Abstract

This study analyses, firstly, the achievement of local governments’ reform based on their Performance Accountability System (SAKIP) as part of the national administrative reform program in Indonesia. Secondly, this paper examines factors that have been affecting reform output. The study uses a mixed method perspective by analyzing the whole population of local governments from SAKIP data (2016–2019; quantitative) and applies the qualitative method of in-depth interviews with key informants. The study finds that, although there were improvements in the performance accountability system, the improvement processes have been slow and dominated by formalism at provincial and regency/city levels. Several determining factors affected the implementation of the local government performance accountability system, that is, the regulations’ arrangements, the norms, the cognitive culture, and management problems. Thus, this study confirms the theory of institutional change that considers cultural factors, political commitment, and organizational aspects that influence the dynamic of bureaucratic reform implementation.

Keywords

Introduction

Various public sector institutional reform studies focus on issues around motivation and behavior in institutional change that involved formal and informal institutions (Leftwich & Sen, 2010). Public sector institutional reform needs to consider institutions’ components to address reform challenges such as priorities, policies, incentives, rules and law, culture, drivers for change, and voice and partnership (DFID, 2003 in Joshi & Carter, 2015). The urgency to consider the component of the institution is in line with the perspective of scholars on the institutional theory that identifies three pillars of an institution: regulative pillar, normative pillar, and cultural cognitive pillar (Scott, 2013). Various studies found formal and informal institutions that lie behind reform failure, such lack of financial incentives (Fritz et al., 2012), informal norms (Colignon & Usui, 2003), isomorphic mimicry (Andrews et al., 2017; Pritchett et al., 2010), clientelism (Leftwich & Sen, 2010), the capacity of individuals, organization, and institutional, and enabling environment (Berman, 2013).

One of the key trends in institutional reform agendas includes emphasizing decentralization to facilitate democratic decentralization strategies. Zhang and Chen (2015) confirm that the most significant means of enhancing local governance performance is to substantially enhance the transparency of governmental fiscal behaviors by putting them under the budget and supervision of the local legislature. Following decentralization, several local governments have implemented performance measurement and management systems to enhance accountability. Existing studies have found challenges in implementing local governments in developing countries to enhance performance management (Siti-Nabiha & Jurnali, 2020). Institutional work, particularly performance culture, influences the enhancement of performance-driven behavior at the local government level (Ateh et al., 2020). Hall (2017) identifies and elucidates a series of challenges local governments face in successfully implementing performance-based management approaches. Some of these obstacles are insufficient administrative capacity, inadequate strategic planning, and complex implementation environments.

A number of scholars and governments around the world have argued that decentralization offers numerous advantages (Cheema & Rondinelli, 2007; Rondinelli et al., 1983; Schiavo-Campo, 2019), though others have contradictory perspectives (Ahmad & Tanzi, 2002; Prud’homme, 1995). So, decentralization has mixed results in different cases. Ebinger et al. (2011) state that many of the theoretical assumptions about the effects of public sector reform are important to provide a better understanding of enabling factors of reform. The institutional reform also produces mixed, often disappointing results (Andrews, 2013; Independent Evaluation Group, 2008; The World Bank, 2011), placing developing countries in a challenging position. Grindle (2004) argues that governance reforms toward good governance principles are too much for developing countries, where most public sector institutions are still weak, inflating concepts or principles of good governance. These countries are in a deficit of these principles (Grindle, 2017).

Thus, this study aims to contribute through its findings by looking at the element of the institution that currently affects the implementation of performance measurement and management functions because each institution’s capabilities vary amid the push for reform in Indonesia. Indonesia is a developing country that has strengthened its decentralized system (Suharyo, 2009) and reforms (Wihantoro et al., 2015, p.46). Indonesia instituted radical decentralization reform in 1999. More government functions and taxations have been assigned to local government; more autonomy has been given to decide its local budget, more fund through the block grant system, independent local elections both for the executive and legislative branches, and a new kind of central-local relationship to strengthen local autonomy and abolished almost all central government agency at the local level except for few such as the central government tax office at all regions, immigration office which not been decentralized. These huge and fast change has been labeled as a big bang process (Ichimura & Bahl, 2008). Following the above reform, in 2003, there was a budget system reform for both central and local governments to adopt Performance Based Budgeting. In 2004, there was another reform on the Planning System for all government entities to adopt the strategic planning system, and in 2010, there was a systematic and targeted administrative (bureaucratic) reform for all levels of government. The targeted reform program has eight areas: public service quality, human resources management, control system, business process, organization structure, performance accountability system, legal or regulation arrangement, and change management.

Contextual Information on GOI’s Performance Accountability System

Following the 2010 reform, The Ministry of Administrative and Bureaucratic Reform (MoAB) has the authority to decide the technical aspect of implementing reform. Like many other countries, Indonesia believed that administrative reform through decentralization and governance reform would bring greater accountability for local government dynamics (Law No.22, 1999; President Regulation No. 81/2010). This study deals with administrative reform in building fiscal accountability, particularly in the planning and budgeting system, which the government of Indonesia (GoI) through MoAB regulation referred to as the “Government Performance Accountability System” (Sistem Akuntabilitas Kinerja Instansi Pemerintah (SAKIP)). Therefore, every rupiah spent on every activity should support or relate to the goals and objectives of related programs and targeted performance in annual and mid-term planning documents.

SAKIP is a Planning and Budgeting system integrating three main subjects as subsystems. First, strategic planning belongs to each local government (the 5-year planning); second, performance-based budgeting system; and third, performance management. To integrate the first and second sub-systems, the system builds the cascading process, which consists of programs, activities, and procedures to decide indicators and targets to measure the government’s performance. The above three main subjects are blended into one larger system called SAKIP or Government Performance Accountability System.

Therefore, SAKIP consists of developing strategic planning, performance agreement, performance measurement, performance data management, performance reporting, and performance evaluation and review. Each government institution, from the local government to the national level, needs to develop SAKIP. The MoAB has been annually evaluating the implementation of SAKIP since 2015. Indonesia is still using the 5-year planning system based on the strategic planning concept as the basis of development activities and for its budgeting system (Shafritz et al., 2017, p.526), as described by national law (GoI, Law on National Planning, No. 25/2004).

There are five main functions of SAKIP; the first is to sharpen the goals and targets, starting from the 5-year strategic planning (Rencana Strategis or “Renstra”), together with performance indicators designed for achieving specific outcomes. Within this document are visions and missions for local government, the policy setting and prioritizing of sectors and programs, and the targeted outputs and outcomes, all with clear key performance indicators for 5 years. The second function involves helping cascade the macro planning up to organizations and units of organization planning using the logic model (Poister, 2003) to produce integrated development planning for local governments. The third function is to cascade the “5-year planning” to the “annual planning” in a 5-year time, so there will be close linkages between each “annual planning” and its roots, the 5-year planning, and its program, activities, key performance indicators, and targets. The fourth function of SAKIP is cascading and using annual planning for budgeting. The final function of SAKIP is to design the monitoring and evaluation process for the performance and the money each local government spends.

These five functions should be linked very closely to one another; together, they became a system of performance accountability of government. Every rupiah spent on each activity should be linked or traceable to its program, both yearly and in 5-year plans, as well as being clear that it supports the targeted outputs and outcomes and for the mission and vision of the specific local government (Presidential Regulation Number 29/2014). This information can be analyzed in the fourth component, the report. SAKIP makes performance-based budgeting very powerful tools to create allocative efficiency (Schick, 1998) and has a very good capability to enhance accountability. For the local government in Indonesia, it means strengthening the local resource allocation and strengthening local government accountability. Therefore, performance management functions aim to bundle all functions together to create one system.

Administrative Reform

Undertaking an analysis of the government performance accountability system at local levels in Indonesia requires an in-depth review of administrative reform because strengthening the government’s performance accountability system is one of Indonesia’s key areas of administrative reform. Poorly functioning public sector institutions and weak governance are major constraints to growth and equitable development in several developing countries (The World Bank, 2000).

Administrative reform has been a key topic under discussion in Indonesia since the Grand Design of Bureaucratic Reform 2010 to 2025 was released under the umbrella of Presidential Regulation Number 81, 2010. Writing in the late 1970s, Caiden (1979) suggests a theoretical framework to clarify the scope of administrative reform. Before this point, administrative reform was part of the transformation in coping with resistance (Caiden, 1969). Administrative reforms aim to increase government capacity related to state apparatus, public sector productivity, public accountability, and control. Three proposed characteristics of administrative reform include the significant role of government across society, the essential contribution of effective policy implementation, and the importance of effective management under sound rational principles (Caiden, 1979). However, administrative reform efforts not only aim to strengthen the inside aspects of bureaucracy, the effectiveness, and the efficiency of bureaucracy but also strive to attain national development goals (Quah, 2010; Turner & Hulme, 1997). In developing countries, administrative reform deals with modernization and change to affect social and economic transformation (Farazmand, 2002).

Previous studies on the factors that encourage administrative reform in local governments are varied and have been sensitive to the data and the methodological framework used. One aspect of factors that encourage administrative reform, namely leadership, has been discussed in previous studies (Keuffer, 2018; Ruhil et al., 1999). Ruhil et al. (1999) found that city manager leadership was essential in accelerating governance efficiency and highlighted the role of city managers as modernizers and adopting reforms, although a city manager alone is no guarantee of reform (Ruhil et al., 1999). There are still numerous constraints, such as local political alignment and external environments, that could limit governments’ ability to reform (Ruhil et al., 1999; Turner et al., 2019).

Furthermore, the latitude of local policymaking can encourage administrative reform in local government. Keuffer (2018) found that, in Switzerland, local governments with a sufficient latitude of local policymaking are likely to take initiatives to enhance service delivery. With their ability to make policy, local governments will be able to know more about the structural problems and pressures that may lead to reforms (Keuffer, 2018). However, on the other hand, reform factors can depend on the size of the municipality and the type of actors involved; the larger the municipality, the larger actor or administration involved (Lockert et al., 2019).

A number of studies have investigated the effect of bureaucratic reforms on improving public services (Lapuente & Van de Walle, 2020; Slack & Singh, 2015). The reform of public management was found to enhance organizational performance. In the Indonesian context, the success of the reform agenda is affected by the quality of service and the implementation of good governance (Prasojo & Kurniawan, 2008). Furthermore, a positive association exists between bureaucratic reform and the implementation of good governance and organizational performance (Nofianti & Suseno, 2014). Research in Aceh Province found that using e-government and bureaucratic reforms has enhanced the implementation of good governance principles and improved organizational performance (Jauhari et al., 2020).

However, there is limited research on bureaucratic reform in Indonesia and its relation to government agencies’ performance accountability system. A study with an ethnographic approach in the Directorate General of Taxation underlined that Javanese culture influences mindsets and interactions between bureaucrats, including in implementing bureaucratic reforms (Wihantoro et al., 2015). A study at the Archival Institutions in Indonesia found that bureaucratic reform significantly affected the quality of service and implementation of good governance (transparency, accountability, responsiveness, independence, and fairness) but did not affect organizational performance (Kurniawati et al., 2019). The results of this study suggest that bureaucratic reform has not been fully able to encourage organizations to improve their performance.

Accountability and Performance Measurement

This study examines the reform of the local government performance accountability system to increase public sector accountability. Accountability is defined as the ability of the public sector to demonstrate performance or answerability (Romzek & Dubnick, 1987). Performance management is often a concern for private sector management (Johnson & Kaplan, 1987; Kaplan, 1983). However, the public sector is now paying close attention to performance management (Hood et al., 1998). Public sector reform requires performance management and measurement (Gianakis, 2002). Performance management is critical in measuring the achievement of outcomes important in generating support for the public sector (Osborne & Gaebler, 1992).

Performance management in the public sector in Indonesia began to develop after being introduced with the Performance Accountability Report of State Apparatus (LAKIP) in 1999, which was later developed into a government agency performance accountability system (SAKIP). In 2014, the President of Indonesia released President Regulation 29/2014 on the Government Performance Accountability System (SAKIP). This regulation aims to overcome the discussed problems, specifically increasing the quality of allocative efficiency in planning and budgeting and enhancing local government performance and accountability. Local governments from the regency, city, and provincial levels, as well as ministries and institutions, must implement SAKIP. SAKIP is expected as an integrated system and a bureaucratic reform movement to change the government system toward performance-based governance. In the grand design of bureaucratic reform (2010–2025), the GoI stated that bureaucratic reform was expected to achieve good governance goals reflected in the realization of a clean government, the improved quality of public services to the community, and increased capacity and accountability of bureaucratic performance. There are several areas of change to achieve these targets: organization, governance, legislation, human resources apparatus, supervision, accountability, public services, and work data apparatus. SAKIP has become an instrument to evaluate the achievement of the direction of accountability change in government in the framework of bureaucratic reform.

Research on performance management in the public sector in Indonesia has found that there still needs to be a gap between government authority and public expectations for the quality of public services (Riandi, 2003). Mahsun (2005) criticizes the lack of relevant performance indicators to measure failure and success in public services, showing a gap between public service performance and community expectations (Mahsun, 2005). Research on factors that affect the implementation of performance measurement in local governments in Indonesia has found that four organizational factors, namely metric difficulties, technical knowledge, management commitment, and legislative requirements, contributed to achieving performance indicators (Akbar et al., 2012). Among these organizational factors, regulatory factors have the most significant impact and demonstrate the effort to fulfill performance indicators at the local government level, which are still focused on meeting regulations in accordance with the mandate of the central government rather than efforts to improve the effectiveness and efficiency of government (Akbar et al., 2012). A quantitative study of intergovernmental efforts found that this effort was essential in enhancing performance management. This action includes local leaders’ awareness and commitment, technical assistance for increasing local government capacities, the incentive to implement performance management, and institutionalizing local efforts that deepen and broaden performance management practice (Ateh et al., 2020).

Institutionalizing Performance Management

Institutionalizing a performance-driven culture has become an important topic that attempts to improve public sector accountability. A recent study with the case study of Indonesia found that, in terms of institutionalizing performance management, the understanding of performance culture was important (Ateh et al., 2020). There have been efforts to identify the type of work done by local government public managers to institutionalize performance measurement and management mandated by the central government (Siti-Nabiha & Jurnali, 2020).

This research analyses the implementation of SAKIP by evaluating the influence of the three pillars of the institution (Siti-Nabiha & Jurnali, 2020), identifying the elements of each pillar, and considering the development of SAKIP on a yearly basis.

Institutional theory itself understands that institutions, that is, beliefs, rules, and norms, influence the design and conduct of an organization (Berthod, 2016). The organization’s efforts to conform to this institution aim to gain legitimacy, reduce uncertainty, and increase the intelligibility of the organization’s actions and activities (Berthod, 2016). The new institutionalism theory underlines a new direction focusing on the legitimacy that encourages or calls for organizations to adapt to the environment (Selznick, 1996). Regarding reform, institutionalism stresses the need to modify collective values, culture, and structure to make an organization adaptive and dynamic. The regulative pillar relates to regulation or laws that enforce behavior change through fear and coercion and is associated with monitoring and sanctioning. The normative pillar emphasizes normative rules that prescribe rights, privileges, responsibilities, and duties. Normative pillars arise driven by a shared sense that determines the appropriate or inappropriateness of an action or behavior. This pillar is associated with values, norms, work roles, and habits. The cultural cognitive pillar relates to taken-for-granted behavior or mental models routinely conducted in the organization (shared meaning and ways of thinking).

In the administrative reform field, a growing literature has examined factors that influence the reform process. Caiden (1969) classifies administrative reform into two broad categories: reforms concerning individuals and groups and reforms concerning institutions. These two categories provide different approaches to reform. In reform concerning individuals and groups, administrative reform may involve ideological, moral, and educational approaches. On the other hand, in reform concerning institutional, administrative reform may involve reform in decision-making, structural arrangement, procedure, communication, and adaptability. Caiden (1969) mentions several obstacles to administrative reform, such as geography, history, technology, culture, economy, society, and polity, which confirm institutional aspects such as culture and history in reform. Furthermore, there is a possibility of management issues in implementing reform. In defining administrative reform as a program, management scholars have already classified four management functions in maintaining program quality: planning, organizing, leading, and controlling (Jones & George, 2007).

This study explores the dynamics of the institution by focusing the analysis on internal and external factors that will shape the institution where the reform takes place (neo-institutionalism). North (1990) defines an institution as a rule of the game. The institution must consider political, economic, and political processes (Acemoglu & Robinson, 2008). These three components provide an understanding that the internal aspect of the public sector in a reform needs to consider the political process, which is often influenced by how regulative, normative, and cultural values are inside and outside the organization. Therefore, this research analyzes the regulative, normative, cultural, and management that imply internal and external factors of the organization to understand the dynamic of reform in Indonesia.

Materials and Methods

Research Context

Indonesia is a country consisting of a central government and local governments. In line with decentralization, there is a division of authority between the central and local governments. At a central government level, the Minister leads the ministry and assists with the duties of the President. The local government is comprised of autonomous regions responsible for carrying out decentralization and deconcentration. In implementing bureaucratic reform, the MoAB plays a significant role in encouraging and monitoring the development of administrative reform in central government and local governments. This research aims to analyze the results of administrative reform by analyzing The MoAB’s report on the government accountability system and conducting interviews with public servants at the central and local government levels. The methodology of this research aims to get a general overview of all government institutions' progress in administrative reform through MoAB’s report and explore the factors that influence administrative reform implementation through interviews.

Research Design

Using a mixed method, this research employed the pragmatic paradigm to analyze government performance management and its relation to bureaucratic reform in developing countries. Creswell and Creswell (2018) state that pragmatic philosophy focuses on real-world practice. This study also employed the case study method to examine the case of Indonesia, investigating the real world using both qualitative and quantitative data.

Data Collection

The study is based on different data sets: secondary data analysis (quantitative data) and interviews (qualitative data). Firstly, the researchers analyze quantitative data of SAKIP and illustrate the descriptive statistics in the graph. The researcher obtained quantitative data from The MoAB evaluation of government performance (SAKIP) between 2016 and 2019. The SAKIP data illustrate the data of local government performance accountability system from provinces (2016–2019), 464 regencies/cities (2016), 483 regencies/cities (2017), 498 regencies/cities (2018), and 506 regencies/cities (2019).

The MoAB has developed SAKIP as a performance measurement that evaluates five components: performance planning, performance measurement, performance reporting, internal evaluation, and performance output. The ministry annually appraises provincial and local governments based on these components:

Performance Planning (30%)

Performance Measurement (25%)

Performance Reporting (15%)

Internal Evaluation (10%)

Performance Achievements (20%)

Secondly, the researchers conducted interviews to follow up the results with seven central government officers, eight provincial government officers, and three regency/city officers. The central government informants are experts from Independent Team on National Bureaucratic Reform (Tim Independen Reformasi Birokrasi Nasional/TIRBN), Commissioner from the Civil Service Commission (KASN), practitioners from the Ministry of Finance (MoF) and the MoAB, officers from Yogyakarta Province, officer from West Java Province, officers from South Sulawesi Province, officer from Bandung City, and officers from Banyuwangi Regency.

Individual interviews were conducted in 2017 and 2021, and were provided informed consent based on the agreement that personal information would remain confidential. The interview in 2017 was part of a research project funded by MoAB. The interview in 2021 was an individual research project funded by the University of Indonesia. The researcher used pseudonyms to quote actual conversations during the interview. The authors obtained a review including ethical consideration of the research before obtaining funding support from the Faculty of Administrative Science, University of Indonesia.

Interpretation and Data Analyzes

The researcher categorized, analyzed, and visualized data using Microsoft Excel to provide a map of the median and annual trends of the score. Meanwhile, the qualitative data were analyzed using NVivo software to establish thematic coding from informants. Following the qualitative analysis proposed by Creswell and Creswell (2018), this study interprets the thematic code and analyses the findings. The authors categorize findings into five factors that influence SAKIP implementation and provide selected quotes from informants to support the analysis.

Discussion

Performance of Government Accountability System 2015 to 2019

Along with implementing bureaucratic reforms in Indonesia, SAKIP has become an instrument used to analyze the performance accountability system of government institutions. Until now, the provincial and municipal governments have been active in learning and establishing the performance accountability system reflected in the planning and budgeting system to the reporting in each institution. The MoAB has been assisting local governments through workshops, training, coaching clinics, and direct visits to local governments to create an accountability system through the preparation of SAKIP in accordance with the strategic plan for each local government. There are over 30 individuals who assist the process for 504 regencies’ and cities’ governments and 34 provinces, plus over 32 Ministries and 50 institutions at the central government level. The MoAB also conducts workshops in several regions for dozens of local governments to train trainers at the province level to help the regencies and cities in every province.

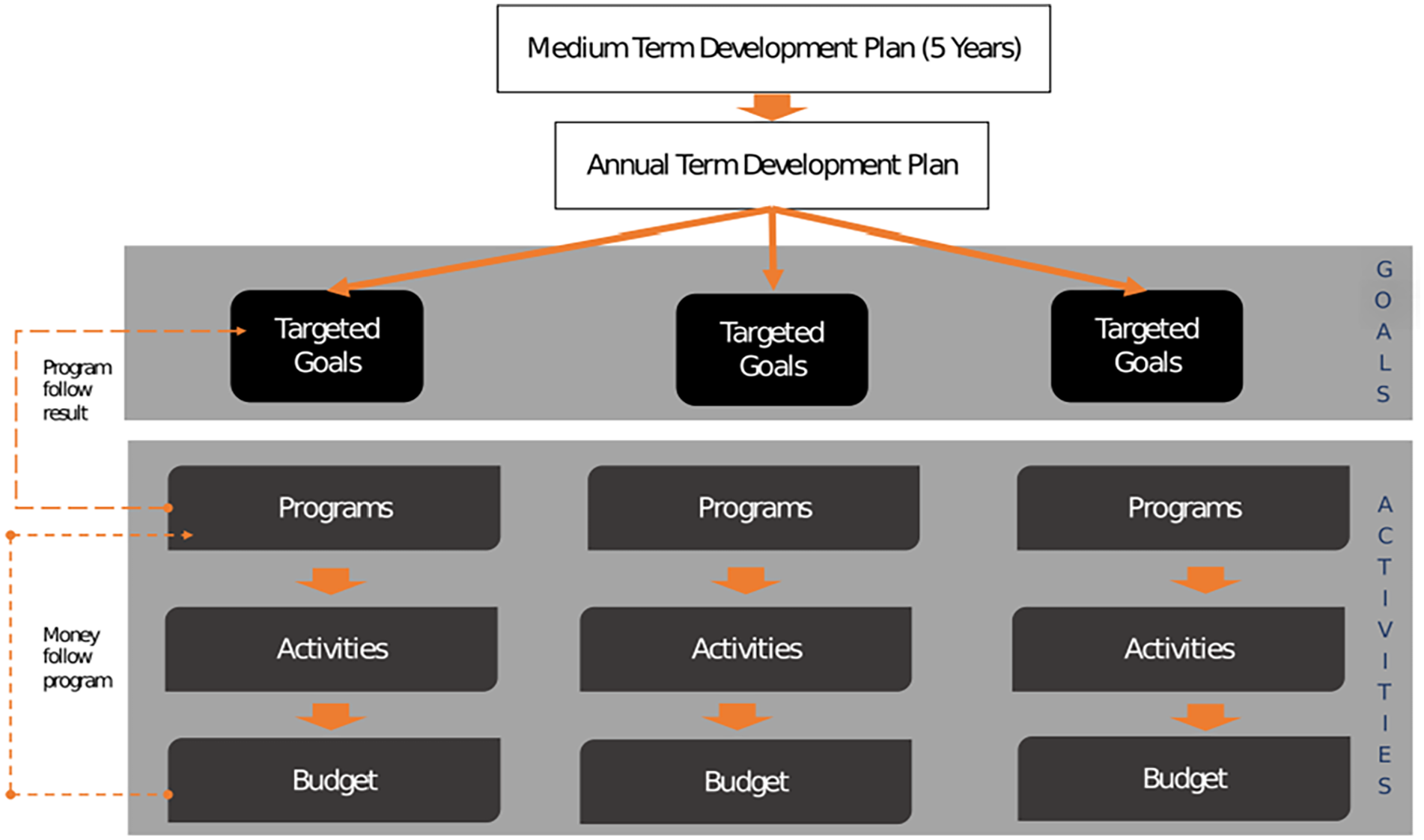

The implementation of e-budgeting or e-performance-based budgeting allows for the completion of the budget in accordance with program activities carried out (money follow program). The principle of the money follow program is to prevent stealth programs and/or activities and irregularities. In addition to adjusting between the budget and the program of activities, e-performance-based budgeting provides an opportunity to adjust between program activities and national priorities (follow result programs). This principle can increase effectiveness and reduce budget waste. E-performance-based budgeting is a form of integration of financial planning and performance that connects budgeting through e-budgeting and performance accountability through SAKIP. The government implements the SAKIP cascading process to enhance allocative efficiency (value for money; Figure 1). That means the government is accountable for every rupiah that they spend. This process is important for Indonesia to correct its main performance indicators, such as funds absorption.

SAKIP and cascading process.

Annually, the MoAB evaluates SAKIP performance implementation across all government institutions, including all local governments at both levels. The evaluation results are categorized into eight groups: E; D; C; CC; B; BB; A; and AA. Based on SAKIP evaluation indicators, the MoAB categorizes the score of each public institution with “E” as the lowest and AA as the highest.

A poor score indicates that an institution needs a planning document and has a low-quality budget document. On the other hand, the highest score indicates that institutions have the capacity or conditions to build SAKIP and demonstrates the usefulness of SAKIP for other system reforms.

For example, the Province of Yogyakarta, the only provincial government to receive the “AA” score, has used SAKIP to cut irrelevant programs and activities to its visions and missions and liquidated organizations that do not contribute to its visions and missions. Local governments that had achieved “BB,”“A,” and “AA” were ones that not only implemented SAKIP effectively but also did it within the spirit of reform (Informant 1, Deputy Minister of MoAB, 2018). The spirit of reform involves not only the implementation of SAKIP; some regulations go beyond the implementation. This characteristic significantly differs from the other groups (“D,”“C,”“CC,” and “B”). These situations are far from the ideals of reform of the local government’s performance accountability system in Indonesia.

The MoAB conducts an annual evaluation of SAKIP that divides the assessment into three regions and provides awards for high-performance institutions developing and implementing SAKIP. This effort was significant in motivating local governments to improve their SAKIP. SAKIP score for a provincial level between 2015 and 2019, as illustrated in Table 1, shows that most provinces received “CC” grades in 2015 but rose to grade “B” from 2016 to 2019. This finding shows an improvement in the value of SAKIP in most provinces. Only one province was left in the “CC” category in 2019, and Yogyakarta Province has steadily received the highest score from 2018 to 2019.

Distribution of SAKIP Scores for Provinces in Indonesia (2015–2019; in %).

Different conditions were seen in developing SAKIP values at the regency and city levels. Table 2 shows that the improvement in SAKIP value in regencies and cities has been slower than at the provincial level. Most regencies and cities achieved category “B” from 2018 to 2019, and the percentage of regencies and cities that earned “A” and “BB” scores was no more than 12% in 2019. Since the SAKIP assessment was conducted, no regencies and cities, such as the provincial level, had received the highest scores (“AA”). In 2019, regencies and cities that had obtained a “CC” category were still the regencies with the second-highest percentage. This condition shows that the provincial level’s transformation efforts through SAKIP from 2015 to 2019 were more effective than the regencies and cities.

Distribution of SAKIP Scores for Regencies and Cities in Indonesia (2015–2019; in %).

Both provincial, regency, and city levels show that, after 20 years of radical decentralization and 10 years of systematic SAKIP reform, the changes were only a process of formalism with no significant deepening. Figure 2 presents the percentage of central, provincial, regency, and city governments that reach at least the “BB” category. Figure 2 implies substantial progress from 2018 to 2019 at the central government level, increasing total institutions with at least “BB” from 43.4% to 78.4%. There is a different trend among provinces, regencies, and cities, which have experienced a slow improvement in the performance accountability system. There was no improvement at the province level from 2018 to 2019. The interview found that two provinces saw their score drop from “A” to “BB” in 2020 because of a lack of commitment from the elites of those two provinces (Informant 2, Officer of MoAB, 2021). Based on these findings, it may be argued that the local government reform on SAKIP is still in the “big stuck” terminology used by Pritchett et al. (2010). Pritchett et al. (2010) define big stuck” as low state capability or persistent stagnation of administrative capability.

Trends in trends in SAKIP value (performance accountability system) with a good category at least “BB.”

Figure 3 shows that there has been an impressive significant improvement at all levels of government if the” B” group institutions or local government are included. The percentages achieved by the three levels of government exceeded the target for the year 2019. However, the “B” value only shows the willingness to change and make reform happen; the “soul” of reform is not yet there (Informant 1, Deputy Minister of MoAB, 2018). The improvements made so far for documents were only apparent at the behavior level. The “BB” score value and above show that the SAKIP reform is in progress. It has been found that the “soul” of reform is already in place; the significant results are real and can be measured. Figure 3 implies that, although scores were significantly improved, they were not followed by the system’s functioning. This situation may be described as “isomorphic mimicry” (Dimaggio & Powell, 1983), though further research is required for this terminology.

Trends in SAKIP value (performance accountability system) with very good category at least “B.”

The local government is still facing a challenging situation in building rationale and relationship between the 5-year planning (Renstra) as strategic planning to the yearly planning and budgeting (Rencana Kerja Pemerintah). Informant 4 (Practitioner in Provincial Government and Academic) stated that the challenge emerges mainly because of the very poor quality of the Renstra themselves.

The research suggests that the local government needed to be committed to its strategic planning documents. Other facts show how poorly Renstra has been developed, even nationally. These issues are serious problems that local governments have experienced in implementing the SAKIP. If it is assumed that the quality of the Renstra problem still occurs in the local governments that scored CC or below, it is likely to have occurred in over 50% of local governments in 2018.

Another serious problem in SAKIP implementation is numerous cases of miss-cascade from the program in the Renstra document to the program and activities in annual planning and budgeting. One of the criticisms regarding the analysis of allocative efficiency, among others, is the need to improve the interrelationship between programs and activities with goals or objectives. In addition, the activity details do not correspond with the intended purposes. This indicates that the activities and objectives have no alignment.

These situations were exacerbated when the budget behavior both from the MoF and the inspectorate at the local levels used “percentage of spending absorption” as a key indicator in evaluating the performance of government institutions. Government institutions that can execute this expenditure in a high percentage of their budget are considered to have excellent performance. The general budget behavior is spending all available money, especially at the fiscal year’s end.

Other problems often found involved using indicators and their targets for development programs and activities in both national and local governments. In various cases, these indicators still needed to be fully result-oriented. The performance measures of each goal and the goals themselves often needed a clearer performance measure. The central government’s performance in planning, budgeting, and performance management needs to be improved. The absence of alignment between 5-year planning and the Ministry and Institution Plan, and the Prepared Performance Report is also part of the weakness. Also, ministries and institutions need to be stronger in determining the measure of success (Key Performance Indicators), and the budget needs to focus on achieving strategic goals that will be realized.

Local governments in Indonesia have adopted a new and modern budget system, namely performance-based budgeting, a budget system that can push the allocation of funds to the highest program priorities (Shafritz et al., 2017, pp. 525–526) since 2000. Three years later, the central government adopted the same budget system through Law No. 17/2003 on Public Finances. This law was considered to bring significant improvements to the process and system of budgeting in Indonesia. The improvements were then expected to bring further improvements in implementing public resource allocation. However, the behavior in planning and budgeting remained the same.

Though the process of SAKIP reform is slow, in monetary terms, its implementation in 2018 offered efficiency to the local government budget. At the provincial level, in 25 of 34 provinces, the government estimated that there were 35 trillion rupiahs saved. At the regency and city level, from 217 regencies and cities, the efficiency was estimated to have saved approximately 30.1 trillion rupiahs. In total, the efficiency at local government levels in 2018 is approximately 65.1 trillion rupiah (4.6 billion USD; Informant 1, Deputy Minister of MoAB, 2018). These figures are a significant amount of money for development funds in Indonesia and were achieved because of improvements in various aspects of SAKIP, such as programs, activities, performance indicators, and targets of the development program, as well as more effective cascading from planning to budgeting documents, ensuring that both the planning and budgeting documents reflect the needs of society (Ministry of State Apparatus Utilization and Bureaucratic Reform, 2019). Various programs and activities for development have been re-focused to be more relevant to the vision and missions of development.

Factors Influencing the Government Performance Accountability System

This study investigates the factors that influence the implementation of SAKIP in Indonesia based on institutional theory perspectives that consist of three pillars, namely regulatory, normative, and cognitive, as well as the management factor.

Regulatory Issues

The law of Public Finance is one of the foundations for the change to accountable governance that not only accommodates financial decentralization from the central to the regional government but also increases accountability throughout the process and implementation of performance-based budgeting (Law No 28/1999, Law No 17/2003, Law No 1/2004, Government Regulation No. 8/2006). Regulation on SAKIP (Presidential Regulation No. 29/2014) affirms all the above regulations that can increase accountability and effectiveness of using results-oriented budgets.

Regulations to date have changed governance since the implementation of SAKIP. Presidential Regulation No. 29/2014 has encouraged the central and local governments to develop SAKIP by integrating from planning to output activities. The Indonesian government is not establishing a coercive system to encourage accountable governance, instead providing incentives and monitoring. The MoAB has been evaluating SAKIP fulfillment since 2015; this evaluation encourages local and central governments to look for appropriate implementation models. The MoAB publishes the results of evaluations on the implementation of SAKIP every year and grants awards for each annual evaluation.

In addition, the evaluation of SAKIP is connected to the financial incentive system. Currently, the acquisition of a high SAKIP value will be one of the consideration indicators for public institutions to receive regional incentive funds. The Central Government, through the MoF, provides “Incentives for Regional Incentive Funds” for regions that meet financial performance indicators. One of the indicators is to obtain a minimum SAKIP value of BB. In 2018, 14 local governments received regional incentive funds with high SAKIP values, namely eight provinces (West Sumatra, South Sumatra, West Java, Central Java, East Java, DIY, South Kalimantan, and Bali) and six regencies (Bantul, Kulon Progo, Sleman, Banyuwangi, Badung, and Karimun) (Ministry of State Apparatus Utilization and Bureaucratic Reform, 2018). In 2021, the allocation of regional incentive funds (Dana Insentif Daerah) for the SAKIP category reached Rp 633.87 billion, or 4.7% of the total budget received by 4 provinces, 52 regencies, and 12 cities (Ministry of Finance, 2021).

According to the term “carrot and stick,” existing regulation only provides carrots because there is no disincentive for government agencies that have not met the SAKIP value of good categories. The results of the interviews with KASN support the disincentive pattern for public institutions whose SAKIP performance is still not efficient because the change of public officials’ culture still dominated by Weberian culture requires sticks: “We have to need a stick because our bureaucracy is still a Weberian bureaucracy” (Informant 3, Commissioner of State Apparatus Commission, 2021).

Although there have been no pressing sanctions at the central government level, a number of local governments have implemented practices to impose social sanctions and incentives, as done in the Province of Yogyakarta through the summoning of the highest and lower performing agencies over each performance implementation evaluation period (Informant 6, Provincial Development Planning Agency Officer, 2017). Existing research has also found that, although Indonesia formally has begun to use performance-based budgeting since 2003 through the Indonesia Public Finance Law, the practices of many local governments are still strongly influenced by incremental budgeting. The budget behavior and the rules do not match or are often called formalism (Pritchett et al., 2010).

In the pillars of this regulation, there are a number of things that characterize the development of the current conditions, such as the synchronization between the regulations proposed by the Ministry of Finance, Ministry of Home Affairs, and Ministry of Development and Planning in terms of performance measurements by considering the simplification of the report preparation process and increasing the impact on performance. Furthermore, although there has been an evaluation of the value of SAKIP, there is no easily accessible publication of SAKIP value from year to year.

Normative Issues

In SAKIP, appropriateness is performance-based in terms of output indicators and outcomes that have been set. Current conditions indicate that the most influential factor inhibiting the internalization of the value of appropriateness is budget behavior, which assesses that budget spending is the standard of appropriateness. SAKIP has determined performance indicators as a standard of appropriateness. However, it still needs to be determined to establish the basis because it is still perceived that budget spending is a performance indicator. Current budget behavior is still not in accordance with the norms in SAKIP. For this reason, it is very important that regulations compiled by the government are followed by habits in performance-based financial governance.

Furthermore, the lack of understanding of strategic planning of performance management will mean that local governments do not develop indicators for inputs, outputs, and outcomes in the strategic planning of the organization and budget documents. If there is available output, it has not been able to measure performance management. Until 2005, almost all local governments only had input indicators. It is difficult to find local governments that have output and outcome indicators within their Renstra and budget documents (Salomo, 2006). The World Bank’s research shows that local governments have no knowledge of what the standard for the appropriateness of strategic planning is. In one of the focus group discussions on the reform roadmap, there are still many officials who do not understand the definition of reform (The World Bank, 2020).

Cultural Cognitive Issues

The cultural cognitive pillar relates to taken-for-granted behavior or mental models routinely used in the organization (shared meaning and ways of thinking). This research considers the cultural standards Hofstede Insights (2021) developed to analyze the cultures that influence SAKIP implementation. Hofstede Insights (2021) finds that Indonesia has unequal power distribution, a collectivist society, and long-term orientation goals. The unequal distribution of power and feudalism still affects bureaucracy in Indonesia. In some areas in Indonesia, it is still common to call public officials with high positions with noble titles that associate those high officials with a stronger position. The system of value traditions and symbols that still appear in bureaucracy can be seen from the title of nobility for public officials such as Karaeng in Makassar and Peta or Puang in Bugis. Feudal culture in bureaucracy produces ambivalence that, on the one hand, bureaucracy is expected to realize the merit system of serving society. On the other hand, there is still a culture that considers that the position in the bureaucracy places public officials as nobles who must be served. Interestingly, Yogyakarta Province is led by a sultan and associated with feudal culture capable of obtaining the highest SAKIP value.

SAKIP implementation strongly encourages a performance-based culture and coordination across sectors. However, the culture of coordination and cooperation has not yet become a culture across society. Collaboration among regency agencies is still challenging, and silo mentalities hinder coordination between actors. For SAKIP, this cooperation and collaboration must be strong. The local government still considers SAKIP a program of the MoAB entrusted to the region, meaning that the sense of ownership over the program is low. Ownership of low programs affects actors’ behavior. Therefore, the new implementation is at the level of regulatory fulfillment and has not been culturally and normatively embedded. Previous studies have also found that the organization’s partial commitment significantly affects the implementation of performance accountability (Tahir et al., 2016).

Organizational Issues

Management functions also influence the implementation of SAKIP in local government. Jones and George (2007) state that management has four main responsibilities: planning; organizing; leadership; and supervision. Of the four functions, the planning function that informants often refer to still needs to be more powerful in supporting bureaucratic reform, particularly in SAKIP implementation. Informant 4 (Practitioner in Provincial Government and Academic, 2021) mentioned that “SAKIP was 55 percent. It was a planning aspect that there are two, namely performance plans and performance measures.” This response reflects that planning is decisive in SAKIP. Informant recognizes obstacles; among others, local governments do not prioritize planning and political promises of elected regional leaders that cannot be transformed into a measurable, doable planning document. During campaigns, political promises from regional leaders are a component of regional planning in Indonesia because regional planning consists of essential service planning, regional head priority programs, and synergy programs sourced from the Ministry.

Informant 5 (Executive at the TIRBN and academic, 2021) found that the SAKIP system had been sufficiently built. However, the capacity of local governments and institutions requiring further development was included in compiling performance indicators in the planning process. Informant 5 (Executive at the TIRBN and academician, 2021) stated, “. . . now I see that the problem of SAKIP is in its capacity in the ministry or institution to start from planning performance. Planning performance is complicated, starting from planning strategic goals, strategic target indicators, targets, programs, to activities.” The inability of the MoAB employees to implement capacity building also occurs as one of the challenges in aiding each region. Therefore, one solution is offered to the MoAB to provide local government with institutions related to reform and SAKIP through online media (Informant 3, Commissioner of State Apparatus Commission, 2021).

Conclusion

This study concludes that, firstly, based on SAKIP data (2016–2019) in Indonesia, the bureaucratic reform in Indonesia, particularly in the regency and cities, shows slower development than the central government and provincial government. Secondly, this study confirms that institutional theory is relevant to investigating affecting factors behind the lack of progress in the administrative reform, such as cultural cognitive, regulative, and normative. In addition, management issue also plays a vital role in influencing the speed of administrative reform in Indonesia. Leadership is a key factor that affects the implementation of governance reforms such as SAKIP. These strong leaders can cooperate with the central government ministry, particularly the Ministry of Administrative Reform.

Further research that may be conducted to analyze SAKIP should be implemented at national and provincial levels, focusing on how the institutions implement bureaucratic reform faster. In addition, the analysis of local government institutions’ challenges in implementing SAKIP could answer the slow progress of bureaucratic reform in Indonesia. Also, the case study of the government accountability system at the local level, specifically Yogyakarta, is significant in contributing empirical findings of local government experience in pursuing faster bureaucratic reform.

Footnotes

Acknowledgements

The researchers thank the Ministry of PAN and RB for funding research through UI CSGAR in 2017 and allowing researchers to use several archives of data and experience from that research for this study. The study in 2017 involved several researchers, including Nidaan Khafian, Marcel Angwyn, and Rudiarto Sumarwono. Researchers also thank for the cooperation and opportunities provided by the local government at the study site, who have received and provided information in 2017 and 2021. Researchers appreciate Tiara Farchana Ramadhanty, a research assistant who aided in organizing secondary data for this study.

Author Contributions

The first author was responsible for writing the original draft preparation and review editing for background, conceptualization, and analysis of SAKIP development. Moreover, this project obtained funding from the Faculty of Administrative Science, Universitas Indonesia, under the first author’s name. The second author contributed to developing the methodology and writing drafts of the factors affecting the implementation of SAKIP. Both authors conducted the investigation and participated in data collection.

Declaration of Conflicting Interests

The author(s) declared no potential conflicts of interest with respect to the research, authorship, and/or publication of this article.

Funding

The author(s) disclosed receipt of the following financial support for the research, authorship, and/or publication of this article: This research was funded by the Faculty of Administrative Science, Universitas Indonesia in the form of a functional position grant, and “The APC was funded by the Faculty of Administrative Science Universitas Indonesia.”