4) To what extent does the behavioral intention to use influence the adoption of MBS? Addressing these research questions not only contributes to the literature on e-commerce and m-banking, especially with the inclusion of government regulations and technological infrastructure support into the modified UTAUT model but also allows governments, financial institutions, and mobile banking practitioners to develop sustainable mobile banking systems as a catalyst to achieve greater financial inclusion and accessibility, especially in rural regions.

The research is structured as follows: literature review and hypotheses advancement, research model, methodology, presentation of findings, discussions, conclusion and drawback of the paper, and proposed future works.

Literature Review and Hypotheses

China’s M-Banking Environment

China introduced m-banking through the Bank of China in 1999. Since then, the use of mobile banking has grown significantly due to the increasing popularity of smartphones. The majority of Chinese banks have launched their mobile banking services for different mobile systems. More financial services are being offered through mobile phones, replacing some of the traditional functions and operations of physical banking outlets (Guo, 2018). Moreover, in the face of fierce competition from Fin-tech companies, the loyalty of bank customers is declining. Mobile banking can provide banks with the perspective to achieve a competitive advantage in retaining and developing new consumers while improving user gratification by reducing the service cost and delivering value-added MBS to the customers (Shankar & Kumari, 2016). With mobile banking, consumers are always in control of their money—users can send or receive money worldwide regardless of location and time through a mobile handset. Mobile banking applications empower users to check their balance (account), get updates regarding new financial offerings, locate closed branches (bank) or ATMs, undertake transfers of funds and card payments, and repayments promptly, which truly allows us to enjoy 24 hr MBS (X. Chen & Wen, 2020). Consequently, the powerful nature of integrated m-banking solutions and services allows users to get connected with their finances throughout the year. Also, the capacity of m-banking can direct consumers to know and locate the next-door restaurants and shopping opportunities in their neighborhood.

Furthermore, the Industrial and Commercial Bank of China (ICBC), China Construction Bank (CCB), Bank of China (BoC), and Agricultural Bank of China (ABC) are dominant local banks that lead in the number of mobile banking users/subscribers in China. Other banks, such as Joint-stock banks (JSB), Urban Commercial Banks (UCB), and Rural Commercial Banks (RCB), have also increased their investment and promotion of mobile banking to attract more consumers. This has contributed to the growing number of mobile banking customers in China at a faster pace (G. Chen, 2019). All of these banks have integrated four types of business functions: First, the traditional online banking services which include services such as inquiry, account notification, consultation (financial matters), transfers and remittances, and payment options to m-banking. Second, payment services such as water, electricity, mobile phone fees, etc. Third, financial services such as timely deposits, deposit notices, funds, insurance products, etc. Fourth, business loan services such as mortgage, operation, decoration, educational loans, etc. Additionally, individuals can apply online to obtain funds or loans after it has been authorized online.

With the rapid development of third-party payment platforms, many businesses have integrated their financial transactions with mobile banking, which has affected the business development of physical banks. As a result, more Chinese banks are launching mobile banking services in China. However, the development of mobile banking in China has also revealed some challenges in the sector. These challenges include cumbersome procedures, limited promotion efforts, higher fees, concerns over personal information security, and privacy issues (Huang & Sun, 2020).

In recent years, the Chinese mobile banking industry has experienced significant growth. The outbreak of the COVID-19 pandemic further accelerated this growth by increasing the demand for “contactless banking” services in China. As a result, traditional bank operations, such as physical branches, have been impacted and the usage of mobile banking apps in China has continued to rise (Liu, 2020). The post-pandemic period has witnessed a significant shift in consumer behavior, with the increased integration of digital technologies into everyday life (C.-H. Lee et al., 2021; Tut, 2023). Data indicates that in the first quarter of 2020, ICBC’s m-banking applications/services were used by 68 million customers monthly (Statista, 2021). During the peak of the COVID-19 pandemic, the National Banking Regulatory Commission (CBIRC) of China directed Chinese banks and financial institutions to enhance their online and mobile banking operations/services (Statista, 2021). The policy directive drove an upsurge in the number of virtual and mobile banking users, which reached 241 million in 2020. This represents 13.6% of China’s total population (Statista, 2021). According to a CNNIC report, 700 million Chinese used the Internet in 2016, with 95% of them accessing the virtual system (internet) through mobile handsets/systems (CNNIC, 2017). As of July 2023, the number of mobile device subscribers in China reached 1.7 billion, with an estimated mobile internet penetration rate of 99.8% (Statista, 2023b). This indicates a high level of digitalization in the Chinese economy and society. In terms of m-banking, the number of active consumers has risen to 254 million, and the total transaction volume has reached 47 trillion Yuan in 2023 (Statista, 2023a).

UTAUT Model

Theoretical systems have been advanced to foretell the desires of people to accept technology. The UTAUT is the major theory regarding technology adoption (Venkatesh et al., 2003) which was initially established to understand the usage of technology in managerial (organizational) settings. It is considered more powerful in predicting consumer embracing of technology as it integrates other known models/theories that include the technology acceptance model (TAM), innovation diffusion theory, theory of reason action, social cognitive theory, PC utilization model, theory of planned behavior (TPB), motivational model, and joint TAM and TPB models. This makes it the most preferred theoretical foundation for most researchers since it empowers them to reach their research goals. These integrated models saw the UTAUT model performing superior as compared to other individual models (eight) with an r-square of 69% (Venkatesh et al., 2003).

The UTAUT proposes four major concepts: performance expectancy (PE), effort expectancy (EE), social influence (SI), and facilitating conditions (FC) that drive information system usage (Venkatesh et al., 2003). It is incorporated with moderating constructs such as age, gender, experience, and voluntariness (Venkatesh et al., 2003). These core constructs (PE, EE, SI, and FC) worked as antecedents of acceptance behavior among various people (Chang, 2012) and thus provided a strong basis for its continued validation in various research settings. The robustness and reliability of UTAUT is a key testimony to its application in diverse fields such as e-commerce/mobile payment (L. Chen et al., 2021; Widyanto et al., 2022), mobile banking (Hanif & Lallie, 2021; Ivanova & Kim, 2022), e-health/mobile health (Alkhalifah, 2022; Mina et al., 2023), etc. Additionally, UTAUT is extensively applied in connection with a diversity of technologies such as tax payment systems, hospital information systems, communication systems (instant messaging, automated feedback systems, and kiosk systems, etc.), the internet, mobile technology, and specialized systems like e-procurement, and e-voting systems along with the introduction of control elements like age, experience, gender, voluntariness to use, income and education (Venkatesh, 2022; Williams et al., 2015). Most of the focus groups in the application of UTAUT are in its diverse user segments like students, professionals, and general users of technology (Williams et al., 2015). Many new variables are integrated into the initial theory of UTAUT and mixed with other theoretical models. Sometimes the re-arrangement (extension and modification) of the fundamental interactions amongst UTAUT variables are tested (Al-Saedi & Al-Emran, 2021; Williams et al., 2015). For instance, extending the UTAUT model to elucidate the continuous usage intention of learning management systems (LMS) under the influence of learning tradition, it was shown that performance expectancy, e-learning self-efficacy, effort expectancy, facilitating conditions, and social influence had a positive effect on the continued use of LMS (Al-Adwan et al., 2022). Also, the same study validated that performance expectancy showed a partial mediating impact on the connection between effort expectancy and continued usage intention of LMS while self-directed learning and learning tradition had a negative influence on continued usage intention of LMS (Al-Adwan et al., 2022). Another research suggested an extended meta-UTAUT framework to examine the usage of chatbots in the service sector by the inclusion of perceived intelligence and anthropomorphism (system elements) in the model. The outcomes indicate that perceived intelligence and anthropomorphism are directly connected to attitude and continued intention usage of Chabot-based service than the known traditional meta of UTAUT variables (Balakrishnan et al., 2022). The study also showed that system factors are adversely linked to continuous usage intention when interacting with social self-efficacy (Balakrishnan et al., 2022).

These widespread testing and authentications of the UTAUT model via extension or modified versions of the original UTAUT provided the assurance and justification for its utilization in this research paper since its reliability and robustness can be guaranteed. Additionally, the UTAUT model is a cohesive hypothetical framework and if adequately planned and implemented within a research based on a robust statistical analysis, this framework can be instrumental in the development and promotion of the adoption and utilization of emerging technologies (Andrews et al., 2021) such as mobile banking services.

The modified UTAUT, upon which the hypotheses are developed in the next section, incorporates four new constructs: perceived financial cost, awareness, technology infrastructure support, and government regulations. In contrast, two variables, social influence, and facilitating conditions, have been excluded from the UTAUT to create a more succinct model that better measures the drivers of mobile banking adoption. The rationale for excluding these variables is that their influence can be captured and reflected in the added constructs of awareness, technological infrastructure support, and government regulations. Retaining the excluded variables in the proposed model would not provide additional value. This modified UTAUT offers a fresh perspective for scholars and researchers to explore when studying the drivers of technology adoption and diffusion, particularly in the context of mobile banking.

Hypotheses Formation

Performance Expectancy (PE)

PE is akin to the advantages users expect from the use of new technologies. It is considered as the magnitude to which using technology will deliver some beneficial outcomes to empower users to execute their jobs better (Venkatesh et al., 2003). PE is a vital predictor and antecedent of the behavioral intention to use (Basri, 2018; Sarfaraz, 2017). Consumers anticipate enjoying some form of fulfillment and pleasure when using a particular system (Wei et al., 2021). In the circumstance of m-banking PE measures people’s understanding that using m-banking services will empower them to perform better banking services and processes (Hanif & Lallie, 2021; Purwanto & Loisa, 2020). Additionally, mobile banking systems are designed to achieve higher performance expectancy in terms of faster funds transfer, quicker inquiries on accounts, saving time to undertake transactions, improved prompt response, ease of use, and cost savings, which attract more usage (Anene, 2021). The empirical studies have concluded that PE, in terms of the benefits of m-banking services, drives users’ behavioral intention to adopt MBS (Nasri, 2021; Savić & Pešterac, 2019; Wang, 2021). Consequently, H1 is advocated.

Effort Expectancy (EE)

EE is the extent of ease of use connected with the operation and use of information systems (Venkatesh et al., 2003). The concept is that the more ease and comfort attached to m-banking services, the greater the possibility that people will be attracted to use them for their banking services (Jadil et al., 2021; Savić & Pešterac, 2019). The ease of use (EE) of mobile banking systems makes mobile banking services digitally friendly and more accessible. It offers consumers a good user experience, such as creating user access and authorization that is both effortless and secure (Ali et al., 2023). Financial institutions, including banks, can offer some additional EE features in m-banking to attract potential users, including enhanced card control, budgeting tools, account opening, text banking, wearable widgets, and instant payments. Scholars (e.g., Marpaung et al., 2021; Saparudin et al., 2020) argue that the level of effort expectancy (complexity and ease of use) is significantly connected to people’s intention to use m-banking services (MBS). Based on this, H2 is proposed.

Awareness

Awareness creation is crucial for the diffusion of any technology-driven services such as MBS and it also plays an essential role in the success of widespread technology adoption. The bank customers’ awareness of MBS is directly related to the quantum of information they have about these services (Amin et al., 2008). M-banking awareness is the creation of knowledge of m-banking systems and services along with their benefits to the users concerned (Al-Somali et al., 2009; Saif Almuraqab, 2020). Similarly, consumers’ awareness of the availability of m-banking services is based on the level of information produced on the services (Amin et al., 2008; Khatimah & Halim, 2016). The lack of awareness and appreciation of the benefits associated with m-banking are barriers to m-banking adoption. The awareness creation can empower the consumer to go through processes such as product knowledge acquisition, persuasion, judgment, and final confirmation about a product before accepting the product or service of mobile banking (Sathye, 1999). Awareness campaigns by banks driven by practical actions and programs can empower the consumer to pick services that add the greatest value (N. Alkhaldi, 2017; Tiwari et al., 2021). It has been emphasized that knowledge formation about services or products among customers is an important step toward the execution of innovative services like m-banking (Tiwari et al., 2021). The more well-aware consumers are of the information about MBS services and their accompanying benefits, the more likely they are to make informed decisions to use such services. Hence, consumers’ awareness of m-banking services can have a significant influence on their usage intention of MBS (Tiwari et al., 2021). Accordingly, H3 is put forward.

Perceived Financial Cost (PFC)

Perceived financial cost refers to the extent to which individuals recognize that using MBS will involve a financial commitment (Shanmugam et al., 2014). The financial cost incurred by consumers when interacting with new information systems/technology can either discourage or encourage their level of usage and adoption. The availability of financial resources may drive users’ intention to use mobile technologies like m-banking (Huili & Zhong, 2011; Jeong & Yoon, 2013). The use of mobile banking services does not only depend on a good mobile handset (smartphones) but also on other equally important factors such as mobile data and wireless connections (Jeong & Yoon, 2013; Yang, 2009). Therefore, perceived cost accounts for resistance and reluctance to the acceptance of MBS (Cruz et al., 2010). Thus, individuals with good financial resources (able to pay for service fees) are more likely to use MBS compared to those with fewer resources. Consequently, if the cost of using MBS is reasonable and affordable then it will encourage more usage but if not then it will dissuade people’s active utilization of mobile banking. Studies have empirically validated that perceived financial cost is positively linked with the usage intention of MBS (Singh & Srivastava, 2018). Hence, H4 is proposed.

Technological Infrastructure Support

Technological infrastructure support is fundamental for IT systems to achieve sustainable outcomes. This involves aligning technologies, IT working practices, and communal services that can shape and sustain business application development (Croteau et al., 2001; Jabbouri et al., 2016). It includes issues such as connectivity, distributed computing, flexibility, consumer participation, and technology awareness (Croteau et al., 2001; Jabbouri et al., 2016). There is a need to provide adequate technical infrastructure support for consumers/users to adopt m-banking services (MBS) in a less challenging environment (Savić & Pešterac, 2019). Technological infrastructure goes beyond physical infrastructure but combines both physical and human (technical knowledge and expertise) capital to support a firm’s business activities (Chituc & Azevedo, 2007; Vedovello & Godinho, 2003). It also integrates other segments like captivation and diffusion of key business information and offers support on issues concerning organizational and managerial procedures (Vedovello & Godinho, 2003). Broadly technological infrastructures may cover (a) process mechanisms that deal with service-connected activities developed by firms; (b) process mechanisms that deal with organizational arrangements by new departments, and; (c) output results concerning the performance of developing business activities (Vedovello & Godinho, 2003).

Mobile banking services (solutions) based on sound technological infrastructure support can facilitate banks to provide innovative mobile banking services in areas such as account security alerts, customer service, account balance updates and history, ATM and branch whereabouts, electronic bills (domestic and international funds transfer), insurance and pension policy management, mortgage alerts and blocking of lost bank cards, etc. (Lacmanovic et al., 2012). Banks’ utilization of the right technological infrastructure will bolster consumer confidence in their mobile banking capacity to deliver to meet the expectations of consumers. This study thus proposed that based on the nature of the technological infrastructure that banks use to develop their m-banking systems will influence people’s usage intention, adoption, and performance expectancy of m-banking services (MBS). Consequently, H5, H6, and H7 are put forward.

Government Regulations

Government regulations are effective mechanisms instituted by a government or its agency that define the boundary of legal behaviors (Cummins, 2010; Noll, 2021). The government controls banks or other financial institutions through policies and regulations to determine the nature of what they can legally do or can’t do to perform their business activities. Policy and regulations provide some form of consistency in business operations/practices and compliance with regulatory demands/requirements (Cummins, 2010; Meng et al., 2022). Regulations being a key aspect of knowledge and control demonstration can drive/enforce a body of requirements ranging from the configuring of complex products to discovering a design defect (Cummins, 2010). It also impacts banks’ administration and operations along with other financial institutions by heightening monitoring and vigilance to the protection of government, financial bodies, and vitally the consumer’s interests. Therefore, mobile banking needs transparent and clear regulations and laws to protect the confidentiality and safety of individual personal records and reduce the likelihood of them being misused (Aithal, 2015). Mobile banking regulations may be based on these five standards and principles: consumer protection, legally enforceable contracts, data privacy (reduce unauthorized data access), data confidentiality (avoid misuse of data), and right to self-determination (reject or accept communication) (Aithal, 2015). Sufficient government policy and regulations in the banking sector particularly in the advancement and diffusion of MBS provide some confidence to the consumer that they will be protected when something goes wrong. The protection offered by the government via laws and regulations of mobile banking transactions creates a positive effect on users’ attitudes and behaviors regarding MBS since it will increase the expected benefits and trust of using such MBS (AlGhamdi et al., 2012; Purwanegara et al., 2014). This confidence through the right regulations on mobile banking systems does empower consumers to harbor the usage intention and mobile banking services (MBS) adoption. Hence, H8 and H9 are accordingly suggested.

Usage Intention

The individual’s aspiration to participate in a particular course of behavior is termed as behavioral intention or usage intention (Misra et al., 2022). Behavioral intention encourages behaviors that drive an individual’s acceptance and adoption of technological innovations (Misra et al., 2022). It is considered an important construct especially in the context of technology adoption models to measure the intention and actual behavior of consumers (Abubakar & Ahmad, 2013; A. U. Rehman et al., 2022). The examination of the users’ intention offers appropriate signals concerning the behavior of users which may contribute to changes in intention and actual behaviors (Misra et al., 2022; A. U. Rehman et al., 2022). For example, the behavioral usage intention is linked to the desire of users to accept mobile banking services (Morales & Trinidad, 2019). Intention is a crucial compartment for actual usage and serves as a proxy to determine actual behavior (Awwad & Al-Majali, 2015). Research supports the assertion that when users develop the desire to use an information system like m-banking services, they eventually adopt such services (Ivanova & Kim, 2022; Jadil et al., 2021). Accordingly, H10 was proposed.

Conceptual Research Model

The investigated model is grounded on the hypothesis developed in the preceding segments (Figure 1).

Conceptual research model.

Method

This study aims to understand the nature of MBS among Chinese citizens. We used an adapted scale (questionnaire) to collect data for analysis, including performance expectancy, effort expectancy, and usage intention scales (Malaquias & Silva, 2020; Wei et al., 2021), awareness scale (Laukkanen & Kiviniemi, 2010; Mutahar et al., 2018), perceived financial cost scale (Cruz et al., 2010), technological infrastructure support scale (Jabbouri et al., 2016; Kilani, 2020), and a self-developed government regulation/policy scale. Items in the questionnaire were measured using a five-point Likert scale: strongly disagree (1) to strongly agree (5). The questionnaire was converted into the Chinese language to guarantee that respondents could resonate with the content of the instruments and provide appropriate, meaningful responses. Additionally, we pre-tested the instrument and conducted a pilot study with 30 respondents to improve the respondent comprehension ability and data quality (Collins, 2003; Geisen & Murphy, 2020). However, data collected from the experimental (pilot) study was not incorporated into the final data analysis due to their small nature and inability to statistically influence the conclusions and interpretation of the main study.

Since the researchers could not determine the exact information in terms of the total number of people (Hu et al., 2022) within the targeted population of the study (Jiangxi University of Science and Technology and its environs), we applied a convenient sampling framework to approach respondents for data collection. Convenient sampling is relevant since a researcher cannot connect with every member of a chosen population for a study (Buntin, 2020; Etikan et al., 2016). Additionally, it is quick, easy, less time-consuming, inexpensive, and less challenging compared to other sampling approaches. Based on information gathered from the convenient sample, an appropriate reference can be made for the population concerned (Cornesse et al., 2020; Ragab & Arisha, 2017).

The populations of the study include teaching staff, students, and other administrative staff within the premises of Jiangxi University of Science and Technology (JUST) located in Ganzhou, Jiangxi Province of China. We placed our questionnaire on a Chinese online survey software—Questionnaire Star (问卷-wènjuàn xı–ng) for 2 months—from October to November 2021. The link to the questionnaire was shared via social media platforms such as WeChat—a popular social media platform in China. We used individuals’ social media moments/posts, and students, faculty, and non-faculty members’ social media groups to disseminate the questionnaire in JUST and requested the participants to complete and share it with their friends and colleagues. WeChat was utilized as a medium to research the respondents because it provided readily available respondents who were easily accessible.

The questionnaire was designed in such a way that no respondents could submit their responses without completing all research items. We obtained a total of 567 valid responses, which were deemed suitable for analysis. This is because it exceeds the minimum sample size of 381, as calculated using the following indicators: confidence interval (95%), margin of error (5%), population proportion (50%), and estimated population size (40,000; calculator.net, 2023).

Data Analysis

We use Statistical Package for Social Science (SPSS–26) for data analysis and apply multiple linear regression tests to confirm the proposed hypotheses. The exploratory factor analysis (EFA), Composite Reliability (CR), Cronbach’s alpha (CA), and Average Variance Extracted (AVE) tests are also conducted to validate the scale constructs and assess their reliability. Additionally, we applied descriptive statistics and Pearson correlation analysis to examine the interaction between the study’s constructs.

Common Method Bias

This study uses a self-report-survey to test the hypotheses, and therefore, Harman’s single-factor analysis (HSFA) was used to check the CMB (common method bias) in the study. HSFA test extracted a total of 39.879% variance for a single factor, which is well within the limits of the required 50% threshold of the aggregate variance. Additionally, the correlation between variables is also well below the threshold of r > .90 (Podsakoff et al., 2003) (Table 1). Hence, we did not find any evidence of CMB in this study.

Descriptive Statistics.

***p < .001. **p < .01.

Demographics

The study involves a total of 567 participants, of which the majority are female (n = 310, 54.7%), while the remaining 257 participants (45.3%) are male. Most of the participants are young adults aged 18 to 30 (n = 461, 81.3%), whereas only a small proportion of respondents belong to the age group of 41 and above (n = 24, 4.3%). The participants mainly comprise college and undergraduate students (n = 462, 81.5%), with a smaller portion being master’s and doctoral students (n = 80, 14.1%). Additionally, 25 participants (4.4%) have technical education. Moreover, the vast majority of respondents (n = 529, 93.3%) have bank accounts in China, while only a small proportion of respondents (n = 38, 6.7%) do not have any bank accounts.

Results

Descriptive Statistics

As shown in Table 1 (descriptive statistics) indicate a robust correlation between the studied items, including Performance Expectancy (PE), Effort Expectancy (EE), Awareness (AW), Perceived Financial Cost (PFC), Technical Infrastructure Support (TIS), Government Regulations (GR), Intention to Use Mobile Banking (IUMB), and Adoption of Mobile Banking (AMB). Additionally, the mean and standard deviation of the variables are in the study direction.

Reliability Analysis

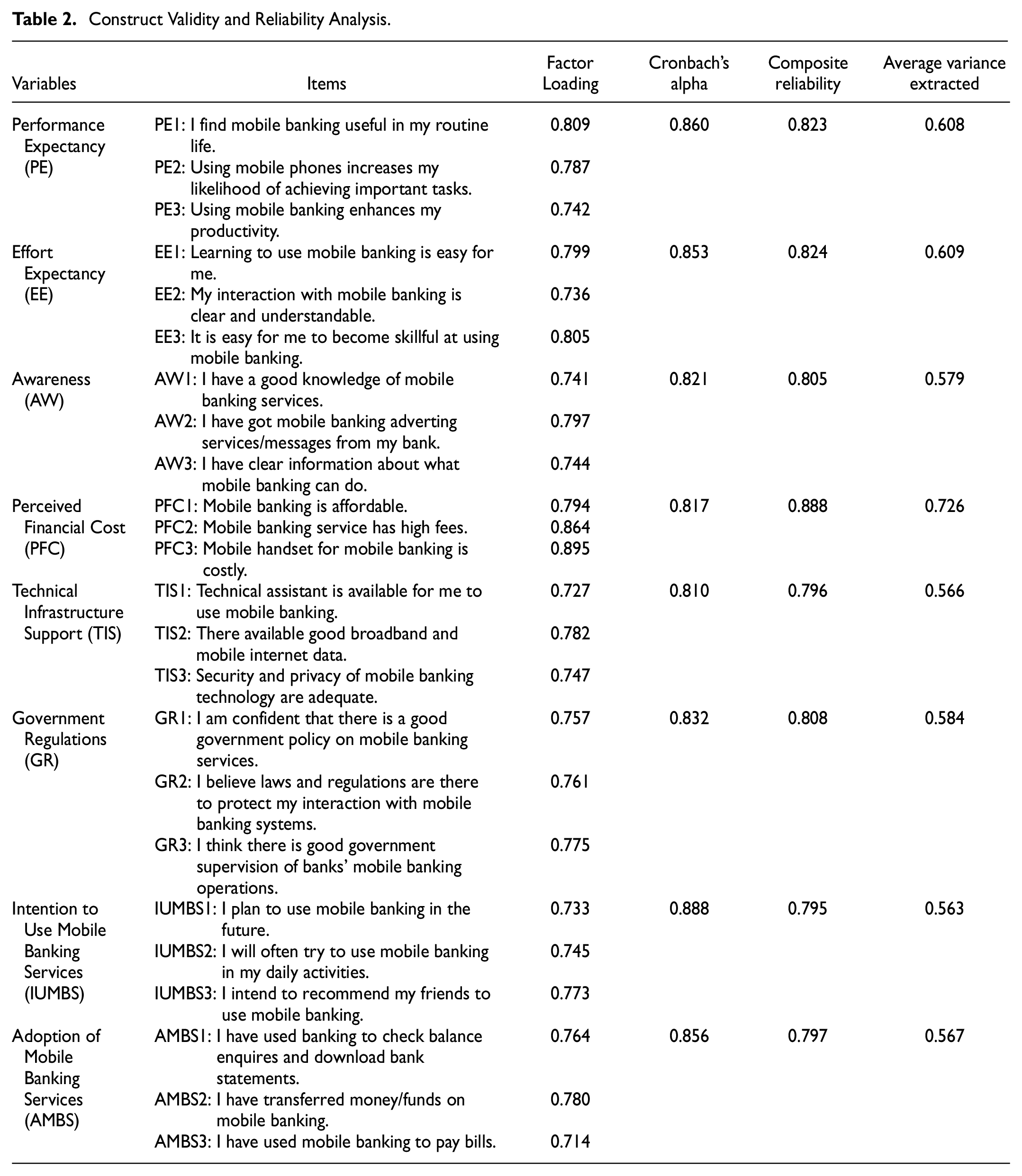

To confirm the reliability and validity of the scales used in this study, we utilized multiple tests, including exploratory factor analysis (EFA), composite reliability (CR), average variance extracted (AVE), and Cronbach’s alpha (CA). Firstly, we applied EFA (principal component method) to extract the possible factor loadings (FL) for each variable’s items. Then, we used CA, CR, and AVE to assess the validity and reliability of the study’s variables. The results indicate that all the tests (EFA, CA, CR, and AVE) align with the standard threshold values. That is factor loading <0.600; CA and CR = 0.700 or above; and AVE < 0.500 of variance (Hair, 2011) (Table 2).

Construct Validity and Reliability Analysis.

Regression Analysis

We used multiple linear regression tests to confirm our proposed research model (H1-H10). H1 hypothesized that performance expectancy is positively associated with the behavioral usage intention of mobile banking services (MBS). Results indicate a positive relationship between performance expectancy and the intention to use MBS (β = .265, p < .001) in China, thus supporting H1. H2 hypothesized that effort expectancy is positively associated with the behavioral usage intention of MBS. However, results indicate a positive but relatively weak relationship between effort expectancy and the usage intention MBS (β = .069, p < .10) in China, partially supporting H2.

Results support H3, which hypothesized a positive relationship between awareness and the usage intention of MBS (β = .110, p < .01). Similarly, results also support H4, which indicates a positive connotation between perceived financial cost and the usage intention of MBS (β = .070, p < .05). Furthermore, H5, H6, and H7 hypothesized positive associations between technological infrastructure support (TIS) and the usage intention of MBS (H5), the adoption of MBS (H6), and the performance expectancy of MBS (H7) in China. Results confirm support for H5, H6, and H7, indicating that technological infrastructure support is positively associated with the behavioral usage intention of MBS (β = .178, p < .001), the adoption of MBS (β = .153, p < .001), and performance expectancy of MBS (β = .395, p < .001) in China.

H8 and H9 hypothesized positive associations between government regulation and the usage intention of MBS and the adoption of MBS in China. Results confirm that government regulation is positively connected to the intention to use MBS (β = .262, p < .001) and the adoption of MBS (β = .150, p < .001) in China. Finally, results also support H10, which hypothesized that the behavioral usage intention of MBS is positively connected with the adoption of MBS (β = .516, p < .01) (Table 3).

Regression Analysis.

***p < .001. **p < .01. *p < .05. †p < 0.10.

Discussion

The advent of new information technologies in the banking sector has empowered banks to leverage this powerful tool to improve services delivered to consumers. One of the innovations resulting from mobile technology integration into the banking sector is MBS. While mobile banking developments are a good initiative from banks, their corresponding acceptance and adoption by consumers are needed to achieve a maximum outcome from the investment in mobile banking technological systems. This paper thus realizing the role consumers play (readiness to use/adopt) in the success of m-banking systems, set out to examine the factors that drive users to accept and use mobile banking services (MBS) from the Chinese citizen perspective. The results provide crucial insights for e-commerce and mobile banking practitioners since they can empower them to devise strategies and campaigns to retain mobile banking customers and promotion of mobile banking services for individual non-users. Ultimately, knowing the driving forces behind mobile banking acceptance and usage can drive the design and execution of strategic policies to enhance m-banking services.

The results discovered that fundamental constructs from the UTAUT model that is, performance expectancy and effort expectancy both had a direct significant influence on the usage intention of MBS. The positive influence of PE on the usage intention of MBS demonstrates that mobile banking systems that are carefully designed to have user-friendly and advanced benefit features will encourage users to use them. Banks should ensure the performance and quality enhancement of mobile banking systems for individual performance if they are to retain and attract potential mobile banking users. The positive influence of PE on usage intention corresponds to studies that have also reported the same findings that mobile banking’s usefulness drives its usage (Ivanova & Kim, 2022; Khan et al., 2022; Wang, 2021).

Regarding the effort expectancy of m-banking systems, MBS should be designed with ease to comprehend and use by individual consumers to increase the benefits in terms of efficiency in undertaking financial operations at the bank. That is the design and processes of m-banking should be simple and easy to comprehend to make transactions on mobile banking easier without wasting time on learning how to operate and use it. Also, banks can utilize special consumer experiences and individual user interface systems to entice customers from diverse age-groups. Our findings are consistent with some studies that effort expectancy influences consumers to use MBS (Mer & Virdi, 2023; Nasri, 2021). However, it also contradicts the findings that performance and effort expectancy do not drive the usage intention of MBS (Angelia et al., 2021).

Furthermore, the study demonstrated that consumer awareness concerning mobile banking services influences the usage intention of MBS. This implies that the nature of awareness creation by banks could have the potential to directly impact their consumer base to sign up for MBS as compared to traditional banking services. This can help in reducing walk-in banking services and easing pressure on the banking staff and facilities, especially in a situation like COVID-19 (where limited gathering/contact is encouraged). Mobile banking services may be new to some consumers and bank operating areas, especially the unbanked population, and thus much publicity/awareness is required to capture the people’s attention. Awareness can be created by banks via promotion tactics such as educating the public and engaging in sensitization programs that provide motivations for consumers who may act as recommenders of MBS to friends, family, and colleagues and thus contribute to the spreading of information about MBS. This can also be done through the use of celebrities and influencers in society (disseminating valuable information about MBS) to drive awareness of mobile banking services among consumers through advertising campaigns. Mobile banking promotions should regularly emphasize the advantages (benefits) of mobile banking systems and their related functions effectively. Additionally, banks can utilize social media influencers to promote and create awareness about mobile banking services through the creation of positive eWOM (electronic word-of-mouth) communications. The direct influence of awareness on the intention to use MBS substantiates other studies that also displayed the same findings that awareness creation leads to the intention to use new technology (Almaiah et al., 2019; Ammar & Ahmed, 2016; Khazaei, 2020). It has also been elaborated that adequate awareness creation reduces consumers’ resistance and perceived risk of technology and is consequently instrumental in driving and attracting new users (Siyal et al., 2019).

Additionally, the perceived financial cost of the use of MBS is significant in driving the intention of consumers to use MBS. This means that the consumers are ready to pay for a new technology system that can empower them to attain maximum efficiency and effectiveness of MBS consumed. This is in line with past studies that the cost incurred by consumers has a positive effect on the desire of people to use MBS (Cudjoe et al., 2015; Twum et al., 2022). It rather contradicts the findings that pricing/financial cost does not drive the intention to use mobile banking (Bhatiasevi, 2016; Malaquias & Silva, 2020).

Furthermore, technological infrastructure support is significant in driving usage intention, adoption of m-banking, and performance expectancy of MBS. This suggests that banks’ acquisition of the right technological innovations in the development of m-banking systems can send a tough signal to consumers and thus higher patronage will be recorded. Banks should invest in new emerging technologies such as AI, cloud, and cyber-security to ensure they can introduce new products and services, and enhance consumer experiences and efficiencies in their operations. The transformation empowered by good technological investment can lead banks to shift their focus from a product-centric to a customer-focused culture. These technologies should ensure that customers can access banking services and information from anywhere and at any given time, improving consumer productivity and user experience. Also, physical security is an important aspect that banks can invest in, to ensure the protection of hardware, software, personnel, and data from any actions that could cause serious damage to the technological innovations of banks and thus lead to disruptions in the provision of MBS.

Additionally, government regulation significantly drives the usage intention and actual adoption of MBS. Our finding is similar to a past study that demonstrates government support as an influential element in driving the acceptance of MBS (Ammar & Ahmed, 2016). Banking industries should adhere strictly to government policy and regulations for the banking sector to provide confidence to the consumer in their services. The government could promulgate the required protocols to guide the operation of mobile banking systems to protect consumers’ investments, especially to guide against fraud in the virtual internet environment.

Lastly, this paper showed that the usage intention is linked positively to the acceptance behavior of MBS. This places lots of responsibilities on banks to utilize all available resources to provide adequate information to the consumers (through publicity- traditional and social media) about MBS. With this, banks can attract consumers and cultivate a higher desire to use MBS, which may account for their actual adoption. The positive influence of usage intention on adoption behavior corroborates other research findings that consumer intention leads to actual adoption tendencies (Purwanto & Loisa, 2020).

Theoretical Implications

The continuous validation of the UTAUT model provides a fundamental basis for its continued utilization in IT and IS research to explain user adoption behaviors in varied fields of study. Its current application in the circumstance of MBS contributes to a better understanding of the UTAUT model in providing drivers of MBS acceptance from the Chinese standpoint. The modified UTAUT that saw the integration of awareness, perceived financial cost, technological infrastructure support, and government policy guidelines along with core constructs of UTAUT such as performance expectancy and effort expectancy contribute substantially to the literature on e-commerce and mobile commerce. First, jointly these factors (awareness, perceived financial cost, technological infrastructure support, government policy guidelines, performance expectancy, and effort expectancy) account for 53.9% of the variance toward behavioral usage intention of MBS. Secondly, the usage intention, technological infrastructure support, and government regulations accounted for 56.2% of the variance toward the consumer acceptance of MBS. Thirdly, the technological infrastructure support construct accounted for 23.7% of the factors driving the performance expectancy of MBS. These discoveries are exceptional to this study and consequently provide the basis for researchers to expand the model in the framework of UTAUT to explain the utilization of technology innovations like mobile banking systems.

Practical Implications

The decision-makers, marketers, and IT designers in charge of the deployment of m-banking services should develop m-banking applications that consumers can resonate with. Mobile banking services should meet the maximum output expectations of users in terms of active availability of 24-hr services and efficiency. Efficiencies in checking account balances, consumer data updates, and history, information on ATM branches, payment of bills, and funds transfer (local and international). Mobile banking should have easier-to-use features such as easy upload and download of data/information, faster navigations between web pages, and easily reachable contacts for support. Banks must constantly develop consumer-friendly products and services, systems of delivery, easy and accessible services, and competitive pricing regimes.

Furthermore, Banks should develop a strategy to generate adequate publicity and awareness of MBS to their consumers and the public in general. Banks can depend on social media innovations to better reach consumers about their mobile banking services. Social media provides cheaper costs and strong targeting capabilities and thus an effective way to deliver mobile banking awareness creation to customers. Banks should empower their customer service department personnel with the right tools to help promote mobile banking services to customers. Banks and financial institutions should use multiple targeted communication channels (i.e., mass and interpersonal) to increase the acceptance rate of MBS among consumers especially in rural regions.

More so, banks should deploy the latest and safest mobile banking technological systems if they are to attract higher penetration of usage. The deployment of the right mobile technology in the banking industry can improve reputation and consumer service, reduce cost serving, easy to integrate into current Internet banking services, generate comfort for consumers with mobile systems, and encourage in-house experience and capacity building. Technological infrastructure support can provide consumer satisfaction by reducing the threats in MBS such as cloning (copying the identity of a mobile phone to another), hijacking (where intruders size control of messages between two parties), malicious codes (viruses), malware, phishing (tricking) and spoofing, etc. All these benefits of utilization of adequate technological support will translate into driving consumers to have confidence and thus will be drawn to use MBS.

In addition, the huge role the actions of the government in terms of policy and regulations can play in driving the acceptance of MBS and its success should not be downplayed. The success of any financial system such as MBS hinges on the capacity of the government to make the right policy regulations to guide not only the implementation of such a system but chiefly to protect consumers and investors alike. Government policy for instance can determine the service charges (cost) that banks can charge on their mobile banking services. Proper government regulation can ensure the strengthening of bank supervision/oversight to achieve a diversified stronger banking system. A stronger banking system as a result of adequate government regulations provides a baseline for people to trust the banking systems in place like mobile banking services and thus will be much attracted to using it. Additionally, public policy to regulate the banking sector can be in areas of anti-money laundering, countering terrorism financing, consumer protection, payment systems, data privacy and security, and taxation.

Furthermore, banks should engage in co-creation systems that provide incentives to consumers to sign up for mobile banking services through the introduction of reduced charges. Ultimately, this implies that managers should engage in the productive co-creation of banking processes that can generate and co-create value between consumers and the banking industry. Managers/firms and consumers should engage in productive collaboration to create value given the competitive banking environment, higher rate of internet penetration, and highly motivated consumers, empowered and connected digitally. Also, this can be fundamental for organizations to sustain a future competitive advantage based on a co-creation system between consumers and organizations. Moreover, firms’ engagement in co-creation processes can ensure that they generate and develop value with consumers, rather than for them which has a beneficial outcome for both banking sector firms and consumers. It is thus vital for firms to get involved in co-creation with customers if they are to harvest financial rewards from it. For instance, banks can invite customers to take part in the development and planning (brainstorming) sections when designing and creating mobile banking services via smartphone systems or websites. Also, actively engaging the consumer in the co-creation process can influence the consumers’ appreciation of the compatibility of m-banking innovations. There is no doubt that adequate collaboration and involvement of consumers in the co-creation process/activities can drive people’s attitudes toward the usage intention of MBS and consequently, their actual adoption of MBS.

Finally, the economic and commercial impact of developing sustainable mobile banking systems could be instrumental in creating sustainable socioeconomic development and financial inclusion for the unbanked population especially for people in rural communities. Its social and economic impact may be felt in areas of job creation, business, savings behavior, remittance, expenditure, reduced economic inequality (i.e., creating growth for opportunities for rural poor and thus diminishing the rural-urban divide), and agriculture development. Financial inclusion can further promote inclusive growth and increase a country’s GDP and thus the key to economic empowerment and solutions to rising poverty standards.

Limitations and Future Work

The model and approach used in this paper may be applied in other studies but their results may not correspond to the discoveries reported in this article. Thus, restraint should be applied in the elucidation and generalization of the results. Also, many factors drive the acceptance of MBS but the finding of this study is not exhaustive on the factors influencing consumers’ decision to use MBS, especially, when this study is limited to the Chinese environment. Future works would be based on the utilization of the structural equation model (SEM) to better analyze the direct and indirect effect of the modified model considered especially (i) the mediating/moderating role of technological infrastructure support between behavioral intention to use m-banking services and adoption of m-banking services, and (ii) the mediating/moderating role of government regulations between behavioral intention to use m-banking services and adoption of m-banking services. Additionally, future research is required to explore other elements such as the role of Chinese guanxi (relationship) characteristics such as mutual understanding, relationship harmony, and reciprocal favors in driving the adoption of MBS. Additionally, it would be important to examine the role of sustainability and digital transition processes in the design and circulation of m-banking systems. Especially, the contribution of digital transition to environmental, economic, and social sustainability dimensions since digital transformation in the banking sector is an ongoing process that influences both the external and internal environment. Digitization in the banking sector could drive the implementation of effective policies to protect public interests.

Conclusion

This paper examined the adoption behavior of MBS among Chinese citizens based on a modified UTAUT. The results show that performance expectancy, effort expectancy, and awareness play a key role in the acceptance of MBS among both new and existing consumers. Additionally, banks should utilize the most advanced technological infrastructure support since it drives both the usage intention and the performance expectancy of MBS. The government through its policy regulations can influence and guide the implementation of m-banking systems since it will boost consumer confidence and trust in the banking systems and thus people will be encouraged to use it. This paper through its findings provides policymakers and stakeholders in the financial and mobile banking industry clues to help design and implement mobile banking regimes that will lead to maximum adoption among the people particularly for the unbanked populations. Financial institutions including banks should implement robust mobile banking systems and strategies to encourage the stimulation of greater financial inclusion to reduce economic inequality between rural and urban populations.

Footnotes

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.

Data Availability

Data will be available on request.