Abstract

Organizational resilience is a company’s ability to quickly recover and adapt when it encounters sudden and unexpected challenges. Our study looks at how a company’s level of international involvement before such challenges can influence its resilience, particularly when faced with the global disruptions caused by the COVID-19 pandemic. We also examine whether a company’s prior investment in digital technologies can help soften any negative impacts. From January 20 to June 10, 2020, we analyzed data from 2,363 Chinese companies that are traded on stock exchanges. We assessed their organizational resilience based on how their stock prices fluctuated and how quickly they returned to their pre-shock performance levels. Our findings indicate that companies with more international activities before the pandemic were generally slower to recover. However, companies with advanced digital capabilities before the pandemic demonstrated greater resilience, overcoming the negative repercussions more effectively. This research contributes new insights to the understanding of how international business activities affect a company’s ability to withstand and bounce back from global crises. Additionally, it underscores the importance of digitalization in enhancing organizational resilience.

Introduction

The COVID-19 pandemic, which began in December 2019, has brought a significant economic impact globally (Brodeur et al., 2021; Goodell, 2020). Many companies were influenced by the COVID-19 pandemic, and they struggled to survive it. Therefore, organizational resilience has attracted scholars’ attention because it captures an organization’s capability to protect, avoid, and adapt to shocks in its environment (Ortiz-de-Mandojana & Bansal, 2016), helps firms improve their sustainability and adaptability to environmental changes, thereby surviving longer (Gittell et al., 2006; Gunderson & Pritchard, 2003; Markman & Venzin, 2014).

Internationalization is an important influencing factor for organizational resilience. Since public health measures, such as lockdowns and border closing, cause firm global supply chain interrupted, internationalization may affect multinational enterprises (MNEs) to survive and develop during the pandemic. However, extant research has not reached a consistent conclusion on this question. Some scholars argue that under some lockdown policies, the global supply chain makes Chinese products unavailable (Eppinger et al., 2020; Kersan-škabić, 2022), thus internationalization may cause organizations fragile. But Puhr and Müllner (2022) found that international assets make companies more visible and reliable for investors, which increases MNEs’ resilience. The possible reason for these mixed conclusions may be that there is a potential endogenous problem, that is, resilient firms usually have good financial performance and management capability (Do et al., 2022; Ortiz-de-Mandojana & Bansal, 2016), and these features make them more likely to choose an international strategy (Bahl et al., 2021; Kim et al., 2020; Wang et al., 2020). Therefore, this study aims to solve the above problem and assesses how internationalization affects organizational resilience to the COVID-19 pandemic.

Furthermore, the effect of internationalization on organizational resilience is influenced by the boundary condition. Before the COVID-19 pandemic, firms’ digital transformation has become a trend. Firms’ digitalization includes not only the application of digital technology but also the changes in business processes, firm structure, and business models (Kane et al., 2015). When facing the challenge of physical asset-intensive supply chain disruptions, digitalization can make digital assets available from anywhere in the world, so firms’ dependence on physical assets diminishes (Autio et al., 2021; Mudambi, 2008). The more accessible assets and transformations brought by digitalization shorten the supply chain (Kurpjuweit et al., 2021). This may further affect the relationship between internationalization and organizational resilience.

Our study thus makes important contributions to the literature. First, we identify internationalization as an important predictor of organizational resilience. This yields new insights into the determinants of organizational resilience, such as CEO characteristics (Buyl et al., 2019; Sajko et al., 2021) and corporate social responsibility (DesJardine et al., 2019; Huang et al., 2020). We go further and demonstrate digitalization as an important contingency factor that influences the relationship between internationalization and organizational resilience. Overall, our study advances the literature on the drivers of organizational resilience and boundary conditions.

Second, this study contributes to the research on internationalization related to crisis management by illuminating the association between internationalization and organizational resilience. With a few exceptions (Notteboom et al., 2021), extant research tends to ignore the dark side of internationalization during the crisis. We offer a deeper understanding of how internationalization influences organizational resilience in the context of the COVID-19 pandemic and thus contribute to the emerging research that focuses on the dark side of internationalization in crisis management.

Third, we contribute to internationalization research by identifying a situation where facets of internationalization once viewed favorably for firm crisis (Chang et al., 2016; Mihov & Naranjo, 2019), unexpectedly contributes to value depreciation. Conventional internationalization paradigms emphasize globalization’s positive economic impacts but fail to address the complexities of an unprecedented systemic crisis like the COVID-19 pandemic (Hadjielias et al., 2022; Hu et al., 2023; Puhr & Müllner, 2022). This pandemic reveals internationalization components, like supply chains, human capital, and investments, as potential obstacles to business operations. Our study specifically concentrates on the situation of the COVID-19 pandemic to enrich understanding of the COVID-19 pandemic’s impact on international business (Guedhami et al., 2022; Notteboom et al., 2021).

Literature Review

Organizational resilience is the capability to survive adversity, recover, and preserve structure after a crisis (Gunderson & Pritchard, 2003). It is constructed by two dimensions: stability and flexibility (DesJardine et al., 2019). Stability enables a company to maintain its fundamental traits and functions, such as core functions and identities, when facing environmental shocks (Weick et al., 2008). Flexibility means having flexible and various resources that can help a firm develop alternative solutions to the same crisis (Sanchez, 1995). When facing unexpected environmental shocks, a resilient organization can maintain its core structures, and recover from crisis due to its ability to adapt to changes (Ortiz-de-Mandojana & Bansal, 2016). Buyl et al. (2019) emphasized that to understand a firm’s reaction to a systemic shock, its characteristics before the shock should be taken into account. Scholars have analyzed many factors before various types of shocks that affect organizational resilience, including top management team characteristics (Sajko et al., 2021), supply chain capabilities (Bak et al., 2023; Brusset & Teller, 2017), and corporate social responsibility (DesJardine et al., 2019; Huang et al., 2020), but most research is conducted in the context of financial crises, and the COVID-19 pandemic is quite different from other crises that have been researched. In this special context, there may be other influencing factors affecting organizational resilience, for example, internationalization, but extant research has not deeply investigated this problem.

There are large amounts of studies on internationalization (Anand et al., 2023; Elia et al., 2021; Holmes et al., 2013; Hoskisson et al., 2013; Nambisan et al., 2019; J. Paul & Rosado-Serrano, 2019; Terjesen et al., 2016). Notably, extant literature has analyzed the relationship between internationalized firms’ performance (Banalieva & Dhanaraj, 2013; Graves & Shan, 2014; L. Zhou & Wu, 2014), innovation (Autio et al., 2021; Piperopoulos et al., 2018; Vrontis & Christofi, 2021), risk (C. Zhou, 2023), among other aspects. A well-established idea in internationalization research and risk management is that internationalization enables firms to operate flexibly by transferring business activities between subsidiaries in different countries, thereby mitigating downside risks (Allen & Pantzalis, 1996; Rangan, 1998). For instance, scholars have found that during the 2008 Global Financial Crisis, internationalization endowed multinational assets with risk dispersion capabilities, consequently bolstering firm resilience (Meliciani & Tchorek, 2019). However, recent scholarly discourse has shed light on a contrasting perspective; disruptions in global supply chains during the COVID-19 pandemic have unveiled potential drawbacks of internationalization (Notteboom et al., 2021). Despite these emergent discussions, a comprehensive exploration into the underlying mechanisms dictating how internationalization influences organizational resilience remains incomplete.

Moreover, digitalization, as one of the potential boundary conditions of the relationship between internationalization and organizational resilience, is worth studying. Digitalization refers to a company’s capability to pursue strategic alternatives and create values for stakeholders through the utilization of different IT and business resources (Annarelli et al., 2021; Drnevich & Croson, 2013; Nylén & Holmström, 2015; Sambamurthy et al., 2003). It can help firms establish competitive advantages inside and outside, and achieve value cocreation (Barua et al., 2004; Karimi & Walter, 2015; Scuotto, Del Giudice, & Carayannis, 2017; Scuotto, Del Giudice, Peruta, et al., 2017). By providing accurate standards and rules, firms can promote the efficiency of the production process (Karimi & Walter, 2015). By developing online information capability which helps to exchange strategic and tactical information, firms can increase interaction and cooperation with suppliers and customers (Barua et al., 2004). Also, digitalization can improve return on investment and firm innovation (Scuotto, Del Giudice, & Carayannis, 2017; Scuotto, Del Giudice, Peruta, et al., 2017). In our study, digitalization includes all these activities because when facing the lockdown policy, firms not only need a digital production process, but also need to interact with their employees, suppliers, and customers online.

Theoretical Development and Hypotheses

Internationalization and Organizational Resilience

Global supply chains established by firms before the pandemic have become fragile after the shock. According to Fortune magazine, 94% of Fortune 1,000 firms experienced COVID-19-related supply chain disruptions (Sherman, 2020). These disruptions are due to challenges faced by suppliers, manufacturers, and transporters. To protect citizens’ health, almost all governments around the world had imposed full or partial lockdown policies, such as closing the border, restricting vehicle movements, and requiring home quarantine (S. K. Paul & Chowdhury, 2020). Border closure and vehicle movement restrictions result in delays or interruptions of product circulation (Chiaramonti & Maniatis, 2020). Mandatory home quarantine leads to a labor shortage, which results in suppliers’ production being interrupted, and firms not delivering goods to consumers on time (Ivanov & Das, 2020). Therefore, the pandemic influences all nodes (i.e., suppliers, manufacturers, and transporters) and ties of global supply chains (Gunessee & Subramanian, 2020; S. K. Paul & Chowdhury, 2021), and the flow of global chains is disrupted greatly.

Disrupted global supply chains change firms’ key attributes. Companies that originally exported products for profit cannot continue this business because foreign demands are satisfied by local companies. For example, foreign enterprises shift to local suppliers, and even though local suppliers may be more expensive than Chinese suppliers, they are more certain (Kersan-škabić, 2022). Production has become more localized, and both companies and consumers are less reliant on foreign suppliers. Thus, Chinese firms cannot maintain their prior core functions and identities, and their stability decreases. Therefore, we propose the hypothesis:

H1: The firm with a higher degree of internationalization before the shock is less likely to maintain stability following the shock.

When global supply chains are suddenly interrupted because of the shock, it is difficult for MNEs to change their business quickly to accommodate changes. Different degrees of lockdown policies decrease interactions between members in global supply chains. The lack of communication and interaction leads to incomplete information, thus reducing information accuracy and clarity (Gunessee & Subramanian, 2020). This further reduces a firm’s degree of participation in the global supply chain so MNEs find it difficult to integrate all potential resources that members in supply chains have to develop alternative solutions when facing global supply chain disruption brought by the pandemic (Di Vaio et al., 2020).

Additionally, the outbreak of COVID-19 increased demand for basic products, especially food and medical products, and the flow of intermediate industrial products (e.g., paint, plastic, and production machinery), dropped rapidly during the crisis (Notteboom et al., 2021). During the lockdown period, it is hard for firms to decide to change the products they produce. If firms decide to produce basic products instead, purchasing machines needed for production and mastering new production technologies require high costs, which is of high risk in an uncertain environment. Therefore, these firms’ flexibility decreases following the shock, and we propose the hypothesis:

H2: The firm with a higher degree of internationalization before the shock is likely to recover less quickly following the shock.

The Moderating Effect of Digitalization

MNEs that applied digitalization before the pandemic demonstrate advantages when global supply chains are disrupted. Digitalization frees the firm from restrictions of transportation and collocation and changes the means of delivery and acquisition of goods (Autio et al., 2021). For example, firms can use drones or driverless delivery trucks to deliver goods timely and contactless (Quayson et al., 2020; Singh et al., 2021), thus the negative impact of vehicle movement restriction on the supply chain reduces. Using 3-D printing technology and robot technology, manufacturers can alleviate the labor shortage caused by home quarantine. Digital communication technology helps employees communicate remotely. Digitalization helps companies maintain original supply chains and businesses to some extent.

This maintenance helps the firm be stable following the COVID-19 pandemic. Although MNEs are affected by lockdown policies brought on by the pandemic, if the firm is digitalized, it can still partly maintain its prior business with tools that run automatically, so its core functions and identities are maintained, and the negative impact of internationalization on stability is alleviated. Therefore, we propose the hypothesis:

H3: If the firm has a higher degree of digitalization before the shock, the negative impact of internationalization on maintaining stability following the shock reduces.

Digitalization can help a firm’s recovery from the crisis. A highly digitalized company is better equipped to handle the impact of the COVID-19 pandemic by implementing innovative solutions. Online communication technology makes firms communicate with other members of the supply chain, so firms can regain interactions with each other, and exchange accurate and clear information. Firms can use the information to seek potential resources that may help them develop alternative solutions to global supply chain disruptions. To meet the sudden demand for medical products, companies can employ digital manufacturing techniques like 3-D printing (Iyengar et al., 2020; Larrañeta et al., 2020). Quick changes in products and production processes indicate firms’ flexibility. Therefore, we propose the hypothesis:

H4: If the firm has a higher degree of digitalization before the shock, the negative impact of internationalization on time to recovery following the shock reduces.

The summary of the theoretical model is illustrated in Figure 1.

Theoretical model of internationalization, digitalization, and organizational resilience.

Methodology

Data and Samples

Our samples are Chinese A-share listed companies from 2019 to 2020. We focused on public firms to permit the analysis of stock prices in response to the COVID-19 pandemic.

We have chosen the COVID-19 pandemic as the context to test our hypotheses for several reasons. Firstly, the COVID-19 pandemic has been identified as the most severe crisis since the Global Financial Crisis (GFC) (Bae et al., 2021). For instance, in the first 5 months of 2020, the Standard & Poor’s (S&P) 500 dropped by 34% from its peak to its lowest point. Similarly, during this period, stock exchanges in Brazil, Hong Kong, Italy, and Japan witnessed substantial declines from their highs to lows, ranging from 25% to 46% (Ding et al., 2020). Bernanke (2020) highlighted that the COVID-19 pandemic significantly restricted global economic activity, leading to considerable corporate losses due to governmental lockdowns and disruptions in the supply chain. Secondly, the COVID-19 pandemic shares similarities with other crises, such as economic downturns and political events. Theories on crisis management and organizational resilience from previous research can be applied in our study (Buyl et al., 2019; DesJardine et al., 2019; Sajko et al., 2021). Although the COVID-19 pandemic is a crisis, it is not entirely unique and falls under the concept of crisis management. Thirdly, despite some similarities, the COVID-19 pandemic differs significantly from past crises concerning its cause, scope, and severity (Reinhart, 2020). For example, the 2008 GFC stemmed from the housing bubble and didn’t cause major disruptions in global supply chains (Scott, 2010). Political events might disrupt specific supply chains in certain regions or industries, allowing firms to seek alternatives. However, the pandemic’s impact on supply chains is far-reaching and global due to widespread government-imposed lockdown policies, making it challenging for firms to immediately find substitutes. The varying degrees of impact on global supply chains can yield different research outcomes, making the direct application of conclusions from other crises (Meliciani & Tchorek, 2019) challenging in this study. Consequently, the COVID-19 pandemic offers a unique natural backdrop for investigating organizational resilience. Businesses across diverse sectors and sizes encountered significant impacts, leading to varying degrees of both setback and recovery.

After eliminating samples in the financial industry and samples with missing values, we constructed a data set of 2,363 firms. We collect accounting and financial data of these companies from China Stock Market Accounting Research (CSMAR) databases which is one of the largest databases on Chinese listed companies and stock market information. It covers data on economics, listed companies, stocks, bonds, futures, etc. It provides raw data for many studies (Jiang et al., 2021; Qian et al., 2017; Xia et al., 2014; Zhang & Qu, 2016), and is reliable and authoritative.

In our study, we identify 21 January 2020 as the starting date of the shock, considering that the COVID-19 pandemic was officially announced on China Central Television news on the evening of 20 January 2020 and the Chinese stock market halts trading at 3 p.m. every day. Since the Chinese government applied strict public health measures, the number of newly confirmed cases dropped to 0 on 10 June 2020, and later there was no large number of newly confirmed cases, so we identify 10 June 2020 as the shock finishing date in our study. The pandemic influences all industries and all aspects of the economy, so it is an ideal context in which we can examine organizational resilience.

Measures

Dependent Variables

Organizational resilience, defined as the capacity to endure adversity, rebound, and maintain structure post-crisis (Gunderson & Pritchard, 2003), is composed of two dimensions: stability and flexibility (DesJardine et al., 2019). However, empirical research faces challenges due to the latent, multidimensional nature, and path dependency of this construct (Linnenluecke et al., 2012; Ortiz-de-Mandojana & Bansal, 2016). Latent constructs like resilience cannot be directly observed or measured but are inferred through changes they induce in other constructs. Researchers have addressed these measurement challenges in two primary ways. One method involves examining organizational outcomes over an extended period. Ortiz-de-Mandojana and Bansal (2016) conducted a 15-year study demonstrating that firms anticipating and adapting to environmental disruptions experience lower financial volatility, higher growth, and improved survival rates. The other approach focuses on studying general environmental shocks to gauge organizational responses, thereby inferring organizational resilience from these reactions. This method effectively addresses the question of “resilience to what?.” For example, DesJardine et al. (2019) assessed the severity of organizational losses and recovery time following the 2008 GFC.

In this study, we adopt the second approach. We evaluate organizational resilience based on the severity of organizational losses and recovery time from the COVID-19 pandemic. Following research conducted by Buyl et al. (2019), DesJardine et al. (2019), and Sajko et al. (2021), we use two dimensions, stability and flexibility, to measure organizational resilience. These two dimensions are both calculated by stock prices. The idea that stock prices can reflect stakeholders’ immediate responses to new events and firm behaviors is widely accepted (Barrett et al., 1987; Fama, 1965; Rossi & Gunardi, 2018), and research has shown that stock prices in China have become as informative as they are in the US, indicating that the Chinese stock market is efficient (Carpenter et al., 2021). Therefore, it is reasonable to rely on the stock price to judge organizational resilience.

Stability

It represents the severity of loss after the shock. We calculate it as the absolute percentage change in every company’s stock price between the pre-shock (i.e., 20 January 2020) closing price and the lowest point that the stock price reached between 21 January 2020 and 10 June 2020. A higher value of this indicator reflects a more significant loss, indicating that the firm had lower levels of stability during the COVID-19 pandemic and reduced organizational resilience.

Flexibility

It represents the time to recover to the pre-shock price level. We calculate it as the number of days it would take the firm to recover its stock price to its pre-shock level, within the period spanning from 21 January 2020 to 10 June 2020.

Independent Variable

The independent variable is the degree of internationalization (Internationalization). Consistent with prior studies (Sun et al., 2015), we calculate it as the proportion of overseas subsidiaries to the total number of the firm’s subsidiaries.

Moderator

The moderator is the degree of digitalization (Digitalization). Following prior research (Li et al., 2023; Q. Xu et al., 2023; Zeng et al., 2022), this study uses the text analysis method to capture keywords related to digitalization in firm annual reports and constructs an index of digitalization according to the captured results. Annual reports can reflect firms’ operation situation and strategies, so it is reasonable to evaluate firm digitalization value through the text analysis method.

Specifically, we measure it as the frequency that the firm-mentioned words related to digitalization in the annual report. The steps are as follows. First, we download PDF files of annual reports from the official websites of the Shanghai and Shenzhen stock exchanges. Second, we use Python software to change PDF files to txt files. Third, we capture keywords related to digitalization from text files and count frequency. In the selection of keywords related to digitalization, we refer to previous studies (Ren et al., 2023; Q. Xu et al., 2023) and read the Chinese government’s policy documents such as “China Financial Technology Operation Report” and “Big Data Industry Development Specification.” The keywords we choose are in five aspects, that is, artificial intelligence technology, blockchain technology, cloud computing technology, big data technology, and digital technology application, and are shown in Table 1.

Keywords Related to Five Aspects of Digitalization.

Control Variables

We control six variables associated with the firm’s characteristics (Sales growth, Concentration, Separation, Integration, R&D intensity, and Patent stock). Sales growth is measured by the operating income growth rate. Concentration represents the ownership concentration and is calculated by the shareholding ratio of the top 10 shareholders. Separation means the degree of separation of ownership and management. Integration is a dummy variable, if one person serves as both chairman and general manager, it equals 1, otherwise 0. R&D intensity is calculated by the proportion of R&D investment in operating income. Patent stock is calculated by the logarithm of the patent stock of the company in the research year.

Estimation Procedures

We use two-stage least squares (2SLS) and a Cox regression model to test hypotheses. Our empirical analysis has a potential concern: the endogenous problem. Resilient firms usually have good financial performance and management capability (Do et al., 2022; Ortiz-de-Mandojana & Bansal, 2016), and these features make them more likely to choose an international strategy (Bahl et al., 2021; Kim et al., 2020; Wang et al., 2020). Also, there may be omitted variables, for example, firms with good management capabilities are easier to recover from the pandemic (Bundy et al., 2017; Rapaccini et al., 2020).

To solve the endogenous problem, we choose the industry average internationalization degree as the instrumental variable because it is correlated to a firm’s degree of internationalization but exogenous to residuals in models. Firms in the same industry inevitably imitate and compete with each other, so the industry average internationalization degree is correlated to a firm’s degree of internationalization. However, the industry average internationalization degree is irrelative to organizational resilience, otherwise, firms in the same industry have similar organizational resilience.

Details of estimation procedures for two dimensions of organizational resilience are as follows.

Stability

We use 2SLS to test H1 and H3. The first stage regression model is

where i indexes firms,

The second stage regression model is

where Equation 2 is to test H1, and Equation 3 is to test H3. i indexes firms,

Flexibility

To test H2 and H4, we still use the industry average internationalization degree as an instrumental variable. The first stage is the same as Equation 1, and the second stage is a Cox regression model. Since not all firms had recovered from the COVID-19 pandemic during the observation period, our data were right censored. The time of recovery of these firms is set to (142, +

Results

Descriptive Statistics and Correlation Analysis

Table 2 reports descriptive statistics and Pearson correlation coefficients. In the 142 days following the shock, the stock price dropped 21.3% on average, and the mean value of recovery time is 46.81 days, but the time of recovery varies widely from company to company. Internationalization is significantly and positively correlated to stability and is negatively associated with flexibility, but we still need further regression analysis to test our hypotheses. All correlation coefficients between important explanatory variables are below .6, indicating that the likelihood of a multicollinearity problem is low. Furthermore, the mean of variance inflation factors (VIFs) is 1.05, and the largest one is 1.15, so there is no multicollinearity problem.

Descriptive Statistics and Correlations.

p < .1. **p < .05. ***p < .01.

Results for Stability

Table 3 reports results for stability from 2SLS. We test for endogeneity first. Through the Durbin-Wu-Hausman test for Internationalization, we find that there is an endogenous problem indeed (F = 21.563, p = .000, rejecting the null hypothesis that Internationalization is exogenous). Then we test whether the instrumental variable, industry average internationalization, is suitable. Column (1) in Table 3 shows the result of the first stage. Industry average internationalization is significantly and positively correlated to a firm’s internationalization (p = .000). Moreover, Shea’s partial R2 (Shea, 1997) is .0532, and the Cragg-Donald F statistic is 149.121 (p = .000) exceeding Stock-Yogo critical values (Stock & Yogo, 2005) at the 5% (16.38), 10% (8.96), 20% (6.66), and 30% (5.53), indicating that the instrumental variable is not weak. Overall, the instrumental variable is suitable.

2SLS Predicting Stability.

Note. Values in the table are unstandardized regression coefficients. Standard errors are in parentheses.

p < .1. **p < .05. ***p < .01.

Column (2) in Table 3 shows the result of the second stage of 2SLS testing the main effect of internationalization. Internationalization has a significantly positive effect on stability (p = .000), indicating that if the firm has a higher degree of internationalization before the shock, the stock price following the COVID-19 pandemic falls more seriously, and organizational resilience is worse, so H1 is supported.

Column (3) in Table 3 reports the result of the second stage of 2SLS testing the interaction between internationalization and digitalization. There is a negative and significant interaction between these two variables on stability (p = .083), supporting H3 that a high level of digitalization before the shock can reduce the negative impact of internationalization on maintaining stability following the shock. Figure 2 also shows this result.

Moderating effect of digitalization on stability.

Results for Flexibility

Table 4 reports results for flexibility from a Cox regression model. We still use industry average internationalization as the instrumental variable, so the result of the first stage is the same as that in column (1) of Table 2, and we do not repeat it. Table 4 reports the results of the second stage using the Cox regression model.

Cox Regression Model Predicting Flexibility.

Note. Values in the table are unstandardized regression coefficients. Standard errors are in parentheses.

p < .1. **p < .05. ***p < .01.

Table 4 column (1) demonstrates a significantly negative coefficient of internationalization (p = .017), supporting H2 that the firm with a higher degree of internationalization has a lower possibility of recovering after the pandemic. The Cox regression model indicates a hazard ratio of 0.307 (p = .017), indicating that a one-standard-deviation increase in internationalization results in a 69.3% drop in the probability of recovery time. Figures 3 and 4 show hazard estimate result intuitively.

Smoothed hazard estimate.

Nelson–Aalen cumulative hazard estimate.

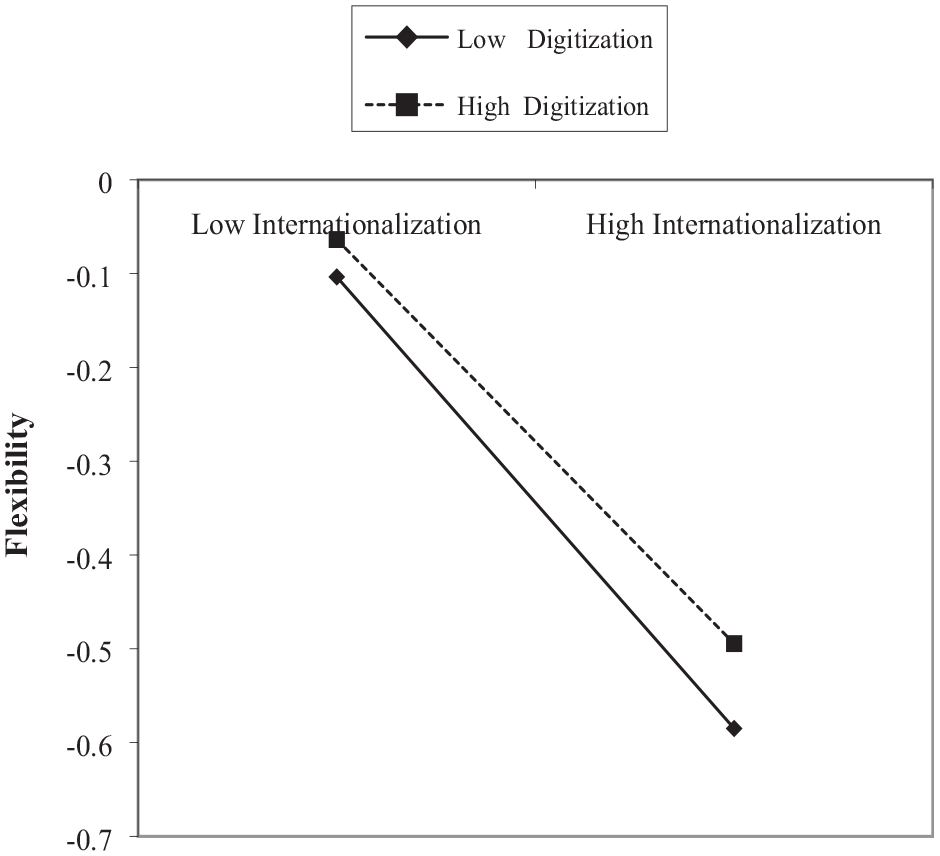

Column (2) in Table 4 reports the result of the interaction between internationalization and digitalization, revealing a positive and significant interaction between these two variables on flexibility (p = .049), supporting H4 that if the firm has a higher degree of digitalization before the shock, the negative impact of internationalization on time to recovery following the shock reduces. The hazard ratio of interaction between internationalization and digitalization is 1.045 (p = .049), indicating that each additional point in this interaction causes the probability of recovery to increase by 4.5%. Figure 5 also shows this interacting result.

Moderating effect of digitalization on flexibility.

Additionally, to use the Cox regression model, the proportional-hazards assumption should be satisfied. A proportional risk test based on Schoenfeld residuals is utilized. The overall p-value is .2699, not meeting the rejection criterion for the null hypothesis, indicating that the Schoenfeld residual does not alter systematically over time. More specifically, we test the independent variable by drawing Figure 6, showing that the slope of Schoenfeld residual with time is roughly zero. Therefore, the proportional-hazards assumption is satisfied.

Test of internationalization’s proportional-hazards assumption.

Robustness Checks

We conduct several robustness checks to corroborate our results. First, we measure internationalization as the proportion of overseas subsidiaries to the total number of the firm’s subsidiaries, and in the robustness check, we change the measurement to the proportion of overseas revenue to overall operating revenue, another common measurement. Based on this measurement of internationalization, we also calculate industry average internationalization as the instrumental variable and use 2SLS to check whether our results are robust. Results in Tables 5 and 6 reveal that all hypotheses still hold.

Using the Proportion of Overseas Revenue to Overall Revenue to Measure Internationalization as a Robustness Check for Stability.

Using the Proportion of Overseas Revenue to Overall Revenue to Measure Internationalization as a Robustness Check for Flexibility.

Note. Values in the table are unstandardized regression coefficients. Standard errors are in parentheses. *p < .1. **p < .05. ***p < .01.

Second, we change the measurement of internationalization as the proportion of overseas assets to overall assets. Results in Tables 7 and 8 show that all hypotheses still hold.

Using the Proportion of Overseas Assets to Overall Assets to Measure Internationalization as a Robustness Check for Stability.

Note. Values in the table are unstandardized regression coefficients. Standard errors are in parentheses.

p < .1. **p < .05. ***p < .01.

Using the Proportion of Overseas Assets to Overall Assets to Measure Internationalization as a Robustness Check for Flexibility.

Note. Values in the table are unstandardized regression coefficients. Standard errors are in parentheses.

p < .1. **p < .05. ***p < .01.

Third, to check our Cox regression model, we use the proportional hazard model to corroborate our results. Our results, reported in Table 9, remained consistent when we assumed three different distributions for the baseline hazard function, as shown in Table 4.

Using Proportional Hazard Model as a Robustness Check for Flexibility.

Note. Values in the table are unstandardized regression coefficients. Standard errors are in parentheses.

p < .1. **p < .05. ***p < .01.

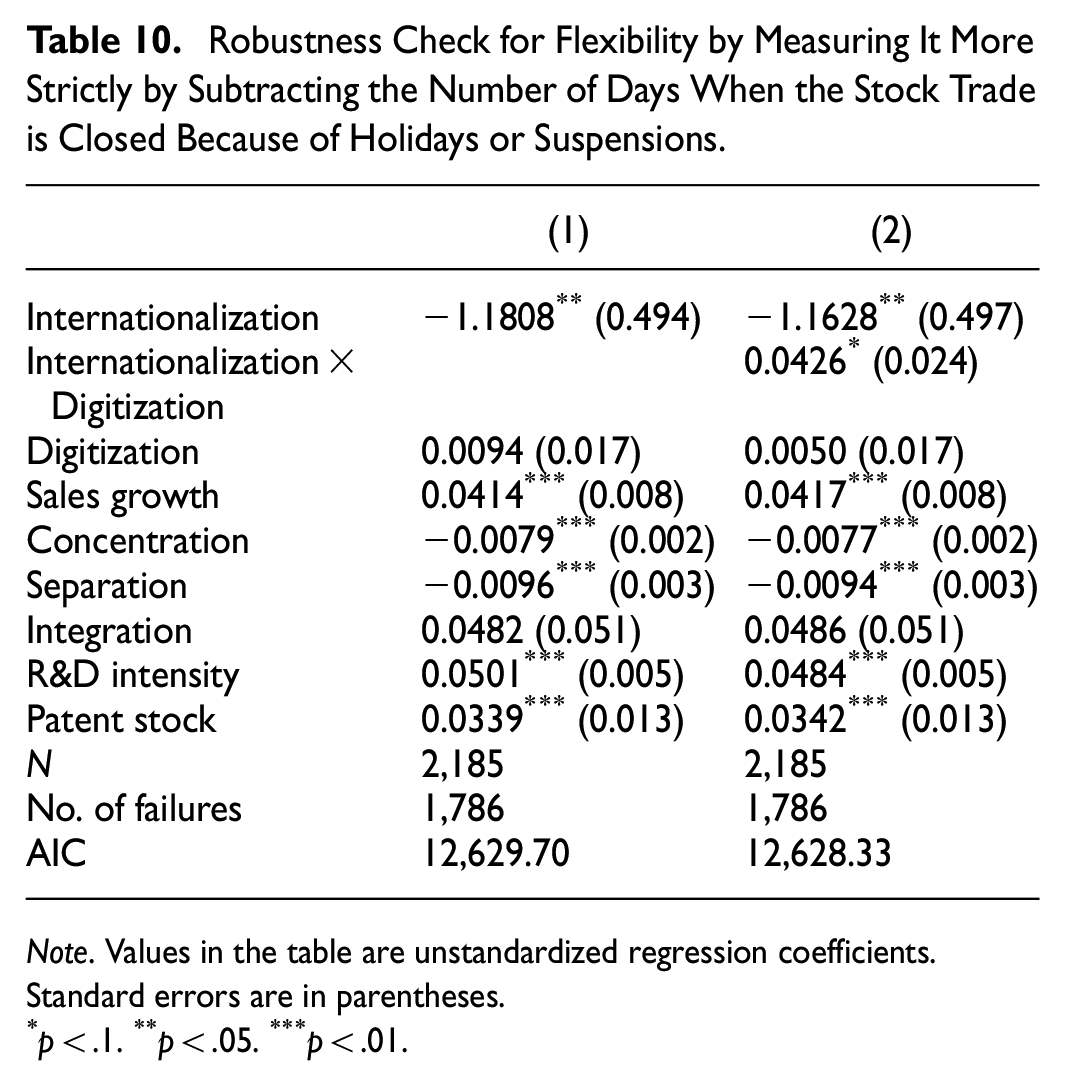

Fourth, to measure Flexibility more strictly, we subtract the number of days when the stock trade is closed because of holidays or suspensions. Results are shown in Table 10, indicating that H2 and H4 still hold.

Robustness Check for Flexibility by Measuring It More Strictly by Subtracting the Number of Days When the Stock Trade is Closed Because of Holidays or Suspensions.

Note. Values in the table are unstandardized regression coefficients. Standard errors are in parentheses.

p < .1. **p < .05. ***p < .01.

Fifth, to measure digitalization more strictly, we manually remove expressions indicating some attempts or plans about digitalization in the future, only retain expressions describing digitalization that has taken place, and subtract the negative expressions about digitalization. Tables 11 and 12 show the results, indicating that our results are robust.

Robustness Check for Stability by Measuring Digitalization More Strictly by Subtracting the Negative and Prospective Expressions about Digitalization.

Note. Values in the table are unstandardized regression coefficients. Standard errors are in parentheses.

p < .1. **p < .05. ***p < .01.

Robustness Check for Flexibility by Measuring Digitalization More Strictly by Subtracting the Negative and Prospective Expressions About Digitalization.

Note. Values in the table are unstandardized regression coefficients. Standard errors are in parentheses.

p < .1. **p < .05. ***p < .01.

Sixth, to consider the impact of technical barriers caused by de-internationalization on technology-based enterprises, we add a control variable, that is, technical barrier. It is a dummy, if the firm is in the high-tech industry classified by the National Bureau of Statistics of China, indicating that it has technical barriers, so it equals 1, otherwise 0. Tables 13 and 14 show the results, meaning that our hypotheses still hold.

Robustness Check for Stability by Considering the Impact of Technical Barrier.

Note. Values in the table are unstandardized regression coefficients. Standard errors are in parentheses.

p < .1. **p < .05. ***p < .01.

Robustness Check for Flexibility by Considering the Impact of Technical Barrier.

Note. Values in the table are unstandardized regression coefficients. Standard errors are in parentheses.

p < .1. **p < .05. ***p < .01.

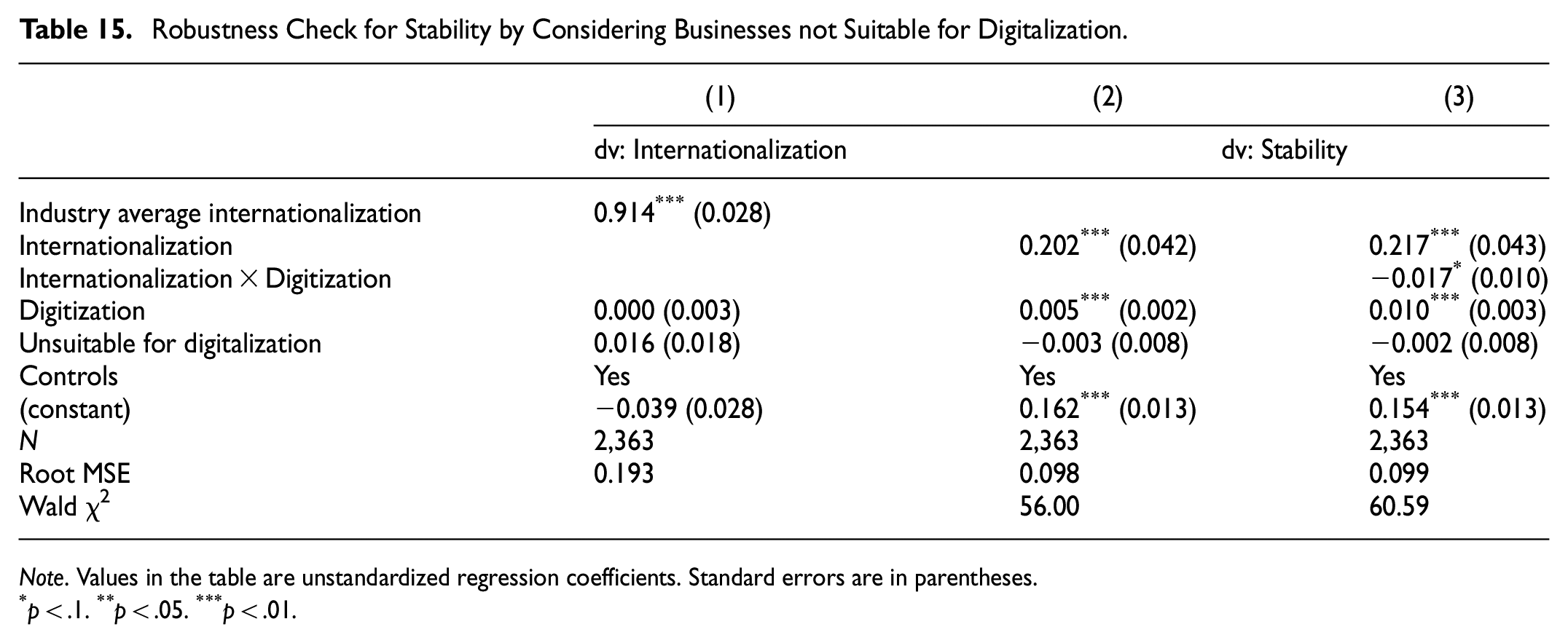

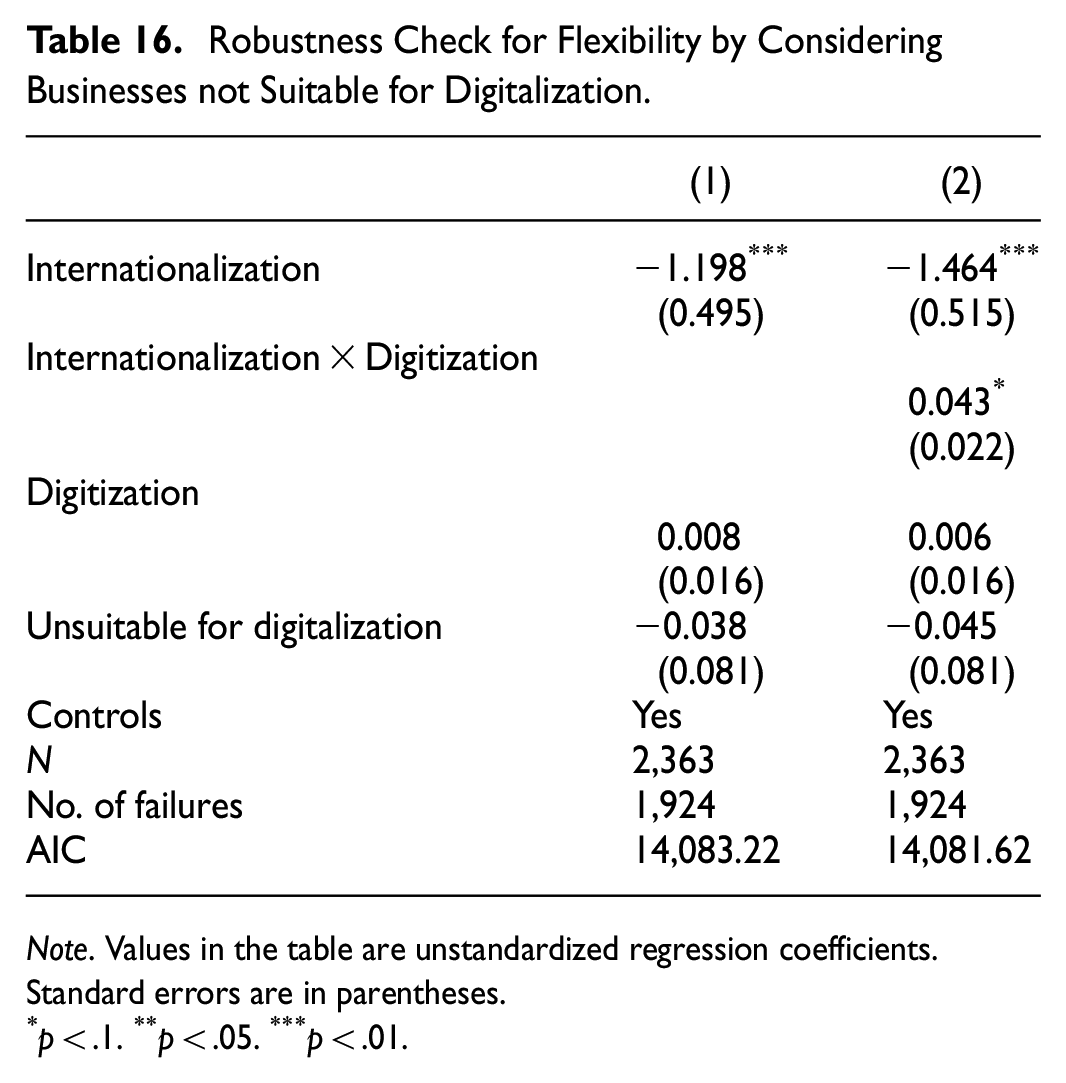

Seventh, there are some businesses not suitable for digitalization. To exclude the impact of businesses that are not suitable for digitization, we add a control variable, unsuitable for digitalization. It is a dummy, if the firm is in an industry unsuitable for digitalization, it equals 1, otherwise 0. Industries unsuitable for digitalization are classified by a report released by McKinsey&Company (2017). The report argued that industries with the lowest level of digitalization in China are mostly fragmented localized industries, such as real estate, agriculture, local service industries, and the construction industry. These industries are not very suitable for digitalization because even if the firm itself does not invest too much in digitalization, it can still make profits. Tables 15 and 16 show the results, indicating that our hypotheses still hold.

Robustness Check for Stability by Considering Businesses not Suitable for Digitalization.

Note. Values in the table are unstandardized regression coefficients. Standard errors are in parentheses.

p < .1. **p < .05. ***p < .01.

Robustness Check for Flexibility by Considering Businesses not Suitable for Digitalization.

Note. Values in the table are unstandardized regression coefficients. Standard errors are in parentheses.

p < .1. **p < .05. ***p < .01.

Discussion

Anchored in the literature on organizational resilience (DesJardine et al., 2019; Puhr & Müllner, 2022; Sajko et al., 2021), this study provides empirical evidence about the impact of internationalization on organizational resilience to the COVID-19 pandemic.

Based on Chinese listed companies’ data, our results show that internationalization has a negative effect on organizational resilience to the COVID-19 pandemic, which is consistent with prior studies on the pandemic resulting in disruptions of global supply chains (Kersan-škabić, 2022; Pujawan & Bah, 2022; Z. Xu et al., 2020), and disrupted global supply chains hurting resilience (Chowdhury et al., 2021; Hossan Chowdhury & Quaddus, 2021; Ivanov, 2022). However, this result is inconsistent with Meliciani and Tchorek (2019) and Puhr and Müllner (2022) which argued that internationalization increases resilience. There are two reasons for these mixed conclusions: first, they did not consider an endogenous problem that resilient firms usually have good financial performance and management capability, and with these characteristics, they can internationalize more easily (Bahl et al., 2021; Do et al., 2022; Wang et al., 2020); second, compared with other crises, such as the 2008 GFC and political events and political events, the pandemic is a little bit different. Although all of them are crises, and theories on crisis management and organizational resilience can also be used in our study (Buyl et al., 2019; DesJardine et al., 2019; Sajko et al., 2021), due to the different causes of these crises, they have different impacts on global supply chains. The COVID-19 pandemic is caused by the virus, and the best way to prevent its spread is isolation, so at the beginning of the pandemic, many governments adopted lockdown policies, which disrupted global supply chains heavily. The 2008 GFC was caused by the housing bubble (Scott, 2010), so global supply chains were not disrupted, and internationalization had a positive impact when firms faced the 2008 GFC (Chang et al., 2016; Mihov & Naranjo, 2019). Political events can lead to supply chain disruption in some countries or some industries, but not the whole world supply chain disruption, so firms can seek alternatives. For example, the Russo-Ukrainian War disrupted supply chains in Europe and the petroleum industry, but other regions in the world or other industries suffered fewer shocks. The pandemic made many governments all over the world apply lockdown policies, so its impact on supply chains is quite large and global, and it is hard for firms to seek alternatives immediately. Our study solves these problems and clears the relationship between internationalization and organizational resilience to the COVID-19 pandemic.

Moreover, the results highlight the moderating effect of digitalization and show that if a firm has a higher degree of digitalization, the negative effect of internationalization on firm resilience weakens. Prior studies support our results that with a higher degree of digitalization, the disruption of transportation can be alleviated by turning to contactless delivery ways, thus the supply chain is no longer disrupted (Autio et al., 2021; Quayson et al., 2020; Singh et al., 2021). Employees can continue their work through digital communication technology. Through communication online, the firm can exchange information with others of the supply chain, and find new opportunities in this special circumstance. A firm with a higher degree of digitalization can maintain its core functions, and change its business quickly to adapt to the shock.

Implications for Research

This study has several theoretical implications. First, our study presents novel insights into the determinants of organizational resilience. Previous studies have identified influencing factors contributing to organizational resilience, focusing on firm capabilities and resources (Bak et al., 2023; Brusset & Teller, 2017). However, limited scholarly attention has been dedicated to the formation processes underlying these capabilities and resources (DesJardine et al., 2019; Huang et al., 2020). In the context of the COVID-19 pandemic, which triggered global supply chain disruptions, internationalization has led to substantial loss of critical capabilities for firms, such as access to raw materials, global production, worldwide distribution, and immediate information exchange and interactions with upstream and downstream firms, consequently diminishing firms’ resilience. Additionally, our findings propose that the impact of internationalization on organizational resilience is contingent upon digitalization. Specifically, firms with a higher level of pre-shock digitalization are better positioned to mitigate the adverse effects of internationalization on post-shock organizational resilience, as digitalization aids in minimizing the loss of capabilities and resources during a pandemic. These discoveries may serve as a catalyst for future research endeavors, encouraging a nuanced exploration into how firms acquire or fail to acquire such capabilities and resources.

Second, by elucidating the correlation between internationalization and organizational resilience, our research enriches the existing literature focused on the pivotal role of internationalization within crisis management. Some scholars propose that internationalization empowers firms with operational flexibility, enabling the transfer of business activities across subsidiaries operating in diverse countries, thus potentially mitigating inherent risks (Meliciani & Tchorek, 2019; Puhr & Müllner, 2022). However, recent scholarly investigations have introduced a nuanced perspective; the disruptions in global supply chains during the pandemic have illuminated potential adverse effects, commonly termed the “dark side,” associated with internationalization (Guedhami et al., 2022; Notteboom et al., 2021). This study paves the way for scholars in crisis management to conduct further exploration regarding the dualistic nature of internationalization as a potentially double-edged sword and its effects on other pivotal firm outcomes.

Finally, our findings contribute nuanced insights to the realm of internationalization literature by identifying a situation where facets of internationalization, traditionally perceived as predominantly positive contributors to firm performance amidst crises, unexpectedly emerge as catalysts for value depreciation. The prevailing paradigm within internationalization literature often espouses the advantageous economic impacts of globalization. However, these theories inadequately address the complexities presented by a systemic event or crisis of such unprecedented magnitude as the COVID-19 pandemic. The unique circumstances of the COVID-19 pandemic underscore a paradigm in which components of internationalization, including international supply chains, human capital, and investments, transition into potential hindrances for business operations. Our revelation that internationalization exhibits markedly reduced resilience following the onset of the COVID-19 pandemic suggests that the pandemic might amplify the adverse aspects of internationalization. This examination sheds light on the unforeseen implications of internationalization in the face of a global crisis, adding depth to the understanding of its multifaceted consequences. In sum, our study enriches the growing body of literature concerning the influence of the COVID-19 pandemic on internationlization (Guedhami et al., 2022; Notteboom et al., 2021).

Implications for Practice

Our study also has practical implications for top executives of multinational corporations (MNCs) seeking to expedite recovery post-COVID-19 and fortify their organizations against potential future global crises. Firstly, the unexpected decline in MNCs’ resilience during the pandemic, as unveiled in our study, stands in contrast to the conventional understanding derived from both strategic management and international business literature regarding the perceived value of multinational entities. Preceding the COVID-19 outbreak, the primary motives driving internationalization were centered around cost minimization or acquiring learning competencies. However, post-2020, managerial perspectives should be evolved, recognizing unforeseen challenges linked with internationalization, such as travel restrictions and lockdown policies, significantly complicating global operations.

Secondly, the vulnerabilities accentuated among MNCs in our analysis hold substantial implications for managerial decision-making regarding the global footprint of their enterprises and future business strategies. A discernible shift is underway, wherein pivotal business functions once outsourced are being reconsidered for internalization, aimed at retaining control over essential organizational facets. Despite the inevitable rise in costs accompanying deglobalization, the strategic recalibration between cost and risk becomes imperative. Strategies emphasizing supply chain consolidation and a pivot toward regional trade, rather than global trade, are emerging as prudent choices in the current landscape (Kersan-škabić, 2022).

However, the contextual adaptation of firms does not advocate for a complete cessation of internationalization efforts. Firms must recognize that crises are transient phenomena. During periods of normalcy, internationalization continues to offer manifold advantages to firms, including enhanced performance (Banalieva & Dhanaraj, 2013; Graves & Shan, 2014; L. Zhou & Wu, 2014), fostering innovation (Autio et al., 2021; Piperopoulos et al., 2018; Vrontis & Christofi, 2021), and mitigating downside risks (Allen & Pantzalis, 1996; C. Zhou, 2023). Hence, a complete discontinuation of cross-border business and technological collaborations is not advisable.

Furthermore, while our study highlights the adverse impacts of internationalization, it equally underscores the positive moderating role played by digitalization. MNCs stand to benefit from an in-depth analysis derived from our research, delineating digitalization as pivotal in expediting their recovery compared to others. Specifically, when MNCs are expanding and are worrying that internationalization brings less resilience, they can compensate by investing more in digitalization. When crises come, digitalization can make a difference. The nuanced understanding of how digitalization aids in navigating through crises can serve as a compass for MNCs seeking effective strategies for resilience-building and adaptation in an ever-evolving global landscape.

Limitations and Future Research

Although this study investigates the impact of internationalization on organizational resilience to the COVID-19 pandemic and its boundary condition, there are still limitations that need to be improved and deepened in further research.

First, in this study, our focus was exclusively on Chinese-listed companies due to limitations in data availability. However, it holds significance to examine how firms in other countries respond to similar shocks. Anticipating COVID-19 transmission, governmental lockdowns, and supply chain disruptions, firms in other nations might have drawn insights from the reactions of Chinese firms. Consequently, these firms might possess distinct factors influencing organizational resilience in response to the COVID-19 pandemic, and the mechanisms at play could vary. Therefore, future research endeavors should encompass a broader and more diverse sample to confirm the universal applicability of our research conclusions.

Second, in this study, organizational resilience is measured by stock prices. Although research has shown that stock prices can reflect stakeholders’ immediate responses to new events and firm behaviors (Barrett et al., 1987; Fama, 1965; Rossi & Gunardi, 2018), the Chinese stock market is efficient (Carpenter et al., 2021), and many scholars use this method to measure organizational resilience (Buyl et al., 2019; DesJardine et al., 2019; Sajko et al., 2021), there are other qualitative research methods. In future research, we may use case studies, interviews, or other methods to further examine influencing factors for organizational resilience.

Conclusions

This study examines the impact of internationalization on organizational resilience to the COVID-19 pandemic and its boundary condition. All four hypotheses we proposed are held, that is, internationalization negatively affects two dimensions of organizational resilience (i.e., stability and flexibility), and this relationship appears to be weaker when firms have a higher level of digitalization. During the COVID-19 pandemic, the imposition of lockdown policies resulted in global supply chain disruptions, particularly affecting highly internationalized firms, hindering their rapid recovery from the shock. Digitalization offers a potential solution to mitigate these supply chain disruptions by embracing contactless delivery mechanisms and exploring novel avenues in online communication. Consequently, digitalization serves as a mitigating factor against the adverse impact of internationalization. We suggest that firms should consider crisis scenarios when making their internationalization strategies, and meanwhile, they should pay more attention to digitalization, which is envisaged to ameliorate the ramifications of unforeseen crises.

Footnotes

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: This work was supported by National Natural Science Foundation of China under Grant [number 71941023].

Ethics Statement

The authors declare that ethical permission was not applied for this study, because the research question and research design of this study do not involve any animal and human ethical issues.

Data Availability Statement

The data that support the findings of this study are available from CSMAR and Wind databases. Restrictions apply to the availability of these data, which were used under license for this study. Data are available with the permission of CSMAR and Wind.