Abstract

Amidst the framework of dual circulation, innovation emerges as a pivotal strategy for realizing high-quality economic development. Concurrently, digital finance, serving as a potent complement to traditional financial systems, significantly influences regional innovation enhancement. This research employs a spatial panel methodology to thoroughly investigate the inherent mechanisms through which digital finance development shapes regional innovation. Empirical testing is conducted using panel data derived from 283 mainland Chinese prefecture-level cities spanning from 2013 to 2020. The findings underscore that digital inclusive finance plays a crucial role in amplifying regional innovation output, unveiling a distinct spatial impact on innovation. The progression of each facet of digital finance contributes to mitigating supply-side financing constraints, thereby directly fostering heightened regional innovation. The study delves into a Chinese regional sub-sample, revealing a prevalent driving effect with conspicuous heterogeneity across the major regions—East > Central > West. As scientific and technological innovation stands as the primary driving force, its profound interplay with the evolution of financial inclusion in China is evident. This study provides valuable insights to fortify regional modernization efforts and serves as a reference for policymakers and researchers navigating the complex intersection of finance and innovation in the Chinese context.

Plain Language Summary

Amidst the framework of dual circulation, innovation emerges as a pivotal strategy for realizing high-quality economic development. Concurrently, digital finance, serving as a potent complement to traditional financial systems, significantly influences regional innovation enhancement. This research employs a spatial panel methodology to thoroughly investigate the inherent mechanisms through which digital finance development shapes regional innovation. Empirical testing is conducted using panel data derived from 283 mainland Chinese prefecture-level cities spanning from 2013 to 2020.

Introduction

The Fifth Plenary Session of the 19th CPC Central Committee (held from October 26 to 29, 2020) pointed out that during the current important strategic opportunity period, when faced with the complicated international situation, the difficult and serious task of domestic reform, development, and stability, especially the severe impact of the COVID-19 pandemic, “forging ahead, pioneering and innovating” is still the main way for us to overcome risks and challenges. Moreover, on May 14, 2020, a meeting of the Standing Committee of the Political Bureau of the CPC Central Committee proposed for the first time to “build a new development pattern with dual domestic and international circulation to promote each other.” In short, dual (domestic and international) circulation’ refers to expanding China’s domestic demand, focusing on its domestic market, improving its innovation capacity, avoiding over-reliance on international markets, and maintaining its openness to the outside world. China will continue to strengthen and highlight domestic circulation’s main position. It will also rely on domestic circulation to achieve its mutual influence as well as promote each type of circulation to promote its high-quality economic development. Furthermore, efforts to improve the capacity of scientific and technological innovation are the core elements of high-quality economic development along with the construction of a new development pattern in which domestic and international circulation promote each other. Objectively speaking, at present, China’s scientific and technological innovation has steadily improved in terms of its vitality and strength. In addition, technological innovation’s contributions to China’s economic and social development have become increasingly apparent. However, China’s capacity for independent innovation still needs extensive improvements, which prevents it from becoming a powerful way for China to achieve high-quality development (Y. Z. Wang et al., 2019).

Studies have theoretically verified that financial development may play an unparalleled role in supporting technological innovation by alleviating information asymmetry on both sides of funds supply, reducing transaction costs, strengthening spillover effects, and easing financing constraints (Ji, 2018). However, practically, the traditional development model’s constraints as well as the old economic system’s limitations have caused the development of China’s financial market to remain underdeveloped. In addition, problems resulting from imbalance and underdevelopment such as inadequate transmission mechanisms, inefficient resource allocation, and long-term structural contradictions have affected the ability of micro-entities to finance their entrepreneurial ventures and curbed improvements in regional technological innovation (Hu et al., 2020). Digital finance as a new financial service model characterized by high efficiency and wide coverage presents potential opportunities to solve the problem of enterprise technological innovation’s financing constraints. Digital finance is an important part of building a digital China based on the 19th Party Congress’ proposal, and is also an essential part of building a modern financial system. Digital finance combines mobile Internet, cloud computing, and big data with traditional financial services to provide China with new finance options and new phenomena, as it has the advantages of high efficiency, comprehensive services, a wider customer reach, and more extensive geographical penetration. According to Peking University (PKU)’s Digital Inclusive Finance Index Report, China’s digital inclusive finance services have rapidly developed during 2011 to 2018, with the median value of the digital inclusive finance index in each of its provinces growing from 33.6 in 2011 to 214.6 in 2015 and expanding to 294.3 in 2018, an 8.9-fold increase in the index throughout 8 years, with an average annual growth of 36.4%. Therefore, can digital finance’s rapid development accelerate regional technological innovation?

On one hand, digital finance’s development may address traditional finance’s shortcomings, help to alleviate the problem of enterprises’ financing difficulties, provide financial support for innovation, and increase innovative R&D investment, thus enhancing regional technological innovation (R. Huang et al., 2021). As it relies on digital technologies such as cloud computing, big data, and blockchain, digital finance can effectively reduce information asymmetry between funding supply and demand, as well as effectively reduce transaction costs and improve the efficiency of capital use by screening valuable projects beforehand and dynamically supervising them afterwards (Bai, 2021). At the same time, digital finance simplifies the lending and borrowing approval process, expands the scope and target of financial services, and provides important support for enterprises’ technological innovation. On the other hand, digital finance’s development also helps to effectively guide the flow of social capital, reshape the direction of industrial development, promote the optimization and upgrading of industrial infrastructure (Tian et al., 2021), and create favorable conditions for the transfer and optimal allocation of opportunities for technological innovation, thus strengthening the spillover effect of technological innovation and enhancing technological innovation in a regional context. Therefore, digital finance’s development may help to enhance regional technological innovation, while it may also have a spatial effect of regional innovation.

On this basis, this paper empirically tests the relationship between digital finance and regional technological innovation using municipal-level data. First, it verifies the impact of digital finance’s development on regional technological innovation by constructing a panel regression model. Second, considering the possibility of a spatial spillover effect of digital finance’s role on innovation, this paper further explores the geospatial dependence and spillover effect of digital finance and regional technological innovation by using a spatial panel model. Finally, considering China’s significant geographical differences and digital finance’s stage development, the possible significant differences in the spatial and temporal dimensions of the incentive effects of digital finance’s innovation are further explored.

This paper’s innovation is mainly reflected in the following aspects. First, unlike previous literature that examined the impact of traditional financial models such as capital markets and banks on technological innovation, this paper explores financial development’s role in enhancing regional innovation capacity by considering a new financial model of digital finance, that is, it analyzes each service’s innovation effect from multiple dimensions such as credit, investment, funds, insurance, and payment, thus providing more comprehensive data support and a theoretical basis for China’s development of high-quality digital finance. Second, prefecture-level cities are used as a basis for the development of digital finance. An empirical analysis is conducted of prefecture-level cities. This rejects the mainstream provincial-level analysis, which involves an overly large sample size that is not representative of each city’s innovation. Third, based on technological innovation’s dynamic inertial change, this paper integrates multiple methods to explore the relationship between digital finance’s development and technological innovation in order to avoid the possible shortcomings of static analysis. It adds robustness tests to fully ensure robust research findings.

This paper’s findings also have important practical significance. First of all, in the context of this century’s unprecedented changes, China’s 14th Five-Year Plan (2021–2025)’s mission is to connect the great visionary goals of “achieving major breakthroughs in core technologies and entering the forefront as an innovative country.” Furthermore, “innovation” and “sustainable development” are the focuses of the current development plan, which includes scientific and technological innovation as its core strategic support. At this point in time, exploring the potential breakthroughs in China’s regional technological innovation in the financial supply side can provide references for the continued implementation of the innovation-driven development strategy. Secondly, as financial reform is methodically and continuously promoted, digital finance has emerged and developed rapidly as a recent model. In the context of the policy of “financial support for a system of innovation and service to the real economy,” it is urgent to investigate digital finance’s impact on the real economy, especially on technological innovation, which is a key factor determining economic growth. This paper’s findings will not only help government departments to more effectively assess the key elements of regional development, improve the institutional mechanism of scientific and technological innovation, enhance the efficiency of financial services, and formulate increasingly efficient financial supervision programs during the 14th Five-Year Plan’s initial stage. It can also help enterprises by serving as a practical guide and policy reference for them to apply digital finance for achieving technological launches, transformations, and breakthroughs. Furthermore, it can enable them to integrate resources for promoting regional business growth and development, refining “dual circulation” within China and throughout the world, while seeking to achieve the vision of socialist modernization by 2035.

This paper will firstly determine the research’s background and practical significance. Secondly, it will draw on the theoretical basis of digital finance and regional technological innovation, which it will use to propose the research hypothesis. It will then construct a comprehensive index system of these two factors. Furthermore, it will determine the sample and data sources as well as set up the model. Moreover, it will use panel regression and spatial econometric methods to empirically analyze the municipal panel data. Finally, it will draw this paper’s conclusions and apply them to propose policy recommendations.

Theoretical Analysis and Research Hypothesis

Literature Review on the Relationship Between Financial Development and Technological Innovation

Scholars first explored the relationship between financial development and technological innovation in 1912 (Schumpeter, 1912). However, it was not until the promotion of financial marketization and the third technological revolution that research into this relationship formally attracted extensive attention from Chinese and international scholars and became a major emphasis of academic debates. A literature review reveals that scholars mainly focus on the following perspectives in an attempt to build a macro and micro research framework. One is the study of relational outcomes. The literature has shown that both the financial development profile (Nanda & Nicholas, 2014), measured by patterns such as venture capital, the stock market or credit market, and financial development, represented by its scale, structure, and efficiency (L. B. Guo & Wang, 2020), significantly affect technological innovation. Their specific effects are subject to these patterns (Zhou et al., 2021), intellectual property protection (S. Tang et al., 2020), aspects of firm ownership (X. Zhang, 2017), and other factors, and demonstrate heterogeneous variations.

The second is the exploration of the relational process, that is, the mechanism of financial development’s influence on technological innovation. On one hand, some scholars believe that financial development may stimulate micro enterprises to achieve technological innovation by opening to trade (K. Zhang & Huang, 2019), or reducing transaction costs and loosening R&D capital investment (Q. Q. Tang & Wu, 2015). On the other hand, additional scholars believe that the characteristics of technological innovation projects, such as high investment and long cycles, cause innovative enterprises to become strongly dependent on external financing. Other scholars believe that the characteristics of technological innovation projects, such as high investment and a long cycle, increase innovative enterprises’ dependency on external financing. Furthermore, regions with sound financial market systems and high financial development tend to screen value-based technological innovation projects by optimizing the allocation of financial resources, reasonably directing the flow of funds, reducing information asymmetry, and generating the “herd effect” to point out the direction for technological innovation, thus further improving its regional extent (K. Y. Li, 2020).

Although the existing literature confirms the significant role of traditional financial development in enterprise technological innovation from multiple perspectives (Jia et al., 2017), these studies’ results also illustrate the fact that China’s financial system’s development is still unsound, its traditional financial services have insufficient coverage, the prices of financial factors and resource allocation are distorted, enterprises (especially small and micro ones) face financing constraints, the growth of intra-regional and inter-industry innovation investment has gradually slowed, and the improvement of innovation efficiency is inhibited (T. Li & Li, 2019).

As real finance has developed and the technological revolution’s third wave has arrived, finance has become active in the public eye in the new form of digital empowerment. Within a decade, digital finance research is flourishing. Overall, the literature in this area can be broadly categorized into two groups. The first discusses digital finance’s development, including a purely theoretical discussion of the current state of affairs (F. Guo, Kong, & Wang 2016), as well as risk identification and regulation (Jiao et al., 2015). The second category examines digital finance’s practical impact, such as its impact on entrepreneurship (Xuan et al., 2018), banking behavior (Qiu et al., 2018), narrowing the urban-rural income gap (H. Zhang & Bai, 2018), contributing to economic growth (X. Zhang et al., 2020), and fulfilling the financial service needs of disadvantaged groups such as small and micro enterprises and China’s “three rural issues” (agriculture, rural areas, farmers) (Fu & Huang, 2018) on the basis of indicators (F. Guo, Kong, Wang, Zhang, et al., 2016) and empirical studies. However, there is still a lack of research on how digital finance contributes to regional technological innovation.

The Relationship Between Digital Finance’s Development and Technological Innovation

In the traditional financial market, typical financing channels such as banks generally require collateral with strong liquidity, while innovative enterprises have a lower percentage of tangible assets, weaker collateral capacity, and less financing availability. The lack of effective financial support for technological innovation may lead to the cancellation of many innovative projects and curb innovation’s regional efficiency, which ultimately does not contribute to optimizing and upgrading China’s industrial structure or its goal of becoming an innovative country (Aghion et al., 2014).

As a new financial industry focused on inclusion and emphasizing the grassroots, digital finance may be compatible with the characteristics of technologically innovative enterprises’ financing needs and innovation environment. Specifically, digital finance’s positive impacts on regional enterprises’ innovation are mainly reflected in alleviating corporate financing constraints and promoting upgrades in industrial structure. First, digital finance’s development alleviates enterprises’ financing constraints and increases the intensity of their innovative R&D investment, which can develop their technological innovation projects and promote improvements in regional technological innovation. First, as digital finance relies on digital technologies including mobile Internet, cloud computing, big data, and blockchain, it has more unique and efficient information collection and processing capabilities, which can effectively alleviate information asymmetry that potentially occurs between funds’ supply and demand sides during lending. Secondly, digital finance breaks the bottleneck of traditional financial services’ economic development, expands financial coverage, reduces the cost of financial services (W. Wang & Pan, 2015), and fulfills the continuous and stable capital demand for financial services from SMEs, a long-tail customer group, during technological development. Once again, digital finance simplifies the lending approval process and also improves the customer audit and evaluation system, which not only achieves the universal benefit for long-tail users and other regional technological innovators, but also achieves the goal of providing precise and efficient services to developed regions and large enterprises (Liu & Yang, 2017). Finally, while digital finance substantially impacts China’s traditional financial institutions based on the competition effect and demonstration effect, it also accelerates digital transformation and upgrading, and significantly improves the efficiency and quality of traditional financial institutions when they serve technologically innovating enterprises. Second, digital finance’s development promotes the optimizing and upgrading of regional industrial structure, maximizes the spillover effect of technological innovation opportunities, and improves enterprises’ regional innovation capacity. Digital finance, as a combination of digitalization and the traditional financial industry, can use information processing technology to build an evaluation system involving multidimensional indicators to select technologically innovative financing projects with long-term investment value or higher market recognition (H. C. Huang et al., 2021). It can also further direct the flow of idle social financial resources to ensure the sustainability of technological innovation, reshape industrial development’s orientation, and promote the optimization and upgrading of the regional industrial structure (Zheng, 2020). At the same time, digital finance’s credit catalytic effect provides the financial support needed to transform and upgrade regional enterprises. In particular, this effect can alleviate SMEs’ liquidity difficulties, transform labor-intensive enterprises into capital- or technology-intensive enterprises, and can accelerate the regional industrial structure’s optimization. At the regional level, the industrial structure’s upgrading provides ideal conditions for transfers of technological opportunities and optimal allocations of factors, which will positively impact technological innovation (Xu & Xing, 2019). Upgrades of regional industrial structure not only empowers regional enterprises to share and effectively utilize technological opportunities, but also guides transfers of these opportunities to enterprises in more efficient industries, improving these enterprises’ regional technological innovation. In summary, this paper proposes the following hypotheses:

H1: Digital finance development enhances regional innovation.

Although financial agglomeration contributes towards improving economic performance and optimizing economic quality, this effect does not occur unconditionally and must be supported by an ideal local institutional environment (McKinnon, 1973). In general, an ideal institutional environment includes a healthy relationship between the government and the market, adequate factor circulation, free competition of products, and a sound legal system, that is, an efficiently functioning market economy. Therefore, an ideal institutional environment not only protects financial institutions’ legitimate rights and interests, but also can promote healthy competition in the financial industry, which can promote its sustainable and stable development. In other words, optimizing the external institutional environment can effectively enhance the external scale effect, network effect. competition effect, and self-reinforcing effect resulting from financial agglomeration; further improve financial institutions’ resource allocation ability, improve economic development quality, and stimulate economic development momentum while enhancing economic development. Economic development involves significant differences between internal and external conditions, while each region tends to have a different institutional environment. China’s eastern coastal regions have more thorough market-oriented reforms and a more favorable institutional environment, and their financial agglomeration can more easily promote high-quality economic development (Levine, 2005). In contrast, its central and western regions have less market economic development, its market-oriented reforms still need improvements, while it has weaker intellectual property protection mechanisms and lower contract enforcement efficiency. In these circumstances, this region has low resource allocation efficiency (Yi & Zhou, 2018), and its market mechanisms cannot be readily perform their roles, preventing them from achieving full utilization (X. P. Ma, 2020). These regions’ underdeveloped institutional environment reduces their financial institutions’ freedom to obtain resources, restricts their development, and causes their financial institutions’ resource allocation efficiency to decline. Moreover, it is difficult to truly and effectively prevent violations of these institutions’ rights and interests. As a result, the costs and prices of financial products and services could rise, eventually triggering distortions in resource allocation (K. Zhang, 2019). In summary, an underdeveloped institutional environment weakens financial institutions’ resource allocation ability, makes it challenging to effectively maximize financial agglomeration, and negatively impacts economic development.

H2: Compared with other regions, financial agglomeration in China’s eastern coastal regions contribute more significantly to economic development and its quality.

Sample, Variables and Model Setting

Sample and Data Sources

This study utilizes panel data encompassing 283 Chinese cities from 2013 to 2020 to analyze the relationship between digital inclusive finance and regional innovation. Data sources for specific variables are detailed in Table 1.

Variable Definitions.

Variable Selection

Explained Variables

Regional innovation capacity (innovation). Referring to research results from scholars such as K. Zhang (2019) and Bian et al. (2019), a comprehensive evaluation of regional innovation capacity is conducted based on the dimension of innovation output, and the evaluation index is the amount of patents granted. Patent grants in China currently include three types: invention patents, utility patents, and design patents. Utility and design patent grants are usually the results of strategic innovation in pursuit of quantity and speed, while invention patent grants are high-standard, substantial, and breakthrough innovation output that can more comprehensively and objectively reflect regional innovation capacity (W. Q. Li & Zheng, 2016). Therefore, in this paper, regional innovation capacity (innovation) is evaluated comprehensively based on the number of invention patents granted per 10,000 people in prefecture-level cities. For robustness, the total number of patents granted per 10,000 people (ppat) is used as an alternative indicator. The logarithm of patent data is applied to mitigate heteroskedasticity.

Core Explanatory Variables

Cities’ digital inclusive financial development serves as a focal point in this study, assessed through the PKU’s prefecture-level cities’ digital inclusive finance index, as compiled by F. Guo et al. (2020). This index functions as a proxy, capturing the multifaceted aspects of digital inclusive finance development. Three primary sub-dimension indices—namely coverage, depth of use, and the degree of digital support services—are selected for analysis. The composite value is utilized for examination, with the natural logarithm applied to the original digital inclusive finance data to account for scale differences.

Control Variables

A comprehensive selection of control variables is employed based on an exhaustive review of existing research. Economic development, represented by urban GDP per capita (lngdp), is included as the first control variable. The second variable, regional credit constraint (finance), gauges the extent of traditional financial development, expressed as the proportion of the balance of financial institutions’ RMB loans to end-of-year GDP. The third variable, the degree of openness to the outside world (open), is measured by the proportion of cities’ total actual foreign investment to GDP. The fourth variable, science and education investment (szi), is crucial for regional innovation, reflecting the contribution of talent development and scientific research. Human capital (he), the fifth variable, aligns with human capital theory, emphasizing the interdependence of regional innovation and economic growth. The industrial structure (stru), as the sixth variable, is assessed through the proportion of the secondary industry’s output value to GDP, capturing the intricate relationship between regional innovation and industrial structure. The seventh variable, infrastructure (facility), evaluates the impact of developed infrastructure on innovation factors’ flow cost. Measured as road ownership area per capita in cities, it plays a vital role in facilitating innovation (Xuan et al., 2018). Detailed definitions of these variables are available in Table 1.

Model Setting

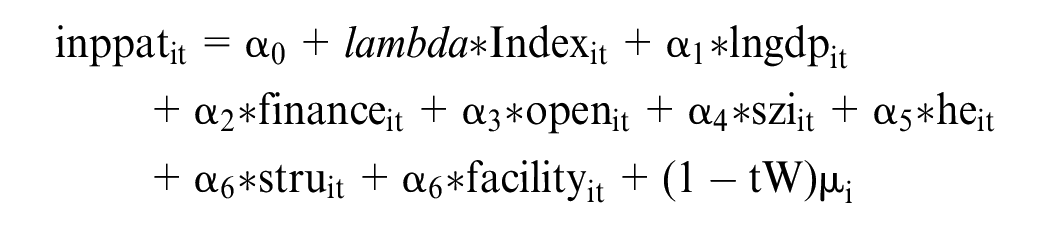

The econometric model, drawing from the methodologies of Cui et al. (2018) and Y. J. Li et al. (2018), constructs a panel econometric model to examine the impact of digital finance on regional innovation. The benchmark regression model is articulated as follows:

The spatial error model (SEM) is presented as follows.

Here, ρ, lambda are spatial lag coefficients reflecting the spatial dependence of sample observations, that is, the direction and degree of influence of neighboring regions on observations in the region W, which is the spatial weight matrix of lag order among n, and εit is the disturbance term.

Spatial weight matrix. According to the first law of geography, two things with a closer geographic distance have a closer connection. Specifically, they signify the directional and quantitative impact of neighboring regions on observations within the region W. Here, W represents the spatial weight matrix, capturing lag order among n observations, and εit denotes the disturbance term. Regarding the spatial weight matrix, its formulation aligns with the first law of geography, asserting that regions in closer geographic proximity exhibit a stronger connection. Consequently, scholars commonly establish the spatial weight matrix based on the geographic distance between locations. In this study, we adhere to the methodology proposed by Q. Guo et al. (2021) for constructing the geographic distance weight matrix. The approach involves selecting 283 prefecture-level cities as the sample and utilizing the reciprocal of the squared geographic distance (d) between cities to formulate the spatial weight matrix. The precise calculation is expressed as follows:

where d is the geographical distance between the two cities. This methodological choice ensures a rigorous and consistent treatment of spatial relationships within the analytical framework.

Empirical Results and Analysis

Descriptive Statistical Analysis

In this paper, 283 cities are selected as samples, and relevant data is obtained through PKU’s Digital Inclusive Finance Index published by its Digital Finance Research Center, as well as the China Statistical Yearbook, China City Statistical Yearbook, and China City Construction Statistical Yearbook. The patent data was then counted according to data from the China Research Data Service Platform. Table 2 displays the descriptive statistical results for the main variables.

Descriptive Analysis.

Table 2 displays the descriptive analysis, and lists each variable’s maximum, minimum, mean, standard deviation, and median.

Correlation Analysis

Table 3 displays the results for the correlation analysis using the Pearson correlation analysis. These results indicate that regional innovation capacity (inppat) is significantly and positively correlated with the digital finance index (Index) with a correlation coefficient of 0.381, which is significant at the 1% level. The correlation between regional innovation capacity (inppat) and economic development (lngdp), regional credit constraint (finance), openness to the outside world (open), science and education investment (szi), human capital (he), and infrastructure (facility) is significantly positive with correlation coefficient values of 0.689, 0.457, 0.319, 0.113, 0.619, 0.379, respectively. However, correlation analysis is only a single factor analysis, and multiple linear regression must be used to calculate the final correlation between the variables.

Correlation Analysis.

Correlation is significant at the .01 level (two-tailed).

Spatial Correlation

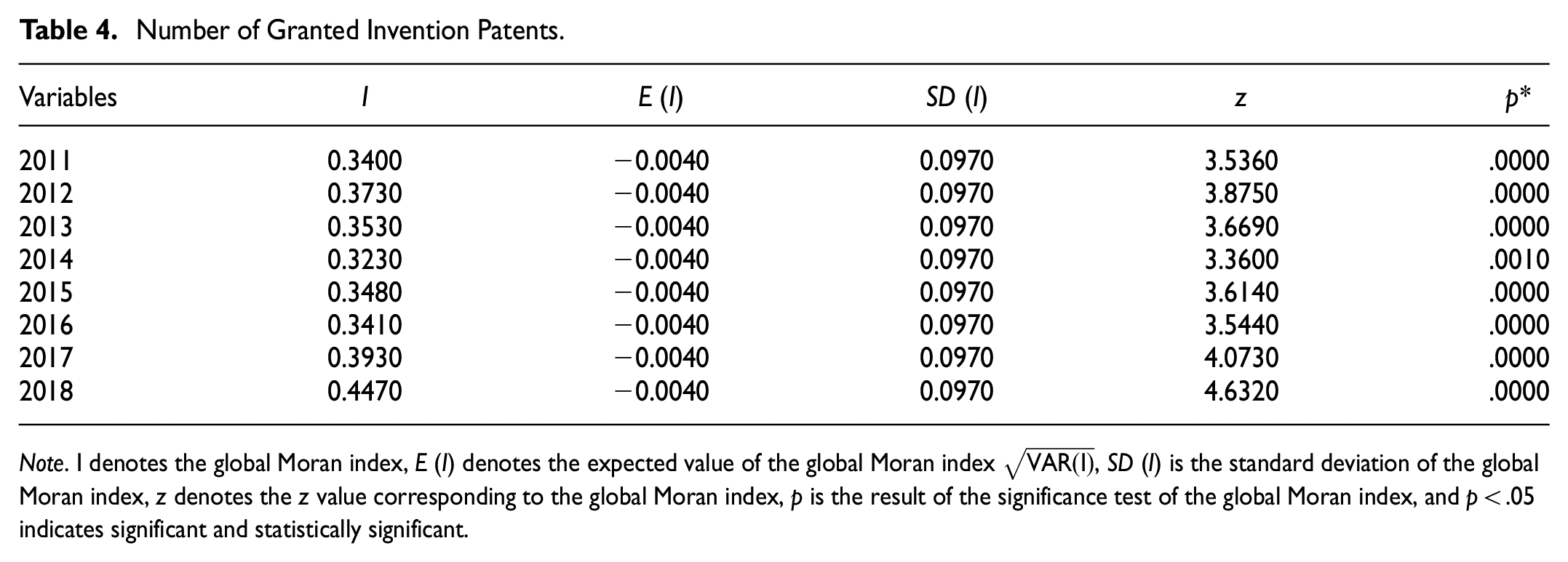

The analysis of the global Moran’s index was conducted before the spatial panel regression. STATA software was used to calculate the number of granted invention patents and digital finance index (Index) of 283 prefecture-level cities from 2011 to 2018 in accordance with global spatial correlation’s meaning and formula. The results of Moran’s index are displayed in Tables 4 and 5.

Number of Granted Invention Patents.

Note. I denotes the global Moran index, E (I) denotes the expected value of the global Moran index

Digital Finance Index.

Table 4’s results indicated that the Moran’s I value of the number of granted invention patents fluctuates between 0.3 and 0.4 and also fulfills the significance test at the 1% level, indicating that the sample cities’ innovation capacity is not randomly distributed at the spatial level, but very significantly influenced by the neighboring areas, demonstrating the phenomena of high-high agglomeration and low-low agglomeration. Table 5’s results indicate that the Moran’s I value of the digital finance index fluctuates between 0.4 and 0.5, and also fulfills the significance test at the 1% level, indicating that the spatial correlation of financial innovation in these cities is significant.

Regression Results of the Underlying Econometric Model

Table 6 displays the results of the mixed model, static fixed model, and stochastic model. First, the coefficients of the numerical financial index (index) for each prefecture-level city are positive in all three models, while the stationary model (fe) and stochastic model (re) are significant at the 1% confidence level, but the mixed model (ols) is not significant (the concomitant probabilities of this model’s F-statistic and LM test are 0, which are less than the significance level of 0.05, rejecting the hypothesis that the mixed cross-sectional model is more effective relative to the fixed-effects and random-effects models; therefore, a mixed cross-sectional model is not required). The numerical financial index has a positive effect on regional innovation. Economic development (lngdp), regional credit constraint (finance), as well as science and education investment (szi) are significantly positively correlated, and industrial structure (stru) is significantly negatively correlated. A higher extent of regional economic development and credit constraint increases science and education investment’s ability to promote regional innovation. A higher proportion of secondary industry inhibits the development of regional innovation.

Base Regression Results.

Note. t statistics in parentheses. OLS indicates multiple linear regression, fe indicates fixed effects regression, and re indicates random effects regression; _cons is the constant term; r2 is the degree of interpretability, and F/Wald chi2 is the model’s equation test.

p < .1. **p < .05. ***p < .01.

Spatial Panel Regression

In this paper, firstly, the fixed effect or random effect model was selected. The econometric model was tested using the Hausman test with a chi-square value of 195.73, corresponding to a p-value of 0.000. The empirical test results were obtained through panel calculations in the following table.

Table 7 displays the regression results. In this paper, the LR test is intended to verify whether the SAR or SEM model is used. The test results indicate that if LM(lag) is greater than LM(error), the SAR model is used; otherwise, the SEM model is used. When considering the current results, authoritative literature, and previous studies, the current results tend to use the SEM model. In the specific results, lambda is significant, indicating the existence of spatial benefits and of spatially significant spatial spillover effects of regional innovation capacity in China’s prefecture-level cities. The numerical financial index (index) is significantly positively correlated with a regression coefficient of 0.0904, and the numerical financial index (index) can positively promote regional innovation. This research result is consistent with the findings of scholars such as H. C. Huang et al. (2021), while hypothesis H1 verified that the hypothesis holds. Based on the premise of improving risk regulation, digital inclusive finance positively impacts innovative subjects’ financial innovation ability, and to a certain extent, it can overcomes the obstacles affecting innovation input and transformation. As for the control variables, economic development (lngdp), regional credit constraint (finance), science and education investment (szi), and human capital (he) are significantly and positively correlated, and improvements in regional economy, enhancements in regional credit constraints, increases in government science and education investment, and the continuous improvement of human capital can all positively promote improvements of regional innovation capacity in line with the existing situation. This study found that the degree of openness to the outside world (open) and industrial structure (stru) are significantly negatively correlated, and a higher proportion of secondary industry and a higher degree of openness to the outside world do not tend to increase regional innovation.

Spatial Regression Results.

Note. t statistics in parentheses. SAR is the spatial autoregressive model; SEM is the spatial error model; LM (error)/LM (lag) is the Lagrange multiplier form, and R-LM (error)/R-LM (lag) is the Lagrange multiplier form of the robust form, which is used to determine whether to choose the SAR or SEM model.

p < .1. **p < .05. ***p < .01.

Region-Based Heterogeneity Analysis

As a powerful complement to traditional finance, the development and promotion of digital finance focuses more on fulfilling the financial needs of less developed regions and special groups such as SMEs. Therefore, considering the inclusive nature of digital finance, the spillover effects of its innovation may also vary across geographic regions with varying economic development. In order to further investigate what kind of multivariate characteristics that digital finance presents among different geographic regions, this section divides the national sample into three geographic regions (eastern, central, and western) according to the National Bureau of Statistics’ criteria, and conducts regressions to further analyze digital finance’s impact on regional innovation.

The SEM model results for the three major regions (eastern, central and western) are presented sequentially in Table 8. First, eastern and central’s lambda are significant in the results, indicating that a spatially significant spatial spillover effect of regional innovation capacity exists in China’s eastern and central prefecture-level cities. Consistent with the full-sample regression results, the estimated coefficient of the digital finance development variable is significant at the 1% level, further corroborating hypothesis H1. but the western region’s lambda results are not significant, and its innovation spillover effect is not significant. This effect differs significantly among each region, specifically “East > Central > West.” 1 The regression analysis of the numerical financial index (index) on regional innovation indicates that the central region’s numerical financial index (index) is not significant, while the eastern and western regions are significant at the 1 and 10% levels, respectively. In other words, compared with the western and central regions, the eastern region can obtain more spillover dividends during digital finance’s development, indicating to a certain extent that if the eastern region can further develop and rationally utilize digital finance, it will not only effectively improve regional innovation, but also drive inter-regional innovation and enhance regional economic development (Table 9).

Regional Variability Analysis.

Note. t statistics in parentheses.

p < .1. **p < .05. ***p < .01.

Robustness Test Results.

Note. t Statistics in parentheses.

p < .05. ***p < .01.

Robustness Test

The results of the heterogeneity tests on the overall regression and sub-regions have somewhat proved the robustness of this paper’s basic conclusions. To further enhance the research findings’ reliability, this paper chooses the number of total patents granted per 10,000 people as a proxy variable for regional innovation in its spatial panel analysis, using the SEM model. The results indicate that both the overall regression and sub-regional heterogeneity analysis found that the hypothesis is valid.

Conclusions and Recommendations

Research Findings

In the context of China’s economic development entering a new era and gradually forming a new development pattern with its domestic circulation as the main focus and its domestic and international dual circulation promoting each other, innovation is increasingly becoming an important strategic method for achieving high-quality economic development. Moreover, information technology’s rapid development has promoted a combination of finance and technology, resulting in a new financial industry and significantly impacting economic development. In this context, it is highly practical to explore digital finance’s impact on regional innovation. This paper examines digital finance’s impact on regional technological innovation by using panel data of 283 cities from 2011 to 2018. The research results indicated that digital finance’s development significantly impacted efforts to enhance regional technological innovation. This is mainly since (1) finance, which provides powerful support to promote an innovation-driven strategy, and its new manifestation (digital finance) has a significantly positive impact on the enhancement of regional innovation. This is an indication that when verifying the following theory, digital finance breaks the bottleneck of traditional financial services’ economic development, expands financial coverage, reduces the cost of financial services, and fulfills the needs of small and medium-sized enterprises (SMEs) as a long-tail customer group during technological research and development for the funding needs of continuous and stable financial services. As it relies on digital technologies such as mobile Internet, cloud computing, big data, and blockchain, digital finance has more unique and efficient information collection and processing capabilities, which can effectively alleviate information asymmetry that may occur between funds’ supply and demand during lending. (2) Furthermore, there is a spatial spillover of regional innovation as well as spatial correlation of regional innovation among China’s prefecture-level cities. In other words, regional innovation can affect not only a region’s technological innovation, but can also improve technological innovation in its neighboring regions. Digital finance’s development can help to promote the optimization and upgrading of regional industrial structure, maximize the spillover effect of technological innovation opportunities, and improve regional enterprises’ innovation capability. As a combination of digitalization and traditional finance, digital finance can apply information processing technology to build an evaluation system with multidimensional indicators for selecting technologically innovative financing projects with long-term investment value or higher market recognition (G. R. Ma & Yang, 2011), further guide the flow of idle financial resources to ensure the sustainability of technological innovation, reshape industrial development orientation, as well as promote optimization and upgrading of regional industrial structure (Zheng, 2020). (3) The correlation between digital finance and regional innovation has significant variability, with more significant innovation spillover effects in the eastern regions compared to the central and western regions. This confirms that digital finance’s incentive effect on regional technological innovation is stronger in a better institutional environment. The development of innovation is highly dependent on the environment where firms are located. When the region’s institutional quality is poor, digital finance may face a continuous lack of regulation and unsustainable development, so it cannot release financing constraints on regional enterprises’ technological innovation. At the same time, poor institutional quality may also mean that institutional rigidity makes it difficult to create an atmosphere that encourages financial and technological innovation. In a market environment without proper fault tolerance, digital finance’s development will encounter bottlenecks, weakening its ability to provide financial support and resource orientation for regional enterprises’ technological innovation, while the technology market’s long-term monopoly will eventually discourage protected and similar enterprises from continuing their technological R&D, ultimately inhibiting regional enhancement of technological innovation (

Policy Recommendations

Based on the above analysis and conclusions, this paper offers the following policy recommendations.

First, it is important to strengthen the comprehensiveness and richness of digital finance’s business development, and further develop high-quality digital finance. Furthermore, fully exploiting digital finance business’ service capacity for regional innovation, widening the breadth of digital finance’s coverage and digitalization, and enhancing digital finance’s service capacity will improve its service efficiency as well as enhance the innovation spillover effect. Relying on digital technology can strengthen the symmetry of market information, enable regional financial networks to provide more efficient credit services to innovative subjects, and overcome innovative SMEs’ financing obstacles. According to the science and technology finance development plan issued by the People’s Bank of China, the Chinese government should accelerate its improvements of the digital financial supervision system and further enhance the capability of technological applications in the financial industry. Based on the premise of protecting user privacy, digital inclusive finance’s penetration should be expanded to promote the development of regional innovation.

Secondly, it is important to guide the release of domestic demand and create effectively operating transmission channels for residents’ consumption. In the context of dual circulation, the key to domestic circulation relies on innovation, while domestic demand’s expansion is an important transmission channel for digital finance to positively impact regional innovation.

Third, it is important to build an evaluation system involving multi-dimensional indicators to select technologically innovative financing projects with long-term investment value or higher market recognition, further guide the flow of idle social and financial resources to ensure the sustainability of technological innovation, reshape the orientation of industrial development, as well as promote regional industrial structure’s optimization and upgrading.

Fourth, venture capital’s spillover effect on regional technological innovation in China’s eastern region is higher than in its central and western regions, indicating that an efficient spillover channel for venture capital has formed in the eastern region. The western region’s governments should attract venture capital funds, advanced technology, and management experience to improve venture capital’s positive impact on technological innovation. They should accelerate their changes in innovation modes, enhance their regional innovation quality audits, improve their development of innovation evaluation systems, cautiously prevent the emergence of false or strategic innovation, as well as intensify the effectiveness of financial support and industrial policies to introduce measures aiming to encourage innovation development.

Research Limitations and Future Research Focus

The current study has shortcomings as well as room for further development. First, regional innovation level is a multidimensional concept, while the number of invention patents per 10,000 people as a measurement indicator in this study is slightly low (

Footnotes

Acknowledgements

We gratefully acknowledge the assistance of my teachers and my classmates.

Author Contributions

All authors contributed to the study conception and design. Material preparation, data collection and analysis were performed by Yang Dong and Haiying Pan. The first draft of the manuscript was written by Yang Dong and all authors commented on previous versions of the manuscript. All authors read and approved the final manuscript.

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.

Notes

Data Availability Statement

The research data supporting this publication are available from the corresponding author.