Abstract

The aim of this paper is to deepen the analysis of services reshoring in the Spanish services sector, both as a whole and for its constituent elements, examining both intra- and inter-sectoral components. Likewise, it analyzes the impact of this strategy on employment in the services sector, also differentiating between broad reshoring, intra-sectoral reshoring and inter-sectoral reshoring. The data used come from the Input-Output Tables of the Spanish National Accounts published since 2000. The results show Spanish service companies significantly reduced their contracting of activities abroad between 2008 and 2010, substituting foreign intermediate services for domestic services. This process of reshoring is observed with greater intensity in inputs of the same sector. However, since 2010 Spanish service companies have slightly increased their contracting of foreign services per unit of output, adopting new services offshoring strategies, although to a lesser extent than in the period prior to the recession. In the analysis of the effect of reshoring on services employment can be concluded that services reshoring has not generated employment in the Spanish service sector.

Introduction

From the 1990s until the Great Recession of 2008, the world experienced a process of increasing globalization, mainly due to the intense development of the offshoring phenomenon (Baldwin, 2016). The term offshoring means the displacement of part of a company’s production process abroad in order to take advantage of the comparative cost advantages to be gained in those countries. Until 2008, there was a strong process of offshoring of low-skilled labor-intensive phases of production from advanced economies to emerging economies, where the greatest comparative advantages in the cost of this factor may be found. On the other hand, the phases of the processes that require more skilled labor have remained in the advanced economies (Blinder, 2006; Zhang, 2003). All this has led to an unprecedented growth in international trade flows and enormous interdependence between countries.

However, the 2008 Great Recession slowed this offshoring growth process and gave rise to the beginning of a reshoring process in advanced economies, returning the manufacturing of certain goods and the performance of activities that had previously been transferred abroad, mainly to emerging countries, back to the countries of origin or nearby locations (Borga et al., 2020; Dachs et al., 2019; Foerstl et al., 2016; Kataryniuk et al., 2021).

The reasons behind the emergence of this phenomenon of reshoring in the first decade of the 21st century have been widely studied in the economic literature in regards to manufacturing (Di Mauro et al., 2018; Foerstl et al., 2016; Johansson & Olhager, 2018; Stentoft et al., 2016; Vecchi, 2017) and also, albeit to a much lesser extent, to service activities (Albertoni et al., 2015, 2017; Lacity et al., 2016; Margulescu & Margulescu, 2014; Xia et al., 2015).

The public health crisis brought about by COVID-19 led to major cuts in the supply of essential components for European and U.S. manufacturers from China, the world’s main supplier of intermediate inputs. This, together with the subsequent increase in energy costs and the problems that arose in global shipping, accentuated the shortages and increased the cost of supplies from Asian countries. In this adverse scenario for the industries of the advanced economies immersed in offshoring processes, the new restrictions in the international supply derived from the War in Ukraine, are accentuating some reshoring processes initiated during the previous crisis, with considerable expectations that this phenomenon will continue to grow in the future (Chowdhury et al., 2021; Ivanov & Dolgui, 2020; Juergensen et al., 2020; Sharma et al., 2020; Strange, 2020). However, no in-depth studies analyzing such impacts on offshoring and reshoring processes around the world are yet available.

During both the first crisis of 2008 and the subsequent crisis of 2020, political leaders in Europe and the United States spoke out in favor of returning production and activities that were previously offshored to emerging regions back to their own countries in order to support their reindustrialization, eliminate dependence on a few providers located in foreign countries and generate new jobs in their economies (Baldwin & Evenett, 2020).

However, these expectations, coming mainly from political circles that associate offshoring with job losses and reshoring with job creation in advanced economies, are not supported by economic analysis. On the one hand, in relation to delocalization or offshoring processes, which consist of the relocation of some inputs to more efficient locations, it has been demonstrated in the economic literature that they lead to improvements in the efficiency and the welfare of the countries involved, which, in turn, should generate higher economic growth and, therefore, employment in the long run (Blinder, 2006; Grossman & Rossi-Hansberg, 2006; Helpman, 2011; Olsen, 2006). Likewise, in relation to the impacts on employment levels, there is ample empirical evidence showing that such processes do not generate significant employment losses in the countries that implement them (Fuster et al., 2019; Hummels et al., 2018). On the other hand, reshoring processes comprise the relocation of inputs in the country of origin, totally or partially undoing a previous offshoring strategy through which the most efficient localization had been sought. Therefore, without knowing the causes of the reshoring strategy, its possible implications for employment or other economic variables cannot be theoretically supported, since this will depend on whether or not the reasons for implementing the strategy respond to efficiency criteria. There is still no theoretical framework in the academic literature that demonstrates the implications of the reshoring strategy. There is also limited evidence on the effects that reversing offshoring strategies has on employment. To the best of our knowledge, there are only two papers studying the implications of reshoring on employment; Fuster et al. (2020), referring to the service sector and Krenz et al. (2021), referring to manufacturing. The first analyzes services reshoring, concluding that this practice does not generate new jobs. The second studies reshoring motivated by automation in manufacturing and concludes that this strategy generates high-skill employment, but not low-skill employment, which had been lost in advanced economies as a result of previous offshoring processes. These results show that the employment effects of reshoring processes are not obvious and that, therefore, further analysis is needed to understand these processes and their causes in greater depth so as to be able to make general predictions or hypotheses about these impacts..

For all these reasons, the aim of this paper is, firstly, to deepen the analysis of services reshoring in the Spanish services sector, both as a whole and for its constituent elements, examining both intra- and inter-sectoral components to obtain detailed knowledge of the process. Secondly, to analyze the impact of this strategy on employment in the services sector, also differentiating between global or broad reshoring, intra-sectoral reshoring and inter-sectoral reshoring, with the aim of expand on the findings available in the economic literature for this sector and thus provide new evidence that can contribute to a debate, which is so relevant in the current climate, in which so many prominent voices base the defense of the return home of productions located in foreign countries on the assumption of a causal relationship between reshoring and employment generation.

Using a methodology based on sectoral data from the Input-Output Tables of the Spanish National Accounts, the nature of the reshoring and offshoring processes in the service sector during the period 2008 to 2015 is analyzed, with 2015 being the last available year with complete data available to perform the analysis. Likewise, an analysis is carried out to determine whether offshoring and reshoring stem from, respectively, higher or lower dependence on imported services from the same branch of activity (intra-sectoral) or from other activities (inter-sectoral). In this way, for each sector previously involved in offshoring that has reversed the strategy in recent years, it is possible to distinguish in which cases and to what extent the activities returning to the country of origin belong to the same sector (intra-sectoral reshoring) or are activities from other different sectors (inter-sectoral reshoring). This approach also enables an estimation of the impact of reshoring on employment levels, distinguishing between intra- and inter-sectoral reshoring. A more precise explanation is therefore obtained of the type of activities that return to the country of origin through reshoring and of the effects in each case on employment levels.

Following the introduction to this paper, the available empirical evidence on causes of services reshoring is reviewed. There is then a description of the methodology used to calculate the offshoring and reshoring indicators and a reference to the data used in the empirical analysis. The next section presents the results obtained in the analysis of these strategies. Subsequently, we estimate the effects of services reshoring on the level of employment in the services sector using panel data. Finally, the conclusions are presented.

Literature on the Causes of Services Reshoring Processes

The existing literature on the phenomenon of services reshoring is particularly scarce. It is limited to a very small number of case studies, referring to specific services such as call centers, financial, accounting, and IT services, as well as two more recent studies that take a more general approach covering all service categories.

In the case studies, the drivers for reshoring processes are analyzed for the specific types of services listed. All involve services that were previously offshored from advanced economies to countries offering cost advantages, mainly in terms of labor, and which have since been returned to the countries of origin through reshoring processes.

For call centers, from the companies’ perspective, Aksin et al. (2007), Heizer and Render (2014), and Nearshore Americas (2010) find that the determining factors for reshoring are poor service from foreign suppliers, the negative image in the home country, lower productivity in foreign countries, the technological requirements to provide quality services, and the desire to eliminate geographical risk. Other studies, focusing on consumer considerations (Bharadwaj & Roggeveen, 2008; Roggeveen et al., 2007; Metters, 2008), suggest consumer preferences for interacting with domestic operators as causes of reshoring. Meanwhile, Isidore (2011) and Luce and Merchant (2003) analyze the reshoring process of specific cases of U.S. companies that terminated their previous offshoring contracts of their call centers in India to bring them back to the country of origin. Others use theoretical models to study which characteristics determine the optimal location of call centers, obtaining results that explain the reshoring phenomenon (Xia et al., 2015).

For financial and accounting services, Lacity et al. (2016) show how a large U.S.-based company, which reversed previous offshoring contracts with Indian suppliers and replaced them with a domestic supplier, obtained advantages derived from the higher productivity of domestic workers, reductions in coordination costs with foreign suppliers, lower transaction costs of domestic provision, and greater transparency and flexibility in the provision of services.

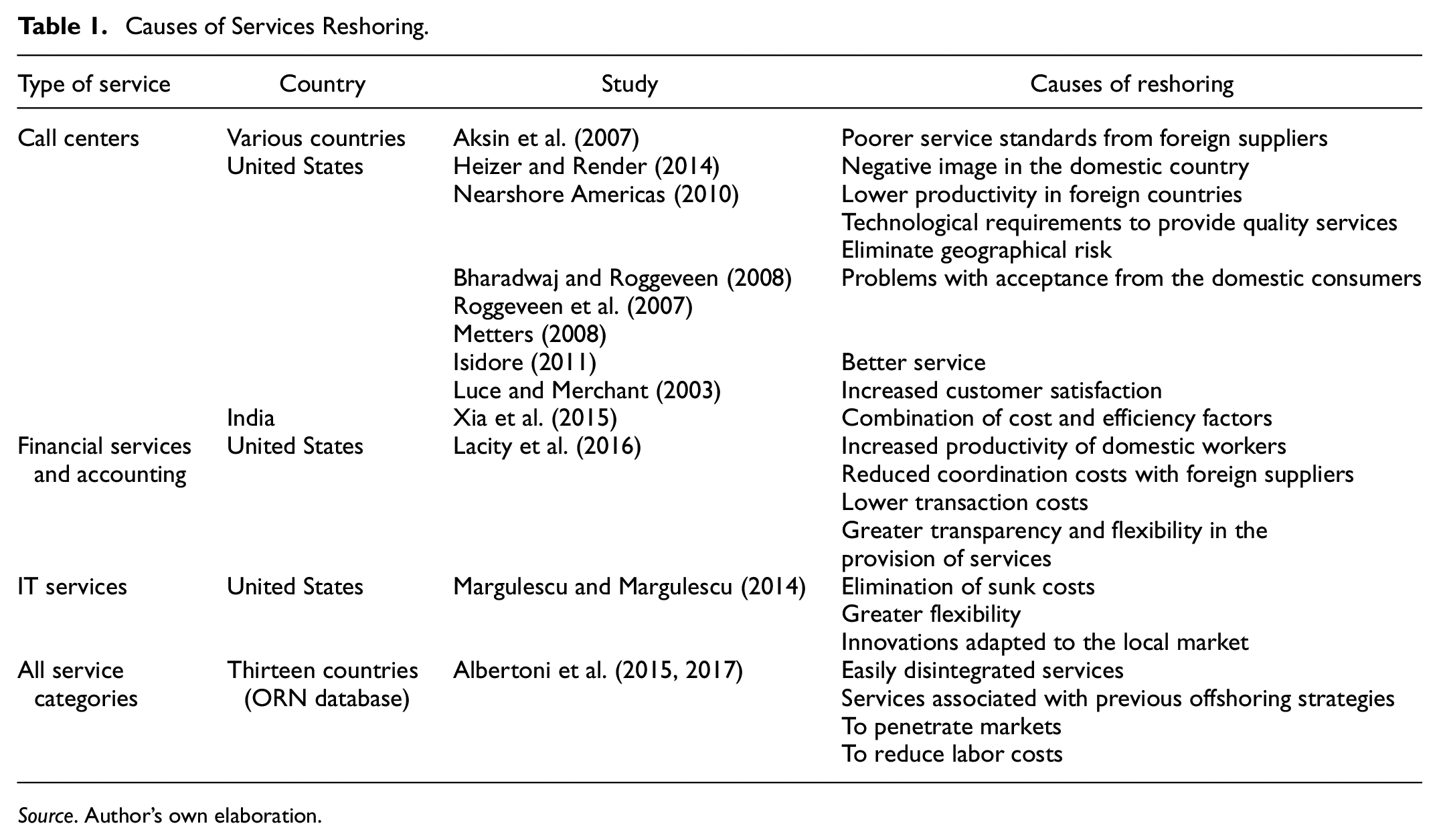

With respect to IT services, the main reasons identified in Margulescu and Margulescu (2014) as to why many multinational companies in advanced economies are repatriating their offshoring outsourcing processes from China and India back to their home countries stem from increased flexibility and greater innovation adapted to the local market through the integration of such services into the company. Finally, the two most recent studies, Albertoni et al. (2015, 2017) analyze the nature of the services reshoring processes detected worldwide until 2015 and investigate their causes, through a standard logistic regression for a sample of 454 companies. In both cases the information comes from the database developed by the Offshoring Research Network (ORN). The results of these studies show that the service activities most likely to engage in reshoring processes are those that are more easily disintegrated. This is because in these cases there is no need for the activities to remain integrated within the company in the country of origin and, therefore, they can more easily be transferred to other countries through offshoring processes. For the same reasons, these services can also return to the country of origin through reshoring processes when the objectives of previous offshoring strategies are not achieved. Another characteristic of the services most likely to participate in reshoring processes involve situations where previous offshoring strategies linked to the penetration of new markets are reversed. Examples include offshoring strategies for the likes of marketing, financial or commercial services, where services are relocated to other countries to support the introduction of an industry in a new market and return to the country of origin when, for example, that industry returns. Finally, the third variable that explains services reshoring processes is labor cost savings. When these cost savings diminish or disappear in the countries where offshoring has taken place, the strategy tends to be reversed through reshoring. The results described are listed in Table 1.

Causes of Services Reshoring.

Source. Author’s own elaboration.

Methodology and Data

Although Feenstra and Hanson (1996, 1999) were the first to measure offshoring using the ratio of imported inputs over total inputs employed (domestic plus imported) as an indicator, the most widely used indicator in subsequent empirical literature is the ratio of imported inputs over output (Cadarso et al., 2008, 2012; Campa & Goldberg, 1997; Castellani et al., 2013; Díaz Mora et al., 2007; Ekholm & Hakkala, 2005; Falk & Wolfmayr, 2008; Fuster et al., 2018, 2019; Geishecker & Görg, 2005; Michel & Rycx, 2012). This final indicator will be used in this paper to measure the dependence on imported intermediate services and, in this way, to analyze the intensity of services offshoring and reshoring strategies by companies in the Spanish service sector. The index used is expressed as:

Where BDI jt is an indicator to measure the dependence on imported intermediate services for sector j in year t; IIijt the intermediate services imported by sector j from sector i in year t; and Yjt the value of sector j’s production.

An increase in this index indicates a greater dependence on imported intermediate services per unit of output, that is, it reveals that firms are increasing their sourcing of intermediate services from other countries, a strategy known as services offshoring. A reduction in this indicator, on the other hand, implies a reversal of the previous offshoring strategy, that is, a return of previously offshored activities to the country of origin, which translates to less dependence on foreign services. This more recent strategy has been referred to as “services reshoring.”

Although this indicator measures dependence on total imported service inputs, both from the same service sector as well as other service sectors, it is also interesting to determine the extent to which the sectors that source services from abroad do so from their own or other service sectors. To this end, a distinction can be made between intra- and inter-sectoral dependence. Dependence on imported inputs from the same sector, i.e., intra-sectoral dependence, was labeled narrow offshoring by Feenstra and Hanson (1999). The indicator to be used to measure intra-sectoral offshoring and reshoring strategies is expressed as:

where NDI jt represents the index of narrow dependence of imported services of sector j in year t; IIjjt the total imported inputs used by sector j of its same sector j in year t; and Yjt the value of sector j’s production in year t.

The inter-sectoral dependence indicator can be calculated as the difference between the broad dependency indicator (BDI) and the narrow or intra-sectoral dependence indicator (NDI).

The joint analysis of these indicators makes it possible to determine whether offshoring and reshoring stem from, respectively, higher or lower dependence on imported intermediate services from the same branch of activity (intra-sectoral) or from other activities (inter-sectoral).

The data used in this paper come from the Input-Output Tables of the Spanish National Accounts published by the National Statistics Institute (INE in Spanish abbreviation) for the period between 2000 and 2015, with 2015 being the last year with complete data available to perform the analysis. In the period 2000 to 2010 the input-output tables are published annually with complete data, including the import destination table. However, since 2010 the import destination table is published every 5 years and therefore after 2010 this information is only available for 2015. The next input-output tables with complete information will present 2020 data, which are yet to be published. Since the calculation of the offshoring/reshoring indicators requires information from the import destination table, the analysis can only be carried out for the period 2000 to 2010 and for 2015, which are the only years for which we have all the information necessary for the analysis.

Services Offshoring and Reshoring

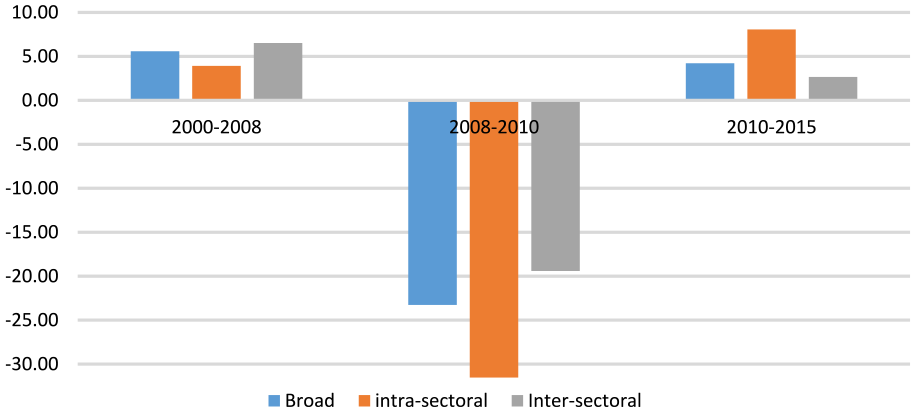

Empirical evidence shows a growing trend in services offshoring by the Spanish service sector between 2000 and 2008, which reveals that service companies increasingly imported activities that were previously integrated internally or sourced from domestic suppliers (Figure 1). The service sectors recorded a sharp increase in the contracting of foreign services per unit of output, both from the same sector and other sectors, with average annual variation rates of 3.91% and 6.52%, respectively, with inter-sectoral offshoring therefore being more pronounced (Figure 2). Inter-sectoral dependence in 2008 represented 66.35% compared to 33.65% for intra-sectoral dependence (Table 2).

Dependence on imported intermediate services (imported intermediate services/production index).

Services Offshoring/Reshoring (annual average variation rate of imported intermediate services/production).

Broad, Intra-Sectoral and Inter-Sectoral Services Offshoring and Reshoring.

Source. Prepared by the authors from Input-Output Tables, Spanish National Accounts, INE.

Note. NDI represents the intra-sectoral index and refers to the dependency on intermediate services imported from the same sector of activity relative to the production value; Inter-sectoral index refers to the dependency on intermediate services from other service sectors relative to the production value. The sum of the two indicators gives the BDI index, a measure of the total dependency on imported intermediate services relative to the production value (II/Y). An increase in the indexes indicates offshoring and a reduction in the indexes indicates reshoring. BDI = broad dependency index; NDI = narrow dependency index; IDI = inter-sectoral dependency index.

Since 2008, coinciding with the onset of the Great Recession, a change in trend has been observed (Figure 1). Spanish service companies significantly reduced their contracting of activities abroad, substituting foreign intermediate services for domestic services, which led to a partial return of service production to Spain. This process of reshoring is observed with greater intensity in inputs of the same sector, so that a process of narrow reshoring is more pronounced than that of inter-sectoral reshoring (Figure 2). While inter-sectoral dependence decreased between 2008 and 2010 at an average annual rate of −19.41%, intra-sectoral dependence decreased at a rate of −31.53%.

The process of reshoring services observed since 2008 takes place in a context that Baldwin and Taglioni (2009) described as “the great trade collapse,” in which world trade flows suffered an unexpected and large-scale collapse, registering the sharpest drop since the Great Depression.

However, since 2010, after the first years of the Great Recession, Spanish service companies have slightly increased their contracting of foreign services per unit of output, adopting new services offshoring strategies, although to a lesser extent than in the period prior to the recession. The contracting of foreign services per unit of output grew between 2010 and 2015 at an average annual rate of 4.22%, with most of this increase corresponding to intra-sectoral services, those that were most affected by the previous reshoring strategy (Figure 2). Despite the recovery of offshoring strategies, the level of dependence on imported intermediate services per production unit in 2015 is lower than in 2008 (Table 2).

Although data are not yet available from the source used in this study to analyze the strategies followed by service companies in the context of the current health crisis, Baldwin and Tomiura (2020) and Baldwin (2020) argue that 2020 will show a much larger commercial collapse than that of the 2008 crisis, since the shock caused by COVID-19 has its origin in both a demand and supply shock, whereas the sharp crash of 2008 to 2009 was mainly driven by a demand shock. A major trade collapse, even larger than that of the previous crisis has taken place as a result of the containment policies adopted by governments to combat the pandemic, which have led to a drastic reduction in global production and consumption. Kejzar et al. (2022) find an overall decline of over 20% in trade between EU countries following the COVID-19 outbreak. Both supply and demand shocks are shown to contribute to this trade decline associated with COVID-19 in the origin and destination countries. This negative impact on world trade has also affected global value chains as well as companies’ strategies (Baldwin & Freeman, 2022; Chowdhury et al., 2021).

In the sectoral analysis, the incidence of services reshoring strategies carried out by Spanish services companies since the onset of the financial crisis are analyzed, differentiated by sectors.

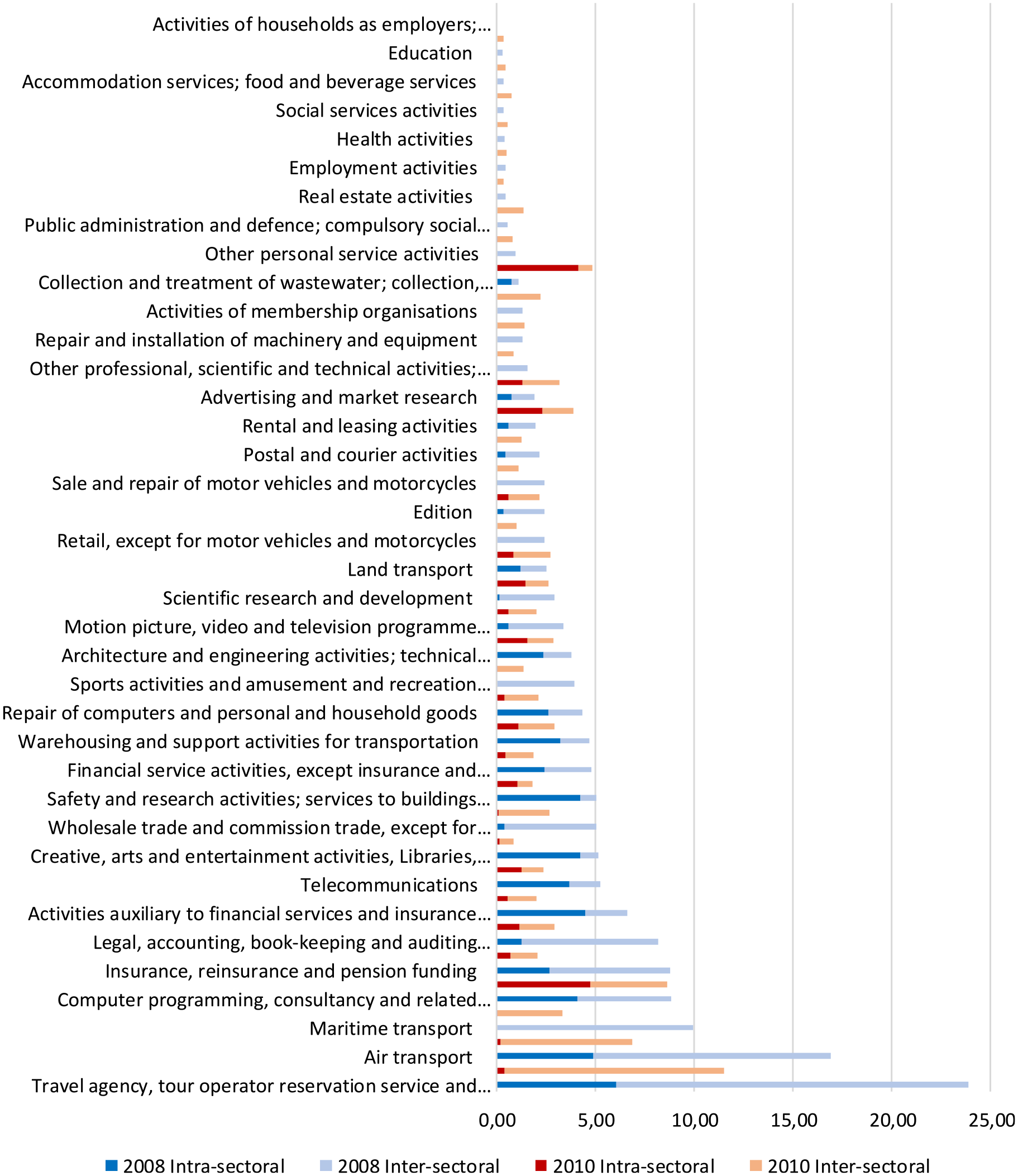

After a period of growth in the adoption of services offshoring strategies by Spanish service companies, in 2008 the sectors with the highest foreign service contracting per unit of output were travel agency services, air transport, and maritime transport. These were followed by computer programming and consultancy, insurance and pension plans, legal, accounting and auditing activities, and financial auxiliary services and insurance. These activities showed high rates of intra-sectoral offshoring, that is, a high dependence on foreign services from the same sector, with the exception of maritime transport, whose service imports correspond entirely to other sectors (Figure 3 and Table 3). A detailed study of the services offshoring in the Spanish economy for the 2000 to 2007 expansive period can be found in Fuster and Martínez (2013).

Intra- and inter-sectoral dependency indexes of imported intermediate services per unit of output.

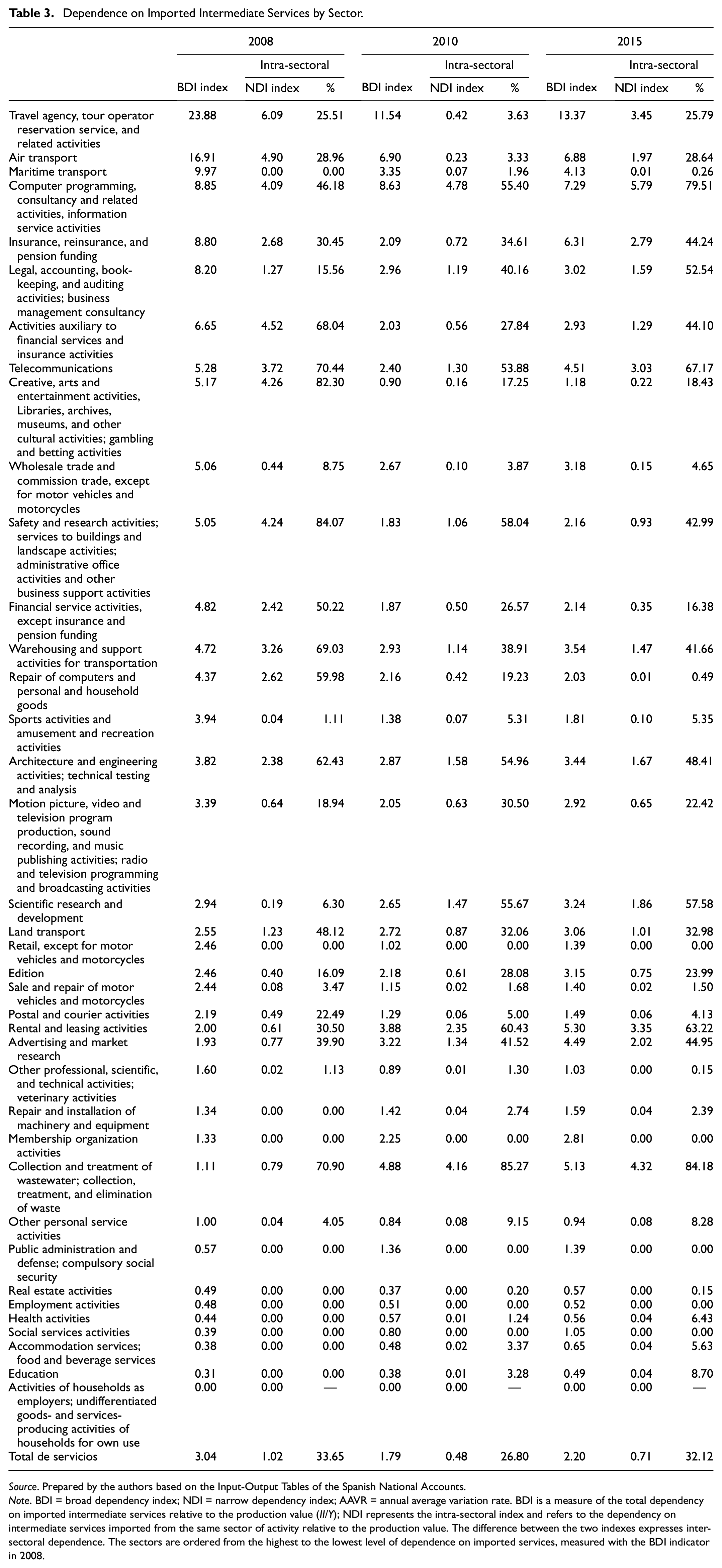

Dependence on Imported Intermediate Services by Sector.

Source. Prepared by the authors based on the Input-Output Tables of the Spanish National Accounts.

Note. BDI = broad dependency index; NDI = narrow dependency index; AAVR = annual average variation rate. BDI is a measure of the total dependency on imported intermediate services relative to the production value (II/Y); NDI represents the intra-sectoral index and refers to the dependency on intermediate services imported from the same sector of activity relative to the production value. The difference between the two indexes expresses inter-sectoral dependence. The sectors are ordered from the highest to the lowest level of dependence on imported services, measured with the BDI indicator in 2008.

Since 2008 there has been a reversal of the initial strategy of services offshoring in most service sectors, with part of the production of previously offshored services returning to Spain (Figure 4). Those activities that in 2008 showed a greater dependence on imported intermediate services are those that subsequently registered greater reshoring practices, both intra- and inter-sectoral. Computer programming and consultancy is an exception since, although fewer foreign services were contracted from other sectors, it increased the import of inputs from its own sector. Likewise, maritime transport and, to a lesser extent, legal, accounting and auditing activities show only inter-sectoral reshoring. However, there are sectors of activity that did not follow the general trend of reshoring, but rather continued to increase the contracting of services abroad per unit of output during the crisis. This is the case of collection and treatment of waste management, rental and leasing activities, advertising and market research, activities of membership organizations, public administration and defense activities, social services activities, land transport, health activities, accommodation services, food and drink, repair and installation of machinery and equipment; education; and employment activities (Figure 4).

Variation in the dependency index of imported intermediate services by sector, 2008 to 2010 (in percentage points).

The latest available data for 2015 reveal the existence of new services offshoring processes since 2010 in all sectors, with the only exceptions being computer programming and consultancy, repair of computers and personal and household goods, air transport, and health activities. These sectors show services reshoring processes which are entirely attributable to the inter-sectoral component, except for repair of computers and personal and household goods, in which case the decrease is attributable to inputs from the same sector of activity (Figure 5).

Variation in the dependency index of imported intermediate services by sector, 2010 to 2015 (in percentage points).

Effects of Service Reshoring on Employment in the Service Sector

This section empirically analyzes the possible effect of services reshoring on the level of employment in service sectors. As previously mentioned, one of the main arguments used by governments to defend and promote reshoring processes in their countries is the generation of employment implied by these strategies. However, this is a hypothesis for which there is still no confirmatory empirical or theorical evidence.

The limited empirical evidence available on the impacts of reshoring on employment, for the manufacturing sector (Krenz et al., 2021) and for the services sector (Fuster et al., 2020), shows that the employment generation expected from some governments does not always occur and, therefore, this assumption should be considered with caution.

In manufacturing industries, Krenz et al. (2021) analyze the impacts of reshoring on employment, in the particular case where the cause of reshoring is automation. Using a theoretical model in which the location decisions of firms’ intermediate inputs (materials or tasks) depend on the profits associated with production at home or abroad, an increase in automation at home encourages the substitution of low-skilled labor previously offshored in low-wage-cost countries by the use of robots at home, which implies the return of offshored production through the reshoring strategy. In this way, companies save on customs duties and other costs associated with manufacturing abroad. In this specific context of reshoring in manufacturing explained by automation, the employment effects obtained are different depending on the type of job qualification considered. No new low-skilled jobs are created, which are those that were lost with the previous offshoring processes, since this type of work is replaced by robots. Furthermore, it does increase the demand for high-skilled labor, which complements the automated processes. On the other hand, Fuster et al. (2020) study the impact of service reshoring on employment, both in manufacturing and service industries, finding that there are no significant impacts on employment.

In the case of services reshoring for the services sector, as mentioned above, there is no theoretical framework in the academic literature from which hypotheses on its impacts can be derived. Moreover, it is also difficult to formulate any intuitive hypotheses regarding these effects with the empirical evidence available in this sector on the causes that may be motivating them.

In offshoring processes, the causes always theoretically respond to the search for the localization of production with the lowest costs, which improves efficiency and, therefore, production and employment in the long term (Grossman & Rossi-Hansberg, 2006). However, the available studies on the causes of reshoring in services show that reshoring is not always carried out for efficiency reasons.

The sectoral data used in this study does not allow us to determine the reasons why companies adopt reshoring strategies. On the one hand, these decisions could respond to economic motivations to reduce costs and gain efficiency within a context of changes in the geographical distribution of comparative cost advantages between countries. On the other hand, these business strategies could respond to issues of a different nature, unrelated to efficiency, for example, those derived from the economic downturn that forced companies to dispense with foreign suppliers, even if they were more efficient. They could also be explained by geopolitical reasons or trade disputes, which would hinder economic relations between certain countries and prevent the continued provision of services from more efficient suppliers in those countries.

In the absence of a theoretical framework on the effects of reshoring of services, the possible intuitive hypotheses that may be formulated will depend on the causes that motivate it. In the case where reshoring is carried out for efficiency-related reasons, the positive results achieved with this strategy could also generate a positive impact on employment, at least in certain types of jobs depending on their skill level. However, it is possible that the reshoring strategy does not respond to efficiency reasons, but rather to political reasons or to unforeseen obstacles that were not present in the previous offshoring decisions and that prevent or hinder the continuity of this strategy. In this case, the effects on employment should intuitively be negative, since, theoretically, a reduction in efficiency leads to a reduction in activity and, therefore, in employment.

For these reasons, in this section we study whether the process of services reshoring that took place during the period 2008 to 2010 has generated employment or not, without any assumptions about possible outcomes. Likewise, the analysis differentiates between the effect of services reshoring on employment in the same sector of activity and in other service sectors.

As in previous studies analyzing the effects of offshoring/reshoring strategies on employment (Agnese, 2012; Amiti & Wei, 2005, 2006, 2009; Fuster et al., 2019; Michel & Rycx, 2012; Winkler, 2010; Wrigth, 2014 for the case of offshoring, and Fuster et al., 2020 for the case of reshoring), a log-linear labor demand function is derived from a homogeneous production function with constant returns to scale (CRS) (Hamermesh, 1993). In addition, the dependence of imported service inputs on total output is included as an explanatory variable. In the previously cited papers, this variable is measured with the ratio of imported inputs to total inputs used (domestic plus imported), in some cases, and to total output, in others. The estimation of its coefficient is carried out with panel data for the reshoring period 2008 to 2010 with the following equation:

i = 1…n, where n is the number of service sectors; j = 1…k, where k is the number of periods analyzed; Lij = total employment in logarithms; Yij = value of production in logarithms; wi = average wage in logarithms; DIij = dependence on imported services per unit of output yeij; vij = random disturbance.

According to economic theory, the estimated value of coefficient β1, output-employment elasticity, should have a positive sign, and coefficient β2, wage-employment elasticity, should have a negative sign. This is because an increase in production has a positive effect on the level of employment and an increase in wages has the opposite effect.

With respect to the coefficient of interest, β3, a positive and significant sign of this coefficient would indicate that a lower dependence on imported inputs per unit of output causes a reduction in employment in the country of origin, while a negative and significant sign would indicate that a lower dependence on foreign inputs per unit of output implies an increase in employment.

Using equation (1), a fixed effects panel model and a random effects panel model are performed for all service sectors to determine whether or not there is an effect on employment in the period 2008 to 2010 using three estimations:

Labor demand function in which broad or total reshoring (BDI), measured as the ratio of total imported inputs to the value of output, is included as a regressor.

Labor demand function in which the narrow or intra-sectoral reshoring (NDI), measured as the proportion of imported inputs of the same sector of activity over the value of production, is included as a regressor.

Labor demand function in which inter-sectoral reshoring (IDI), measured as the proportion of inputs imported from other service sectors over the value of production, is included as a regressor.

The results of these estimates are presented in Table 4.

Labor Demand in Services.

Source. Author’s own elaboration based on data from the Input-Output Tables (INE) and calculation of the respective.

Note. Panel Data 2008 to 2010. Robust errors in parentheses. The dependent variable is employment in services in logarithms.

p < .01.

In addition, several tests have been carried out to determine, on the one hand, whether the panel model with both fixed and random effects is better than the pooled model. The F-test with the fixed effects model proves to be better than the cross-sectional OLS for the pooled data. The Lagrange multiplier test, Breusch and Pagan’s (1980) test for random effects, also indicates that the random effects method is preferable to the pooled (OLS).

On the other hand, the null hypothesis of homoscedasticity was tested with the Wald test. The result indicates that it should be rejected, that is, heteroscedasticity was found in the model. Therefore, the panel model with robust errors in heteroscedasticity is estimated.

After determining that the panel model is better, in order to know whether to consider the fixed effects or the random effects model, we must perform the Hausman test. Hausman (1978) showed that the difference between the random effects and fixed effects coefficients can be used to test the null hypothesis that the explanatory variables of the model and the ei are not correlated. The null hypothesis of the Hausman test is that the fixed and random effects estimators do not differ substantially. If we accept it, as in our case, the best model for estimation is the random effects model, which is a consistent and efficient model.

The elasticities obtained, production-employment (β1) and wages-employment (β2), are practically the same in the three estimates made and include the expected signs.

As explained in the previous section, in the estimated period, 2008 to 2010, there is a process of services reshoring, as the dependence on imported intermediate services as a proportion of total production is reduced.

The results obtained for the random effects model show that in all cases the effect of reshoring, β3, is very small, negative, and not significant with respect to the level of employment in services. Therefore, it can be seen that an increase in employment is not being generated the country performing services reshoring. This result holds for both broad reshoring and for all its components, narrow (intra-sectoral) and inter-sectoral. In other words, the return of previously offshored services to the country of origin has not led to an increase in sectoral employment levels.

It should be borne in mind that in Spain, the 2008 crisis led to a sharp decline in employment, resulting in a significant increase in the unemployment rate, which more than doubled from 8.23% in 2007 to 19.86% in 2010. The offshoring reversal strategy analyzed in this paper coincides with the onset of the economic crisis in a context of collapsing international trade. In this context, it may well be that the job losses resulting from the economic recession have been absorbed by the potential generation of new jobs due to the return of some previously offshored services. Consequently, this temporal coincidence in the occurrence of the two phenomena, with possible opposing effects on employment, could mask the impact of reshoring in isolation.

Another explanation for the result obtained could reside in the possible causes that motivated the reshoring processes during the period of economic contraction. If that context of crisis had forced some industries to do without foreign suppliers, for example, because the reduction of their activity and size was not conducive to it (Martínez-Mora & Merino, 2014), then the substitution of foreign suppliers with probably less efficient domestic production would not help to improve competitiveness or activity and, therefore, neither would employment.

And, finally, if the reasons behind the reshoring processes were related to the search for efficiency, the results would not necessarily be very different from those obtained. For example, a substitution of foreign suppliers with domestic suppliers as a result of advances in information and communication technologies (ICT) and artificial intelligence, which would make it possible to improve the management of some activities in service industries, would not be expected to increase employment to any great extent. In line with the results of Krenzet al. (2021), jobs in professions related to computer engineering and artificial intelligence could be expected to increase, but low-skilled jobs that could be eliminated due to the use of new technologies could also decrease, which could lead to zero net effects on job creation.

Conclusions and Discussion

The Great Recession decelerated the advance of the offshoring strategy, which had become widespread since the 1990s. This gave rise to the process known as reshoring, consisting in the return of previously offshored goods and tasks to the countries of origin. Given the few existing studies in the specialized literature on the reshoring of services, this paper analyzes this strategy in depth and its implications for employment in the services sector for the Spanish economy.

The value of this work is evident in that it represents an advance in the study of services reshoring, since, for the first time, this strategy is analyzed only for the services branches. In addition, it differentiates between total, intra-sector and inter-sector reshoring. In other words, it studies not only whether the dependence of service industries on imported intermediate services is reduced, but also expands this analysis by determining in which activities foreign dependency is reduced, in activities within the same branch or in other branches of activity. It also contributes new evidence to the economic literature on the effects of services reshoring on employment in the services sector of the countries whose companies carry out this strategy.

The empirical analysis shows that Great Recession has led to a reversal of the services offshoring strategy that Spanish service companies had carried out between 2000 and 2007. Thus, since 2008 there has been a partial return to the production of previously offshored services, which is reflected in a notable reduction in the contracting of foreign services per unit of output, especially of an intra-sectoral nature. Although a slight increase in dependence on imported services is subsequently observed, the pre-crisis level has not been reached.

The sectoral analysis reveals that the sectors with the highest dependence on foreign services per unit of output in 2008 (travel agency activities, air transport and maritime transport, computer programming and consultancy, insurance and pension plans, legal, accounting and auditing activities, and financial auxiliary services and insurance) were those that recorded the highest reshoring practices during the crisis, both intra-sectoral and inter-sectoral. It should be noted that computer programming and consultancy, maritime transport, and legal, accounting and auditing activities show reshoring of a cross-sectoral nature, although not of activities in the same sector. Nevertheless, some sectors of activity continued to increase during the crisis in terms of foreign service contracts per unit of output (collection and treatment of waste management, rental and leasing activities, advertising and market research, membership organization activities, public administration and defense activities, social services activities, land transport, health activities, accommodation services, food and drink, repair and installation of machinery and equipment, education, and employment activities).

In the analysis of the effect of services reshoring on services employment, a random-effects panel data model has been estimated and found to be consistent and efficient. Three estimations have been made, for total, intra-sectoral and inter-sectoral reshoring, and the results obtained show that the coefficients of the indexes studied are not significant in any of the estimations. On the one hand, this result coincides with that obtained in Fuster et al. (2020), the latter using a different model, OLS (ordinary least squares), and estimating the impact on employment only for total reshoring, without differentiating by components. On the other hand, Krenz et al. (2021) find that reshoring has a positive impact on skilled employment, being non-significant for unskilled employment. However, in Krenz et al. (2021) the analytical framework differs since the impact of manufacturing reshoring on manufacturing employment is analyzed when the reshoring is motivated by automation.

Therefore, it can be concluded that services reshoring, in those years of economic crisis, has not generated employment in the Spanish service sector, which may have been due to it coinciding with a severe economic crisis that generated significant job losses, which could be masking possible increases in employment caused by reshoring. Likewise, another possible explanation could be derived from some of the causes recently detected in the literature (Krenz et al., 2021), such as the the automatization of production processes and the application of new technologies in the country undertaking services reshoring, which would not foreseeably lead to increases in employment in that country.

These results show that the political voices that associate reshoring processes with employment generation should be considered with caution, at least for the time being, since the scarce empirical evidence available in the economic literature does not support these hypotheses. Therefore, we believe that new studies and empirical evidence are required to analyze this phenomenon in greater depth.

In this study, the main limitation lies in the period of analysis. With the information currently available, it is not possible to analyze this strategy with input output data from the Spanish National Accounts for years after 2015.

We propose future lines of research to gain a deeper understanding of reshoring strategies. On the one hand, it is necessary to extend the period of analysis with sectoral data to be able to evaluate the influence that relevant events, such as the pandemic and the war in Ukraine, have had on these strategies. It would also be interesting to deepen our knowledge of the causes of reshoring of services with company data. For example, it would be interesting to analyze the effect of information and communication technologies (ICT) and new innovation processes, or the increase in human capital in companies that return their intermediate tasks to the country of origin. This would help us to better understand the magnitude and causes of reshoring strategies, as well as their impact on the level of employment.

Footnotes

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.