Abstract

This article examines the evolution of approaches to the content of venture capital based on the evolution of venture capital and venture capital investment, post-industrial society, institutional theory, and experience of forming the venture capital market in developing economies. Hypotheses of the functioning of venture capital in the transforming economy of the UAE and China are proposed and tested. An economical and mathematical model for assessing the efficiency of venture capital functioning has been developed. It was found that there is a particular relationship between the national characteristics of the country’s venture capital industry and the capital invested in innovative industries, as well as the production efficiency of these industries. Moreover, the attractiveness of venture capital investments somehow increases with investments in other sectors in both countries. Since the Chinese market evolved earlier than UAE, it has the most remarkable characteristics, including higher capital workforce ratios and higher exports of science and technology-intensive products. In addition, the Chinese market has a high level of development and focuses on a sustainable financing cycle than UAE.

Keywords

Introduction

One of the global trends in the active development of venture capital in the global economy (Mărginean et al., 2018; Matyushok et al., 2021). So, in China, at the end of the 20th century, a research system was formed to disseminate scientific knowledge following the needs of a growing industry and not at the development of knowledge boundaries (Stefani et al., 2019). Thanks to the expansion of the network of state laboratories and institutions, an increase in the share of state funding, and the strengthening of the state’s regulatory function in the field of science, the evolution of national innovation systems received an impetus for development (Băzăvan, 2019).

The venture capital market was already emerged in Europe by the end of the 1970s. However, it emerged most in China in the mid-1990s for geographic, socio-economic, and other reasons. Moreover, in UAE, it could emerge after the 2000s. Characteristically, the Chinese venture capital system is based on a continuous financing cycle; that is, the venture capital market’s main task is to accumulate investor funds and place them in various innovative projects; for instance, green innovation for fashion brands even with ordinary apparel has been put forward from Chinese markets (Chen et al., 2021). Unlike the UAE, China tends to form its venture capital and direct investment funds for a specific project promoted by the state (Cheng, Hua et al., 2019; Wang & Zhao, 2017).

The main difficulty in studying the formation of the UAE venture capital market is that, despite the increased interest in it, there is still no single theoretical and methodological approach to defining the content of the category of venture capital (Zarrouk et al., 2021). Besides, a methodology for assessing the efficiency of venture capital functioning (particularly in the sectoral context) that is adequate to the conditions prevailing in the Arab economy has not been developed (Bakhouche, 2021; Elbanna et al., 2020). There are also no comprehensive models of effective venture capital in developed, developing, and transforming economies.

These problems require an early solution since they are important for determining the most effective prospects for developing the Arab economy. Venture capital can become a driver of innovative growth and modernization of the transforming economy of the UAE (Tipu & Sarker, 2020) since mathematical modeling has remained the best choice for the analysis of the functioning of various aspects of management (Wang et al., 2019). Thus, this study was done to answer the following questions.

What is the association of the effectiveness of venture capital investment with the national model of introducing venture capital to raise capital invested in innovative industries?

What is the relationship between the volume of venture investments in the industry and the volume of innovative products, and the efficiency of these industries’ production processes?

Are venture investments proportional to the national economy’s output and characterize the level of scientific and technological progress? In other words, if there are proportional to the total output of goods and services.

Should the attractiveness of venture capital investments in one sector of the economy increase with other sectors’ investments?

Thus, studying venture capital’s content, forms, and characteristics is a fundamental scientific problem that requires deep study. Venture capital is closely related to the formation and development of a new economy; determining compelling scenarios and developing models for the efficiency of venture capital functioning seems to be especially interesting in the innovative development path’s current conditions. We believe that this manuscript shall be beneficial for understanding the effect of venture capital investment and their volumes in innovation entrepreneurship at national levels and the effect and consequence of improving all sectors by initiating one sector.

Theoretical Foundations

Venture capital was introduced long ago (Schram, 1949); there are various interpretations of the concept of venture capital and venture capital in the economic literature. This is since economic theory recognizes a practical economy’s functioning based on allocating an economic dominant. Also, there are several well-known evolutionary theories of venture capital (Anwar, 1997; Black & Gilson, 1999; Gompers & Lerner, 2004; Lerner, 1995; Sohl, 1999). Despite the significant theoretical interest in venture capital and venture capital investment, these concepts are not well developed. Discussion issues are the content of concepts and features of venture capital and methods for assessing and building models of the effectiveness of venture capital, particularly in the sectoral context.

As a result of the professional and thematic literature analysis on venture capital financing, many definitions of this economic category were identified. The variety of interpretations varies depending on the emphases set by the authors in the definition: the basis may be the main function of capital, the area of its application or concentration, and its main characteristic (Azarmi, 2002). However, a theoretical and methodological analysis of approaches to venture capital study has revealed two main directions for developing this category: American and European.

Differences in the historical development of foreign venture capital funds and associations have influenced the divergence of interpretations of the content of the venture capital category (Bonini & Capizzi, 2019). In the United States, venture capital refers to investments in high-tech companies that are in the early stages of development (the stages of “seeding” and “startup”).

Scientists considered the process of venture financing as financing the equity capital of small innovative companies with high growth potential, combined with consulting support and a significant degree of involvement in the decision-making process (The Economist, 1997). Obviously, along with financial resources, economists emphasized the practical component’s importance—human capital. The European interpretation is broader than the American one. It includes financing companies at various stages of the project life cycle, including later ones (Guilhon, 2020). European Private Equity and Venture Capital Association characterizes venture capital as equity capital provided by professional firms that invest in private enterprises that demonstrate significant growth potential in their early stages of development, expansion, and transformation while simultaneously managing these enterprises. Investments of this kind are called direct investments (Tykvová, 2018).

Though the venture capital might be strongly related to the condition of investment culture and overall geopolitical situation of a country, as it has been reported for the case study of India (Aktaruzzaman & Farooq, 2020); with some significance at even individuals or family level (Nguyen et al., 2021), yet the internationalization and monetary liberalization have made financial markets more interrelated (Aybar et al., 2020). Thus, in modern UAE practice, the concept of venture capital is characterized by its ambiguity and inaccurate interpretation: venture capital funds invest not only in enterprises in the early stages of development but also in enterprises at the stage of business expansion and restructuring. The authors believe that the main reason for various definitions in the UAE is that venture capital, an alternative source of business financing, originated in the UAE relatively late than in Western markets in the early 2000s. So, Avnimelech and Teubal (2004), in their definition, emphasize the special riskiness of venture projects and the possibility of quickly obtaining a high rate of return. At the same time, Avnimelech and Teubal (2008) treat venture capital as long-term, risk capital invested in the shares of new fast-growing companies to generate high returns, the shares of these companies are listed on the stock exchange.

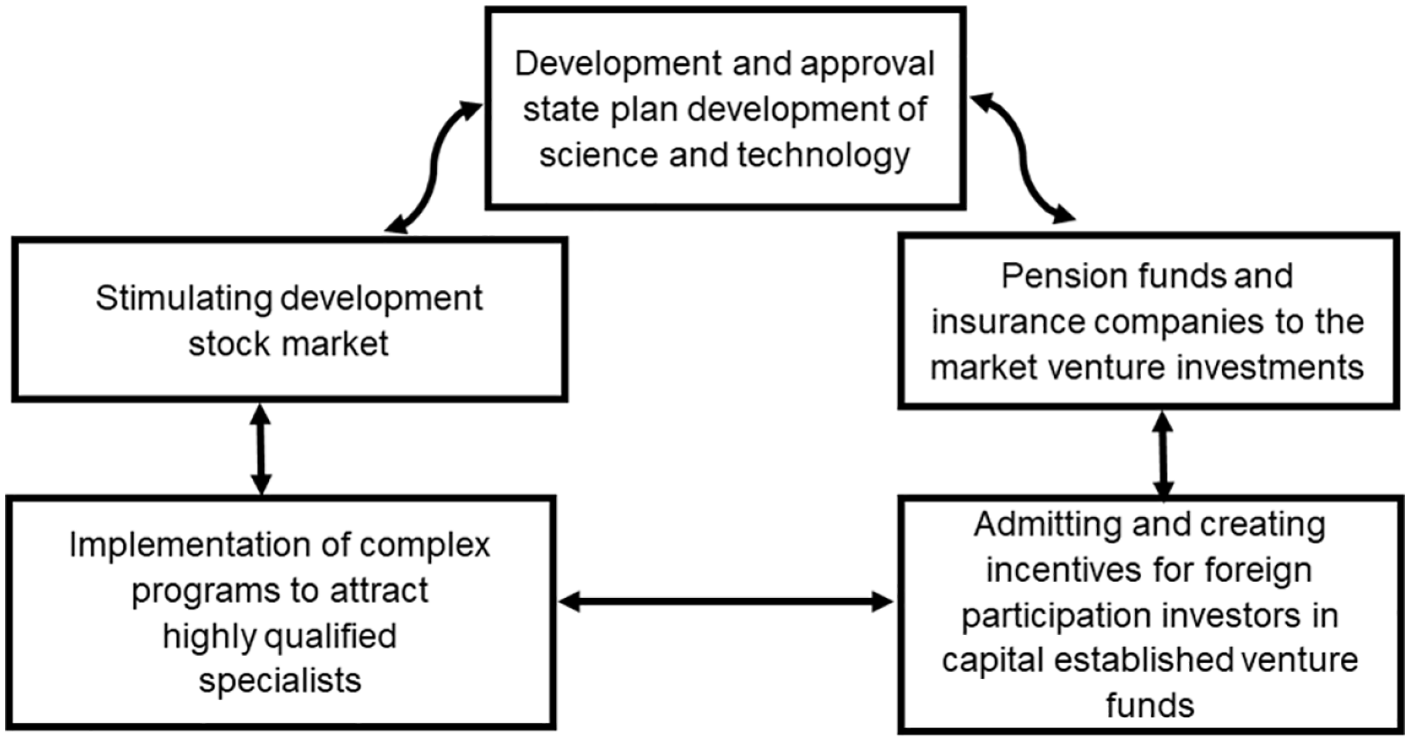

Khan et al. (2020) provided enlightenment for companies and decision-makers on how different types of uncertainty in the enterprise environment affect capital structure decision-making. The most striking examples of the justification of efforts to develop the venture capital market include the UAE and China’s experience (Fu & Ng, 2021; Zarrouk et al., 2021). Both the UAE and China created a developed system of venture capital investment in just over 10 years. In 2000, the total volume of transactions in the Chinese venture capital market did not exceed $2 billion, and already in 2019, this figure was $57 billion (Yang & Lee, 2018). Such results would not have been possible without a systematic and consistent government policy that includes five main elements, as shown in Figure 1.

The main elements of China’s state policy on the development of the venture capital market.

Over the past 10 years, the Chinese government has done significant work to develop the venture capital market, which is already bearing fruit. Thus, the share of the total volume of transactions in the venture capital market concerning the country’s GDP in recent years has increased from 0.9% to 0.37%, and the total number of transactions performed annually has increased more than six times—45 transactions in 2005, 1,270 transactions in 2018 (Yang & Lee, 2018).

The main features of venture capital and venture capital investments are the following:

(1) High profitability of venture companies, associated with a high degree of risk.

(2) Investments are made by a specially organized professional team consisting of an entrepreneur, investors, a management team, mainly in new, not listed companies, focusing on non-linear growth of profitability.

(3) Attraction of investments is carried out in the company’s authorized capital by issuing shares, converting debt, or direct investment in equity capital (private equity).

(4) The investment strategy is medium and long term.

(5) The venture investor’s goal is to obtain financial profit because of the resale of the fund’s assets to a strategic or portfolio investor or the issue of company shares at a public auction.

(6) Promoting technological progress and enhancing innovation activity.

(7) Reduction of the cycle “scientific development–production–market.”

(8) A guarantee of economic sustainability of small and medium-sized businesses focused on innovative developments.

(9) Financial support of scientific and technical, scientific and production and innovation activities.

Thus, it is possible to understand venture capital as a source of investment and a form of investment in private companies to ensure innovative activities to obtain a profit rate above the market average, associated with a high degree of riskiness (Viviani et al., 2021). An essential feature of venture capital investment is the direct relationship between the level of risk and the rate of return or profit, as shown in Figure 2a.

Understanding venture capital profitability, risk, and investment: (a) the relationship between profitability and risk and (b) dependence on the profitability of venture investments on time.

Besides, venture capital is characterized by a particular relationship between profitability and the stage of implementing an investment project, illustrated in Figure 2b. In addition to the main features of venture capital, it is necessary to consider the studied definition’s functions.

The first functional feature is associated with the accumulation and mobilization of temporarily free funds of institutional, state investors, and local and foreign investors’ savings. This function is implemented through professional participants in the venture market—venture capitalists, united in management companies of specialized funds, in which the accumulation and redistribution of funds occur. In this regard, it is possible to single out the second functional feature of venture capital—the redistribution of investments between the venture capital market participants. In addition to investing money in innovative enterprises, venture investors provide them with financial, marketing, and other nature consulting services. Hence, venture capital’s third functional feature is transferring management experience to newly created or already operating innovative companies. The fourth functional feature is the stimulation of innovation, as recently appropriate materials have been chosen by testing simulation for properties for leather selection of garments (Memon et al., 2021).

It should be noted that this function is implemented through scientific and technical developments, the development of science, and the educational process. Thus, the fifth function can be called interaction between science and business or integrating scientific and technical developments into business projects. Shortening the cycle “scientific development–production–market” forms the sixth transformation function, which in this context is considered as a tool for creating new science-intensive or innovative industries that produce the latest types of goods (Tyulin & Chursin, 2020).

All the listed functional features can be combined into one—synergistic. From the point of view of a systems approach (Mikhailov & Loskutov, 2012), venture capital combines economic functions, that is, accumulation and redistribution of financial capital, stimulating the production process; social functions, that is, transferring experience, stimulating the development of scientific research. In general, venture capital can be viewed as a single developing system that contributes to scientific and technological progress and increases the population’s well-being. Venture capital can be understood as financial capital invested by a professional investor in a high-tech or traditional sector of the economy at the startup stage or expansion to obtain super-profits and associated with high risk (Díaz-Santamaría & Bulchand-Gidumal, 2021). Venture investment is the process of introducing a mass of venture capital in the national economy to obtain venture capital gains and give impetus to innovative economic growth (Kang, 2020). Funding can take various forms of financial transactions, in the form of purchases of common stock, convertible preferred stock, convertible debt, and assistance in transferring knowledge and economic characteristics to a specialized investor. In return for taking on relatively high risk, venture capitalists receive higher rates of return in the form of preferred shares, equity appreciation, and otherwise.

Hypothesis and Model Establishment

Hypothesis A is based on the assumption that there is a relationship between a country’s venture capital industry’s national characteristics and a compelling investment model. Such dependence is explained by the existence of historical, cultural, economic, and political characteristics inherent in a particular region, which affect the formation of a unique economic environment and its characteristics.

The criteria for testing this hypothesis were such indicators as the presence and perfection of the legal framework governing the venture capital industry; the number and composition of participants participating in the venture capital market, and the system of their interaction; organizational and legal forms assigned to venture capital firms; as well as indicators such as market transparency, the influence of government agencies and the historical characteristics of the development of venture capital activities in countries. However, the main criterion for assessing the effectiveness of the national venture investment system’s functioning is the capital-labor ratio in the industries involved in venture capital investment and the volume of high-tech products produced.

This hypothesis was confirmed by an economic and mathematical model of the venture capital market for the UAE and China. Based on this model, it can be judged that the Chinese market, which appeared at an earlier stage, is characterized by the most remarkable development compared to the UAE, namely, a significantly larger volume of production of science-intensive products and a higher investment rate.

Hypothesis B was tested based on one of the assumptions of Keynesian theory (Keynes, 2018) on the existence of a linear relationship between the volume of investment and total output. This assumption was adapted to the studied object: a linear relationship is assumed between the volume of venture capital investments in all sectors of the national economy, using venture capital in their activities, and the output of these sectors.

where:

Vv.i.—the volume of the venture and direct investments.

fm—free member;

ri—investment rate;

Vi.p.—the volume of innovative products produced by industries using venture capital investment in monetary units.

This model with known values of the parameters of venture capital investments (Vv.i.) and the volume of innovative products produced by these industries (Vi.p.) allows finding the value of the unknown coefficient (ri), characterizing the rate of investment. Finding this parameter will make it possible to estimate the share of the total volume of innovative products in the country that enterprises invest in new enterprises in the scientific and technical sphere or expand existing enterprises using venture capital investment.

While testing this hypothesis for the UAE and China, the following results were obtained.

For the UAE, the regression equation is:

{2.47} {3.08}

For China:

{2.47} {2.54}

Based on the calculations carried out, one can judge the differences between the UAE and the Chinese venture capital markets: for example, in the UAE, the share of investment is 10% of the production of scientific and technical products, while in China, 30% of the income is directed for investment purposes. In general, we can say that the hypothesis put forward has been confirmed.

In this hypothesis, we need to understand the consequence of venture investment at the national level; for instance, if the GDP rises, the effects might be positive or negative overall.

Hypotheses C and D were tested based on the investment accelerator, adapted for the venture capital market (Hunt & Lautzenheiser, 2015).

where:

Tv.t—cumulative venture capital investment at a point in time t,

fm—free member;

εt—moment in time error t;

VtGDP—GDP volume at time t;

δ—unknown coefficient characterizing the volume of GDP.

In addition to GDP, the model includes the lagged value of venture capital investments. This modification is because investments often occur in several stages; respectively, the volume of financial investments made in the period (t−1) will affect the investment activity in period t.

This model was reduced to a linear form to assess the impact of GDP and the lagged value of venture capital investments.

Based on formula (4), regression equations for the UAE and China are constructed. The construction of this model for the UAE was carried out based on annual data from 2015 to 2018. about GDP and venture investments. In 2018, the number of venture capital deals raised by startups in the UAE to 366 deals. The total value of venture capital raised in the UAE for this period was about $893 million (Statista, 2020a). The time series were considered in 2015 prices; for China, the time series was taken from 2009 to 2019. In 2019, new venture investments to about 157.78 billion yuan (Statista, 2020b). Models that did not include the lagged investment value turned out to be of better quality, so they were considered further.

The following equation characterizes the UAE venture capital market:

{5.11} {5.87}

The resulting model shows that with a 1% growth in GDP, the volume of venture capital investments in all sectors of the economy will grow by an average of 5.62%.

A similar model was built for the Chinese economy:

{0.67} {3.12}

The constructed model confirms the hypothesis about the dependence of venture capital investments on total output: with GDP growth of 1%, total venture capital investments in China will increase by 0.92%. Based on the constructed regression equations, we can conclude that the hypothesis of proportionality of venture investments to GDP volume is confirmed for both states.

To test hypothesis D about an increase in the attractiveness of venture capital investments in one industry with an increase in financial investments in other sectors of the economy, one can use the formula:

Where:

α—unknown coefficient characterizing the lagged value of investments in the i-th industry at time t;

β—unknown coefficient characterizing the total venture capital investments in all industries except the i-th industry at time t.

To assess each factor’s influence on the volume of venture investments in industry i, model (7) was brought to a linear form. Coefficient

The regression was built for China, and the results are presented in Table 1. The statistics of venture investments by sectors of the economy were considered as data for modeling. The regression equation included annual data adjusted for the 2020 Consumer Price Index.

Testing the Hypothesis About the Growth in the Attractiveness of Investments in One Industry Increases Total Investments for the Chinese Economy.

Based on the data presented in Table 1, we can conclude that the hypothesis about the impact of the total investment on the growth of financial investments in a particular industry is confirmed for the Chinese economy. The following sectors of the economy will most actively respond to investment growth: Consumer goods and fast-moving consumer goods; finance, insurance, real estate; and technology and telecommunications. With an increase in total financial investments by 1%, the flow of investments in these industries will increase by 1.32%, 1.18%, and 1.17%, respectively.

It should be noted that an increase in venture capital investments in the previous period will entail an increase in financial investments in all studied sectors of the economy by an average of 0.22%, except for the Transportation and logistics industry, which shows a negative result. At the same time, it is fair to say that, on average, an increase in venture capital investments in all industries except the investigated one by 1% will increase investments in this industry by approximately 0.72%.

A similar model was built for all sectors of the UAE economy involved in venture capital investment. However, the hypothesis was confirmed only for technology and telecommunications. With a probability of 97.29%, it can be argued that an increase in investments in technology and telecommunications by 1% in the previous period will lead to an increase in subsequent financial investments by 0.47%. At the same time, an increase in all industries’ investments by 1% will lead to an increase in funding for technology and telecommunications by 0.67%. Based on the results of the testing hypotheses, we will draw the following conclusions.

First, both states confirmed the hypothesis, suggesting mutual influence and interrelation between the volume of venture capital investments in the industry and the volume of innovative products produced and the production process’s efficiency in these industries. As a result of checking this assumption, the value of the venture capital market industries’ investment rate was obtained. For the UAE, the investment rate is 0.1 of innovative products’ output; for China—0.3.

Secondly, for the UAE, the hypothesis about the dependence of venture investments on the country’s economic development and their proportionality to the total output of goods and services was confirmed. However, testing this hypothesis for China gave a negative result. The following relationship was revealed during the verification of the above assumption: with the growth of the UAE’s GDP by 1%, total venture capital investments will increase by 4.93%, for China—by 0.85%.

Third, the assumption of a direct positive relationship between the attractiveness of venture capital investments in one sector of the economy and the growth of investment in other sectors gave a negative result for all sectors of the UAE economy except technology and telecommunications. At the same time, this hypothesis was fully confirmed for China.

Results and Discussion

The model is presented in the form of an economic and mathematical model that reveals the mechanism of interaction between the volume of output of innovative products, the number of the labor force in the country, capital-labor ratio, the amount of venture investments, and the level of development of scientific and technological progress. The model is based on optimizing and simplifying relations between the entities participating in the venture investment processes. The main task in building the model was to analyze the efficiency of the venture capital market functioning based on the capital-labor ratio, the investment rate, and the output of innovative products.

In order to obtain a comprehensive assessment of the efficiency of the venture capital market, it is necessary to build a model that describes the impact of the venture capital market on the economic state of the national systems under study.

Because one of the main functions of venture capital is to stimulate economic development by improving output, increasing production capacity, increasing welfare, and, as a result, increasing indicators characterizing the economy’s total output. The model was chosen as a basis for modeling the venture capital market economic growth by Solow (1970), considering scientific and technological progress adapted to the study of the venture capital market:

Where:

Note that as an indicator

Utilizing mathematical transformations, system (8) can be reduced to a representation in specific indicators, that is, to the following form:

Where:

We also note that in the theory of systems, the law of S-shaped development of the system (Berdonosov & Redkolis, 2015) involves the development of systems through the transition from one qualitative state to another, as can be seen in Figure 3. Thus, it is planned to determine the system’s point of transition from one state to another in further studies.

S-shaped curve of development.

As the production function, the Cobb-Douglas function was chosen, which meets all the characteristics of the neoclassical:

Where

Based on statistical data, production functions for the UAE and China were obtained, and the parameters required for modeling were calculated and are presented in Table 2.

Model Data by Country Compiled by the Author.

The production function characterizes the technological process inherent in enterprises producing innovative products. Note that for the UAE, the labor factor is more significant in the technical process: with its growth by 1%, the output will increase by 0.64%, while with an increase in capital by 1%, the objective function will increase 0.36%. At the same time, for China, the most significant factor is capital.

Further, the obtained constants and functions were substituted into the system (11), making it possible to determine the optimal capital-labor ratio and output values. The values of these indicators corresponding to Phelps’s Golden Rule of Accumulation (Phelps, 1965):

where:

Consider the results obtained, presented in Table 3.

Results of Building a Model for the UAE and China, Compiled by the Author.

It should be noted that the actual value of the capital of the industries involved in venture capital investment in the UAE in 2018 was $1.12 billion, the output was $0.87 billion. It should be noted that based on the model, it is possible to calculate the value characterizing the underproduction of products in the sectors using venture investments, which is $0.68 billion (differs from the optimal one by 37.1%). Underproduction is caused by the equipment of fixed assets below the optimum: the difference between the real and the optimal value is $1.63 billion (59.7%), while the value of the investment rate in 2018 and the modeled value are almost identical, in the first case it is 0, 11, in the second—0.12.

Based on the obtained production function, the labor force parameter mainly affects innovative products’ production and their growth in the UAE, but the constructed model shows a low capital-labor ratio. Hence, we can conclude that in the venture capital market in the UAE, there are projects focused on large technological production that require enormous financial costs, while investors are ready to invest in smaller amounts. If economic agents in the UAE begin to act based on maximizing consumption, then the consumption rate will be 0.88; that is, 88% of all income will be directed to consumption. At the same time, there will be an increase in production to $1.57 billion, which will necessitate an increase in the capital-labor ratio to the level of $3.13 billion. A similar model has been built for China.

It should be noted that the actual value of the output of high technology products in China in 2018 was $93.6 billion, while the optimal value obtained while constructing an economic and mathematical model is $237.8 billion, insufficient equipment of funds: the real value is less than the model value by $662.3 billion (70%). If economic agents act based on maximizing consumption, then the investment rate will be 0.81; that is, 81% of all income will be directed to investment. A reduction in consumption to 19% will lead to an increase in the capital-labor ratio and an increase in the output of high-tech products, which will amount to $125,887.71 and $12,022.32 billion, respectively.

Conclusions

Thus, the constructed models make it possible to determine the optimal development of various national economies in a venture market structure. This model is a universal tool that determines the optimal output of high technology products in a particular economic environment. In addition, these models made it possible to confirm hypothesis A about the existence of a relationship between the national characteristics of the venture capital industry of a certain country and a compelling investment model. The constructed models mathematically confirmed that the Chinese market, which began its development at an earlier stage, is characterized by the most remarkable development, namely, a higher level of capital-labor ratio, a large volume of production of science-intensive products, as well as a higher investment rate—0.3 compared to the UAE, equal to 0.1. The figures obtained indicate a higher level of development of the Chinese market and its focus on a continuous financing cycle.

Research Limitations and Suggestions

The policymakers at the national level should consider this that although it is also important to invest in other sectors as well to attract venture capital more, yet it is directly related to capital workforce ratios as well as higher innovative products; moreover, they also need to focus on a sustainable financing cycle to maximize the efficiency of venture capitals. It should be noted that the constructed models did not include external interference and excluded the state’s role. In the future, the constructed models can be improved: as exogenous variables, in addition to parameters characterizing the growth of labor efficiency due to scientific and technical progress, investment and depreciation rates, and the rate of population growth, the model can include variables responsible for individual characteristics. These features may include the rate of riskiness inherent in the venture capital market, the degree of government intervention in the investment process, the legal framework’s effectiveness obtained by expert assessments, or other methods. An effective venture capital model built in this way will characterize more fully and allow the inclusion of new endogenous variables in the model, which will also characterize the venture capital market. Moreover, a nonparametric approach to data envelopment, that is, data envelopment analysis, and a parametric approach to estimation by stochastic boundaries, that is, stochastic frontier analysis, might also be carried and compared with the current model.

Footnotes

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.

Data Availability Statement

Data can be provided by emailing the corresponding author of this manuscript.