Abstract

Fragmented governance of international value chains, operating in multiple jurisdictions, is insufficient to prevent social and environmental mismanagement. Smart Mixes, which are combinations of compulsory and voluntary measures, have been proposed as a possible means of securing environmental and social standards, but the concept has not been operationalized in the academic literature. We aim to identify the factors that have contributed to, or hindered, the performance of existing Smart Mixes in three international value chains (conflict minerals, palm oil, and bonds) using data from interviews with 32 experts, supplemented by a literature review. The results suggest that Smart Mixes are effective when they cover a specific issue under conditions in which enforcement mechanisms create a level playing field: thereby aligning public and private sector interests. The keys to success in a Smart Mix include positive interactions, harmonization, and complementary and supportive measures, which combine to motivate engagement by the private sector. We conclude that Smart Mixes can contribute to sustainability in value chains but their effectiveness is dependent on the strength of the relationships between the measures that compose them.

Plain Language Summary

Governments of consumer countries have to satisfy the wishes of their citizens for sustainability of imported products, but most of the global value chains lie outside their jurisdictions. A solution is to create Smart Mixes of national and international, compulsory, and voluntary measures that align the goals of government and industry, but the practicability of such mixes has been challenged. The aim of this contribution is to identify whether such Smart Mixes exist in the real world and examine which factors contribute to their performance. We interviewed 32 experts from three international value chains (conflict minerals, palm oil, and bonds) and found that the Smart Mix concept is indeed viable under certain conditions. This implies that Smart Mixes may indeed a tool for governments of consumer countries to achieve sustainability goals with regard to imports. Although this study was limited to three sectors, the results may be applicable in other contexts.

Introduction

In the global context of modern economies, many companies seek to lower production costs by locating their production in emerging economies that feature lax application of environmental and social regulations (Rajeev et al., 2017). As a result, damage to the environment and severe human rights violations, such as chemical spills (Cuervo-Cazurra, 2018), unsafe workplaces (Bair et al., 2020), and inhumane working conditions (Malik & Abdallah, 2019) are common. Unprecedented access to information by the consuming public has created increased pressure for companies to take responsibility for social and environmental issues related to their value chains (Boström et al., 2015; Mota et al., 2015). In a functioning market, this pressure should drive companies to adopt sustainable behavior based on the assumption that consumers will reward, either with price premiums or increased custom, the companies that adapt their practices to socially and environmentally sustainable production. However, Lingnau et al. (2019) point out that consumers’ ethical demands tend to not be reflected in their purchasing decisions, which suggests that companies will not perceive that their interests are aligned with societal demands for sustainability.

The failure of consumers to force their ethical demands with their purchasing choices means that the responsibility for ensuring that supply chains are socially and environmentally sustainable lies largely with the governments of consumer countries. This responsibility is typically addressed with legislation for sustainable production, which is one of the few options available, and one with which governments are familiar. Chandler (2006, p. 66) points out that “the whole of corporate history shows unequivocally that protection of the interests of stakeholders other than the shareholder has come not from voluntary corporate initiative, but from external pressure followed by legislation.”Hendry and Vesilind (2005) appear to agree when they point out that the strongest motivations for corporations to engage in environmentally sustainable behavior are compliance with regulations, followed by cutting costs. However, Cossart et al. (2017) noted that government efforts to force corporate social responsibility (CSR) are usually met with strong opposition from the business sector, as was evidenced by the vigorous industry campaign against the recent Swiss “Responsible Businesses Initiative” that would have extended liability over international human rights abuses and environmental harm caused by major Swiss companies and the firms they control abroad (Neghaiwi, 2020).

The ability of governments in consumer countries to legislate for CSR are complicated by international supply chains spanning multiple jurisdictions. Governments of consumer countries are therefore faced with the challenge of responding to public demand for sustainability by attempting to change the behavior of actors who they cannot influence with hard powers (Nye, 2004) such as legislation. This dilemma is further complicated by industrial production being commonly transferred to emerging economies in the Global South (Rajeev et al., 2017), where legal frameworks are often insufficiently enforced due to lack of resources or corruption (Salmivaara, 2018). A further reason for lack of enforcement is that mobile industries can relatively easily relocate to competing economies with more favorable, from their perspective, legislative environments, and take their supply of international revenue with them (Chan & Yang, 2022). Thus, governments of consumer countries have to find ways to apply their powers to promote sustainable value chains when the majority of the chain, and most of the issues, lie outside their jurisdiction, and when the enforcement of legal frameworks is perceived by those with the power to do so, to be against their own interests.

New forms of governance, such as voluntary standards, certification schemes, labels, codes of conduct, and procurement guidelines that complement and go beyond the traditional command and control regulation may contribute to finding a solution (Kinderman, 2016). Ervin et al. (2013) studied motivations for corporations to engage in voluntary environmental management by combining two frameworks: (1) the utility maximization approach, which centers on using market mechanisms to decrease cost and increase revenue; and (2) institutional theory, which considers how external pressure, such as market pressure and pressure from NGOs, direct a firm’s environmental efforts. They concluded that these frameworks are complementary and that both affect a business’ environmental practices (Ervin et al., 2013). However, as Wettstein (2015, p. 6) points out, “neither voluntary market-based approaches nor a grand legal framework on their own” can create the desired change.

These realizations have led to proposals for smart mixes (Gunningham et al., 1998) of hard and soft powers (Nye, 2004), with the concept having been mainstreamed by its inclusion in the UN guiding principles on Business and Human Rights “as an intelligent mix of national and international, binding and voluntary measures” (Ruggie, 2011, p. 8). Kinderman (2016, p. 30) commented that “a Smart Mix implies that private governance and hard law regulation are complementary, or at the very least compatible. The suggestion seems to be that a Smart Mix combines the best of both worlds: the flexibility, dynamism, innovativeness, reflexivity, and adaptability of voluntary market-based solutions and the authoritativeness, scope, and binding force of legal regulation.” On the other hand, Kinderman (2016, p. 39) also questions the political viability of the concept by questioning whether business organizations will voluntarily participate in Smart Mixes, simply because they are needed, and notes that “existing scholarship tends to over-state the convergence of public and private actors’ interests.”

However, such convergence is precisely what Ruggie (2011) suggests that governments in consumer countries must achieve if they are to influence the behavior of supply chain actors in producer countries in which social and environmental regulations are insufficiently enforced. Given the “reality check” called for by Kinderman (2016), and insufficient academic study to allow confident conclusions, there is a need to investigate the viability of the Smart Mix concept and its applicability to solving real-world problems (Home et al., 2021). The aim of this contribution is to respond to Home et al.’s (2021) challenge by exploring whether Smart Mixes exist in the real world and, if so, to evaluate their outcomes and the factors that enable or hinder their performance. To address these aims, we take a case study approach with the logic that identifying real world examples of existing Smart Mixes would support the theoretical concept, while identifying enablers and barriers to performance would provide governments of consumer countries with a tool for aligning framework conditions so that private supply chain actors voluntarily act in the interests of society and contribute to ecological and social goals.

Methodology

Analytical Framework

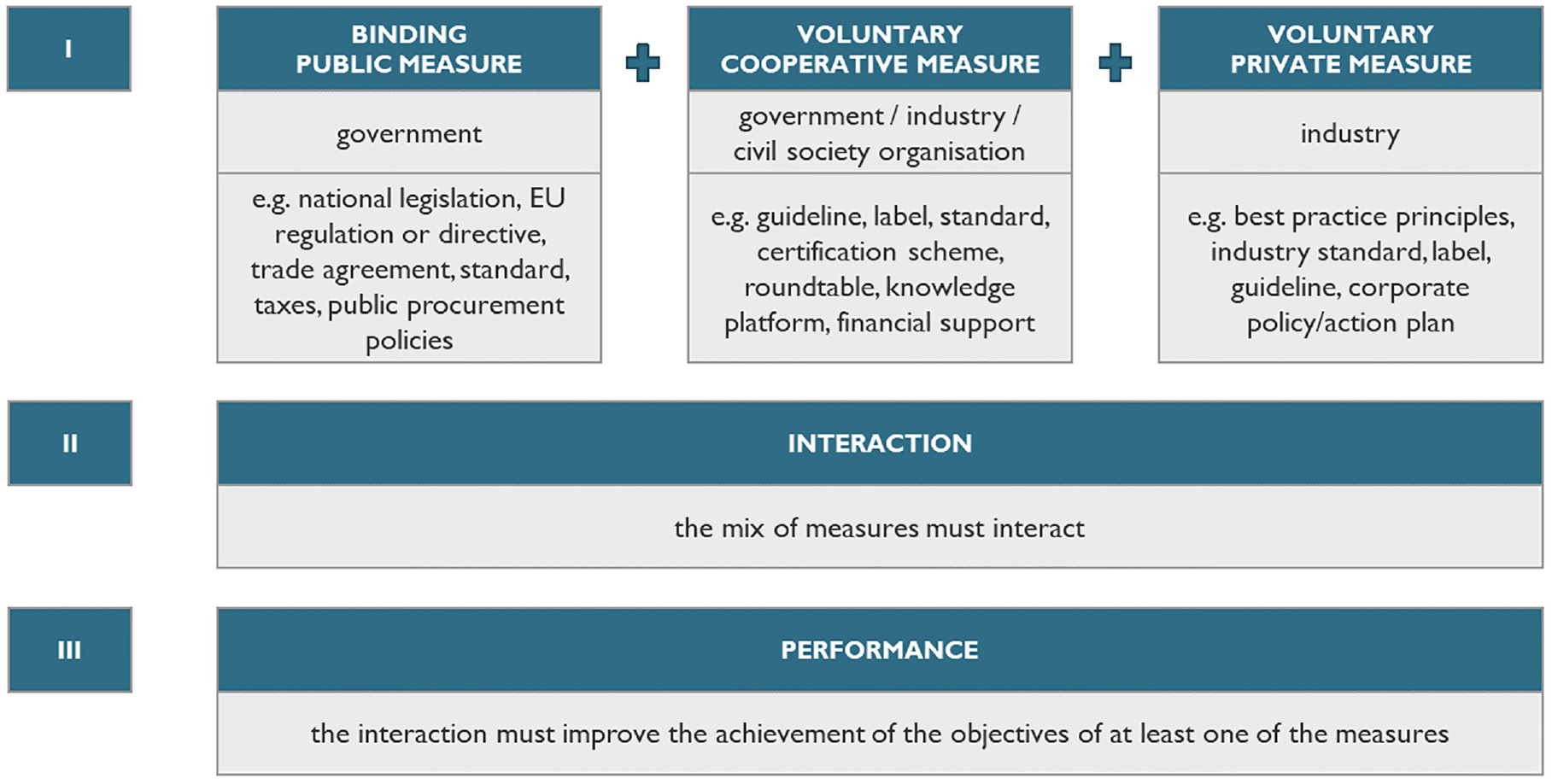

Research into the usefulness of the Smart Mix concept as a potential solution has been hampered by the lack of an accepted working definition. Gunningham et al. (1998) were the first to use the term: Smart Mix, to describe a variety of actors, levels of governance, or institutional structures with optional private measures. Ruggie (2011, p. 5) then declared that “States […] should consider a smart mix of measures—national and international, mandatory and voluntary,” which implies that a Smart Mix includes actions taken by a state in which binding and non-binding measures are combined to contribute to the achievement of goals: a position echoed by the (Swiss Federation, 2016). Rees (2019, n.p.) elaborated further to propose that a Smart Mix must “comprise measures across all those categories of ‘national and international’ and ‘mandatory and voluntary’.”Kinderman (2016, p. 29) proposed that a mix will be “smart” if there is some alignment of policy with the measure(s) that a business undertakes voluntarily and stated that, “a Smart Mix implies that private governance and hard law regulation are complementary or at the very least compatible.”Van Erp et al. (2019) returned to basic principles to define “smart” as meaning that a mix of measures addresses both the cause and solution to the problem it is intended to solve. Home et al. (2021, p. 6) synthesized these contributions into a conceptual framework that allowed them to define Smart Mixes as:

A combination of measures that includes at least one binding public measure, accompanied by at least one voluntary cooperative measure that gives guidance to the actions that should be undertaken to achieve stated objectives and at least one voluntary private measure that must have consequences outside the jurisdiction of the intervening government. The combination of measures must interact and thus improve the achievement of the objectives of at least one of the measures.

This definition, which is based around the measures that constitute the mix, how the measures interact, and the outcomes of the interactions, leads to the procedure, illustrated in Figure 1, for identifying and analyzing potential Smart Mixes.

Three criteria for a Smart Mix (Home et al., 2021).

Data Collection

Remembering the aim of this contribution, which is to exploring whether Smart Mixes, according to the definition by Home et al. (2021), we first need to identify a sector, or some sectors, in which they are likely to exist, so that they can be examined against the defining criteria. In a first step to identifying potential case studies, we conducted a broad scan of sectors characterized by international value chains to produce a list of 22 potential sectors, which are economic sectors that were found to contain voluntary and binding measures. From this list, three sectors: conflict minerals, palm oil and bonds, were selected based on the likelihood that a Smart Mix might exist within the sector. To limit the scope of the selected supply chains, the case studies were narrowed to only include measures that are relevant to European markets. Nevertheless, measures from the United States are included in the analysis of the conflict mineral case study, because the U.S. due diligence legislation has been identified as a key trigger for the emergence of several other measures, including the corresponding EU regulation. The research is exploratory, so the identified case sectors are not intended to be representative, but should rather be seen as existing examples that contribute to “proof of concept.”

Data on the selected case studies were collected by a literature review, including scientific papers, legal documents, gray literature, corporate reports, press releases, and targeted websites. The literature review was supplemented by semi-structured interviews with 32 supply chain experts, which consisted of 10 experts in conflict minerals (labeled MM 01-10), 13 in palm oil (labeled PA 01-13), and 9 in bonds (labeled FI 01-09). The sampling method of the interviewees was based on the principle of maximum variety (Patton, 1990), with at least one representative of a governmental institution, civil society organization (CSO), academia and business in the sample for each case study. Experts were selected using a snowball sampling method, which was regarded as effective due to the reasonably narrow focus of the case study sectors, which meant that sector experts were easily identifiable. Furthermore, the collected data were primarily descriptive, rather than discursive, which suggests that the snowball sampling method is appropriate. Sampling was continued until no new measures, interactions, or performance indicators were forthcoming, after which three supplementary interviews were conducted with respondents in each sector to confirm that saturation had been reached.

Following the analysis, which is described in detail in section 2.3, two confirmation workshops, with 17 and 10 of the interviewed experts respectively, were conducted to confirm that their responses had been interpreted correctly. The world café methodology was used in the workshops to facilitate discussion of the analysis, with particular regard to the transfer potential of the individual case studies to other sectors.

Analysis

Criterion I: For each case study, we compiled a long-list of all identified measures aimed at improving social and environmental standards in the value chain. We reduced this list to a smaller selection of measures that were considered relevant for the identification of potential Smart Mixes (rather than relevant for the sustainability of the sector) based on desk research and the expert interviews. Based on the first criterion of the Smart Mix concept of Home et al. (2021), we screened the selected measures and assigned them to the three different types of measures according to their actors (binding public measures; voluntary cooperative measures; voluntary private measures).

Criterion II: In a second step, we identified interactions between the selected measures. According to Home et al. (2021), interactions are a requirement for a Smart Mix. However, only positive interactions can improve the performance of the mix of measures. We considered occurrences of components/concepts referring to or demonstrating, collaboration, implementation, support, and integration as positive interactions and occurrences of refusal to cooperate or replacement of components/concepts as negative interactions.

Criterion III: In a third step, we assessed the performance of the selected measures by their contribution to the achievement of the stated objectives of the other measures. This evaluation of performance is in accordance with the definition, and should not be confused with the performance of the measure in contributing to the general achievement of a sustainable value chain.

Results

Case Study 1: Conflict Minerals

Tin, tantalum, tungsten and gold (3TG) are essential for the manufacture of components for a wide range of everyday products, such as mobile phones and jewellery. Mining and trading of 3TG minerals from conflict regions, such as the Democratic Republic of Congo (DRC), contributes to environmental pollution and serious human rights violations, including the financing of armed groups (Global Witness, 2009). Unstable or autocratic political systems with relatively weak institutions and enforcement capacity are confronted with armed rebel and militia groups taking control of mines to finance their activities (Van Bockstael, 2018). Consequently, consumers and business operators further down the value chain risk financing armed activities by purchasing products containing conflict minerals. For the purposes of this paper, 3TG minerals from conflict regions are simply referred to as “conflict minerals.” The conflict minerals case study focuses on social issues related to armed conflicts that restrict the abilities of governments to ensure human rights.

Criterion I: Presence of Each Measure Type

In the conflict mineral sector, the first criterion is met, as we identified measures of all three types (binding public; voluntary cooperative; voluntary private). Among the most important binding public measures is the Dodd-Frank Wall Street Reform and Consumer Protection Act (section 1502, 1503 and 1504) (DFA) adopted in 2010. The law limits funding sources for armed militia operating in the DRC by making it mandatory for companies to identify risks through reporting on their upstream suppliers and creating transparency. The “sanction” for non-compliance is not to get listed on the U.S. stock exchange, which also has financial implications (Rüttinger & Griestop, 2015b). The European equivalent is the EU Regulation 2017/821, which came into effect on 1 January 2021 and requires EU importers of 3TG minerals to carry out due diligence on their value chain by adhering to the recommendations of the OECD Due Diligence Guidance (OECD-D) (European Parliament, 2017).

The OECD-D is a voluntary cooperative measure that came from a government-backed multi-stakeholder process with engagement from the OECD and 11 countries of the International Conference on the Great Lakes Region (ICGLR) (OECD, 2016a). Further relevant voluntary cooperative measures are the Public-Private Alliance for Responsible Minerals Trade (PPA) and the European Partnership for Responsible Minerals (EPRM). Activities of the PPA include financing of projects aimed at producing scalable, self-sustaining systems (OECD, 2016b). The EPRM derives from a multi-stakeholder partnership and accompanies the EU Regulation 2017/821 with a main focus on project financing on the ground, for example, access to finance or cost-sharing in due diligence (EPRM, 2019).

Voluntary private measures include the Responsible Minerals Assurance Process (RMAP), which was launched in 2008 and was formerly known as Conflict-Free Smelter Initiative (CFSI); the ITRI Tin Supply Chain Initiative (iTSCi), which establishes traceability in the upstream mineral chain for 3T (International Tin Association Ltd, 2019); and the Policy on Responsible Sourcing of the London Metal Exchange (LME), which seeks to ensure that conflict minerals meet international transparency and accountability standards by requiring all LME listed companies to undertake a “Red Flag Assessment,” based on the OECD-D, by the end of 2024 (LME, 2019).

Criterion II: Interactions

In 2012, the US Securities and Exchange Commission described the due diligence measures of the OECD-D as a means of reporting under Section 1502 of the DFA (Rüttinger, Wittmer, et al., 2016). The PPA responds to the DFA and is the main actor in implementing projects and initiating dialogs on responsible sourcing. The PPA is partly comparable to the OECD when it comes to 3TG issues, but to a much smaller scale. The PPA assists initiatives such as iTSCi in developing a transparent chain of custody system (International Tin Association Ltd, 2011). iTSCi was developed on the basis of the OECD, and its “Chain of Custody” system allows buyers of minerals to obtain all the information on production and trade recommended in the OECD-D. While iTSCi covers one part of the supply chain (mining and trade, but only 3T), RMAP covers another part (smelters and refineries). Both are closely interlinked and coordinated (Rüttinger et al., 2015). The RMAP was also developed in coordination with the OECD-D and is intended to facilitate the implementation of the DFA (Rüttinger & Griestop, 2015a). The EU Regulation has been strongly inspired by the DFA and refers directly to the OECD-D in terms of due diligence (European Parliament, 2017), thereby converting the voluntary nature of the OECD-D into a binding regulation for EU importers. The EU Regulation is accompanied by the EPRM, which provides guidance for alignment with the EU Regulation, but also with the OECD-D. The LME policy is also based on the OECD-D and was introduced in response to the EU Regulation (LME, 2019).

Criterion III: Performance

Analyzing the impact of certain measures in the conflict minerals sector is difficult due to a lack of comprehensive baseline-data and comprehensive qualitative studies. Further difficulties in assigning impacts to specific measures arise from the following intervening variables: regulations of the Congolese government; sharp fall in commodity prices of 3T; shift in employment from 3T to gold; changes in the militarization of mining sites; changes in the conflict and the actors involved; and the associated negative effects on the region (Rüttinger & Scholl, 2016). With regard to the DFA, the measure can be considered successful in terms of due diligence, but the DFA’s influence on reducing conflict financing is not clear. Reports and studies often show considerable differences and are sometimes contradictory. According to a comparison of two IPIS studies (impact of armed interference & responsible sourcing) by Rüttinger and Scholl (2016), there has been no significant decline in the militarization of mining sites in the entire (artisanal) mining sector. The decline observed in the 3T sector is due to the decline in 3T production, and militarization has shifted from 3T to gold. Despite methodological challenges, it has become clear that the introduction of the DFA has created a “window of opportunity” for various processes and regulations in the conflict minerals sector and strengthened the understanding of due diligence in mineral supply chains (Rüttinger & Scholl, 2016). The DFA gave a new dynamic to the global debate on conflict raw materials and triggered discussions and new legislative proposals far beyond the United States (Rüttinger & Griestop, 2015b). The OECD-D is considered as a best practice governance measure (Cruz Vieyra & Masson, 2014), which is referenced and used as a basis for several initiatives and legislation (e.g., EU Regulation 2017/821). The OECD delivered a common and practically relevant benchmark that was negotiated with multiple stakeholders. The results showed that part of its success was the legitimate authority of the OECD to initiate such a reference document and the participative process under which the benchmark was developed (MM-05; MM-06; MM-07).

Due to the involvement of various stakeholders in the regular reviews, the guidelines have a high degree of legitimacy (Rüttinger, Wittmer, et al., 2016). Several initiatives have demonstrated that responsible sourcing projects can be implemented in conflict regions and that they can have a positive impact on the ground. Their impact includes not only the supply of conflict-free minerals, but also investment, improved safety standards, transparent prices, and tax payments (Manhart & Schleicher, 2013). One of the key voluntary private measures is RMAP, which contributes to enabling companies to trace the origin of raw materials. The standard already covers a relatively large part of global gold mining for example and there is still potential for further expansion. While it is difficult to measure impact, RMAP is on track to achieve its goal of supporting companies in identifying responsibly sourced minerals (Rüttinger & Griestop, 2015a).

Synthesis

In the conflict minerals sector, we identified a Smart Mix that aims at conflict-free mineral extraction (Figure 2). We identified numerous positive interactions, whereby the measures support, recognize, and complement each other. Each measure focuses on a specific function in order to jointly improve value chain standards. Alongside the OECD-D, the DFA is of major importance for effective interaction between the measures. With its leverage function, it plays an important role in the Smart Mix. The introduction of the DFA has given many initiatives an impulse, strengthened them and thus created a high degree of dynamism in the sector (Rüttinger et al., 2016). However, the lack of comprehensive baseline data and qualitative studies makes it difficult to analyse the impact of specific measures, so while it can be considered effective in terms of due diligence, the impact of the measures on the reduction of conflict financing cannot be clearly evaluated. An emerging Smart Mix was identified at the EU level as a combination of the EU Regulation, the OECD-D and voluntary private measures such as the LME policy. However, since we cannot yet evaluate the performance of the EU regulation, this mix should be considered a potential future Smart Mix.

Smart Mix identified in the 3TG sector (own figure).

Case Study II: Palm Oil

Palm oil is the most widely used vegetable oil, accounting for around a third of global production (USDA Foreign Agricultural Service, 2018). The expansion of oil palm plantations is important for the economic development of the producing countries (Pacheco et al., 2018). However, its economic significance is countered by a number of negative ecological and social effects. These include, among others, the oil palm cultivation in large monocultures, deforestation of tropical rainforests, fire clearance, intensive use of fertilizers and pesticides and the violation of land and labor rights (Gottwald, 2018; Moreno-Peñaranda et al., 2015; Silva-Castañeda, 2012).

Criterion I: Presence of Each Measure Type

We also identified measures of all three measure types in the palm oil sector. A binding public measure in the palm oil sector is the EU Renewable Energy Directive 2009/28/EC (RED), which was adopted in 2009 for the period of 2010 to 2020 (Stattman et al., 2018). The legislation required economic operations using raw material, including crude palm oil to be used as biodiesel in the EU market, to be certified according to a sustainability standard recognized by the European Commission (Pacheco et al., 2018). The revised Renewable Energy Directive 2018/2001/EU (RED II) entered into force in December 2018. In RED II, the issue of indirect land use change (ILUC) was addressed by setting gradually increasing limits on biofuels, bioliquids and biomass fuels with a significant expansion in land with high carbon stock (ILUC-risk) (European Commission, 2019b). In the Delegated Regulation (EU) 2019/807, the European Commission specified the sustainability criteria for biofuels and classified palm oil as unsustainable (European Commission, 2019a). Two binding public measures in producer countries are the Indonesian Sustainable Palm Oil (ISPO) and Malaysia Sustainable Palm Oil (MSPO), which are standard and certification schemes that were implemented in 2011 and 2013 respectively.

The Roundtable on Sustainable Palm Oil (RSPO) is a voluntary cooperative measure that was implemented in 2002 by several industry participants and the Worldwide Fund for Nature (WWF; Pye, 2016). The RSPO Supply Chain Certification System verifies compliance with its principles and criteria (P&C) through third-party monitoring and certification (Moreno-Peñaranda et al., 2015; Pacheco et al., 2018). The International Sustainability and Carbon Certification (ISCC) is another voluntary cooperative measure that is applicable worldwide and covers all types of agricultural, forestry and other raw materials (ISCC e.V., 2019). Further measures are the Amsterdam Declarations (AD), which are non-legally-binding political commitments (Partnerships for Forests, 2019) to eliminating deforestation and supporting sustainable palm oil (Amsterdam Declarations Partnership, 2015a, 2015b); the European Sustainable Palm Oil (ESPO) project with the objective of achieving “100 percent sustainable palm oil in Europe by 2020” (ESPO, 2019, n.p); and the Tropical Forest Alliance (TFA) founded by the Consumer Goods Forum (CGF) and the US government to support the partners’ zero net deforestation commitments.

The CGF itself is a voluntary private measure as it is a global industry network, with approximately 400 consumer goods manufacturers and retailers, that published the Sustainable Palm Oil Sourcing Guidelines in 2015 to help companies develop their own policies for effectively sourcing palm oil (CGF, 2015). Another measure of this type is the No Deforestation, No Peat, No Exploitation Policy (NDPE), which is an example of a corporate sourcing policy. Most large international palm oil traders/refiners have adopted NDPE sourcing policies, with Wilmar being the first company to come out of the Sustainable Palm Oil Manifesto (SPOM) and launching the NDPE in 2013 (Steinweg et al., 2017).

Criterion II: Interactions

The RSPO engages with other initiatives in the palm oil sector and serves as a platform for dialog and to support thinking processes (PA-02; PA-11; PA-10). The voluntary private measure: CGF, recommends the RSPO as a minimum standard and the NDPE refers to some of the RSPO principles (Wilmar International Ltd, 2013). However, the content and objectives of the measures are not consistent, and they do not interact in a way that can be expected to contribute to goal achievement. The RSPO developed “add-on schemes” to include additional requirements for sustainable palm oil: one of which is the RSPO RED, which was introduced to the European market in 2014 to ensure compliance with the requirements of the EU RED (RSPO, 2012, 2019). The ISCC is also recognized by EU RED as proof of compliance with the sustainability criteria for biofuels and bioliquids defined by the EU (ISCC e.V., 2019). RSPO and ISCC are both voluntary international standards that are increasingly used by consumer countries to verify the origin of their palm oil imports. They are therefore in line with their (supra)-national measures (EU RED, ESPO), but are not consistent with the standards of producer countries (ISPO, MSPO) (Pacheco et al., 2018). Hardly any positive interaction could be identified between the binding public measures: ISPO and MSPO, and the other measures. In contrast, negative interactions could be identified, as shown by the reaction of the Indonesian government to the industry initiative; the Indonesian Palm Oil Pledge (IPOP). Instead of cooperating with, or promoting, this initiative, the Government accused IPOP of violating its authority to set standards. They argued with concern about the emergence of a cartel dominated by foreign interests, non-compliance with Indonesian laws, and overly strict regulations beyond the means of small farmers (Hidayat et al., 2017). With respect to the ISPO, it is assumed that the national standard has not been launched to implement the global private RSPO standard at national level, but to challenge or replace it (Hospes, 2014; Luttrell et al., 2018). Compared to the RSPO, the ISPO’s requirements regarding clearing of (primary) forests and peatlands are considered to be less demanding (PA-08), as RSPO requires a number of sustainability criteria in addition to compliance with national laws (Efeca, 2016). In general, harmonization between the RSPO and national initiatives in producing countries is missing. There is no attempt for co-certification of the national standards ISPO and MSPO with the RSPO, which leads to a doubling of standard requirements (PA-05).

Criterion III: Performance

Currently, 5.17 million hectares of palm oil production are ISPO certified, which represents growth of over 140% from 2017 (ESPO, 2019; Reuters, 2019). The growth rate in Malaysia is even higher with over 450% from 2017 to 2019 and more than half of the palm oil plantation area in Malaysia is MSPO certified (ESPO, 2019; MOPCC, 2019). The objective of the MSPO is “to establish and operate a sustainable palm oil certification scheme in Malaysia” (MPOCC, 2017, p. 5), which can be considered to be successful, given the increasing area of Malaysian plantations that are MSPO certified. However, the challenge of achieving objectives depends not only on how high the individual measures set their targets, but also on the requirements for compliance with their standards. Compared to the RSPO, the ISPO’s requirements regarding clearing of (primary) forests and peatlands are considered to be less demanding (PA-08), as RSPO requires a number of sustainability criteria in addition to compliance with national laws (Efeca, 2016). Around 19% (2.91 million hectares) of global palm oil is certified under the RSPO standard (RSPO, 2019). Nevertheless, given continuing reports about violations of the P&C by certified members, which are often published by environmental and social NGOs overseeing the industry (see e.g., Amnesty International Ltd, 2016), the RSPO’s role and impact on improving sustainability in the palm oil value chain remains contentious (Hidayat et al., 2017; Ruysschaert & Salles, 2014). The objective of the ESPO to increase the share of certified sustainable palm oil in Europe to 100% by 2020 has almost been achieved with 99% of palm oil imported into Europe traceable to the oil mill, and 84% of palm oil is covered by the companies’ sustainability policies, such as NDPE (ESPO, 2019).

Nevertheless, despite these efforts, the palm oil industry cannot be considered as sustainable, according to Pye (2019). The above-mentioned measures certify large-scale monocultures as sustainable if they meet certain management criteria. Pye (2019, p. 219) argues that “better management of monocultures does not prevent the conversion to monocultures,” which causes a dramatic decline in biodiversity and release of carbon dioxide.

Synthesis

In line with the Smart Mix concept developed by Home et al. (2021), no Smart Mix could be identified in the palm oil sector (Figure 3) because of the lack of positive interactions between the measures, especially between the ISPO and the MSPO. In general, the governments of palm oil producing countries are not in favor of private zero-deforestation initiatives and have criticized the European Parliament’s vote to exclude palm oil as biofuel (CPOPC, 2019; Pacheco et al., 2018). In general, a disharmony between the voluntary standards and government regulations in the producer countries was identified, which leads to a doubling of standard requirements, as well as to irritation among the actors in the chain and ultimately to further conflicts (Pacheco et al., 2018; Pirard et al., 2015).

No Smart Mix identified in the palm oil sector (own figure).

Case Study III: Bonds

Unlocking private finance, worth trillions of dollars, is repeatedly mentioned in the public discourse as a critical element in achieving sustainability goals, such as the SDGs and the Paris Agreement (Clark et al., 2018; UNEP, 2018). In addition, the reorientation of private capital toward more sustainable investments could help to mitigate the exposure and vulnerability to environmental disasters and ensure the stability of the financial system by promoting greater transparency and long-termism (European Commission, 2018a). We focus in this case study on the so-called “green bonds” and basic measures to define, identify, or label them. Bonds are fixed-income debt instruments that represent a debt security, similar to a loan, made by an investor to a corporate or governmental borrower. Green bonds are bonds whose proceeds are used to finance projects or business activities that have a positive impact on the environment or help to mitigate the effects of climate change (Park, 2018). The scope of the bond case study is confined to the product level, which includes measures directed at the financial instrument, the bond. Consequently, the following analysis does not cover instruments at the corporate level, which are measures directed at financial institutions or companies, such as disclosure regulations.

Criterion I: Presence of Each Measure Type

We did not identify any binding public measures in the bond market. However, the European Commission released an Action Plan (AP) on sustainable finance in 2018. The Action Plan combines legislative and non-legislative actions (European Commission, 2018b). The EU AP measures presented hereafter are proposals or recommendations by the EU Technical Expert Group and therefore not yet implemented. A binding public measure of the EU AP is the so called “Taxonomy.” The proposal establishes a framework for a common definition of environmentally sustainable economic activities for investment purposes at EU level, including the definition of “green” in the context of green finance (European Commission, 2018d). Another EU AP proposal is to amend Regulation (EU) 2016/1011 on low carbon benchmarks and positive carbon impact benchmarks. The objective of the proposal is to prevent greenwashing by introducing minimum requirements and standards: thus, ensuring better information on the carbon footprint and ESG (Environmental, Social, and Governance) factors relating to assets in which the index invests (Vander Stichele, 2018).

A voluntary cooperative measure of the EU AP is the Green Bond Standard (EU-GBS). The four elements of the standard are (1) alignment with EU-taxonomy, (2) publication of a Green Bond Framework, (3) mandatory reporting (allocation and impact) and (4) mandatory verification of the allocation report by an external reviewer (European Commission, 2019c). Among the established measures that are not part of the EU AP is the Climate Bonds Initiative’s (CBI) Standard and Taxonomy. The CBI is an investor-focused not-for-profit organization launched in 2009 (CBI, 2019d), which receives funding from non-profit and public organizations (CBI, 2019e) to promote investment in projects and assets that aim for climate change solutions (CBI, 2019a).

A voluntary private measure is the creation of the Green Bond Principles (GBP), which are voluntary best practice principles developed by a consortium of investment banks in 2014 (CBI, 2019c). Green bond indices also belong to this type of measure, such as the Bloomberg Barclays MSCI Green Bond Index and the S&P Green Bond Index. They track the global green bond market and can be taken as a benchmark with the caveat that the green bonds are only one segment of the green bond market (S&P Dow Jones Indices LLC, 2016).

Criterion II: Interactions

The CBI supports the GBP, which serves as the basis for the Climate Bonds Standard (CBI, 2019c). While the GBP have in the past promoted a market-based approach of self-definitions, jurisdictions like the EU develop clear and binding technical criteria with specific quantitative thresholds. The GBP itself contain high level categories for eligible green projects and cooperate where necessary with other parties that provide complementary definitions, taxonomies and standards (ICMA, 2018). Many regional standards are based on the GBP, and the EU-GBS is also strongly inspired by the governance principles (FI-07). The EU AP includes several measures that are inspired by existing initiatives, such as the EU Taxonomy, which builds upon the Climate Bonds Taxonomy. The CBI welcomes this new EU measure and claims full alignment with it (CBI, 2019b). Furthermore, the CBI was heavily involved in the development of the AP (FI-07; FI-08). Another measure of the EU AP are the low carbon benchmarks and positive carbon impact benchmarks. However, they are not yet in place and the absence of harmonized rules has led to divergent standards for such benchmarks and confusion among investors in the past (European Commission, 2018c). For bonds to be considered as “green” in the S&P Green Bond Index, they must meet the Climate Bonds Standard criteria. The eligibility criteria of the Bloomberg Barclays MSCI Green Bond Index on the other hand, incorporate the GBP (Park, 2018).

Criterion III: Performance

The Bloomberg Barclays MSCI Green Bond Index was voted best index at the Green Bond Awards 2018 (Field Gibson Media Ltd, 2018). Since there is no universally agreed definition for green bonds, the index provider accepts and excludes bonds according to its own criteria. An EU harmonized standard for transparent methodologies for such benchmarks would have the potential to reduce the asymmetry of information between investors, index providers and issuers, reduce the current fragmentation of the market, and improve the quality and comparability of published ESG information (European Commission, 2018c). However, the measures of the EU AP have not yet entered into force so it is not possible to evaluate their performance. In principle, the established initiatives have all led to greater transparency in the financial market and have influenced governance structures as well as impact reporting and external verification (FI-06). GBP, for example, is also used for other products, such as loans (FI-06), and the CBI is trusted by financial market players (FI-08). The performance of these measures to achieve their stated objectives, such as “to mobilize the largest capital market of all: the $100 trillion bond market for climate change solutions” (CBI, 2019a, n.p.), is difficult to assess because these measures are still new and their impact on a growing green bond market cannot be isolated within this study. The participating experts repeatedly emphasized that sustainable investments in the financial sector are still considered a niche products (Fi-06; FI-08; FI-09). Clark et al. (2018) conducted a literature review to identify barriers for unlocking private finance. The results include, among others, short-termism, information gaps, absence of binding commitments, and inconsistent and counterintuitive polices. This is in line with Busch et al. (2015), who refer to a reorientation toward long-termism and ESG data becoming more trustworthy.

Synthesis

The EU AP measures in the bond market are not yet in force so there are insufficient binding public measures means for a Smart Mix to be identified according to the criteria outlined by Home et al. (2021). Although the three established measures (CBI, GBP, green bond indices) interact very positively with each other, they are all voluntary. However, the EU AP measures have potential to be part of a potential future Smart Mix if the new EU AP measures interact with the established initiatives and thus jointly enable them to achieve their objectives more effectively. The former is already recognizable, as the gray arrows in Figure 4 show.

Potential future Smart Mix in the bond market (own figure).

Discussion and Conclusions

This study is subject to some limitations. As the study is based on three case studies, the conclusions drawn are only valid for these and their respective scope. In addition, we selected the cases based on indications from the initial screening that a Smart Mix might exist in the sectors, so we cannot exclude that the similarities and differences we found are due to selection bias. A further limitation concerns the scope, as we conducted a maximum of 13 interviews per case study. We deliberately chose these interview partners on the basis of their expert knowledge, so the data collected is rich. However, we were not able to interview people directly affected by the violations of environmental and social standards, such as miners or farm workers. It will be the task of future research to investigate applications of Smart Mixes in sufficient depth to evaluate whether the intended improvement of living conditions for supply chain workers in supplier countries become manifest.

A further limitation is that a comprehensive analysis of the performance of the measures, in particular the chain of cause and effect, is the difficulty of finding reliable data. This challenge is not unique to this study, and studies assessing the impact of measures such as certification schemes, are hardly available in the certification literature (Oya et al., 2018). Our performance assessment is based on expert interviews, with the inherent bias that experts use their individual points of reference. For example, some referred to quantifiable parameters, such as the number of members participating in an initiative, the estimated share of certified precious metals dependent on the total market, or the number of companies publicly reporting. Other respondents referred to more qualitative parameters describing the change on the ground, such as if the livelihoods of the mine workers have improved, if they have better access to healthcare or if violence reduced. The interviews were supplemented by reviewing published reports referring to achievement of objectives, which were often published by stakeholders with an interest in the measures, so may be unreliable. Objectively assessment of the performance of Smart Mixes is an important area for future research but one that will require considerable commitment of resources due to the scarcity of impact evaluation studies and baseline data. Despite these limitations, the richness of the findings and the consistency of the responses with regard to the fundamental principles gives us confidence to make some generalizations of the results.

A key finding of this study is the importance of binding public measures, which were found to be fundamental to the identified Smart Mix in the conflict minerals sector. The introduction of the DFA has given many initiatives an impulse and strengthened them (Rüttinger, Griestop & Scholl, 2016). Legal institutions that impose regulatory oversight and sanction misconduct are also highlighted by Dupont and Karpoff (2020) as one of the building blocks for trust in the financial market. The bond market, in which industry engagement has been high, currently lacks supporting legislation that could create a “level playing field” by preventing stakeholders who choose not to comply with voluntary measures from gaining a competitive advantage. Financial actors, in particular banks and institutional investors who are engaged in responsible investments, have expressed the need for government regulation. They are looking for concrete criteria that allow for a common understanding and greater transparency (FI-01; FI-02; FI-03). The unregulated situation has so far led different providers to come up with different methodologies, metrics, and outcomes in their sustainability assessments. Due to the large amount of leeway, the risk of greenwashing is currently still high (FI-08). However, this might change with the planned EU AP measures.

Even if all the required elements for a Smart Mix are in place, a lack of positive interactions or even the presence of negative interactions, such as was found in the palm oil case study, can lead to the goals not being met. Competition between existing standards, certification schemes, or labels can be considered as negative interaction as it might lead to a race to the bottom. Compared to the RSPO, the ISPO’s requirements regarding clearing of (primary) forests and peatlands are considered to be less demanding (PA-08), as RSPO requires a number of sustainability criteria in addition to compliance with national laws (Efeca, 2016). This makes it tempting to source palm oil from competing but less stringent certification systems. The approach of the EU RED to outsource monitoring and certification to different private certification schemes can also motivate companies to choose the least demanding standard that still gives them access to the European market, instead of adopting the best available standard in terms of improving environmental and social standards (Stattman et al., 2018). A lack of positive interactions is characterized by parallel, uncoordinated measures, which leads to irritation among the value chain actors and causes further conflicts.

In the case studies where, in contrast, positive interactions were identified, the importance of voluntary cooperative measures, such as multi-stakeholder initiatives, became clear. These measures are often the link between binding public and voluntary private measures, which only in a few cases interact directly with each other. We observed this in the conflict minerals case study where several initiatives are in line with the OECD-D. This result supports the Smart Mix concept developed by Home et al. (2021) by underlining the value of voluntary cooperative measures in Smart Mixes. Rotter et al. (2014) also emphasize the importance of joint cooperation and dialog among and beyond industry peers. It is not only seen as a basis for moral legitimacy, joint strategies can create win-win situations for all stakeholders.

To improve the environmental and social standards in value chains, we observed the fundamental condition of an accepted definition of the more “sustainable” product. The product-specific requirements for a sustainable value chain should be universally agreed, which can be achieved, for example, by a binding regulation or by a commonly accepted standard. In the bond market for example, a definition for “green bonds” is currently missing, but will probably implemented in the near future through the EU taxonomy. In the palm oil sector, the sustainable option is defined through certification systems. However, disharmony of procurement requirements between different measures, such as “sustainable,”“clean,” and “legal” supply, leads to irritation among the value chain actors (Pacheco et al., 2018; Pirard et al., 2015). The same applies to different definitions regarding a deforestation-free supply chain, such as “zero deforestation” or “zero net deforestation” (Pacheco et al., 2018). Furthermore, a definition that is too concrete can also cause difficulties. Due to the naming of a certain producer country in the DFA, namely the DRC, companies switched to other countries for the procurement of raw materials, with the result that the population working in the DRC was excluded from the world economy by industrial mining (Giller & Tost, 2019; Manhart & Schleicher, 2013). Hence, the DFA was very effective regarding the legislative text, nevertheless, it could have been even more effective if the definition had been broadened and mainstreamed among more countries, sectors, and companies (MM-04; MM-06).

The results further indicate that sustainably sourced products must be clearly identifiable and traceable along the entire value chain. Certification schemes and labels are valuable measures to identify these products and thus distinguish them from the unsustainable option. iTSCi for example is the most widely used program for tracing 3T minerals from mine to smelter and is successfully working to achieve its goal of making it easier for companies to meet the requirements of the OECD as well as international and national legislation. By marking minerals and the associated traceability, iTSCi counteracts the exclusion of the DRC and surrounding countries by the DFA (Rüttinger et al., 2015).

In addition, we observed the importance of effective monitoring and verification mechanisms to ensure that operations and products comply with the requirements of the defined sustainable value chain. As claimed by Von Geibler (2013), monitoring systems support the effectiveness of standard setting by providing scientific proof. Bartley (2014) stresses the importance of government involvement with regard to monitoring and enforcement. This is in line with a finding by Van der Ven (2015) showing that voluntary private measures (in this case industry-funded eco-labeling organizations) perform worse than public measures in involving scientists and experts in the development of standards and in selecting competent auditors to ensure compliance. However, in the palm oil sector, the binding public measures in producer countries suffer from a lack of monitoring and sanctioning capacity and from failures to enforce their certification schemes (PA-01; PA-07; PA-05). Hofmann et al. (2015) recommend third-party certification organizations to be used for compliance measures.

The aim of monitoring, in this context, is to relieve upstream companies, which have few resources available, of cost pressure and to guarantee the reliability of certification. Furthermore, enforcement is indispensable to guarantee that the requirements are met. It is essential that binding measures are indeed binding, that misconduct is followed by consequences, and that all actors in the value chain are aware of them and strive to avoid sanctions. Penalizing unsustainable behavior has the effect of leveling the playing field by protecting industry actors who choose the, usually more costly, sustainable options. Lockie et al. (2015) argue that demanding compliance with stricter national legislations will be meaningless if state monitoring and enforcement mechanisms are weak, as there is no requirement for certifying business to demonstrate legal compliance. In the same vein, Braithwaite (2006) maintains that limited capacity of the public sector to monitor and enforce regulations and/or adherence to the less demanding of public and private standards can result in regulatory failure.

According to the interviewed palm oil experts sanctioning mechanisms of the ISPO and the MSPO are poor or non-existent, given that violations of the commitments are disregarded (PA-01; PA-08; PA-07). The criticism is in line with Hidayat et al. (2017) pointing to weak administrative structures of the ISPO as a cause for its inability to influence enforcement mechanisms. Political instability, the lack of strong state institutions, corruption, and overriding political interests are major barriers to the enforcement of social and environmental standards in producer countries (MM-06). In the conflict minerals sector, however, the DFA can be regarded as a single intervention that had a significant impact on the enforcement of due diligence. Enforcement through regulatory and legal sanctions has been a key factor for effectiveness in the sector (MM-10).

The performance of Smart Mixes was found to be enhanced when the interests of industry and government become aligned. This can be achieved by the existence of guidelines for the industry, which are supported by effectively implemented legislation. However, alignment between government and industry does not necessarily contribute to sustainability, such as was demonstrated in the case study on palm oil. In that case, the interests of the industry align with the interests of the government in the producer countries: namely keeping production at a high level, which is especially important when the product is a major contributor to the country’s economy. This finding is in line with Hidayat et al. (2017) who identified competing interests together with bureaucratic and technical complexity, corruption, decentralized authoritative responsibilities and reluctance to strictly elaborate sustainability ambitions as barriers for solving sustainability problems in the palm oil sector.

The scope of a Smart Mix is important in that mixes of measures with rather specific goals work well due to their narrow scope but can be bypassed and therefore do often not solve sustainability problems in practice. In the conflict minerals case, for example, the Smart Mix identified was effective in terms of due diligence with measures aiming to stop conflict financing. However, conflict-free mineral extraction only covers a few environmental and social issues related to the value chain activities. In cases in which measures, or combinations of measures, were created to address the whole of a complex value chain, such as in the palm oil sector, it proved to be too difficult to align the interests of the industry stakeholders, who consequently reduced their engagement and sought to avoid restrictions. Smart Mixes appear to be effective when they cover a very specific topic under conditions in which enforcement mechanisms are in place and are effective to create a level playing field: thereby aligning the goals of the public and private sectors.

Revisiting the aims of this study, which were to analyse governance structures in value chains of different sectors, based on the concept of Smart Mixes of Home et al. (2021) and to answer the two research questions: (1) Do Smart Mixes exist in the sector of conflict minerals, palm oil and the bond market? (2) What are factors that enable or hinder the performance of existing mixes of measures that aim at improving environmental and social standards in international value chains? We conclude that the Smart Mixes concept is fundamentally sound and have identified a Smart Mix in the conflict mineral sector and a potential future Smart Mix in the bond market. Among our key findings is that the Smart Mix in the conflict mineral sector, works well due to its narrow scope, but can be bypassed which hinders the ability to solve sustainability issues in practice. Such outcomes are particularly likely in countries with unstable or autocratic political systems with relatively weak institutions and enforcement capacities. The palm oil case highlighted the need for positive interactions and effective enforcement of the “binding” measures, which suggests the value of improving regulatory performance, such as through stricter formulation, implementation, monitoring and in particular enforcement. The keys to success of Smart Mixes are positive interactions, harmonization, and complementary and supportive measures. Our results contribute to the scientific debate with real-world examples of Smart Mixes and informs governments of consumer countries who might wish to apply the Smart Mix concept to improve social and environmental standards of value chains in other sectors.

Footnotes

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: The primary research in this submission was funded by the Swiss National Science Foundation (SNSF) through the project “Enhancing supply chain stability, resilience and sustainability through improved sub-supplier management -chocolate and cotton apparel case studies” within the National Research Program 73 “Sustainable Economy” (grant number NFP73: 172451). The literature review part of this submission was co-funded by the European Commission as part of the horizon Europe: Farm to fork, Communities Development and Climate Action, in the ENFASYS project with grant number 101059589; and the Swiss National Science Foundation. The views and opinions expressed herein are those of the authors and do not necessarily reflect those of the European Commission or SNSF. The designations and terminology employed may not conform to European Commission or SNSF practice and do not imply the expression of any opinion whatsoever on the part of the European Commission or SNSF. Neither SNSF nor the European Commission are liable for any use that may be made of the information contained herein.

Data Availability Statement

Data sharing not applicable to this article as no datasets were generated or analyzed during the current study.