Abstract

This study examines the relationship between climate risk and stock crash risk and the moderating effect of greenhouse gas emission trading scheme (ETS). Numerous studies have tested stock price crash risk measured by the negative skewness of return distributions in the areas of internal governance mechanism. While interest in environmental performance for sustainable growth of firms has increased, there are no studies on the effect of climate risk on stock crash risk. Thus, we find that climate risk (a firm’s greenhouse gas emissions and energy consumption) increases stock crash risk, and the positive effect of climate risk on stock crash risk is weakened after introduction of the emission trading scheme. This study theoretically extends the literature on the empirical determinants of stock crash risk, and practically provides investors with proven information about whether climate risk is worth considering during investment decisions. Furthermore, at the level of government policy, we can suggest that a monitoring system is needed to mitigate potential information asymmetry problems in firm with high climate risk.

Keywords

Introduction

Information asymmetry between corporate insiders and external investors in the capital market is a major factor that increases the stock risk premium (Merton, 1987). From this perspective, academic and practical interest in stock price crash risk is increasing (Habib et al., 2018). Stock crash risk is a phenomenon in which stock prices drop sharply as negative inside information is not disclosed in a timely manner but is disclosed in a mass (L. Jin & Myers, 2006). Therefore, risk-averse investors wary of stock crash risk have incentives to actively identify which ex-ante information affects ex-post stock crash risk from an investment strategy point of view. Numerous research has tested the factors influencing stock crash risk in the areas of internal governance mechanism, which covers accounting information transparency (C. Chen et al., 2017; DeFond et al., 2015; Hutton et al., 2009; J. B. Kim & Zhang, 2016), characteristics of shareholder and management (Boubaker et al., 2014; Jebran et al., 2020; H. M. Jin et al., 2022; J. B. Kim & Zhang, 2016; Zhou et al., 2021), and corporate social responsibility (CSR) (Thuy et al., 2022). However, few studies are interested in the relationship of firm’s environmental issue and stock crash risk.

Climate change is identified as one of the major and complicated problem facing the world economy today. This phenomenon can have a significant impact on the valuation of financial assets and the stability of the financial system (Lin & Wu, 2023). The “Global Risk Report 2023” published by the World Economic Forum mentions the most serious risks in the world over the next decade, including natural disasters and rapid climate change due to the collapse of ecosystems. Thus, following the U.S. Inflation Reduction Act of 2022, the EU (European Union) Commission announced Net-Zero Industry Act and European Critical Raw Materials Act of 2023. This aims to scale up the EU manufacture of key carbon neutral or net-zero technologies to ensure secure, sustainable, and competitive supply chains for clean energy in view of reaching the EU’s climate and energy ambitions. Khan et al. (2021) explained that green supply chain practices which is becoming a hot topic in strict environmental laws promote economic growth by providing trade opportunities in pro-environmentalist countries. Environmental sustainability is positively related to national level eco-friendly practices, including sustainable use of natural resources and regulatory pressure (Khan et al., 2020). Especially, Europe, which is at the forefront of environmental issues, gives an official status to the Green Deal, which is a set of policy initiatives aimed at achieving the EU’s goal of making the continent carbon-neutral by 2050.

Korea has a relatively large proportion of coal power generation, and mainly focuses on industries with high carbon emissions such as steel, petrochemicals, and cement. Thus, Korea produced the ninth-largest amount of carbon dioxide in the world in 2019, accounting for about 1.4% of global emissions. Above all, Korea’s carbon emission increase rate is the highest in OECD countries, and per capita emission is 15.5 tons, which is more than double the global average (7.3 tons) (IEA, 2020). Therefore, Korea is a country with a high possibility of carbon leakage. Environmental regulations can cause changes in the business environment in Korea, leading to problems such as a decrease in sales due to damage to product price competitiveness, and a decrease in earnings due to an increase in environmental costs (Korea International Trade Association, 2021). For example, if the European Union (EU), which is leading the global eco-friendly paradigm, implements the Carbon Border Adjustment Mechanism in 2026, the price competitiveness of Korean products will decrease and exports to the EU will inevitably decrease.

The Korean government is also moving toward a low-carbon economy through policies such as the introduction of advanced technologies to reduce greenhouse gas and the expansion of green infrastructure investment for sustainable growth. Previously, the government enacted “the Framework Act on Low Carbon Green Growth” and introduced the “Greenhouse Gas and Energy Target Management System” to cope with climate change in 2010. Through this system, the government can designate firms to manage national greenhouse gas emission targets by using energy efficiently. Accordingly, firms selected for management can emit greenhouse gas within the level permitted by the government, and if they violate this, they will be subject to administrative sanctions. Therefore, firms with high energy consumption and greenhouse gas emissions are exposed to threats such as administrative sanctions and damage to reputation in the short term, and face problems such as large-scale financing in the mid to long term as eco-friendly process conversion is required. In summary, as the government’s environmental regulations are strengthened, environmental issues are growing in importance in the business environment.

This study examines climate risk as one of the factors affecting stock crash risk. Firm-level climate risk was reported to be associated with several adverse outcomes such as lower profitability and higher cost of debt (Busch & Lewandowski, 2018; L. H. Chen & Silva Gao, 2012; Goss & Roberts, 2011; Jung et al., 2018; Konar & Cohen, 2001; Matsumura et al., 2014; Russo & Fouts, 1997; Saka & Oshika, 2010). Accordingly, firms with a high climate risk might have incentives to disclose higher financial performance to cover some of the negative effects (Amin et al., 2021; Ding et al., 2021; Lemma et al., 2020; Litt et al., 2013; Velte, 2019, 2021). Furthermore, managers of firms with high environmental risk may use earnings management as tool of greenwashing policy (Velte, 2021), which causes accounting transparency problems. And environmental risk may have a negative effect on corporate disclosure quality (Y. Kim, 2021). Ultimately, insincere disclosure of corporate information, including climate risks, can cause information asymmetry in the capital market, leading to the stock crash risk (Bae et al., 2021). Thus, we expect that climate risk increases stock crash risk.

Meanwhile, as economic development accompanied by environmental protection has become a universal issue, emissions trading systems (ETS) have become important environmental policy instruments. The greenhouse gas emission trading scheme (GHG ETS) is a system in which the government allocates annual penalties to firms that emit large amounts of greenhouse gas, evaluates actual emissions, and allows trade between firms for excess or insufficient allowances (Korea Environment Corporation). In other words, the ETS is a means of providing economic incentives to entities that emit greenhouse gas based on market principles, unlike the direct regulation method that relies on administrative and judicial orders. Accordingly, the Korean government introduced the GHG ETS in 2015 to effectively manage firms that emit large amounts of greenhouse gas.

Numerous studies show that regulatory factors on climate change risks, such as the GHS ETS, induce firms to respond actively and voluntarily to climate change (Clarkson et al., 2004; Griffin & Mahon, 1997; Porter, 1991; Porter & Van der Linde, 199517; van Leeuwen & Mohnen, 2017; Waddock & Graves, 1997; Zang et al., 2020). For example, after the introduction of GHS ETS, firms’ response to climate change such as technology innovation, productivity enhancement, and product competitiveness improvement might increase, and the information opacity related to climate risk of firms in the capital market can decrease. Thus, environmental regulation can increase the clarity of corporate information including environmental issues, and improve the accuracy of earnings forecast, thereby mitigating stock crash risk (Hutton et al., 2009; Li et al., 2017; Wen, 2023). According to the discussion above, after the introduction of GHS ETS, firms’ responses to climate change might increase, and the information opacity related to climate risk of firms in the capital market can decrease. Therefore, we expect that a positive association between climate risk and stock crash risk will weaken after the introduction of ETS.

The research period of this study is from 2011 to 2019, and a sample for the study is composed of KSE (the Korea Stock Exchange) and KOSDAQ (Korean Securities Dealers Automated Quotations) listed corporations. We report that the greater is the climate risk at the firm level, the greater is the stock crash risk. This phenomenon means that the more exposed a firm is to climate risks (GHG emissions and energy consumption), the greater the risk of a stock crash due to the loss of accounting transparency resulting from earnings management etc. and the deterioration of the disclosure quality. We also report that the positive association between climate risk and stock crash risk is weakened after introduction of ETS, which suggests that introduction of GHS ETS might increase firm response to climate change and decrease the information opacity related to climate risk of firms in the capital market.

We contribute to previous studies by developing an understanding of the influence of climate risk on capital markets through this research. Considering that there is no study on climate risk, while various factors such as information transparency, shareholder characteristics, TMT (Top Management Team) characteristics, and corporate social responsibility have been reviewed regarding the causes of the stock crash risk, the research extends the research on the empirical determinants of stock crash risk. Research findings also provide investors with proven information about whether climate risk is worth considering during investment decisions in the stock market. And at the level of government policy, we can suggest that a monitoring system is needed to mitigate potential information asymmetry problems in firm with climate risk. Because we show the effect of climate risk on stock crash risk which is related to information asymmetry. Especially, we also propose that policy agency must demonstrate efficient use of regulation on climate change risks, such as the GHS ETS, given that the introduction of the ETS has a meaningful moderating effect on the association between climate risk and stock crash risk. Specifically, we expect the implementation effect of environmental policies, which causes firms to burden substantial environmental violation costs.

The structure of this study is as follows. We develop hypotheses after reviewing the relevant studies on the effect of climate risk on firm performance and transparency and the determinants of stock crash risk in Section 2. We develop research model for hypothesis test and explain the empirical results in Section 3 and Section 4. In Section 5, we conclude the meaning of the empirical results and contributions of the research.

Prior Research and Hypothesis Development

The Effects of Climate Risk on Financial Performance and Transparency

Many studies have argued that climate risk negatively affects firm performance in a long run. Bragdon and Marlin (1972) showed that better environmental performance improved profitability based on CEP social audit rankings of firms’ pollution records. Russo and Fouts (1997) documented that companies that care more about the environment achieve higher performance economically, especially in fast-growing industries. Konar and Cohen (2001) and Saka and Oshika (2010) provided the results that the more the CO2 a company emits, the lower the value of a company. Matsumura et al. (2014) found that a 1,000 metric ton increase in carbon emissions reduces a value of a company by an average of $212,000 based on carbon emission data of S&P 500 firms. According to Busch and Lewandowski (2018), environmentally high-performing companies have high accounting performance, and these companies also receive positive responses in the market.

In addition, several research showed that climate risk is negatively related to firms’ financial transparency. Litt et al. (2013) documented that firms with environmental initiatives have lower earnings management as measured in discretionary accruals under the modified Jones model. According to Velte (2019), ESG performance of companies listed on the German Prime Standard has a negative effect on accrual earnings management. Lemma et al. (2020) reported that higher carbon risk exposures tended to provide lower quality financial statements based on a sample of companies listed on the Johannesburg Stock Exchange. Amin et al. (2021) found that the greater is the carbon footprint, the greater is the earnings management by real activity. Ding et al. (2021) provided the results that climate risk is positively associated with firms’ engagements in earnings management using a country-level climate risk indicator presented by Germanwatch. Velte (2021) reported that environmental performance reduces accrual earnings management in firms listed on the STOXX Europe 600. This result means that firms with high environment risk have incentives to use earnings management in their greenwashing policies because earnings management is difficult to detect by other stakeholders.

According to prior studies, climate risk (bad environmental performance) can harm both accounting-based and market-based performance (Bragdon & Marlin, 1972; Busch & Lewandowski, 2018; Konar & Cohen, 2001; Matsumura et al., 2014; Saka & Oshika, 2010; Spicer, 1978), affect negatively on corporate financial transparency measured by earnings management, etc. (Ding et al., 2021; Litt et al., 2013; Velte, 2019), and then provide poor quality financial statements (Lemma et al., 2020). However, studies on the impact of corporate climate risk on stock price behavior in the capital market is very limited.

Determinants of Stock Crash Risk

Numerous research tested stock price crash risk estimated by the negative skewness of return distributions in the areas of internal governance mechanism, which covers quality of Financial Information (DeFond et al., 2015; Hutton et al., 2009), characteristics of shareholders and management (Boubaker et al., 2014; Jebran et al., 2020; H. M. Jin et al., 2022; J. B. Kim & Zhang, 2016; Zhou et al., 2021), and corporate social responsibility (CSR) (Thuy et al., 2021, 2022). Hutton et al. (2009) found that earnings management which is evaluated as a proxy for financial opacity increases stock crash risk. DeFond et al. (2015) found that IFRS adoption reduces stock crash risk of firms, especially in a bad information environment. J. B. Kim and Zhang (2016) reported a negative relationship between conditional conservatism and stock crash risk based on the notion that it limits managers’ ability to conceal bad news. Zhou et al. (2021) examined effect of shareholder’s pledging behavior to hoard bad news on stock crash risk. J. B. Kim et al. (2011) presented evidence that a CFO’s sensitivity to the stock price of an option portfolio is positively related to their firm’s future stock crash risk, explaining that stock option compensation encourages managers to hide bad news. Jebran et al. (2020) noted board diversity, which consists of relationship-oriented diversity (gender and age) and task-oriented diversity (tenure and education) and reported that the greater the diversity of the board, the lower the risk of future stock crash. H. M. Jin et al. (2022) showed that academic independent directors (AIDs) reduce future stock crash risk by improving the financial reporting quality, promoting CSR, and mitigating agency costs. Y. Kim et al. (2014) explained that stock crash risk will decrease if firms with social responsibility maintain information transparency such as accumulating less bad news based on the empirical results that CSR performance reduces the future crash risk.

Summarizing the prior studies above, the causes of stock crash risks have been analyzed from various internal governance mechanisms such as information transparency, shareholder characteristics, TMT’s characteristics, and corporate social responsibility. However, there are no studies on the impact of climate risk, using direct measurement of environmental pollution not affected by green washing, on stock crash risk.

Hypothesis Setting

Climate change is a critical issue facing humanity today, with significant implications to evaluate global financial assets and the financial system’s stability (Lin & Wu, 2023). Numerous studies have found that firm-level climate risk is associated with several adverse results such as lower profitability and lower firm value (Busch & Lewandowski, 2018; Konar & Cohen, 2001; Matsumura et al., 2014; Russo & Fouts, 1997; Saka & Oshika, 2010). Given the adverse effects of climate risk, firms can have an incentive to attempt to report higher income in periods of high climate risk to offset some of the negative effects. Several prior studies have reported that firms with high climate risk strive to manage earnings to report higher income (Amin et al., 2021; Ding et al., 2021; Lemma et al., 2020; Litt et al., 2013; Velte, 2019, 2021).

In summary, managers of firms with high environmental risk may use earnings management as tool of greenwashing policy (Velte, 2021), which causes accounting transparency problems. And environmental risk measured by amount of emitted greenhouse gas and consumed energy of a firm may have a negative effect on corporate disclosure quality (Y. Kim, 2021). Ultimately, insincere disclosure of corporate information, including climate risks, can cause information asymmetry in the capital market (Bae et al., 2021). Accordingly, we can understand that firm exposure to climate risk can undermine accounting transparency, which can increase the possibility of stock crash risk (Hutton et al., 2009). Therefore, we expect that firms with climate risks as measured by greenhouse gas emissions and energy consumption have a high probability of facing stock crash risk. Based on the discussion, we establish the following hypothesis.

Meanwhile, a firm’s response to environmental risks depends on its ability to take risks, which may vary depending on external environment such as system (Dunbar et al., 2020). The ETS (emission trading scheme) is an ESG mitigation mechanism that environmentally responsible firms can use to mitigate climate risks. As the harmonious development of the environment and the economy has emerged as a global issue, the ETS has become an important policy instrument in the field of environment. The ETS is a means of providing economic incentives to entities that emit greenhouse gas based on market principles, unlike the direct regulation method that relies on administrative and judicial orders and is based theoretically on Coase’s Theorem (1960). The Porter hypothesis (Porter, 1991; Porter & Van der Linde, 1995) states that environmental regulations such as ETS encourage firms to invest environment-friendly technological innovations, which helps improve productivity and product competitiveness. Thus, both firms and society can experience the positive role of environmental regulation based on a dynamic equilibrium (van Leeuwen & Mohnen, 2017). According to Zang et al. (2020)’s empirical analysis on EU ETS, ETS promotes the upgrade of the country’s industrial structure. Also, regulated firms can reduce costs through efficient investment (Porter & Van der Linde, 1995) and can obtain benefits such as sales increase and firm value improvement through good reputation in fulfilling their environmental responsibilities (Clarkson et al., 2004; Griffin & Mahon, 1997; Waddock & Graves, 1997).

Regulatory factors on climate change risks, such as the GHS ETS, induce firms to respond actively and voluntarily to climate change (43Clarkson et al., 2004; Griffin & Mahon, 1997; Porter, 1991; Porter & Van der Linde, 199517; van Leeuwen & Mohnen, 2017; Waddock & Graves, 1997; Zang et al., 2020). Thus, environmental regulation can reduce stock crash risk by alleviating information asymmetry problem, such as by improving the quality of environmental information disclosure (Hutton et al., 2009; Li et al., 2017). For example, Wen (2023) systematically investigated the influence of CEPI (central environmental protection inspection) on the stock crash risk in of Chinese listed firms in pollution industries, and then showed that CEPI can reduce the firms’ stock crash risk. According to this logic, after the introduction of GHS ETS, firms’ responses to climate change might increase, and the information opacity related to climate risk of firms in the capital market can decrease. Therefore, we expect that the positive relationship between climate risk and stock crash risk will weaken after introduction of ETS. Based on the discussion, we establish hypothesis 2.

Research Methods

Model Specification

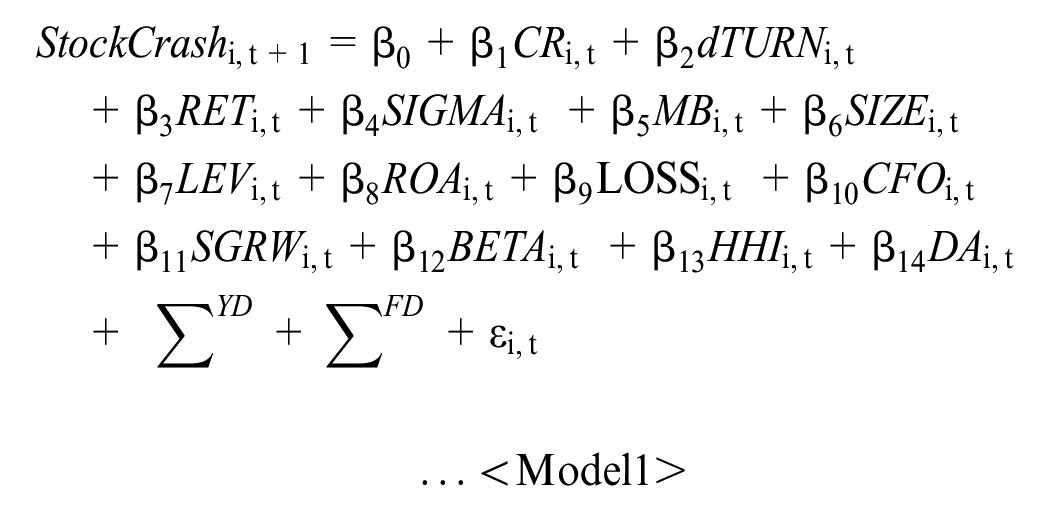

We estimate Model 1 to test Hypothesis 1 using Ordinary Least Squares (OLS). A regression model is designed with stock crash risk as the dependent variable and climate risk as the independent variable. Stock crash risk (StockCrash), our dependent variable is measured in three ways: (i) NCSKEW, (ii) DUVOL, and (iii) COUNT as in prior studies (Callen & Fang, 2013, 2015; C. Chen et al., 2017; Hutton et al., 2009; L. Jin & Myers, 2006; J. B. Kim et al., 2011). We measure stock crash risk using the distribution of firm-specific weekly returns. To this purpose, the following Equation 1 is first estimated:

where, for firm i on week τ,

According to prior studies, we use three firm-specific stock price crash risk proxies for each firm i and year t: (i)

where n is the number of observations

According to previous research, we have defined climate risk as the risk of companies related to climate change or fossil fuel use (Hoffmann & Busch, 2008), which brings the uncertainty of future cash flows of companies due to business risk factors, such as regulations (Bauer & Hann, 2010; Sharfman & Fernando, 2008). We measure our independent variable, Climate risk (CR), using data of amount of emitted carbon dioxide and amount of consumed energy by a company according to recent research (S. I. Kim & Kim, 2023). CR consists of two variables: CR1 (amount of emitted greenhouse gas divide by unit of sales) and CR2 (amount of consumed energy divide by unit of sales). These proxies are not affected by greenwashing because they are measured using environmental performance directly.

According to prior research, we include factors that are expected to affect stock crash risk in the model (C. Chen et al., 2017; Hutton et al., 2009). Factors related to stock crash risk are change in average monthly share turnover (dTURN), weekly average stock returns (RET), standard deviation of weekly average stock returns (SIGMA), market-to-book value (MB), firm size (SIZE), debt-to-asset ratio (LEV), net profit margin (ROA), loss dummy (LOSS), operating cash flow to total assets (CFO), growth rate of sales (SGRW), market beta coefficient (BETA), market competition (HHI), and performance matched to discretionary accrual by Kothari et al. (2005) (DA). Dummy variables for year (YD) are included additionally. Particularly, we include firm fixed effects to minimize the effect of unobserved heterogeneity.

We estimate Model 2 to test Hypothesis 2 concerning the moderating effect of ETS on the relation between climate risk and stock crash risk using Ordinary Least Squares (OLS). Greenhouse gas emission trading scheme (ETS) and an interaction variable (CR*ETS) are employed to test the moderating effect of ETS on the positive association between climate risk and stock crash risk. The values of VIF (variance inflation factor) in Model 1 and 2 showing less than 4, indicate that our models are not suffered from severe multicollinearity (Table 1).

Definition of Variables.

Sampling and Data Collection

Our sample consists of firms listed on the KSE and KOSDAQ fiscal years from 2011 to 2019 that report the amount of emitted greenhouse gas and the amount of consumed energy to the Ministry of. We collect the financial data such as sales, earnings, assets, liabilities, and stock price from the Data Guide (equivalent to Compustat and CRSP in the United States). Environmental data is collected from the National Greenhouse Gas Management System (NGMS). The final sample used for test is 1,045 firm-years after discarding a few observations for which key variables are not available. We winsorize continuous variables in the top 1% and bottom 1%, to eliminate the influence of outliers on the test results.

Results

Descriptive Statistics and Correlation

We present descriptive statistics of the variables in Table 2. The means of NCSKEW, DUVOL, and COUNT, the proxies of the stock crash risk, are −0.078, −0.110, and −0.201, respectively. The means of CR1 and CR2 are 0.764 and 0.786, respectively. Therefore, the mean value of greenhouse gas emissions per unit of sales (KRW 1 million) is 0.764 tCO2-eq, and the mean value of energy consumption per unit of sales (KRW 100 million) is 0.786 TJ. The mean value of dTURN is 0.000, RET is 0.001, SIGMA is 0.049, and MB is 1.033. The means of LEV, ROA, and LOSS are 0.456, 0.029, and 0.212, respectively; thus, the average leverage ratio and return on assets are 45.6% and 2.9%, respectively. The proportion of firms with a net income less than 0 is 21.2%.

Descriptive Statistics.

Note. Variable definitions: NCSKEW = negative coefficient of skewness of

Table 3 reports Pearson correlation coefficient of the main variables. The climate risk variables (CR1 or CR2) are associated significantly and negatively with stock crash risk variables (NCSKEW, DUVOL, or COUNT). These results imply that the higher is the climate risk, the lower is the stock crash risk. However, we conduct multivariate regression including control variables that might influence stock crash risk because correlation test means a simple relationship between variables.

Correlations.

Note. p-Values are reported below the correlation coefficients, and respectively and detailed definitions of variables are in the notes of Table 1.

Review of the Relationship Between Climate Risk and Stock Crash Risk

We show the results of the regression analysis investigating Hypothesis 1 that climate risk is positively related to stock crash risk in Table 4. We predict that climate risk induces stock crash risk. The significantly positive coefficient of CR means that the results support our Hypothesis 1. In columns (1) through (6) of Table 4, the coefficients of CR are 0.268, 0.173, 0.056, 0247, 0.136, and 0.105, respectively, and generally are significant. The companies emit more greenhouse gases and consume more energy, the greater the stock crash risk. These results support Hypothesis 1 that climate risk increases stock crash risk. We know that the more exposed a firm is to climate risks (GHG emissions and energy consumption), the greater the risk of a stock crash due to the loss of accounting transparency resulting from earnings management etc. and the deterioration of the disclosure quality (Y. Kim, 2021; Velte, 2021). Therefore, we can suggest that stock market investors need to consider firm’s climate risk when they make investment decisions.

Effect of Climate Risk on Stock Crash Risk.

Note.*, **, and *** denote significance at the 10%, 5%, and 1% levels, respectively and detailed definitions of variables are in the notes of Table 1.

Review of Moderating Effects of Greenhouse Gas ETS Between Climate Risk and Stock Crash Risk

We show the results of the regression analysis of the moderating effects of the GHG ETS on the relationship between climate risk and stock crash risk in Table 5. We predict that the positive relationship between climate risk and stock crash risk tested in Hypothesis 1 will weaken after the introduction of ETS. If coefficient

Moderating Effect of ETS in the Relationship Between Climate Risk and Stock Crash Risk.

Note.*, **, and *** denote significance at the 10%, 5%, and 1% levels, respectively and detailed definitions of variables are in the notes of Table 1.

In columns (1) through (6) of Table 5, the coefficients of CR*ETS are 0.119, −0.073, −0.062, −0.191, −0.128, and −0.054, respectively, and are generally significant. This supports Hypothesis 2 that the positive relationship between climate risk and stock crash risk is expected to weaken after the introduction of ETS. Therefore, we suggest that firm response to climate change will increase after the introduction of GHS ETS, and the information opacity related to climate risk of firms in the capital market will decrease. Ultimately, a regulatory system can reduce the stock crash risk by avoiding the accumulation of negative information about firms, such as increasing exposure to environmental violations (Hutton et al., 2009; Li et al., 2017).

For the robustness, we test Hypothesis 2 by sub-sample analysis to confirm the moderating effect of ETS on a positive relation between climate risk and stock crash risk. The total sample is divided into periods before (2011–2014) and after (2016–2019) introduction of ETS. The year 2015, when ETS was introduced, is excluded from the sample because of the mixed effect.

Table 6 shows the test results for the effect of climate risk on stock crash risk in each sample divided into pre-and post-ETS. In Panel A (Pre-ETS), the values of the coefficients of CR are positive and significant, whereas, in Panel B (Post-ETS), the values of the coefficients of CR are marginal or not significant. We conduct the test of the coefficients of CR in each sample divided into pre-and post-ETS. The results in Panel C show that the coefficients of CR in sample divided into pre-and post-ETS are significantly different. These results are consistent with Table 5 and strongly support Hypothesis 2.

Effect of Climate Risk on Stock Crash Risk (Pre-ETS vs. Post-ETS).

Note.*, **, and *** denote significance at the 10%, 5%, and 1% levels, respectively and detailed definitions of variables are in the notes of Table 1.

Additional Analysis

Generalized Method of Moment (GMM) analysis is conducted to eliminate endogeneity problem that the CR variable representing the firm’s climate risk may have (Wintoki et al., 2012). This is because CR is likely to be an endogenous variable rather than an exogenous variable derived according to a firm’s characteristics. We use industrial average of tangible asset (tangible asset to total asset ratio) and big4 auditor (dummy variable of big4 auditor) as instruments for climate risk (Hirschey & Weygandt, 1985; Y. Kim & Kim, 2022; Saka & Oshika, 2014). Dummy variables for year (YD), and industry (IND) are included instead of the dummy variable of firm. The over-identification test is conducted to confirm the validity of the instrumental variables used in the GMM analysis. The test results show not significant test statistics meaning that the selected instruments are valid. Table 7 shows GMM analysis results to check the association between climate risk and stock crash risk. In columns (1) through (6) of Table 6, the coefficients of CR are significantly positive in general. As such, the results of GMM analysis are not qualitatively different from those of Ordinary Least Squares (OLS), and thereby supporting Hypothesis 1 that climate risk increases stock crash risk.

GMM (Generalized Method of Moment) Analysis: Effect of Climate Risk on Stock Crash Risk.

Note.*, **, and *** denote significance at the 10%, 5%, and 1% levels, respectively and detailed definitions of variables are in the notes of Table 1.

The GMM test result to investigate the moderating effects of the ETS on the relationship between climate risk and stock crash risk is presented in Table 8. In columns (1) through (6) of Table 8, the coefficients of CR*ETS are generally significantly negative. This supports Hypothesis 2 that the positive association between climate risk and stock crash risk is expected to weaken after the introduction of ETS.

GMM (Generalized Method of Moment) Analysis: Moderating Effect of ETS in the Relationship Between Climate Risk and Stock Crash Risk.

Note.*, **, and *** denote significance at the 10%, 5%, and 1% levels, respectively and detailed definitions of variables are in the notes of Table 1.

We conduct further additional test using two-stage least squares (2SLS) to alleviate endogeneity problem driven by unobservable firm and CEO characteristics. We use CEO’s shareholding ratio in addition to industrial average of tangible asset and big4 auditor (dummy variable of big4 auditor) as instruments for climate risk (S. I. Kim & Kim, 2023). The over-identification test statistics, which are not significant, mean that the selected instruments are valid. Table 9 shows the results of 2SLS analysis to verify the relation between climate risk and stock crash risk. The values of the coefficients of CR are significantly positive in general. As such, the results of 2SLS analysis are qualitatively consistent with those of Ordinary Least Squares (OLS). These results are consistent with Hypothesis 1 that climate risk increases stock crash risk.

2SLS Analysis: Effect of Climate Risk on Stock Crash Risk.

Note.*denote significance at the 10% levels and detailed definitions of variables are in the notes of Table 1.

The 2SLS test result to investigate the moderating effects of the ETS on the relation between climate risk and stock crash risk is presented in Table 10. The coefficients of CR*ETS are generally significantly negative. These results support Hypothesis 2 that the positive association between climate risk and stock crash risk is expected to weaken after the introduction of ETS.

2SLS Analysis: Moderating Effect of ETS in the Relationship Between Climate Risk and Stock Crash Risk.

Note.*denote significance at the 10% levels and detailed definitions of variables are in the notes of Table 1.

Conclusion

This study analyzes the relationship between climate risk and stock crash risk and the moderating effect of the GHG ETS. We find that a firm’s climate risk measured by greenhouse gas emissions and energy consumption increase stock crash risk. This finding suggests that that the more exposed a firm is to climate risks (GHG emissions and energy consumption), the greater the risk of a stock crash due to the loss of accounting transparency resulting from earnings management etc. and the deterioration of the disclosure quality. We also report that the positive effect of climate risk on stock crash risk is weakened after the introduction of ETS, indicating an important moderating effect of the scheme. Thus, we suggest that firm response to climate change can increase after the introduction of GHS ETS, and the information opacity related to climate risk of firms in the capital market can decrease.

We contribute to prior studies by enhancing the grasp of the effect of climate risk on the capital market. Specifically, we reveal the stock crash risk affected by a firm’s climate risk beyond the effect of various internal governance mechanism, which have been discussed in prior studies. Our findings provide validated information to the investors whether it is worth taking in consideration the climate risk during investment decision for the stock market. And at the level of government policy, we can suggest that a monitoring system is needed to mitigate potential information asymmetry problems for firms with climate risk. Especially, based on the moderating effect of ETS, we propose that policy agency needs to use efficiently regulation on climate change risks, such as the GHS ETS, to produce a moderating effect on the relationship between climate risk and stock crash risk. Specifically, we expect the implementation effect of environmental policies, which causes firms to burden substantial environmental violation costs.

However, we know that it may be difficult to generalize the test results as our study because we focus firms that report greenhouse gas emissions and energy consumption to the government. In addition to the introduction of the ETS policy, we suggest future meaningful research on the role of internal and external environments that can affect a firm’s climate risk management, such as specific policy contents and each firm’s business strategy.

Footnotes

Author’s note

Yujin Kim is now affiliated to Sejong Cyber University, Seoul, South Korea.

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) received no financial support for the research, authorship, and/or publication of this article.