Abstract

In 2016, the People’s Bank of China (PBC) together with multiple departments issued the Guidance on Building a Green Financial System (the Guidance), which marked a great breakthrough in China’s green finance policy. Aiming to clarify the actual impact and underlying mechanisms of green finance policy on Chinese listed companies’ ESG disclosure quality, this study employs the difference-in-differences (DID) model and examines the impact of the Guidance on ESG disclosure practices of A-share listed companies on the Shanghai Stock Exchange (SSE) and the Shenzhen Stock Exchange (SZSE) during the period 2006 to 2022. This study reveals a positive correlation between the Guidance and listed companies’ ESG disclosure. Upon further examination, it becomes evident that the Guidance has a more noticeable positive impact on the quality of ESG disclosure among listed companies that operate in industries with high levels of pollution, state-owned enterprises, and regions that exhibit greater levels of economic development. This paper provides essential insights to policymakers, facilitating a deeper understanding and more thorough assessment of the economic implications of green finance policies. Additionally, it acts as a strategic resource for listed companies, guiding the enhancement of corporate ESG disclosures and the implementation of ESG strategies influenced by green finance policies.

Plain Language Summary

To clarify the impact and mechanism of China’s green finance policy on improving listed companies’ ESG disclosure, this paper treats the introduction of the Guidance as a quasi-natural event and employs the DID method to examine how the Guidance influence listed companies’ ESG disclosure. In 2016, the issuance of the Guidance leading by the PBC marked China as an early adopter of a relatively comprehensive green finance policy system, placing it among the forefront of global economies. The Guidance has put forth a proposal for the implementation of a gradual and improved mandatory system for listed companies’ environmental disclosure Our findings indicate that the issuance of the Guidance improves ESG disclosure quality among listed companies. In addition, this effect is amplified in highly polluting industries, state-owned enterprises, and economically advanced regions.

Keywords

Introduction

China has incorporated sustainable development strategies into its long-term development plans since the turn of the 21st century. From the 15th to the 20th, the National Congress of the Communist Party of China (CPC) respectively elaborated “the implementation of sustainable development strategy,”“must put sustainable development on a very prominent position,”“building ecological civilization,”“vigorously promoting the construction of ecological civilization,”“accelerating the reform of the ecological civilization system,” and “promoting the harmonious coexistence between human and nature,” which achieved layer by layer progressive leap of the economic, social and ecological harmonization from the concept to the system. Meanwhile, with the increasing openness of China’s capital market, more and more international investors adhering to the green and responsible investment philosophy have started to participate, which has promoted the further recognition of ESG investment principles in China. However, under the “top-down” guidance model, Chinese listed companies seem to be hesitant to execute ESG responsibilities and lack the internal drive to enhance ESG performance (Ruan & Liu, 2021). While few Chinese listed companies regularly release comprehensive ESG reports, their disclosure quality also varies, which limits timely and efficient communication between listed companies and stakeholders (S. Kim & Yoon, 2023; X. Wu & Hąbek, 2021). To sum up, doubts remain regarding whether China’s green finance policy can boost listed companies’ ESG disclosure.

To clarify the impact and mechanism of China’s green finance policy on improving listed companies’ ESG disclosure, this paper treats the introduction of the Guidance as a quasi-natural event and employs the DID method to examine how the Guidance influence listed companies’ ESG disclosure. In 2016, the issuance of the Guidance leading by the PBC marked China as an early adopter of a relatively comprehensive green finance policy system, placing it among the forefront of global economies. The Guidance has put forth a proposal for the implementation of a gradual and improved mandatory system for listed companies’ environmental disclosure Our findings indicate that the issuance of the Guidance improves ESG disclosure quality among listed companies. In addition, this effect is amplified in highly polluting industries, state-owned enterprises, and economically advanced regions.

Our research may contribute to the following aspects. First, this paper contributes to the existing research on the economic implications of green finance policy. Previous studies related to green finance policy’s effects have primarily examined its macro-level impact, while neglecting the analysis of its influence on micro-organizational behavior, this study explores how Chinese green finance policy’s issuance influence listed companies’ ESG disclosure, which is an essential and interesting topic. Second, this study extends the discussion of sustainability disclosure from an integrated perspective. Previous literature has demonstrated research accomplishments regarding the relevance of individual disclosures to the “E,”“S,” or “G” dimensions of “ESG.” In contrast, this study adopts a comprehensive approach by considering the interconnectedness of “E,”“S,” and “G” in evaluating ESG disclosure, representing a significant breakthrough and novel attempt. Third, this study extends the exploration of impact mechanisms by analyzing the heterogeneous effects of green finance policy according to industry attributes (heavily and non-heavily polluting industries), ownership nature, and local economic development levels. This analysis not only deepens our understanding of the impacts of green finance policies but also provides valuable insights for policymakers and crucial guidance for publicly listed companies to enhance corporate ESG disclosures.

The subsequent sections are organized in the following manner. Section 2 offers an overview of the institutional background that led to the issuance of the Guidance. Section 3 conducts a comprehensive review of relevant literature. Section 4 explores theory derivation and hypothesis development. Section 5 presents the research sample, data sources, variable definitions and model settings. Section 6 presents the primary empirical findings. Section 7 conducts heterogeneity tests. Section 8 summarizes the research findings and discusses their policy implications.

Institutional Background

China’s Green Finance Policy

Since the inception of the initial environmental protection policy bank, commonly referred to as “Eco-bank,” in 1974, there has been a notable surge in endeavors to synchronize economic, social, and environmental dynamics through financial policy transformations. This momentum has been further propelled by the introduction of the Equator Principles in 2002, a collaborative effort between the International Finance Corporation (IFC) and ABN AMRO Bank (Lian et al., 2022). The evolution of green finance policy in China can be categorized into three distinct phases (Z. F. Liu et al., 2019). The initial phase can be identified as the formative era of green finance policy (1995–2006), commencing with the promulgation of the Notice on Implementing Credit Policy and Enhancing Environmental Conservation by the PBC in 1995. The keyword for the second phase is development (2007–2011), which was initiated in 2007 through the issuance of two circulars by the China Banking Regulatory Commission (CBRC). These circulars are titled “Guidance on Crediting for Energy Conservation and Emission Reduction” and “Circular on Preventing and Controlling Loan Risks in High Energy-Consuming and Highly Polluting Industries.” The third stage signifies the maturation of policy, spanning from 2012 to the present era. The Green Credit Guidelines were issued by the CBRC in 2012 (Chen et al., 2022). In 2015, the CPC Central Committee and the State Council issued the General Plan for the Reform of the Ecological Civilization System (Y. Zhao et al., 2019), which put forward a general framework for establishing a green financial system. In the year 2016, the Guidance was formulated, which outlined a comprehensive framework for the advancement of green finance. This development marked a notable milestone in the realm of Chinese green finance policy. In the year 2019, the Green Industry Guidance Catalog (2019 Edition) was jointly issued by China’s National Development and Reform Commission (DRC) and six other ministries and commissions. This catalog highlights the significance of prioritizing the development of green industries. Two years later, these two departments issued the “Opinions on Completely and Accurately Implementing the New Development Concept and Performing the Work of Carbon Peak and Carbon Neutrality,” which proposed to help eligible enterprises realize low-carbon transformation and expand the scale of green bonds (L. L. Sun et al., 2022).

ESG Disclosure Regulation for Listed Companies in China

China’s capital market has experienced significant growth and development since 1990, spanning a period of three decades (Kathiravan et al., 2021). Meanwhile, China’s capital market has been continually strengthening its role as an “economic development barometer,” deepening its two-way opening and enhancing the level of market openness. The regulatory trajectory of ESG disclosure in China’s capital market can be delineated into three distinct phases: a period of voluntary disclosure preceding 2008, a transitional phase characterized by a blend of voluntary and mandatory disclosure spanning from 2008 to 2015, and a subsequent phase marked by mandatory disclosure from 2015 to nowadays (X. Huang et al., 2021). The Notice on the Work of 2008 Annual Reports of Listed Companies was jointly issued by the SSE and the SZSE in December 2008 (Han et al., 2019), requiring companies included in the SSE Corporate Governance Index, companies that issue foreign shares listed overseas and financial institutions to issue their CSR reports in conjunction with annual reports. Meanwhile, the SZSE 100 Index mandated that listed companies disclose CSR reports and also encouraged others to follow. The Code on Governance of Listed Companies was issued by the China Securities Regulatory Commission (CSRC) in 2002, marking the first instance of explicit clarification regarding the social responsibility of listed companies (H. Sun et al., 2022). The Integrated Reform Plan for Promoting Ecological Progress, released by the CPC Central Committee and the State Council in 2015, introduced the concept of a compulsory disclosure mechanism for the environmental information of publicly traded companies (L. Tang et al., 2022). The Code on Governance of Listed Companies was revised by the CSRC in 2018, thereby establishing a framework for listed companies’ ESG disclosure, also marking the initial implementation of ESG disclosure practices in the country (Ruan & Liu, 2021). The Guidelines on Investor Relations Management for Listed Companies were issued by the CSRC in 2022. This issuance marked the initial inclusion of ESG disclosure within the realm of investor relations management. The implementation of a regulatory framework to enforce listed companies’ compulsory environmental disclosure is now progressing rapidly (Du et al., 2022).

To conclude, the Guidance places significant emphasis on the crucial role played by the securities market in promoting and facilitating green investment. It advocates for the establishment of standardized criteria to define green bonds, actively supports the listing and refinancing of eligible green enterprises and aims to facilitate the development of green financial products. Furthermore, it aims to gradually establish and enhance a mandatory system for listed companies to make environmental disclosure. The green finance system imposes specific requirements on ESG disclosure in the securities market (H. B. Wang et al., 2022). Therefore, it is of great value for policymakers, listed companies, and investors to investigate how China’s green finance policy influences listed companies’ ESG disclosure.

Literature Review

Effectiveness of Green Finance Policy

Green finance policy may exhibit solid spatial agglomeration and spillover effects (G. Xu et al., 2022). It has the potential to promote environmentally friendly initiatives and facilitate high-quality development (Feng et al., 2022; Y. Liu et al., 2021). Additionally, it can effectively mitigate environmental pollution and address climate change challenges (K. Q. Zhang et al., 2022), optimize ecological environment (Ge et al., 2022), enhance energy efficiency (Peng & Zheng, 2021), support industrial transformation and upgrading (Xiong & Sun, 2022), foster the ecologization of industrial composition (Meng, 2021) and improve industrial structure (L. Gao et al., 2022) Moreover, it can boost innovation capacity (X. Li & Yang, 2022; T. Zhao et al., 2022). Nevertheless, how green finance policy impacts at the at the corporate level remains uncertain. Several scholars have noted a positive linear correlation between green finance policy and corporate environmental performance (Abbas et al., 2021). However, an alternative perspective suggests the relationship between green finance policy and corporate efficiency is U-shaped (D. Huang, 2022). Moreover, it has been posited by certain scholars that green finance policy could potentially yield adverse effects on CSR (Sinha et al., 2021). Specifically, it has been argued that such influence is more noticeable environmentally sensitive industries in China. This could occur through the imposition of financial constraints, diminished allocation of resources toward environmental initiatives, and a decline in technological innovation (He et al., 2022).

Several researchers argue that the adoption of green finance policy may result in a decrease in carbon emission intensity (Muganyi et al., 2021). However, others have identified noteworthy adverse impacts of green financial instruments on carbon emission intensity (F. Wang et al., 2021). Regarding how green finance policy influences micro-firms’ development, there are varying opinions among researchers. According to Hafner et al. (2020), the presence of uncertainty and short-termism within the financial system presents significant challenges in attaining sustainable business growth. In this context, long-term and consistent environmental policy is considered preferable to short-term incentives for promoting corporate green investment (Criscuolo & Menon, 2015). For instance, studies have shown that while green credit policy stimulates firms’ short-term financing, they may hinder firms’ long-term investment behavior. In addition, green credit policy may also ease financing constraints for firms that engage in significant levels of pollution. With the reduction of financing costs, listed companies will be able to make more achievements in green innovation and transformation (C. H. Yu et al., 2021).

According to S. Xu and Zhu (2022), it is anticipated that China will emerge as a prominent global influencer in the dissemination of green finance concepts. The first aspect of scholarly investigation is the alignment between China’s green finance policy and green economy, whose regional disparities and imbalances have been proved to be apparent (H. Zhang et al., 2022). Moreover, it is observed that the influence of green finance on green development in China demonstrates a notable effect characterized by a single threshold. (J. Zhang et al., 2022). The second aspect pertains to the influence of China’s green credit policy. Although the complete implementation of China’s green policy remains incomplete (B. Zhang et al., 2011), it has exerted an influence on listed companies, compelling them to embrace more sustainable practices by means of debt financing redistribution (W. Li et al., 2022). The third aspect focuses on the policy effects of China’s pilot zones. These pilot zones have a long-term value-enhancing effect on green firms (J. Hu et al., 2021), contribute to the improvement of regional environmental performance (H. Huang & Zhang, 2021), stimulate both regional and firm-level green innovation (C. Zhang et al., 2022; Y. Zhang & Li, 2022), and result in a reduction of illegal emissions from heavily polluting enterprises within the pilot zones (Y. Zhang & Lu, 2022).

Determinants of ESG Disclosure

External Pressure of ESG Disclosure

Current studies have has predominantly concentrated on examining how external pressures influence corporate environmental disclosure. Stringent environmental regulations have significantly influenced the extent of environmental disclosure (D. Wu & Memon, 2022; Y. Zheng et al., 2020). National policy legitimacy requirements and market-driven financing demand synergistically contribute to the adoption of sustainable accounting and reporting practices by listed companies (Ng, 2018). Firms that experience heightened environmental legitimacy pressure demonstrate a heightened motivation to strategically manage their carbon disclosure practices (X. Luo et al., 2022). While government regulation usually promotes local green innovation, it is crucial to acknowledge that this favorable impact is accompanied by an adverse spatial spillover effect, impeding the advancement of environmentally-friendly innovation in adjacent areas. (R. Ma et al., 2022). Mandatory environmental disclosure institutions provide reflexivity, deterrence, and enhancement mechanisms (X. Liu et al., 2010). Industry-specific factors play a crucial role in driving CSR disclosure among Chinese listed companies (Dyduch & Krasodomska, 2017; Suárez-Rico et al., 2018). The imposition of environmental regulatory penalties may positively influence listed companies’ environmental voluntary disclosure (Ding et al., 2019). Numerous studies have proved that adverse media coverage plays a crucial role in optimizing environmental disclosure among publicly traded companies. To conclude, the correlation between public media and government regulation yields a favorable impact on the caliber of CSR disclosure (Xue et al., 2021).

Intrinsic Dynamics of ESG Disclosure

Firm size is a critical internal factor influencing ESG disclosure, and extensive research has consistently shown a positive correlation between firm size and ESG disclosure (Gallego-Álvarez & Quina-Custodio, 2016; Lu & Abeysekera, 2014; Miklosik et al., 2021). Effective corporate governance significantly influences ESG disclosure (Bae et al., 2018), and a robust corporate governance framework promotes the transparent management and disclosure of social responsibility information (X. Liu & Zhang, 2017). Corporate governance encourages CSR reporting through a socially responsible board of directors. Moreover, government shareholding affects the quality of CSR reporting, and corporate governance mitigates negative cultural influences on CSR reporting (Mohamed Adnan et al., 2018). High-quality financial information from the previous period can also positively influences ESG disclosure in the current period (Abeysekera et al., 2021). Additionally, lower perceptions of corruption are also associated with better ESG disclosure (Khalid et al., 2022).

Investigations have provided evidence supporting a direct association between corporate financial performance of and their carbon disclosure (H. C. Yu et al., 2020). Moreover, it has been observed that companies that demonstrate robust financial performance have a tendency to provide a greater amount of ESG information (Gutierrez-Ponce et al., 2022). Conversely, financially troubled firms tend to exhibit lower quality ESG disclosure in comparison to firms that are not facing financial distress, (Harymawan et al., 2021). Companies that exhibit superior CSR performance usually produce extensive CSR reports (Uyar et al., 2020). However, Doan and Sassen (2020) argue that environmental performance negatively relates to environmental disclosure.

Executive and board characteristics influence ESG disclosure. The educational background of top managers positively impacts environmental disclosure (Y. Ma et al., 2019). However, H. Chen et al. (2021) have proved a notable negative relationship between chairman’s military background and corporate environmental disclosure. According to Rauf et al. (2021), there exists a negative correlation between executives’ political affiliations and the quality of CSR disclosure. Board size has a favorable correlation with CSR disclosure (M. Hu & Loh, 2018). The gender ratio of the board and the proportion of foreign directors do not show significant associations with the quality of environmental information disclosure (Agyemang et al., 2020). The percentage of director holdings has a negative correlation with the disclosure of sustainability reports (M. C. Wang, 2017). A noticeable correlation exists between board governance and sustainability disclosure. Equity concentration does not significantly affect the overall environmental accounting information quality of firms (Z. Liu & Bai, 2022). Additionally, foreign ownership significantly influences overall sustainability disclosure (Rustam et al., 2019) and possesses the capacity to stimulate the voluntary carbon disclosure (E. Kim et al., 2021).

In summary, despite considerable scholarly attention devoted to the examination of corporate ESG disclosure and green finance policy, there has been a notable lack of focus on the logical interconnection between these two areas within the academic sphere. For instance, F. Wang et al. (2019) believes that the adoption of green policy may not improve corporate environmental disclosure, and the environmental disclosure system failed to effectively transmit meaningful signals to the capital market. For this reason, this study not only fills the gap on the impact of green finance policy on listed companies’ ESG disclosure, but also applies the well-established quasi-natural experiment method and DID model to test the policy effects of the Guidance on listed companies’ ESG disclosure.

Theory Analysis and Hypothesis Development

Green Finance Policy and Listed Companies’ ESG Disclosure Quality

First and foremost, green finance policy can effectively address the issue of information asymmetry pertaining to ESG factors in the capital market. By doing so, it helps mitigate market failures in making ESG investment decisions, fosters the development of a standardized ESG disclosure framework, and guides listed companies toward the adoption of consistent ESG disclosure practices. The origins of institutional research can be attributed to the perspective of “ceremony conformity” within the framework of the new institutionalist theory. This perspective highlights that organizations adhere to institutional rules to gain legitimacy through compulsory, imitative, and normative isomorphism (DiMaggio & Powell, 1983). China’s capital market is not yet perfectly efficient, and information asymmetry is still relatively prominent (N. Li et al., 2021). Although ESG disclosure can address the information asymmetry among market participants, Chinese listed companies are still unwilling to make ESG disclosure (X. Wu & Hąbek, 2021). To address this issue, government intervention becomes crucial in overseeing the release of ESG information by listed companies and ensuring their compliance with relevant regulations. The Guidance proposes a significant focus on the advancement of green credit and the facilitation of green investment through the promotion of the securities market. Under this situation, companies should make credible ESG disclosure to meet the evaluation needs of financial institutions and social funders regarding ESG risks associated with lenders or investment projects. This disclosure becomes crucial for green investors in the securities market, as they rely on the ESG information released by listed companies to make informed investment decisions, including green securities purchasing and investments in environmentally responsible stocks (Barnea & Rubin, 2010; Broadstock et al., 2019). Therefore, green finance policy may effectively regulate issuers, certifiers, investors, and other participants in green finance products. It also encourages the spontaneous enhancement of listed companies’ ESG disclosure through the establishment of unified ESG evaluation standards, stricter enforcement of relevant systems, increased penalties for non-compliant disclosures, and enhanced supervision to ensure proper, comprehensive, timely, and accurate public disclosures (X. Liu & Anbumozhi, 2009).

Secondly, green finance policy encourages listed companies to enhance the “environmental isomorphism” of ESG disclosure, thereby exerting pressure and motivation on them to legitimize their ESG disclosure. Suchman (1995) argued that organizational legitimacy refers to stakeholders’ perceptions and judgments of whether a company’s behavior is consistent with social expectations. If an organization fails to adhere to socially acceptable goals, methods, and outcomes, it will not achieve success or even survive. This is because there exists an implicit agreement between a company and the market upon which it relies, allowing it to emerge, grow, and thrive. As legitimacy theory assumes, ESG disclosure is a response to the influence exerted by institutional and public stakeholders. Legitimacy theory significantly influences corporate ESG disclosure primarily manifested in two aspects: legitimacy pressure and legitimacy management (Dawkins & Fraas, 2011). At its core, legitimacy theory revolves around the concept of a social contract, establishing explicit, or implicit social contractual relationships between stakeholders and firms. Different stakeholders exert varying levels of legitimacy pressure on companies, driven by diverse economic or social interests. In response to such legitimacy pressure, companies engage in legitimacy management. The strategic choice of legitimacy management necessitates effective information disclosure (Akerlof, 1970). ESG disclosure aligns with the principles of legitimacy theory, exemplifying listed companies’ adaptation and control of the sustainable development environment. Non-compliance with government mandated ESG disclosure rules can result in direct legal consequences for listed companies (Albrizio et al., 2017). Conversely, proactive and voluntary ESG disclosure enables companies to cultivate a positive public image, gain increased recognition, and obtain legitimacy, thereby facilitating their development (Archel et al., 2009; Neu et al., 1998; Rockness, 1985). The proposed guidance seeks to establish mechanisms for sharing corporate environmental information, enhance mandatory environmental disclosure systems for companies, and develop financial instruments such as carbon emission rights. These mechanisms create the necessary conditions for the application and effectiveness of legitimacy pressure and legitimacy management in the context of ESG disclosure by listed companies.

Last but not least, ESG disclosure serves as a crucial signaling tool for listed companies (Spence, 1973; Yang et al., 2021). Via disclosure, companies communicate their ESG performance to external stakeholders, highlighting proactive environmental management, social responsibility initiatives, corporate planning and management, and sustainable development practices. Stakeholders gain a comprehensive understanding of the investee company by accessing publicly available information, enabling them to make informed decisions (Bhandari & Javakhadze, 2017). Signaling theory explains how green finance policy promotes ESG disclosure among listed companies, encompassing three key aspects. Firstly, green finance policy makes ESG disclosure a signaling tool for listed companies to convey superior ESG performance to the market, eliciting market response and generating additional market returns (Barnett & Salomon, 2012; Freeman et al., 2004; Mishra, 2017). Secondly, green financial policy can foster signaling interactions among listed companies, reducing the cost for companies with lower ESG disclosure levels to emulate those with higher levels, thereby elevating the overall ESG disclosure standard in the capital market (Hassan & Guo, 2017). Lastly, green finance policy establishes a disciplinary mechanism for non-compliant disclosures, creating a “bottom-line” signal that encourages listed companies to prioritize ESG compliance, thus enhancing overall ESG disclosure conformity (Bhandari & Javakhadze, 2017).

In conclusion, outstanding companies possess not only well-managed asset holdings and favorable market ratings, but also demonstrate self-discipline in adhering to statutory compliance in disclosure. Achieving this requires the government to enhance supervision and management, assign the responsibilities of administrative and supervisory authorities, trading platforms, and other market intermediaries in accordance with the law, and effectively allocate resources from public institutions. Moreover, it is crucial to ensure that companies can comprehensively, accurately, and completely release ESG-related information, thereby enhancing the quality of ESG disclosure. A robust ESG disclosure framework generates multiple benefits, including increased company value and greater social impact. Multi-departmental joint supervision offers the advantage of avoiding reliance on a single regulatory body and enables comprehensive oversight of various aspects of information disclosure by listed companies. This approach ensures that government supervision is thorough, facilitates compliance with system requirements, and promotes effective ESG disclosure. Based on these considerations, we propose the following hypothesis:

Hypothesis 1 (H1). Since 2016, the Guidance issued by the PBC and six other ministries and departments has improved the ESGdq of listed companies in China.

The conceptual framework underpinning H1 is depicted in Figure 1.

Conceptual framework.

Ownership Nature’s Heterogeneity Effect

In China, state-owned listed companies are owned by the State Council or local governments (Guo et al., 2019). China’s state-owned listed companies are an important subject of ESG responsibility (Y. Gao, 2009). Apart from creating economic value, the state-owned listed companies are given the mission to promote environmental protection, alleviate social problems, perfect corporate governance (Ervits, 2023). Besides being responsible for main shareholder, state-owned listed companies should also take into account other stakeholders (Bai et al., 2006). Chinese people view state-owned listed companies as “social organizations” rather than simply “economic organizations” due to their intimate association with the government (Enderle, 2001) with a strong sense of obligation and responsibility to the country and the people (Y. Y. Hu et al., 2018). Many studies have supported the assertion that state-owned listed companies exhibit commendable ESG performance (Shahab et al., 2019; Voinea et al., 2022).

Conversely, with excessive emphasis on shareholders’ interests, non-state-owned listed companies inevitably ignore interests of other stakeholders and the public (P. Tang et al., 2018). Additionally, non-state-owned listed corporations have a limited awareness of ESG. They view ESG activities as a cost burden rather than a sacred obligation, resulting in the absence of initiative to consciously fulfill ESG obligations (Wood & Jones, 1995; H. Zheng & Zhang, 2016). ESG performance of non-state-owned public firms cannot be properly guaranteed because their ESG operations are utilitarian, which is essentially self-interested (File & Prince, 1998; Peloza & Hassay, 2006). In fact, China’s non-state-owned listed companies are frequently criticized for severe environmental pollution, poor product quality, and lack of protection of employees’ rights and interests, and numerous negative ESG events have also occurred (Lin, 2010; L. Wang & Juslin, 2009).

According to the preceding analysis, this study suggests that state-owned listed companies focus more on ESG activities and integrate ESG principles into their daily operations. This implies that, compared to non-state-owned listed companies, they are more proactive, responsive, and timely in their efforts to meet the requirements and standards of the newly introduced green finance policy. Therefore, we introduce the following hypothesis:

Hypothesis 2 (H2). The Guidance has a stronger positive impact on the ESG disclosure quality of state-owned listed companies.

Economic Development Level’s Heterogeneity Effect

China is a geographically expansive nation characterized by notable variations in levels of economic development across its various regions. These disparities also impact various aspects of listed companies’ ESG activities, including ESG disclosure (Démurger, 2001). On one hand, in regions characterized by elevated levels of economic development, governmental entities tend to implement more extensive regulatory frameworks pertaining to ESG matters. Due to the need for legal status, listed companies tend to comply with regulations issued by government departments and minimize the risk of non-compliance as much as possible. Consequently, these jurisdictions will make listed corporations actively participate in disclosing their ESG practices and continuously enhance ESG disclosure quality. This leads to greater transparency and openness in the company’s own ESG performance, ultimately enabling them to effectively meet regulatory requirements (Kong et al., 2023).

On the other hand, stakeholders in regions characterized by elevated levels of economic development generally exhibit a greater degree of ESG awareness and are more willing to support and assist listed companies with better ESG performance (Baron et al., 2011). Therefore, listed companies can regard ESG strategy as an important means to gain competitive advantage (Harjoto et al., 2015). They can actively fulfill their ESG responsibilities and engage in high-quality ESG disclosure, thus showing their outstanding ESG performance to the outside world and establishing a favorable ESG reputation (Clarkson et al., 2008; Jawahar & Mclaughlin, 2001). This ultimately reduces the information asymmetry with stakeholders and allows companies to obtain various benefits from them (Flammer, 2013; Mullainathan & Shleifer, 2005).

According to the preceding analysis, this study posits that listed companies operating in regions characterized by higher levels of economic development encounter more pronounced external regulatory pressure and exhibit heightened internal motivation to improve their ESG disclosure practice. Hence, in the face of recently implemented green finance policy, it is probable that these companies will prioritize enhancing the quality of ESG disclosure. Thus, we posit the following hypothesis:

Hypothesis 3 (H3). The Guidance has a stronger positive impact on the ESG disclosure quality of listed companies with higher local economic development level.

Research Design

Sample and Data

This paper employs a research sample consisting of A-share listed companies on the main boards of the SSE and the SZSE during the period from 2006 to 2022. The control group comprises of samples in non-heavily polluting industries, while the test group consists of samples operating in industries with high levels of pollution. The initial sample is processed based on several standards: (1) exclusion of companies marked with ST (Special Treatment) and *ST due to concerns regarding data authenticity and accuracy; and (2) exclusion of listed companies with missing or abnormal data to ensure data comparability and validity. The final sample consists of data from 1,341 listed companies covering the years 2006 to 2022, with a total of 13,831 observations (as showed in Table 1).

Composition of Sample Groups.

The ESGdq scores come from the Bloomberg database, whereas other data are sourced from WIND and CSMAR database. We apply Stata MP 16.0 for descriptive statistics and regression analysis.

Variable Measurement

Dependent Variable

ESG Disclosure Quality (ESGdq) was selected as the dependent variable. In practice, listed companies typically disclose ESG information through CSR reports, ESG reports, sustainability reports, integrated reports, and company annual report appendices. At present, a series of mature standards guiding the preparation of ESG reports have emerged internationally, such as the AA1000 series of standards, the GRI standards and the SASB standards (D’Apice et al., 2021; Sethi et al., 2017; Siew, 2015). Based on these standards and rules, some third-party rating agencies, such as Bloomberg, have emerged to evaluate and score the ESG reports of listed companies. Bloomberg has established a professional ESG report evaluation team comprised of 44 ESG analysts to help standardize third-party ESG data based on the framework of the SASB standards. Also, Bloomberg established a scientific assessment system which includes 122 indicators, thus can comprehensively evaluate listed companies’ ESG disclosure quality (K. Luo & Wu, 2022). Moreover, the system assigns scores separately to the dimensions of environment, society, and governance, making the final results more detailed and accurate (Albuquerque et al., 2020). As a result, this paper evaluates listed companies’ ESG disclosure based on based on ratings published by Bloomberg.

Independent Variable

The independent variable is Policy Treatment Effect (Treat × Time), the multiplication of the experimental variable and the time variable. Experimental variable (Treat): Treat = 1 if the listed company belongs to a heavily polluting industry, 0 otherwise; Time variable (Time): Time = 1 if the observation period is after 2016, 0 otherwise.

Control Variables

Drawing on Karim et al. (2021) and Gholami et al. (2022), we control necessary variables which relate to firm characteristics and may impact listed companies’ ESG disclosure, including Company Size (Size), Listed Years (Age), Financial Leverage (Lev), Profitability (Roe), Cash Flow Ratio (Cashflow), Growth Capacity (Growth), Ownership Nature (Soe), Time Fixed Effect (Year), and Firm Fixed Effect (ID). Specific definitions of control variables and descriptions are clarified in Table 2.

Variables Definition.

Model Development

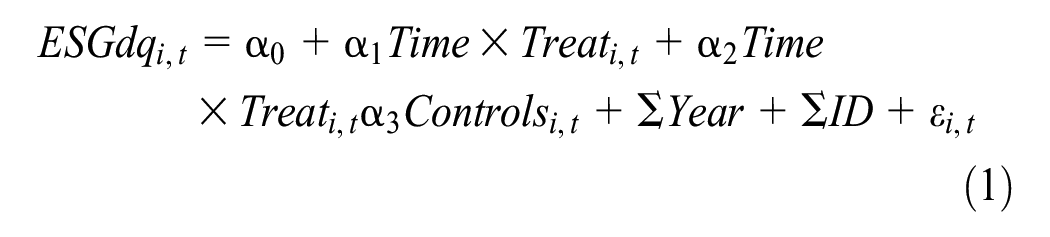

Regression analysis is frequently performed using the DID approach while evaluating the effects of regulatory system installation. This study establishes the following model (1) and takes into account the error problem, referring to Bertrand et al. (2004) and Chen et al. (2022).

In model (1), ESGdq stands for ESG disclosure quality, i for the listed company, t for the time, Time represents the implementation of the Guidance, Treat shows whether the sample belongs to heavily polluting industries, X represents the control variable, Year represents the year, ID represents the company code. This paper focuses on the Treat × Time coefficient when assessing the regression findings. The adoption of the Guidance has greatly enhanced listed companies’ ESG disclosure quality, and hypothesis H1 is confirmed if the coefficient of Treat × Time in model (1) is significant.

Empirical Analysis and Discussion

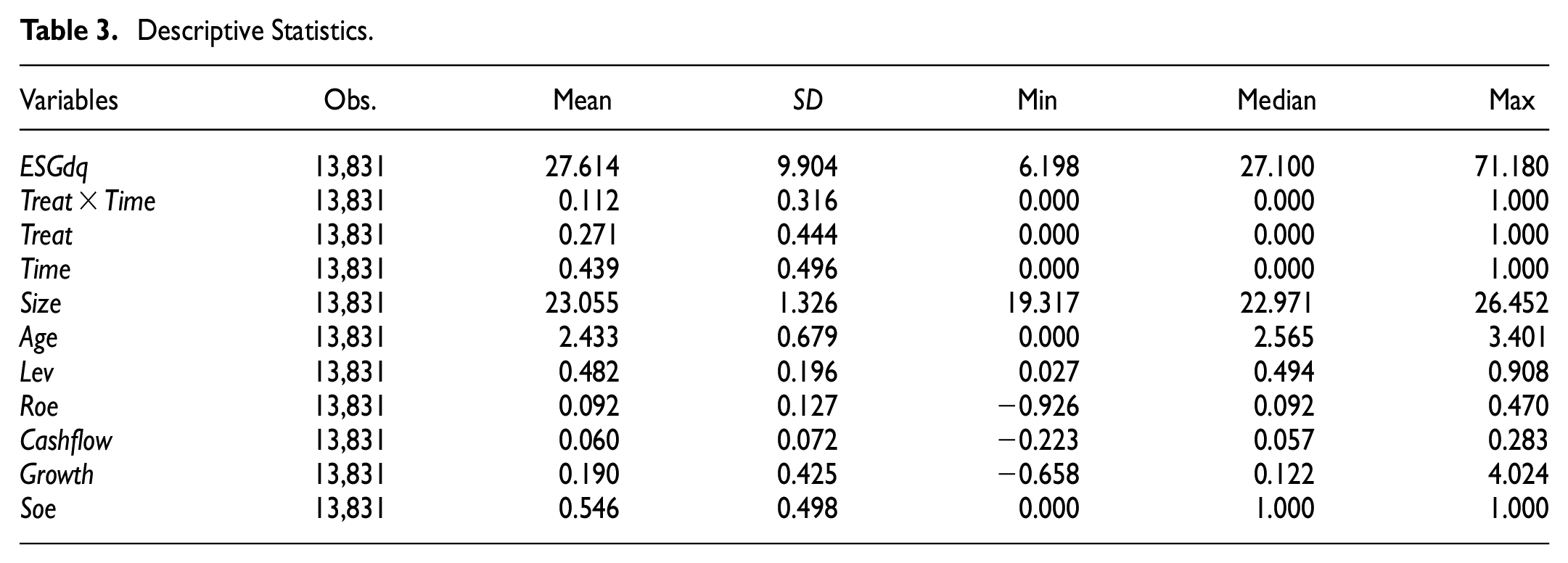

Descriptive Statistics

Table 3 displays primary variables’ descriptive statistics. Our sample consists of 1,341 listed companies, encompassing a total of 13,831 observations. The mean value of Time is 0.439, indicating that 43.9% of the observed data points are located after the year 2016. The mean value for Treat is 0.271, suggesting that 27.1% of the sampled companies are affiliated with the heavy pollution industry. The lower and upper bounds of ESGdq are 6.198 and 71.180, correspondingly. The standard deviation of ESGdq is 9.904, suggesting a significant level of dispersion in ESGdq.

Descriptive Statistics.

Univariate Test

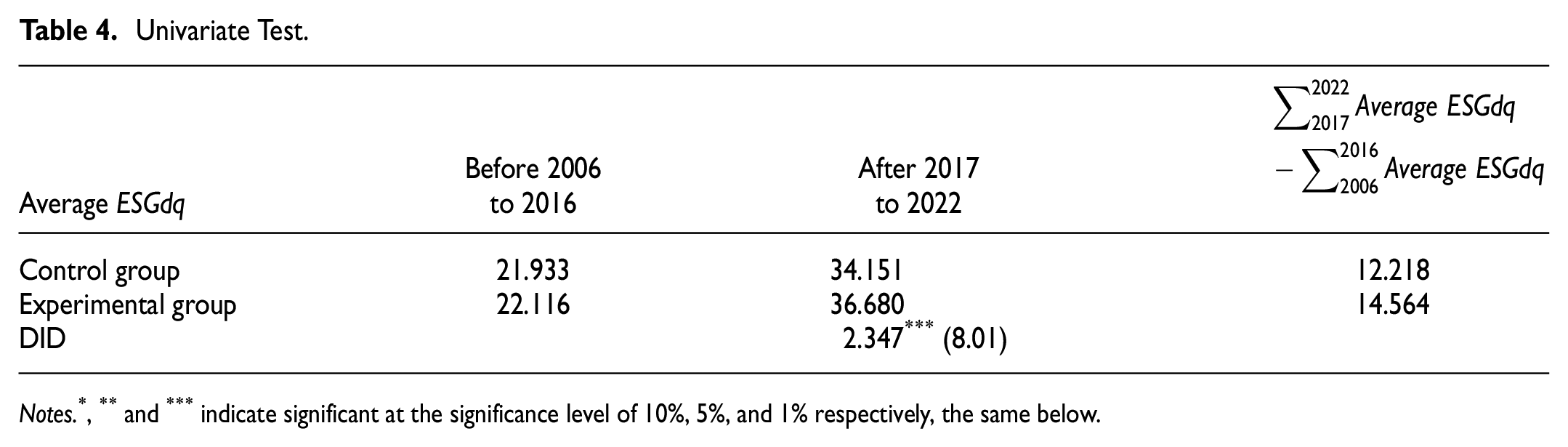

The univariate test was performed individually for the experimental group, which consisted of heavily polluting listed companies listed, and the control group, which consisted of non-heavily polluting listed companies. According to the data presented in Table 4, it can be observed that after the implementation of the Guidance, the average ESGdq of the companies in the experimental group notably increased about 14.564. Similarly, the control group companies also experienced an increase in their average ESGdq, albeit to a lesser extent, with a mean increase of 12.218. Our findings offer empirical support for the notion that listed companies’ESGdq in the experimental group exhibited a statistically significant increase compared to the companies in the control group. Consequently, this outcome serves to validate the initial hypothesis H1.

Univariate Test.

Notes. *, ** and *** indicate significant at the significance level of 10%, 5%, and 1% respectively, the same below.

Parallel Trend Test

The soundness of the DID model is contingent upon the implementation of the parallel trend test. This test assesses whether the experimental/control group demonstrate comparable or identical trends prior to the commencement of the experiment. It is essential for the parallel assumption to hold in order to accurately test the DID model and obtain reliable results. Drawing on Hong and Kacperczyk (2010), we constructed Model 2, designating the year of guideline implementation as the baseline period. Data from both previous and post 4 years were selected to conduct parallel trend test.

As shown in Table 5 and Figure 2, before the Guidance was issued, the coefficients of Pre_4, Pre_3, Pre_2, and Pre_1 are not significant at all, while in the years after the implementation of the Guidance, the coefficients of Post_1, Post_2, Post_3, and Post_4 are significant. The parallel assumptions of the DID model are met, and therefore the estimation of the role of ESGdq of listed companies by the publication of the Guidance is valid.

Parallel Trend Test.

Dynamic effect of the guidance.

Baseline Results

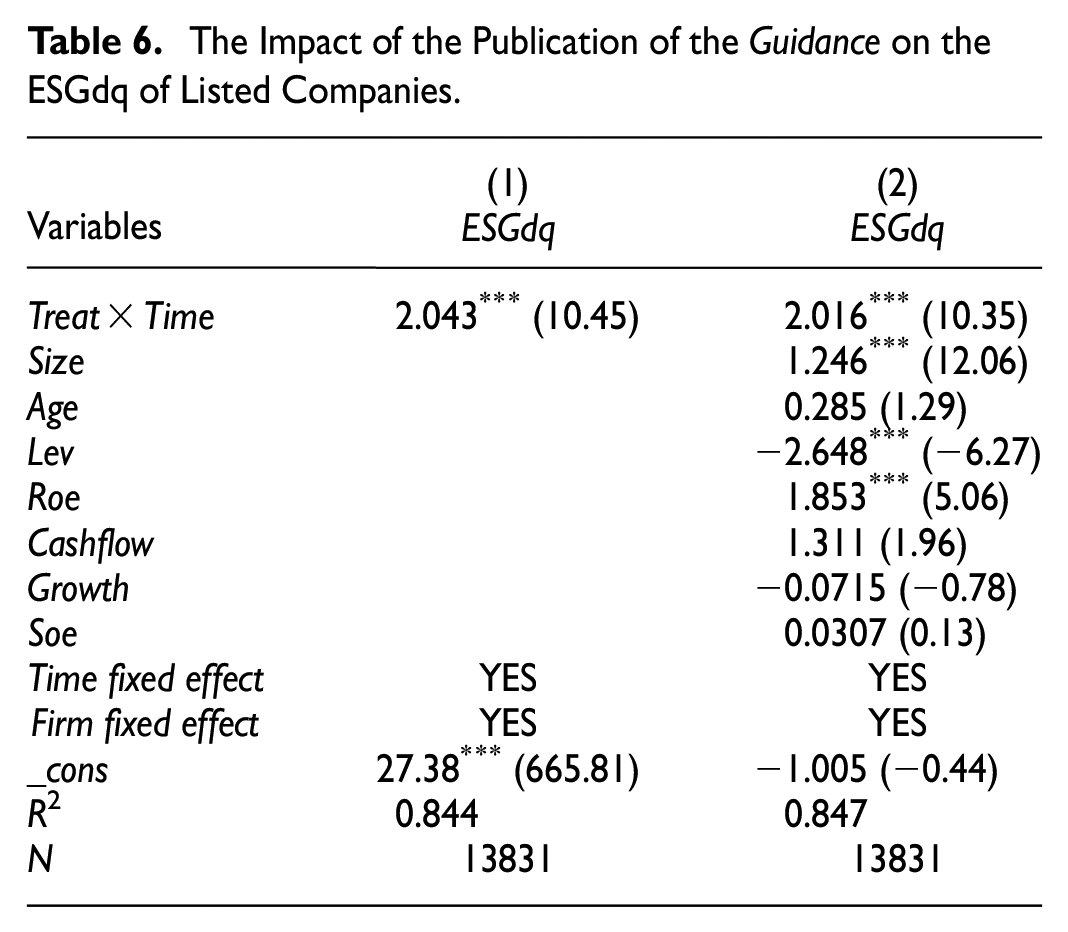

The test results in Table 6 analyze the influence of the publication of the Guidance on listed companies’ESGdq. The table demonstrates the variations in ESGdq prior to and subsequent to the implementation of the Guidance, taking into consideration time and firm fixed effects. Column (1) displays the results considering solely accounting for fixed effects, whereas column 2 further integrates control variables. The regression results using the full sample reveal that the coefficients of Treat × Time are all positive and significant at 1% level. Furthermore, these coefficients exhibit an increasing trend with the inclusion of control variables. The aforementioned findings suggest that the Guidance has a positive impact on ESGdq. From an economic perspective, after accounting for control variables, time and firm fixed effects, the coefficient of ESGdq is found to be 2.016, demonstrating significance at 1% level. This finding indicates that the issuance of the Guidance has led to a positive increase in ESGdq. Consequently, hypothesis 1 (H1) is validated.

The Impact of the Publication of the Guidance on the ESGdq of Listed Companies.

Robustness Checks

Endogeneity Test

The empirical findings indicate a notable enhancement in listed companies’ESGdq subsequent to the implementation of the Guidance. However, it is important to acknowledge that this outcome could potentially be influenced by other factors. Aiming to effectively ascertain the causal relationship between the Guidance on ESGdq, we utilized the works of Gholami et al. (2022) and employed Propensity Score Matching (PSM) technique to conduct one-to-one nearest neighbor matching based on the criteria of company size, listed years, financial leverage, profitability, cash flow ratio, growth capacity and ownership nature in the preceding year. Subsequently, this study re-evaluated the identified matches. As shown in Table 7, the coefficients of Treat × Time demonstrate statistical significance. Therefore, the primary conclusions drawn from the aforementioned analysis remain consistent, and the hypothesis under investigation remains valid.

PSM: One-to-One Nearest Neighbor Matching.

Placebo Test

According to T. Chen et al. (2015), there could be no particular point in time that would lead to ESGdq’ enhancement, so a placebo test is necessary to identify the uniqueness of the Guidance. The assumed implementation year of the Guidance was specifically identified as 2014 and 2015. Subsequently, the test was rerun. According to Table 8, we can observe that none of the coefficients of Treat × Time is significant, which indicates that there is no effect on ESGdq after switching the time when the policy is implemented. The results of placebo test confirm the distinctiveness of the implementation of the Guidance and lend support to the credibility of the findings presented in this paper.

Placebo Test: The Guidance Implementation Time Conversion.

Further Research

Heterogeneous Effects of Ownership Nature on Listed Companies’ ESGdq

The Chinese economy exhibits a dual ownership structure (Khan et al., 2019), wherein SOEs and non-SOEs collaborate to foster economic growth. However, due to the disparity in ownership structure, these two types of publicly traded companies exhibit divergent ESG practices. Drawing upon legitimacy theory, SOEs demonstrate greater responsiveness to policies and tend to exhibit stronger compliance with regulatory requirements when confronted with green finance policy. As shown in Table 9, after considering all control variables, the regression analysis reveals that the coefficients of Treat × Time are 2.047 for SOEs and 1.722 for non-SOEs, indicating that the Guidance has a more noticeable effect on improving ESGdq for SOEs in comparison to non-SOEs. As a result, hypothesis 2 (H2) is validated.

Heterogeneity Test of Ownership Nature.

Heterogeneous Effects of Local Economic Development Level on Listed Companies’ ESGdq

According to the classification criteria established by the National Bureau of Statistics (NBS) of China, excluding Hong Kong, Macao, and Taiwan, the regions can be categorized in the following manner. The eastern region encompasses a total of 11 provinces and cities, specifically Beijing, Tianjin, Hebei, Liaoning, Shanghai, Jiangsu, Zhejiang, Fujian, Shandong, Guangdong, and Hainan. The provinces and cities under consideration, which are strategically positioned and play a crucial role in national economic advancement, exhibit notable levels of economic development. The remaining regions, characterized by lower economic development, are classified as the Midwest. Table 10 presents the regression results under different economic development levels. After considering all control variables. the coefficients of Treat × Time is 2.588 for regions with higher economic development and 1.669 for regions with lower economic development, both significant at 1% level. Notably, the coefficient is larger in regions with higher levels of economic development, indicating a more substantial impact of the Guidance on the ESGdq of listed companies in those regions, hypothesis 3 (H3) is thereby confirmed.

Heterogeneity Test of Economic Development Level.

Conclusions and Implications

Drawing on institutional theory, signaling theory, and legitimacy theory, this study applies the DID method to examine the impact of the Guidance on ESG disclosure of A-share listed companies in the SSE and SZSE from 2006 to 2022. The main finding of the paper indicates that the Guidance positively influences listed companies’ ESG disclosure quality, the robustness of this finding is ensured after endogeneity test and placebo test. Furthermore, we examine this impact based on different ownership natures and local economic development levels. The impact of this phenomenon is notably significant for listed companies operating within industries that have a substantial environmental footprint, state-owned enterprises, and areas characterized by higher levels of economic development, as supported by empirical data.

The primary recommendations of this study are as follows. First, regulators should prioritize the establishment of a robust regulatory system for ESG disclosure among listed companies, including the formulation of standardized ESG disclosure criteria. Furthermore, they should assume primary supervisory responsibility and enhance cross-departmental cooperation to ensure effective oversight. Additionally, it is crucial to introduce norms to enhance listed companies’ ESG disclosure. Second, listed companies should integrate the ESG concept into their corporate strategy and culture. Moreover, they should incorporate ESG disclosure quality into their corporate management and internal control systems. Third, investors should embrace the international ESG investment concept, closely monitor ESG information provided by listed companies, and prioritize long-term value creation.

Some limitations remain in this study. First, this paper lacks the discussion based on an industrial perspective. In reality, listed companies in different industries exhibit significant differences in terms of business strategies, production models, and development philosophies. Consequently, the same green finance policy may yield vastly different outcomes across different sectors. Conducting a more in-depth exploration based on listed companies’ sector-level characteristics is quite necessary. Additionally, this paper is primarily a quantitative empirical study based on Chinese samples, lacking qualitative case studies and comparative studies. The subsequent study can select some typical Chinese and overseas cases for comparison, summarize the advanced ESG disclosure regulation of developed economies, and make adjustments based on China’s national conditions. Finally, this study solely relies on ESG data sourced from the Bloomberg database. Further research is needed to ascertain if similar findings can be replicated using other data sources.

Footnotes

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: This work was supported by the National Social Science Foundation Key Projects of China (19AGL009) and Jiangsu Province Postgraduate Scientific Research Innovation Project (KYCX23_0832; KYCX23_1523).

Data Availability Statement

Data sharing not applicable to this article as no datasets were generated or analyzed during the current study.