Abstract

Studies illustrate progress in financial technology in Pakistan; nevertheless, the uncertain obstacle that prevents clients from adopting financial technology remains unclear. The research on the perceived risk, particularly in using financial technology in Pakistan, is limited. Therefore, this research bridges this gap. Two hundred ten members partook in this exploration. We have used the structural equation modeling approach to probe the acquired information and hypothesis. Empirical results show that three of eight perceived risk factors: performance risk, financial risk, and overall risk, have a substantial adverse effect on the intention to utilize financial technology. The highest impact was performance risk, followed by financial risk and overall risk. Whereas the other five risks: social risk, time risk, security risk, legal risk, and psychological risk, statistically have no substantial adverse effect on intent to utilize financial technology. The outcomes help experts better conceptualize and diminish hazard boundaries in planning for the disturbance of financial technology (fintech). Experts are likewise encouraged to focus on fintech’s operational aptitudes and utilitarian framework execution in fintech administrations.

Introduction

The fusion of “finance” and “technology” in the form of fintech has recently generated significant excitement and attention (Arner et al., 2015). EY alludes that fintech is “an organization that combines innovative business models and technologies to realize, enhance, and disrupt financial services” (EY, 2019). From a broader standpoint, fintech refers to institutes that provide solutions for financial software to their clientele. Fintech companies are categorized into various classes: insurance, investment, management, trade services, governance technology, and incentive program. The global adoption rate of fintech has exceeded expectations in 2019 (EY, 2019; C. Li et al., 2023).

Fintech businesses have given the financial industry a considerable boost in recent years. A recent World Bank study shows that fintech companies operate in over 189 countries globally (Adrian & Pazarbasioglu, 2019). Many financial institutions benefit from collaborating with fintech businesses, such as operational cost savings, reduced client costs, and speedier service, all of which contribute to improved market value and financial performance. Given these benefits, numerous financial professionals and academics have identified certain hazards linked with fintech businesses due to their activities (Magee, 2011; Serrano-Cinca et al., 2015). The International Monetary Fund (IMF), for example, has listed data privacy, cybersecurity, and difficulties inside fintech businesses as concerns. According to reports, nearly 79% of fintech organizations are exposed to cyber-security threats (Adrian & Pazarbasioglu, 2019). Furthermore, the Financial Stability Board (FSB) identified a crucial danger in the fintech business, exacerbating stock volatility, and leading to a financial catastrophe.

Concurrently, the global reach of fintech knowledge is remarkably high, with 89% of payments being made through computers or smartphones devices, and services related to non-bank money transfers and peer-to-peer payment systems accounting for 82% (EY, 2019). Moreover, several studies have been conducted to probe the determinants influencing virtual transactions. But there is no work on the restraints and risk determinants that frustrate users’ aim to utilize fintech (C. Li et al., 2023; Y. H. Li & Huang, 2009). Thus, it is crucial to explore the perceived risk components that influence the expectations of Pakistani customers regarding fintech.

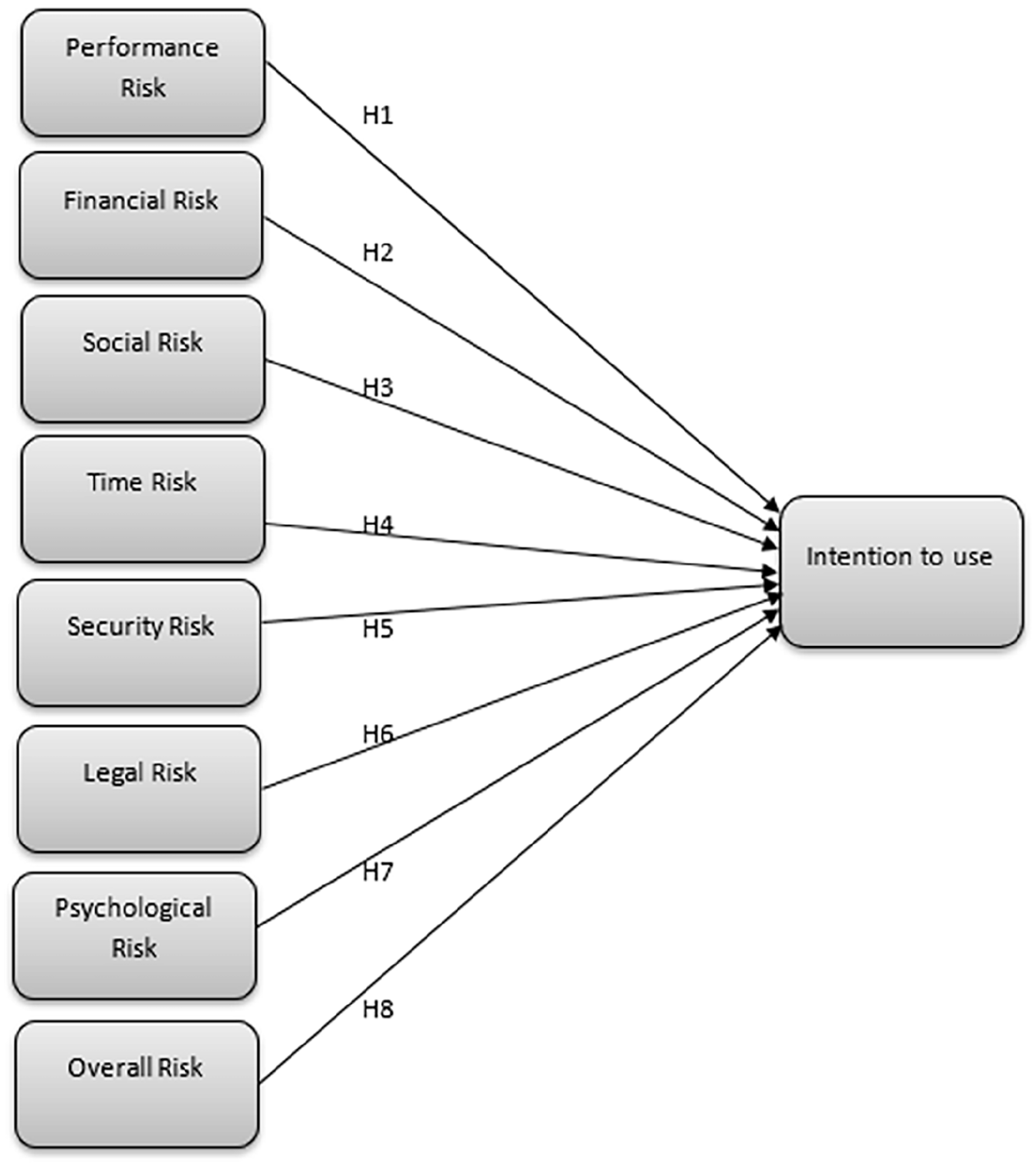

We created our first research question based on these viewpoints; fintech users may face a larger risk in terms of performance risk, financial risk, social risk, time risk, security risk, legal risk, psychological risk, and overall risk.

Financial Technology in Pakistan

Pakistan is a cash-based economy with the world’s sixth most populated nation. A lack of access to capital has long hampered Pakistan’s economy (World Bank, 2017). According to the report, 93% of the grown-up populace doesn’t have bank accounts (Rizvi et al., 2017). Pakistan has a lower economic inclusion position than regional and worldwide norms (Nenova & Niang, 2009). Small and medium-sized businesses lack finance because of high intermediary costs, large loan charge splits, financial illiteracy, strict security requirements, and restricted loaning rates (Lukonga, 2021). This higher rate of financial restrictions makes people and organizations defenseless against pay stun and expands their working expenses such as operational expenses and hoses forecasts. Technology can be bridled to expand the topographical effort. Physical access to finance may be considerably enhanced by innovative mechanical arrangements such as branchless banking and mobile banking (Kemal, 2016). Collaboration and good relations among banking institutions and informal vendors might enable their administrations’ services and operations to be topographically accessible, not so much perplexing, but relatively more effectively reasonable for buyers (Ali & Abdullah, 2020). Pakistani buyers’ overall judgment concerning the insignificance of formal money in their daily lives, troublesome financial systems, low effort, and not admissible items give a chance to fintech to configure customized items. Microfinance Institutions (MFIs) in Pakistan are confronted with more noteworthy subsidizing to develop and incorporate with monetary business sectors; however, they have tremendous ability to grow outreach. New businesses’ technology utilization and associations with financial technology will permit these institutions to boost outreach. The financial industry’s current shortcomings can fill in as a chance for virtual monetary institutions to provide answers for effort.

Compared to less advanced countries, the financial system in developed countries is more accessible. According to Kendall et al. (2010), 81% of individuals in industrialized nations have official bank accounts, but just 28% of persons in developing countries have one. According to Demirgüç-Kunt and Klapper (2013), seven countries, including the Philippines, China, Bangladesh, Pakistan, Vietnam, India, and Indonesia, account for almost 92% of the 1.5 billion unbanked individuals in growing economies in developing Asia.

Financial Technology Regulations in Pakistan

In reality, Pakistan’s State Bank has shown itself as a digital financial leader. The state bank’s efforts to encourage electronic and branchless banking (such as mobile payments) have been meticulously recorded. One research looks at the past and frameworks of online banking to see how far the sector has developed and changed the country’s traditional banking systems in Pakistan (Rizvi et al., 2017). In 2008, the State Bank of Pakistan (SBP) supported the branchless banking sector by issuing branchless banking laws and developing a regulatory mechanism strategy. Since 2008, the SBP and other government agencies have promoted banking technology. The creation and enactment of laws of PSPs (Payment Service Providers) and PSOs (Payment System Operators) in 2014 were the most relevant and clear actions taken by SBP to support and facilitate fintech (PSPs, 2014). The SBP enacted Laws for Mobile Banking Interoperability4 in May 2016. Fintechs should achieve long-awaited Transactional Interoperability under these rules, allowing users to transfer payments across mobile accounts and service providers. The other form of interoperability, Account-to-Account Interoperability (A2A Interoperability), has been available to consumers and Fintech service providers since 2014.

This study differs from the other studies, such as more latest studies have identified various variables that determine fintech adoption. Only a little research has been done on the limitations and risks that deter customers from using fintech. As a result, it’s critical to look at the risk perception variables that influence Pakistani customers’ willingness to utilize fintech. Most of the current fintech literature in Pakistan is based on the technology acceptance model (TAM). Yet, no one has thoroughly investigated the perceived risk variables. Agha and Saeed (2015) used TAM and included one social risk factor to know the customers’ acceptance of the technology. We characterize perceived risk in fintech applications or transactions such as online banking as the emotionally decided assumption of a loss while reviewing given online transactions. This paper has examined risk factors with respect to payment applications for the online transfer of money in Pakistan. Data is collected from highly educated, literate consumers with financial literacy, and we used a direct impact of risk facets on the intentions to use fintech. The proposed model is not used before with respect to fintech usage in Pakistan.

On the other hand, establishing a risk-free fintech transaction environment is much more complicated than providing client privileges. Consequently, fintech companies must seek a risk-reduction strategy to gain greater trust in potential customers. Surprisingly, our findings vary from those of the other researchers. Second, providing professionals with a better knowledge of consumers’ risk perceptions is vital. It can then be utilized to develop risk-reduction methods and trust-building processes to improve and promote users’ online trade adoption, particularly in the growing field of online payments. Third, regulating the associated risk aspects broadens the study area of economic repercussions based on fintech use. In short, it is critical to grasp the effect of risk variables on the adoption of fintech by Pakistan’s whole public.

The following are the objectives of this research:

To see whether perceived risk elements affect consumers’ intentions to utilize fintech.

To determine which elements have a more significant impact on the intention to utilize fintech and are associated with risk.

To determine if PRT plays a vital role in investigating fintech uptake in Pakistan.

The remainder of the paper is organized as follows: Section 2 covers related research in the conceptual framework and presents the hypothesis; Section 3 explains the methodology, Section 4 results; Section 5 contains the discussion of the results, implications, limitations, and future studies, and Section 6 includes a conclusion.

Conceptual Framework

Fintech isn’t merely restricted to monetary services. It includes financing, making new plans, and designing business models (P2P lending and crowdsourcing). It also performs business tasks, offers assistance, and conveys items as an option compared to conventional financial sectors. (Arner et al., 2015; Puschmann, 2017). By and large, fintech, in general, is a novel and troublesome technical service offered by present-day nonfinancial establishments (D. K. C. Lee & Teo, 2015). Fintech also alludes to utilizing IT, such as mobile technologies, data analytics, and cloud technology, to boost services and management efficiency and extend financial assistance (Hu et al., 2019; Y. H. Li & Huang, 2009). This way, fintech can be considered an innovation that enhances consumers’ experience and competitiveness in financial services. Fintech is characterized as the technology innovation of financial operations and services by non-monetary ventures. Fintech assists clients in partaking in an assortment of portable climate administrations. The vast advantages of fintech give consumers a chance to acquire a climate of enhancement and straightforwardness, diminish costs, make financial data more open, and eliminate intermediaries.

From the customer’s perspective, the aim to utilize it is still questionable and unsure, even though fintech has pulled in much consideration. It is accepted that a more pessimistic individual will negatively influence such conduct (Ryu, 2018; Singh et al., 2020). Buyers might be hesitant to utilize fintech fundamentally because the risks are considerable and cannot be ignored (Liao et al., 2010). These unexpected risks of fintech usage can hurt clients, impeding their utilization. Along these lines, this has prompted this research on the consumer’s perceived risk aspects of fintech utilization. The theory of reasoned action (TRA) concerning behavior or intentions, and the perceived risk theory (PRT) concerning risk, play a vital role in technology adoption.

Theory of Reasoned Action

Fintech usage intent is constrained by fintech users’ attitudes toward using fintech, which is attained by employing the theory of reasoned action (TRA) in the fintech ecosystem. It is accepted that consumers will be indulged in considering accessible services and selecting services (Kim et al., 2008; Roh et al., 2023; Rossmann, 2021). As buyers might be hesitant to utilize fintech because of danger contemplations, it is vital to comprehend the perceived risk facets when creating and advancing the utilization of fintech. Subjective norms and the actual use of the fintech is not included in this study as this study only focuses on the risk facets and their impact on consumers’ intention to use.

Perceived Risk Theory

Cox (1967), as referred to by Ryu (2018) and Mitchell (1999), explains perceived risk as the inevitable sensation when the outcome is very unfavorable. Perceived risk influences individuals’ trust and confidence in their choices. In prior consumer research studies, perceived risk was characterized as the apparent vulnerability or uncertainty in a buy circumstance. Perceived risk has been utilized to clarify and comprehend consumer behavior. Bauer (1960), as referred to by Quintal et al. (2006), presented perceived risk and considered it the impact that led to the total perceived value of buying behavior.

Cox (1967), as referred to by Ryu (2018) and Mitchell (1999), alludes to perceived risk as the inevitable sensation if the outcome is very unfavorable. Perceived risk is a sort of subjective predicted loss. According to Featherman and Pavlou (2003), perceived risk is the possibility of loss while seeking the desired result. Cox (1967) noticed that perceived risk comprised the extent of the possible loss (e.g., at stake) if the demonstration’s aftereffects weren’t positive; and the individual’s personal feelings of certainty that the results would not be proper. In traditional consumer decision-making, promising research has analyzed the effect of Risk (Lin, 2008).

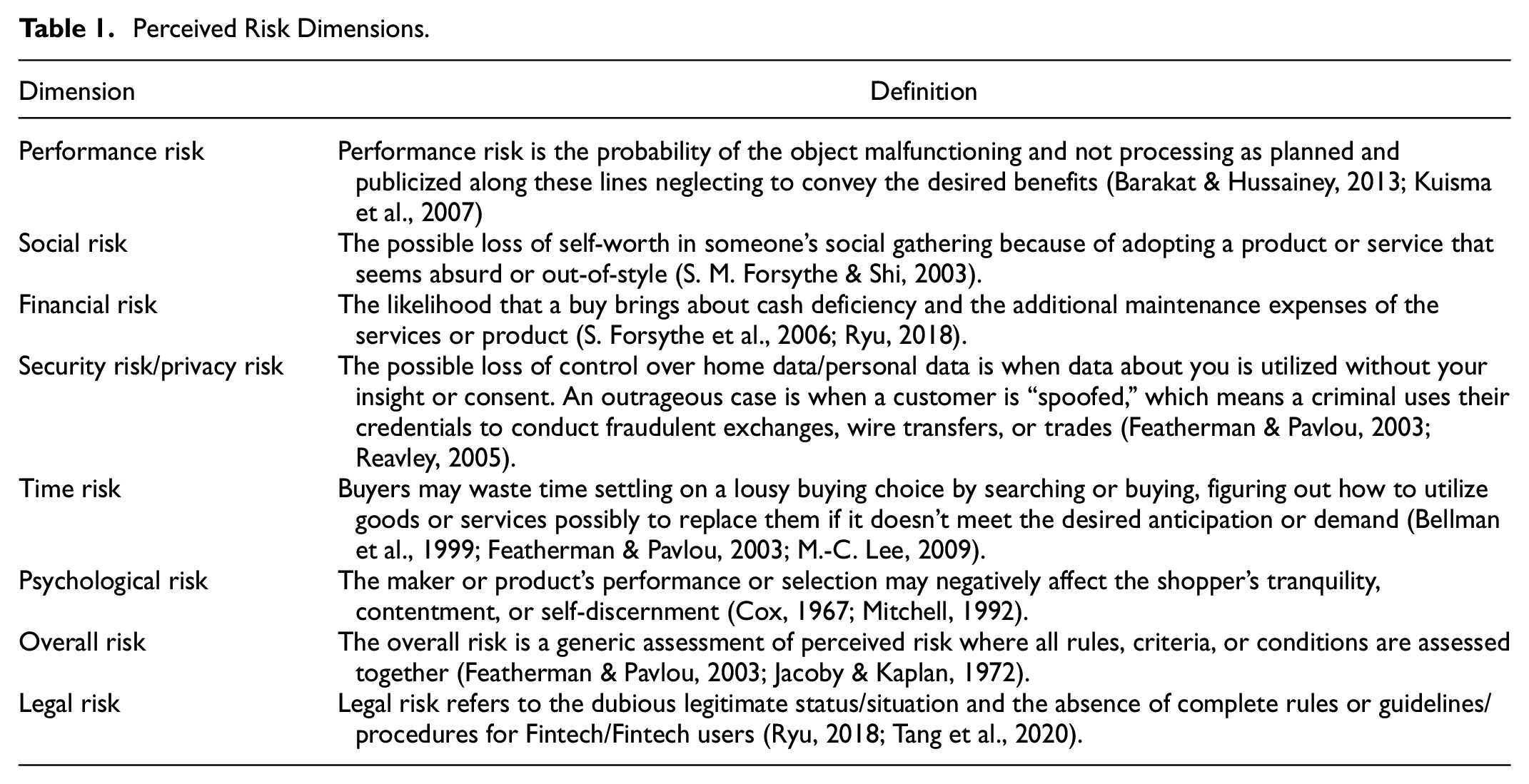

Many scholars asserted that users’ perceived risk is a multi-dimensional construct. In any case, perceived risk components may change per the product class (Featherman & Pavlou, 2003). Ryu (2018) indicated six perceived risk dimensions: financial, time or opportunity, social, performance, psychological, and safety. According to Luo et al. (2010), financial, performance, psychological, time, privacy, social, and overall risk are the main risk elements in the wireless Internet’s early adoption phase. Web-based banking doesn’t endanger human existence; therefore, the physical risk was excluded from this study. The components of perceived risks are characterized in Table 1.

Perceived Risk Dimensions.

Fintech Risk Perception

There are various definitions of perceived risk. In the data framework setting, perceived risk negatively affects the adoption of the information system or information technology (Ryu, 2018). Ryu (2018) alludes that perceived risk relates to services or products in utilizing technological innovation. Perceived risk is characterized as “customers’ impression of weakness, vulnerability and the possible negative outcomes related to fintech.” Given Ryu (2018) measurement of perceived risk and the fintech setting, the study distinguished seven components of perceived risk. They are financial risk, privacy/security risk, operational risk, legal risk, social risk, psychological risk, time/convenience, and overall risk, which may influence buyers’ fintech reception expectations (see Fig.1) are described as follows:

Performance Risk/Operation Risk

Operational risk alludes to misfortunes caused by inadequacies or breakdowns of web-based financial sites such as online banking (Barakat & Hussainey, 2013). Featherman and Pavlou (2003) observed frequent site failure and disconnection recurrence restraining electronic-services assessment. Luo et al. (2010) characterized operational risk as a performance risk. Users won’t intend to utilize financial technology because of the high-risk possibility of operation and financial system of fintech organizations. The absence of operational and quick reaction capabilities, structural problems, and a weak or a lack of internal procedure will prompt users’ doubt and frustration (Dvorský et al., 2018; Oláh et al., 2017). This will hinder intentions from utilizing fintech. Hence, this investigation hypothesizes that operational risk negatively affects the use of fintech. Therefore, it follows that:

H1: Performance risk negatively affects intention to use fintech.

Financial Risk

Financial risk alludes to the chance of monetary losses in monetary transactions, such as financial transactions led by fintech (S. Forsythe et al., 2006; Gai et al., 2018). It is possible for money-related misfortune because of transaction errors, exchange mistakes, or account misuse. Previous data systems research has demonstrated that perceived FR is the main factor embraced by cell phones and networks (Ryu, 2018). Ryu (2018) clarified that fintech’s monetary misfortunes are the danger posed by the monetary exchange framework, money distortion, moral threat, misrepresentation, and the risk of extra trade charges related to a preferred value. These financial risk factors adversely influenced the aim to utilize fintech. Previous studies state monetary dangers have expanded and incorporated the chance of the reoccurrence of economic misfortunes in financial services because of misrepresentation (Luo et al., 2010; Najaf et al., 2021). In this manner, financial risk negatively affects fintech use intents.

H2: Financial risk negatively affects intention to use fintech.

Social Risk

Social risk is a negative self-image when buying or utilizing specific services or products that a particular portion of society considers unsuitable (S. M. Forsythe & Shi, 2003). It insinuates the probability that using financial technology may bring about dissatisfaction with one’s companions, family, or workmates (Franks et al., 2014). Individuals likely have different perspectives toward financial technologies, such as online banking, influencing their views on its adopters. Social buzz and contribution behavior are essential for interaction with any online platform (Thies et al., 2014). On the other hand, not adopting web-based banking may negatively or positively affect social status. In line with technology acceptance research, Davis (1989), Fishbein and Ajzen (1975) concern the assessment and opinion of referents (companions, family, colleagues) to one’s activities as subjective norms. Given these studies, it’s sensible to believe that social risk could have a negative impact on consumers’ attitudes to fintech use. Subsequently, it follows that:

H3: Social risk negatively affects intention to use fintech.

Time Risk

Time risk refers to the extra time used and difficulty or inconvenience brought about by the deferrals of payment or some other trouble of route (finding suitable services or hyperlinks). There are two driving causes for disappointing online experiences that might be considered a time risk: unorganized or befuddling webpages that are too delayed when browsing (S. M. Forsythe & Shi, 2003). Bellman et al. (1999) provided that “harried” buyers were bound to shop online to save time. These time-conscious clients are likely to be wary of the risk of hitting time and are less likely to choose an e-service with high transition, installation, and upfront costs (Featherman & Pavlou, 2003). A time factor is not only a concern for an individual, but time risk has a more significant impact on the global financial market (Elsayed et al., 2020; Le et al., 2021). According to S. M. Forsythe and Shi (2003), time risk is a considerable obstruction to web-based buying, and it is thus hypothesized that:

H4: Time risk negatively affects intention to use fintech.

Security Risk

Security risk is defined as a danger that makes a situation, condition, or occasion riskier, such as demolition, revelation, alteration of information, refusal of service, misrepresentation, waste, and misuse (Macedo, 2018). It has been expressed in various studies that gaining consumers’ confidence in security and privacy problems would be a big hurdle for the online banking market (Degerli, 2019). Ryu (2018) contended that the utilization of fintech is generally accompanied by more considerable potential loss, for example, secrecy, individual data, and exchange. It likewise adds to the development of the perceived risk of fintech utilization. Accordingly, the Security risk is estimated to affect the utilization of fintech negatively. It is hence speculated that:

H5: Security risk negatively affects intention to use fintech.

Legal Risk

Legal risk refers to the dubious legitimate status/situation and the lack of regulations, standards, and procedures for fintech or fintech users (Tang et al., 2020). Fintech is novel in many markets globally; hence, the lack of regulations, guidelines, or procedures for consumers on fintech’s cash and security-related problems has led to dread, doubt, and anxiety among clients (Tang et al., 2020). Customers’ data, privacy, and the financial system’s protections are all examples of legal risk. In this regard, fintech businesses still operate in an unclear zone when determining if their operations need special permission or licenses from the appropriate authorities. Uncertainty about regulatory requirements is still dangerous for fintech companies (Ng & Kwok, 2017). Aside from regulatory uncertainty, fintech businesses are being forced to exit some markets due to the high cost of compliance. Besides the regulatory uncertainty, the considerable cost of compliance also forces fintech firms to withdraw from particular markets, ultimately affecting consumers’ intentions to use fintech. In this way, legal risk is estimated to affect fintech utilization intention negatively.

H6: Legal Risk has a negative effect on fintech use intention.

Psychological Risk

Psychological risk is the possibility that the brand or product’s quality, performance, or selection will negatively affect the shopper’s peace of mind, contentment, or self-perceptions (Mitchell, 1992). Cox (1967) defined psychological risk as the expected damage to self-esteem or ego from the disappointment of not accomplishing a purchasing objective. According to the survey, a psychological risk impacts the P2P lending market (Wang et al., 2022).

H7: Psychological risk negatively affects intention to use fintech.

Overall Risk

The overall risk is a generic assessment of perceived risk where all rules and parameters are assessed. End-user responses to an electronic service gateway design are often essential to understand since they can be interpreted as indicators of overall service quality. The seminal work of Bauer (1967) was used by Jacoby and Kaplan (1972) to derive a general metric of perceived risk. After a risk “tradeoff” behavior, he theorized it to be made up of many different types of risk. A large car, for example, can minimize physical/safety risks while increasing financial risk. This assessment of overall risk perception is also put to the test (Figure 1).

Proposed model.

H8: Overall risk negatively affects intention to use fintech.

Methodology

In this survey, Pakistanis were chosen as the responders, older than 18, and possessed personal bank accounts that meet the legitimate age of legally contractual capability. Respondents got self-managed questionnaires via a website (Google structure) with URLs messaged to them. Five Likert ratings were used to assess each construct, extending from 1 (strongly disagree) to 5 (strongly agree).

Sampling and Data Collection

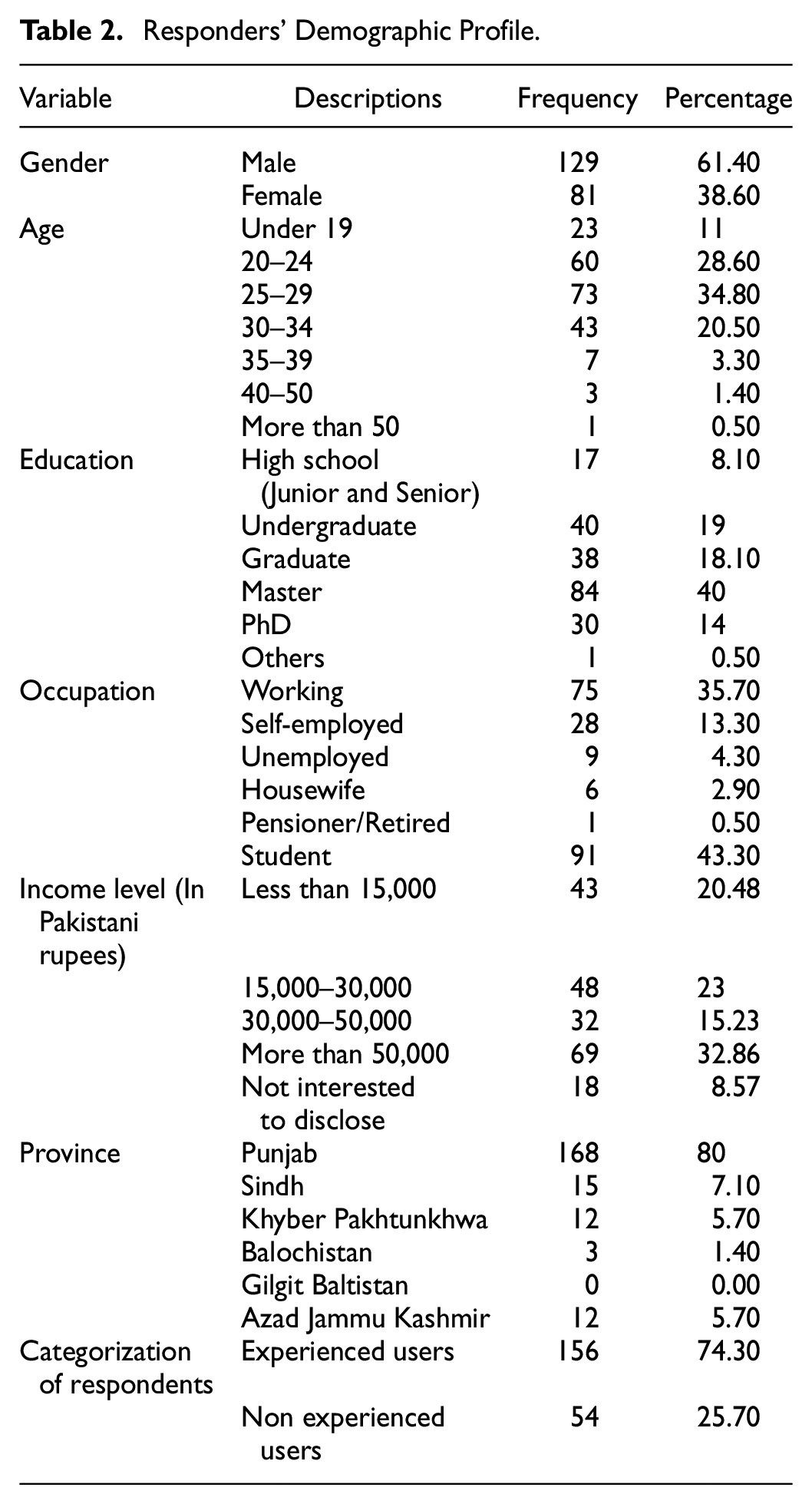

The sample responses were collected from 210 people with different backgrounds and conducted via an online survey for over 3 months between 1st February to 1st May 2021. The demographics of the responders are shown in the given Table 2. The proposed hypotheses were tested with all of the replies.

Responders’ Demographic Profile.

Table 2 shows that males constituted 61.40% of the collected data, while 38.60% were females. The majority of the responders, 34.80%, were people aged between 25 and 29. Regarding the respondents’ education, 40% were in the master category occupying the most positions in the survey. Furthermore, concerning respondents’ occupation, 43.30% were students, the highest percentage. About 32.86% had a higher income level than PKRs 50,000. In Pakistan, the majority of the population is from Punjab. From Table 2, we can also see that 80% are from Punjab. We found that 74.30% of respondents had fintech experience.

Measurement Development

The survey experiment was intended to incorporate a questionnaire having two parts, as shown in Appendix A, with nominal scales in the first part and five-point Likert scales in the second, extending from “strongly disagree” (1) to “strongly agree” (5). As a result, the first section is comprised of fundamental facts. This part of the questionnaire was developed to gather respondents’ descriptive information, such as gender, age, education, employment, and fintech experience.

The questionnaire’s second section was built around the ideas of performance risk, financial risk, social risk, time risk, security risk, legal risk, psychological risk, overall risk, and intention to utilize fintech. The performance risk and financial risk were operationalized by considering Featherman and Pavlou (2003) and M.-C. Lee (2009), containing 3 and 5 elements, respectively. The social risk scale was operationalized from Featherman and Pavlou (2003), M.-C. Lee (2009), and Wu and Chen (2005), containing two items. The assessment of security risk and time risk followed Featherman and Pavlou (2003), including three items for each. The measurement of legal risk was adopted from Ryu (2018), including six items. The psychological risk was taken from Cox (1967) assessment, including two items. The overall risk was formulated by considering Featherman and Pavlou (2003) and Jacoby and Kaplan (1972), including five items, and the intention was adopted from Cheng et al. (2006).

We conducted a pre-test to verify the instrument before performing the main survey. Ten people with more than 3 years of fintech expertise took part in the pre-test. Respondents were invited to give feedback on the instrument’s length, structure, and scale language. As a result, the instrument’s content validity has been established.

Results

We used Anderson and Gerbing (1988) two-step technique for assessing the data we obtained. We looked at the measurement model for convergent and discriminant validity first. The structural model was then investigated to determine the direction and strength of the connections between the constructs. This paper used the statistical structural equation modeling (SEM) approach to measure and analyze the relationships between observed and latent variables. Regression analyses are similar, but generally, SEM is more powerful. We may create complex path models with direct and indirect effects using SEM. Smart PLS-SEM has also provided more accurate results when evaluating validity and reliability.

Measurement Model Assessment

The assessment scores in Table 3 showed that each construct had a high level of internal reliability. The indicators’ computed coefficients were significant on their theorized underlying construct factors, used to determine convergent validity. The measuring scales were examined using the three criteria proposed by Fornell and Larcker (1981): all indicators’ factor loadings should be significant and more than 0.5. Construct reliabilities should be more than 0.8. The average variance extracted (AVE) for each construct should be greater than the variance attributable to measurement error (e.g., AVE should be more than 0.5).

Fornell-Larcker Criterion.

Note. Diagonal elements are the square root of AVE.

The construct reliabilities varied from 0.849 to 1.00 (see Figure 2). The AVE, which ranged from 0.594 to 1, was more significant than the variance due to the measurement error; as a result, all three convergent validity criteria were fulfilled.

Composite reliability.

Discriminant validity measures how different one idea and its indicators are from another idea (Bagozzi et al., 1991). In any two constructs, the correlations between items, according to Fornell and Larcker (1981), ought to be smaller than the square root of the average variance shared by items within a construct.

The square roots of the variance between a construct and its items were more extensive than the correlations between the construct and any construct in the analysis (Table 3), demonstrating discriminant validity defined by Fornell and Larcker (1981). All diagonal values surpassed the inter-construct correlations. Consequently, we determined that our instrument had enough construct validity.

Internal Consistency Reliability and Convergent Validity

Figure 2 shows the composite reliability (CR) is greater than 0.70. Figure 3 shows the average variance extracted (AVE) is higher than 0.5. Figure 4 shows that all constructs and indicators follow the reflective measurement criteria, that is, all indicators’ loadings are higher than 0.7, except for one indicator, FR3, which has a loading of 0.665, which is very close to 0.7. Finally, the findings indicate that all indicators are accurate, convergence validity is ensured, and the internal consistency of the data is obtained.

Average variance extract.

Results of structural equation model.

Discriminant Validity

Fornell and Larcker (1981) allude, in the model, the loading of own constructs should be greater than those of other constructs to achieve discriminant validity. In Table 3, all constructs fulfill this criterion. The results of the discriminant analysis method that compares cross loads between structures are provided in Appendix B.

The discriminant validity results are tested using the Heterotrait-Monotrait (HTMT) correlation criteria shown in Table 4. All obtained values meet the HTMT 1 criterion (Palacios et al., 2011), confirming discriminant validity.

Heterotrait-Monotrait Ratio (HTMT).

Structural Model Assessment

This paper used a bootstrapping procedure with 5,000 sub-samples to assess the structural model and validate the stated assumptions. The structural model is assessed concerning the estimates and hypothesis tests regarding the causal relations among variables specified in the path diagram (Figure 4).

Collinearity

Correlations among constructs are relatively robust, ranging from .7 to 1, shown in Table 3. The possible multicollinearity issue can be formally examined in the regression analysis framework. A typical metric of multicollinearity in regression analysis is the variance inflation factor (VIF), which measures the degree to which one predictor variable is described by other predictor variables (Hair et al., 1998). It’s typical to recommend a threshold VIF of less than or equal to 10 (i.e., tolerance > 0.1) (Hair et al., 1998). We used Smart PLS 3 in our study, and the AVE values are less than 10. Table 5 shows the VIF values of all constructs in the model. The results show that the VIF values of all constructs are less than 5, demonstrating that the structural model has no collinearity issues.

Inner VIF Values.

Assess Path Coefficient

The path coefficient was examined using a bootstrapping procedure with 5,000 subsamples. Table 6 summarizes the testing results of the hypothesis, indicating that performance risk (H1), financial risk (2), and overall risk (H8) are all adversely associated with using fintech. Meanwhile, the associations between social risk (H3), time risk (H4), security risk (H5), legal risk (H6), and psychological risk were discovered to be insignificant in the given relationship.

Hypothesis Testing.

p-Value statistics values (*p < .1. **p < .05. ***p < .01).

Impact of Risk Factors

According to the findings, overall risk, financial risk, and performance risk are all adversely connected to utilizing fintech. In other words, Pakistanis’ user of fintech is hampered by performance risk, financial risk, and overall risk. Performance risk (β = −.157) is the greatest of the three risk categories, followed by financial risk (β = −.197) and overall risk (β = −.510).

According to H1, perceived risk (PR) is adversely associated with intention (IN). The value of H1 (β = −.157, t = 3.295, p = .001) indicates its relevance; hence H1 is supported.

H2 determines whether FR has a negative impact on IN. According to the findings, FR has a strong negative influence on IN to utilize fintech. As a result, H2 was supported (β = −.197, t β = 3.513, p = .000). This research is in line with Ryu (2018).

H3 determines whether Social risk (SR) negatively relates to IN. According to the findings, SR had no significant negative influence on IN (β = −.085, t = 1.589, p = .113). The results show that social risk has no impact on intention. As a result, H3 is not supported. Our study is also consistent with M.-C. Lee (2009).

H4 evaluates whether time risk (TR) is negatively related to IN. The results revealed that TR has no significant negative impact on IN (β = −.073, t = 1.201, p = .230). Consequently, H4 is not supported. Our results contradict the study of Featherman and Pavlou (2003), who researched that the time factor is one of the most influencing aspects in changing consumers’ intentions.

H5 determines whether Security risk (SSR) negatively relates to IN. According to the results, SSR had no significant negative impact on IN (β = .013, t = 0.268, p = .789). As a result, H5 isn’t supported. However, this conclusion is similar to the findings of M.-C. Lee (2009) research found that Malaysian consumers’ perceptions of electronic payment had no association with perceived security (Teoh et al., 2013). It may be shown by deploying stringent security mechanisms in network information transmission and fintech applications, such as digital signatures, encryption, and a double-check for verification. It reduces the perceived security risk as a significant deterrent to using fintech.

H6 states that legal risk (LR) negatively relates to IN. As (β = −.023, t = 0.439, p = .661), the data demonstrated that LR had no significant influence on IN. As a result, H6 isn’t supported. In the context of fintech, the legal risk relates to the legal position/status/situation of fintech, which is ambiguous and for which no general regulation exists. Relevant fintech regulatory and security concerns are assured before being executed regarding a legal risk.

H7 states that psychological risk (PPR) has a negative relationship with IN. According to the findings, PPR had no significant detrimental influence on IN (β = .004, t = 0.072, p = .942). As a result, H7 is rejected. Psychological risk had low path loadings for this sample and setting, which was less worry than performance-related risk variables. This study’s research findings matched Featherman and Pavlou (2003).

Finally, H8 states that overall risk (OR) has a negative relationship with IN. H8 is supported by its significant result (β = −.510, t = 8.339, p = .000). Table 6 summarizes the findings. Our findings are consistent with previous research (Featherman & Pavlou, 2003).

Discussions

The present study examines the elements that influence fintech usage intentions. This research proposes an integrated model for describing consumers’ intention to use fintech based specifically on PRT. Our study yielded several interesting findings reported in one category: negative predictors. The discriminant analysis results reveal factors that negatively affect consumers’ usage intention; performance risk is the greatest of factors, followed by financial risk and overall risk. This study’s results have many crucial implications for fintech practitioners and researchers.

According to the findings, PR has a significant negative influence on consumers’ intentions to embrace fintech. As a result, whether there are continuous transactions failure, unfinished or failed transactions/deals/processes, or a lack of operational expertise and solutions to fintech-related difficulties, the intention to utilize fintech decreases. As a result, lowering the risk of website failure may boost customers’ willingness to undertake transactions online. Our findings are in line with M.-C. Lee (2009) research.

This finding of H2 suggests that possible financial damages, such as fraudulent activities, the failure of trade frameworks, and monetary misrepresentation, impact customers’ willingness to utilize fintech. Financial risk is an important consideration when deciding whether or not to employ fintech. Economic activities will be secured when fintech service providers can offer solid systems and services and complete protection. Once consumers perceive financial risk, they are less prone to use fintech applications. Even damage or overcharging consumers will create a threat in their minds. That’s why fintech service providers should always pay attention to these monetary misrepresentations, such as hidden charges to buyers. Our study is in line with Ryu (2018).

The fact that social risk does not impact intention to use fintech demonstrates that consumers are unconcerned about internet banking’s cultural conditioning from their friends, family, or coworkers. One view is that fintech has already been widely used, and most respondents had positive experiences with it via friends or family. Another rationale is that using fintech is a personal choice rather than a requirement. This is in line with the results of M.-C. Lee (2009) also showed that social risk is insignificant. Our results have challenged the research of Agha and Saeed (2015), who found that social risk negatively affects the consumers’ acceptance of the technology as Pakistan has a collectivist culture. Pakistani culture is a collectivist culture where social values are on priority; still, the social risk is not found to have a negative effect on consumers’ usage intention in this study. This shows that trends are being changed. On the other hand, Venkatesh and Davis (2000) found that social risk has little impact on the consumers’ intentions. They found that social norms considerably influence intents to utilize in a mandatory-usage situation but have minimal impact in a voluntary-usage case. In the modern world, now the trend is being changed. Fintech users are more worried about fintech companies’ performances, not social issues.

In previous studies, time risk has been demonstrated to have a negative impact on the intention to use internet banking (S. M. Forsythe & Shi, 2003; M.-C. Lee, 2009). This means that online banking customers may be worried about payment delays and the time spent waiting for the website or learning how to use it. However, our research proved that time risk does not affect intentions to use fintech because technology now is relatively faster than before. Our study, to some extent, is in line with Andreoni and Sprenger (2012), who found that consumers are more worried about the risk of financial matters than time; when there is a financial matter, buyers can wait. On the other hand, everyone has some indirect sense of feature about technology relating to time, that technology saves time, so it is not going to affect them. Consumers are not worried about the delays in fintech. As fintech is far faster than traditional dealings, for example, during covid-19, the use of fintech overall increased (Fu & Mishra, 2022). Now, fintech organizations should focus on other main issues that users face. The rejection of the hypothesis of time risk indicates that fintech has already won consumers’ trust with respect to time management.

Security risk is essential for consumers’ online transactions (M.-C. Lee, 2009; Ryu, 2018). Interestingly, our study shows that Pakistani consumers are less worried about security. It shows that it is not easy to hack any online system nowadays. Thus, this hypothesis that security risk negatively affects fintech intention use is insignificant. This conclusion is in line with research findings that found no link between consumers’ perceptions of electronic payment and perceived security (Tang et al., 2020; Teoh et al., 2013). It may be shown by deploying stringent security mechanisms in network data transmission and fintech applications, such as encryption, digital signatures, and two-step verification, reducing the perceived security risk as a significant deterrent to using fintech.

According to previous studies, consumers are less likely to adopt fintech when legal risks rise. Interestingly, our results contradict Ryu (2018), who found that customers are apprehensive about legal issues and unwilling to use fintech. The majority of respondents are unconcerned about the restrictions around fintech. Our research contradicts Tang et al. (2020), who presented a model to describe the influence of legal concerns on users’ intents. Now, these days, fintech is in its boom position. Countries have rules and regulations. Even if consumers are unaware of the fintech regulations, they still trust the fintech companies prevalent in the markets. Though where legal issues have arisen, consumers will not use fintech. The current study found that consumers are less worried about the legal issues because all the fintech companies have to register themselves to get a license from the government’s recommended organizations, for example, the state bank of Pakistan. The government is also trying to digitalize the country by allowing more fintech companies to work (PSPs, 2014; Rizvi et al., 2017).

Psychological risk is found to have a low-risk impact on the fintech usage intention and is insignificant. Psychological concerns are found less critical. Now consumers are more mature than olden days when technology was new, and consumers were more worried about each step of using fintech. Now, consumers are more in touch with fintech and better understand fintech usage. However, some other factors may increase psychological risk if there is poor performance of the fintech services or financial risk, which may ultimately increase consumers’ psychological risk. Our research is in line with Featherman and Pavlou (2003), who found no significant impact of psychological risk on the intention to use fintech.

The overall risk is found to be significant. It negatively affects the intention to use fintech. Our study is consistent with Bauer (1967) and Jacoby and Kaplan (1972). However, five hypotheses are rejected, meaning there is no negativity with the intention of fintech usage. According to the results, consumers think overall, it is risky, but they are still using fintech. It shows that fintech is now a consumer’s need. Despite the fact it is a risker, consumers are still using fintech.

The facts above highlight the risks of implementing current IT technologies that alter management and accounting preconditions, change information exchange, aggregation, and distribution methods, and establish a new financial structure. Changes in the IT industry may substantially impact an accounting system’s postulates and categories. Although implementing creative IT advancements in accounting allows for processing enormous amounts of data in the fastest time possible, the risk concerns must also be acknowledged.

Research Implications

The research findings give insight into several vital aspects surrounding customer intentions toward fintech that have been overlooked in prior research. This method is expected to result in a steady evolution of theory. Consequently, the suggested approach significantly the growing fintech literature. This study’s finding has wide-ranging ramifications for subsequent fintech research. The empirical results imply that the risk element has a more significant effect on consumers’ judgment than the gain component, meaning that risk takes precedence over benefit for online banking clients when considering fintech.

Furthermore, the empirical findings demonstrate that the proposed model has strong explanatory power. Information technology (IT) acceptance research, for example, by Venkatesh and Davis (2000), has produced several competing models, each with its own set of acceptance determinants, such as social cognitive theory (SCT), innovation diffusion theory (IDT), and expectation confirmation model (ECM). This finding is expected to inspire further research that combines these opposing theories to create a unified one.

Practical Implications

The findings of this study give insight into certain key concerns surrounding consumer intentions toward fintech adoption that have not been addressed in earlier research. The perceived risk significantly affects whether or not consumers want to embrace fintech. This conclusion is especially relevant for managers deciding how to deploy resources to keep and grow their current customer base. On the other hand, building a risk-free online transaction environment is much more challenging than providing consumers with advantages. As a result, electronic business organizations must look for risk-reduction measures that will help them inspire high levels of trust in prospective consumers. According to the findings, they should prevent infiltration, fraud, and identity theft. Building secure firewalls to prevent incursion, inventing techniques to increase encryption, and certifying websites to avoid scams and identity theft are just a few actions that should be implemented. Effective risk-reducing strategies may include money-back guarantees and prominently advertised customer satisfaction assurances to offset financial and performance-based risk concerns. Consumers may be ready to accept the perceived risk if they trust the service provider’s commitment to them.

Limitations and Future Study

The research is restricted in scope and only looks at risk variables as they are viewed. It looks at how perceived risk variables affect Pakistani consumers’ willingness to utilize fintech. Future studies should examine perceived advantages and risks in understanding fintech adoption intentions. This study also didn’t include the complete cognitive models of TRA and UTAUT and only considered the negative elements of risk theories that affect the fintech usage intention. Future academics should also perform more analysis to analyze the actual use of financial technology in their study framework. Aside from that, researchers may look at financial literacy and economic issues to see the intentions.

Conclusion

The components of perceived risk factors have been intensively researched in various domains. This research seeks to contribute to the corpus of information on the usage of consumer-related fintech systems in Pakistan, mainly to assist professionals in effectively conceptualizing, reducing risk barriers, and preparing for fintech upheaval. The findings of this research are, to some degree, similar to prior research in that performance risk/operation risk, financial risk, and overall risk are all critical issues that deter people from using fintech.

According to the findings, security, time, psychological, and legal risks had no statistically significant influence on fintech usage intention in Pakistan. The results indicated that the performance, financial, and overall risk aspects were the primary reasons for worry for this sample and context, resulting in lower system assessment and adoption. After identifying the most significant risk aspects, the focus may shift to determining the maximum acceptable risk levels for each perceived risk facet. These thresholds may serve as a guideline for deciding how low-risk perceptions should stimulate adoption in each target market. Several simple risk-reduction measures may be implemented into the user interface to counteract customer worries.

Finally, operational skills/technical expertise and system functional performance must be considered while offering services. Consumer discontent and distrust will result from insufficient or failed financial services operations, creating hurdles to fintech adoption.

Footnotes

Appendix

| Cross loadings | |||||||||

|---|---|---|---|---|---|---|---|---|---|

| FR | IN | LR | OR | PPR | PR | SR | SSR | TR | |

| FR1 | 0.692 | −0.473 | 0.482 | 0.371 | 0.423 | 0.512 | 0.396 | 0.434 | 0.397 |

| FR2 | 0.849 | −0.654 | 0.513 | 0.585 | 0.416 | 0.580 | 0.448 | 0.477 | 0.526 |

| FR3 | 0.665 | −0.406 | 0.391 | 0.337 | 0.304 | 0.367 | 0.370 | 0.464 | 0.368 |

| FR4 | 0.836 | −0.642 | 0.560 | 0.643 | 0.493 | 0.558 | 0.445 | 0.456 | 0.622 |

| FR5 | 0.793 | −0.622 | 0.530 | 0.548 | 0.463 | 0.534 | 0.485 | 0.480 | 0.570 |

| IN1 | −0.741 | 1.000 | −0.634 | −0.841 | −0.624 | −0.680 | −0.618 | −0.531 | −0.730 |

| LR1 | 0.656 | −0.557 | 0.798 | 0.551 | 0.541 | 0.511 | 0.439 | 0.562 | 0.523 |

| LR2 | 0.575 | −0.525 | 0.783 | 0.512 | 0.415 | 0.424 | 0.437 | 0.549 | 0.518 |

| LR3 | 0.533 | −0.537 | 0.785 | 0.527 | 0.377 | 0.455 | 0.473 | 0.496 | 0.537 |

| LR4 | 0.438 | −0.427 | 0.808 | 0.449 | 0.393 | 0.331 | 0.413 | 0.423 | 0.428 |

| LR5 | 0.448 | −0.510 | 0.845 | 0.471 | 0.363 | 0.468 | 0.449 | 0.471 | 0.450 |

| LR6 | 0.422 | −0.467 | 0.792 | 0.457 | 0.413 | 0.387 | 0.470 | 0.452 | 0.463 |

| OR1 | 0.620 | −0.759 | 0.590 | 0.855 | 0.689 | 0.537 | 0.517 | 0.500 | 0.662 |

| OR2 | 0.537 | −0.714 | 0.523 | 0.869 | 0.589 | 0.541 | 0.532 | 0.418 | 0.697 |

| OR3 | 0.567 | −0.709 | 0.478 | 0.887 | 0.662 | 0.499 | 0.469 | 0.418 | 0.624 |

| OR4 | 0.572 | −0.757 | 0.561 | 0.891 | 0.582 | 0.505 | 0.508 | 0.455 | 0.656 |

| OR5 | 0.590 | −0.719 | 0.546 | 0.851 | 0.583 | 0.520 | 0.455 | 0.466 | 0.558 |

| PPR1 | 0.515 | −0.614 | 0.507 | 0.705 | 0.968 | 0.413 | 0.463 | 0.448 | 0.556 |

| PPR2 | 0.548 | −0.592 | 0.504 | 0.673 | 0.965 | 0.410 | 0.428 | 0.410 | 0.599 |

| PR1 | 0.501 | −0.532 | 0.392 | 0.414 | 0.268 | 0.786 | 0.346 | 0.309 | 0.412 |

| PR2 | 0.616 | −0.572 | 0.441 | 0.507 | 0.349 | 0.882 | 0.407 | 0.391 | 0.474 |

| PR3 | 0.532 | −0.574 | 0.501 | 0.550 | 0.429 | 0.799 | 0.437 | 0.499 | 0.503 |

| SR1 | 0.560 | −0.618 | 0.539 | 0.566 | 0.414 | 0.489 | 0.915 | 0.413 | 0.618 |

| SR2 | 0.372 | −0.415 | 0.404 | 0.390 | 0.380 | 0.316 | 0.799 | 0.303 | 0.582 |

| SSR1 | 0.518 | −0.480 | 0.500 | 0.447 | 0.455 | 0.427 | 0.425 | 0.884 | 0.508 |

| SSR2 | 0.577 | −0.499 | 0.597 | 0.491 | 0.342 | 0.429 | 0.378 | 0.897 | 0.417 |

| SSR3 | 0.473 | −0.423 | 0.542 | 0.435 | 0.382 | 0.440 | 0.316 | 0.869 | 0.426 |

| TR1 | 0.564 | −0.603 | 0.545 | 0.564 | 0.467 | 0.439 | 0.599 | 0.427 | 0.827 |

| TR2 | 0.518 | −0.617 | 0.492 | 0.675 | 0.526 | 0.481 | 0.523 | 0.379 | 0.840 |

| TR3 | 0.580 | −0.624 | 0.507 | 0.617 | 0.515 | 0.504 | 0.634 | 0.482 | 0.859 |

Acknowledgements

All the authors have contributed equally. Chunling Li worked as a supervisor and did a peer review. Nosherwan Khaliq conceptualized the idea and wrote the first draft. Leslie Chinove used software and participated in the methodology. Usama Khaliq worked on the data collection, rewriting. Judit Oláh, did a formal analysis and resources.

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.

An Ethics Statement

This paper is only being uploaded in this journal and not submitted in the other journal at the same time. All the ethical values have been considered for collecting the data and writing this paper.