Abstract

China’s urban commercial banks are more likely to face risks with the rapid development of Internet finance. However, few studies unfold the impact of Internet finance on the risk-taking level of urban commercial banks and explore their role path in depth. To study the relationship between the two and their path of action, this paper takes 62 city commercial banks in China from 2011 to 2020 as research objects and makes empirical tests by Stata. The intermediary effect model is used to study its impact path from the perspectives of assets, liabilities, and intermediate services. The conclusions are as follows: (1) Internet finance aggravates the risk-taking of urban commercial banks; (2) This effect shows heterogeneity in listed and non-listed, trans-region and non-trans-region urban commercial banks; (3) Net interest margin, debt structure, and non-interest income show the mediating effect when Internet finance affects the risk-taking of urban commercial banks. The results are beneficial for urban commercial banks to change their business strategies with their characteristics and achieve sustainable and healthy development.

Introduction

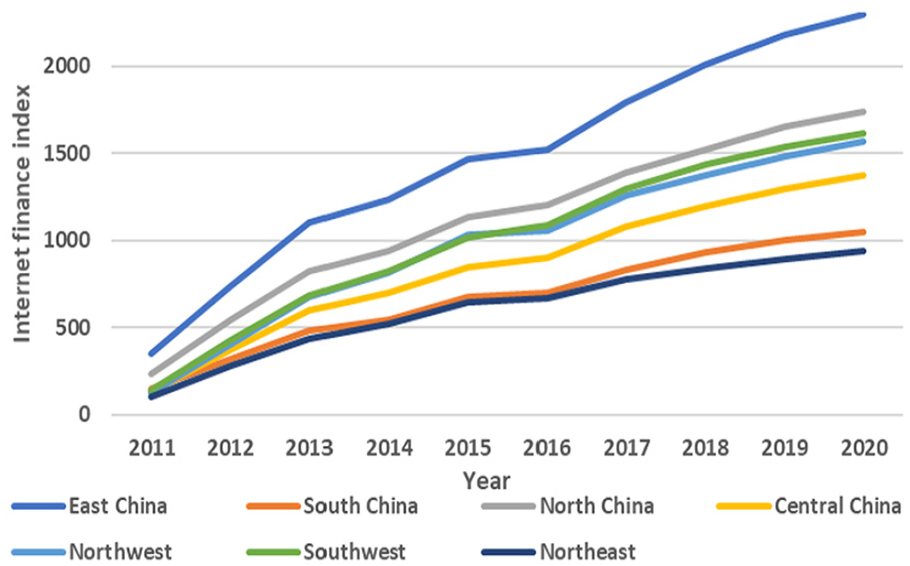

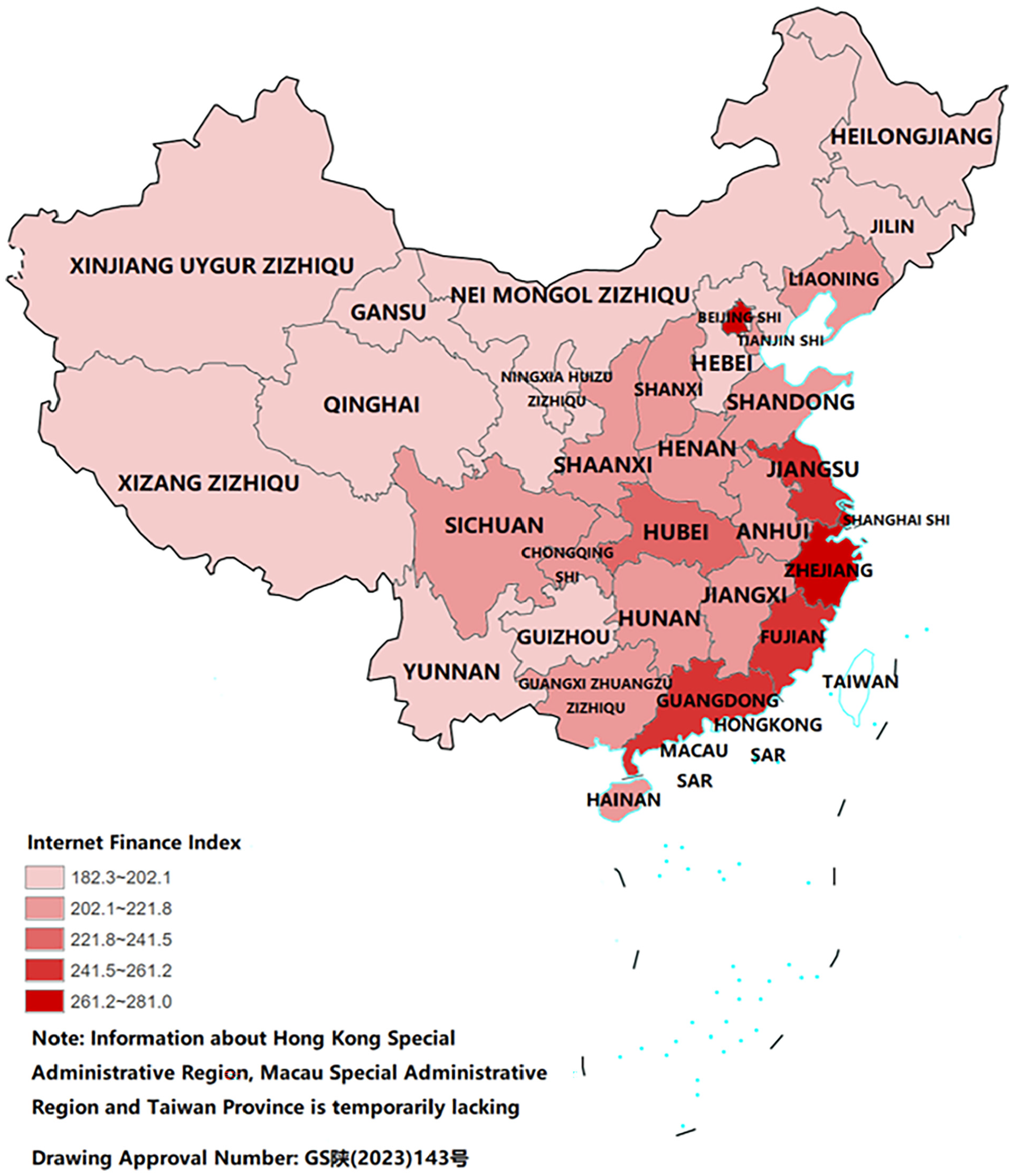

As a new financing model, Internet finance has come into being. Since the emergence of China's first P2P network platform in 2007, Internet giants such as JD and Baidu have joined the battle, and platforms such as Ant Micro Loan and Crowdfunding have been launched one after another. We sorted out the sub-regions of the Internet finance index from the Institute of digital finance of Peking University and divided China into seven regions: Northwest, Southwest, Northeast, North China, Central China, East China, and South China (Figure 1) (Ministry of Natural Resources of the People’s Republic of China, 2023). The sorting results are shown in Figure 2 (F. Guo et al., 2020). Figure 3 (Ministry of Natural Resources of the People’s Republic of China, 2023) is to average the Internet finance index of each province in China from 2011 to 2020, and indicates the development of Internet finance according to the color shade, the darker the color, the better the development of Internet finance in the region. This is mainly in the Chinese Mainland. These figures show that Internet finance in China is characterized by regional and unbalanced development. The beneficial impact of Internet finance is that, on the one hand, it enriches China’s economic growth structure (Yan et al., 2019) and promotes economic growth (Z. Liu, 2016). On the other hand, commercial banks are urged to use Internet technology to reform themselves, improve their operation mechanism, innovate financial products and services (R. Xie et al., 2021), reduce information asymmetry in the application of Internet technology in the financial field, and enhance the risk management level of commercial banks (S. Wang et al., 2021). The negative impact is that, on the one hand, it causes the phenomenon of “bad money driving out good money” in the banking industry (M. A.Khan & Malaika, 2021), which may affect the risk-taking level of commercial banks and even increase the possibility of systemic risks (Zhu & Hua, 2018). On the other hand, Internet finance is rapidly taking over the market scale, causing commercial banks to be robbed of profits from traditional businesses such as deposit and loan management (S. Wang et al., 2021). Table 1 shows the most representative third-party payment transaction size in the Internet finance sector and its proportion to the total transaction size from 2011 to 2020, according to the Research Consulting Data Network. The rapid growth of third-party transactions can be seen in Table 1.

China geographic division.

Development of Internet finance in China.

Internet financial index distribution map of China’s provinces.

Development Scale of Third-Party Payment.

As small and medium-sized commercial banks, the overall size of urban commercial banks is relatively small and in line with Internet finance for a competitive market of small and medium-sized enterprises. This makes city commercial banks more vulnerable in the context of the rapid development of Internet finance.

Therefore, how does the development of Internet finance affect the level of risk-taking of urban commercial banks? Is there heterogeneity in the impact of Internet finance on city commercial banks that are listed or not and operate across regions or not? What are the specific paths of the role of Internet finance in affecting the risk-taking level of urban commercial banks? Addressing these questions has important theoretical value and practical significance for promoting the sustainable and healthy development of urban commercial banks and maintaining the stability of the financial system.

Therefore, using a sample of 62 city commercial banks in China from 2011 to 2020, this paper examines the impact of Internet finance on the risk-taking of city commercial banks and considers the heterogeneity of different city commercial banks. The paths of influence are further explored based on the mediating effects model.

This research has some novelty. The first is to take urban commercial banks as research objects; the second is to further explore the role mechanism of Internet finance affecting the risk-taking of urban commercial banks based on three business sides: assets, liabilities, and intermediate business. Accordingly, there are some contributions in this study. On the one hand, taking urban commercial banks as research objects not only enriches the research related to the risk-taking of urban commercial banks but also increases the applicability of the findings. On the other hand, the mechanism of the role of Internet finance on the risk-taking of urban commercial banks is further explored to help urban commercial banks to change their business strategies according to their acteristics to guide the impact of Internet finance on risk-taking of urban commercial banks away from negative and toward positive.

Literature Review

Internet Finance Related Research

In the beginning, people’s understanding of Internet finance mainly stayed on its surface, thinking that Internet finance is the application of Internet technology in the financial field (Herbst, 2001), and is an emerging financial model (P. Xie & Zou, 2012). Since then, there has been a growing awareness of it. Hyung et al. (2014) believed that Internet finance is a new application of information technology and network security, and is a leapfrog development of information technology itself. Wu (2015) argued that Internet finance is a new financial industry that uses the Internet as a platform to perform financial functions based on the integration of information using cloud data. K. Li (2016) pointed out that Internet finance is an emerging financial model that relies on Internet technologies such as search engines, social networks, and big data to realize the business of payment and settlement, capital financing, and information intermediation. It is a new development model of the financial industry with big data and artificial intelligence as the technical foundation and the Internet and electronic hardware as the support platform (Baki & Bagci, 2021). However, some scholars believed that Internet finance is not a new financial model, and essentially does not change the transaction object, or payment structure (Chen, 2014), but only improves the function and efficiency of finance (Chu & Guo, 2014). Although it has an impact on traditional financial institutions, it does not fundamentally disrupt the traditional financial industry (D. Wang, 2014).

Research Related to Risk-taking of Commercial Banks

“Risk-taking” was first introduced in non-financial companies. Highhouse and Yüce (1996) paid early attention and pointed out in their study that risk-taking is a behavior that manifests itself in the process of making behavioral choices by decision-makers. Risk-taking in commercial banks is influenced by internal and external factors. The main internal influencing factors are equity structure, the board size, non-interest income, innovation level, and quality of financial information. Gu and Yan (2020) concluded that there is a positive U-shaped relationship between equity concentration and bank risk-taking, and that board size increases bank risk-taking. Abou-El-Sood (2021) found that female bank directors tend to take higher risks when they perceive that venture capital will bring positive returns. Zhao (2021) believed that the development of non-interest income business significantly increases the risk level of the overall banking sector. Jiang and Wu (2020) pointed out that moderate bank innovation can weaken risk-taking. Lu and Song (2020) showed that the more opaque a bank is, the more risk it takes.

In terms of external factors, the main ones are industry competition, economic policies, and capital regulation. Niinimaki (2004) and Bahri and Hamza (2020) found that intense industry competition stimulated the risk-taking behavior of commercial banks. Regarding the relationship between economic policy and commercial banks’ risk-taking, L. Li and Huang (2022) found that monetary policy uncertainty increases commercial banks’ NPL ratio. Ma and Yao (2021) and others indicated that accommodative monetary policies stimulate bank credit expansion resulting in higher levels of risk-taking. Capital regulation can dampen banks’ risk-taking (Gu & Yan, 2020; M. S. Khan et al., 2017).

Research Related to the Risk-Taking of Commercial Banks by Internet Finance

Regarding the research on the impact of Internet finance on the risk-taking of commercial banks, some scholars believed that Internet finance would increase the risk-taking level of commercial banks. Based on the perspective of four major functions of Internet finance (Merton & Bodie, 1995): payment and settlement, resource allocation, information processing, and risk control, P. Guo and Shen (2015) concluded that Internet finance divides the profit margin of commercial banks, and banks increase their risk level in order to expand their revenue and its sources. P. Guo and Shen (2019) found that Internet finance aggravates the risk-taking level of commercial banks by worsening the deposit structure and increasing interest payment costs. S. Li and Xu (2020) concluded that the positive relationship between the two is more significant in systemically important banks. Yang et al. (2020) considered that in the context of fintech, commercial banks maintain their performance by lowering their asset review standards, and thus their own credit risk level increases.

However, some other scholars believed that Internet finance weakened the risk-taking level of commercial banks. He et al. (2017) concluded that the penetration of Internet technology has effectively reduced the information asymmetry between banks and customers, thus reducing the level of risk-taking. X. Sun et al. (2021) concluded that fintech can suppress bank risk and improve risk tolerance. J. Yu and Wu (2021) showed that for commercial banks as a whole, digital finance brings positive external spillovers and suppresses systemic risk, with urban commercial banks and agricultural commercial banks being more significantly affected.

A few other scholars believed that the two showed a nonlinear relationship. K. Wang et al. (2017) concluded that in the initial stage, the relationship between Internet finance and commercial banks is mainly competitive, and the risk-taking of commercial banks is increased through competitive effects, but this effect is reduced by later bank controls. S. Wang et al. (2021) pointed out that the relationship between Internet finance and bank risk-taking is not linear, and that state-owned banks lag behind urban commercial banks and agricultural commercial banks in their response due to asset size or policy protection.

Through the above literature, it can be seen that although scholars agree that Internet finance has an impact on commercial banks, the following questions remain to be further addressed: first, for urban commercial banks, the subdivision of commercial banks, is the impact of the development of Internet finance on their risk-taking level beneficial or detrimental? Second, is there any heterogeneity in the impact of Internet finance on the risk-taking of different types of urban commercial banks? Third, previous studies have generally found that Internet finance has an impact on the risk-taking of commercial banks, but they have not studied the path of the impact of Internet finance on the risk-taking of urban commercial banks in-depth to explore how urban commercial banks themselves should respond to the impact brought by Internet finance.

Based on this, this paper takes urban commercial banks as research objects, and after analyzing the overall impact of Internet finance on urban commercial banks’ risk-taking, heterogeneous impact analysis is conducted according to whether urban commercial banks are listed or not and whether they operate across regions or not. Further, based on the business-side perspective of urban commercial banks, the paths of the effects of Internet finance on the risk-taking of urban commercial banks are explored from three perspectives: asset, liability, and intermediate service side, respectively.

Hypotheses

Internet Finance and Risk-Taking of Urban Commercial Banks

Based on the long tail theory (Anderson & Andersson, 2013), Internet finance provides more convenient and efficient financial services such as investment, lending, payment, and settlement, which meets the diversified investment and financial needs of the public. Relying on a large market of ordinary consumers, Internet finance has been able to grow. Its development has broken the monopoly position of traditional banks. As a result, the competitive pressure on commercial banks has risen. According to financial vulnerability theory (Minsky, 1982), the competitive pressures and erosion of the safety boundaries of financial institutions brought about by Internet finance increase the vulnerability of commercial banks. Thereby commercial banks assume a higher level of risk.

Combined with existing studies, the development of Internet finance has led to the narrowing of deposit and lending spreads for commercial banks (Gu & Yang, 2018) and shrinking profit margins. To expand earnings and their sources, commercial banks will increase their own risk levels (P. Guo & Shen, 2015). At the same time, the development of Internet finance has accelerated the pace of financial liberalization, which has exposed commercial banks to a more intense market environment, which in turn has stimulated them to take higher levels of risk (S. Li & Xu, 2020). Compared with other commercial banks, city commercial banks are smaller in size and have a more relaxed risk prevention and control system. And it has a high overlap with the Internet finance customer base, which is more exposed to risks (Z. Liu, 2016).

Based on the above analysis, the following hypothesis is proposed:

H1: Internet finance has increased the risk assumption of city commercial banks.

Internet Finance Heterogeneity and Risk Assumption by Urban Commercial Banks

Listed urban commercial banks are characterized by large asset size, rich business, many outlets, and strong risk control ability (W. Wen & Wang, 2021). Under the external impact of Internet finance, they have a solid adjustment ability to face it, so as to achieve the effect of risk diversification and minimize the level of risk borne by themselves (Markowitz, 1967). At the same time, listed city commercial banks are under even greater regulatory pressure. Credit decisions under the regulation will be more prudent. In contrast, non-listed city commercial banks are usually smaller and subject to less regulation than listed ones (B. Zhang, 2020). Under the impact of Internet finance, non-listed city commercial banks are less able to adjust and adapt (W. Wen & Wang, 2021). Their credit decisions tend to be aggressive due to weak regulation, which increases their level of risk-taking.

Therefore, based on the above analysis, the following hypothesis is proposed:

H2a: Compared with listed city commercial banks, the impact of Internet finance on the risk assumption of non-listed city commercial banks is more significant.

Cross-regional operation or not makes a difference in the response of urban commercial banks themselves when facing external shocks. Compared with non-cross-regional operations, firstly, cross-regional operations lead to a greater tendency for urban commercial banks to make aggressive behavioral decisions in the face of greater competitive pressure (Feng & Hong, 2018). Secondly, cross-regional operations weaken the local advantages of urban commercial banks, which may reduce their understanding of the new environment they are in (Feng & Hong, 2018). Thirdly, cross-regional operations increase the commercial banks’ management structure complexity, which in turn leads to information lag and serious information asymmetry problems in their risk management under the impact of Internet finance (X. Sun et al., 2021). As a result, the trans-regional operation assumes a higher level of risk.

Based on the above analysis, the following hypothesis is proposed:

H2b: Compared with urban commercial banks that do not operate across regions, Internet finance has a more significant impact on the risk-taking of urban commercial banks that operate across regions.

Impact Path Analysis

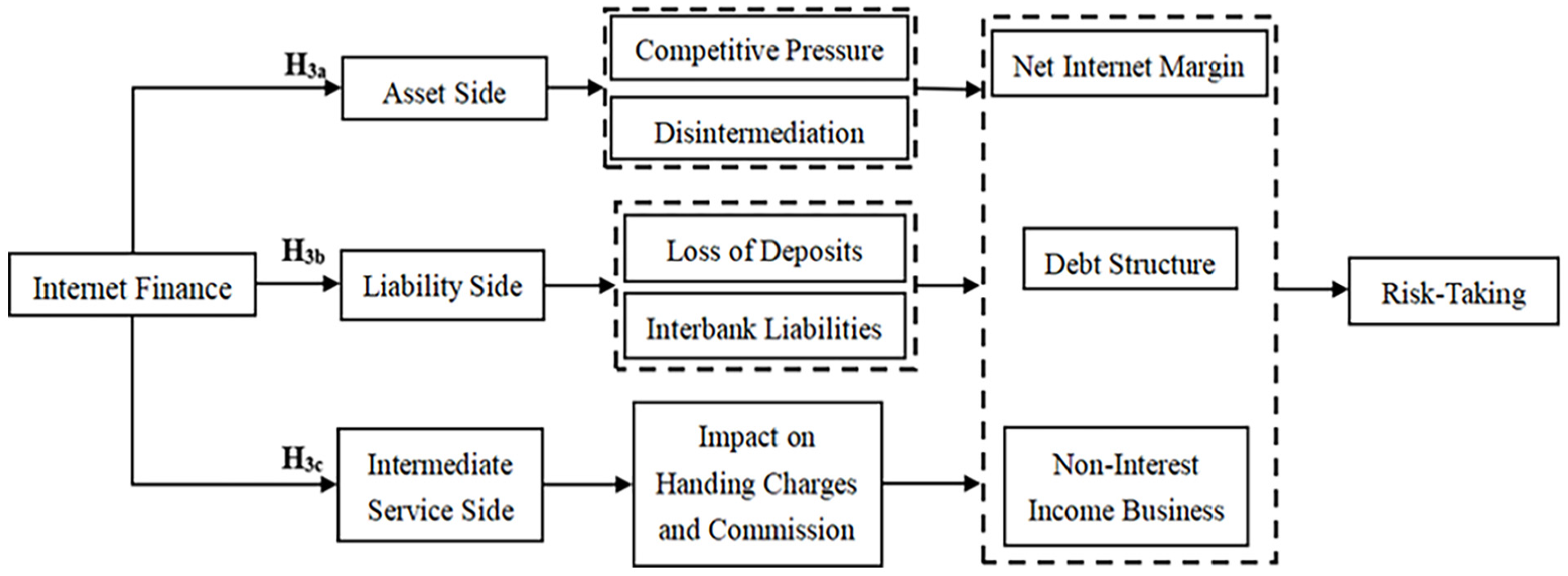

The development of Internet finance has an impact on the asset side, liability side, and intermediate service side of urban commercial banks, which in turn affects their risk-taking level (Fu & Pei, 2022).

On the asset side, urban commercial banks mainly operate in the loan business. Net interest margin is the main source of bank income and reflects the earning capacity on the asset side (Shang & Li, 2019). According to financial function theory, credit resource allocation is one of the functions of urban commercial banks (Merton & Bodie, 1995). Compared with city commercial banks, Internet finance provides more open resources and has lower peer-to-peer transaction costs. It achieves a more efficient resource allocation efficiency and disintermediates both sides of the transaction. This causes a diversion of customer resources and lower net interest income for city commercial banks (M. Liu & Wang, 2021). Combined with financial vulnerability theory (Minsky, 1982), when facing increased competitive pressure and lower net interest margin, in order to improve their own profitability, urban commercial banks will experience a profit-seeking effect (Kang & He, 2018; Z. Liu, 2016), and tend to make imprudent lending decisions, increasing the vulnerability of the institution. Thereby, their own risk-taking level is raised (C. Li & Wei, 2020).

On the liability side, Deposit liabilities and non-deposit liabilities constitute the liability structure of urban commercial banks, and non-deposit liabilities mainly refer to wholesale financing such as interbank liabilities. Urban commercial banks are mainly engaged in the deposit business. The financial products brought by Internet finance offer a diversity of choices other than deposits and can even offer financial products that are more convenient and more profitable than banks (Xiong et al., 2021). According to the financial function theory (Merton & Bodie, 1995), it creates a certain substitution for city commercial banks in the performance of its functions, which leads to the loss of its deposits. When it becomes more difficult to obtain deposits, city commercial banks tend to borrow from other banks to maintain liquidity, leading to a rise in the proportion of interbank liabilities (X. Liu et al., 2020). On the one hand, city commercial banks that borrow from peers generally enjoy an implicit government guarantee, which increases the vulnerability of banks (L. Liu & Li, 2021). On the other hand, interbank liability funding is large and has a short maturity structure (Gorton & Metrick, 2012). In the face of external uncertainty, the interbank sector tends to redeem early, which leads to severe interbank runs (T. Sun & Liu, 2021). The risk-taking level of city commercial banks is thus raised (J. Sun & Dai, 2020).

On the intermediate service side, urban commercial banks mainly focus on non-interest income business. According to portfolio theory, when the returns of two investments are not perfectly correlated, then the portfolio composed of these two investments has the effect of risk diversification (Markowitz, 1967). Non-interest income is earned through fees and commissions charged by city commercial banks and through investment activities. It can be regarded as a combination of investment income that is not fully correlated with interest income and can serve as a risk diversifier (W. Wang & Dong, 2016). If one of the incomes decreases, the effect of risk diversification is diminished. Internet finance third-party payment business models continue to innovate and payment methods become more convenient (Zheng, 2015), to meet the diversified needs of customers. As the acceptance of third-party payment software by the general public increases, banks’ fees and commission income gradually flow to third-party software (M. Liu & Wang, 2021). The development of Internet finance has resulted in lower non-interest income and lower risk diversification for the city commercial banks. As a result, the level of risk-taking of the city commercial banks was increased.

In summary, at different business sides of city commercial banks, Internet finance affects risk-taking paths differently. Therefore, the following assumptions are proposed from different business-side perspectives (Figure 4):

H3a: On the asset side, Internet finance has increased the risk assumption of city commercial banks by affecting their net interest margin.

H3b: On the liability side, Internet finance has increased the risk assumption of city commercial banks by affecting their debt structure.

H3c: On the intermediate business side, Internet finance has increased the risk assumption of city commercial banks by influencing their non-interest income.

Influence path diagram of different business sides.

Variable Selection and Model Setting

Research Samples and Data Sources

This paper selects all the relevant data of urban commercial banks from 2011 to 2020 as research samples. From the asset side, liability side, and intermediate business side, we clarify the impact mechanism of Internet finance on the risk assumption of urban commercial banks. In order to ensure the validity of the data and the accuracy of the conclusions, this paper screens the data according to the following criteria: (1) delete the city commercial banks with severe data loss, (2) delete the city commercial banks that went bankrupt during the sample period. Finally, obtained A total of 450 sample observations from 62 city commercial banks were non-balanced panel data. The data of relevant city commercial banks mainly comes from the Wind database, Oriental Wealth Network, and so on. The data is also necessary supplement through the manual collection and collation of the annual reports of various city commercial banks. The relevant data of Internet finance includes two parts: First, the provincial inclusive financial index published by Peking University, which is matched with the province where each city commercial bank is registered after obtaining the index. Second, in the robustness test, the basic data of the Internet financial index synthesized by the factor analysis method mainly relies on the “China Core Newspaper Databases (CCND)” to manually organize and pass EXCEL, SPSS, and other software for processing. At the same time, all variables are winsorized in this paper to reduce the influence of extreme values on empirical results.

Variable Definitions

Dependent Variable-The Risk of Urban Commercial Banks

Risk-weighted asset ratio (W. Yu & Zhou, 2018), non-performing loan ratio (S. Wang et al., 2021), and Z-value (P. Guo & Shen, 2019; S. Li & Xu, 2020; J. Yu & Wu, 2021) are the main measures of risk-taking of urban commercial banks. However, the data related to risk-weighted assets of urban commercial banks are fragmented and the NPL ratio does not reflect the overall risk. Therefore, combining the applicability of indicators and the availability of data, this paper uses the Z value to measure the risk appetite of urban commercial banks. The Z value is calculated as follows:

Independent Variable-Internet Finance

There are two main ways to measure Internet finance in existing relevant academic research: one is the direct indicator method (Gu & Yan, 2019), another is the comprehensive index method, which is mainly a synthetic Internet financial development index (P. Guo & Shen, 2019; S. Li & Xu, 2020; Z. Liu, 2016) and a Peking University Inclusive Finance Index (M. Liu & Wang, 2021). The comprehensive index method can better represent the overall development level of Internet finance compared with the direct index method. And this study is based on the overall level of Internet financial development. So the comprehensive index method is selected in this research. Meanwhile, the inclusive finance index released by Peking University has a high authority. Therefore, this paper selects the Peking University Financial Index to measure Internet finance.

Mediation Variables

This paper clarifies the role path of Internet finance affecting the risk assumption of urban commercial banks from the asset side, liability side, and intermediate business side. Based on different paths, the selected intermediary variables are as follows:

Net interest margin

On the asset side, the asset business of city commercial banks is mainly loans, and loans are the interest-bearing assets of banks, and the size of the net interest margin generated by them will have a certain impact on risk-bearing. Based on C. Li and Wei (2020), on the asset side, the net interest margin is selected as the intermediary variable of the asset side of the city commercial bank. The symbol is NIM.

2. Liability structure

On the liability side, the liability business of city commercial banks is mainly deposits. Still, in recent years, some non-deposit liabilities have also been added, and the composition of the two has changed the debt structure of banks. Based on J. Sun and Dai (2020), on the liability side, this paper selects the debt structure as the intermediary variable of the liability side of the urban commercial bank and measures the debt structure by the ratio of interbank liabilities to total liabilities, which is symbolized by BLS.

3. Non-interest income business

On the intermediate business side, the intermediate business of city commercial banks is mainly a non-interest income business. Based on Zhao (2021), on the intermediate business side, this paper selects the non-interest income business as the intermediary variable of the intermediate business side of the city commercial bank, with the symbol NII.

Control Variables

In summary, based on Bahri and Hamza (2020), Konishi and Yasuda (2004), S. Wang et al. (2021), and J. Yu and Wu (2021), this paper selects variables such as loan loss reserve adequacy ratio, loan allocation ratio, equity concentration, monetary policy, cost-to-income ratio, and loan growth rate as the control variables of empirical research (Table 2).

Variable Definitions.

Model Setting and Method Selection

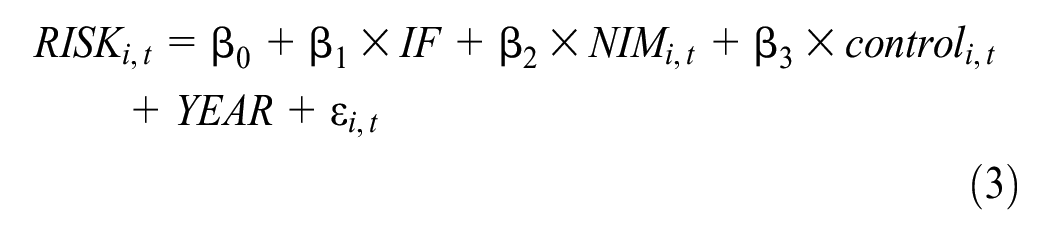

In order to test H1, H3a, H3b, and H3c, we establish the model (1) to (7) based on Z. Wen, Zhang, Hou, and Liu (2004).

In order to discuss the relationship between Internet finance and the risk-taking of city commercial banks, the following regression model is constructed:

To explore whether net interest margin is the intermediary mechanism by which Internet finance affects city commercial banks’ risk-taking on the asset side, we constructed the following regression model:

To explore whether debt structure is the intermediary mechanism by which Internet finance affects city commercial banks’ risk-taking on the liability side, we constructed the following regression model:

To explore whether non-interest income is the intermediary mechanism by which Internet finance affects city commercial banks’ risk-taking on the intermediate business side, we constructed the following regression model:

In the above model,

In order to test H2a and H2b, we use a grouping approach. Urban commercial banks are divided into listed group and non-listed group according to whether it is listed or not. They are divided into trans-regional group and non-trans-regional group according to whether to operate across districts. Regression analysis was conducted for model (1).

Empirical Analysis

Descriptive Statistics

Table 3 shows the descriptive statistical results for all variables in this article. The mean value of the risk assumption (RISK) is 4.38, the minimum value is −1.017, and the maximum value is 7.217. It indicates that there are large differences in the operational stability of commercial banks in various cities in China, and they bear different risk levels. From the descriptive statistical results of the internet financial development index (IF), it can be analyzed that China’s Internet finance has developed to a certain extent from 2011 to 2020. The maximum value of IF is 6.068, the minimum value is 2.916, and the standard deviation is 0.606. There is a significant difference between the maximum and minimum values, which indicates that China’s Internet finance is not in a stable state of development. This may be related to the degree of supervision of China’s Internet finance at different stages of development.

Descriptive Statistics.

In the descriptive statistical analysis of the intermediary variables, from the perspective of the asset side, the maximum value of the NIM is 6.900% and the minimum value is 0.707%, indicating that there are large differences in the net interest margin of each city commercial bank. From the perspective of the liability side, the proportion of inter-bank liabilities in the debt structure of urban commercial banks (BLS) has an average value of 8.978%, indicating that in the selected sample of city commercial banks, each city commercial bank has carried out a certain degree of inter-bank lending, while the maximum value of inter-bank liabilities is 48.22% and the minimum value is 0.003%, indicating that in terms of the debt structure of urban commercial banks, the proportion of inter-bank liabilities varies greatly. From the perspective of intermediate service, the average proportion of non-interest income is 20.491%, the minimum value is 5.045%, and the maximum value is 76.914%, indicating that in the business development of China’s urban commercial banks, non-interest income business accounts for a certain proportion, and the proportion of the non-interest income of various banks also varies greatly.

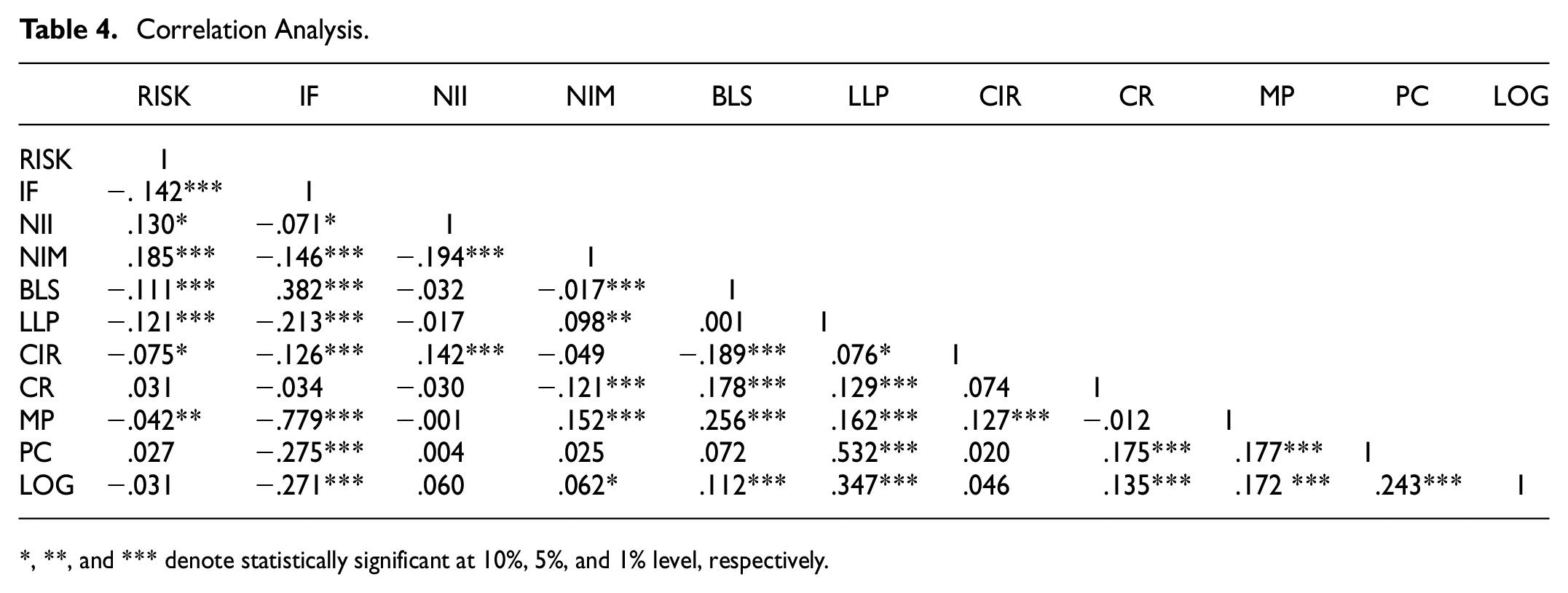

Correlation Analysis

In this paper, all variables are tested for Pearson correlation. From Table 4, the preliminary conclusions are as follows: Internet finance (IF) and risk-taking (RISK) are significantly negatively correlated at the level of 1%, and it can be judged that the development of Internet finance has aggravated the risk-taking level of urban commercial banks, assuming that H1 is initially verified.

Correlation Analysis.

, and *** denote statistically significant at 10%, 5%, and 1% level, respectively.

The correlation test of intermediary variables shows that Internet finance (IF) and net interest margin (NIM) are significantly negatively correlated at the level of 1%; Internet finance (IF) and debt structure (BLS) are significantly positively correlated at the level of 1%; Internet finance (IF) and non-interest income (NII) are significantly negatively correlated at the level of 10%. In summary, Internet finance has a good correlation with intermediary variables. It preliminary shows that the mediating chosen variables are appropriate in this paper, which can be analyzed in the next step.

Regression Analysis

From Table 5, it can be seen that the regression coefficient of Internet finance (IF) and risk assumption (RISK) is 0.3774, and a significant negative correlation at the level of 1%. It shows that the development of Internet finance has increased the risk-taking of urban commercial banks as a whole. The competitive pressure brought about by Internet finance, and the erosion of the security boundaries of financial institutions have increased the vulnerability of commercial banks and made banks take more risks (S. Li & Xu, 2020). At the same time, the lax risk prevention and control system of city commercial banks and the high overlap with the customer base of Internet finance make them more exposed to risks (Z. Liu, 2016). H1 is verified.

Regression Results.

, and *** denote statistically significant at 10%, 5%, and 1% level, respectively.

The city commercial banks are grouped according to different listing conditions. The regression coefficient of Internet finance (IF) and risk-taking (RISK) in the listed group is −0.3754, but it does not pass the significance test. In the sample regression results of non-listed city commercial banks, the regression coefficient of Internet finance (IF) and risk-taking (RISK) is −0.3291 and has a significant correlation at the level of 5%. This shows that compared with listed banks, the impact of Internet finance on the risk assumption of non-listed city commercial banks is more significant. This may be because listed city commercial banks have the characteristics of large asset scale, rich business, numerous outlets, and strong risk management and control capabilities under the external impact of Internet finance (W. Wen & Wang, 2021). It has a strong ability to adjust to facing external shocks, so as to achieve the effect of dispersing risks and minimize the level of risks it bears (Markowitz, 1967). At the same time, listed city commercial banks face greater regulatory pressure. The more perfect disclosure system also strengthens investors’ supervision of the steady operation of city commercial banks, when city commercial banks change their credit decisions due to the competitive pressure of Internet finance, out of the supervision of investors, the credit decisions made will be more prudent. Unlisted banks have the characteristics of small asset scale, concentrated outlets (B. Zhang, 2020). Under the impact of Internet finance, the adjustment and adaptability of unlisted banks are weak (W. Wen & Wang, 2021). The credit decision-making under the impact will also promote the motivation to take the initiative due to the lack of sufficient supervision, thereby improving their own risk-taking level. Therefore, H2a is verified.

In the sample of urban commercial banks that conduct the inter-regional operation, the regression coefficient of Internet finance (IF) and risk-taking (RISK) is −0.7695, and it is significantly correlated at the level of 1%. In the sample of urban commercial banks without trans-regional operation, the coefficient of Internet finance (IF) and risk-taking (RISK) is −0.3252. Although it passes the significance test, the significance level and correlation coefficient are far lower than that of the sample group of urban commercial banks with the trans-regional operation. It shows that the aggravating effect of Internet finance on the risk-taking of urban commercial banks is more significant in urban commercial banks that carry out the trans-regional operation. This is because compared with urban commercial banks that do not operate across regions, urban commercial banks that operate across regions have more complex management structures, and their original local advantages are weakened (Feng & Hong, 2018). When facing the impact of Internet finance, they will face wider impact and competitive pressure due to the establishment of branches in different places. Moreover, the geographical distance between the head office and branches also aggravates the lag of information (X. Sun et al., 2021), making it more difficult to reflect and adjust quickly under external shocks. Therefore, compared with urban commercial banks that do not operate across the region, Internet finance has a more significant impact on the risk-taking of urban commercial banks that operate across the region. H2b has been verified.

Mediation Effect Regression Test

Table 6 shows the results of the mediation effects test. From the regression results of the first column, it can be concluded that the regression coefficient of Internet finance (IF) and risk-taking (RISK) is significantly negative. The next step of analysis can be carried out.

Mediating Effects Regression Test Results.

, and *** denote statistically significant at 10%, 5%, and 1% level, respectively.

From the regression results of the second column with net interest margin as the explanatory variable, Internet finance (IF) and net interest margin (NIM) are significantly negatively correlated at the level of 10%, indicating that Internet finance has reduced the net interest margin of urban commercial banks. The more efficient resource allocation efficiency offered by Internet finance has caused a diversion of customer resources from urban commercial banks. This has resulted in lower net interest income for urban commercial banks (M. Liu & Wang, 2021). In the third column, the regression coefficient between the net interest margin (NIM) and risk assumption (RISK) is 0.2080, and it is significantly correlated at the level of 1%. From the results, it can be concluded that the smaller the value of NIM and the lower the value of RISK, the higher the risk-taking level of urban commercial banks. This indicates that there is a significant negative correlation between the net interest margin and the risk-taking level of urban commercial banks. When net interest income decreases, in order to improve their own earnings, urban commercial banks will experience a profit-seeking effect (Kang & He, 2018; Z. Liu, 2016) and tend to make imprudent lending decisions. As a result, the level of own risk-taking increases (C. Li & Wei, 2020). Net interest margin acts as a partial mediation effect between Internet finance and the risk-taking of urban commercial banks, not a full mediation effect, which verifies hypothesis H3a.

It can be seen from the regression results of the fourth column of Internet finance and debt structure that the regression coefficient of Internet finance (IF) and debt structure (BLS) is 5.6914, and it is significantly correlated at the level of 1%. This indicates that under the impact of Internet finance, the proportion of inter-bank liabilities in the debt structure of urban commercial banks has increased. This is because Internet finance has diverted the deposit scale of urban commercial banks, and the difficulty of banks pulling deposits has increased, relying on non-deposit funds instead, increasing the proportion of inter-bank liabilities in the debt structure (X. Liu et al., 2020). The regression coefficient between the debt structure (BLS) and risk assumption (RISK) is -0.0252, which is significantly correlated at the level of 1%, indicating that in the debt structure of urban commercial banks, the greater the proportion of inter-bank liabilities, the higher the risk level borne by the bank. The large amount and short maturity structure of interbank liability funding (Gorton & Metrick, 2012) lead to a greater susceptibility to interbank runs in the face of external environmental shocks (T. Sun & Liu, 2021). At the same time, urban commercial banks that borrow from the interbank generally enjoy the implicit guarantee of the government (L. Liu & Li, 2021). This all adds to the level of risk-taking of urban merchant banks. The regression coefficient between Internet finance (IF) and risk assumption (RISK) in the fifth column is still significant, indicating that the debt structure shows a partial intermediary effect in the impact of Internet finance on the risk-taking of urban commercial banks, which verifies H3b.

It can be seen from the regression result of the sixth column, the regression coefficient of Internet finance (IF) and non-interest income (NII) is −2.8774. There is a significant correlation, indicating that under the impact of Internet finance, the non-interest income business has suffered a negative impact. Because Internet finance has diverted the income of city commercial banks’ wealth management products with its diversified wealth management products and the diversity of independent choices (Zheng, 2015), reducing non-interest income such as bank investment income and handling fees (M. Liu & Wang, 2021). From the regression results of the seventh column, it can be seen that the regression coefficient of non-interest income (NII) and risk assumption (RISK) is 0.0046, which is significant at the 10% level. It can be concluded that the higher the value of NII and the higher the value of RISK, the lower the risk-taking level of urban commercial banks. There is a significant negative correlation between non-interest income and the risk-taking level of urban commercial banks. This is because the risk diversification of non-interest income (W. Wang & Dong, 2016) reduces the risk level of urban commercial banks. The regression coefficient of Internet finance (IF) and risk-taking (RISK) in the seventh column is still significant, indicating that the non-interest income business shows a partial intermediary effect in the impact of Internet finance on the risk burden of urban commercial banks, which verifies H3c.

Robustness Testing

To ensure the robustness of the empirical results, the article changes the variable measurement method to conduct a robustness test. Based on P. Guo and Shen (2019), factor analysis is used to synthesize an index to measure Internet finance.

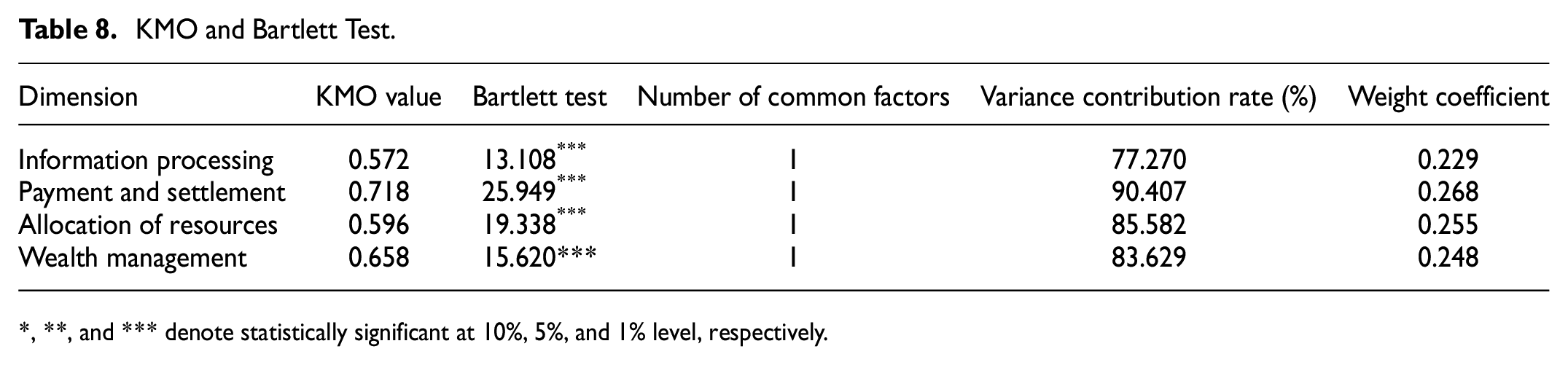

The specific steps are as follows: (1) Collate relevant original thesaurus. Based on the concept of the financial function (Merton & Bodie, 1995), we establish initial keywords for the four dimensions of clearing and payment, resource allocation, wealth management, and information processing, totaling 12 relevant keywords (Table 7). By using “China Core Newspaper Databases” to manually collate the number of news releases from 2011 to 2020 with each keyword, we calculate the annual word frequency of each keyword. (2) Obtain the Internet finance Index by the factor analysis method. We use SPSS software to conduct factor analysis on standardized word frequencies and test the results of factor analysis. From Table 8, it can be seen that the KMO values of the four functional dimensions are all greater than 0.5, and the Bartlett tests of them are significant at the 1% level. So we can conclude that the data is suitable for factor analysis. The common factor variance contribution rates extracted in a manner where the feature value is greater than 1 are all greater than 75%, indicating that the extracted common factor can reflect most of the original information.

Internet Finance Basic Lexicon.

KMO and Bartlett Test.

, and *** denote statistically significant at 10%, 5%, and 1% level, respectively.

To sum up, we have obtained the comprehensive development index of Internet finance:

Table 9 shows the results of our robustness test using the Internet Finance Comprehensive Development Index. After comparing with the previous research, we conclude that the conclusions obtained in this article are robust.

Robustness Tests.

, and *** denote statistically significant at 10%, 5%, and 1% level, respectively.

Conclusions and Recommendations

This paper discusses the risk assumption of urban commercial banks based on the research sample of 62 city commercial banks in China from 2011 to 2020. The results show that Internet finance increases the risk-taking of urban commercial banks. This impact shows heterogeneity due to the listing of urban commercial banks. The net interest margin, debt structure, and non-interest income show an intermediary effect when Internet finance affects the risk assumption of urban commercial banks.

On the theoretical side, this study takes urban commercial banks as research objects, analyzes the impact of Internet finance on their risk-taking level, and further explores its path of action, thus enriching the research related to the risk-taking of urban commercial banks and increasing the practicality of the research findings. Previous studies have explored the impact of Internet finance on commercial banks (Fu & Pei, 2022; Gu & Yan, 2019; J. Guo et al., 2022; P. Guo & Shen, 2019; M. Liu & Wang, 2021; Pei & Fu, 2020). However, there is little literature on exploring the impact of Internet finance on urban commercial banks as a main subject. Among the studies on the impact of Internet finance on commercial banks’ risk-taking, there are fewer studies on the paths of influence.

This study also has important practical significance: for urban commercial banks, it is beneficial for them to correctly understand the impact brought by Internet finance and the channels of the impact of Internet finance on their own risks. This enables them to change their business strategies according to their own characteristics and guide the impact of Internet finance on urban commercial banks’ risk-taking from negative to positive. For regulatory authorities, the results of this study help them to better understand the impact of Internet finance on urban commercial banks. This allows the regulatory authorities to implement precise financial regulatory instruments to effectively guide the positive impact of Internet finance and promote the healthy development of Internet finance and urban commercial banks with a full understanding of the current development of Internet finance and urban commercial banks.

In the meantime, we offer some suggestions.

For urban commercial banks, firstly, they should face up to their own disadvantages, pay attention to the comparative advantages of Internet finance, and realize their own development. City commercial banks should seize their geographical advantages, integrate with Internet finance, carry out business innovation, provide special services for local customers, and improve their competitiveness. Secondly, urban commercial banks with different development statuses should take corresponding measures according to their own situation. On the one hand, listed banks should take advantage of their scale, absorb and train high-level talents, and introduce advanced technology of Internet finance; non-listed banks should pay attention to their own risk control and improve their management structure and governance mechanism by learning from the experience of listed city commercial banks. On the other hand, urban commercial banks operating across regions have achieved business expansion. So they should strengthen internal control construction, promote information communication between head office and branches, and achieve rapid response to external shocks; non-cross-region urban commercial banks with local advantages should seize their own advantages, implement differentiation strategies, and create special financial services. Finally, they should start from the existing business and stabilize their own development. On the asset side, they can use Internet technology to improve the convenience of loan services. On the liability side, they can innovate financial products and provide corresponding products for different customers to increase the diversity of customer choices. On the intermediate service side, based on local advantages, they can provide customized services for local customers to enhance customer stickiness.

For policy makers, on the one hand, they should identify new financial products and potential risks promptly, and on the premise of combining the development status of Internet finance and city commercial banks, formulate precise and effective policies to provide a benign competitive environment for the development of Internet finance and city commercial banks to maintain the stability of the financial system. On the other hand, urban commercial banks should be encouraged to make use of Internet technology to enhance their own Internetization, thus guiding the negative effects of Internet finance into positive ones and promoting the benign development of Internet finance and the urban commercial banking industry.

For regulators, firstly, they should promptly identify the risks brought by new financial products and new business models, scientifically and reasonably define the scope of business, market access, penalties for violations, information disclosure, and so on, and amend and improve the financial regulatory system. Secondly, they should understand the latest developments in Internet finance, identify potential risks promptly, strengthen risk prevention and control, use advanced technologies such as the Internet to quantitatively analyze and classify risk indicators, and implement different regulatory measures for different levels of risk. Thirdly, they should follow the principle of moderate regulation, encourage innovation and development under the premise of strengthening risk prevention and control and enhancing regulation, and strictly prevent all kinds of risks while promoting the “catfish effect” of Internet finance.

Limitations and Future Research

There are some limitations in this study. Firstly, in terms of research content, Internet finance is divided into the financialization of Internet companies and the Internetization of the traditional financial industry (A. Zhang, 2015). Based on the perspective of the financialization of Internet companies, we studied the impact of Internet finance on the risk-taking of urban commercial banks, ignoring the degree of Internetization of urban commercial banks themselves. This is because it is harder to measure the level of Internetization of banks themselves, resulting in fewer relevant studies. Secondly, for the sample selection, there are 62 Chinese city commercial banks, of which listed banks account for 37% of the total. Listed banks account for a minority of the total number of banks, which makes it more difficult to obtain sample data, and the total sample of the study is smaller, which may affect the findings of the study. Finally, for the indicator measurement, we use factor analysis to generate the Internet finance index in the robustness test. The data of this method are obtained by a manual collection of relevant keywords, in which the selection of keywords is somewhat subjective. This may make the generated Internet finance index inaccurate from the actual one, which may have some influence on the research results.

Future research could explore the following aspects: on the one hand, we focus on the impact of the financialization of Internet companies on the risk-taking of urban commercial banks. With the development of the Internet, the traditional financial industry’s level of Internetization is rising, which may also affect the risk-taking level of urban commercial banks. Therefore, in the future, the relationship between the two could be studied from the perspective of the level of Internetization of the traditional financial industry. On the other hand, how city commercial banks should use the advantages of Internet finance to promote their own development is an issue worthy of further study in the future as Internet finance changes to the development trend today.

Footnotes

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: This paper was supported by the Postgraduate Innovation and Practice Ability Development Fund of Xi’an Shiyou University [YCS23113102].

Ethical Statement

This paper does not focus on specific human subjects such as patients or patients’ parent/carer and addresses no private information of human subjects. No consent is needed and applicable.