Abstract

Syndication among venture capital firms (VCFs) is increasingly prevailing in recent years, especially in emerging markets like China. Some of the VCFs have to syndicate with “worse performers” despite the “better performer preference.” The primary aim of this article is to contribute to our understanding of the impact performance gap among syndicated VCFs on formulation and duration of syndicate. The data consist of over 295,000 pair of VCFs syndicated in China mainland from 2000 to 2020. We find the negative effect of performance gap on the propensity of syndication with self-categorization of VCFs as the moderator. The key contribution of this paper is to test the significance of homogenous performance in syndication. This study advances the knowledge of agency in collaboration and sheds new light on organizational performance feedback in venture capital markets.

Plain Language Summary

This paper examines the disparity of performance in syndication among venture capital firms (VCFs). Econometric regressions are used in the paper. We find that syndications are more durable if the members perform similarly to each other. However, performance gap is more tolerable if members have syndicated many times before. Although best performers are most desirable, we recommend that VCFs invite slightly better performers (especially prior partners) when seeking syndication. A major limitation of our study is that we fail to look into the detailed negotiation of syndication due to the lack of available data. Qualitative methods and duration analysis are suggested for future research.

Introduction

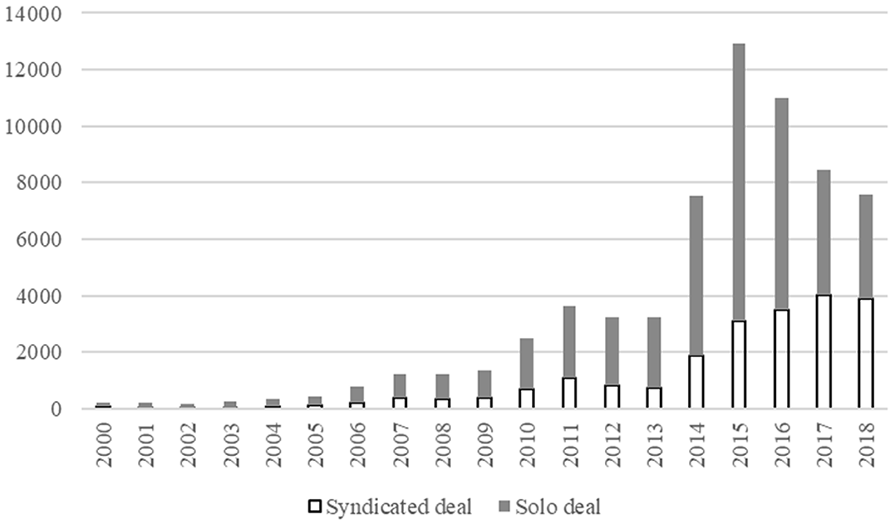

Venture capital (VC) syndication, defined as at least two venture capital firms (VCFs) investing in the same portfolio company (Bygrave, 1987), is a common practice, especially in emerging markets (Aleenajitpong & Leemakdej, 2021). Figure 1 shows the statistics of VC deals (counted as rounds) in China mainland through 2000 to 2018, where the syndicated deals are noticeably growing in terms of number and proportion.

Number of VC deals in China (2000–2018).

Compared with solo investment, syndication among VCFs improves their performance directly (i.e., by improving the exit performance of VCFs) (Bubna et al., 2020; Checkley et al., 2014; Hochberg et al., 2007) and indirectly (i.e., by improving the performance of portfolio companies) (Brander et al., 2002; Bubna et al., 2020; S. R. Das et al., 2011; De Clercq & Dimov, 2008; Hochberg et al., 2007). However, we know little about how the performance of VCFs affects their syndicate. Thus, in this paper, we look into the role of VCFs’ past performance in the formulation of syndication.

First, we notice the paradox of “better performer preference” in VC syndication. As suggested in the prior literature, a VCF is always tend to syndicate with someone who performs better than it does. Syndication with “better performers,” serving as “window dressers,” creates a favorable image during subsequent fundraising (Lerner, 1995) and brings about more potential portfolio companies (Lockett & Wright, 2001; Sorenson & Stuart, 2001). However, such motivation of “window dressing” is not always realized. Consider a pair of VCFs waiting for syndication, where Firm A performs better than Firm B. In this case, Firm A would like to syndicate but will be refused, for Firm B requires someone better than Firm A. In a similar manner, given a sequence of VCFs with different performance, no syndication will ever formulate if every single VCF insists on syndicating with only “better performers.” Despite the above deduction of impossibility, syndication prevailing in reality suggests that “better performer preference” is not always paramount but “worse performers” are sometimes accepted. Thus, we wonder to what extent a “worse performer” is accepted by a syndicate.

According to the theories of resource dependence, the “worse performer,” more dependent on the syndication, is disadvantaged and the syndication is thereby vulnerable. Thus, members of syndication will take balancing operation (Pfefer & Salancik, 1978) to adjust their status and to strengthen the syndication. Thus, we wonder if VCFs take “balancing operation” in terms of performance during syndication. In this paper, we examine to what extent performance gap are tolerable in VC syndication.

Syndication is widely featured with homogeneity (Luo & Deng, 2009; McPherson et al., 2001); that is, both individuals and organizations are tend to syndicate with counterparts who are similar to them per se (Mcdonald et al., 2008). Thus, we observe similarity in terms of age, popularity, and strategy in realized syndication among VCFs (Arundale, 2020; Bubna et al., 2020). On the other hand, heterogeneity within syndicate is costly (Asgari et al., 2017; Goerzen & Beamish, 2005; Kavusan & Frankort, 2019; Kobarg et al., 2019; Lane et al., 2001; Nanda & Rhodes-Kropf, 2019) due to the rising managerial cost for communication and coordination (Estrada et al., 2016; Jiang et al., 2010; Martinez-Noya et al., 2013). Despite rich literature focused on various homogeneity in syndication, yet, to the best of our knowledge, few research investigate the homogeneity in terms of performance in VC syndication. Thus, this paper is to bridge the gap by examining how important homogenous performance is in syndication among VCFs.

In this paper, we theorize the agency problem in syndicate partner selection and test the role of performance gap in VC syndication. We find that syndication is more likely to formulate among VCFs with similar performance. In addition, the self-categorization mitigates the negative relationship between performance gap and syndication performance; that is, performance gap is more tolerable in the syndication if members have syndicated before. Furthermore, we have the negative relationship and the moderating effect not only tested with pairwise evidence but also generalized to the whole network of syndication. This paper contributes in two-folds. First, it enriches the literature on syndication formulation among VCFs by testing the significance of homogenous performance in VC syndication. Second, this paper sheds some new light on organizational performance feedback by presenting evidence on how VCFs behave when the relative performance changes within syndication.

The rest of the paper is organized as follows. Section 2 theorizes the strategy of VCFs when syndicating and proposes hypotheses accordingly. Section 3 elaborates on the source of data, definition of variables, and econometric model used for empirical research. Section 4 presents the major results of empirical research. In Section 5, we generalize the findings from pairwise to network level and also make discussions on the findings. Finally, Section 6 concludes the paper.

Hypothesis Development

Syndicate With Similar Performance

VCFs syndicate to mitigate the information asymmetry between VCFs and their portfolio companies (Brinster & Tykvová, 2021; Engel, 2004; Gompers & Lerner, 2001). As suggested in the theories of social network, inter-organization ties, channeling information from external environment (Koka & Prescott, 2008), mitigate the uncertainty faced by the VCFs (Lee, 2007) and improves their decision-making (Burt, 2000; Granovetter, 1985), which plays a greater role in emerging markets where institutional context is less mature (Aleenajitpong & Leemakdej, 2021). To be specific, the syndicate pools up effort in due diligence to diverse the potential portfolio (Cumming, 2006; Hege et al., 2009, p. 16; Markowitz, 1952; Wilson, 1968) and to optimize the screening and selection of portfolio (Cumming, 2006; Leleux, 2007; Lerner, 1995; Schwienbacher, 2008). Further, coordination of resources in the syndicate (e.g., complementary expertise of each VCF) generates better value-add services and thereby improves the performance of portfolio companies (Brander et al., 2002; Gorman & Sahlman, 1989; Hege et al., 2009; Hochberg et al., 2007, p. 16; Leleux, 2007; Macmillan et al., 1989; Schwienbacher, 2008; Timmons & Bygrave, 1986).

However, the asymmetric information is transferred rather than eliminated. Actually, asymmetric information between VCFs and portfolio companies is internalized among syndicate members and results in agency costs for monitoring and coordination. First, with divided ownership and lack of incentive, free riders emerge in syndication (Cumming, 2006; T. K. Das & Teng, 1999, 2001; De Clercq & Dimov, 2008; Fonti et al., 2017; Meuleman et al., 2009). Hence, monitoring cost is inevitable in the syndication. Moreover, owing to the difficulty in observing ex-ante quality (Owen & Yawson, 2013) and ex-post actions (Dyer & Chu, 2003; Gulati & Singh, 1998) of the counterparty, screening and monitoring prohibitively increase the agency cost in syndication. In such “prisoner dilemma,” syndicate is more likely to take place when participants are with balanced capability (Pruitt & Kimmel, 1977). Given that past performance serves as signal of capability, we propose that

Hypothesis 1: Two VCFs are more likely to syndicate if the gap between their performances is smaller.

Self-Categorisation as Moderator

Prior syndication links might serve as signal in categorization; that is, VCFs cognitively categorize the self in a group whose members have syndicated with each other before. As suggested in the theory of self-categorization (Turner et al., 1987), categorization are perceived to reflect social reality if inter-group differences are maximized and intra-group differences are minimized (Hornsey, 2008). Prior syndication is likely take place among VCFs sharing a variety of attributes like age (Bubna et al., 2020), experience(Lerner, 1994), home market (Qiu et al., 2021), strategy (Arundale, 2020; Bubna et al., 2020), etc. Thus, with categorization based on performance, the differences of these attributes are minimized in-group and maximized intra-group.

VCFs perceive members of their own group in a positive manner. First, the desire for a positive and secure self-concept increases the favor for one’s own group (Tajfel & Turner, 1979). Second, the process of self-categorization (i.e., to categorize oneself as member of a certain group) generates a feeling of attachment and depersonalizes self-conception to conform the group identity (Choi & Hogg, 2020). Thus, the group identity is internal to each member (Spears, 2021). Although the group identity is rooted in the similarity shared among the members, yet it is the categorization more than the similarity per se that exerts a greater influence on cognition and behavior (Spears, 2021).

To sum up, self-categorization leads to overextension of positive properties to in-group members and of negative properties to out-group members (Dunham, 2018; Patterson & Bigler, 2006). Therefore, we propose that

Hypothesis 2: The syndication experience mitigate the negative effect of performance gap on syndication; that is, the gap of performance is more likely to be tolerated in the syndication if the VCFs have rich experience of syndication with each other.

Method

Sample and Data

We extract detailed description of VC deals from the database CVSource (http://www.cvsource.com.cn) and Zero2IPO (https://www.pedata.cn/data/index.html). To be specific, we rely on CVSource as our main source and assign data used in this paper in line with the framework of CVSource. For the missing data in CVSource, we attempt to search in Zero2IPO if possible. Our sample period spans from 1 January 2000 to 31 December 2020.

When two or more VCFs invest in the same portfolio company during the same round, these VCFs are identified as “syndicate.” Notably, CVSource provides data on deal level; that is, a syndication involving several VCFs is reported as ONE deal in CVSource, with no evidence showing who is leading. In this paper, we restructure the dataset as pairwise; that is, every observation includes one focal VCF vis-à-vis ONE syndicate-partner while details of other firms in the syndicate are incorporated in “syndication data.” For example, three VCFs (Firm A, B, and C) syndicate during a certain round. This deal is divided into six equal pairwise observations: Observation 1 including focal Firm A and Syndicate-Partner B with Syndication A + B + C; Observation 2 including focal Firm A and Syndicate-Partner C with Syndication A + B + C; Observation 3 including focal Firm B and Syndicate-Partner C with Syndication A + B + C; Observation 4 including focal Firm B and Syndicate-Partner A with Syndication A + B + C; Observation 5 including focal Firm C and Syndicate-Partner A with Syndication A + B + C; and Observation 6 including focal Firm C and Syndicate-Partner B with Syndication A + B + C.

Variables

Dependent Variable

Pairwise syndication propensity describes to what extent the focal VCF would maintain the dyadic syndicate through the next 3 years. To proxy for this variable, we use the ratio of dyadic syndicated investments (counted in rounds) over the total investments (counted in rounds) of the focal VCF. Specifically, the syndication propensity of focal VCF i with respect to VCF j for Year t is measured as in Equation 1

where

Independent Variable

As the core independent variable, pairwise performance gap describes to which extent the performance of the two VCFs in the pair differs from each other. An initial public offering (IPO) or merge and acquisition (M&A) is commonly described as a “successful” exit for a VCF (Cheng & Tang, 2019; Dai & Nahata, 2016; Hochberg et al., 2007; Nahata et al., 2014). Accordingly, we employ the rate of “successful” exit to measure the performance of VCF. Notably, after investing in a portfolio company, a typical VCF waits for years until the exit; that is, it is possible, at least for some case, that no exit is seen within the 3-year period. Thus, we measure the performance over the entire life cycle of VCF (i.e., from founding till Year t, with Year t excluded). To be specific, the pairwise performance gap between VCF i and j is measured as in Equation 2

where

Moderator

As the moderator variable, the number of prior pairwise syndication describes to which extent that the pair of VCFs have syndicated with each other in the previous 3 years. This variable (NumSyn) counts the number of rounds where both VCF i and VCF j invested through Year

Control Variables

Experience

Investment experience matters in VCF’s strategy of syndication. It is found that green hands are more likely to syndicate while a veteran with increasing experience is less prone to involve in a syndicate (Wang, 2017). We use the number of investment (count in rounds) in the previous 3 years to describe the VCF’s experience. To be specific, the experience (Exp) is defined as the number of rounds that the VCF invested during Year

Similarity of Strategy

Similar strategy leads to syndicate (Arundale, 2020). Thus, we construct variable to describe to which extent the pair of VCFs invest in a similar pattern in terms of portfolio selection. To be specific, we control the similarity of strategy within every pair of VCFs in three-folds: A) portfolio industry similarity (Industry); B) portfolio stage similarity (Stage); and C) portfolio region similarity (Region). The portfolio industry similarity (Industry) measures to which extent the focal VCF and its syndicate-partner in the pair invest in the same industry during the previous 3 years. The variable is computed as in Equation 3

where

Similarly, when Equation 3 is employed to compute the portfolio stage similarity (Stage),

Also, when Equation 3 is employed to compute the portfolio region similarity (Region),

Econometric Model

The empirical research is conducted in two stages. In the first stage, we test only Hypothesis 1 and Equation 4 shows the econometric model of this stage.

where X represents control variables. The pairwise syndication propensity is applied as proxy of Syndicate. According to Hypothesis 1, we predict that

In the second stage, we introduce the moderator and test both Hypothesis 1 and 2. Equation 5 shows the econometric model of the second stage.

where X represents control variables. The pairwise syndication propensity is applied as proxy of Syndicate and prior pairwise syndication number as proxy of Group. According to the hypotheses above, we predict that

Results

Descriptive Statistics

Table 1 reports the descriptive statistics of major variables. We notice that value for pairwise syndication propensity (SynPair1) equals zero for more than three quarters of observations, indicating the variable is left censored. Thus, in baseline regressions, we use Tobit model with lower limit at zero for the dependent variable.

Descriptive Statistics.

Note. Table 1 reports the descriptive statistics of major variables used in the baseline regressions.

For every pairwise observation, we control the experience of focal VCF (Expi) and that of the partner VCF in the pair (Expj). As described in the section of method, the pairwise observations are constructed as symmetric. Thus, the descriptive statistics for Expi and Expj are exactly the same.

Table 2 reports the correlation between major variables. The coefficients with significance of 1% in the first column suggest strong pairwise correlation between dependent variable (i.e., pairwise syndication propensity, SynPair1) and independent as well as control variables, which justifies the selection of variable for empirical research. Further, we notice the significantly negative correlation between the dependent variable and the independent variable (i.e., pairwise performance gap, GapPair), which partly tests Hypothesis 1, that is,

Correlation.

Note. Table 2 reports the correlation between major variables used in the baseline regressions where ***, **, * denotes the significance on level of 1%, 5%, 10% respectively.

Negative Effect of Performance Gap

Table 3 presents the negative effect of pairwise performance gap on pairwise syndication propensity. The coefficient on pairwise performance gap (GapPair) remains significantly negative in both univariate and multivariate regressions; that is, a pair of VCFs, who have ever syndicated before, are more likely to keep syndicated in the next 3 years if the gap between their performances is smaller. Thus, Hypothesis 1 is tested. In addition, the coefficient on the number of prior pairwise syndication (NumSyn) stays significant and positive; that is, the more rounds a pair of VCFs have syndicated before, the more likely they continue syndication in the future. Such positive effect is in line with theories on the embeddedness of syndication (Castellucci & Ertug, 2010; Checkley et al., 2014; Lunnan & Haugland, 2008; Meuleman et al., 2009; Zheng & Xia, 2018).

Role of Performance Gap (Full Sample).

Note. Table 3 reports the negative effect of performance gap on syndication propensity, with t statistics in parentheses, where ***, **, * denotes the significance on level of 1%, 5%, 10%, respectively, with t statistics in parentheses. The dependent variable is the pairwise syndication propensity in 3-year window (SynPair1). Column (2) to (4) control the dummy variable of year. All the columns report the result of Tobit regression with zero as the lower limit of dependent variable.

Pairwise syndication propensity is conditional on general syndication propensity; that is, if the focal VCF determines to make solo investment rather than syndication, it will no longer syndicate with any other VCFs. The pairwise syndication propensity at zero is largely due to the corner solution for VCFs starting solo investment. Thus, we extract samples where the focal VCF ever syndicate with any VCF in the 3-year window. Regressions in Table 4 are rerun with this subsample and Table 4 reports the results. In Table 4, coefficients stay significantly negative in Row 1 and significantly positive in Row 2, consistent with results in Table 3.

Role of Performance Gap (Subsample).

Note. Table 4 reports the negative effect of performance gap on syndication propensity where ***, **, * denotes the significance on level of 1%, 5%, 10% respectively, with t statistics in parentheses. The dependent variable is the pairwise syndication propensity in 3-year window (SynPair1). Column (2) to (4) control the dummy variable of year. All the columns report the result of Tobit regression with zero as the lower limit of dependent variable. Only the observations syndicating at least once in 3-year window are included.

Previous Syndicate as Moderator

Table 5 reports the moderating effect of prior pairwise syndication number on the negative relationship between performance gap and syndication propensity. Coefficients stay significantly negative in Row 1 and positive in Row 3, suggesting that the negative effect of pairwise performance gap (GapPair) on the pairwise syndication propensity (SynPair1) is mitigated when the pair of VCFs have syndicated several times before. Thus, Hypothesis 2 is tested; that is,

Moderator (Full Sample + Subsample).

Note. Table 5 reports the moderating effect of pairwise prior syndication number on the relationship between performance gap and syndication propensity where ***, **, * denotes the significance on level of 1%, 5%, 10% respectively, with t statistics in parentheses. The dependent variable is the pairwise syndication propensity in 3-year window (SynPair1) and the moderator is the number of prior pairwise syndication (NumSyn). The dummy variable of year is controlled in every column. All the columns report the result of Tobit regression with zero as the lower limit of dependent variable. Column (1) and (2) use the full sample while Column (3) and (4) include only the observations syndicating at least once in the following 3 years.

The moderator variable is constructed as cumulative; that is, the number of prior pairwise syndication (NumSyn) accumulates year by year. Hence, we wonder how the moderator works on a broader time horizon. First, we construct a long-term proxy for the dependent variable, the pairwise syndication propensity in 5-year window focal VCF i with respect to VCF j for Year t as in Equation 6

where

We employ the pairwise syndication propensity in 5-year window (SynPair2) as dependent variable and rerun the regression in Table 5. The long-term results are reported in Table 6. Compared with Table 5, the coefficients of moderator (GapPair×NumSyn) keep positive with greater significance in Table 6, which indicates that the moderating effect of prior pairwise syndication number works in a longer term.

Moderator in Longer Term (Full Sample + Subsample).

Note. Table 6 reports the long-term moderating effect of pairwise prior syndication number on the relationship between performance gap and syndication propensity where ***, **, * denotes the significance on level of 1%, 5%, 10% respectively, with t statistics in parentheses. The dependent variable is the pairwise syndication propensity in 5-year window (SynPair2) and the moderator is the number of prior pairwise syndication (NumSyn). The dummy variable of year is controlled in every column. All the columns report the result of Tobit regression with zero as the lower limit of dependent variable. Column (1) and (2) use the full sample while Column (3) and (4) include only the observations syndicating at least once in the following 3 years.

Discussion

Generalization: From Pair to Network

Corollary of Network

We wonder if the negative effect of performance gap on the syndication propensity and the moderating effect of previous syndicate still work on a larger scale. Thus, in this section, we test the following corollary of Hypothesis 1 and 2 on the level of syndication network.

Corollary 1: The VCF is more likely to syndicate if it performs at a similar level of the other VCFs in the syndication network.

Corollary 2: The syndication experience mitigate the negative effect of performance gap on syndication; that is, the VCF is more likely to syndicate despite gap of performance if it has richer experience of syndication.

Variables of Network

We construct a set of variable to describe a VCF’s behavior and status against the network of syndication.

As the dependent variable in this section, the general syndication propensity describes to what extent the focal VCF would syndicate with any other VCF through the following 3 years and is measured as in Equation 7

where

As the interdependent variable of this section, the general performance gap describes to which extent the performance of the VCF differs from the others in the syndication network. Given the interaction and familiarity between syndicate members, performance of other members in the same syndicate is more readily perceivable. Thus, to measure the social aspiration of performance, we use the average rate of “successful” exit among focal VCF’s syndicate members and focal VCF per se. To be specific, the performance perception focal VCF i is measured as in Equation 8

where

As the moderator, the closeness centrality describes to which extent the focal VCF have syndicated with other VCFs in the dataset. To be specific, the closeness centrality of focal VCF i is measured as in Equation 9

where

Definition of control variables and descriptive statistics for in this section are presented in the appendix.

Results of Network

Table 7 reports the negative effect of performance gap on syndication propensity as well as the moderating effect of self-categorization on a generalized level. Coefficients on the independent variable (i.e., general performance gap based on average, GapGen1) in Row 1 stay significantly negative, which suggest that the gap between focal VCF’s performance and the average performance of all its prior syndicate partners has a negative effect on the syndication propensity of focal VCF in the 3-year window. However, such negative effect is mitigated by the centrality of focal VCF, for the coefficients in Row 3 remain significantly positive. Therefore, we test Corollary 1 and 2.

Generalization.

Note. Table 7 reports the negative effect of performance gap and syndication propensity and the moderating effect of centrality where ***, **, * denotes the significance on level of 1%, 5%, 10% respectively, with t statistics in parentheses. The dependent variable is general syndication propensity of focal VCF in 3-year window (SynGen) and the moderator is the closeness centrality of focal VCF (Centrality). Column (1) and (3) does not control the dummy variable of year while the other columns do. All the columns report the result of OLS regression.

One concern about the general performance gap is the perception of other VCFs’ performance (i.e., the social aspiration of performance). Thus, we also proxy the social aspiration of performance with the median value and compute the general performance gap as in Equation 10

where

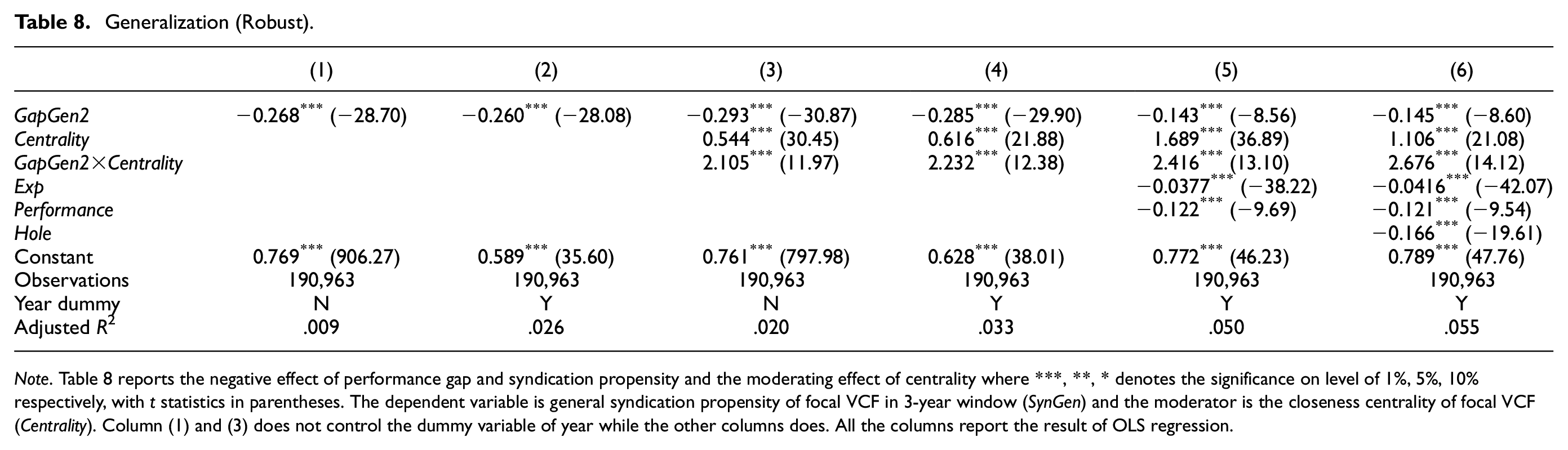

We employ the general performance gap based on median (GapGen2) as dependent variable and rerun the regression in Table 7. The results are reported in Table 8. Coefficients on the independent variable in Row 1 stay significantly negative, suggesting that the gap between focal VCF’s performance and the median performance of all its prior syndicate partners has a negative effect on the syndication propensity of focal VCF in the 3-year window. Notably, compared with Table 8, the coefficients on the dependent variable are greater in Table 7, which indicates that the perception of performance gap is more relied on the mean value than the median of peers. Furthermore, such negative effect is mitigated by the centrality of focal VCF, for the coefficients in Row 3 remain significantly positive. Therefore, we test Hypothesis 1 and 2 on the level of syndicate network.

Generalization (Robust).

Note. Table 8 reports the negative effect of performance gap and syndication propensity and the moderating effect of centrality where ***, **, * denotes the significance on level of 1%, 5%, 10% respectively, with t statistics in parentheses. The dependent variable is general syndication propensity of focal VCF in 3-year window (SynGen) and the moderator is the closeness centrality of focal VCF (Centrality). Column (1) and (3) does not control the dummy variable of year while the other columns does. All the columns report the result of OLS regression.

Perspective of Performance Feedback

The performance relative to aspiration has an impact on the decision-making process of VCFs (Gaba & Bhattacharya, 2012; Hu et al., 2022; Makarevich, 2018). As suggested by the behavioral theory of firms (Cyert & March, 1963b), discrepancy between actual and referent performance (i.e., aspiration) changes the decision makers’ risk tolerance, thereby modifying risk involved in the firm’s strategy to either promote or maintain its prior performance (Greve, 1998; Hu et al., 2011).

Syndication is classically viewed as an approach that buffers the risk of investment (Engel, 2004; Gompers & Lerner, 2001; Schwienbacher, 2008). Conversely, jumping out of the syndication or updating partners in syndicate are risky (Shipilov et al., 2011). Notably, in Equations 8 and 10, performance of the focal VCF is perceived relative to the social aspiration. In the frame of performance feedback, Corollary 1 is translated into a U-shape relationship between the performance relative to aspiration and the risky strategy. On one hand, when the actual performance is below the aspiration, the VCF with worse performance is more likely to stay out of syndicate, taking the strategy of problemistic search 2 (Baum et al., 2005; Mount & Baer, 2022; Ref et al., 2021; Smulowitz et al., 2020). On the other hand, when the actual performance is above the aspiration, the VCF with better performance is more likely to stay out of syndicate, taking the strategy of slack search 3 (Deng et al., 2022; Greve, 2003; Iyer & Miller, 2008; Surdu et al., 2021). In this sense, Corollary 1 echoes the findings of Zhang and Cheng (2023) who suggests a U-shape relation between performance relative to aspiration and the risky strategy in terms of internationalization.

However, given the reasoning of free-rider in the section of hypothesis development, VCFs with performance below aspiration, performing worse than average peers, are expected as less capable and suspected as free-rider. It is plausible that these VCFs are dumped passively from the syndicate more than stay out actively. In this sense, a deeper look is required for “problemistic search.”

Role of Self-Efficacy

In the section of hypothesis development, we focus on the problem of agency and derive the negative effect of performance gap on syndication; that is, the VCF with a relatively worse performance is perceived as free rider and will be thereby rejected from syndication. However, the perception of free rider is more of an external prediction (or even suspicion). In this section, we attempt to justify the internal motivation of free rider in the framework of self-efficacy.

Self-efficacy, defined as “people’s beliefs about their capabilities to produce designated levels of performance that exercise influence over events that affect their lives” (Bandura, 1994, p. 71), has an effect on motivation (Bandura, 1994). To be specific, those with a high level of self-efficacy are more likely to set a higher goal (Bandura, 2012; Baron et al., 2016), to put in greater effort (Beck & Schmidt, 2018), and to persist for a longer time (Çetin & Aşkun, 2018).

According to Bandura (1994), social models and mastery experiences (i.e., past success) are sources of self-efficacy. Thus, relative performance is also a source of self-efficacy for the VCF; that is, when a VCF performs worse than its peer(s), it receives negative feedback and its self-efficacy is lower.

Higher self-efficacy (i.e., higher relative performance) leads to greater effort while lower relative performance leads to less effort. In the syndication, the better performer will contribute more while the worse performer will contribute less. Therefore, the worse performer is free riding.

Limitation and Future Direction

First, the motivation of syndicate needs further identification. Syndication is a “concrete, living unit” (Simmel, 1955, p. 20) filled with conflicts and collaboration. A major concern about syndication is the duality; that is, a syndication takes place when the entire members are willing to syndicate and are accepted by the other members. A typical syndication is proposed by one or several members and accepted by the others after series of negotiation. However, the current dataset includes only fait accompli, the realized syndications. We have little information about who proposes and who accepts, which limits our discussion on the motivation of syndication. Thus, the future research might focus more on the ex-ante analysis of syndication and dive into the negotiation details, using qualitative methods.

Second, the measurement of relative performance needs enrichment. Apart from social aspiration based on peer performance, historical aspiration based on past performance is also widely employed as reference point. In terms of the effect on decision-making process, some empirical evidence shows the performance relative to social aspiration functions differently from that relative to historical aspiration (Ye et al., 2021) while other evidence suggests the similar effect of performance relative to the two aspirations (Wan et al., 2022). Noticeably, prior research on such topic is largely focused on the evidence from individual perception and decision-making process of the managers (Berchicci & Tarakci, 2022; Blettner et al., 2015). Therefore, comparison between performance relative to social and historical aspiration in the sense of organization would be interesting for future research.

Last, the regression method needs improvement. In this paper, the performance of VCFs is measured as the rate of “successful” exit and the rate is computed with historical data throughout the VCF’s lifecycle. Notably, up-datedness determines the value of data and recent data thereby outweigh earlier data in prediction. Thus, it is plausible to focus more on the recent performance by computing the rate with data in the 3-year window. Given the longstanding investment and syndication out-surviving the 3-year window, we suggest duration analysis for the future research.

Conclusion

In this paper, we examine how syndicate formulates among VCFs with different performance. We find that performance gap between syndicate members has a negative effect on the propensity of syndication. To be specific, syndication is more likely to break down when performance gap between members enlarges, as those with worse performance tend to free ride. Furthermore, we find the self-categorization mitigates the above-mentioned negative effect. To be specific, performance gap is more tolerable in syndication if members have syndicated before.

These findings are generalized from pairwise evidence to the whole network of syndication. We find that the VCF is more likely to syndicate if its performance is similar to the average level around the syndication network. Besides, the VCF is more likely to syndicate despite gap of performance if it has rich experience of syndication.

Although the best performer is the most popular partner for syndication, we recommend that VCFs who aspire to syndicate send invitation to those with slightly better performance rather than someone perform too much better. In addition, prior syndication partner is the best choice and the repeated syndication is less vulnerable.

Footnotes

Appendix

Acknowledgements

The authors would like to extend gratitude to Prof. Yi Tan from Shanghai Jiaotong University, Prof. Jo-Ann Suchard from the University of New South Wales, and Dr. Heng Du from Shanghai University of Finance and Economics for their the insightful comments that helped improve this paper.

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: This research was funded by: the NATIONAL NATURAL SCIENCE FOUNDATION OF CHINA, grant number 72172077; the NATIONAL SOCIAL SCIENCE FOUNDATION OF CHINA, grant number 20BJY190; the UNIVERSITIES’ PHILOSOPHY AND SOCIAL SCIENCE RESEARCH PROJECT IN JIANGSU PROVINCE, grant number 2022SJYB1326; the CHANGZHOU SCI&TECH PROGRAM, grant number CJ20235022; the SHANGHAI SOFT SCIENCE PROJECT, grant number 23692111700; and the GRADUATES INNOVATIONAL FOUNDATION OF SHANGHAI UNIVERSITY OF FINANCE AND ECONOMICS, grant number CXJJ-2022-358.

Data Availability Statement

Data sharing not applicable to this article as no datasets were generated or analyzed during the current study.